exit

Auto Added by WPeMatico

Auto Added by WPeMatico

As companies expand worldwide and meet online in tools like Zoom, the language barrier can be a real impediment to getting work done. Zoom announced that it intends to acquire German startup Karlsruhe Information Technology Solutions or Kites for short, to bring real-time machine-learning-based translation to the platform.

The companies did not share the terms of the deal, but with Kites, the company gets a team of top researchers, who can help enhance the machine-learning translation knowledge at the company. “Kites’ talented team of 12 research scientists will help Zoom’s engineering team advance the field of [machine translation] to improve meeting productivity and efficiency by providing multilanguage translation capabilities for Zoom users,” the company said in a statement.

The deal appears to be an acqui-hire as the company adds those 12 researchers to the Zoom engineering group. It intends to leave the team in place in Germany with plans to build a machine-learning translation R&D center with additional hires over time as the company puts more resources into this area.

While the Kites website reveals little about it other than an address, the company’s About page on LinkedIn indicates that the startup was founded in 2015 by two researchers who taught at Carnegie Mellon and Karlsruhe Institute of Technology with the goal of building machine-learning translation tooling.

“The Kites mission is to break down language barriers and make seamless cross-language interaction a reality of everyday life,” the LinkedIn overview stated. It claims to be among a handful of companies, including Google and Microsoft, to have developed “leading speech recognition and translation technologies,” which would suggest that Zoom has acquired some key technologies.

It does not appear the company had a commercial product, but the site does indicate that there is a machine-learning translation platform that is in use in academia and government. Regardless, the fruits of the company’s research will now belong to Zoom.

Powered by WPeMatico

Last year, Seattle-based network security startup ExtraHop was riding high, quickly approaching $100 million in ARR and even making noises about a possible IPO in 2021. But there will be no IPO, at least for now, as the company announced this morning it has been acquired by a pair of private equity firms for $900 million.

The firms, Bain Capital Private Equity and Crosspoint Capital Partners, are buying a security solution that provides controls across a hybrid environment, something that could be useful as more companies find themselves in a position where they have some assets on-site and some in the cloud.

The company is part of the narrower Network Detection and Response (NDR) market. According to Jesse Rothstein, ExtraHop’s chief technology officer and co-founder, it’s a technology that is suited to today’s threat landscape, “I will say that ExtraHop’s north star has always really remained the same, and that has been around extracting intelligence from all of the network traffic in the wire data. This is where I think the network detection and response space is particularly well suited to protecting against advanced threats,” he told TechCrunch.

The company uses analytics and machine learning to figure out if there are threats and where they are coming from, regardless of how customers are deploying infrastructure. Rothstein said he envisions a world where environments have become more distributed with less defined perimeters and more porous networks.

“So the ability to have this high-quality detection and response capability utilizing next generation machine learning technology and behavioral analytics is so very important,” he said.

Max de Groen, managing director at Bain, says his company was attracted to the NDR space, and saw ExtraHop as a key player. “As we looked at the NDR market, ExtraHop, which [ … ] has spent 14 years building the product, really stood out as the best individual technology in the space,” de Groen told us.

Security remains a frothy market with lots of growth potential. We continue to see a mix of startups and established platform players jockeying for position, and private equity firms often try to establish a package of services. Last week, Symphony Technology Group bought FireEye’s product group for $1.2 billion, just a couple of months after snagging McAfee’s enterprise business for $4 billion as it tries to cobble together a comprehensive enterprise security solution.

Powered by WPeMatico

Paytm, India’s most valuable startup, confirmed to its shareholders and employees on Monday that it plans to file for an IPO.

In a letter to shareholders and employees, Paytm said that it plans to raise money by issuing fresh equity in the IPO, and also sell existing shareholders’ shares at the event. The startup has offered its employees the option to sell their stakes in the firm.

This is the first time the Noida-headquartered firm, which is valued at $16 billion and has raised over $3 billion to date, has commented on its plans about the IPO. The startup said in the letter that it has received an in-principle approval from the board of directors to pursue the public market.

Paytm, which is backed by Alibaba and SoftBank, hasn’t shared when it plans to file for the IPO, but has sought shareholders’ response to their intention to sell stakes by the end of the month.

Two sources familiar with the matter told TechCrunch that Paytm plans to raise about $3 billion and is targeting a valuation of up to $30 billion in the IPO. Paytm declined to comment.

