EC Newsletter

Auto Added by WPeMatico

Auto Added by WPeMatico

It’s Squarespace direct-listing day, and the SMB web hosting and design shop’s reference price has been set at $50 per share.

According to quick math from the IPO-watching group Renaissance Capital, Squarespace is worth $7.4 billion at that price, calculated using a fully diluted share count. The company’s new valuation is sharply under where Squarespace raised capital in March, when it added $300 million to its accounts at a $10 billion post-money valuation, according to Crunchbase data.

The Exchange explores startups, markets and money.

Read it every morning on Extra Crunch or get The Exchange newsletter every Saturday.

The company’s reference price, however, is just that: a reference. It doesn’t mean that much. As we’ve seen from other notable direct listings, a company’s opening price does not necessarily align with its formal reference price. Until Squarespace opens, whether it will be valued at a discount to its final private price is unclear.

While the benefits of a direct listing are understood, the post-listing performance for well-known direct listings is less obvious. Indeed, Coinbase is currently under its reference price after starting its life as a public company at a far-richer figure, and Spotify’s share price is middling at best compared to its 2018-era direct-listing reference price.

While the benefits of a direct listing are understood, the post-listing performance for well-known direct listings is less obvious. Indeed, Coinbase is currently under its reference price after starting its life as a public company at a far-richer figure, and Spotify’s share price is middling at best compared to its 2018-era direct-listing reference price.

This morning, we’re going over Squarespace’s recently disclosed Q2 and full-2021 guidance. Then we’ll ask how its expectations compare to its reference price-defined pre-trading valuation. Finally, we’ll set some stakes in the ground regarding historical direct-listing results and what we might expect from the company as it adds a third set of data to our quiver.

This will be lots of fun, so let’s get into the numbers!

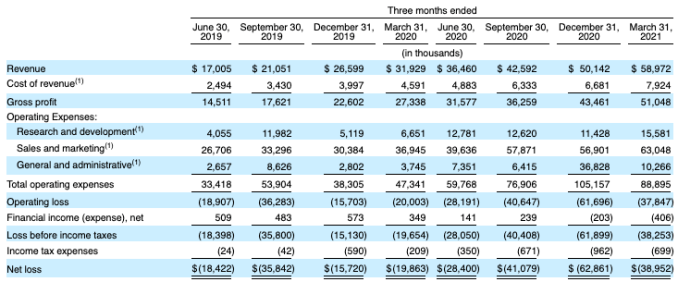

Per Squarespace’s own reporting, it expects revenues between $186 million and $189 million in Q2 2021, which it calculates as a growth rate of between 24% and 26%. That pace of growth at its scale is perfectly acceptable for a company going public.

For all of 2021, Squarespace expects revenues of $764 million to $776 million, which works out to a very similar 23% to 25% growth rate.

In profit terms, Squarespace only shared its “non-GAAP unlevered free cash flow,” which is a technical thing I have no time to explain. But what matters is that the company expects some non-GAAP unlevered free cash flow in Q2 2021 ($10 million to $13 million), and lots more in all of 2021 ($100 million to $115 million).

Powered by WPeMatico

Hot off the heels of our look into Marqeta’s IPO filing and dives into SPACs for Bright Machines and Bird, we’re parsing the WalkMe IPO filing. Later this week, Squarespace will direct list and we’ll see IPOs from Oatly and Procore. It’s a super busy time for public debuts of all sorts.

Given how hectic the IPO market is, we’re going to skip our usual throat clearing and dig into WalkMe’s IPO document. As always, we’ll start with a brief overview of its product and then move into discussing its financial performance.

Image Credits: Alex Wilhelm

WalkMe is the second Israel-based technology company to file to go public this week: No-code startup Monday.com is also pursuing an American IPO.

Alright! Into the breach.

WalkMe’s software provides visual overlays on websites that help users navigate the product in question. I base that explanation on my time at Crunchbase, which was a customer during at least part of my time there. WalkMe is popular with marketing teams who want to introduce users to a new or refreshed experience.

Per the company’s F-1 filing, other elements of its service that matter include its onboarding system and what WalkMe calls Workstation, or its “single interface to the applications within an enterprise and simplifies task completion through a natural language conversational interface and automation.” We’re including that last feature because it says “automation,” which, in the wake of the UiPath IPO, is a word worth watching. Investors are.

