exit

Auto Added by WPeMatico

Auto Added by WPeMatico

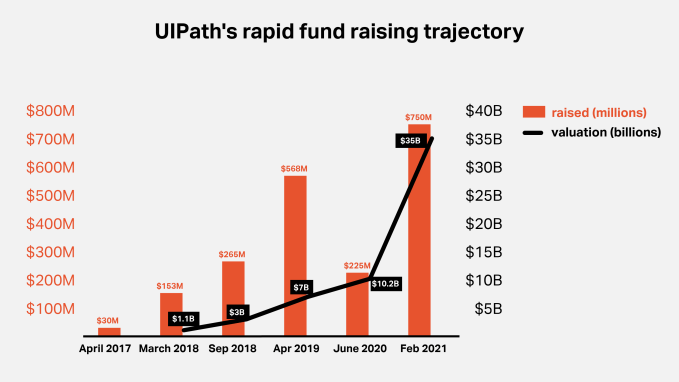

When TechCrunch covered UIPath’s Series A in 2017, it was a small startup out of Romania working in a little known area of enterprise software called robotic process automation (RPA).

Then the company took off with increasingly large multibillion dollar valuations. It progressed through its investment rounds, culminating with a $750 million round on an eye-popping $35 billion valuation last month.

This morning, the company took the next step on its rapid-fire evolutionary path when it filed its S-1 to go public. To illustrate just how fast the company’s rise has been, take a look at its funding history:

Image Credits: Bryce Durbin/TechCrunch

RPA is much better understood these days with larger enterprise software companies like SAP, Microsoft, IBM and ServiceNow getting involved. With RPA, companies can automate a mundane process like processing an insurance claim, moving work automatically, while bringing in humans only when absolutely necessary. For example, instead of having a person enter a number in a spreadsheet from an email, that can happen automatically.

In June 2019, Gartner reported that RPA was the fastest-growing area in enterprise software, growing at over 60% per year, and attracting investors and larger enterprise software vendors to the space. While RPA’s growth has slowed as it matures, a September 2020 Gartner report found it expanding at a more modest 19.5% with total revenue expected to reach $2 billion in 2021. Gartner found that stand-alone RPA vendors UIPath, Blue Prism and Automation Anywhere are the market leaders.

Although the market feels rather small given the size of the company’s valuation, it’s still a nascent space. In its S-1 filing this morning, the company painted a rosy picture, projecting a $60 billion addressable market. While TAM estimates tend to trend large, UIPath points out that the number encompasses far more than pure RPA into what they call “Intelligent Process Automation.” That could include not only RPA, but also process discovery, workflow, no-code development and other forms of automation.

Indeed, as we wrote earlier today on the soaring process automation market, the company is probably going to need to expand into these other areas to really grow, especially now that it’s competing with much bigger companies for enterprise automation dollars.

While UIPath is in the midst of its quiet period, it came up for air this week to announce that it had bought Cloud Elements, a company that gives it access to API integration, an important component of automation in the enterprise. Daniel Dines, the company co-founder and CEO said the acquisition was about building a larger platform of automation tools.

“The acquisition of Cloud Elements is just one example of how we are building a flexible and scalable enterprise-ready platform that helps customers become fully automated enterprises,” he said in a statement.

While there is a lot of CEO speak in that statement, there is also an element of truth in that the company is looking at the larger automation story. It can use some of the cash from its prodigious fundraising to begin expanding on its original vision with smaller acquisitions that can fill in missing pieces in the product road map.

The company will need to do that and more to compete in a rapidly moving market, where many vendors are fighting for different parts of the business. As it continues its journey to becoming a public company, it will need to continue finding new ways to increase revenue by tapping into different parts of the wider automation stack.

Powered by WPeMatico

The latest in a string of space tech SPACs announced this year is Redwire, an entity created by a PE firm in 2020, which has acquired a number of smaller companies including Adcole Space, Roccor, Made in Space, LoadPath, Oakman Aerospace, Deployable Space Systems and more — all within the last year or so. Redwire announced that it will go public through a merger with special purpose acquisition company Genesis Park Acquisition Corp., and the combined company will list on the NYSE.

