exit

Auto Added by WPeMatico

Auto Added by WPeMatico

Rumors have been flying this week that SAP was going to buy Berlin business process automation startup Signavio, and sure enough the company made it official today. The companies did not reveal the purchase price, but Bloomberg reported earlier this week that the deal could be worth $1.2 billion.

With Signavio SAP gets a cloud-native business process management tool. SAP CFO Luka Mucic sees a world where understanding and automating businesses processes has become a key part of a company’s digital transformation efforts.

“I cannot overstress the importance for companies to be able to design, benchmark, improve and transform business processes across the enterprise to support new capabilities and business models,” he said in a statement.

While traditional enterprise BPA tools have existed for years, having a cloud-native tool gives SAP a much more modern approach to attacking this problem, and being able to automate business processes via the cloud has become more important during the pandemic when many employees are working entirely from home.

SAP also sees Signavio as a key missing piece in the company’s business process intelligence unit. “The combination of business process intelligence from SAP and Signavio creates a leading end-to-end business process transformation suite to help our customers achieve the requirements needed to gain a competitive edge,” he said.

SAP has been making moves into process automation of late. In fact at SAP TechEd in December, the company announced SAP Intelligent Robotic Process Automation, its foray into the RPA space. This should fit in nicely alongside it.

Dr. Gero Decker, Savigno co-founder and CEO, sees SAP resources helping push the company beyond what it could have done on its own. “Considering the positioning of SAP, its geographical coverage and financial muscle, SAP is the biggest and best platform to bring process intelligence to every organization,” he said in a statement.

The increased resources and reach argument is one that just about every acquired company CEO makes, but being pulled into a company the size of SAP can be a double-edged sword. Yes, it has vast resources, but it also can be hard for an acquired company to find its place in such a large pond. How well they fit in and make that transition from startup to big company cog, will go a long way in determining the success of this transaction in the long run.

Signavio launched in 2009 in Berlin and has raised almost $230 million, according to Crunchbase data. Investors include Apax Digital and Summit Partners. The most recent investment was a July 2019 Series C for $177 million, which came in at a $400 million valuation.

Customers include Comcast, Bosch, Liberty Mutual and yes SAP. Perhaps it will be getting a discount now.

Powered by WPeMatico

Bloomreach, an API company that helps eCommerce customers with search and web site creation, announced a $150 million investment today from Sixth Street Growth. Today’s funding values the company at $900 million.

At the same time, the company announced it has acquired Exponea, a startup that gives Bloomreach a marketing automation component it had been missing. The two companies did not reveal the acquisition price, but along with the pure functionality, the company gains 200 additional employees, which is significant, considering Bloomreach had 300 prior to the acquisition. It also gains 250 net new customers, giving it a total of 750.

“Historically, we have had two major pillars of the business — the search part of it and the content part,” Bloomreach CEO and co-Founder Raj De Datta told TechCrunch. The content management component lets customers build websites, while the search powers the search box, navigation and merchandising. He points out that all of it is powered by an underlying data analysis engine that matches data to people and people to products.

Exponea will give the company more of a complete platform of services, allowing marketers to target and personalize their marketing messages across multiple channels. De Datta says the two companies had similar missions and made a good fit. “We have a common vision and common sort of product direction. […] Both companies are data-driven optimization technologies[…] and both are entrepreneurial product-driven companies,” he said.

It also helped that they had been partnering together for six months prior to the sale, which has now closed. Exponea was founded in 2016 in Slovakia and has raised over $57 million, according to Pitchbook data. The plan is to leave Exponea as a stand-alone product, while finding ways to integrate it more smoothly with the other components in the Bloomreach platform. They expect the integration parts to happen over the next year.

While De Datta did not want to share specific revenue figures, he did say that the company had a record second half as business was pushed online due to the pandemic. Michael McGinn, partner at Sixth Street and co-head at investor Sixth Street Growth doesn’t see the demand for eCommerce abating, even post-COVID, and that will drive a need for more customized online shopping experiences.