At a high level, WalkMe is a SaaS business, which means that when we digest its results we are digging into a modern software company. Let’s do just that.

From 2019 to 2020, WalkMe grew its revenues from $105.1 million to $148.3 million, a gain of 41%. In its most recent quarter, the company’s growth rate slowed: From Q1 2020 to Q1 2021, WalkMe’s top line grew 25% from $34.2 million to $42.7 million.

In SaaS terms, WalkMe calculates that its annual recurring revenue, or ARR, grew from $131.2 million at the end of 2019 to $164.3 million in 2020. In more granular terms, the company’s ARR grew from $137.8 million to $177.5 million in the first quarters of 2020, and 2021, respectively.

Powered by WPeMatico

At long last, the Monday.com crew dropped an F-1 filing to go public in the United States. TechCrunch has long known that the company, which sells corporate productivity and communications software, has scaled north of $100 million in annual recurring revenue (ARR).

The countdown to its IPO filing — an F-1, because the company is based in Israel, rather than the S-1s filed by domestic companies — has been ticking for several quarters, so seeing Monday.com drop the document on this Monday morning was just good fun.

The Exchange explores startups, markets and money.

Read it every morning on Extra Crunch or get The Exchange newsletter every Saturday.

The Exchange has been riffling through the document since it came out, and we’ve picked up on a few things to explore. We’ll start by looking at the company’s revenue growth on a historical basis to see if it has accelerated in recent quarters thanks to the pandemic. Then, we’ll turn to profitability, cash burn, share-based compensation expenses and product vision.

We’ll wrap at the end with a summary of what we’ve learned and also make sure to check out the company’s marketing spend, because I’m sure you’ve seen its digital ads.

We’ll wrap at the end with a summary of what we’ve learned and also make sure to check out the company’s marketing spend, because I’m sure you’ve seen its digital ads.

It’s a lot to chew through, so no more dilly-dallying. Into the numbers!

As always, we’re starting with revenue growth because it’s still the single most important thing about any venture-backed company.

This is great news for the startup, its employees and its investors. From 2019 to 2020, Monday.com grew its revenues from $78.1 million to $161.1 million, or 106%.

From Q1 2020 to Q1 2021, the company’s revenues grew from $31.9 million to $59 million. That’s about 85% growth. So, by what measure do we mean that the company’s revenue growth is accelerating? Its sequential-quarter revenue growth is picking up. Observe the following:

Image Credits: Monday.com F-1 filing

From Q2 2019 to Q3 2019, the company added around $4 million in revenue. From Q2 2020 to Q3 2020, that number was $6.1 million. More recently, the company’s revenue added $7.6 million from Q3 2020 to Q4 2020, which accelerated to $8.8 million from the final quarter of 2020 to the first quarter of 2021. Of course, from an ever-larger base, the company’s growth rate may decline. But the super clean and obvious expanding sequential revenue gains at the company are solid.

The fact that it added so much top line in recent quarters also helps explain why Monday.com is going public now. Sure, the markets are still near record highs and the pandemic is fading, but just look at that consistent growth! It’s investor catnip.

Powered by WPeMatico

As far as I can tell, low-code and no-code services are rapidly proving that prior models for products as broad as enterprise app creation and AI-powered data analytics were lackluster. My evidence? A mix of public- and private-market low- and no-code companies are putting up impressive results.

The Exchange caught up with Appian CEO Matt Calkins after his enterprise app software company reported its first-quarter performance to discuss the low-code market and what he’s hearing in customer meetings. To round out our general thesis — and shore up our somewhat bratty headline — we’ve compiled a list of recent low-code and no-code venture capital rounds, of which there are many.

As we’ll show, the pace at which venture capitalists are putting funds into companies that fall into our two categories is pretty damn rapid, which implies that they are doing well as a cohort. We can infer as much because it has become clear in recent quarters that while today’s private capital market is stupendous for some startups, it’s harder than you’d think for others.

The Exchange explores startups, markets and money.

Read it every morning on Extra Crunch or get The Exchange newsletter every Saturday.

