EC Newsletter

Auto Added by WPeMatico

Auto Added by WPeMatico

Amidst all the hype that Lemonade (IPO), Root (IPO), Metromile (SPAC-led debut) and other insurtech players have generated in the last year, it’s been easy to forget about Oscar Health. But now that the company founded in 2012 is approaching the public markets, one of the early tech-themed insurance companies is catching up on the attention front.

The Exchange explores startups, markets and money. Read it every morning on Extra Crunch, or get The Exchange newsletter every Saturday.

So this morning we’re digging into Oscar Health’s first IPO pricing interval, hoping to understand how the market is valuing its unprofitable health-insurance enterprise.

Recall that Oscar Health was valued at around $3.2 billion in March of 2018. That datapoint, via PitchBook, is dated. Oscar Health raised hundreds of millions since (per several venture-capital tracking databases, including Crunchbase) but we lack a final private valuation for the company.

Recall that Oscar Health was valued at around $3.2 billion in March of 2018. That datapoint, via PitchBook, is dated. Oscar Health raised hundreds of millions since (per several venture-capital tracking databases, including Crunchbase) but we lack a final private valuation for the company.

Regardless, with Oscar Health now targeting a $32 to $34 per-share IPO range, we can get our hands dirty.

Let’s get some valuation numbers and then decide if Oscar Health feels cheap or expensive at that price.

Oscar Health is looking to reap as much as $1.21 billion in its IPO, a huge sum. The company is selling 30,350,920 shares, with 4,650,000 additional shares reserved for its underwriters. Existing shareholders are selling another 649,080 shares.

This means that after the IPO, Oscar Health will have 197,037,445 Class A and B shares in circulation, or 201,687,445 after counting shares reserved for its underwriters.

Using the company’s $32 to $34 per-share range, we can calculate a valuation minimum of $6.31 billion for the company (lower share count, low-end of price range) and $6.86 billion (higher share count, high-end of price range). That’s the company’s simple IPO valuation.

Oscar Health may also sell up to $375 million of its shares at its IPO price to three different funds. The company advises that the “indication of interest is not a binding agreement or commitment to purchase,” so we can ignore it for now.

Powered by WPeMatico

Mere days after we discussed Coinbase at $77 billion and Stripe at $115 billion in the private markets, those same semi-liquid exchanges have provided a new valuation for the cryptocurrency company. It’s now $100 billion, per Axios’ reporting.

Good thing we argued last week that there could be some merit to Coinbase’s $77 billion secondary market valuation from a particular perspective. We’d look silly today if we’d mocked the $77 billion figure only for it to go up by about a third in just a few days.

The Exchange explores startups, markets and money. Read it every morning on Extra Crunch, or get The Exchange newsletter every Saturday.

Luckily for us, Axios also got its hands on a few numbers regarding Coinbase’s 2019 and 2020 financial performance, so we can get into all sorts of trouble this morning. We’ll look at the data, which stretches to the end of Q3 2020, and then do some creative extrapolating into Q1 2021 to decide whether Coinbase at $100 billion makes no sense, a little sense or perfect sense.

As always, we’re riffing, not giving investment advice. So read on if you want to noodle on Coinbase with me; its impending direct listing will be one of the year’s most watched financial events.

We’ll drag Stripe back in at the end. Given that the companies now nearly share private-market valuations, we’d be remiss to not unfairly stack them against one another. Into the breach!

Axios’ Dan Primack, a good egg in my experience, got the goods on Coinbase’s historical performance. Summarizing the bits we need, here’s what the crypto exchange got up to recently:

It’s simple to take the 2020 data that we have and extrapolate it into full-year data. Indeed, you get revenues of $921.33 million and net income of $188 million. Compared to its 2019 data, Coinbase would have managed around 74% growth while swinging steeply into the profitable domain.

That’s a killer year. But it’s actually a bit better than we are giving Coinbase credit for. Poking around volume data compiled by Bitcoinity.org, Coinbase had its biggest period of 2020 in terms of bitcoin trading volume in the fourth quarter. Thinking about Coinbase’s 2020 from a trading perspective using the same dataset, it had a great Q1, more staid Q2 and Q3, and a blockbuster Q4 that ramped to record highs at the end.

