Column

Auto Added by WPeMatico

Auto Added by WPeMatico

An estimated 41 million Americans say they need life insurance but have yet to purchase coverage. Despite this awareness among consumers, the Life Insurance Marketing and Research Association estimates a $12 trillion coverage gap, with about 50% of millennials planning to purchase coverage within the next year.

There’s latent demand for life insurance currently unaddressed by much of the financial services industry, and embedded finance can be the solution. It’s imperative for companies to consider product lines and partnerships to expand markets, create new revenue streams and provide added value to their customers.

There’s latent demand for life insurance currently unaddressed by much of the financial services industry, and embedded finance can be the solution.

Connecting consumers with products they need through channels they already know and trust is both a massive revenue opportunity and a social good, providing financial resilience to families at a time when they need it most.

The concept of digitally bundling financial products in a packaged offering to a customer is certainly not new — but it is for the life insurance space.

Embedded finance uses technology and operations infrastructure to offer products and services through entities that may not be financial institutions at all. Think of embedded finance like on-demand shopping; customers benefit from both the transaction (buying financial protection for their families) and the convenience it provides (from whatever platform they are currently engaging with).

Similar to how Amazon saves shoppers 75 hours a year, bundling life insurance gives consumers back time in their day and can improve their financial health.

Powered by WPeMatico

The global tech sector is booming, and as technologies like cloud and AI accelerate their growth, the demand for tech talent outpaces supply globally. Specifically, the U.S. tech sector has seen unprecedented growth in recent years, with four tech firms reaching a $1 trillion market cap by the beginning of 2020 — all of which have seen double-digit growth since achieving a 13-digit valuation pre-pandemic.

One of the major factors in the growth and adoption of tech in the U.S. is the increasing focus on software as a service and broader digital transformations across industry sectors, which have accelerated due to the COVID-19 pandemic. As such, there is an insatiable appetite for quality tech talent in the U.S., with projections showing an 11% increase by 2029 from 2019 numbers, which amounts to over half a million new jobs.

Given that the U.S. produces only about 65,000 computer science graduates, there is a vast deficit in the tech talent market, which materialized as over 900,000 unfilled IT and related positions in 2019 alone. The problem is so vast that more than 80% of U.S. employers stated that recruiting for tech talent is a top business challenge, according to a survey by top HR consulting firm Robert Half.

Mexico’s tech talent can help to fill the gaps left in a hypercompetitive U.S. market for tech workers. Unlike the U.S., 20% of Mexican college graduates have relevant engineering degrees, amounting to over 110,000 per year, far surpassing the U.S. in technical talent. Investors and tech firms have noticed and are increasing operations in Mexico.

20% of Mexican college graduates have relevant engineering degrees, amounting to over 110,000 per year, far surpassing the U.S. in technical talent.

Some have referred to the cities of Monterrey and Guadalajara as the “Silicon Valley of Latin America,” and while their tech sectors are also seeing tremendous growth, the pace falls short of Mexico’s talent production, leading to a surplus of highly trained and capable individuals in the tech sector. The cost of higher education in Mexico is far less than in the U.S., so we’re likely to see that talent surplus grow in the coming years.

Under current conditions, the U.S. has an incredible opportunity to capitalize on the surplus of tech talent in Mexico. Because tech jobs are more scarce than in the U.S., the cost of talent in Mexico is considerably less than in the U.S. or in Canada. In general, talent in Mexico can be two to three times cheaper than in the U.S. while still delivering outstanding quality and specialized experience.

More so than other Latin American countries, Mexico has the experience and economy to support a robust tech talent export ecosystem. In fact, Mexico City’s concentrated market is larger than the sum total of every other Spanish-speaking country in Latin America. Specifically, Mexico’s IT outsourcing industry has been growing at an annual rate of 10%-15% and is now considered the third-largest exporter of IT services.

What’s more, the U.S./Mexico relationship is seeing a refresh after several tumultuous years. With Mexico ranked No. 1 among U.S. trade partners, the political and economic mechanisms for investments and partnerships are in place. Technology leaders such as Cisco and Intel have already set up shop in Mexico, demonstrating confidence in the country’s ability to support tech and economic growth.