The deal puts Redwire’s pro forma enterprise value at $615 million, and is expected to provide an additional $170 million to Redwire’s coffers post-merger, including a PIPE valued at over $100 million. Unsurprisingly, one of the uses of the proceeds that Redwire intends to pursue is continued M&A activity to build out its list of service offerings in the space domain.

Redwire’s mandate isn’t specifically to go after new space companies, and instead its targets share in common expertise in a particular, rather narrow slice of the severally crowded space market. It’s capabilities include on-orbit manufacturing and servicing; satellite design, manufacture and assembly; payload integration; sensor design and development; and more. The idea appears to be to build a full-stack infrastructure company that can offer tip-to-tail space technology services, exclusive really only of launch and ground station components (for now).

It’s a smart approach for a bourgeoning new space economy where increasingly, technology companies who want to operate in space would rather focus on their unique value proposition, and outsource the complex, but mostly settled business of actually getting to, and operating in, space. Other companies are addressing the market in similar ways, with launchers bringing more of that part of the process in-house so their payload customers basically only have to show up with the sensor or communication device they want to send to space, and the launcher providing everything else — including even the satellite, in the relatively near future.

Redwire has proven revenue-generating power, with projected 2021 revenue of $163 million, and many of the companies now operating under its umbrella are fairly mature and have been operating cash flow positive for many years. Accordingly, a SPAC as a path to public markets likely does make sense in this particular instance, but the increasing frequency and volume of space companies choosing this route, is, on the whole, a trend to watch with healthy skepticism.

Powered by WPeMatico

OneTrust, a late stage privacy platform startup, announced it was adding ethics and compliance to the mix this morning by acquiring Convercent, a company that was built to help build more ethical organizations. The companies did not share the purchase price.

OneTrust just raised $300 million on a fat $5.1 billion valuation at the end of last year, and it’s putting that money to work with this acquisition. Alan Dabbiere, co-chairman at OneTrust sees this acquisition as a way to add a missing component to his company’s growing platform of services.

“Integrating Convercent instantly brings a proven ethics and compliance technology, team, and customer base into the OneTrust, further aligning the Chief Ethics & Compliance Officer strategy alongside privacy, data governance, third-party risk, GRC (governance, risk and compliance), and ESG (environmental, social and governance) to build trust as a competitive advantage,” he said.

Convercent brings 750 customers and 150 employees to the OneTrust team along with its ethics system, which includes a way for employees to report ethical violations to the company and a tool for managing disclosures.

Convercent can also use data to help surface bad behavior before it’s been reported. As CEO Patrick Quinlan explained in a 2018 TechCrunch article:

“Sometimes you have this interactive code of conduct, where there’s a new vice president in a region and suddenly page views on the sexual harassment section of the Code of Conduct have increased 200% in the 90 days after he started. That’s easy, right? There’s a reason that’s happening, and our system will actually tell you what’s happening.”

Quinlan wrote in a company blog post announcing the deal that joining forces with OneTrust will give it the resources to expand its vision.

“As a part of OneTrust, we’ll be combining forces with the leader across privacy, security, data governance, third-party risk, GRC, ESG—and now—ethics and compliance. Our customers will now be able to build centralized programs across these workstreams to make trust a competitive differentiator,” Quinlan wrote.

Convercent was founded in 2012 and has raised over $100 million, according to Pitchbook data. OneTrust was founded in 2016. It has over 8000 customers and 150 employees and has raised $710 million, according to the company.

Powered by WPeMatico

ServiceNow became the latest company to take the robotic process automation (RPA) plunge when it announced it was acquiring Intellibot, an RPA startup based in Hyderabad, India. The companies did not reveal the purchase price.

The purchase comes at a time where companies are looking to automate workflows across the organization. RPA provides a way to automate a set of legacy processes, which often involve humans dealing with mundane repetitive work.

The announcement comes on the heels of the company’s no-code workflow announcements earlier this month and is part of the company’s broader workflow strategy, according to Josh Kahn, SVP of Creator Workflow Products at ServiceNow.

