EC Newsletter

Auto Added by WPeMatico

Auto Added by WPeMatico

To close out the week, a short meditation on value, or, more precisely, how assets are valued in today’s markets.

Do you recall the pre-direct-listing hype Coinbase enjoyed? After reporting its estimated first-quarter financial performance, interest in the domestic cryptocurrency trading giant ran red-hot.

When Coinbase set a $250 per-share direct listing reference price, it was broadly viewed as modest, if not downright low. Of course, a reference price is just that — a reference — so it wasn’t too big a deal. But it also wasn’t surprising that Coinbase shares traded as high as $429.54 on their first day, according to Yahoo Finance data.

Coinbase equity hasn’t topped $400 in any following day and is now under the $300 mark, with more declines set to arrive as trading commences. Its reference price looms, and suddenly a price that felt intensely conservative before Coinbase began to trade is starting to look nearly reasonable.

The Exchange explores startups, markets and money.

Read it every morning on Extra Crunch or get The Exchange newsletter every Saturday.

There have been other notable declines in value among some recently public, more technologically differentiated companies. The Exchange has watched with something akin to polite confusion as the value of Root, a neoinsurance company, fell to a third of its public-market highs after going public, even though it beat growth expectations in its most recent quarterly report.

There have been other notable declines in value among some recently public, more technologically differentiated companies. The Exchange has watched with something akin to polite confusion as the value of Root, a neoinsurance company, fell to a third of its public-market highs after going public, even though it beat growth expectations in its most recent quarterly report.

We could toss UiPath into our trend of wildly meandering value. The company’s initial IPO price range targeted a price as low as $43 per share. Today it’s worth $76.75 per share in pre-market trading.

No one knows what anything is worth, again. This is the feeling I get while watching the markets work to determine how to value assets as diverse as startups crossing the private-public divide to the value of Bitcoin, which was supposed to keep going up. Until it suddenly reversed gear.

Frankly, we’re still dealing with new-enough models — or big-enough guesses about the future baked into business models — that it’s hard to really value the most uncertain (and therefore most exciting) companies, let alone cryptocurrencies. Let’s discuss.

Powered by WPeMatico

The global venture capital market had a cracking start to the year. Coming off a 2020 high, VC totals in the United States, in Europe, and among competitive verticals like insurtech and AI are on pace to set new records in 2021.

The rapid-fire deal-making and trend of larger venture checks at higher valuations that The Exchange has tracked for some time require private-market investors to make decisions faster than ever. For venture capitalists, the timeline for reaching conviction around a startup’s thesis and executing due diligence has become compressed.

Some venture capitalists are turning to data to move more quickly. Some are spending more time preparing to be vetted themselves. And some investors are simply doing the work beforehand.

The Exchange explores startups, markets and money.

Read it every morning on Extra Crunch or get The Exchange newsletter every Saturday.

We were tipped off to the concept of pre-diligence during the reporting process for a look into recent fundraising trends in the AI/ML space. Sapphire investor Jai Das, when asked about how he was handling a competitive and swiftly moving market for AI startup investments, said that “most firms are completing their due diligence way before the financing actually happens.”

How does that work in practice? Per Das, startups that raise quick Series A and B rounds are “tracked by [early-stage] investors as soon as they raise their seed financings. So there is no need to do any due diligence during the financing and hence most of these financings are pre-emptive.”

How does that work in practice? Per Das, startups that raise quick Series A and B rounds are “tracked by [early-stage] investors as soon as they raise their seed financings. So there is no need to do any due diligence during the financing and hence most of these financings are pre-emptive.”

Venture capital: Now more about sales than ever before!

This morning, The Exchange is digging into the question of how VCs are handling diligence in a world where the most attractive deals can open and close faster than ever, and old models of deep diligence and paced deal-making are outmoded.

One way that investors are betting on themselves in a bid to speed their diligence and decision-making is by investing in their own tech. That may sound obvious, given that venture capital dollars often land in the accounts of tech-focused companies, but in a business that was previously known for its relationship focus — more on that shortly — the trend is worth considering.