The dividing factor? Signs of impressive present-day traction: Startups that are growing very fast have nearly unlimited access to capital, while those that are growing at merely fast rates are often finding it difficult to find a dance partner.

So if we can show that a huge, diverse set of no-code and low-code startups are raising oodles of capital, we can infer something relatively sturdy about market demand for their products. (It also doesn’t hurt that no-code automation service Zapier is growing like a weed and has reached IPO scale. In other news, Appian just dropped a new version of its low-code automation platform, for whatever that is worth.)

First Appian’s CEO, then a venture capital roundup. This should be fun.

Briefly, Appian reported $88.9 million in Q1 2021 revenue, of which $39.1 million came from its cloud subscription business. The latter figure rose 38% in the quarter compared to the year-ago period. Appian also swung to adjusted EBITDA profit in the period. Investors responded by hammering the company’s stock in the wake of the results. From an April share-price range in the mid-$130s, Appian is now trading in the mid-$80s, though only some of those declines came post-earnings.

But the company’s stock price is only so important. Precisely how conservative any one public company’s guidance is for the current year and how those forecasts play with investor expectations during a period of generally excessive valuations is not our game. What does matter is what the company’s CEO had to say about the low-code space itself.

Powered by WPeMatico

As expected, Bill.com is buying Divvy, the Utah-based corporate spend management startup that competes with Brex, Ramp and Airbase. The total purchase price of around $2.5 billion is substantially above the company’s roughly $1.6 billion post-money valuation that Divvy set during its $165 million, January 2021 funding round.

Divvy’s growth rate tells us that the company did not sell due to performance weakness.

Per Bill.com, the transaction includes $625 million in cash, with the rest of the consideration coming in the form of stock in Divvy’s new parent company.

Bill.com also reported its quarterly results today: Its Q1 included revenues of $59.7 million, above expectations of $54.63 million. The company’s adjusted loss per share of $0.02 also exceeded expectations, with the street expecting a sharper $0.07 per share deficit.

The better-than-anticipated results and the acquisition news combined to boost the value of Bill.com by more than 13% in after-hours trading.

Luckily for us, Bill.com released a deck that provides a number of financial metrics relating to its purchase of Divvy. This will not only allow us to better understand the value of the unicorn at exit, but also its competitors, against which we now have a set of metrics to bring to bear. So, this afternoon, let’s unpack the deal to gain a better understanding of the huge exit and the value of Divvy’s richly funded competitors.

The following numbers come from the Bill.com deck on the deal, which you can read here. Here are the core figures we care about:

This lets us price the company somewhat. Divvy sold for around 25x its current revenue rate. That’s a software-level multiple, implying that the company has either incredibly strong gross margins, or Bill.com had to pay a multiples-premium to buy the company’s future growth today. I suspect the latter more than the former, but we’ll have to scout for more data when Divvy shows up in Bill.com results after the deal closes; that data is a few quarters away.

Powered by WPeMatico

People have been discussing the importance of expanding opportunities for women in venture capital and startup entrepreneurship for decades. And for some time it appeared that progress was being made in building a more diverse and equitable environment.

The prospect of more women writing checks was viewed as a positive for female founders, a cohort that has struggled to attract more than a fraction of the funds that their male peers manage. All-female teams have an especially tough time raising capital compared to all-male teams, underscoring the disparity.

Then COVID-19 arrived and scrambled the venture and startup scene, creating a risk-off environment during the end of Q1 and the start of Q2 2020. Following that, the venture world went into overdrive as software sales became a safe harbor in the business world during uncertain economic times. And when it became clear that the vaunted digital transformation of businesses large and small was accelerating, more capital appeared.

But data indicate that the torrent of new capital has not been distributed equally — indeed, some of the progress that female founders made in recent years may have eroded.

The Exchange explores startups, markets and money.

Read it every morning on Extra Crunch or get The Exchange newsletter every Saturday.

During a time of plenty, many female founders are still going without. The Exchange reached out to a number of American and European investors and founders to get their perspective on how today’s venture market treats female founders.

Recurring among the responses was a general view that more women venture capitalists would help lessen the gender gap in investments, and that VCs became more conservative due to COVID-19 and its constituent economic disruption, reverting to offering capital to repeat founders and their existing networks, both groups that are less diverse than the pool of new founders.