Powered by WPeMatico

Since the pandemic began, have you been walking more, or do you know someone who bought a new car? Perhaps you ran your first errand on a rented e-bike or scooter?

Over the last year, I’ve experimented with different mobility options to see which ones best suit my needs, as have most people I know. It can be challenging to maintain a recommended physical distance on a bus or subway. (After a decade-plus hiatus, I even briefly considered rejoining the ranks of automobile owners!)

Full Extra Crunch articles are only available to members.

Use discount code ECFriday to save 20% off a one- or two-year subscription.

It took some getting used to, but I now enjoy traveling around San Francisco on a scooter or e-bike. Pre-pandemic, I was leery of riding two-wheeled vehicles in a city with a high rate of injury collisions, but there are fewer cars on the road than there used to be.

COVID-19 has spotlighted many of the weakest points in our transportation system, but some of the rapid shifts in consumer behavior are creating opportunities for tech once considered fanciful, like sidewalk delivery robots and eVTOLs (electric vertical and takeoff vehicles).

Transportation editor Kirsten Korosec reached out to 10 investors to learn more “about the state of mobility, which trends they’re most excited about and what they’re looking for in their next investments.”

Here’s who she interviewed:

Thanks very much for reading Extra Crunch this week!

Walter Thompson

Senior Editor, TechCrunch

@yourprotagonist

Image Credits: Nigel Sussman (opens in a new window)

Yesterday’s House Financial Services Committee hearing on the GameStop short squeeze saga was fairly typical: Most lawmakers used their time to grandstand and little new information was revealed.

But Alex Wilhelm found one tidbit: Much of Robinhood’s revenue is generated from payment for order flow (PFOF). Under the practice, market makers pay the trading platform for executing trades.

To get a sense of how much Robinhood’s high rollers contribute to the company’s general health, he calculated its PFOF revenues for the last three months of 2020.

“Borrowing a term from the casino trade, these whales generate the bulk of the company’s revenue stream.”

Image Credits: John Lund (opens in a new window) / Getty Images

HubStop introduced usage-based pricing in 2011 to boost its retention rate, then near 70%.

When it went public three years later, its net revenue retention rate was edging close to 100%, “all without hurting the company’s ability to acquire new customers.”

Offering new users frictionless onboarding, customer support and free credits is a proven method for making them more active — and loyal.

So, why do public SaaS firms with usage-based pricing see faster growth?

“Because they’re better at landing new customers, growing with them and keeping them as customers,” says Kyle Powar, VP of growth at OpenView.

Image Credits: Nigel Sussman (opens in a new window)

In October 2018, private-market money valued Coinbase at around $8 billion. As of this week, it’s valued at $77 billion.

Similarly, Stripe is valued at $115 billion on secondary markets. In the middle of last year, that figure was closer to $36 billion.

“Would I line up to pay $77 billion for Coinbase?” asked Alex. “Probably not, but that doesn’t mean that the public markets won’t.”

Image Credits: Witthaya Prasongsin (opens in a new window) / Getty Images

Natasha Mascarenhas reports that some edtech startups are hitching rides with special purpose acquisition vehicles so they can speed up their journey to the public markets.

To learn more, she interviewed Susan Wolford, chairperson of $200 million SPAC Edify Acquisition, and Nerdy CEO Chuck Cohn. Nerdy, parent company of Varsity Tutors, is going through a reverse merger with TPG Pace Tech Opportunities.

“It’s less about going into the public markets and more about that this transaction allows us to take an offensive position and lean into the big opportunities,” Cohn said.

Image Credits: Bryce Durbin/TechCrunch

Dear Sophie:

My fiancé is in the U.S. on an H-1B visa, which is set to expire in about a year and a half.

We were originally planning to marry last year, but both he and I want to have a ceremony and party with our families and friends, so we decided to hold off until the pandemic ends. I’m a U.S. citizen and plan to sponsor my fiancé for a green card.

How long does it typically take to get a green card for a spouse? Any tips you can share?