Powered by WPeMatico

The investment landscape for insurtech startups is off to a hot start in Q2 2021. Since the end of the first quarter, we’ve seen several players in the broad startup category announce new capital, including Clearcover, Alan, Next Insurance and The Zebra.

But, as anyone who’s familiar with startups that offer insurance-related products and services knows, the sector is enough of a mixed bag that one needs to segment down to get clarity on how constituent companies are performing. So while Clearcover’s $200 million round from last week, Next Insurance’s $250 million round from the first of the month and Alan’s $220 million round from yesterday are interesting, this morning we’re going to focus a bit more on The Zebra’s side of the insurtech house.

The Exchange explores startups, markets and money.

Read it every morning on Extra Crunch or get The Exchange newsletter every Saturday.

The Exchange divides insurtech startups into three categories: neoinsurance providers, insurtech marketplaces and insurtech enablers. (You can see why we need to segment the insurtech genre!)

Briefly, neoinsurance providers are companies like Root, Metromile and Next Insurance, which use technology to underwrite and sell insurance in an updated manner; these companies also often have optimized mobile experiences.

Marketplaces like The Zebra, Gabi, Insurify and others provide a way for consumers to better identify their insurance options. And, finally, there are companies like AgentSync, which fit neatly into our third category of firms that help other companies in the insurance business digitize their operations or otherwise modernize.

Insurtech marketplaces came back into our view when The Zebra put together a $150 million Series D earlier this month and released a host of metrics regarding its growth, and Insurify dropped the news that it is partnering with Toyota.

Insurtech marketplaces came back into our view when The Zebra put together a $150 million Series D earlier this month and released a host of metrics regarding its growth, and Insurify dropped the news that it is partnering with Toyota.

This morning, let’s discuss insurtech’s 2020 as a whole, peek at some preliminary 2021 venture data and then dive deep into what we’ve collected regarding growth among insurtech marketplace players. The Exchange has data and other details from The Zebra, Insurify, Wefox and more.

Covering longitudinal progress of specific startup categories is one of our favorite things to do. So, please, walk with us!

PitchBook data regarding the insurtech category in 2020 underscores how large the startup niche has grown. Per the data company, $18.3 billion was spent last year on insurtech startups across venture capital, private equity and M&A activity. That was a billion dollars under its 2019 result, but given the pandemic’s onset, 2020’s final result is somewhat impressive — who expected insurance investing to hold up during an unprecedented global catastrophe?

This year is proving lucrative for the insurtech market, at least from a venture capital perspective. Normally I’d make a joke about how unprofitable some neoinsurance providers are at this juncture, but because our focus is elsewhere, bringing up the fact that, say, Lemonade’s adjusted losses in the final quarter of 2020 were around 150% of its revenue is kind of irrelevant. So we won’t!

Powered by WPeMatico

A stunning first quarter in venture capital funding was not restricted to the United States; Europe also had one hell of a start to the year.

According to data from Dealroom and Crunchbase News, an investor, and an analyst from PitchBook, European startups put together an impressive fundraising haul. The venture capital world kicked off its 2021 European investing cycle with enough activity to set the continent on the path that would crush yearly records.

The Exchange explores startups, markets and money.

Read it every morning on Extra Crunch or get The Exchange newsletter every Saturday.

Inside the data, there’s lots to unpack, including which sectors of European startups stood out in terms of capital raised, rising seed and late-stage deals, and dollar volume. We’ll also need to discuss exits — the Deliveroo IPO and its various woes was not the only transaction from the period worth understanding.

As with our prior looks at AI startup fundraising and the United States’ own blistering start to the year, we’ll lean on multiple sources to ensure that we have a wide lens. And we’ll keep in mind that all venture capital data lags reality somewhat, as many deals from a particular period are not disclosed or discovered until long after they actually occurred.

As with our prior looks at AI startup fundraising and the United States’ own blistering start to the year, we’ll lean on multiple sources to ensure that we have a wide lens. And we’ll keep in mind that all venture capital data lags reality somewhat, as many deals from a particular period are not disclosed or discovered until long after they actually occurred.

In this case, it makes the numbers all the more impressive. Let’s get into the data.