Our collection of founders and investors also said that women have been especially double-tasked during the pandemic to take on more domestic responsibilities in part due to sexist societal expectations, adding that that sexism more generally remains a problem that either isn’t improving or is improving too slowly.

But before we get into the core issues that prevent improvements in gender equity in venture funding, let’s check in on the data from last year and contrast it to its antecedents.

While there have already been reports on gender disparities in funding, Nokia-backed VC firm NGP Capital made a great contribution to research on the topic with its 2021 dossier.

Powered by WPeMatico

The public markets give, and the public markets take away. Earlier this morning, enterprise cloud storage and productivity company Box got into a more public spat with some of its shareholders upset with its performance and management decisions. But while Box endures the more difficult chapters of being a public company, other companies are racing to join the ranks of the listed concerns of the world.

If it feels like IPO news slowed for a few weeks at the start of the second quarter, your gut is correct. Investors previously told The Exchange that the first, third and fourth quarters of 2021 would be hot periods for public debuts, but that Q2 would be slower. Their argument revolved around reporting cadences and how long it takes for certain periods of accounting work to be completed.

The Exchange explores startups, markets and money. Read it every morning on Extra Crunch or get The Exchange newsletter every Saturday.

So we weren’t surprised when the second quarter’s IPO cycle began to feel a bit soft compared to the rapid-fire first quarter. And, as we’ve all heard in recent days, the great SPAC rush is slowing.

But that hasn’t stopped a number of firms from defying expectations and going public all the same. Online hosting and website builder Squarespace has not only filed but filled in its public filing with notes on its anticipated direct listing. We have to talk about its choice to list directly in light of new financial information we have concerning its recent performance.

But there’s more: Expensify filed to go public yesterday, albeit privately. And the SmartRent SPAC combination, though now slightly dated, is also worth a moment of our time.

But there’s more: Expensify filed to go public yesterday, albeit privately. And the SmartRent SPAC combination, though now slightly dated, is also worth a moment of our time.

The final element in the current IPO landscape is the recent Darktrace IPO in the United Kingdom, which, after that market had a rough start to its tech IPO calendar, is now seeing better results. So, let’s discuss IPOs to fully understand where we stand today in the realm of unicorn liquidity.

When The Exchange first dug into Squarespace’s IPO filing, we did our best to parse its full-year results because we lacked its quarterly details. This leaves us with two things to chew on: Why is Squarespace pursuing a direct listing over another listing technique, and what can its current and more granular operating results tell us about the choice?

On the first count, if Squarespace is direct listing, we can presume that it doesn’t need more cash to operate. So, how much cash does the company have on hand? A good chunk of change: $183.3 million.

Powered by WPeMatico

It’s a big morning for fintech startups today: Flywire, a Boston-based magnet for venture capital, has filed to go public.

Flywire is a global payments company that attracted more than $300 million as a startup, according to Crunchbase, most recently raising a $60 million Series F last month. We don’t have its most recent valuation, but PitchBook data indicates that the company’s February 2020, $120 million round valued Flywire at $1 billion on a post-money basis.

So what we’re looking at here is a fintech unicorn IPO. A great way to kick off the week, to be honest, though I’d thought that Robinhood would be the next such debut.

Fintech venture capital activity has been hot lately, which makes the Flywire IPO interesting. Its success or failure could dictate the pace of fintech exits and fintech startup valuations in general, so we have to care about it.

The Exchange explores startups, markets and money. Read it every morning on Extra Crunch or get The Exchange newsletter every Saturday.

Regardless, we’re doing our regular work this morning. First, what does Flywire do and with whom does it compete? Then, a closer look at its financial results as we hope to get our hands around its revenue quality, aggregate economics and growth prospects.

After that, we’ll discuss valuations and which venture capital groups are set to do well in its flotation. The company had a number of backers, but Spark Capital, Temasek, F-Prime Capital and Bain Capital Ventures made the major shareholder list, along with Goldman Sachs. So, a number of firms and funds are hoping for a big Flywire exit. Let’s dig in.

Flywire is a global payments company. Or, as it states in its S-1 filing, it’s “a leading global payments enablement and software company.” And it thinks that its market, and by extension itself, has lots of room to grow. While “substantial strides [have been] made in payments technology in the retail and e-commerce industries,” the company wrote, “massive sectors of our global economy—including education, healthcare, travel, and business-to-business, or B2B, payments—are still in the early stages of digital transformation.”

