exit

Auto Added by WPeMatico

Auto Added by WPeMatico

With Roblox joining the end-of-year unicorn stampede toward the public markets, we’re set for a contentedly busy second half of November and early December. I hope you didn’t have vacation planned in the next few weeks.

This morning we need to get deeper into the Roblox S-1 so we can better understand the nature of its revenue generation. Why? Because we want to start working on what the gaming company is worth; some comparisons are being made to Unity, another unicorn that went public earlier this year with a gaming focus.

The Exchange explores startups, markets and money. Read it every morning on Extra Crunch, or get The Exchange newsletter every Saturday.

Should we apply Unity’s revenue multiple to Roblox? Or does the company deserve a slimmer multiple based on the substance of its revenue?

We’ll also have to remind ourselves how much capital Roblox last raised while private, and at what price. Given our historical knowledge of its financial results, we might be able to nail some valuations to revenue figures, helping us understand, roughly, how the venture capital community was valuing Roblox while it was private.

We’ll also have to remind ourselves how much capital Roblox last raised while private, and at what price. Given our historical knowledge of its financial results, we might be able to nail some valuations to revenue figures, helping us understand, roughly, how the venture capital community was valuing Roblox while it was private.

If you want an overview of just the numbers, Natasha and I wrote a digest here.

Now, let’s get to work.

To get a foundation, let’s recall how Roblox was valued during its last private round. According to Crunchbase data, Roblox’s $150 million Series G was raised at a $3.9 billion pre-money valuation. So, Roblox was worth $4.05 billion after the February 2020 funding event.

Naturally there is a lag between when a deal is struck and when it is announced. So, let’s rewind the clock to Q4 2019 and ask ourselves what Roblox looked like at the time. From its S-1, here are the Q4 2019 numbers:

Annualizing that revenue figure, Roblox was on a $553.3 million run rate at around the time it raised that Series G. In revenue-multiple terms, Roblox was valued at 7.3x its top line on an annualized basis.

If you are a SaaS fan you are probably pretty shocked right now. Why the hell was Roblox, a software company, worth so little? Well let’s remind ourselves how it makes money:

We generate substantially all of our revenue through the sales of Robux to users. Users can spend Robux to purchase access to experiences, enhancements in experiences, and items in the Avatar Marketplace. Robux are available as one-time purchases or monthly subscriptions. We recognize revenue ratably over the estimated average lifetime of a paying user. […]

Other revenue streams include a minimal amount of revenue from advertising, licenses, and royalties.

Powered by WPeMatico

Snapchat helped pioneer the use of lenses on faces in photos and videos to turn ordinary picture messages into fantastical creations where humans can look like, say, cats, and even cats can wear festival-chic flower crowns. Now it sounds like the company might be turning its attention… to sound.

The company appears to have acquired Voisey, a U.K. startup that features instrumentals that you overlay with your own voice to create short music tracks (and videos), and also lets musicians upload instrumentals that become the basis for those tracks. Users can apply audio filters (like auto-tune, automated harmonies and some funny twists like a Billie-Eilish-ish effect) to their voices; and they can browse and view other people’s Voisey tracks.

The results look something like this or this.

The deal was first reported by Business Insider, which noted Voisey had changed its company address in London to that of Snap’s. In addition to that, we have seen that filings in Companies House indicate that the the four people who co-founded the startup — Dag Langfoss-Håland, Pal Wagtskjold-Myran, Erlend Drevdal Hausken and Oliver Barnes — as well as the startup’s first two investors — Terry Steven Fisher and Jason Lee Brook — all resigned as directors of the company on October 21. At the same time, two employees at Snap — Atul Manilal Porwal on the legal team and international controller Amanda Louise Reid — were assigned directorship roles.

Snap’s London spokesperson Tanya Ridd said Snap declined to comment for this story. Voisey did not respond to our email.

Voisey had raised only $1.88 million to date (per PitchBook data), and it’s ranked at 143 in iOS in Music in the U.S. currently, according to AppAnnie stats. It’s not clear how much Snap would have paid for the startup, but the news comes on the heels of a Snap filing earlier this month that indicated that the U.K. entity, which is still loss-making, is poised to borrow up to $500 million, so there is possibly some cash for acquisitions reserved as part of that.