Dealroom was first out of the gate, reporting that European startups had a record quarter in Q1 2021 back when April just got started. Its preliminary results for the first quarter indicated that startups on the continent raised €16.6 billion, or $19.9 billion at today’s exchange rates.

That total was not only a record, but what Dealroom described as double the results of Q1 2020. While we’ve become slightly inured in recent months to the venture capital market’s rapid pace and capital-rich environment, it’s worth considering for a moment, as the first quarter of last year ended, how few of us would have guessed that just a year later — as COVID-19 still harms public health and disrupts life and business — we’d see numbers like this.

The Dealroom data, however, was not all records. Round volume by the group’s estimates was down from the year-ago period, if slightly better than the last few quarters. The general move toward the later-stage and larger-round venture capital market is alive and well in Europe.

Powered by WPeMatico

Coinbase’s direct listing was a massive finance, startup and cryptocurrency event that impacted a host of public and private investors, early employees, and crypto-enthusiasts. Regardless of where one sits in the broader tech and venture world, Coinbase storming north of a $100 billion valuation during its first day of trading was the biggest startup happening of the year.

The transaction’s effects will be felt for some time in the public market, but also among the startups and capital that comprise the private market.

In the buildup to Coinbase’s flotation — and we’d argue especially after it released its blockbuster Q1 2021 results — there was a general expectation that the unicorn’s direct listing would provide a halo effect for other startups in the space. Anthemis’ Ruth Foxe Blader told The Exchange, for example, that “the Coinbase listing shows this great inflection point for crypto,” with another “wave” of startup work in the space coming up.

The widely held perspective raised two questions: Will the success of Coinbase’s direct listing bolster private investment in crypto-focused startups, and will that success help other areas of financially focused startup work garner more investor attention?

The Exchange explores startups, markets and money.

Read it every morning on Extra Crunch or get The Exchange newsletter every Saturday.

Presuming that Coinbase’s listing will positively impact its niche and others around it is not a stretch. But to make sure we weren’t misreading sentiment, and to get deeper into the why of the concept, The Exchange reached out to venture capitalists who invest in the broader fintech world to get their take. We even roped in an analyst or two to round out our panel.

The answer is not a simple yes. There are several ways to approach investing in the cryptocurrency space — from buying coins themselves, to investing in mainstream-ish institutions like legal exchanges, to the more exotic, like supporting efforts on the forefront of the decentralized blockchain world. And while it is somewhat clear that most folks expect more capital to be available for crypto projects, it’s not clear where it may end up inside the market.

We’ll wrap by considering what impact Coinbase’s direct listing will have, if any, on non-crypto fintech venture capital investing.

After yesterday’s examination of how blazingly hot the venture capital market looked in the first quarter, we’re again trying to gauge the private market’s temperature. Let’s talk to some folks on the ground and hear what they are seeing.

Coinbase’s direct listing floated a company that is worth more than all but two major blockchains, namely Ethereum and Bitcoin. Several other chains have aggregate coin values in the 11-figure range, but a 12-digit worth is still rare among crypto assets.

The scale of Coinbase’s valuation post-listing matters, according to Chainalysis Chief Economist Phillip Gradwell. Gradwell told The Exchange that “Coinbase’s $100 billion valuation today demonstrates that venture investors can make great returns from putting money into crypto companies, not just cryptocurrencies. That proof point is good for the entire ecosystem.”

More simply, it is now eminently reasonable to invest in the companies working in the crypto space instead of merely putting capital to work hard-buying coins themselves. The other way to consider the comment is to realize that Coinbase’s share price appreciation is steep enough since its 2012 founding to rival the returns of some coins over the same time frame.

Cleo Capital‘s Sarah Kunst expanded on the point, telling The Exchange in an email that “it’s now credible to say you’re a crypto startup and plan to IPO [versus] having acquisition or ICO be the only proven exit paths in the U.S.”

Powered by WPeMatico

It’s no surprise that the venture capital market was incredibly active in the United States during the first quarter of 2021, but precisely how strong has only recently become clear. This morning, we’re digging into the data.

According to a report from PitchBook, venture capitalists unleashed a wave of capital in the first three months of the year. So much, in fact, that funding in the United States nearly doubled compared to the same quarter of 2020.

