exit

Auto Added by WPeMatico

Auto Added by WPeMatico

Pokémon GO creator Niantic has acquired a small SF gaming startup building a league and tournament organization platform to help gamers create their own communities around popular titles.

Mayhem was in Y Combinator’s winter 2018 batch and went on to raise $5.7 million in funding, according to Crunchbase. Other backers include Accel, which led the startup’s Series A in 2018, Afore Capital and NextGen Venture Partners.

The startup’s focus has shifted quite a bit since its initial YC debut, when it announced a service called Visor that would analyze video of esports gameplay and coach users on how they could improve their performance. The company has seemed to shift its focus wholly to community tools to help gamers find matches and organize tournaments for games like Overwatch on its platform.

Terms of the acquisition weren’t disclosed by Niantic .

The “majority” of Mayhem’s team will be joining Niantic with the startup’s CEO Ivan Zhou landing in the company’s Social Platform Product team while the rest of the team joins Platform Engineering.

In a statement, Niantic asserts that the acquisition “reinforces our commitment to real-world social as the centerpiece of our mission.”

Most of Niantic’s acquisitions of late have focused on augmented reality backend technologies, so it’s interesting to see them buying tech that focuses on community organization.

Pokémon GO continues to be Niantic’s cash cow, though the company hasn’t seen the same levels of viral success with subsequent releases where organic growth hasn’t been quite as easy to come by. Buying a startup building community tools suggests the company is ready to bring in some outside tech to push their own efforts forward as they strive to create a broader platform for their AR ambitions and more standalone hits of their own.

Powered by WPeMatico

Today Bumble, a popular dating-focused startup, was reported by Bloomberg to have filed IPO documents, albeit privately.

The news that Bumble is pursuing an IPO is not a surprise. TechCrunch covered the story in September, noting the huge revenues that its rival Tinder has managed to accrete, possibly indicative of a sufficiently large market to support two public dating players.

That Bumble has privately filed puts it, along with the crypto-focused Coinbase, as far along the IPO path before we can see their numbers. When they make their S-1 filings public the two companies will provide the market a look into their financial results.

Bumble and Coinbase are preceded in making such disclosures by Roblox, Affirm and Poshmark. The five companies will join others in seeking IPOs over the next few months.

According to a recent interview with GGV’s Hans Tung — an investor in Affirm and Airbnb and other unicorns — TechCrunch understands that quarters one, three and four in 2021 could prove to be active IPO periods. Bumble joining the fray in the final weeks of 2020 underscores how active the start of the year could be for highly priced private companies seeking liquidity while public markets trade near all-time highs.

TechCrunch reached out to Bumble for comment on the IPO report. The company declined to comment.

Bloomberg reports that Bumble could target a valuation of between $6 and $8 billion. This squares with prior reporting. How much revenue the market will require of Bumble to reach those prices, and at what pace of growth, is not clear.

But with the company reaching 100 million users earlier this year, perhaps all the math will pencil out.

Powered by WPeMatico

UiPath, the robotic process automation startup that has been growing like gangbusters, filed confidential paperwork with the SEC today ahead of a potential IPO.

“UiPath, Inc. today announced that it has submitted a draft registration statement on a confidential basis to the U.S. Securities and Exchange Commission (the “SEC”) for a proposed public offering of its Class A common stock. The number of shares of Class A common stock to be sold and the price range for the proposed offering have not yet been determined. UiPath intends to commence the public offering following completion of the SEC review process, subject to market and other conditions,” the company said in a statement.

The company has raised more than $1.2 billion from investors like Accel, CapitalG, Sequoia and others. Its biggest raise was $568 million led by Coatue on an impressive $7 billion valuation in April 2019. It raised another $225 million led by Alkeon Capital last July when its valuation soared to $10.2 billion.

At the time of the July raise, CEO and co-founder Daniel Dines did not shy away from the idea of an IPO, telling me:

We’re evaluating the market conditions and I wouldn’t say this to be vague, but we haven’t chosen a day that says on this day we’re going public. We’re really in the mindset that says we should be prepared when the market is ready, and I wouldn’t be surprised if that’s in the next 12-18 months.

This definitely falls within that window. RPA helps companies take highly repetitive manual tasks and automate them. So for example, it could pull a number from an invoice, fill in a number in a spreadsheet and send an email to accounts payable, all without a human touching it.