That’s the same logic behind Stripe’s epic valuation and the rising value of payments-focused companies like Finix.

Powered by WPeMatico

In the never-ending stream of venture capital funding rounds, from time to time, a group of startups working on the same problem will raise money nearly in unison. So it was with OKR-focused startups toward the start of 2020.

How were so many OKR-focused tech upstarts able to raise capital at the same time? And was there really space in the market for so many different startups building software to help other companies manage their goal-setting? OKRs, or “objectives and key results,” a corporate planning method, are no longer a niche concept. But surely, over time, there would be M&A in the group, right?

During our first look into the cohort, we concluded that it felt likely that there was “some consolidation” ahead for the group “when growth becomes more difficult.” At the time, however, it was clear that many founders and investors expected the OKR software market to have material depth.

They were right, and we were wrong. A year later, in early 2021, we asked the same group how their previous year had gone. Nearly every single company had a killer year, with many players growing by well over 100%.

The Exchange explores startups, markets and money. Read it every morning on Extra Crunch or get The Exchange newsletter every Saturday.

OKR company Ally.io grew 3.3x in 2020, for example, while its competitor Gtmhub grew by 3x over the same time period. More capital followed. Ally.io raised $50 million in a Series C in the first quarter, while Gtmhub put together a $30 million Series B during the same period.

They won’t be the final startups in the OKR cohort to raise this year. We know this because we reached out to the group again this week, this time probing their Q1 performance, and, critically, asking the startups to discuss their level of optimism regarding the rest of 2021.

As before, the group’s recent results are strong, at least when compared to their own planning. But notably, the collection of competing companies is more optimistic than before about the rest of the year than they were before Q1 2021. Things are heating up for the OKR startup world.

A takeaway from our work today is that our prior notes about how impressively deep the software market is proving to be may have been too modest. And frankly, that’s super-good news for startups and investors alike. So much for SaaS-fatigue.

In a sense, we should not be surprised that OKR startups are doing well or that the startup software market is so large. You’d imagine that the historic pace of venture capital investment that we’ve seen so far in 2021 in Europe and the United States was based on results, or evidence that there was lots more room for software-focused startups to grow.

Interestingly, while these companies look similar to outsiders, they are each betting on strategies and differentiators that could help them win in their selected portion of the OKR space. Which also means that the sector may not be as crowded as it seems.

Don’t take our word for it. Let’s hear from Gtmhub COO Seth Elliott, Workboard CEO and co-founder Deidre Paknad, Koan CEO and co-founder Matt Tucker, Ally.io CEO and co-founder Vetri Vellore, and Perdoo CEO and founder Henrik-Jan van der Pol about just what the software market looks like to them.

We’ll start with how the startups performed in Q1 2021, dig into how they feel about the rest of the year, and then talk about how differentiation among the cohort could be helping them not step on each other’s toes.

WorkBoard is having a strong start to 2021. Paknad’s company, which raised in both March of 2019 and January of 2020, told The Exchange that it hired 82 people in the first three months of 2021, and that it plans on doing it again in the current quarter. WorkBoard is “investing heavily,” Paknad said via DM, and “made [its] Q1 targets.”

Powered by WPeMatico

Origin stories are satisfying because we already know the hero will overcome the odds — and in doing so, they’ll reveal their core strengths.

This week, we published a four-part series about how Klaviyo co-founders Andrew Bialecki and Ed Hallen bootstrapped their startup into an e-commerce marketing automation platform now valued at $4.15 billion.

Neither founder was bitten by a radioactive spider or received a serum that enhanced their entrepreneurial skills; instead, they focused on outreach to prospective customers to find out what they were willing to pay for and largely ignored the competition.

“Bootstrapping Klaviyo, it came out of this: ‘Hey, if we are super disciplined about finding a problem that someone will pay us to solve, we have a real company,’” said Hallen.

Full Extra Crunch articles are only available to members.

Use discount code ECFriday to save 20% off a one- or two-year subscription.