— Sweetheart in San Francisco

Image Credits: Nigel Sussman (opens in a new window)

When I saw that Alex Wilhelm wrote on Tuesday about two more startups that were taking the SPAC route to public markets, I briefly wondered if we’ve been covering special purpose acquisition companies too frequently.

After I read his first sentence, I realized Alex made exactly the right call because the trend that emerged in 2020 may be turning into a actual wave: This week, pet e-commerce company Rover and fintech startup MoneyLion both announced that they’re planning SPAC-led debuts.

On Monday, Alex covered the news that Lerer Hippeau Acquisition Corp. and Khosla Ventures Acquisition Co. I, II and III. filed S-1 filings last week.

“You have to wonder if every VC worth a damn in the future will have their own raft of SPAC offerings,” says Alex.

Wrote Lerer Hippeau Acquisition Corp.:

With our portfolio now maturing to the stage at which many are considering the public markets, we view SPACs as a natural next step in the evolution of our platform.

“If we are not careful, every entry of this column could consist of SPAC news,” writes Alex.

Image Credits: CasarsaGuru (opens in a new window) / Getty Images

Fifteen U.S.-based institutions of higher learning have joined forces to create the University Technology Licensing Program LLC (UTLP).

The program makes it easier for entrepreneurs and investors to find IP that can drive their companies forward, but it’s also an attempt to repair what one participant calls “the somewhat broken interface between universities and very large companies in the tech space.”

Image Credits: Mallika Wiriyathitipirm/EyeEm (opens in a new window) / Getty Images

Here’s some real talk for technical founders: if you find it frustrating to work with growth experts and marketing professionals, the feeling’s probably mutual.

“Incredible growth people are independent and creative and are drawn to environments that explicitly value these traits,” says Jessica Li, a content/growth professional who was previously a VC.

To land top talent, “demonstrate that you have a team structure in place where a growth marketer could fit in and thrive.”

Image Credits: Donald Iain Smith (opens in a new window) / Getty Images

Before my first cup of coffee this morning, I’d already interacted with four different devices that transmitted details about my behavior to a data lake.

Hopefully, the response I sent to an automated text while waiting for the kettle to boil will generate a discount offer in my inbox later today. (And hopefully, the raw data I’m transmitting has been properly secured and cataloged.)

Enterprise reporter Ron Miller interviewed nine investors to learn more about their approach to the lucrative data lake market:

Image Credits: Felicis Ventures / Guideline

When it comes to building a durable relationship between a founder and an investor, “the trust starts in the pitch deck,” says Guideline CEO Kevin Busque.

Busque joined Extra Crunch Live last week with Felicis Ventures’ Aydin Senku to discuss the seed round Senku declined to join — and the Series B he led a short while later.

In keeping with our new format, the pair also offered feedback on pitch decks submitted by members of the audience. Read highlights, or watch a video with the full conversation.

Powered by WPeMatico

If we are not careful, every entry of this column could consist of SPAC news.

Special purpose acquisition companies, or blank-check companies, whatever you prefer to call them, are enormous business today. But they aren’t the only thing going on, and we’ll get to other things shortly. Consider this an apology for having written about SPACs twice in two days.

Yesterday, we considered the rise of the VC-led SPAC and whether venture capital groups that offer seed-through-SPAC money will wind up with advantage in the market over firms that specialize on any particular startup stage. Sticking to the blank-check theme, this morning we’re looking into two SPAC-led deals, namely those involving Rover and MoneyLion.

The Exchange explores startups, markets and money. Read it every morning on Extra Crunch, or get The Exchange newsletter every Saturday.

We’re doubling up to prevent more SPAC-related posts. And we’ve selected Rover because Chewy, another pet-themed entity, is an already-public company. As both were venture-backed, we may be able to contrast their trading performance post-debut. Sadly, Chewy is focused on pet e-commerce while Rover is more centered around pet services, but they may prove close enough for some loose comparisons.

And why chat about MoneyLion? Because it’s a heavily venture-backed fintech startup, one that TechCrunch has covered extensively. If its SPAC-assisted vault into the public markets goes well, it could smooth the same path forward for myriad other yet-private fintechs sitting atop a mountain of raised capital.

So this is a SPAC post, but as we’ll largely be looking at the financial health of two companies that we’ve heard about for ages and never got to see inside of, I hope you join me all the same.