We’ll dig into specific numbers and trends regarding aggregate venture capital results in a moment, but what stood out the most while digesting the Q1 dataset was how strong VC results appeared across different states; a solo late-stage boom the quarter was not.

Seed deal volume appeared strong and early-stage venture capital activity could reach new highs in 2021, but late-stage venture capital activity in the United States is already setting records in both deal count and invested dollars.

The Exchange explores startups, markets and money.

Read it every morning on Extra Crunch or get The Exchange newsletter every Saturday.

We’ll parse the headline numbers and then dive into seed and super late-stage data with the help of Sarah Kunst of Cleo Capital, Jenny Lefcourt of Freestyle Capital, Iris Choi of Floodgate and Laela Sturdy of CapitalG.

With their help, we’ll contextualize the numbers and weave anecdotal observations into what the charts and graphs tell us. Especially in the case of seed data, which is famously laggy, added context is crucial. Let’s go!

According to PitchBook’s report, some 3,987 venture capital rounds were closed in the United States during Q1 2021. Those deals were worth $69 billion, a figure up nearly 93% from 2020’s first-quarter results.

In broad strokes, the United States had a crushing venture capital start to the new year, pandemic be damned. That is especially true when we consider 2020’s full-year figures. Last year, venture capitalists deployed some $166 billion into U.S.-based startups across 12,546 rounds. In contrast, if the first quarter’s pace was maintained during the rest of 2021, the United States would see around 16,000 rounds worth around $280 billion.

Of course, we cannot see the future, so those projections are merely shared to underscore how active the first quarter proved to be; we’ll have to wait for at least another quarter’s data to confidently predict full-year records for 2021.

Powering the rapid start to the venture capital year was a holistic boom: Seed deal volume is forecasted to have set a multiyear high, perhaps matching the historically strong Q2 2018 period. Early-stage venture capital during Q1 2021 was also robust, with $14.5 billion deployed across 1,170 rounds. Both numbers set a pace for fresh records in 2021.

Then there was late-stage dealmaking, which soared in the first quarter. In 2020, late-stage venture capital deals were worth $111.4 billion raised from 3,504 rounds. In the first quarter of 2021, some $51.9 billion was invested into late-stage startups across 1,291 deals.

Valuations and round sizes continued to rise across the board. If there was a better time to raise a big whack of venture capital as a U.S.-based startup, we cannot recall it. And the data seems to scream that the good times are now as good, or gooder, than ever.

Powered by WPeMatico

Microsoft’s huge purchase of health tech AI company Nuance led the technology news cycle this week. The $19.7 billion transaction is Microsoft’s second-largest to date, only beaten by its purchase of LinkedIn some years ago.

For the AI space, the sale is a coup. Nuance was already a public company, but to see Microsoft offer a firm premium over its public-market value demonstrates the value that AI technology can have to wealthy companies. For startups working in the AI space, the Nuance deal is good news; the value of AI revenue was repriced by the acquisition’s announcement — and for the better.

In light of the megadeal, The Exchange dug into the AI venture capital market. What’s happening on the startup side of the coin in the artificial intelligence and machine learning (AI/ML) space?

The Exchange explores startups, markets and money. Read it every morning on Extra Crunch, or get The Exchange newsletter every Saturday.

To get a handle on the situation, we’ve compiled Q1 2021 and historical venture capital investment data via PitchBook, spoken to an active venture capitalist with a focus on AI-powered startups, and heard from a couple of startups recently featured on CB Insights’ list of leading AI upstarts for their take on the recent news.

The picture that emerges is one of strong investor interest and the expectation of even more in the wake of the Microsoft-Nuance tie-up. For AI startups, it’s a great time to be in the market.

This morning, we’ll start with a look into recent venture capital activity in the AI/ML market and its historical context. Then we’ll talk to Zetta Ventures’ Jocelyn Goldfein and a few companies in the AI space. Let’s go!

According to historical data compiled by PitchBook, venture capital investment into U.S.-based, AI-focused startups is enjoying a strong start to the year. Per the group’s provided dataset, from the start of 2021 through April 12, or the first 101 days of the year, 442 deals in the space were worth $11.65 billion.