Voisey has been described in the past as a “TikTok for music creation”. And it does look a little like the popular video app, which like Voisey is also focused around user-generated content. Voisey has a distinctly stronger creator feel to it, and there has even been at least one singer discovered on the platform. The Billie Eilish-esque Olivia Knight, who goes by “poutyface,” signed with Island Records/Warner Chappell earlier this year.

On the other hand, TikTok — at least for now — is less about music creation and more about people creating other kinds of content — dancing, written messages, chitchat — set to music. We write “for now” because TikTok’s parent ByteDance has also quietly acquired assets for music creation, so maybe we should watch this space.

It’s not clear whether Snap would look to integrate some or all of Voisey’s features into its flagship app Snapchat to create new music services, or run Voisey as a separate app (with easy hooks into Snapchat), or a combination of the two. Based on experience it could be any of these.

Snap has been slowly building up its music cred, but up to now that has felt more like work to clone TikTok: last month, it launched Sounds on Snapchat, a feature to let people add tunes to their Stories, to make them, well, more like TikTok videos. That has come with a growing trove of licensing deals with big publishers.

Even before it launched that, Snap hadn’t ignored the power of sound completely. It has been offering voice filters, to give your videos a more comedic twist, for years already. But with music being one of the most engaging of formats on social media, Voisey could potentially give Snap, and Snapchat, a leg up in the feature race with a platform to build original content.

What’s interesting is the timing of this deal.

It was just last week that we revealed another voice-focused acquisition of Snap’s, the Israeli startup Voca.ai, which it acquired for $70 million (although a close source disputed that and said it’s $120 million…).

As with Voisey, no word on where Voca.ai tech will be used, but Voca.ai is an AI-based startup that lets companies create interactive voice-based chatbots for customer service interactions. That could see Snap expanding the kinds of services it provides to businesses, or expanding how people can interact using voice on its existing services, specifically its Spectacles, or both (or, again, something completely different).

Put together with the Voisey deal, it’s a sign of the company doing a lot more than just snapping pictures.

Powered by WPeMatico

Onit, a workflow software company based in Houston, announced this week that it has acquired 2018 TechCrunch Disrupt Battlefield alum McCarthyFinch. Onit intends to use the startup’s AI skills to beef up its legal workflow software offerings.

The companies did not share the purchase price.

After evaluating a number of companies in the space, Onit focused on McCarthyFinch, which gives it an artificial intelligence component the company’s legal workflow software had been lacking. “We evaluated about a dozen companies in the AI space and dug in deep on six of them. McCarthyFinch stood out from the pack. They had the strongest technology and the strongest team,” Eric M. Elfman, CEO and co-founder of Onit told TechCrunch.

The company intends to inject that AI into its existing Aptitude workflow platform. “Part of what really got me excited about McCarthyFinch was the very first conversation I had with their CEO, Nick Whitehouse. They considered themselves an AI platform, which complemented our approach and our workflow automation platform, Aptitude,” Elfman said.

McCarthyFinch CEO and co-founder Whitehouse says the startup was considering whether to raise more money or look at being acquired earlier this year when Onit made its interest known. At first, he wasn’t really interested in being acquired and was hoping to go the partner route, but over time that changed.

“I was very much on the partner track, and was probably quite dismissive to begin with because I was quite focused on that partner strategy. But as we talked, all egos aside, it just made sense [to move to acquisition talks],” Whitehouse said.

The talks heated up in May and the deal officially closed last week. With Onit headquartered in Houston and McCarthyFinch in New Zealand the negotiations and meetings all happened on Zoom. The two companies’ principals have never met in person. The plan is for McCarthyFinch to stay in place, even after the pandemic ends. Whitehouse expects to make a trip to Houston whenever it is safe to do so.