“Technology serving more bespoke customer experiences is a rapidly expanding market and we are pleased to join Bloomreach in its leadership of the digital commerce experience and marketing sector,” McGinn said in a statement.

De Datta says the money was used in part to buy Exponea, but he also plans to invest more in engineering to continue building the product line. The ultimate goal is an IPO, but as you would expect, he wasn’t ready to commit to any timeline just yet.

“I wouldn’t say we have a timeline, but our goal is that the company over the course of 2021 should make investments towards that, so that it’s an option for us.”

Powered by WPeMatico

This week, Latch becomes the latest company to join the SPAC parade. Founded in 2014, the New York-based company came out of stealth two years later, launching a smart lock system. Though, like many companies primarily known for hardware solutions, Latch says it’s more, offering a connected security software platform for owners of apartment buildings.

The company is set to go public courtesy of a merger with blank check company TS Innovation Acquisitions Corp. As far as partners go, Tishman Speyer Properties makes strategic sense here. The New York-based commercial real estate firm is a logical partner for a company whose technology is currently deployed exclusively in residential apartment buildings.

“With a standard IPO, you have all of the banks take you out to all of the big investors,” Latch founder and CEO Luke Schoenfelder tells TechCrunch. “We felt like there was an opportunity here to have an extra level of strategic partnership and an extra level of product expansion that came as part of the process. Our ability to go into Europe and commercial offices is now accelerated meaningfully because of this partnership.

The number of SPAC deals has increased substantially over the past several months, including recent examples like Taboola. According to Crunchbase, Latch has raised $152 million, to date. And the company has seen solid growth over the past year — not something every hardware or hardware adjacent company can say about the pandemic.

As my colleague Alex noted on Extra Crunch today, “Doing some quick match, Latch grew booked revenues 50.5% from 2019 to 2020. Its booked software revenues grew 37.1%, while its booked hardware top line expanded over 70% during the same period.”

“We’ve been a customer and investor in Latch for years,” Tishman Speyer President and CEO Rob Speyer tells TechCrunch. “Our customers — the people who live in our buildings — love the Latch product. So we’ve rolled it out across our residential portfolio […] I hope we can act as both a thought partner and product incubator for them.”

While the company plans to expand to commercial offices, apartment buildings have been a nice vertical thus far — meaning the company doesn’t have to compete as directly in the crowded smart home lock category. Among other things, it’s probably a net positive if you’re going head to head against, say Amazon. That the company has built in partners in real estate firms like Tishman Speyer is also a net positive.

Schoenfelder says the company is looking toward such partnerships as test beds for its technology. “Our products have been in the field for many years in multifamily. The usage patterns are going to be slightly different in commercial offices. We think we know how they’re going to be different, but being able to get them up and running and observe the interaction with products in the wild is going to be really important.”

The deal values Latch at $1.56 billion and is expected to close in Q2.

Powered by WPeMatico

Taboola is the latest company seeking to go public via special purpose acquisition company — more commonly known as a SPAC.

To achieve this, it will merge with ION Acquisition Corp., which went public in 2020 with the aim of funding an Israeli tech acquisition (Haaretz reported last month that Taboola was in talks with ION). The transaction is expected to close in the second quarter, and the combined company will trade on the New York Stock Exchange under the ticker symbol TBLA.

Founded in 2007, Taboola powers content recommendation widgets (and advertising on those widgets) across 9,000 websites for publishers including CNBC, NBC News, Business Insider, The Independent and El Mundo. It says it reaches 516 million daily active users while working with more than 13,000 advertisers.

The company had previously planned to merge with competitor Outbrain before the deal was canceled last fall, with sources pointing to the market impact of the COVID-19 pandemic, a “challenging culture fit” and regulatory issues to explain the deal’s end.