We’re starting with the Rover investor presentation, before zipping over to MoneyLion’s own.

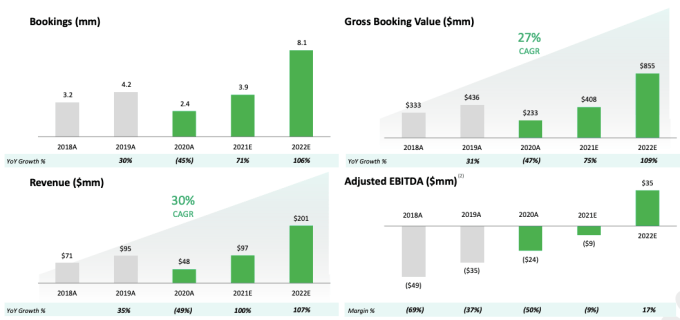

Rover is merging with Nebula Caravel Acquisition Corp., which is affiliated with True Wind Capital. The deal gives Rover an anticipated market cap of around $1.6 billion, with around $300 million in cash on its books.

So, how attractive is this new unicorn? You can find its investor deck here, if you want to read along as we peek.

First up, the company stresses rising use of digital services in the last year thanks to the pandemic and the fact that pet ownership is growing. Both of which are true. We’ve seen the accelerating digital transformation for both companies and consumers. And if you’ve tried to adopt a pet lately, you’ve seen how few are left waiting for forever homes.

With those things behind it, you might be wondering why Rover is pursuing a SPAC-led debut as well. If its market is hot and it has previously raised venture capital, why not just go public via an IPO? Because 2020 was tough on the company.

Image Credits: Rover

Revenue dipped from $95 million in 2019 to just $48 million last year. Bookings fell from 4.2 million to 2.4 million over the same time frame, leading to gross booking value falling from $436 million in 2019 to $233 million in 2020. Why? Because everyone was stuck at home. With their pets. A situation that limited demand for Rover-delivered pet services.

Powered by WPeMatico

I’m very proud of the work we’re doing here at Extra Crunch, so it gives me great pleasure to announce that today is our second anniversary.

Thanks to hard work from the entire TechCrunch team, authoritative guest contributors and a very engaged reader base, we’ve tripled our membership in the last 12 months.

As Extra Crunch enters its third year, we’re putting our foot on the gas in 2021 so we can bring you more:

Full Extra Crunch articles are only available to members

Use discount code ECFriday to save 20% off a one- or two-year subscription

To be completely honest: Eric and I wavered about posting this announcement. Both of us would prefer to show the results of our work than make a list of future-looking statements, so I’ll sum up:

I’m proud of the work we’re doing because people around the world use the information they find on Extra Crunch to build and grow companies. That’s big!

Thanks very much for reading Extra Crunch; have a great weekend.

Walter Thompson

Senior Editor, TechCrunch

@yourprotagonist

Image Credits: Bryce Durbin

Image Credits: Nigel Sussman (opens in a new window)

Before the pandemic began, I took about seven or eight hailed rides each month. Since I began physically distancing from others to stem the spread of the coronavirus in March 2020, I’ve taken exactly 10 hailed rides.

Your mileage may vary, but last year, Uber and Lyft both reported steep revenue losses as travelers hunkered down at home. Today, Alex Wilhelm says both transportation platforms plan to reach adjusted profitability by Q4 2021.

He unpacked the numbers “to see if what the two companies are dangling in front of investors is worth desiring.” Since he usually doesn’t focus on publicly traded stocks, I asked Alex why he focused on Uber and Lyft today.

“Utter confusion,” he replied.

“Investors have bid up their stocks like the two companies are crushing the game, instead of playing a game with their numbers to reach some sort of profit in the future,” Alex explained. “The stock market makes no sense, but this is one of the weirder things.”

Image Credits: Techstars (opens in a new window)

In the theater, a “four-hander” is a play that was written for four actors.

Today, I’m appropriating the term to describe this roundup by Greg Kumparak, Natasha Mascarenhas, Alex Wilhelm and Jonathan Shieber that recaps their favorite startups from Techstars accelerators.