Mexico provides a number of benefits that make drawing from its talent surplus easier and more efficient. For one, Mexico’s time zones align with those in the U.S., enabling real-time collaboration at times that work best for both parties. Compare this to the time difference in India, which is over 12 hours ahead of California’s Silicon Valley.

Beyond the time difference, there are also many cultural similarities that make working with Mexico the clear choice for IT outsourcing. For example, the U.S. is home to more than 41 million native Spanish speakers, and plus over 12 million bilingual Spanish speakers, making the U.S. the second-largest Spanish-speaking country after Mexico. While difficult to quantify, the number of consumer and cultural exports from Mexico to the U.S. also helps to build familiarity and solidarity between the two countries, which can only improve an already healthy relationship.

The steady progression of America’s tech sector is now seen as a strategic priority at the federal level. Meanwhile, public and private sector decision-makers are more interested than ever in conducting business under favorable trade treaty terms with friendly governments amid a new climate of geopolitical uncertainty.

As the U.S. tech sector continues its explosive growth, technology companies in the U.S. will need to seek alternative means to supplement its in-demand tech workforce. Rather than turning to countries undergoing increased regulatory scrutiny, or distant talent bases requiring significant business travel, business leaders are looking to geographically close, diplomatically friendly nations. U.S. companies are finding Mexico’s status as a key business partner and strategic ally to be a massive value driver.

By 2030, the middle-class population in Mexico is expected to reach 95 million, placing it in the top 10 countries with the highest share of global middle-class consumption. As the middle class rises, so will companies to meet their consumer needs, and, as such, Mexico’s own tech sector will grow and require significantly more tech talent, reducing or potentially eliminating Mexico’s talent surplus.

This is evidenced by the uptick in Mexico-based technology companies, such as Mexican used-car startup Kavak, which recently hit a $4 billion valuation. Amid an exciting backdrop of skyrocketing tech valuations and potential, the U.S. tech sector should look to Mexico as a key growth market and technology partner. The time is now for the U.S. to tap into the surplus of quality tech talent in Mexico.