Taboola’s founder and CEO Adam Singolda (pictured above, left) told me that this didn’t lead directly to the SPAC deal. But he said, “I always wanted to go public,” which wasn’t possible while the merger was in the works. Once that deal was called off, and with 2020 turning out to be a strong year for Taboola — it’s projecting revenue of $1.2 billion, including $375 million ex-TAC revenue (revenue after paying publishers), with over $100 million in adjusted EBITDA — the time seemed right, and ION seemed like the right partner.

“We believe Taboola is an open web recommendation leader which is well positioned to challenge the walled gardens,” said ION CEO Gilad Shany in a statement. “We were looking to merge with a global technology leader with Israeli DNA and we found that in Taboola. The combination of long-term partnerships built by the company with thousands of open web digital properties, their direct access to advertisers, massive global reach and proven AI technology, allows Taboola to provide significant value to their partners while also achieving attractive unit economics as the company grows.”

The deal will value Taboola at $2.6 billion. Through this transaction, the company plans to raise a total of $545 million, including $285 million in PIPE financing secured from Fidelity Management & Research Company, Baron Capital Group, funds and accounts managed by Hedosophia, the Federated Hermes Kaufmann Funds and others.

Singolda said that the company plans to invest $100 million in R&D this year, and that he hopes to expand the technology into areas like e-commerce and TV advertising, with the goal of moving “beyond the browser.” More broadly, he said he wants Taboola to be “a strong public company that champions the open web.”

“The open web is a $64 billion advertising market [according to Taboola estimates], but there’s no Google for the open web,” he said.

Yes, Google itself spends plenty of time talking about similar ideas, but Singolda argued that while Google has consumer products like search and YouTube that compete with other publishers for time and attention, “Taboola is not in the consumer business … We serve our partners, and it’s in our identity to drive audience growth, engagement and revenue.”

Powered by WPeMatico

At Battery, a central part of our consumer investing practice involves tracking the evolution of where and how consumers find and purchase goods and services. From our annual Battery Marketplace Index, we’ve seen seismic shifts in how consumer purchasing behavior has changed over the years, starting with the move to the web and, more recently, to mobile and on-demand via smartphones.

The evolution looks like this in a nutshell: In the early days, listing sites like Craigslist, Angie’s List* and Yelp effectively put the Yellow Pages online — you could find a new restaurant or plumber on the web, but the process of contacting them was largely still offline. As consumers grew more comfortable with the web, marketplaces like eBay, Etsy, Expedia and Wayfair* emerged, enabling historically offline transactions to occur online.

More recently, and spurred in large part by mobile, on-demand use cases, managed marketplaces like Uber, DoorDash, Instacart and StockX* have taken online consumer purchasing a step further. They play a greater role in the operations of the marketplace, from automatically matching demand with supply, to verifying the supply side for quality, to dynamic pricing.

The key purpose of being end-to-end is to deliver an even better value proposition to consumers relative to incumbent alternatives.

Each stage of this evolution unlocked billions of dollars in value, and many of the names listed above remain the largest consumer internet companies today.

At their core, these companies are facilitators, matching consumer demand with existing supply of a product or service. While there is no doubt these companies play a hugely valuable role in our lives, we increasingly believe that simply facilitating a transaction or service isn’t enough. Particularly in industries where supply is scarce, or in old-guard industries where innovation in the underlying product or service is slow, a digitized marketplace — even when managed — can produce underwhelming experiences for consumers.

In these instances, starting from the ground up is what is really required to deliver an optimal consumer experience. Back in 2014, Chris Dixon wrote a bit about this phenomenon in his post on “Full stack startups.” Fast forward several years, and more startups than ever are “full stack” or as we call it, “end-to-end operators.”

These businesses are fundamentally reimagining their product experience by owning the entire value chain, from end to end, thereby creating a step-functionally better experience for consumers. Owning more in the stack of operations gives these companies better control over quality, customer service, delivery, pricing and more — which gives consumers a better, faster and cheaper experience.

It’s worth noting that these end-to-end models typically require more capital to reach scale, as greater upfront investment is necessary to get them off the ground than other, more narrowly focused marketplaces. But in our experience, the additional capital required is often outweighed by the value captured from owning the entire experience.