The quartet selected four startups each from Chicago, Boston and Techstars Workplace Development.

“As always, these are just our favorites, but don’t just take our word for it. Dig into the pitches yourself, as there’s never a bad time to check out some super-early-stage startups.”

Image Credits: Nigel Sussman (opens in a new window)

Neoinsurance company Metromile began trading publicly this week after it combined with a special purpose acquisition company.

Metromile will likely be one of 2021’s many SPAC-led debuts, so Alex interviewed CEO Dan Preston to learn more about the process and what he learned along the way.

A notable takeaway: “Preston said SPACs are designed for a specific class of company; namely those that want or need to share a bit more story when they go public.”

Image Credits: alashi (opens in a new window) / Getty Images

Senior Writer Anthony Ha and Extra Crunch Managing Editor Eric Eldon surveyed three investors who back adtech and martech startups to learn more about what they’re looking for and whether deal flow has recovered at this point in the pandemic:

Image Credits: VCG (opens in a new window) / Getty Images

I have a hard time envisioning all of the hurdles deep tech founders must overcome before they can land their first paying customer.

How do you sustainably scale a company that probably doesn’t have revenue and isn’t likely to for the foreseeable future? How big is the TAM for an unproven product in a marketplace that’s still taking shape?

Vin Lingathoti, a partner at Cambridge Innovation Capital, says entrepreneurs operating in this space face a unique set of challenges when it comes to managing growth and risk.

“Often these founders with Ph.D.s and postdocs find it hard to accept their weaknesses, especially in nontechnical areas such as marketing, sales, HR, etc.,” says Lingathoti.

Image Credits: Nigel Sussman (opens in a new window)

This week, auto insurance startup Metromile completed its combination with SPAC INSU Acquisition Corp. II.

Last Friday, health insurance company Oscar Health announced its plans to launch an initial public offering.

As the saying goes: Past performance is no guarantee of future results, but using 2020 debuts by neoinsurance firms Lemonade and Root as a reference point, Alex says the IPO window is wide open for other players in the space.

“All the companies in our group are pretty good at adding customers to their businesses,” he found.

Image Credits: Bryce Durbin/TechCrunch

Dear Sophie:

We’ve been having a tough time filling vacant engineering and other positions at our company and are planning to make a more concerted effort to recruit internationally.

Do you have suggestions for attracting workers from abroad?

— Proactive in Pacifica

Image Credits: ALLVISIONN (opens in a new window) / Getty Images

The people who produce viral TikTok duets, in-demand Substack newsletters and popular YouTube channels are doing what they love. And the money is following them.

Many of these emerging stars have become media personalities with full-fledged production and distribution teams, giving rise to what one investor described as “the enterprise layer of the creator economy.”

More VCs are backing startups that help these digital creators monetize, produce, analyze and distribute content.

Natasha Mascarenhas and Alex Wilhelm interviewed five of them to learn more about the opportunities they’re tracking in 2021:

Image Credits: Nigel Sussman (opens in a new window)

Simple agreements for future equity are an increasingly popular way for startups to raise funds quickly, but “they don’t generate the same paperwork exhaust,” Alex Wilhelm noted this week.

This creates cognitive dissonance: Investors see a hot market, while people who rely on public data (like journalists) get a different picture.

“SAFEs have effectively pushed a lot of public signal regarding seed deals, and even smaller rounds, underground,” says Alex.

Image Credits: Andriy Onufriyenko / Getty Images

Many enterprise companies were snapping up container security startups before the pandemic began, but the pace has picked up, reports Ron Miller.

The growing number of companies going cloud-native is creating security challenges; the containers that package microservices must be correctly configured and secured, which can get complicated quickly.

“The acquisitions we are seeing now are filling gaps in the portfolio of security capabilities offered by the larger companies,” says Yoav Leitersdorf, managing partner at YL Ventures.

Image Credits: Bryce Durbin / TechCrunch

In December 2019, Alex Wilhelm began reporting on startups that had reached the $100M ARR mark. A year later, he decided to reframe his focus.

“Mostly what we managed was to collect a bucket of companies that were about to go public,” he said.