Powered by WPeMatico

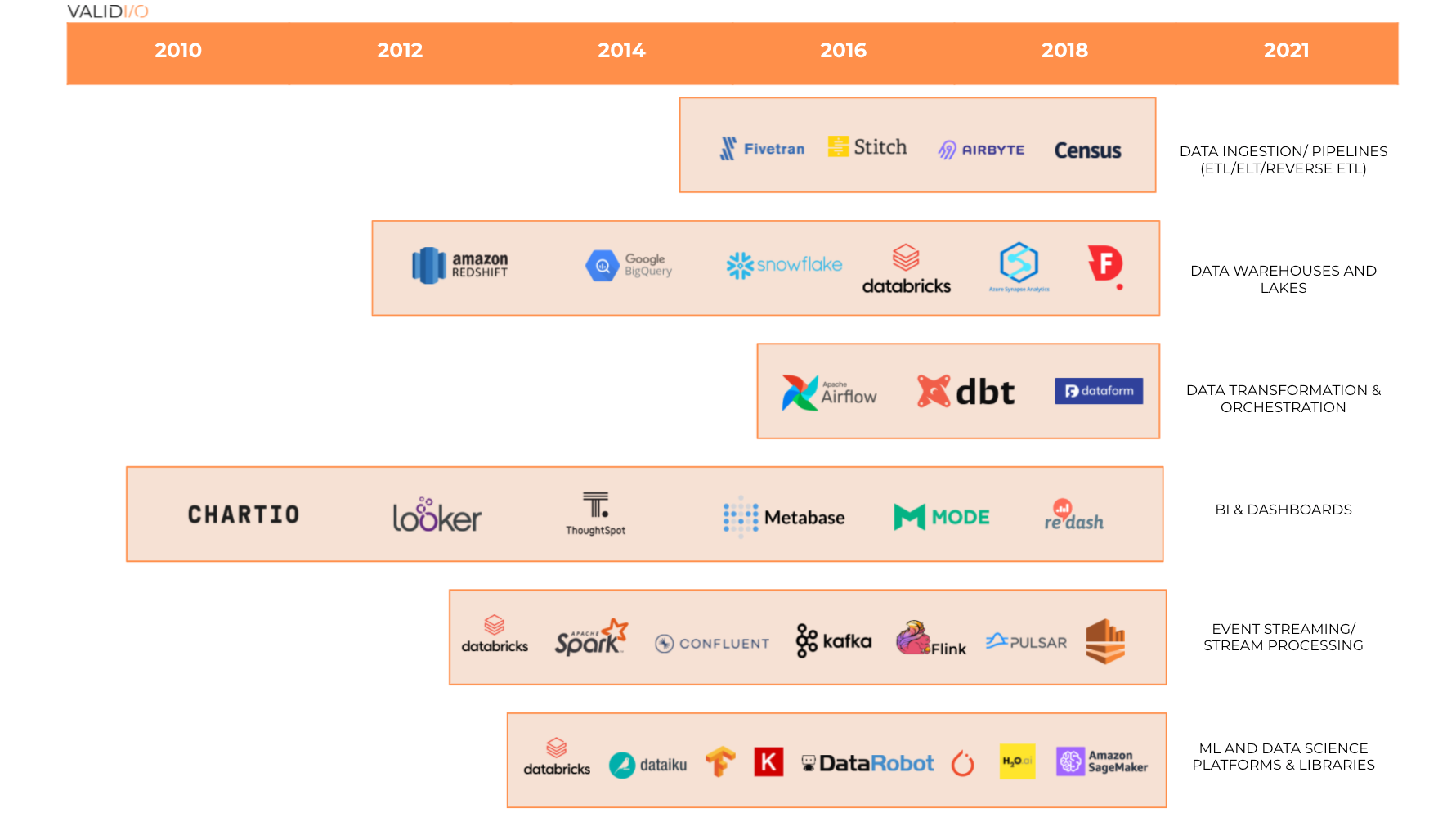

A little over a decade has passed since The Economist warned us that we would soon be drowning in data. The modern data stack has emerged as a proposed life-jacket for this data flood — spearheaded by Silicon Valley startups such as Snowflake, Databricks and Confluent.

Today, any entrepreneur can sign up for BigQuery or Snowflake and have a data solution that can scale with their business in a matter of hours. The emergence of cheap, flexible and scalable data storage solutions was largely a response to changing needs spurred by the massive explosion of data.

Currently, the world produces 2.5 quintillion bytes of data daily (there are 18 zeros in a quintillion). The explosion of data continues in the roaring ‘20s, both in terms of generation and storage — the amount of stored data is expected to continue to double at least every four years. However, one integral part of modern data infrastructure still lacks solutions suitable for the Big Data era and its challenges: Monitoring of data quality and data validation.

Let me go through how we got here and the challenges ahead for data quality.

In 2005, Tim O’Reilly published his groundbreaking article “What is Web 2.0?”, truly setting off the Big Data race. The same year, Roger Mougalas from O’Reilly introduced the term “Big Data” in its modern context — referring to a large set of data that is virtually impossible to manage and process using traditional BI tools.

Back in 2005, one of the biggest challenges with data was managing large volumes of it, as data infrastructure tooling was expensive and inflexible, and the cloud market was still in its infancy (AWS didn’t publicly launch until 2006). The other was speed: As Tristan Handy from Fishtown Analytics (the company behind dbt) notes, before Redshift launched in 2012, performing relatively straightforward analyses could be incredibly time-consuming even with medium-sized data sets. An entire data tooling ecosystem has since been created to mitigate these two problems.

The emergence of the modern data stack (example logos and categories). Image Credits: Validio

Scaling relational databases and data warehouse appliances used to be a real challenge. Only 10 years ago, a company that wanted to understand customer behavior had to buy and rack servers before its engineers and data scientists could work on generating insights. Data and its surrounding infrastructure was expensive, so only the biggest companies could afford large-scale data ingestion and storage.