Many of these businesses have reached meaningful scale across industries:

Image Credits: Battery Ventures (opens in a new window)

All of these companies have recognized they can deliver more value to consumers by “owning” every aspect of the underlying product or service — from the bike to the workout content in Peloton’s case, or the bank account to the credit card in Chime’s case. They have reinvented and reimagined the entire consumer experience, from end to end.

As investors, we’ve had the privilege of meeting with many of these next-generation end-to-end operators over the years and found that those with the greatest success tend to exhibit the five key elements below:

The end-to-end approach makes the most sense when disrupting very large markets. In the graphic above, notice that most of these companies play in the largest, but notoriously archaic industries like banking, insurance, real estate, healthcare, etc. Incumbents in these industries are very large and entrenched, but they are legacy players, making them slow to adopt new technology. For the most part, they have failed to meet the needs of our digital-native, mobile-savvy generation and their experiences lag behind consumer expectations of today (evidenced by low, or sometimes even negative, NPS scores). Rebuilding the experience from the ground up is sometimes the only way to satisfy today’s consumers in these massive markets.

Powered by WPeMatico

Hims & Hers, a San Francisco-based telehealth startup that sells sexual wellness and other health products and services to millennials, began trading publicly today on the NYSE after completing a reverse merger with the blank-check company Oaktree Acquisition Corp.

Its shares slipped a bit, ending the day down 5% from where they started, but the company, which was founded in 2017 and now claims nearly 300,000 paying subscribers for its various offerings, has never been focused on a splashy headline about its first-day performance, co-founder and CEO Andrew Dudum told us earlier today.

On the contrary, Dudum says that while Hims might have once imagined a traditional IPO, it decided to go the special purpose acquisition company (SPAC) route because of their pricing mechanisms and because it was approached by a SPAC led by renowned money manager Howard Marks, the founder of the global alternative investment firm Oaktree Capital Management. (“We fell in love with the Oaktree team and the capital market experience and deep resources they have.”)

We talked with Dudum about that SPAC’s structure; the lockups involved now that Hims’ shares are trading; and how much of the business still centers around one of its first offerings, which was a generic version of erectile dysfunction pills. Our conversation has been edited lightly for length and clarity.

TC: You’re a Bay Area-based company selling to a mostly U.S. audience. How are you thinking about expanding that footprint geographically?

AD: We do have a small operation selling in the U.K.; we’re getting our feet wet in that market and building out a team and infrastructure and fulfillment. If you look at the regulatory landscape, there’s a huge amount of room [to grow] in Europe, Australia, Canada, the Middle East and Asia, and so in that order, we’ll start to [move into those markets].

TC: What is your average customer cost?

AD: It has come down from $200 when we first launched, to roughly $100 last year, and we make, on average, close to $300 in the first couple of years in terms of a patient’s lifetime value.

TC: How quickly do customers churn?

AD: We break down lifetime value projections by quarter cohorts, and quarter over quarter, year over year, we’re monetizing each of these cohorts better, with high-margin profiles.

As of last quarter, the business was growing 90% year-over-year, with 76% gross margins and greater cash efficiency, and that’s because as we provide more offerings, there is more cross-purchasing. Also, word of mouth is becoming more of a dynamic, with more than 50% of the traffic to the site free at this point because we have built a brand with a young demographic.

TC: When are you projecting that you’ll turn profitable?

AD: We’ve reduced our annual burn and increased our margin efficiency and organic growth, so on a quarterly basis, we think in the next couple of years is a real possibility.

Image Credits: Hims & Hers

TC: Hims’ first wellness offerings included pills for male pattern hair loss and erectile dysfunction. How much revenue does that ED business account for?

AD: What we’ve disclosed is that roughly half [of our revenue] is that sexual health category — which includes [medicines for] generic erectile dysfunction, birth control, STDs, UTIs and premature ejaculation. The other half is predominately dermatology, including hair care [to address hair loss] and acne, and we’ve more recently moved into primary care and behavioral health.