Since then, he has recalibrated his sights. In the latest entry of a new series focusing on “$50M-ish” companies, he studies SimpleNexus, which offers digital mortgage software, and photo-editing service PicsArt.

Alex has more interviews and data dives coming on other companies in this cohort, so stay tuned.

Image Credits: Nigel Sussman (opens in a new window)

Dating platform Bumble initially set a price of $28 to $30 for its upcoming IPO, but at its new range of $37 to $39, Alex calculated that it could reach a max valuation of $7.4 billion to $7.8 billion.

Extrapolating revenue from its Q3 2020 numbers, he attempted to find the company’s run rate to see if it’s overpriced — and how well it stacks up against rival Match.

Mario Schlosser (Oscar Health) at TechCrunch Disrupt NY 2017

Jon Shieber and Alex Wilhelm co-bylined a story about Oscar Health, which filed to go public last week.

Although the health insurance company claims 529,000 members and a compound annual growth rate of 59%, “it’s a deeply unprofitable enterprise,” they found.

Jon and Alex parsed Oscar Health’s 2019 comps and its 2020 metrics to take a closer look at the company’s performance.

“Both Oscar and the high-profile SPAC for Clover Medical will prove to be a test for the venture capital industry’s faith in their ability to disrupt traditional healthcare companies,” they write.

Image Credits: Tomohiro Ohsumi (opens in a new window) / Getty Images

Managing Editor Danny Crichton filed a column about Softbank’s Vision Fund that tried to answer a question he asked in 2017: “What does a return profile look like at such a late stage of investment?”

Softbank’s recent earnings report shows that its $680 million bet on DoorDash paid off handsomely, bringing back $9 billion. Compared to its competition, “the fund is actually doing quite decent right now,” he wrote. But Softbank has invested $66 billion in 74 unexited 74 companies that are worth $65.2 billion today.

“SoftBank quietly chopped half of the performance fees for its VC managers, from $5B to $2.5B, which led us to ask: are the best investments in the fund already in SoftBank’s rearview mirror? One upshot: WeWork seems to have turned something of a corner, with some improvements in its debt profile portending more positive news post-COVID-19.”

Powered by WPeMatico

Remote-first startups were still controversial in Silicon Valley when we launched Extra Crunch two years ago today. Back then, if you can recall, the rest of the world was not even sure how all those unicorns were going to do on the public markets.

Today, Silicon Valley resides on the cloud and is publicly traded. We’ve covered the stunning changes, and as we help founders navigate the path from idea to first check to IPO, we also tripled the number of Extra Crunch members.

Take 20% off the price of a 2-year Extra Crunch membership

Offer expires Monday, February 15, 2021

Now, as the world glimpses a brighter, post-pandemic future, we are doubling down on the news and analysis that’s helped many early-stage companies make better decisions.

As Extra Crunch enters its third year, we’re putting our foot on the gas so we can bring you more:

We’ll also publish more articles with inside tips from industry experts to help you solve nonsoftware problems that face every company, like fundraising, growth and hiring, as well as deep dives into different industry sectors and pre-public companies.

We’re tying all of these efforts back in with the editorial coverage and event plans at TechCrunch. And to make this holistic approach truly successful, we’re ramping up efforts to engage and expand the Extra Crunch community.

In recent weeks, reporters and editors have appeared on Clubhouse and Discord to discuss their work with readers. We’re planning to expand this outreach, so stay tuned!

To show our appreciation for your support, we’re offering a 20% discount on two-year subscriptions through Monday, February 15 to celebrate our second anniversary. If you’re already a member, you can renew at a discount.

If you’re not a Extra Crunch member yet, we hope you’ll join us.

Powered by WPeMatico

Earlier today, South Korean e-commerce and delivery giant Coupang filed to go public in the United States. As a private company, Coupang has raised billions, including capital from American venture capital firm Sequoia and Japanese telecom giant SoftBank and its Vision Fund.

Coupang’s revenue growth is nothing short of fantastic.

Coupang’s offering, coming amidst the public debut of a number of well-known technology brands, will be a massive affair. Its first S-1 filing indicates that its IPO will raise capital in the range of $1 billion, far larger than the $100 million placeholder that is more common.