It is a technology that has great appeal right now because it enables companies to take advantage of automation without ripping and replacing their legacy systems. While the company has raised a ton of money, and seen its valuation take off, it will be interesting to see if it will get the same positive reception as companies like Airbnb, C3.ai and Snowflake.

Powered by WPeMatico

Two months ago, Kubernetes observability platform Pixie Labs launched into general availability and announced a $9.15 million Series A funding round led by Benchmark, with participation from GV. Today, the company is announcing its acquisition by New Relic, the publicly traded monitoring and observability platform.

The Pixie Labs brand and product will remain in place and allow New Relic to extend its platform to the edge. From the outset, the Pixie Labs team designed the service to focus on providing observability for cloud-native workloads running on Kubernetes clusters. And while most similar tools focus on operators and IT teams, Pixie set out to build a tool that developers would want to use. Using eBPF, a relatively new way to extend the Linux kernel, the Pixie platform can collect data right at the source and without the need for an agent.

At the core of the Pixie developer experience are what the company calls “Pixie scripts.” These allow developers to write their debugging workflows, though the company also provides its own set of these and anybody in the community can contribute and share them as well. The idea here is to capture a lot of the informal knowledge around how to best debug a given service.

“We’re super excited to bring these companies together because we share a mission to make observability ubiquitous through simplicity,” Bill Staples, New Relic’s chief product officer, told me. “[…] According to IDC, there are 28 million developers in the world. And yet only a fraction of them really practice observability today. We believe it should be easier for every developer to take a data-driven approach to building software and Kubernetes is really the heart of where developers are going to build software.”

It’s worth noting that New Relic already had a solution for monitoring Kubernetes clusters. Pixie, however, will allow it to go significantly deeper into this space. “Pixie goes much, much further in terms of offering on-the-edge, live debugging use cases, the ability to run those Pixie scripts. So it’s an extension on top of the cloud-based monitoring solution we offer today,” Staples said.

The plan is to build integrations into New Relic into Pixie’s platform and to integrate Pixie use cases with New Relic One as well.

Currently, about 300 teams use the Pixie platform. These range from small startups to large enterprises and, as Staples and Pixie co-founder Zain Asgar noted, there was already a substantial overlap between the two customer bases.

As for why he decided to sell, Asgar — a former Google engineer working on Google AI and adjunct professor at Stanford — told me that it was all about accelerating Pixie’s vision.

“We started Pixie to create this magical developer experience that really allows us to redefine how application developers monitor, secure and manage their applications,” Asgar said. “One of the cool things is when we actually met the team at New Relic and we got together with Bill and [New Relic founder and CEO] Lew [Cirne], we realized that there was almost a complete alignment around this vision […], and by joining forces with New Relic, we can actually accelerate this entire process.”

New Relic has recently done a lot of work on open-sourcing various parts of its platform, including its agents, data exporters and some of its tooling. Pixie, too, will now open-source its core tools. Open-sourcing the service was always on the company’s road map, but the acquisition now allows it to push this timeline forward.

“We’ll be taking Pixie and making it available to the community through open source, as well as continuing to build out the commercial enterprise-grade offering for it that extends the New Relic One platform,” Staples explained. Asgar added that it’ll take the company a little while to release the code, though.

“The same fundamental quality that got us so excited about Lew as an EIR in 2007, got us excited about Zain and Ishan in 2017 — absolutely brilliant engineers, who know how to build products developers love,” Benchmark Ventures General Partner Eric Vishria told me. “New Relic has always captured developer delight. For all its power, Kubernetes completely upends the monitoring paradigm we’ve lived with for decades. Pixie brings the same easy to use, quick time to value, no-nonsense approach to the Kubernetes world as New Relic brought to APM. It is a match made in heaven.”

Powered by WPeMatico

The WSJ is reporting that Airbnb is expected to price its IPO at either $67 or $68 per share. The American hospitality unicorn raised its IPO price target earlier this week, from $44 to $50 to $56 to $60.

While we’re still waiting for official pricing, Airbnb is worth $41 billion at its IPO price, using the upper pricing estimate and the company’s share count of 602,448,251 from its most recent S-1/A filing. That figure rises sharply if we included more than 50 million shares that could be added to the mix upon the exercise of vested employee options. The company’s fully diluted valuation at its IPO price was calculated to be $47 billion.