In 2020, the same query for U.S.-based startups working in the AI and ML space — the line between ML and AI is blurrier than ever — turned up 1,601 rounds worth $27.49 billion.

Powered by WPeMatico

The first quarter of 2021 was a busy season for technology exits. Coming off a hot period in the final quarter of 2020, it was no surprise that tech upstarts pursued liquidity through a variety of mechanisms as the new year began.

There were IPOs, there were direct listings, there were PE deals. Hell, we even saw enough SPACs that we lost track of a few; amid all the noise, you’ll miss the occasional note no matter how well-tuned your ear.

The Exchange explores startups, markets and money. Read it every morning on Extra Crunch, or get The Exchange newsletter every Saturday.

Each path is still open for later-stage startups to pursue exits: The IPO market was welcoming until a few minutes ago and private equity firms are stacked with cash and willing to pay higher multiples than they might in more normal times. And there are sufficient SPACs to take the entire recent Y Combinator class public.

Choosing which option is best from a buffet’s worth of possibilities is an interesting task for startup CEOs and their boards.

DigitalOcean went public via a traditional IPO, raising a slug of capital in the process. The SMB-focused public cloud company likely felt like a somewhat obvious IPO candidate when you read its results. The Exchange spoke with the company’s CEO, Yancey Spruill, about the choice.

Latch, in contrast, decided that a SPAC was its best route out the gate. The Exchange caught up with the company’s CFO, Garth Mitchell, about the transaction and why it made sense for his company.

And, finally, The Exchange spoke with AlertMedia’s founder and CEO, Brian Cruver, about his decision to sell his Texas-based company to a private equity firm.

To prevent this post from reaching an astronomic word count, we’ll give a brief overview of each deal and then summarize the company’s views about why their liquidity choice was the right one.

Kicking off with DigitalOcean, a few notes: First, the company has been pretty darn public about its growth in the last few years. We knew that it had an annualized run rate of around $200 million in 2018, $250 million in 2019 and around $300 million in the first half of 2020. It later announced that it hit that mark in May of last year.

So when DigitalOcean decided to go public, we weren’t bowled over. The company wound up pricing at $47 per share, the high end of its range. Since then, its stock has struggled somewhat, falling below $37 per share before recovering to $43.80 at the end of trading yesterday.

Enough of all that. Why did the company choose to go public via a traditional IPO? Spruill said his company looked at SPAC deals and direct listings. It selected the IPO route because it fit the company’s goals of generating a broad base of shareholders while creating a branding opportunity.

The cost of an IPO is comparable, he added, to other exit options. Spruill also praised the IPO process itself, noting that its rigorous requirements made DigitalOcean a better company.

Earlier in our chat, I asked Spruill a question that I put to every CEO on IPO day: How are you feeling? It’s a bit of a sop, but it sometimes elicits insights from executives and founders who, after weeks of discussing their companies’ inner workings, are asked a rare personal question.

Spruill said he felt incredible and that nothing could replicate an IPO as the culmination of so much work put into building a company and its team. If you add up the wins and losses over time, with more of the former than the latter, and can cross the finish line with the right metrics and market, you can earn a spot to be “grilled” by the “best investors,” he said.

Those investors put $750 million or so into his company, Spruill added. Funds that it can use to retire debt and free up more cash flow. Not a bad day, I’d say.

Powered by WPeMatico

Substack didn’t invent the paid newsletter, but the startup’s early success with the model is enticing previous backers to more than double down on the media startup.

The Exchange explores startups, markets and money. Read it every morning on Extra Crunch, or get The Exchange newsletter every Saturday.

Last evening, Axios reported that Substack is “raising $65 million in new venture capital” at a valuation of “around $650 million.” As you’ve already guessed, Axios goes on to report that Andreessen Horowitz (a16z) will likely lead the investment.

That we’re seeing a16z pour more capital into what we could call the alt-media space is not a surprise. The investing group is ladling even more cash into its in-house media efforts and has put a small archipelago of capital into audio-based social media app Clubhouse. Its internal publishing schedule is in part an attempt to get around traditional media; the Clubhouse universe is an inverted one in which tech investors are celebrities, producers and gatekeepers. And Substack is a place where publications have bled some well-known talent, shifting the center of gravity in media.

