EC Newsletter

Auto Added by WPeMatico

Auto Added by WPeMatico

Demo days at startup accelerators are a pretty big deal around here.

These events aren’t just a chance to review the latest cohort of hopeful entrepreneurs — they also showcase the technology, products and services that will compete for VC and consumer attention over the next few years.

You never know where a hit will come from, which is why these events capture our attention. Here’s just one example from Y Combinator’s Summer 2013 Demo Day:

Positioning itself as the “FedEx of today,” it hopes to provide a logistics framework that goes beyond food and can be used for any type of on-demand order.

That startup was DoorDash, by the way.

Full Extra Crunch articles are only available to members

Use discount code ECFriday to save 20% off a one- or two-year subscription

Full disclosure: In 2016, I was 500 Startups’ Journalist-in-residence. I covered one demo day in person, spending most of my time backstage where founder teams practiced their pitches.

It was quite a scene: Several people literally jumped up and down to shake off their nervous energy, but I also recall one who calmly recited their lines while gazing through a window.

Yesterday, Jon Shieber and Alex Wilhelm covered 500 Startups’ 27th virtual demo day and selected eight companies as their favorites:

Thank you very much for reading Extra Crunch this week! I hope you have a safe, relaxing weekend.

Walter Thompson

Senior Editor, TechCrunch

@yourprotagonist

Image Credits: David Malan (opens in a new window) / Getty Images

Image Credits: Nigel Sussman (opens in a new window)

I’ve never used “stonkathon” in a headline before, but it’s been that kind of week.

The war between hedge funds and day traders over GameStop vaulted discount trader Robinhood into the headlines for days.

But how did it affect the company’s financial health?

This morning, Alex Wilhelm examined why Robinhood’s investors were willing to inject $3.4 billion more into the company in just one week.

“More trades means more PFOF (payment for order flow) revenue,” says Alex. “And Robinhood effectively doubled in size.”

Image Credits: Andrew_Rybalko / Getty Images

Reporter Natasha Mascarenhas interviewed Greg Brown, new president of digital learning platform Udemy, after his company announced that it surpassed $100 million ARR.

A new arm of the company, Udemy for Business, just secured a 100,000-employee contract with Cisco Systems to offer software, business and technology courses.

“The opportunity that the company sees has really forced us to reallocate resources and strategy,” said Brown.

Image Credits: Nigel Sussman (opens in a new window)

After scaling its ARR to $425 million and reaching a valuation of $28 billion, data analytics company Databricks is clearly IPO-ready.

Battery Ventures has backed Databricks since 2017, so Alex Wilhelm interviewed General Partner Dharmesh Thakker to understand why he thinks the company may be undervalued.

“Whether it’s digital transformation, whether it’s analytics, data is everywhere,” said Thakker. “So the TAM is massive.”

Image Credits: MirageC (opens in a new window) / Getty Images

Deep tech founders face special challenges when pitching investors: they usually don’t have a product, customers or revenue.

It’s difficult enough to ask a stranger for a check when there’s a beta product, but how do you drum up interest in an unproven idea that may exist largely in your imagination?

“Early-stage investors are in the business of funding dreams,” says angel investor Jessica Li.

“Investors are less interested in the intricacies of your technology and more interested in what impact it can create.”

Step one: use storytelling to highlight your big vision.

Image Credits: Images by Tang Ming Tung (opens in a new window) / Getty Images

Investors funded edtech startups with $10 billion last year as the pandemic forced widespread adoption of remote learning.

The valuations of these companies aren’t rising at the same rate as SaaS or fintech startups, but “where edtech lacks in impressive valuations, investors see it gaining in exit opportunities,” writes Natasha Mascarenhas.

For this edtech investor survey, she interviewed:

Image Credits: MF3d (opens in a new window) / Getty Images

In his latest recap of recent breakthroughs in applied science, Devin Coldewey looked at how researchers are using AI to:

Image Credits: Getty Images

In the latest of a series of articles that examines user experiences for consumer apps, UX expert Peter Ramsey and TechCrunch reporter Steve O’Hear studied Spotify Group Session, the shared-queue feature that permits users to create playlists collaboratively.

“Many of these lessons can be applied to other existing digital products or ones you are currently building,” such as the need to add context for important decisions and how to best use “react and explain” prompts.

Extra Crunch Live returned this week with two guests: Lightspeed Venture Partners’ Gaurav Gupta and Raj Dutt, co-founder and CEO of Grafana Labs.