Paytm’s letter — obtained by TechCrunch — to shareholders on Monday.

This isn’t the first time Paytm has planned to explore the public route. Exactly 10 years ago, long before Paytm established itself as the largest mobile wallet firm and expanded to several financial and commerce services, the startup had filed with the regulator with intentions to become public. The startup at the time cancelled the IPO plan and instead raised money from VCs to explore new avenues for growth.

A lot is riding on a successful IPO of Paytm — which reported a consolidated loss of $233.6 million for the financial year that ended in March this year, down from $404 million a year ago. (The startup’s revenue fell 10% during this period to $437.6 million.) India’s stock markets are yet to be fully tested for tech startups’ stocks in the country — though retail investors have shown good signs in recent years.

The startup, which competes with Google Pay and Flipkart-backed PhonePe, has realigned its payments strategy in recent years to assume a leadership position in the merchant payments market.

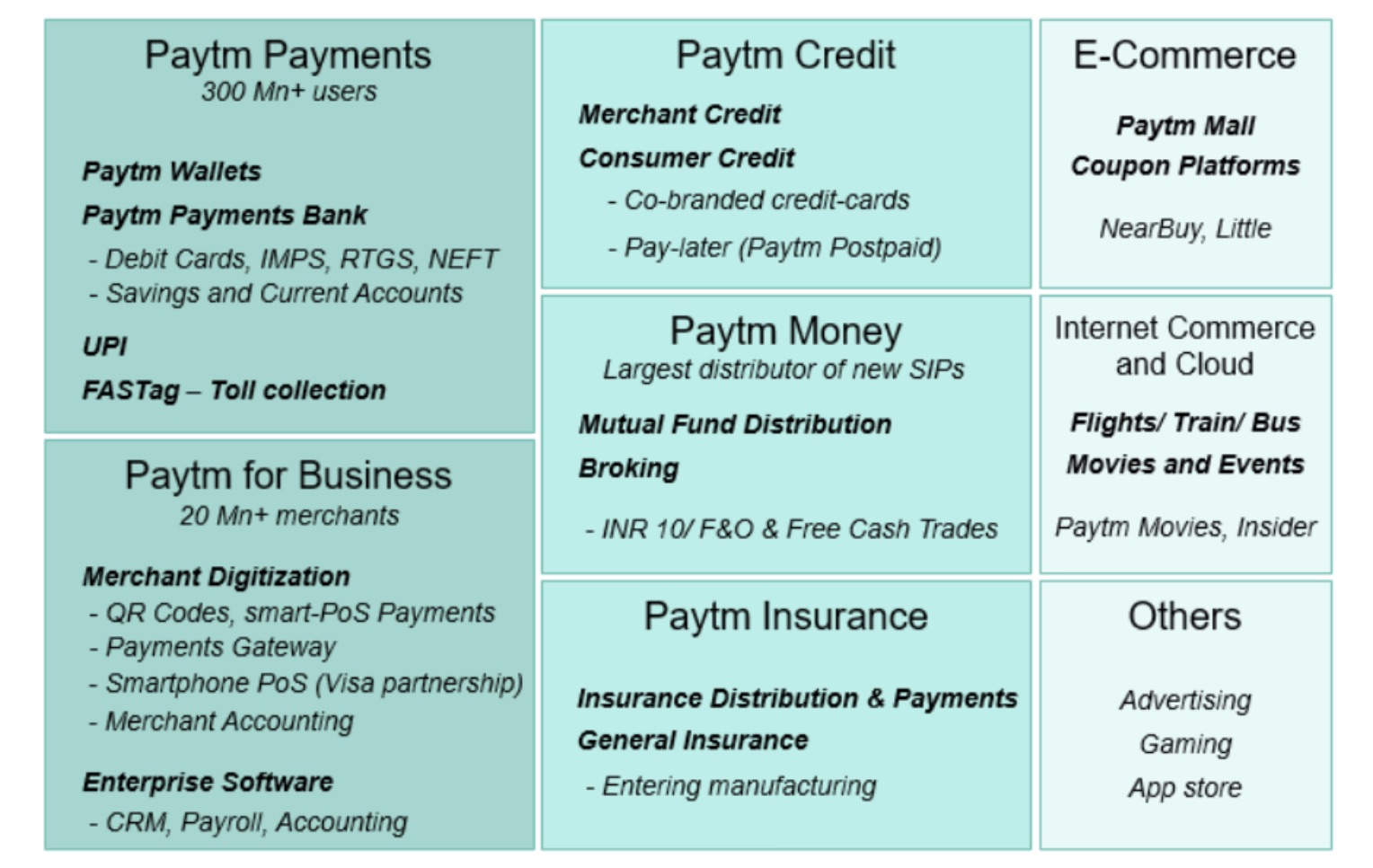

In a report to its clients late last month, analysts at Bernstein said the startup’s credit tech vertical is likely to lead the next wave of its revenue growth.