“RPA enhances ServiceNow’s current automation capabilities including low code tools, workflow, playbooks, integrations with over 150 out of the box connectors, machine learning, process mining and predictive analytics,” Kahn explained. He says that the company can now bring RPA natively to the platform with this acquisition, yet still use RPA bots from other vendors if that’s what the customer requires.

“ServiceNow customers can build workflows that incorporate bots from the pure play RPA vendors such as Automation Anywhere, UiPath and Blue Prism, and we will continue to partner with those companies. There will be many instances where customers want to use our native RPA capabilities alongside those from our partners as they build intelligent, end-to-end automation workflows on the Now Platform,” Kahn explained.

The company is making this purchase as other enterprise vendors enter the RPA market. SAP announced a new RPA tool at the end of December and acquired process automation startup Signavio in January. Meanwhile Microsoft announced a free RPA tool earlier this month, as the space is clearly getting the attention of these larger vendors.

ServiceNow has been on a buying spree over the last year or so buying five companies including Element AI, Loom Systems, Passage AI and Sweagle. Kahn says the acquisitions are all in the service of helping companies create automation across the organization.

“As we bring all of these technologies into the Now Platform, we will accelerate our ability to automate more and more sophisticated use cases. Things like better handling of unstructured data from documents such as written forms, emails and PDFs, and more resilient automations such as larger data sets and non-routine tasks,” Kahn said.

Intellibot was founded in 2015 and will provide the added bonus of giving ServiceNow a stronger foothold in India. The companies expect to close the deal no later than June.

Early Stage is the premier ‘how-to’ event for startup entrepreneurs and investors. You’ll hear first-hand how some of the most successful founders and VCs build their businesses, raise money and manage their portfolios. We’ll cover every aspect of company-building: Fundraising, recruiting, sales, product market fit, PR, marketing and brand building. Each session also has audience participation built-in – there’s ample time included for audience questions and discussion. Use code “TCARTICLE” at checkout to get 20 percent off tickets right here.

Powered by WPeMatico

Dropbox announced today that it plans to acquire DocSend for $165 million. The company helps customers share and track documents by sending a secure link instead of an attachment.

“We’re announcing that we’re acquiring DocSend to help us deliver an even broader set of tools for remote work, and DocSend helps customers securely manage and share their business-critical documents, backed by powerful engagement analytics,” Dropbox CEO Drew Houston told me.

When combined with the electronic signature capability of HelloSign, which Dropbox acquired in 2019, the acquisition gives the company an end-to-end document-sharing workflow it had been missing. “Dropbox, DocSend and HelloSign will be able to offer a full suite of self-serve products to help our millions of customers manage the entire critical document workflows and give more control over all aspects of that,” Houston explained.

Houston and DocSend co-founder and CEO Russ Heddleston have known each for other years, and have an established relationship. In fact, Heddleston worked for Dropbox as a summer in intern in 2010. He even ran the idea for the company by Houston prior to launching in 2013, who gave it his seal of approval, and the two companies have been partners for some time.

“We’ve just been following the thread of external sending, which has just kind of evolved and opened up into all these different workflows. And it’s just really interesting that by just being laser-focused on that we’ve been able to create a really differentiated product that users love a ton,” Heddleston said.

Those workflows include creative, sales, client services or startups using DocSend to deliver proposals or pitch decks and track engagement. In fact, among the earliest use cases for the company was helping startups track engagement with their pitch decks at VC firms.

The company raised a modest amount of the money along the way, just $15.3 million, according to Crunchbase, but Heddleston says that he wanted to build a company that was self-sufficient and raising more VC dollars was never a priority or necessity. “We had [VCs] chase us to give us more money all the time, and what we would tell our employees is that we don’t keep count based on money raised or headcount. It’s just about building a great company,” he said.

That builder’s attitude was one of the things that attracted Houston to the company. “We’re big believers in the model of product growth and capital efficiency, and building really intuitive products that are viral, and that’s a lot of what what attracted us to DocSend,” Houston said. While DocSend has 17,000 customers, Houston says the acquisition gives the company the opportunity to get in front of a much larger customer base as part of Dropbox.