In addition to walking us through the presentation that encouraged Lightspeed to invest in Grafana’s Series A, the duo also gave direct feedback to audience members about their pitch decks.

Watch a video with our complete episode, or read highlights from the chat to get Gupta and Dutt’s insights on what goes into a successful pitch deck.

New episodes of Extra Crunch Live drop each Wednesday at 12 p.m. PST/3 p.m. EST/8 p.m. GMT.

Here’s a breakdown of the complete episode with Gaurav Gupta and Raj Dutt:

Paper plane made from a ten-dollar bill. Image Credits: LockieCurrie (opens in a new window)/ Getty Images

Some IT managers may still be debating the merits of usage-based pricing versus subscription-based models, but SaaS investors have made up their minds.

Compared to their rivals, companies that employ usage-based pricing trade at a 50% revenue multiple premium. You can argue with success, but seven out of the nine IPOs since 2018 with the best net dollar retention offer usage-based models.

If you’re a founder who hopes to break into the $100M ARR club, this guest post can help you identify the right usage metrics for creating a sustainable customer journey.

For more actionable advice regarding SaaS pricing and sales, see these previously published Extra Crunch stories:

Image Credits: Nigel Sussman (opens in a new window)

How many dating networks can the public market support?

In Tuesday’s column, Alex Wilhelm examined the latest IPO filing from relationship-finding service Bumble.

The company set a range of $28 – $30 per share, so Alex set out to find its simple and diluted valuations, how much it expects investors to pay and “how those stack up compared to Match Group’s own numbers.”

Image Credits: Nigel Sussman (opens in a new window)

Discount brokerage Robinhood stayed in the news last week as it became a proxy battlefield for institutional and retail investors, but its backers “put in another billion just last week,” says Alex Wilhelm.

Why were investors so bullish after days of screaming headlines?

In yesterday’s column, Alex unpacked Robinhood’s Q4 2020 numbers, “which shows a return to sequential-quarterly growth at the trading upstart.”

Image Credits: Towfiqu Photography / Getty Images

Before Redditors came after GameStop, zero-cost trading service Public says it was seeing “steady ~30%” month-over-month growth.

Last week, however, “new user signups went up 20x,” founders Leif Abraham and Jannick Malling told TechCrunch.

After closing a $65 million Series C, Public announced yesterday that it would “stop participating in the practice of Payment for Order Flow,” replacing PFOF with an “optional tipping feature.”

Image Credits: Andrii Yalanskyi (opens in a new window) / Getty Images

Startups that don’t directly engage their earliest customers with purpose and intention are leaving money on the table.

Creating a Customer Advisory Board (CAB) is a proven method for soliciting product ideas, testing marketing plans and turning early users into loyal brand advocates.

Before you call a CAB, read this post to find out how to identify customers who’ll contribute real insights, establish goals and “pick members who play well together.”

Red and white stop sign on the wall. Image Credits: Karl Tapales (opens in a new window)/ Getty Images

Identity and access management company Okta announced in a study last week that its largest customers use an average of 175 different applications to manage their operations.

Managing Editor Danny Crichton says this “explosion of creativity and expressiveness and operational latitude” offers widespread benefits, but it’s “also a recipe for disaster,” since many end users aren’t well-trained when it comes to using these tools.

This enterprise version of the Tower of Babel creates an opening for companies that offer “best practices as a service,” says Danny. “The next generation of SaaS software has to take those abecedarian building blocks and forcibly guide users to using those tools in the best possible way.”

Powered by WPeMatico

The recent Databricks funding round, a $1 billion investment at a $28 billion valuation, was one of the year’s most notable private investments so far.

For Databricks signaled its IPO readiness by disclosing to TechCrunch last year that it had scaled its revenue run rate from $200 million to $350 million in a year, so the new capital looked like the capstone on its private fundraising before an eventual public debut.

The Exchange explores startups, markets and money. Read it every morning on Extra Crunch, or get The Exchange newsletter every Saturday.

But I did have a few questions, starting with the price of the round.

At a $28 billion valuation and ARR of $425 million, Databricks is valued at around 66x top line. That’s steep, if not the highest number we can dredge up on the public markets. Of course, for Databricks shareholders, seeing the value of their stock rise so quickly is hardly a bad thing. They are hardly going to complain about having more paper wealth.

But what about the investor perspective? Does the price really make sense? The Exchange caught up with Battery Ventures’ Dharmesh Thakker earlier this week to discuss a number of things, one of which was Databricks’ round and pricing. Thakker is named in the Databricks Series D funding announcement, which brought Battery into the company.