An overview of Paytm’s financial services ecosystem (Bernstein)

“With the advent of UPI, there has been a rising narrative that questioned Paytm’s market leadership,” the analysts wrote, referring to the exponential growth of payments stack developed by retail banks in India that has been adopted by several firms, including Google and PhonePe (as well as Paytm), and which has somewhat lowered the appeal of mobile wallets in India.

“However, under the hood, Paytm leads on merchant payments and has built an ecosystem of synergistic fintech verticals around its ‘super-app.’ The ecosystem spans payments (wallet/UPI), full-suite merchant acquiring, credit tech, digital bank, wealth, and insurance tech. We believe the super-app battle in India is not a ‘winner takes all’ but a game of execution, business building, and creating a superior customer experience with ecosystem integration,” Bernstein analysts added.

Paytm is the latest Indian giant startup that has expressed an interest in becoming public in recent months. Earlier this year, food delivery startup Zomato said it plans to raise $1.1 billion through an initial public offering. TechCrunch reported last month that Flipkart was in talks to raise over $1 billion in what is expected to be its financial fundraise ahead of an IPO.

Powered by WPeMatico

Snap yesterday announced the latest iteration of its Spectacles augmented reality glasses, and today the company revealed a bit more news: it is also acquiring the startup that supplied the technology that helps power them. The Snapchat parent is snapping up WaveOptics, an AR startup that makes the waveguides and projectors used in AR glasses. These overlay virtual images on top of the views of the real world someone wearing the glasses can see, and Snap worked with WaveOptics to build its latest version of Spectacles.

The deal was first reported by The Verge, and a spokesperson for Snap directly confirmed the details to TechCrunch. Snap is paying over $500 million for the startup, in a cash-and-stock deal. The first half of that will be coming in the form of stock when the deal officially closes, and the remainder will be payable in cash or stock in two years.

This is a big leap for WaveOptics, which had raised around $65 million in funding from investors that included Bosch, Octopus Ventures and a host of individuals, from Stan Boland (veteran entrepreneur in the UK, most recently at FiveAI) and Ambarish Mitra (the co-founder of early AR startup Blippar). PitchBook estimates that its most recent valuation was only around $105 million.

WaveOptics was founded in Oxford, and from what we know it will continue to be based in the UK.

We have been covering the company since its earliest days, when it displayed some very interesting, early, and ahead-of-its-time technology: waveguides based on hologram physics and photonic crystals. The important and key thing is that its tech drastically compresses size and load of the hardware needed to process and display images, meaning a much wider and more flexible range of form factors for AR hardware based on WaveOptics tech.

It’s not clear whether WaveOptics will continue to work with other parties post-deal, but it seems that one obvious advantage for Snap would be making the startup’s technology exclusive to itself.

Snap has been on something of an acquisition march in recent times — it’s made at least three other purchases of startups since January, including Fit Analytics for an AR-fuelled move into e-commerce, as well as Pixel8Earth and StreetCred for its mapping tools.

This deal, however, marks Snap’s biggest acquisition to date in terms of valuation. That is not only a mark of the premium price that foundational artificial intelligence tech continues to command — in addition to the team of scientists that built WaveOptics, it also has 12 filed and in-progress patents — but also Snap’s financial and, frankly, existential commitment to having a seat at the table when it comes not just to social apps that use AR, but hardware, and being at the centre of not just using the tech, but setting the pace and agenda for how and where that will play out.

That’s been a tenacious and not always rewarding place for it to be, but the company — which has long described itself as a “camera company” — has kept hardware in the mix as an essential component for its future strategy.

Powered by WPeMatico

Netlify, the startup that’s bringing a micro services approach to building websites, announced today that it has acquired YC alum FeaturePeek. The two companies did not share the purchase price.

With FeaturePeek, the company gets a major upgrade in its design review capability. While Netlify has had a previewing capability called Deploy Previews in the platform since 2016, it lacked a good way for reviewers to discuss and comment on the design. The preview alone was useful as far as it goes, but having the ability to collaborate on the design remained a missing piece until today.