The challenge before us is to ensure that the large volumes of Big Data are of sufficiently high quality before they’re used.

Then came a (Red)shift. In October 2012, AWS presented the first viable solution to the scale challenge with Redshift — a cloud-native, massively parallel processing (MPP) database that anyone could use for a monthly price of a pair of sneakers ($100) — about 1,000x cheaper than the previous “local-server” setup. With a price drop of this magnitude, the floodgates opened and every company, big or small, could now store and process massive amounts of data and unlock new opportunities.

As Jamin Ball from Altimeter Capital summarizes, Redshift was a big deal because it was the first cloud-native OLAP warehouse and reduced the cost of owning an OLAP database by orders of magnitude. The speed of processing analytical queries also increased dramatically. And later on (Snowflake pioneered this), they separated computing and storage, which, in overly simplified terms, meant customers could scale their storage and computing resources independently.

What did this all mean? An explosion of data collection and storage.

Powered by WPeMatico

Here’s another edition of “Dear Sophie,” the advice column that answers immigration-related questions about working at technology companies.

“Your questions are vital to the spread of knowledge that allows people all over the world to rise above borders and pursue their dreams,” says Sophie Alcorn, a Silicon Valley immigration attorney. “Whether you’re in people ops, a founder or seeking a job in Silicon Valley, I would love to answer your questions in my next column.”

Extra Crunch members receive access to weekly “Dear Sophie” columns; use promo code ALCORN to purchase a one- or two-year subscription for 50% off.

Dear Sophie,

Our startup employs several individuals who are on work visas or have employment authorization. Many of them have been waiting for quite a while for the government to tell them their applications have been received.

Why? When will things be back on track? We have a few employees who are waiting for green cards, and a few F-1 visa holders who will be extending their OPT to STEM OPT.

Is there anything we can do?

— Patient in Pasadena

Dear Patient,

Thanks for your questions. Last September, an increase in applications submitted to U.S. Citizenship and Immigration Services (USCIS) amid COVID-19-related staff reductions created a substantial backlog and subsequent delay in USCIS sending out receipt notices.

My law firm partner, Anita Koumriqian, and I provided an update on receipt notices on a recent podcast. Dedicating an entire episode to receipt notices was unthinkable a year ago because applicants usually received receipt notices within one to three weeks after USCIS received their application.

For those who don’t know, USCIS sends a letter called a receipt notice to applicants when it receives an application. The receipt notice — also known as a Notice of Action or Form I-797 — contains information about:

Before the pandemic, applicants would typically be notified in less than one month after USCIS received their application. Currently, applicants are receiving their receipt notice as long as eight to nine weeks after USCIS received their application, and sometimes longer.

As I mentioned earlier, coronavirus-related staffing reductions at USCIS coupled with a substantial jump in the number of applications submitted prompted huge delays that began in September. Application submissions surged primarily due to:

Powered by WPeMatico

Bipartisanship has long been out of fashion, but one common pursuit among Democrats and Republicans in Washington has been placing Big Tech companies under a microscope.

Congressional committees have held scores of hearings, lawsuits have been filed and legislation has been introduced to regulate privacy and data collection. The knock-on effect of these reforms for young companies and their venture investors is unclear. But one aspect of increased antitrust scrutiny — restrictions on acquisitions — would have a significant negative effect on our entrepreneurial ecosystem, and policymakers should approach these changes with caution.

For VC-backed companies, there are effectively three outcomes: standalone company (often via an IPO), merger or acquisition, or bankruptcy. Despite best efforts, company failure is the most common outcome — more than 90% of startups fail. Fortunately, the success stories are often companies with a big impact, like Moderna and Zoom, which helped the world in the pandemic.

Acquisitions contribute to the health of the startup ecosystem, as entrepreneurs who realize liquidity through the sale of their company regularly go on to found innovative new companies and often invest in other startups as angel investors or venture capitalists.