Whitehouse says his experience with Battlefield has had a huge influence on him. “Just the insights that we got through Battlefield, the coaching that we got, those things have stuck with me and they’ll stick with me for the rest of my life,” he said.

The company had 45 customers and 17 employees at the time of the acquisition. It raised US$5 million along the way. Now it becomes part of Onit as the journey continues.

Powered by WPeMatico

The security sector is ever frothy and acquisitive. Just last week Palo Alto Networks grabbed Expanse for $800 million. Today it was FireEye’s turn, snagging Respond Software, a company that helps customers investigate and understand security incidents, while reducing the need for highly trained (and scarce) security analysts. The deal has closed, according to the company.

FireEye had its eye on Respond’s Analyst product, which it plans to fold into its Mandiant Solutions platform. Like many companies today, FireEye is focused on using machine learning to help bolster its solutions and bring a level of automation to sorting through the data, finding real issues and weeding out false positives. The acquisition gives them a quick influx of machine learning-fueled software.

FireEye sees a product that can help add speed to its existing tooling. “With Mandiant’s position on the front lines, we know what to look for in an attack, and Respond’s cloud-based machine learning productizes our expertise to deliver faster outcomes and protect more customers,” Kevin Mandia, FireEye CEO said in a statement announcing the deal.

Mike Armistead, CEO at Respond, wrote in a company blog post that today’s acquisition marks the end of a four-year journey for the startup, but it believes it has landed in a good home with FireEye. “We are proud to announce that after many months of discussion, we are becoming part of the Mandiant Solutions portfolio, a solution organization inside FireEye,” Armistead wrote.

While FireEye was at it, it also announced a $400 million investment from Blackstone Tactical Opportunities fund and ClearSky (an investor in Respond), giving the public company a new influx of cash to make additional moves like the acquisition it made today.

It didn’t come cheap. “Under the terms of its investment, Blackstone and ClearSky will purchase $400 million in shares of a newly designated 4.5% Series A Convertible Preferred Stock of FireEye (the ‘Series A Preferred’), with a purchase price of $1,000 per share. The Series A Preferred will be convertible into shares of FireEye’s common stock at a conversion price of $18.00 per share,” the company explained in a statement. The stock closed at $14.24 today.

Respond, which was founded in 2016, raised $32 million, including a $12 million Series A in 2017 led by CRV and Foundation Capital and a $20 million Series B led by ClearSky last year, according to Crunchbase data.

Powered by WPeMatico

As IBM transitions from software and services to a company fully focussed on hybrid cloud management, it announced its intention to buy Instana, an applications performance management startup with a cloud native approach that fits firmly within that strategy.

The companies did not reveal the purchase price.

With Instana, IBM can build on its internal management tools, giving it a way to monitor containerized environments running Kubernetes. It hopes by adding the startup to the fold it can give customers a way to manage complex hybrid and multi-cloud environments.

“Our clients today are faced with managing a complex technology landscape filled with mission-critical applications and data that are running across a variety of hybrid cloud environments – from public clouds, private clouds and on-premises,” Rob Thomas, senior vice president for cloud and data platform said in a statement. He believes Instana will help ease that load, while using machine learning to provide deeper insights.

At the time of the company’s $30 million Series C in 2018, TechCrunch’s Frederic Lardinois described the company this way. “What really makes Instana stand out is its ability to automatically discover and monitor the ever-changing infrastructure that makes up a modern application, especially when it comes to running containerized microservices.” That would seem to be precisely the type of solution that IBM would be looking for.

As for Instana, the founders see a good fit for the two companies, especially in light of the Red Hat acquisition in 2018 that is core to IBM’s hybrid approach. “The combination of Instana’s next generation APM and Observability platform with IBM’s Hybrid Cloud and AI technologies excited me from the day IBM approached us with the idea of joining forces and combining our technologies,” CEO Mirko Novakovic wrote in a blog post announcing the deal.