Even though millions of us respond every day to the personalized, automated emails sent through its platform, Klaviyo still isn’t a well-known brand. Our ongoing series of EC-1s offers entrepreneurs real insight into growing and scaling successful companies, but they’re also extremely useful for consumers who want to understand how the internet really works.

Thanks very much for reading Extra Crunch; I hope you have a great weekend.

Walter Thompson

Senior Editor, TechCrunch

@yourprotagonist

Image Credits: Nigel Sussman

Image Credits: slowcentury (opens in a new window) / Getty Images

Several micromobility companies once operated in my city, but consolidation has reduced that to a small handful.

Now that many consumers are buying their own e-bikes and e-scooters, shared dockless micromobility “just hasn’t proven itself to be a profitable line of business,” Puneeth Meruva, an associate at Trucks Venture Capital, told TechCrunch.

There’s only one dockless electric moped provider in my town, so price is no longer a consideration. Instead, my first priority is to find a vehicle with the best-charged battery. (San Francisco has a lot of hills, and you never know where the day might take you.)

Larger players like Lime and Bird have vertically integrated tech stacks for fleet management features like this, but there are also opportunities for startups — imagine a “phantom scooter” that drives itself to a neighborhood with high demand or a moped that alerts drivers if there’s traffic ahead.

This in-depth industry analysis shows how increased regulation on the local level and changing consumer habits are pushing micromobility providers to adapt and innovate.

“Whether you want to stack regulatory compliance on the vehicles, do safety features like ADAS or add mapping content, you kind of need this platform where you can actively develop and launch new apps on the vehicle without having to bring it back to the factory,” Meruva said.

Image Credits: TechCrunch/Bryce Durbin

If the definition of insanity is doing the same thing over and over and expecting a different outcome, then one might say the cybersecurity industry is insane.

Criminals continue to innovate with highly sophisticated attack methods, but many security organizations still use the same technological approaches they did 10 years ago. The world has changed, but cybersecurity hasn’t kept pace.

Image Credits: ra2studio (opens in a new window) / Getty Images

By 2025, 463 exabytes of data will be created each day, according to some estimates. It’s now easier than ever to translate physical and digital actions into data, and businesses of all types have raced to amass as much data as possible in order to gain a competitive edge.

However, in our collective infatuation with data (and obtaining more of it), what’s often overlooked is the role that storytelling plays in extracting real value from data.

The reality is that data by itself is insufficient to really influence human behavior. Whether the goal is to improve a business’ bottom line or convince people to stay home amid a pandemic, it’s the narrative that compels action, not the numbers alone.

As more data is collected and analyzed, communication and storytelling will become even more integral in the data science discipline because of their role in separating the signal from the noise.

Image Credits: Raquel Segato/EyeEm (opens in a new window) / Getty Images

We all need to be taking precautionary measures, not just in light of COVID, but to ensure our firms can continue to thrive when faced with unexpected tragedy.

So ask yourself this question: “What would happen if I or my partner(s) checked into the hospital tomorrow and had no phone and/or was too sick to call anyone, and that went on for two or three weeks (or longer)?”

If the answer is “I’m really not sure,” then you don’t have a business continuity plan.

Image Credits: rubberball (opens in a new window) / Getty Images

After years of sustained growth, the pandemic supercharged the outdoor recreation industry. Startups that provide services like camper vans, private campsites and trail-finding apps became relevant to millions of new users when COVID-19 shut down indoor recreation, building on an existing boom in outdoor recreation.

Startups like Outdoorsy, AllTrails, Cabana, Hipcamp, Kibbo and Lowergear Outdoors have seen significant growth, but to keep it going, consumers who discovered a fondness for the great outdoors during the pandemic must turn it into a lifelong interest.

Image Credits: MaboHH / Getty Images

Dell last week agreed to spin out VMware in exchange for a huge one-time dividend, a five-year commercial partnership agreement, lots of stock for existing Dell shareholders and Michael Dell retaining his role as chairman of its board.

So, where does the deal leave VMware in terms of independence and in terms of Dell influence?

Image Credits: Westend61 (opens in a new window) / Getty Images

Many emerging and mature organizations survive or die based on their ability to scale. Scale quicker. Scale cheaper. Scale right.