TC: For retail investors, how do you differentiate the business from that of your rival Ro, which heavily promotes its ED products?

AD: There are a number of core differences between us and public and private players. First is our real focus on diversifying our offerings. With our focus on sexual health, dermatology, primary care and behavioral health, it’s in our DNA to quickly expand into new businesses.

We also think we’re different from most [rivals] in that we really invest time in building deep relationships with [those who represent] the future of healthcare markets — people in their teens, 20s and 30s. This demographic has a different set of tech expectations and consumer expectations than people in their 40s, 50s and 60s, and if we want to build for the future, that means building for the largest body of payers in the future.

Traditional healthcare companies monetize only the sick, but optimizing around that demographic precludes you from understanding what the next generation really needs and wants. I’ve never seen such a divergence between a patient population and legacy experience, and that’s a real advantage to us as a business.

TC: Hims just went public through a SPAC in a deal that gives the company around $280 million in cash — $205 million of that from Oaktree’s blank-check company and another $75 million through a private placement deal. How much runway does that give you?

AD: The company doesn’t burn a tremendous amount — between $10 million and $20 million a year — so a relatively long runway if we keep operating the business as is. But it does allow us to expand and grow into new businesses, too, including into big categories like sleep, infertility, diabetes and other chronic conditions.

TC: What about acquisitions?

AD: We’ll keep an eye open for strategic opportunities and consolidation opportunities. More than a dozen businesses a month come to us to be consolidated into the brand, but generally speaking, we’ve had the belief that so much is in front of us that we don’t want to be distracted.

TC: Is there a lockup period for anyone?

AD: There’s a traditional lockup for executives and employees and the board.

TC: Did your SPAC sponsors get a board seat?

AD: No.

TC: How much do they now own of the company, and can they sell?

AD: Oaktree owns a couple percent and [the syndicate they brought to do the private placement] [owns] 12%. But the very reason we went with them was the quality of the team and the organization . . . and they have the added incentive for the next year or two from a compensation standpoint for the company to succeed and to prove [out their thesis that Hims is a smart investment].

TC: Do you think the traditional IPO process is broken?

AD: The traditional IPO market hasn’t changed. It takes 12 to 18 months of preparation, which is a crazy amount of time for management to be distracted, then there’s this one-day PIPE that gives institutions a tremendous amount of money instantaneously. Maybe it makes for a good CNBC headline, but at tremendous cost to the company. It’s atrocious. If you were a founder or employee and getting diluted twice as much as you have to be, you’d be really upset. It’s no surprise to me that founders like myself are looking at other modalities with better pricing and better structures.

Powered by WPeMatico

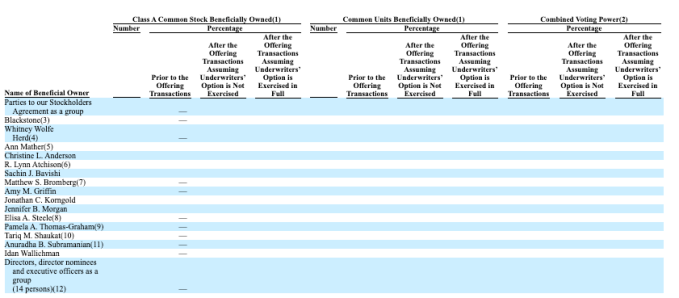

The dating and networking service Bumble has filed to go public.

The company, launched by a former co-founder of the IAC-owned Tinder, plans to list on the Nasdaq stock exchange, using the ticker symbol “BMBL.” Bumble’s planned IPO was first reported in December.

Bumble CEO Whitney Wolfe Herd was on the founding team at Tinder before starting Bumble. She filed suit against Tinder for sexual harassment and discrimination, which was at least somewhat inspirational in her quest to build a dating app that put women in the driver’s seat.

In 2019, Wolfe Herd took the helm of MagicLab, renamed to Bumble Group, in a $3 billion deal with Blackstone, replacing Badoo founder and CEO Andrey Andreev following a harassment scandal at the firm.