Indeed, in a recent interview IBM CEO Arvind Krishna told CNBC’s Jon Fortt, that they are betting the farm on hybrid cloud management with Red Hat at the center. When you combine that with the decision to spin out the company’s managed infrastructure services business, this purchase shows that they intend to pursue every angle

“The Red Hat acquisition gave us the technology base on which to build a hybrid cloud technology platform based on open-source, and based on giving choice to our clients as they embark on this journey. With the success of that acquisition now giving us the fuel, we can then take the next step, and the larger step, of taking the managed infrastructure services out. So the rest of the company can be absolutely focused on hybrid cloud and artificial intelligence,” Krishna told CNBC.

Instana, which is based in Chicago with offices in Munich, was founded in 2015 in the early days of Kubernetes and the startup’s APM solution has evolved to focus more on the needs of monitoring in a cloud native environment. The company raised $57 million along the way with the most recent round being that Series C in 2018.

The deal per usual is subject to regulatory approvals, but the company believes it should close in the next few months.

Powered by WPeMatico

Hello and welcome back to Equity, TechCrunch’s venture capital-focused podcast where we unpack the numbers behind the headlines.

Today we have an Equity Shot for you about Airbnb’s S-1 filing, as it looks to go public before the year is out.

All that, and our trusty other host Danny Crichton was busy filing a post about the winners and losers of the Airbnb IPO. Ownership, you quiet, billionaire beast. There’s more coming from TechCrunch on the company’s IPO, and from the Equity crew on everything else we ferret out on Thursday. Stay tuned!

Equity drops every Monday at 7:00 a.m. PDT and Thursday afternoon as fast as we can get it out, so subscribe to us on Apple Podcasts, Overcast, Spotify and all the casts.

Powered by WPeMatico

Airbnb filed to go public today, bringing the well-known unicorn one step closer to being a public company.

The financial results show a company on the rebound, but smaller than it was. Its more granular financial results also make clear how hard the pandemic was on the travel-reliant unicorn. Regarding Airbnb’s worth, investors will have to balance how they value recovery and recent profits over the company’s disrupted historical growth arc.

The home-sharing startup had a tumultuous year, with the COVID-19 pandemic harming its business in the first and second quarters of the year, and Airbnb later recovering on the strength of more local bookings.

Its filing comes mere days after fellow unicorns DoorDash and C3.ai themselves filed to go public in what could be a rush to the public markets by richly valued startups.

Airbnb’s S-1 filing was expected to come last week, but was delayed due to purported election concerns, a concept that TechCrunch staff did not find entirely convincing.

We’ve scraped together quite a lot about Airbnb’s recent financial performance, but its S-1 is the real treasure trove. What follows is a dive into the company’s high-level numbers. From there, TechCrunch will dig into the company’s financial nuances and ownership stakes.

What we want to know is how the pandemic impacted Airbnb’s business; its year-to-date results, and what we can suss out from its quarterly trends.

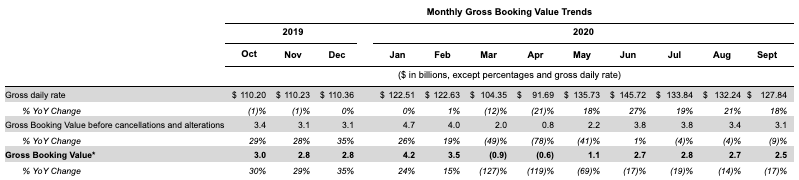

Up top in Airbnb’s S-1 is a chart that shows monthly bookings on its platform. The implication is somewhat simple; namely that Airbnb knows what we want to know and wanted to share. Here are those numbers:

Image Credits: Airbnb S-1

As expected, Airbnb took a huge hit in March. But by May things were back to year-over-year growth, where they stayed.

Now, the company has seen precious little bookings growth since June — indeed it has seen bookings fall in the months since. And, worse, the company’s gross bookings after removing cancellations are down on a year-over-year basis. (Update: We misread this table at first, and have updated our notes on it.)