Typically the IT team bears that burden — on top of countless other demands. IT teams move mountains for their organizations while scaling the tech platform as fast as possible, putting out the latest infrastructure fire and responding to countless day-to-day requests.

The most helpful gift any chief information officer or chief technology officer can give their IT teams is more time. Many people think that means adding another team member. But it could be as simple as introducing a low-code integration platform.

Image Credits: Nigel Sussman (opens in a new window)

A stunning first quarter in venture capital funding was not restricted to the United States; Europe also had one hell of a start to the year.

The venture capital world kicked off its 2021 European investing cycle with enough activity to set the continent on the path that would crush yearly records.

Inside the data, there’s lots to unpack, including which sectors of European startups stood out in terms of capital raised, rising seed and late-stage deals, and dollar volume. We’ll also need to discuss exits — the Deliveroo IPO and its various woes was not the only transaction from the period worth understanding.

We’ll keep in mind that all venture capital data lags reality somewhat, as many deals from a particular period are not disclosed or discovered until long after they actually occurred.

In this case, it makes the numbers all the more impressive.

Image Credits: Zastrozhnov (opens in a new window) / Getty Images

Robotic process automation unicorn UiPath went public this week, concentrating our focus on its value.

UiPath raised its last private round when the markets were most interested in public offerings and is now going public in a slightly altered climate.

In numerical terms, UiPath raised its IPO range from $43 to $50 per share to $52 to $54 per share. That’s a 21% jump in the value of the lower end of its range and an 8% gain to the value of the upper end of its per-share IPO price interval.

UiPath is also selling more shares than before, which should make its total valuation slightly larger at the top end than a mere 8% gain. So let’s go through the math one more time.

Image Credits: Nigel Sussman (opens in a new window)

The investment landscape for insurtech startups is off to a hot start in Q2 2021. Since the end of the first quarter, we’ve seen several players in the broad startup category announce new capital.

But, as anyone who’s familiar with startups that offer insurance-related products and services knows, the sector is enough of a mixed bag that one needs to segment down to get clarity on how constituent companies are performing.

Let’s discuss insurtech’s 2020 as a whole, peek at some preliminary 2021 venture data and then dive deep into what we’ve collected regarding growth among insurtech marketplace players.

Covering longitudinal progress of specific startup categories is one of our favorite things to do. So, please, walk with us!

Image Credits: Kehan Chen / Getty Images

Research papers come out far too frequently for anyone to read them all. That’s especially true in the field of machine learning, which now affects (and produces papers in) practically every industry and company.

This column aims to collect some of the most relevant recent discoveries and papers — particularly in, but not limited to, artificial intelligence — and explain why they matter.

This week, we dove into “introspective failure prediction,” using ML to identify dangerous moles, and spotting cows from space.

Image Credits: Gearstd (opens in a new window) / Getty Images

With strict privacy laws such as GDPR and CCPA already listing big-ticket penalties — and a growing number of countries following suit — businesses have little option but to comply.

It’s not just bigger, established businesses offering privacy and compliance tech; brand-new startups are filling in the gaps in this emerging and growing space.

Privacy isn’t dead, as many would have you believe. New regulations, stricter cross-border data transfer rules and increasing calls for data sovereignty have helped the privacy startup space grow thanks to an uptick in investor support.

This is how we got here, and where investors are spending.

Image Credits: Nigel Sussman (opens in a new window)

UiPath is not worth $36 billion, as we might have expected, but at a figure below $30 billion.

At $29.1 billion, UiPath has a roughly 35x run-rate multiple. That just about ties it for eighth-best overall. Among all public cloud companies. That means that UiPath is insanely valuable, just not that insanely valuable.

So what went wrong with the company’s final private round? The Exchange’s hunch is that UiPath’s final private investors expected the market to stay as hot as it once was, but it has cooled since the first two months of the year. So, instead of UiPath coming to the market in the expected climate, the company instead had to price where it did because the weather predicted by its final private price had already chilled.

Those investors gambled, in other words, hoping that a last-minute, pre-IPO round could snag them a rapid return on a company going public in a hot market. That didn’t work out.

And how bad is that? Not very! UiPath’s IPO is more a meeting of private-market exuberance and modestly more conservative public markets. It’s nothing to cry about.