Axios reports that Airbnb raised $3.5 billion at its fully diluted valuation.

Regardless of how you prefer to value the company, its worth has risen sharply from an early pandemic nadir of $18 billion. After COVID-19 ravaged the company’s business, it laid off staff and took on external capital.

Since the end of Q1 and the first months of Q2, Airbnb has recovered, allowing it to file to go public and earn its highest valuation to date.

The company’s pricing comes after both DoorDash and C3.ai each priced above their own raised ranges, and saw their shares skyrocket in the first day’s trading. Some exuberance was therefore not unexpected.

Airbnb starts trading tomorrow morning. More then.

Powered by WPeMatico

The Federal Trade Commission has sued to block Procter & Gamble’s acquisition of Billie, a NY-based startup that sells razors and body wash.

In the notice, the FTC alleged that the merger would “eliminate innovative nascent competitors for wet shave razors” to the loss of consumers.

Billie was founded in 2017 with the goal of fighting the “pink tax” on goods marketed to women, including razors and body wash. It went up against companies like P&G and Edgewell Personal Care by offering high-quality and cheap razors. The company announced its intent to be acquired by P&G after raising just $35 million in venture capital in June.

“As its sales grew, Billie was likely to expand into brick-and-mortar stores, posing a serious threat to P&G. If P&G can snuff out Billie’s rapid competitive growth, consumers will likely face higher prices,” Ian Conner, director of the FTC’s Bureau of Competition said in a statement.

P&G has been on a buying spree as of late. Along with the Billie news, Procter & Gamble acquired Walker & Company, which created Bevel, a grooming line for men of color, and Form, a hair-care line for women of color. In February 2019, P&G announced plans to acquire This is L, a feminine-care brand that sells tampons, pads and wipes.

If the FTC wins, this is another blow for direct-to-consumer brands on the base of competition dynamics. In May 2019, Edgewell Personal Care announced it intended to buy Harry’s, another direct-to-consumer shaving brand. In February 2020, the FTC filed a lawsuit to block the deal from happening, similarly citing how the deal would limit competition and innovation in the razor market.

Unlike Harry’s, Billie was bought before it broke into brick-and-mortar retail stores. If the deal doesn’t close, Billie lost precious time it could have used to expand into new locations and markets — and P&G will lose some of its competitive advantage in the women’s shaving world.

Harry’s and Billie’s blocks could negatively trickle down to hurt direct-to-consumer products looking at health and wellness more broadly.

Note that exit market isn’t as dull for all companies in the consumer packaged goods (CPG) world. We’ve seen deals close like Blue Bunny’s buy of Halo Top, Mars’ acquisition of Kind Bars and, of course, Unilever’s $1 billion acquisition of Dollar Shave Club.

Andrea Hernández, a founder and consultant on food and beverage CPG, says that DTC companies often need to partner with mega-businesses to get the distribution scale they need, focusing more on omni-channel presence versus a single seller point.

“It’s very limited for these companies to scale at the same level and grow without incurring debt or needing constant injections of [money],” she said. “Or [you can go] the preferred route which is having BigDaddyCorp come whisk you away. You get a success story and the resources to continue your journey.”

That said, the coronavirus has even impacted food CPG companies by forcing them to slash SKUs (or stock keeping units) and prioritize essential goods. Whereas before, CPG companies might stock a variety of goods for a variety of customer needs, they’re now prioritizing a smaller slice of the pie to manage uncertainty among consumer behavior. Long-term, this means that CPGs might be buying fewer of the Billies and Harry’s of the world and just focusing on what’s working now.

Regardless of how this plays out, today’s news shows that the FTC is paying more attention than ever to consumer and tech.

Powered by WPeMatico

According to media reports, food-delivery giant DoorDash priced its IPO at $102 per share, ahead of its final IPO pricing range of $90 to $95 per share.

The company’s debut has been warmly anticipated by public investors, as evinced by the company raising its range from an initial target of $75 to $85.

While we’re still waiting for official pricing, the price point makes DoorDash worth $32 billion at the time of its IPO price on a non-diluted basis (we’re using the company’s final S-1/A share count of 317,656,521). That valuation rises if one includes options that have vested but not been exercised, and even more if shares set aside for future compensation are also tallied. CNBC calculates DoorDash’s valuation to be $38.7 billion on a diluted basis.