It’s worth noting that Box offers a similar secure document-sharing capability enabling users to share a link instead of using an attachment. It recently bought e-signature startup SignRequest for $55 million with an eye toward building more complex document workflows similar to what Dropbox now has with HelloSign and DocSend. PandaDoc is another competitor in this space.

Both Dropbox and DocSend participated in the TechCrunch Disrupt Battlefield, with Houston debuting Dropbox in 2008 at the TechCrunch 50, the original name of the event. Meanwhile, DocSend participated in 2014 at TechCrunch Disrupt in New York City.

DocSend’s approximately 50 employees will be joining Dropbox when the deal closes, which should happen soon, subject to standard regulatory oversight.

Powered by WPeMatico

Coursera, an online education platform that has seen its business grow amid the coronavirus pandemic, is planning to file paperwork tomorrow for its initial public offering, sources familiar with the matter say. The company has been talking to underwriters since last year, but tomorrow could mark its first legal step in the process to IPO.

The Mountain View-based business, founded in 2012, was last valued at $2.4 billion in the private markets, during a Series F fundraising event in July 2020. Bloomberg pegs Coursera’s latest valuation at $5 billion.

The latest financing event brought its cash balance to $300 million, right around the money that Chegg had before it went public. Coursera CEO Jeff Maggioncalda did confirm then that the company is eyeing an eventual IPO.

Coursera has had a busy pandemic. Similar to Udemy, another massive open online course provider planning to go public, Coursera added an enterprise arm to its business. It launched Coursera for Campus to help colleges bring on online courses (credit optional) with built-in exams; more than 3,700 schools across the world are using the software. It is unclear how much money this operation has brought in, but we know that Udemy for Business is nearing $200 million in annual recurring revenue. In February, the company announced that it has received B Corp. certification, which means that it hits high standards for social and environmental performance. It also converted to a public benefit corporation.

GSV, a venture capital firm that exclusively backs edtech companies, had its largest position of its first fund in Coursera. GSV announced a $180 million Fund II yesterday.

It makes sense that edtech companies want to go public while the markets remain hot and remote education continues to be a central way that instruction is delivered. Other companies from the sector that have gone public in recent weeks include Nerdy and Skillsoft, two companies that used a SPAC to make their public debuts. Once – and if – Coursera does go public, it will join these newbies as well as the long-time edtech public companies including 2U, Chegg, and K12 Inc, and Zovio Solutions.

Coursera declined to comment.

Update: The previous version of this story stated that Skillshare has gone public. This is incorrect. Skillsoft has gone public. An update to reflect this change has been made.

Powered by WPeMatico

Real estate tech startup Doma, formerly known as States Title, announced Tuesday it will go public through a merger with SPAC Capitol Investment Corp. V in a deal valued at $3 billion, including debt.

SPACs, often called blank-check companies, are increasingly common. They exist as publicly traded entities in search of a private company to combine with, taking the private entity public without the hassle of an IPO.

When it floats later this year, Doma will trade on the New York Stock Exchange under the ticker symbol DOMA. The transaction is expected to provide up to $645 million in cash proceeds, including a fully committed PIPE of $300 million and up to $345 million of cash held in the trust account of Capitol Investment Corp. V.

CEO Max Simkoff founded San Francisco-based Doma in September 2016 with the aim of creating a technology-driven solution for “closing mortgages instantly.” While it initially was founded to instantly underwrite title insurance, the company has expanded that same approach to handle “every aspect” of closing and escrow.

Doma has developed patented machine learning technology that it says reduces title processing time from five days to “as little as one minute” and cuts down the entire mortgage closing process “from a 50+ day ordeal to less than a week.” The startup has facilitated over 800,000 real estate closings for lenders such as Chase, Homepoint, Sierra Pacific Mortgage and others.

The name change is designed to more accurately reflect its intention to expand “well beyond” title into areas such as appraisals and home warranties.

Its goal with going public is to be able to “continue to invest in growth, market expansion and new products.”