With FeaturePeek, the company can expand on Deploy Previews to not only preview the design, but also enable all the stakeholders in the design process to add their opinions, edits and changes as the design moves through the creation process instead of having to wait until the end or gather the comments in a separate document or communications channel.

As FeaturePeek co-founder Eric Silverman told me at the time of their seed funding last year, his product removed a lot of frustration when the web coders would get all their review comments at the last minute:

“Right now, there’s no dedicated place to give feedback on that new work until it hits their staging environment, and so we’ll spin up ad hoc deployment previews, either on commit or on pull requests and those fully running environments can be shared with the team. On top of that, we have our overlay where you can file bugs, you can annotate screenshots, record video or leave comments.”

Matt Biilmann, CEO and co-founder, Netlify says that when his company created Deploy Previews, it was in reaction to customers who were kloodging together their own solutions to the issue. They learned that even with their own preview feature, customers craved a communications capability.

In the classic build versus buy debate, the company began building its own, then it met the FeaturePeek team and decided to switch course. “We had a team working on a prototype when the founders of FeaturePeek, Eric and Jason, gave us a demo of their product. As the demo progressed, our jaws got increasingly closer to hitting the floor and we knew straight away that what we had just seen was miles away from both our internal prototypes and any of the other tools we had seen in the space,” Billmann told TechCrunch.

He added, “It also quickly became apparent that fully building towards this vision as two different companies, without a deep end-to-end experience from initial Pull Request to a new feature release, would never really allow us to build what we were dreaming of, so we decided to join forces.”

The companies’ combined effort actually comes together today in a new release of Deploy Previews that includes the new FeaturePeek collaboration/commenting capabilities.

FeaturePeek was founded in 2019, went through Y Combinator Summer 2019 batch, and raised around $2 million. Netlify was founded in 2014 and has raised over $97 million, according to Crunchbase. Its last raise was a $53 million Series C in March 2020.

Powered by WPeMatico

Unbounce, a Vancouver startup best known for helping marketers create automated landing pages, added a new wrinkle this morning when it announced it has acquired Snazzy.ai, an early-stage automated copywriting startup. The two companies did not share the terms.

Unbounce Chief Strategy Officer Tamara Grominsky says that her company focuses on helping customers convert their customers into sales, and with Snazzy, it gets some pretty nifty technology based on GPT-3 artificial intelligence technology.

“We’re focused right now on building conversion intelligence software that will allow marketers to work with machines to really unlock their true conversion potential […] and we saw a huge opportunity with Snazzy to focus particularly on the content creation and copy creation space to help us accelerate that strategy,” Grominsky explained.

She points out that the product is really aimed at the marketing generalist charged with overseeing landing pages, and who is responsible for a range of tasks including writing copy. “The average Unbounce customer isn’t a specialized copywriter, so they don’t spend [their work] day writing copy. They’re what we would consider a marketing generalist or really someone who’s responsible for a wide range of marketing responsibilities,” she said.

Snazzy co-founder Chris Frantz says the tech is really about getting people started, and then they can tweak the results as needed. “The hardest part has always been to get that first line, that first page, the first couple of words in — and we eliminate that entirely. That might not always result in amazing copy, but on the plus side you can always click the button again and give it another try,” he said.

Frantz says that with so much competition in the space, he and his co-founder felt they could build a market much faster as part of a larger and broader marketing platform solution like Unbounce.

“I love Tamara’s vision for the future of Unbounce. I think she has a very ambitious vision. She sold me on that very early on in the process. At the same time, there was a lot of competition in the space, and to have a key differentiator with a company like Unbounce, which has a decade of marketing experience and a lot of trust within this community, I think it’s a very powerful wedge that we can use to further grow our audience,” Frantz said.

The tool lets you write a range of copy, from landing pages to Google ad copy. The company launched in alpha last October and already had 30,000 customers, which Grominsky says Unbounce hopes to convert into customers. The good news for those customers is that the company plans to leave Snazzy as a standalone product, while incorporating the tech into the platform in ways that make sense in the coming year.

Powered by WPeMatico

Bright Machines is going public via a SPAC-led combination, it announced this morning. The transaction will see the 3-year-old company merge with SCVX, raising gross cash proceeds of $435 million in the process.