What was surprising about our conversation was not that Thakker was bullish on Databricks — a company that he and his firm have backed since its $140 million, 2017 round when the company was worth just under $1 billion. What surprised me was that he thinks its new $28 billion valuation might be a little low.

What was surprising about our conversation was not that Thakker was bullish on Databricks — a company that he and his firm have backed since its $140 million, 2017 round when the company was worth just under $1 billion. What surprised me was that he thinks its new $28 billion valuation might be a little low.

Intriguing, yeah? So this morning for both of us, I’ve pulled out quotes from our chat to help explain how Thakker views the market for Databricks, unicorns at scale more broadly through the lens of risk-adjusted investing, and the scale of the market some unicorns are playing in.

At the close, we’ll remind ourselves what Databricks CEO Ali Ghodsi told TechCrunch when we asked him the same question. Let’s go!

Here’s how the valuation part of my chat with the Battery Ventures’ investor went down:

The Exchange: I want to talk about Databricks, because I spoke to [CEO] Ali [Ghodsi] yesterday about this round, and hot damn, it’s a lot of money at a valuation that is roughly 64x ARR, give or take. I don’t understand the price, and I know it’s a boring thing to talk about. [It’s a] great company, I get their market, I’ve talked to them a bunch, I know their revenue numbers. [But] I don’t understand the price, and I was hoping you could tell me why I’m being too conservative.

Dharmesh Thakker: I, for what it’s worth, think [the price] fair. If anything, I think it is on the lower end — he could have done better, frankly. But I think it comes down to three major things, right?

One is the addressable market. Just think about the addressable market of data. If there’s a trillion dollars spent in software or technology, I think you and I would be both hard pressed to say, almost all of that [isn’t] influenced by some data-oriented decisioning. Whether it’s digital transformation, whether it’s analytics, data is everywhere. So the TAM is massive … I think you and I both agree on that, whether it is $20 billion or $80 billion — it’s massive.

Powered by WPeMatico

Soon all tech news will be fintech news, all fintech news will be trading platform news and all trading platform news will concern the business mechanics of such services.

So, after looking into Robinhood’s fourth-quarter payment for order flow (PFOF) revenues this morning, we’re back with a related story. This time, however, we’re talking about Public.

Public, like Robinhood, is a zero-cost trading service. Its founders have worked to build a community-first platform, including offering ways to let groups chat about their investments.

And like Robinhood, Public has seen its growth skyrocket in recent days. Company representatives told TechCrunch today it was seeing “steady ~30%” month-over-month growth until Thursday, when “new user signups went up 20x.”

Both share strong backing from investors: Robinhood raised billions in new capital this week to ensure it has enough cash to meet clearinghouse deposit requirements. It managed to do so in part because its Q4 2020 numbers show that its PFOF business is ticking along nicely.

Public, flush with a recent $65 million Series C, took a different tack this morning and announced it would “stop participating in the practice of Payment for Order Flow.”

To which we say … all right.

On one level, this is neat. Public is not going to sell its order flow to market makers for fees. That’s good for users, but how will it make up the lost revenue? Tips, which will prove an interesting experiment in monetization.

TechCrunch asked the company if it believes tips will compensate for PFOF revenue, to which founders Leif Abraham and Jannick Malling replied via email that they were “optimistic that the difference will be offset by the optional tipping feature.”

However, dropping payment for order flow is only so brave a move from Public. After all, Public was not making Robinhood-level amounts of fetti from its PFOF business. Indeed, as we wrote when Public raised its Series C:

Before chatting with Public, I dug into its trading partner Apex’s filings to learn about its payment for order flow results from its recent filings. The resulting sums are somewhat modest for Apex’s collected clients. This means that Public’s revenue metrics, a portion of the aggregate sums, are even more unassuming.

Powered by WPeMatico

Amidst all of the the sturm und drang of l’affaire GameStop, Qualtrics went public today.

After pricing its stock above its raised IPO range, the company received a warm welcome from public investors. After starting its trading life worth $41.85, Qualtrics closed the day worth $45.50, up some 51.67%.

Qualtrics did everything that it said it was going to.

The software company’s debut comes after a lengthy path to the public markets; Qualtrics sold to SAP on the eve of its first run at a public listing back in 2018. Now, SAP has completed spinning the company out, though the software giant remains the Utah unicorn’s largest shareholder.

That Qualtrics’ IPO might perform well was presaged in its pricing run, having prices far above its initial valuation estimates; there was evidence of strong demand even before its shares started to trade.