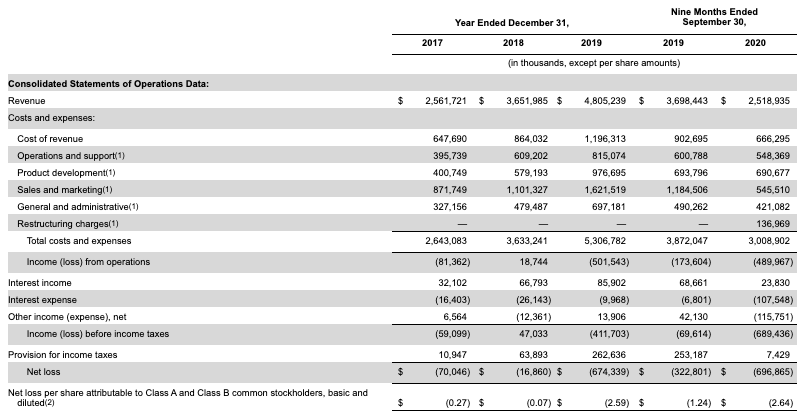

So, what does all of that look like in more traditional accounting figures? Here’s Airbnb’s reported income statement:

Image Credits: Airbnb S-1

As expected, Airbnb’s year has not been tremendous. Indeed, the company is on track to match its 2018 size, if we have our math correct.

What changed from the first three quarters of 2019 to the first three quarters of 2020? The biggest thing, apart from expected lower revenue costs — less revenue costs less — is the huge decline in sales and marketing spend at the company. Airbnb slashed S&M outlays from $1.18 billion in the first three quarters of 2019 to just $545.5 million in the same period of 2020.

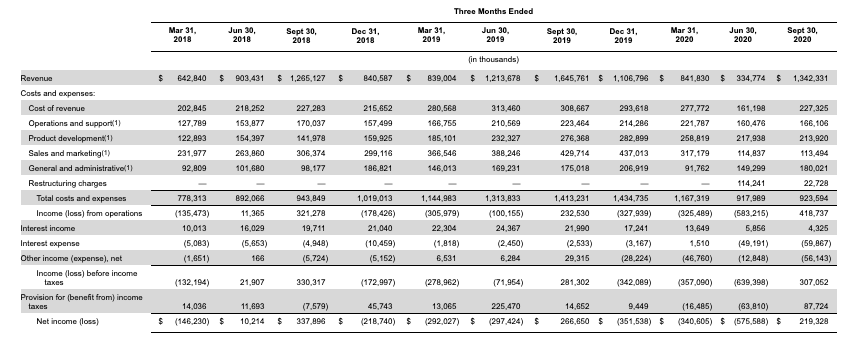

So, where will Airbnb wind up in 2020 once it’s all done? We’ll need to peek at its quarterly results for that. Here they are:

Image Credits: Airbnb S-1

Airbnb’s growth continues in year-over-year terms right until the March 31, 2020 quarter, when it was effectively flat compared to Q1 2019. Or, the company would have grown sans COVID-19. In the June 30, 2020 quarter we see the real damage, with Airbnb’s revenue falling from $1.2 billion in the year-ago quarter to just $334.8 million. That’s a shocking decline.

But, looking ahead to Q3 2020 we see a large return to form. Yes, Airbnb’s third quarter was smaller than its Q3 2019, with $1.34 billion in top line instead of $1.65 billion in 2019, but the company effectively quadrupled from its preceding quarter. If the company manages another Q3 worth of revenue in Q4, it would be larger than it was in 2018 by a few hundred million.

Critically, Airbnb managed to swing from a number of unprofitable quarters to a profit in Q3, akin to its 2019 Q3 when it was also in the black. Of course, Airbnb’s $219.3 million in GAAP net income during the third quarter pales compared to its losses tallied earlier in the year. The company will not break even in 2020.

Airbnb also reported adjusted profit metrics. Its adjusted EBITDA results are based on the following definition:

Adjusted EBITDA is defined as net income or loss adjusted for (i) provision for income taxes; (ii) interest income, interest expense, and other income (expense), net; (iii) depreciation and amortization; (iv) stock-based compensation expense; (v) net changes to the reserves for lodging taxes for which we may be held jointly liable with hosts for collecting and remitting such taxes; and (vi) restructuring charges.