After the transaction is consummated, the startup will sport an anticipated equity valuation of $1.6 billion.

The Bright Machines news indicates that the great SPAC chill was not a deep freeze. And the transaction itself, in conjunction with the previously announced Desktop Metal blank-check deal, implies that there is space in the market for hardware startup liquidity via SPACs. Perhaps that will unlock more late-stage capital for hardware-focused upstarts.

Today we’re first looking at what Bright Machines does, and then the financial details that it shared as part of its news.

Bright Machines is trying to solve a hard problem related to industrial automation by creating microfactories. This involves a complex mix of hardware, software and artificial intelligence. While robotics has been around in one form or another since the 1970s, for the most part, it has lacked real intelligence. Bright Machines wants to change that.

The company emerged in 2018 with a $179 million Series A, a hefty amount of cash for a young startup, but the company has a bold vision and such a vision takes extensive funding. What it’s trying to do is completely transform manufacturing using machine learning.

At the time of that funding, the company brought in former Autodesk co-CEO Amar Hanspal as CEO and former Autodesk founder and CEO Carl Bass to sit on the company board of directors. AutoDesk itself has been trying to transform design and manufacturing in recent years, so it was logical to bring these two experienced leaders into the fold.

The startup’s thesis is that instead of having what are essentially “unintelligent” robots, it wants to add computer vision and a heavy dose of sensors to bring a data-driven automation approach to the factory floor.

Powered by WPeMatico

Cisco has been busy on the acquisition front this week, and today the company announced it was buying threat assessment platform Kenna Security, the third company it has purchased this week. The two companies did not disclose the purchase price.

With Kenna, Cisco gets a startup that uses machine learning to sort through the massive pile of threat data that comes into a security system on a daily basis and prioritizes the threats most likely to do the most damage. That could be a very useful tool these days when threats abound and it’s not always easy to know where to put your limited security resources. Cisco plans to take that technology and integrate into its SecureX platform.

Gee Rittenhouse, senior vice president and general manager of Cisco’s Security Business Group, wrote in a blog post announcing the deal with Kenna that his company is getting a product that brings together Cisco’s existing threat management capabilities with Kenna’s risk-based vulnerability management skills.

“That is why we are pleased to announce our intent to acquire Kenna Security, Inc., a recognized leader in risk-based vulnerability prioritization with over 14 million assets protected and over 12.7 billion managed vulnerabilities. Using data science and real-world threat intelligence, it has a proven ability to bring data in from a multi-vendor environment and provide a comprehensive view of IT vulnerability risk,” Rittenhouse wrote in the blog post.

The security sphere has been complex for a long time, but with employees moving to work from home because of COVID, it became even more pronounced in the last year. In a world where the threat landscape changes quickly, having a tool that prioritizes what to look at first in its arsenal could be very useful.

Kenna Security CEO Karim Toubba gave a typical executive argument for being acquired: it gives him a much bigger market under Cisco than his company could have built alone.

“Now is our opportunity to change the industry: once the acquisition is complete, we will be one step closer to delivering Kenna’s pioneering Risk-Based Vulnerability Management (RBVM) platform to the more than 7,000 customers using Cisco SecureX today. This single action exponentially increases the impact Kenna’s technology will have on the way the world secures networks, endpoints and infrastructures,” he wrote in the company blog.

The company, which launched in 2010, claims to be the pioneer in the RBVM space. It raised over $98 million on a $320 million post-money valuation, according to PitchBook data. Customers include HSBC, Royal Bank of Canada, Mattel and Quest Diagnostics.

For those customers, the product will cease to be standalone at some point as the companies work together to integrate Kenna technology into the SecureX platform. When that is complete, the standalone customers will have to purchase the Cisco solution to continue using the Kenna tech.

Cisco has had a busy week on the acquisition front. It announced its intent to acquire Sedona Systems on Tuesday, Socio Labs on Wednesday and this announcement today. That’s a lot of activity for any company in a single week. The deal is expected to close in Cisco Q4 FY 2021. Kenna’s 170 employees will be joining the Security Business Group led by Rittenhouse.

Powered by WPeMatico

Cisco announced this morning that it intends to acquire Indianapolis-based startup Socio, which helps plan hybrid in-person and virtual events. The two companies did not share the purchase price.

Socio provides a missing hybrid event management component for the company to add to its Webex platform. The goal appears to be to combine this with the recent purchase of Slido and transform Webex from an application mostly for video meetings into a more comprehensive event platform.