But did Qualtrics misprice, given its strong first-day performance? TechCrunch spoke with Qualtrics CEO Zig Serafin, and its founder and current executive chairman Ryan Smith about its public offering, hoping to learn a bit about what is next for the company.

Having spoken to myriad folks on IPO days, I’ve learned the best way to kick off is to ask about emotions. Most CEOs and other execs are tied up in what they can (and cannot) say. And they are well-trained by communications experts regarding what to repeat and emphasize. You can sometimes loosen them up a little, however, by asking them how they feel.

In response to that question, Serafin described a feeling of gratitude and Smith brought up the long game. Qualtrics, he said, had been told that it couldn’t bootstrap, that it couldn’t build in Utah, that SAP had overpaid, that SAP had messed up and so forth.

Powered by WPeMatico

This morning, investor and SPAC raconteur Chamath Palihapitiya announced two new blank-check deals involving Latch and Sunlight Financial.

Latch, an enterprise SaaS company that makes keyless-entry systems, has raised $152 million in private capital, according to Crunchbase. Sunlight Financial, which offers point-of-sale financing for residential solar systems, has raised north of $700 million in venture capital, private equity and debt.

We’re going to chat about the two transactions.

There’s no escaping SPACs for a bit, so if you are tired of watching blind pools rip private companies into the public markets, you are not going to have a very good next few months. Why? There are nearly 300 SPACs in the market today looking for deals, and many will find one.

The Exchange explores startups, markets and money. Read it every morning on Extra Crunch, or get The Exchange newsletter every Saturday.

Think of SPACs are increasingly hungry sharks. As a shark get hungrier while the clock winds down on its deal-making window, it may get less choosy about what it eats (take public). There are enough SPACs on the hunt today that they would be noisy even if they were not time-constrained investment vehicles. But as their timers tick, expect their deal-making to get all the more creative.

This brings us back to Chamath’s two deals. Are they more like the Bakkt SPAC, which led us to raise a few questions? Or more akin to the Talkspace SPAC, which we found pretty reasonable? Let’s find out.

Let’s start with the Latch deal.

New York-based Latch sells “LatchOS,” a hardware and software system that works in buildings where access and amenities matter. Latch’s hardware works with doors, sensors and internet connectivity.

The company has raised a number of private rounds, including a $126 million deal in August of 2019 that valued the company at $454.3 million on a post-money basis, according to PitchBook data. The company raised another $30 million in October of 2020, though its final private valuation is not known.

As Chamath tweeted this morning, Latch is merging with TS Innovation Acquisitions Corp, or $TSIA. The SPAC is associated with Tishman Speyer, a commercial real estate investor. You can see the synergies, as Latch’s products fit into the commercial real estate space.

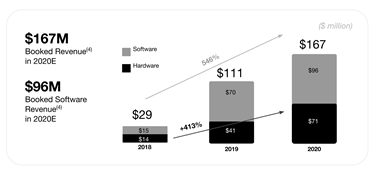

Up front, Latch is not a company that is only reporting future revenues. It has a history as an operating entity. Indeed, here’s its financial data per its investor presentation:

Image Credits: Latch

Doing some quick match, Latch grew booked revenues 50.5% from 2019 to 2020. Its booked software revenues grew 37.1%, while its booked hardware top line expanded over 70% during the same period.

That could be due to strong hardware installation fees, which could later result in software revenues; the company claims an average of a six-year software deal, so hardware revenues that are attached to new software incomes could low key declaim long-term SaaS revenues.

Update: Adding some clarity here, the above are “booked” revenues, which I’ve made more clear, not actual revenues. Its net revenues, better known as actual revenues, were $18 million, with $14 million of that coming from hardware. So, today, the company is certainly more hardware-heavy than I first thought. Damn non-S-1 filings!

While some were quick to note that the company is far from pure-SaaS — correct — I suspect that the model that could get some traction amongst investors is that this feels a bit like Peloton for real estate. How so? Peloton has large hardware incomes up front from new users, which convert to long-term subscription revenues. Latch may prove similar, albeit for a different customer base and market.

Per the deal’s reported terms, Latch will be worth $1.56 billion after the transaction. The combined entity will have $510 million in cash, including $190 million from a PIPE — a method of putting private money into a public entity — from “BlackRock, D1 Capital Partners, Durable Capital Partners LP, Fidelity Management & Research Company LLC, Chamath Palihapitiya, The Spruce House Partnership, Wellington Management, ArrowMark Partners, Avenir and Lux Capital.”

Powered by WPeMatico