The company is targeting the public markets at a particularly heady time for new offerings, with investors embracing venture-backed IPOs throughout late 2020 and the start of 2021. Previously privately held companies like Airbnb, Affirm and others have seen their fortunes soar on the back of prices that public investors are willing to pay, perhaps inducing more IPO filings than the market might have otherwise seen.

You can read its IPO filing here. TechCrunch will have its usual tear-down of the document later today, but we have pulled some top-line numbers for you to kick off your own research.

But before we do, the company’s board makeup, namely that it is over 70% women, is already drawing plaudits. Now, into its numbers.

Let’s consider Bumble from three perspectives: Usage, financial results and ownership.

On the usage front, Bumble is popular, as you would imagine a dating service would have to be to reach the scale required to go public. The company claims 42 million monthly active users (MAUs) as of Q3 2020 — many companies will try to get public on the strength of their third-quarter results from 2020, as it takes time to close Q4 and the full calendar year.

Those 42 million MAUs translated into 2.4 million total paying users through the first nine months of 2020; the percent, then, of paying users to MAUs is not 2.4 million divided by 42, but a smaller fraction.

Turning to the numbers, recall that Bumble sold a majority of itself a few years back. We bring that up as Bumble’s financial results are complicated thanks to its ownership structure.

After the IPO, Bumble Inc. will “be a holding company, and its sole material asset will be a controlling equity interest in Bumble Holdings,” per the S-1 filing. So, how is Bumble Holdings doing?

Medium? Doing the sums ourselves as the company’s S- 1 is fraught with accounting nuances, in the first nine months of 2019, Bumble managed the following:

And then, combining two columns to provide a similar set of results for the same period of 2020, Bumble recorded:

For those following along, we’re using the “Net (loss) earnings” line, for profitability, and not the “Net (loss) earnings attributable to owners / shareholders” as that would require even more explanation and we’re keeping it simple in this first look.

While Bumble saw modest growth in 2020 through Q3 and a sharp swing to losses on a GAAP basis, the company’s adjusted profitability grew over the same time period. The company’s adjusted EBITDA, a very non-GAAP metric, expanded from $80.0 million in the first three quarters of 2019 to $108.3 million in the same period of 2020.

While we are generally willing to allow quickly growing companies some leniency when it comes to adjusted metrics, the gap between Bumble’s GAAP losses and its EBITDA results is a stress-test of our compassion. Bumble also swung from free cash flow positivity during the first nine months of 2019 to the first quarters of 2020.

If you extrapolate Bumble’s Q1, Q2 and Q3 revenue to a full-year number, the company could manage $555.5 million in 2020 revenues. Even at a modest software-ish multiple, the company would be worth more than the $3 billion figure that we discussed before.

However, its sharp unprofitability in 2020 could damper its eventual valuation. More as we dig more deeply into the filing.

Finally, on the ownership question, the company’s filing is surprisingly denuded of data. Its principal shareholder section looks like this:

When we know more, we’ll share more. Until then, happy S-1 reading.

Powered by WPeMatico

Only a few weeks after its SPAC IPO, Porch today announced that it has made four acquisitions, worth a total of $122 million. The most important here is probably the acquisition of Homeowners of America for $100 million, which gets Porch deeper into the home insurance space. In addition, Porch is also acquiring mover marketing and data platform V12 for $22 million, as well as home inspection service Palm-Tech and iRoofing, a SaaS application for roofing contractors. Porch did not disclose the acquisition prices for the latter two companies.

You may still think of Porch as a marketplace for home improvement and repair services — and that’s what it started out as when it launched about seven years ago. Yet while it still offers those services, a couple of years after its 2013 launch, the company pivoted to building what it now calls a “vertical software platform for the home.” Through a number of acquisitions, the Porch Group now includes Porch.com, as well as services like HireAHelper, Inspection Support Network for home inspectors, Kandela for providing services around moving and an insurance broker in the form of the Elite Insurance Group. In some form or another, Porch’s tools are now used — either directly or indirectly — by two-thirds of U.S. homebuyers every month.