The decision to remove restructuring costs raised eyebrows, with Amy Cheetham, an investor at Costanoa Ventures, saying that “it feels like leaving out restructuring costs is a little aggressive?” We agree, as it gives the company too much flexibility to count the good in its results, like lower operating costs, while discounting what it took to get those results, like restructuring its business operations.

That’s having your cake and eating it as well and not counting the calories.

Still, who are we to withhold numbers from you? Here is the very adjusted EBITDA that Airbnb claims:

Image Credits: Airbnb S-1

The numbers are still not good even after ripping out so very any costs. Worse, perhaps is the company’s cash burn in the year. That deficit helps explain why Airbnb took on more capital when it did earlier this year.

It’s hard to put a firm grade on this S-1. It contains what we expected, but how investors weigh the company’s year-over-year revenue declines in Q3 2020 against its rapid comeback from Q2 2020 should help decide its eventual value. On the whole Airbnb has managed something incredibly impressive — bouncing back from so low a low.

But, now that it’s going public we can’t merely say “good job”; it wants to price itself well and trade strongly. So, all eyes on its first IPO range as that should tell us what investors just might be willing to pay for the famous company’s equity.

Powered by WPeMatico

Federal regulators have approved Mastercard’s acquisition of Salt Lake City-based startup Finicity, which provides open-banking APIs. The deal is expected to go for $825 million.

“We were notified that the Department of Justice completed its review of our planned acquisition of Finicity and has cleared it to move forward,” Mastercard wrote in a statement. “We are pleased to have reached this milestone.”

Finicity allows users to be able to decide how their financial information is shared and who can make money decisions on their behalf through open APIs. The buy will allow Mastercard to offer consumers and businesses more choice in these transactions, without requiring them to do heavy lifting themselves.

Finicity, according to Crunchbase, has raised nearly $80 million in known venture capital as a private company. When closed, it will be one of the largest fintech acquisitions at nearly $1 billion in 2020.

The DOJ approval comes just two weeks after the body filed an antitrust lawsuit challenging Visa’s proposed $5.3 billion buy of Plaid. Plaid, which empowers a large chunk of financial services through its data network, including Venmo and Acorns, is being accused of making Visa a monopoly in online debt services.

Plaid has denied these claims, saying that “Visa intends to defend the transaction vigorously.” The feds are also looking into Intuit’s $7 billion proposed buy of Credit Karma, which was first announced in February 2020.

The approval of the Mastercard-Finicity transaction could be a shot in the arm for fintech startup valuations. After both the Plaid and Credit Karma deals came under increasing regulatory scrutiny, it was an open questions whether big-dollar M&A was going to be an option for fintech unicorns.

If the path was closed due to regulatory concerns, fintech startups would have to either pursue earlier, smaller sales themselves, or wait for an eventual IPO. If that was the case, venture capitalists might shun putting as much capital to work in the sector. However, the Finicity approval makes it clear that not all fintech M&A worth $500 million or more is going to encounter oversight headaches. That should be welcome news for late-stage fintech valuations.

Powered by WPeMatico

DoorDash filed to go public today, publishing numbers that showed rapid growth, enhanced profitability and an improving cash flow record which helped explain how the company had grown to a $16 billion valuation while private. The unicorn’s impending liquidity event will enrich a host of venture capital firms that bet on its eventual maturity.

Instead of posting this entry of The Exchange on Monday, we’ve put it out today for your Friday and weekend reading. Enjoy! — Alex and Walter.

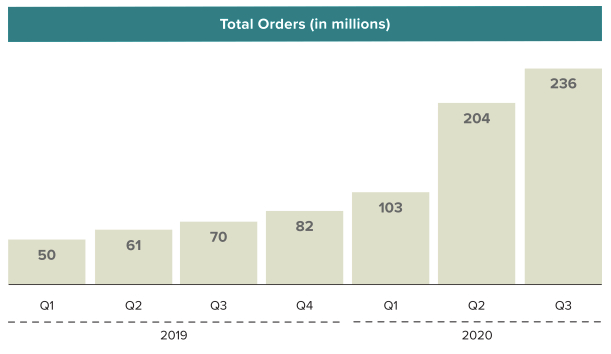

But notable in DoorDash’s impressive results is the impact of COVID-19, accelerating secular trends already in place, and boosting the unicorn’s growth. Before we get into pricing this IPO and guessing what the company might be worth, let’s strive to understand what portion of its 2020 business gains could stem from the pandemic — and might not persist into the future.