You can detect the theme.

Regardless, Substack’s new valuation and investment are eye-catching. This morning, I want to collect all that we can regarding Substack’s historical growth so that we can chew on its new valuation from the best vantage point. Let’s go!

A little history to kick us off. Crunchbase counts Substack’s total funding to date at $17.4 million. PitchBook puts the number at $21.21 million, inclusive of debt. Both sources agree that the company’s most recent round came in July 2019. PitchBook pegs the company’s valuation at $48.65 million at that date.

Raising $17 million in cash around 20 months ago, regardless of debt, is an amount of capital that the company could easily have burned through by now. Raising more funds is therefore not a surprise.

But the size of the new round is notable, as is its constituent valuation. Series A and B rounds have been growing in size in recent years. But a $65 million Series B would stand out, even by 2021 standards. Not shockingly so, but enough that any company raising that sum at its implied level of maturity would demand our attention. That we’re all familiar with Substack only makes the sum more curious.

Powered by WPeMatico

What happens to hot fintech startups that have benefited from a rise in consumer trading activity if regular folks lose interest in financial wagers?

That’s the question facing Robinhood, Coinbase and other trading platforms that have ridden an upward cycle. Each has performed well in recent quarters: Robinhood by securing huge payment-for-order-flow revenues, while Coinbase’s trading fees have proven incredibly lucrative, something we learned when it filed to go public.

The Exchange explores startups, markets and money. Read it every morning on Extra Crunch, or get The Exchange newsletter every Saturday.

According to recent reporting, the consumer trading frenzy could be slowing: Bloomberg recently noted that options trading volume is slipping, Robinhood’s app store ranking is falling, and some alternative assets are also losing steam. Other reporting from the publication notes that many SPAC shares are underwater while Google trends data indicates falling consumer trading interest, perhaps limiting the inflow of new users for equities-focused apps.

There are other indications that the red-hot speculative consumer market is cooling. Bitcoin is off around 10% in the last week after a blistering rise in recent quarters. Hot stocks like Peloton, once a darling of traders, fell more than 10% yesterday alone.

But looking past price declines and other signals of market chop, volume itself at some well-known exchanges could be falling.

There’s a historical precedent for such declines. Coinbase’s historical revenues, to pick an example, have proved variable based on consumer interest in cryptocurrencies, with the company benefiting from rising demand and trading activity and seeing its top line decline in periods of restrained enthusiasm.

Robinhood and its fellow free trading apps have yet to undergo a similar rise-and-fall in trading volume, I’d reckon. At least of the sort of extreme up-and-down that Coinbase endured after the 2017-2018 bitcoin boom. Our question is, what would happen to Robinhood and its cohorts if the apparent cooling in consumer trading demand continues? Let’s talk about it.

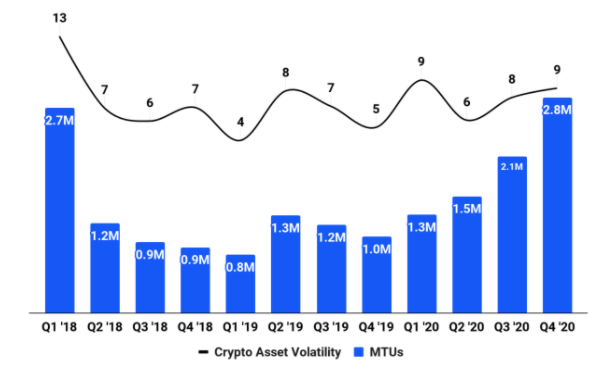

Coinbase was a famously lucrative organization during the 2017-2018 bitcoin boom.

Indeed, we can see from the following chart from its S-1 filing that the company’s monthly transacting users (MTUs) dropped sharply into 2018. The percentage decline from 2.7 million to 800,000 is just over 70%.

Image Credits: Coinbase

And in case you think we’re being rude, we have a related chart from the same SEC filing that shows trading volume falling over the same period, not merely MTUs. We’re not picking a loose proxy to merely infer that trading revenue dipped at Coinbase. We can show it:

Powered by WPeMatico