Regardless, any of the valuation marks for DoorDash at $102 per share are far and away greater than its final pre-IPO valuation of around $16 billion, set this summer when the company took on additional capital. The unicorn raised more money during a growth boom, allowing it to add to its cash reserves ahead of its IPO with limited dilution.

DoorDash, which doubled its private startup valuation, is now incredibly well-capitalized to take on rivals Uber Eats and others. And at a price far above its raised range, it has more cash than it probably hoped for. How it uses that cash to preserve pandemic-driven gains will be a key narrative from the company in 2021.

More when we get official numbers.

Powered by WPeMatico

Vista Equity Partners hasn’t been shy about scooping up enterprise companies over the years, and today it added to a growing portfolio with its purchase of Gainsight. The company’s software helps clients with customer success, meaning it helps create a positive customer experience when they interact with your brand, making them more likely to come back and recommend you to others. Sources pegged the price tag at $1.1 billion.

As you might expect, both parties are putting a happy face on the deal, talking about how they can work together to grow Gainsight further. Certainly, other companies like Ping Identity seem to have benefited from joining forces with Vista. Being part of a well-capitalized firm allowed them to make some strategic investments along the way to eventually going public last year.

Gainsight and Vista are certainly hoping for a similar outcome in this case. Monti Saroya, co-head of the Vista Flagship Fund and senior managing director at the firm, sees a company with a lot of potential that could expand and grow with help from Vista’s consulting arm, which helps portfolio companies with different aspects of their business like sales, marketing and operations.

“We are excited to partner with the Gainsight team in its next phase of growth, helping the company to expand the category it has created and deliver even more solutions that drive retention and growth to businesses across the globe,” Saroya said in a statement.

Gainsight CEO Nick Mehta likes the idea of being part of Vista’s portfolio of enterprise companies, many of whom are using his company’s products.

“We’ve known Vista for years, since 24 of their portfolio companies use Gainsight. We’ve seen Gainsight clients like JAMF and Ping Identity partner with Vista and then go public. We believe we are just getting started with customer success, so we wanted the right partner for the long term and we’re excited to work with Vista on the next phase of our journey,” Mehta told TechCrunch.

Brent Leary, principle analyst at CRM Essentials, who covers the sales and marketing space, says that it appears that Vista is piecing together a sales and marketing platform that it could flip or go public in a few years.

“It’s not only the power that’s in the platform, it’s also the money. And Vista seems to be piecing together an engagement platform based on the acquisitions of Gainsight, Pipedrive and even last year’s Acquia purchase. Vista isn’t afraid to spend big money, if they can make even bigger money in a couple years if they can make these pieces fit together,” Leary told TechCrunch.

While Gainsight exits as a unicorn, the deal might not have been the outcome it was looking for. The company raised more than $187 million, according to PitchBook data, though its fundraising had slowed in recent years. Gainsight raised $50 million in April of 2017 at a post-money valuation of $515 million, again per PitchBook. In July of 2018 it added $25 million to its coffers, and the final entry was a small debt investment raised in 2019.

It could be that the startup saw its growth slow down, leaving it somewhere between ready for new venture investment and profitability. That’s a gap that PE shops like Vista look for, write a check, shake up a company and hopefully exit at an elevated price.

Gainsight hired a new chief revenue officer last month, notably. Per Forbes, the company was on track to reach “about” $100 million ARR by the end of 2020, giving it a revenue multiple of around 11x in the deal. That’s under current market norms, which could imply that Gainsight had either lower gross margins than comparable companies, or as previously noted, that its growth had slowed.

A $1.1 billion exit is never something to bemoan — and every startup wants to become a unicorn — but Gainsight and Mehta are well known, and we were hoping for the details only an S-1 could deliver. Perhaps one day with Vista’s help that could happen.

Powered by WPeMatico

Jason Green has a pretty solid reputation as venture capitalists go. The enterprise-focused firm he co-founded 17 years ago, Emergence Capital, has backed Saleforce, Box and Zoom, among many other companies, and even while every firm is now investing in software-as-a-service startups, his remains a go-to for many top founders selling business products and services.

To learn more about the trends impacting Green’s slice of the investing universe, we talked with him late last week about everything from SPACs to valuations to how the firm differentiates itself from the many rivals with which it’s now competing. Below are some outtakes edited lightly for length.