“As part of Cisco Webex’s vision to deliver inclusive, engaging and intelligent meeting and event experiences, the acquisition of Socio Labs complements Cisco’s recent acquisition of Slido, an industry-leading audience engagement tool, which together will create a comprehensive, cost-effective and easy-to-use event management solution [ … ],” the company explained in a statement.

The impact of the pandemic was not lost on Cisco, and it’s clear that as we can foresee going back to live events, having the ability to combine it with a virtual experience means that you can open up your event to a much wider audience beyond those who can attend in person. That’s likely not something that’s going away, even after we get past COVID.

Jeetu Patel, SVP and GM for security and collaboration at Cisco says that the future of work is going to be hybrid, whether it’s for work meetings or larger events and Cisco is making this acquisition to expand the use cases for the Webex platform.

“Whether it’s a 1:1 call, a small team huddle, a group meeting or a large external event, we want to remove friction and help people engage with each other in an inclusive manner. Slido allows for every voice to be heard — even when you’re not talking. Socio allows for getting your voice heard by a large number of people,” Patel said.

And the company believes that Webex provides the platform to make it all happen. “It’s a really potent combination of technology to make human interactions more engaging, no matter the type of conversation,” he added.

Brent Leary, founder and principal analyst at CRM Essentials, says that it’s a smart move to take advantage of the changing events landscape and that this acquisition helps make Cisco a serious player in this space.

“As we get closer to a post-pandemic world, the need to create hybrid event experiences is going to quickly accelerate as people start venturing out to attend physical events. So having an event stack that combines local event support/participation with tools to integrate a broader virtual audience will be the future of event management,” Leary told me.

Socio was founded in 2016 and raised around $7 million in investment capital, according to Crunchbase data. It has a prestigious list of enterprise customers that includes Microsoft, Google, Jet Blue, Greenpeace, PepsiCo and Hyundai.

The deal is expected to close in Q4 of FY2021. When it does close, Socio’s 135 employees will be joining Cisco. The plan is to incorporate Socio’s tooling into the Webex platform while allowing it to continue as a stand-alone product, according to a Cisco spokesperson.

Powered by WPeMatico

Jamf, the enterprise Apple device management company, announced that it was acquiring Wandera, a zero trust security startup, for $400 million at the market close today. Today’s purchase is the largest in the company’s history.

Using a set of management services for Apple devices, Jamf provides IT at large organizations. It is the leader in the market, and snagging Wandera provides a missing modern security layer for the platform.

Jamf CEO Dean Hager says that Wandera’s zero trust approach fills in an important piece in the Jamf platform tool set. “The combination of Wandera and Jamf will provide our customers a single source platform that handles deployment, application lifecycle management, policies, filtering and security capabilities across all Apple devices while delivering zero trust network access for all mobile workers,” Hager said in a statement.

Zero trust, as the name implies, is an approach to security where you don’t trust anybody regardless of whether they are inside or outside your network. It requires that you force everyone to provide multiple forms of authentication to prove their identity before they can access company resources.

The need for a zero trust approach became even more acute during the pandemic when employees have often been working from home and have needed access to applications and other company resources from wherever they happened to be, a trend that was happening even prior to COVID, and is likely to continue after it ends.

Wandera, which is based in London, was founded in 2012 by brothers Roy and Eldar Tuvey, who had previously co-founded another security startup called ScanSafe. Cisco acquired that company, which helped protect web gateways as a service, for $183 million back in 2009. The brothers raised over $53 million along the way for Wandera. Investors included Bessemer Venture Partners, 83North and Sapphire Ventures.

Sapphire co-founder and managing director Andreas Weiskam had this to say about the company: “I’ve had the pleasure of working with co-founders (and brothers) Eldar Tuvey and Roy Tuvey for the last several years now and I can honestly say they’re great entrepreneurs and leaders, having built a real company of consequence.”

He added, “They’ve created a unique security product which addresses mobile threats by leveraging the increasingly important zero trust network. By joining the Jamf family, the two will help shape the future of the zero trust cloud. And it goes without saying that this is a big win for the customers, especially for those in the Apple ecosystem.”

Under the terms of the deal, Jamf is paying Wandera $350 million in cash, then paying them two $25 million payments on October 1, 2021 and December 15, 2021. The deal is expected to close in the third quarter, assuming it passes regulatory scrutiny.

Powered by WPeMatico