Porch founder and CEO Matt Ehrlichman. Image Credits: Porch

As Porch founder and CEO Matt Ehrlichman told me, he had originally planned to take his company public through a traditional IPO. He noted that going the increasingly popular SPAC route, though, allowed him to push his timeline up by a year, which in turn now enables the company to make the acquisitions it announced today.

“In total, we had a $323 million fundraise that allows us now to not only be a public company with public currency, but to be very well capitalized. And picking up that year allows us to be able to go and pursue acquisitions that we think make really good fits for Porch,” Ehrlichman told me. While Porch’s guidance for its 2021 revenue was previously $120 million, it’s now updating that guidance to $170 million based on these acquisitions. That would mean Porch would grow its revenue by about 134% year-over-year between 2020 and 2021.

As the company had previously laid out in its public documents, the plan for 2021 was always to get deeper into insurance. Indeed, as Ehrlichman noted, Porch these days tends to think of itself as a vertical software company that layers insurtech on top of its services in order to be able to create a recurring revenue stream. And because Porch offers such a wide range of services already, its customer acquisition costs are essentially zero for these services.

Image Credits: Homeowners of America

Porch was already a licensed insurance brokerage. With Homeowners of America, it is acquiring a company that is both an insurance carrier as well as a managing general agent..

“We’re able to capture all of the economic value from the consumer as we help them get insurance set up with their new home and we can really control that experience to delight them. As we wrap all the technology we’ve invested in around that experience we can make it super simple and instant to be able to get the right insurance at the right price for your new home. And because we have all of this data about the home that nobody else has — from the inspection we know if the roof is old, we know if the hot water system is gonna break soon and all the appliances — we know all of this data and so it just gives us a really big advantage in insurance.”

Data, indeed, is what a lot of these acquisitions are about. Because Porch knows so much about so many customers, it is able to provide the companies it acquires with access to relevant data, which in turn helps them offer additional services and make smarter decisions.

Homeowners of America is currently operating in six states (Texas, Arizona, North Carolina, South Carolina, Virginia and Georgia) and licensed in 31. It has a network of more than 800 agencies so far and Porch expects to expand the company’s network and geographic reach in the coming months. “Because we have [customer acquisition cost]-free demand all across the country, one of the opportunities for us is simply just to expand that across the nation,” Ehrlichman explained.

As for V12, Porch’s focus is on that company’s mover marketing and data platform. The acquisition should help it reach its medium-term goal of building a $200 million revenue stream in this area. V12 offers services across multiple verticals, though, including in the automotive space, and will continue to do so. The platform’s overall focus is to help brands identify the right time to reach out to a given consumer — maybe before they decide to buy a new car or move. With Porch’s existing data layered on top of V12’s existing capabilities, the company expects that it will be able to expand these features and it will also allow Porch to not offer mover marketing but what Ehrlichman called “pro-mover” services, as well.

“V12 anchors what we call our marketing software division. A key focus of that is mover marketing. That’s where it’s going to have, long term, tremendous differentiation. But there are a number of other things that they’re working on that are going to have really nice growth vectors, and they’ll continue to push those,” said Ehrlichman.

As for the two smaller acquisitions of iRoofing and Palm-Tech, these are more akin to some of the previous acquisitions the company made in the contractor and inspection verticals. Like with those previous acquisitions, the plan is to help them grow faster, in part through integrating them into the overall Porch group’s family of products.

“Our business is and continues to be highly recurring or reoccurring in nature,” said Porch CFO Marty Heimbigner. “Nearly all of our revenues, including that of these new acquisitions, is consistent and predictable. This repeat revenue is also high margin with less than 20% cost of revenue and is expected to grow more than 30% per year on our platform. So, we believe these deals are highly accretive for our shareholders.”

Powered by WPeMatico

Applications networking company F5 announced today that it is acquiring Volterra, a multi-cloud management startup, for $500 million. That breaks down to $440 million in cash and $60 million in deferred and unvested incentive compensation.