But the company’s scale makes its lofty IPO fundraising goals reasonable. Coupang is huge, with revenues north of $10 billion in 2020 and in improving financial health as it scales. And its revenue growth has accelerated.

Perhaps that explains why the company is reportedly targeting a valuation of $50 billion.

This afternoon, let’s dig into the company’s historical growth, its improving cash flow and its narrowing losses. Coupang’s debut will create a splash when it lands, so we owe it to ourselves to grok its numbers.

And as there are other e-commerce brands with a delivery function waiting in the wings to go public — Instacart comes to mind — how Coupang fares in its IPO matters for a good number of domestic startups and unicorns.

The company’s growth across the last half-decade is impressive. Observe its yearly revenue totals from 2016 through 2020:

Sure, some of that 2020 growth is COVID-19 related, but even taking that into account, Coupang’s revenue growth is nothing short of fantastic. And what’s better is that the company has cut its losses in recent years:

Powered by WPeMatico

Uber and Lyft lost a lot of money in 2020. That’s not a surprise, as COVID-19 caused many ride-hailing markets to freeze, limiting demand for folks moving around. To combat the declines in their traditional businesses, Uber continued its push into consumer delivery, while Lyft announced a push into business-to-business logistics.

But the decline in demand harmed both companies. We can see that in their full-year numbers. Uber’s revenue fell from $13 billion in 2019 to $11.1 billion in 2020. Lyft’s fell from $3.6 billion in 2019 to a far-smaller $2.4 billion in 2020.

The Exchange explores startups, markets and money. Read it every morning on Extra Crunch, or get The Exchange newsletter every Saturday.

But Uber and Lyft are excited that they will reach adjusted profitability, measured as earnings before interest, taxes, depreciation, amortization and even more stuff stripped out, by the fourth quarter of this year.

Ride-hailing profits have long felt similar to self-driving revenues: just a bit over the horizon. But after the year from hell, Uber and Lyft are pretty damn certain that their highly adjusted profit dreams are going to come through.

Ride-hailing profits have long felt similar to self-driving revenues: just a bit over the horizon. But after the year from hell, Uber and Lyft are pretty damn certain that their highly adjusted profit dreams are going to come through.

This morning, let’s unpack their latest numbers to see if what the two companies are dangling in front of investors is worth desiring. Along the way we’ll talk BS metrics and how firing a lot of people can cut your cost base.

Using normal accounting rules, Uber lost $6.77 billion in 2020, an improvement from its 2019 loss of $8.51 billion. However, if you lean on Uber’s definition of adjusted EBITDA, its 2019 and 2020 losses fall to $2.73 billion and $2.53 billion, respectively.

So what is this magic wand Uber is waving to make billions of dollars worth of red ink go away? Let’s hear from the company itself:

We define Adjusted EBITDA as net income (loss), excluding (i) income (loss) from discontinued operations, net of income taxes, (ii) net income (loss) attributable to non-controlling interests, net of tax, (iii) provision for (benefit from) income taxes, (iv) income (loss) from equity method investments, (v) interest expense, (vi) other income (expense), net, (vii) depreciation and amortization, (viii) stock-based compensation expense, (ix) certain legal, tax, and regulatory reserve changes and settlements, (x) goodwill and asset impairments/loss on sale of assets, (xi) acquisition and financing related expenses, (xii) restructuring and related charges and (xiii) other items not indicative of our ongoing operating performance, including COVID-19 response initiative related payments for financial assistance to Drivers personally impacted by COVID-19, the cost of personal protective equipment distributed to Drivers, Driver reimbursement for their cost of purchasing personal protective equipment, the costs related to free rides and food deliveries to healthcare workers, seniors, and others in need as well as charitable donations.

Er, hot damn. I can’t recall ever seeing an adjusted EBITDA definition with 12 different categories of exclusion. But, it’s what Uber is focused on as reaching positive adjusted EBITDA is key to its current pitch to investors.

Indeed, here’s the company’s CFO in its most recent earnings call, discussing its recent performance:

We remain on track to turn the EBITDA profitable in 2021, and we are confident that Uber can deliver sustained strong top-line growth as we move past the pandemic.