TC: What do you make of the assessment that SPACs are for companies that aren’t generating enough revenue to go public the traditional route?

JG: Well, yeah, it’ll be really interesting. This has been quite a year for SPACs, right? I can’t remember the number, but it’s been something like $50 billion of capital raised this year in SPACs, and all of those have to put that money to work within the next 12 to 18 months or they give it back. So there’s this incredible pent-up demand to find opportunities for those SPACs to convert into companies. And the companies that are at the top of the charts, the ones that are the high-growth and profitable companies, will probably do a traditional IPO, I would imagine.

So [SPAC candidates are] going to be companies that are growing fast enough to be attractive as a potential public company but not top of the charts. So I do think [sponsors are] going to target companies that are probably either growing slightly slower than the top-quartile public companies but slightly profitable, or companies that are growing faster but still burning a lot of cash and might actually scare all the traditional IPO investors.

TC: Are you having conversations with CEOs about whether or not they should pursue this avenue?

JG: We just started having those conversations now. There are several companies in the portfolio that will probably be public companies in the next year or two, so it’s definitely an alternative to consider. I would say there’s nothing impending I see in the portfolio. With most entrepreneurs, there’s a little bit of this dream of going public the traditional way, where SPACs tend to be a little bit less exciting from that perspective. So for a company that maybe is thinking about another private round before going public, it’s like a private-plus round. I would say it’s a tweener, so the companies that are considering it are probably ones that are not quite ready to go public yet.

TC: A lot of the SPAC fundraising has seemed like a reaction to uncertainty around when the public window might close. With the election behind us, do you think there’s less uncertainty?

JG: I don’t think risk and uncertainty has decreased since the election. There’s still uncertainty right now politically. The pandemic has reemerged in a significant way, even though we have some really good announcements recently regarding vaccines or potential vaccines. So there’s just a lot of potential directions things could head in.

It’s an environment generally where the public markets tend to gravitate more toward higher-quality opportunities, so fewer companies but higher quality, and that’s where I think SPACs could play a role. I’d say first half of next year, I could easily see SPACs being the more likely go-to-market for a public company, then the latter half of next year, once the vaccines have kicked in and people feel like we’re returning to somewhat normal, I could see the traditional IPO coming back.

TC: When we sat down in person about a year ago, you said Emergence looks at maybe 1,000 deals a year, does deep due diligence on 25 and funds just a handful or so of these startups every year. How has that changed in 2020?

JG: I would say that over the last five years, we’ve made almost a total transition. Now we’re very much a data-driven, thesis-driven outbound firm, where we’re reaching out to entrepreneurs soon after they’ve started their companies or gotten seed financing. The last three investments that we made were all relationships that [date back] a year to 18 months before we started engaging in the actual financing process with them. I think that’s what’s required to build a relationship and the conviction, because financings are happening so fast.

I think we’re going to actually do more investments this year than we maybe have ever done in the history of the firm, which is amazing to me [considering] COVID. I think we’ve really honed our ability to build this pipeline and have conviction, and then in this market environment, Zoom is actually helping expand the landscape that we’re willing to invest in. We’re probably seeing 50% to 100% more companies and trying to whittle them down over time and really focus on the 20 to 25 that we want to dig deep on as a team.

TC: For founders trying to understand your thinking, what’s interesting to you right now?

JG: We tend to focus on three major themes at any one time as a firm, and one we’ve termed ‘coaching networks.’ This is this intersection between AI and machine learning and human interaction. Companies like [the sales engagement platform] SalesLoft or [the knowledge management system] Guru or Drishti [which sells video analytics for manual factory assembly lines] fall into this category, where it’s really intelligent software going deep into a specific functional area and unleashing data in a way that’s never been available before.

The second [theme] is going deep into more specific industry verticals. Veeva was the best example of this early on with with healthcare and life sciences, but we now have one called p44 in the transportation space that’s doing incredibly well. Doximity is in the healthcare space and going deep like a LinkedIn for physicians, with some remote health capabilities, as well. And then [lending company] Blend, which is in the financial services area. These companies are taking cloud software and just going deep into the most important problems of their industries.