Image Credits: d3sign (opens in a new window) / Getty Images

The second half of 2021 will bring incredible growth, the likes of which we haven’t seen in a long time.

Here’s how marketing in tech will shift — and what you need to know to reach more customers and accelerate growth this year.

First and foremost, differentiation is going to be imperative. It’s already hard enough to stand out and get noticed, and it’s about to get much more difficult as new companies emerge and investments and budgets balloon in the latter half of the year.

Additionally, tech companies need to be mindful not to ignore the most important part of the ecosystem: people. Technology will only take you so far, and it’s not going to be enough to survive the competition.

Tactically, the most successful tech companies will embrace video and experimentation in their marketing — two components that will catapult them ahead of the competition.

Ignoring these predictions, backed by empirical evidence, will be detrimental and devastating. Fasten your seatbelts: 2021 is going to be a turbocharged year of growth opportunities for marketing in tech.

Image Credits: Bryce Durbin/TechCrunch

Dear Sophie,

I’m a female entrepreneur who created my first startup a few months ago.

Once my startup gets off the ground — and as COVID-19 gets under control — I’d like to visit the United States to test the market and meet with investors. Which visas would allow me to do that?

—Noteworthy in Nairobi

Despite a somewhat circuitous route, UiPath closed its first day as a public company worth more than it was in its Series F round — when it sold 12,043,202 shares at $62.27576 apiece, per SEC filings. More simply, UiPath closed on Wednesday worth more per-share than it was in February.

How you might value the company, whether you prefer a simple or fully diluted share count, is somewhat immaterial at this juncture. UiPath had a good day.

TechCrunch spoke with UiPath CFO Ashim Gupta, curious about the company’s choice of a traditional IPO, its general avoidance of adjusted metrics in its SEC filings and the IPO market’s current temperature.

Image Credits: Nigel Sussman (opens in a new window)

The global venture capital market had a cracking start to the year. Coming off a 2020 high, VC totals in the United States, in Europe, and among competitive verticals like insurtech and AI are on pace to set new records in 2021.

The rapid-fire deal-making and trend of larger venture checks at higher valuations that The Exchange has tracked for some time require private-market investors to make decisions faster than ever. For venture capitalists, the timeline for reaching conviction around a startup’s thesis and executing due diligence has become compressed.

Some venture capitalists are turning to data to move more quickly. Some are spending more time preparing to be vetted themselves. And some investors are simply doing the work beforehand.

We were tipped off to the concept of pre-diligence during the reporting process for a look into recent fundraising trends in the AI/ML space. Sapphire investor Jai Das, when asked about how he was handling a competitive and swiftly moving market for AI startup investments, said that “most firms are completing their due diligence way before the financing actually happens.”

How does that work in practice?

Image Credits: MartinvBarraud (opens in a new window) / Getty Images

Your clients might not demand 24/7 customer service yet, but they’re certainly hoping for it.

But how can a startup with a lean staff provide round-the-clock customer care? There are several options available, but more than ever, outsourcing is one of them.

When should your startup consider outsourcing its customer care? And what should you look for in a provider?

Here are some insights on what customer care as a service (CCaaS) can do for you, and how fast-growing startups have been leveraging this new class of partners to boost customer satisfaction.

Image Credits: Erik Isakson / Getty Images

Productivity infrastructure is on the rise and will continue to be front and center as companies evaluate what their future of work entails and how to maintain productivity, rapid software development and innovation with distributed teams.

Understanding the benefits, use cases and steps to consider can propel organizations into the next phase of digital transformation.

Image Credits: Klaus Vedfelt (opens in a new window) / Getty Images

The clock begins ticking on a startup the day the doors open. Regardless of a young company’s struggles or success, sooner or later the question of when, how or whether to sell the enterprise presents itself. It’s possibly the biggest question an entrepreneur will face.

For founders who self-funded (bootstrapped) their startup, a boardroom full of additional factors comes into play. Some are the same as for investor-funded firms, but many are unique.

After 18 years of bootstrapping a BI software firm into a business that now serves 28,000 companies and 3 million users in 75 countries, here’s what I’ve learned about myself, my company, about entrepreneurship and about when to grab for that brass ring.

Put happiness at the center of the decision, and let your intuition — the instincts that made you the person you are today — be your guide.

Powered by WPeMatico