Anchoring the PIPE include funds and accounts managed by BlackRock, Fidelity Management & Research Company LLC, SB Management (a subsidiary of SoftBank Group), Gores, Hedosophia, and Wells Capital. Existing Doma shareholder Lennar has also committed to the PIPE and Spencer Rascoff, co-founder and former CEO of Zillow Group, has committed a personal investment to the PIPE.

Up to approximately $510 million of cash proceeds are expected to be retained by Doma, and existing Doma shareholders will own no less than approximately 80 percent of the equity of the new combined company, subject to redemptions by the public stockholders of Capitol and payment of transaction expenses.

In mid-February, Doma announced it had closed on $150 million in debt financing from HSCM Bermuda, which had previously invested in the company. And last May, it announced a massive $123 million Series C round of funding at a valuation of $623 million.

The company posted modest growth from 2019 to 2020, seeing its GAAP revenues rise from $358.1 million to $409.8 million. After removing premiums paid to agents, its revenues (“retained premiums and fees”) decreased to $179.8 million in 2019 and $189.7 million in 2020. (For this section we’re leaning on the reported 2020 numbers that are caveated with an “estimated” tag. As it is March, we expect the final 2020 numbers to come in close enough to what was reported as to make us comfortable citing them.)

In 2021 the company also anticipates modest growth, with GAAP revenues estimated at $416.4 million, and its retained revenue figure landing at $226.4 million. More expansive growth is anticipated and sketched out for 2022 and 2023, though as those figures are far in the future we can discount them for now.

Doma also expects its economics to worsen in 2021, with its adjusted gross profit as a percentage of its retained premiums and fees falling from 48.3% last year to 39.5% this year. Of course we’re so far off the GAAP ranch with that metric as to be lost, but it’s worth noting what the company is telling the street about its impending financial performance.

Other metrics are also pointed in a negative direction, with Doma expecting its adjusted EBITDA to fall from -$19.0 million to -$66.6 million in 2021. The company does predict a rosy 2023 adjusted EBITDA number, for whatever stock you want to put in that.

Without discounting costs, Doma’s 2020 net loss of $35.1 million is expected to expand to $103.1 million this year. Still, as with many entities pursuing a public debut via a SPAC, Doma is debuting while it is still sorting out elements of its business as the pandemic starts to diminish in light of increasingly readily available vaccines. It certainly has high hopes for its future.

Doma joins the growing number of proptech companies going the public route. On Monday, Compass, the real-estate brokerage startup backed by roughly $1.6 billion in venture funding, filed its S-1.

In 2020, Social Capital Hedosophia II, the blank-check company associated with investor Chamath Palihapitiya, announced that it would merge with Opendoor, taking the private real estate startup public in the process.

Porch.com also went public in a SPAC deal in December. And, SoftBank-backed View, a Silicon Valley-based smart window company, will complete a recent SPAC merger to be publicly listed on the NASDAQ stock exchange on March 9. The company is expected to debut trading with a market value of $1.6 billion.

Powered by WPeMatico

The Atlassian platform is chock full of data about how a company operates and communicates. Atlassian launched a machine learning layer, which relies on data on the platform with the addition of Atlassian Smarts last fall. Today the company announced it was acquiring Chartio to add a new data analysis and visualization component to the Atlassian family of products. The companies did not share a purchase price.

The company plans to incorporate Chartio technology across the platform, starting with Jira. Before being acquired, Chartio has generated its share of data, reporting that 280,000 users have created 10.5 million charts for 540,000 dashboards pulled from over 100,000 data sources.

Atlassian sees Chartio as way to bring that data visualization component to the platform and really take advantage of the data locked inside its products. “Atlassian products are home to a treasure trove of data, and our goal is to unleash the power of this data so our customers can go beyond out-of-the-box reports and truly customize analytics to meet the needs of their organization,” Zoe Ghani, head of product experience at platform at Atlassian wrote in a blog post announcing the deal.

Chartio co-founder and CEO Dave Fowler wrote in a blog post on his company website that the two companies started discussing a deal late last year, which culminated in today’s announcement. As is often the case in these deals, he is arguing that his company will be better off as part of large organization like Atlassian with its vast resources than it would have been by remaining stand-alone.