We’re not being pessimistic; we merely want to better understand the company. And DoorDash agrees with our general thrust, writing in its S-1 filing that “58% of all adults and 70% of millennials say that they are more likely to have restaurant food delivered than they were two years ago,” adding that it believes “the COVID-19 pandemic has further accelerated these trends.”

Even more, elsewhere in its filings DoorDash states plainly that COVD-19 led it to experience “a significant increase in revenue, Total Orders, and Marketplace [gross order volume] due to increased consumer demand for delivery, more merchants using our platform to facilitate both delivery and take-out, and improved efficiency of our local logistics platform.” The company then went on to warn investors that the “circumstances that have accelerated the growth of our business stemming from the effects of the COVID-19 pandemic may not continue in the future, and we expect the growth rates in revenue, Total Orders, and Marketplace [gross order volume] to decline in future periods.”

We’re not idly speculating.

Let’s observe how DoorDash’s growth accelerated from 2019 through 2020 and then peek at how the company’s economics improved during the same period, giving the company a shot at adjusted profitability for the full year, a nearly unheard of result in the on-demand market.

DoorDash generates revenue when a customer orders food via its service, splitting the total bill of food costs, taxes, fees and tips, distributing them to itself, the merchant creating the goods and the delivery person.

In an “illustrative” example that DoorDash notes its 2019 “approximate average per-order information,” the split works out as follows:

Given that the company is giving us old data and DoorDash’s performance has been stellar this year in terms of generating more gross profit, I wonder what has happened amidst 2020’s upheaval. But, the old numbers do for what we need, which is to understand the link between gross order volume (GOV) and DoorDash revenue. When the former goes up, the latter goes up.

So, as orders rise:

Powered by WPeMatico

Palo Alto Networks has been on a buying binge for the last couple of years, and today it added to its haul, announcing a deal to acquire Expanse for $800 million in cash and equity awards. The deal breaks down to $670 million in cash and stock and another $130 million in equity awards to Expanse employees.

Expanse provides a service to help companies understand and protect their attack surface, where they could be most vulnerable to attack. It works by giving the security team a view of how the company’s security profile could look to an attacker trying to gain access.

The plan is to fold Expanse into Palo Alto’s Cortex Suite, an AI-driven set of tools designed to detect and prevent attacks in an automated way. Expanse should provide Palo Alto with a highly valuable set of data to help feed the AI models.

“By integrating Expanse’s attack surface management capabilities into Cortex after closing, we will be able to offer the first solution that combines the outside view of an organization’s attack surface with an inside view to proactively address all security threats,” Palo Alto Networks chairman and CEO Nikesh Arora said in a statement.

Expanse sees the acquisition as a way to accelerate the company road map using the resources of a larger company like Palo Alto, a typical argument from companies being acquired. “Joining forces with Palo Alto Networks will let us achieve our most important business goals years ahead of schedule. During the course of conversations with Palo Alto Networks leadership, we shared optimism that the right combination of technology and people can solve many cybersecurity challenges that to date have seemed intractable,” the startup’s founders wrote in a blog post announcing the deal.

The two co-founders, Dr. Tim Junio and Dr. Matt Kraning, will be joining Palo Alto under the terms of the deal, which is expected to close in Palo Alto’s fiscal second quarter, assuming it passes regulatory muster.

Expanse was founded in 2012 and has raised $136 million, according to Crunchbase data. Its most recent raise was a $70 million Series C last year, which was led by TPG.

Today’s acquisition is Palo Alto’s third in 2020 and the 10th since 2018. Palo Alto stock was up 2.15% in early trading.

Powered by WPeMatico