Volterra emerged in 2019 with a $50 million investment from multiple sources, including Khosla Ventures and Mayfield, along with strategic investors like M12 (Microsoft’s venture arm) and Samsung Ventures. As the company described it to me at the time of the funding:

Volterra has innovated a consistent, cloud-native environment that can be deployed across multiple public clouds and edge sites — a distributed cloud platform. Within this SaaS-based offering, Volterra integrates a broad range of services that have normally been siloed across many point products and network or cloud providers.

The solution is designed to provide a single way to view security, operations and management components.

F5 president and CEO François Locoh-Donou sees Volterra’s edge solution integrating across its product line. “With Volterra, we advance our Adaptive Applications vision with an Edge 2.0 platform that solves the complex multi-cloud reality enterprise customers confront. Our platform will create a SaaS solution that solves our customers’ biggest pain points,” he said in a statement.

Volterra founder and CEO Ankur Singla, writing in a company blog post announcing the deal, says the need for this solution only accelerated during 2020 when companies were shifting rapidly to the cloud due to the pandemic. “When we started Volterra, multi-cloud and edge were still buzzwords and venture funding was still searching for tangible use cases. Fast forward three years and COVID-19 has dramatically changed the landscape — it has accelerated digitization of physical experiences and moved more of our day-to-day activities online. This is causing massive spikes in global Internet traffic while creating new attack vectors that impact the security and availability of our increasing set of daily apps,” he wrote.

He sees Volterra’s capabilities fitting in well with the F5 family of products to help solve these issues. While F5 had a quiet 2020 on the M&A front, today’s purchase comes on top of a couple of major acquisitions in 2019, including Shape Security for $1 billion and NGINX for $670 million.

The deal has been approved by both companies’ boards, and is expected to close before the end of March, subject to regulatory approvals.

Powered by WPeMatico

RedHat today announced that it’s acquiring container security startup StackRox . The companies did not share the purchase price.

RedHat, which is perhaps best known for its enterprise Linux products has been making the shift to the cloud in recent years. IBM purchased the company in 2018 for a hefty $34 billion and has been leveraging that acquisition as part of a shift to a hybrid cloud strategy under CEO Arvind Krishna.

The acquisition fits nicely with RedHat OpenShift, its container platform, but the company says it will continue to support StackRox usage on other platforms including AWS, Azure and Google Cloud Platform. This approach is consistent with IBM’s strategy of supporting multicloud, hybrid environments.

In fact, Red Hat president and CEO Paul Cormier sees the two companies working together well. “Red Hat adds StackRox’s Kubernetes-native capabilities to OpenShift’s layered security approach, furthering our mission to bring product-ready open innovation to every organization across the open hybrid cloud across IT footprints,” he said in a statement.

CEO Kamal Shah, writing in a company blog post announcing the acquisition, explained that the company made a bet a couple of years ago on Kubernetes and it has paid off. “Over two and half years ago, we made a strategic decision to focus exclusively on Kubernetes and pivoted our entire product to be Kubernetes-native. While this seems obvious today; it wasn’t so then. Fast forward to 2020 and Kubernetes has emerged as the de facto operating system for cloud-native applications and hybrid cloud environments,” Shah wrote.

Shah sees the purchase as a way to expand the company and the road map more quickly using the resources of Red Hat (and IBM), a typical argument from CEOs of smaller acquired companies. But the trick is always finding a way to stay relevant inside such a large organization.

StackRox’s acquisition is part of some consolidation we have been seeing in the Kubernetes space in general and the security space more specifically. That includes Palo Alto Networks acquiring competitor TwistLock for $410 million in 2019. Another competitor, Aqua Security, which has raised $130 million, remains independent.

StackRox was founded in 2014 and raised over $65 million, according to Crunchbase data. Investors included Menlo Ventures, Redpoint and Sequoia Capital. The deal is expected to close this quarter subject to normal regulatory scrutiny.

Powered by WPeMatico