“While we’ve been proudly independent for years, the opportunity to team up our technology with Atlassian’s platform and massive reach was incredibly compelling. Their product-led go to market, customer focus and educational marketing have always been aspirational for us,” Fowler wrote.

As for Chartio customers unfortunately, according to a notice on the company website, the product is going to be going away next year, but customers will have plenty of time to export the data to another tool. The notice includes a link to instructions on how to do this.

Chartio was founded in 2010, and participated in the Y Combinator Summer 2010 cohort. It raised a modest $8.03 million along the way, according to Pitchbook data.

Powered by WPeMatico

This morning DigitalOcean, a provider of cloud computing services to SMBs, filed to go public. The company intends to list on the New York Stock Exchange (NYSE) under the ticker symbol “DOCN.”

DigitalOcean’s offering comes amidst a hot streak for tech IPOs, and valuations that are stretched by historical norms. The cloud hosting company was joined by Coinbase in filing its numbers publicly today.

DigitalOcean’s offering comes amidst a hot streak for tech IPOs.

However, unlike the cryptocurrency exchange, DigitalOcean intends to raise capital through its offering. Its S-1 filing lists a $100 million placeholder number, a figure that will update when the company announces an IPO price range target.

This morning let’s explore the company’s financials briefly, and then ask ourselves what its results can tell us about the cloud market as a whole.

TechCrunch has covered DigitalOcean with some frequency in recent years, including its early-2020 layoffs, its early-2020 $100 million debt raise and its $50 million investment from May of the same year that prior investors Access Industries and Andreessen Horowitz participated in.

From those pieces we knew that the company had reportedly reached $200 million in revenue during 2018, $250 million in 2019 and that DigitalOcean had expected to reach an annualized run rate of $300 million in 2020.

Those numbers held up well. Per its S-1 filing, DigitalOcean generated $203.1 million in 2018 revenue, $254.8 million in 2019 and $318.4 million in 2020. The company closed 2020 out with a self-calculated $357 million in annual run rate.

During its recent years of growth, DigitalOcean has managed to lose modestly increasing amounts of money, calculated using generally accepted accounting principles (GAAP), and non-GAAP profit (adjusted EBITDA) in rising quantities. Observe the rising disconnect:

Powered by WPeMatico

Kaleido, makers of a drag-and-drop background removal service for images and video, have been acquired by up-and-coming digital design platform Canva. While the price and terms are not disclosed, it is speculated that this young company may have fetched nearly nine figures.

It’s the right product at the right time, seemingly. In 2019, the Vienna-based Kaleido made remove.bg, a quick, simple, free and good-enough background removal tool for images. It became a hit among the many people who need to quickly do that kind of work but don’t want to fiddle around in Photoshop.

Then late last year they took the wraps off Unscreen, which did the same thing for video — a similar task conceptually, but far more demanding to actually engineer and deploy. The simplicity and effectiveness of the tool practically begged to be acquired and integrated into a larger framework by the likes of Adobe, but Canva seems to have beaten the others to the punch.

Image Credits: Unscreen

The acquisition was announced at the same time as another by Canva: product mockup generator Smartmockups, suggesting a major product expansion by the growing design company.

“We completely bootstrapped Kaleido with no investors involved from day one,” said co-founder and CEO of Kaleido, Benjamin Groessing, in a press release. “It has just been two founders and an incredible team. We’ve been profitable from the start — so this acquisition wasn’t essential for our existence. It just made sense on so many levels.”

The company declined to provide any further details on the acquisition beyond that the brand and name are expected to survive — at least Unscreen, which makes perfect sense as a product name even under another company.

German outlets Die Presse and Der Brutkasten cited sources putting the purchase “reiht sich dahinter ein” or in the same rank as the largest Austrian exits (the largest of which was Runtastic at €220 million), though still in the two-digit millions — which suggests a price approaching $100M.

Image Credits: Kaleido

Whatever the exact amount, it seems to have made the team very happy. And don’t worry — they put that image together using their own product for each person.

Powered by WPeMatico