The third of them [centers around] remote work. Zoom, which has obviously has been [among our] best investments is almost as a platform, just like Salesforce became a platform after many years. We just funded a company called ClassEDU, which is a Zoom-specific offering for the education market. Snowflake is becoming a platform. So another opportunity is is not just trying to come up with another collaboration tool, but really going deep into a specific use case or vertical.

TC: What’s a company you’ve missed in recent years and were any lessons learned?

JG: We have our hall of shame. [Laughs.] I do think it’s dangerous to assume that things would have turned out the same if if we had been investors in the company. I believe the kinds of investors you put around the table make a difference in terms of the outcome of your company, so I try to not beat myself up too much on the missed opportunities because maybe they found a better fit or a better investor for them to be successful.

But Rob Bernshteyn of Coupa is one where I knew Rob from SuccessFactors [where he was a product marketing VP], and I just always respected and liked him. And we were always chasing it on valuation. And I think I think we probably turned it down at an $80 million or $100 million valuation [and it’s valued at] $20 billion today. That can keep you up at night.

Sometimes, in the moment, there are some risks and concerns about the business and there are other people who are willing to be more aggressive and so you lose out on some of those opportunities. The beautiful thing about our business is that it’s not a zero-sum game.

Powered by WPeMatico

AvePoint, a company that gives enterprises using Microsoft Office 365, SharePoint and Teams a control layer on top of these tools, announced today that it would be going public via a SPAC merger with Apex Technology Acquisition Corporation in a deal that values AvePoint at around $2 billion.

The acquisition brings together some powerful technology executives, with Apex run by former Oracle CFO Jeff Epstein and former Goldman Sachs head of technology investment banking Brad Koenig, who will now be working closely with AvePoint’s CEO Tianyi Jiang. Apex filed for a $305 million SPAC in September 2019.

Under the terms of the transaction, Apex’s balance of $352 million plus a $140 million additional private investment will be handed over to AvePoint. Once transaction fees and other considerations are paid for, AvePoint is expected to have $252 million on its balance sheet. Existing AvePoint shareholders will own approximately 72% of the combined entity, with the balance held by the Apex SPAC and the private investment owners.

Jiang sees this as a way to keep growing the company. “Going public now gives us the ability to meet this demand and scale up faster across product innovation, channel marketing, international markets and customer success initiatives,” he said in a statement.

AvePoint was founded in 2001 as a company to help ease the complexity of SharePoint installations, which at the time were all on-premise. Today, it has adapted to the shift to the cloud as a SaaS tool and primarily acts as a policy layer enabling companies to make sure employees are using these tools in a compliant way.

The company raised $200 million in January this year led by Sixth Street Partners (formerly TPG Sixth Street Partners), with additional participation from prior investor Goldman Sachs, meaning that Koenig was probably familiar with the company based on his previous role.

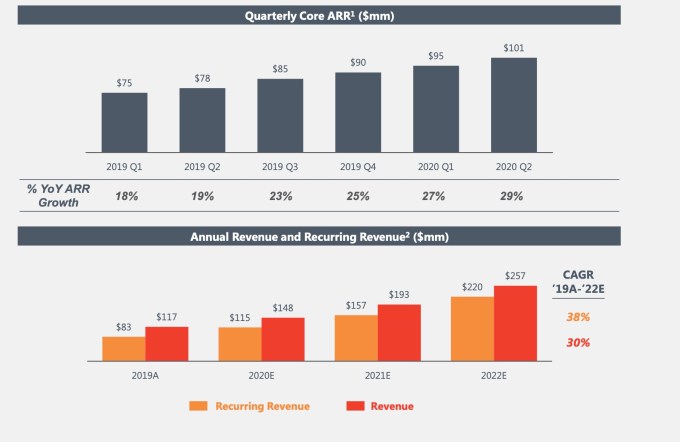

The company has raised a total of $294 million in capital before today’s announcement. It expects to generate almost $150 million in revenue by the end of this year, with ARR growing at over 30%. It’s worth noting that the company’s ARR and revenue has been growing steadily since Q12019. The company is projecting significant growth for the next two years with revenue estimates of $257 million and ARR of $220 million by the end of 2022.

Image Credits: AvePoint

The deal is expected to close in the first quarter of next year. Upon close the company will continue to be known as AvePoint and be publicly traded on Nasdaq under the new ticker symbol AVPT.

Powered by WPeMatico