So, if investors get what Uber promises, they will get an unprofitable company at the end of 2021, albeit one that, if you strip out a dozen categories of expense, is no longer running in the red. This, from a company worth north of $112 billion, feels like a very small promise.

And yet Uber shares have quadrupled from their pandemic lows, during which they fell under the $15 mark. Today Uber is worth more than $60 per share, despite shrinking last year and projecting years of losses (real), and possibly some (fake) profits later in the year.

Powered by WPeMatico

Metromile began trading as a public company yesterday. Its exit from the private market was accelerated by its decision to combine with a special purpose acquisition company, or SPAC.

Such transactions have exploded in popularity in recent years, bridging the gap between a host of richly valued private companies and endless bored capital. SPACs raise cash, go public and then merge with a private entity. The SPAC then dissolves itself into the combined entity, a process that often includes an additional slug of money (PIPE) for good measure.

The Exchange explores startups, markets and money. Read it every morning on Extra Crunch, or get The Exchange newsletter every Saturday.

SPAC-led debuts can move faster than a traditional IPO, making them attractive to companies in a hurry. And with more visibility into how much capital might be raised than during a traditional public-offering pricing run, they can smooth worries amongst target-companies regarding how much cash they can attract by leaving the private-market fold.

Metromile is hardly the final company we expect to debut this year via a SPAC. The list is long and may include fellow neoinsurance company Hippo. (Hippo declined to comment on the matter.)

Metromile is hardly the final company we expect to debut this year via a SPAC. The list is long and may include fellow neoinsurance company Hippo. (Hippo declined to comment on the matter.)

But with many more SPACs coming our way, we took Metromile’s debut as a learning moment. To that end, we got on the horn with CEO Dan Preston to chat about what the day meant for his company, and to elicit a note or two on the SPAC process for our own enjoyment.

TechCrunch asked Preston about the SPAC world and how his combination came about. He said his firm started by dipping its toe into the blank-check waters, kicking off with a small set of conversations, chats that quickly gathered traction.

But don’t take that to mean that any company will elicit a similar market response. Preston said SPACs are designed for a specific class of company; namely those that want or need to share a bit more story when they go public. Younger companies, in other words, for whom a traditional S-1 filing might not be provide a sufficient summation of its potential.

Powered by WPeMatico

The IPO frenzy is not letting up, Bumble informed the world this morning.

Per a new SEC filing, the dating company raised its target IPO price range, indicating that its previous attempt to quantify its per-share value was an undershoot. This means we’ll need to calculate a host of new valuations and revenue multiples for the company.

But more than that, we have a question to answer: Is Bumble aiming for a Match.com price, despite not being as profitable as its already-public rival? The last time we covered the pair, Bumble’s implied revenue multiples were discounted compared to Match, but with this new price, has the smaller company gained ground?

The Exchange explores startups, markets and money. Read it every morning on Extra Crunch, or get The Exchange newsletter every Saturday.

And if so, does it mean that we’re seeing more public market enthusiasm for private companies? We’ll find out.

When it comes to the frenetic demand for IPO shares from public investors, I am reminded of a particular Dilbert. In this particular strip, Wally gets fired and is then hired back as a consultant. People outside the company appear smarter, he said, so he’s now back and getting paid more money than before.

This, but for private companies going public. Some companies appear to have huge promise while private, only to fizzle slowly while public. Or they manage huge price gains during their IPO process, only to cede those wins after they have a few trading months under their belt.

Is that what’s going to happen with Bumble?

Bumble targeted a $28 to $30 per-share IPO price when it first set a range, implying a greater than $1 billion raise. Now the company is selling more shares at an even higher price. From 34.5 million shares to 45 million, and at a new $37 to $39 per share price range, Bumble could raise $1.66 billion to $1.76 billion in its IPO.

And that’s not counting its underwriters’ option of 6.75 million shares, which might bring its total raise to $2.02 billion at the top end of its new pricing interval.

What is Bumble worth at those new prices? Using its simple, shares-outstanding post-IPO count of 112,745,301 — inclusive of its underwriters’ option — the company would be worth $4.17 billion to $4.4 billion.

Powered by WPeMatico