Entrepreneurs are optimists by nature, and so when the company journey begins, there is great hope of one day creating a standalone public company. However, in most cases, an IPO is not possible. The reality is that entrepreneurship is incredibly hard, and the journey from infancy to public company is one that relatively few companies achieve.

Silicon Valley Bank’s 2020 Global Startup Outlook puts it this way: “[T]he fact is most entrepreneurs never expect to reach a public market exit.” Accordingly, 58% of startups expect to be acquired. NVCA-Pitchbook data on acquisitions and IPOs back up the sentiment of founders when it comes to likely exit opportunities. In 2020, there was an approximately 10:1 ratio of acquisitions of VC-backed companies to IPOs, with 1,042 venture-backed companies acquired and 103 entering the public markets.

Some might argue that acquisitions are more dominant today because of the anti-competitive motivations of current tech incumbents. But as Patricia Nakache of Trinity Ventures said in testimony before the Senate Judiciary Committee: “[Acquisitions have] been commonplace in the U.S. since before the dawn of the modern venture capital industry.” In fact, today we are witnessing fewer acquisitions relative to IPOs than in years past, as the average acquisition-to-IPO ratio since 2004 is approximately 15:1. This is happening against a backdrop of challenges in taking small-cap companies public that has reduced the number of companies in the public markets today.

Acquisitions contribute to the health of the startup ecosystem, as entrepreneurs who realize liquidity through the sale of their company regularly go on to found innovative new companies and often invest in other startups as angel investors or venture capitalists.

Furthermore, acquisitions help power the returns of VC funds, thereby allowing VCs to raise new funds and invest in the next generation of entrepreneurs. This “recycling effect” is one of the key drivers of dynamism in our economy and should not be slowed down.

Despite the importance of acquisitions, antitrust reform has included significant changes to how acquisitions are assessed by the federal government. The two most prominent examples in this space are Sen. Amy Klobuchar’s Competition and Antitrust Law Enforcement Reform Act (CALERA) and Sen. Josh Hawley’s Trust-Busting for the Twenty-First Century Act.

These bills are likely a reaction to findings that incumbents have acted like Pac-Man, gobbling up would-be competitors before they become a competitive problem. But both proposals would ultimately harm startup activity and competition rather than propel it.

A common thread between these proposals is to restrict acquisitions by companies valued at more than $100 billion. Hawley’s bill would impose an outright ban on acquisitions by companies of that market cap that “lessen competition in any way.”

Klobuchar’s bill would shift the burden of proof to parties to an acquisition, a major change because the U.S. government bears the burden currently. This means if the government challenges an acquisition in federal court, the parties to the acquisition must demonstrate it does not “create an appreciable risk of materially lessening competition.” If that standard is not met, the acquisition could be blocked.

Both proposals have negative ramifications for venture-backed companies.

First, consider the scope of the proposals: A $100 billion company is indeed a large one, but setting the threshold there captures far more than the large tech companies that have been hauled before Congress for antitrust hearings. Globally, about 150 companies are valued at $100 billion or more, and the U.S. is home to more than 80 of those companies. That exposes acquirers as wide-ranging as Estee Lauder, John Deere, Starbucks and Thermo Fisher Scientific. If you are struggling to recall those companies being under the antitrust spotlight, then you are not alone.

Second, the legal standards imposed by these new bills are daunting. Klobuchar’s proposal leaves startups scratching their heads on where the line is on which acquisitions are tolerated, while Hawley’s bill throws up a misguided red light for vast amounts of acquisitions. These two standards are particularly vexing since acquirers are generally looking for acquirees that complement their existing business. In addition, many of the most acquisitive companies are multifaceted ones that presumably compete with an array of other companies in some way.

Ultimately, the bills from Klobuchar and Hawley would disrupt an important part of our nation’s startup ecosystem. Acquisitions act like grease to help keep the wheels moving by injecting liquidity into the system so participants can move on to create new and hopefully better companies for our country. Those wheels should not be slowed down when the country needs all the entrepreneurship it can muster.

Powered by WPeMatico

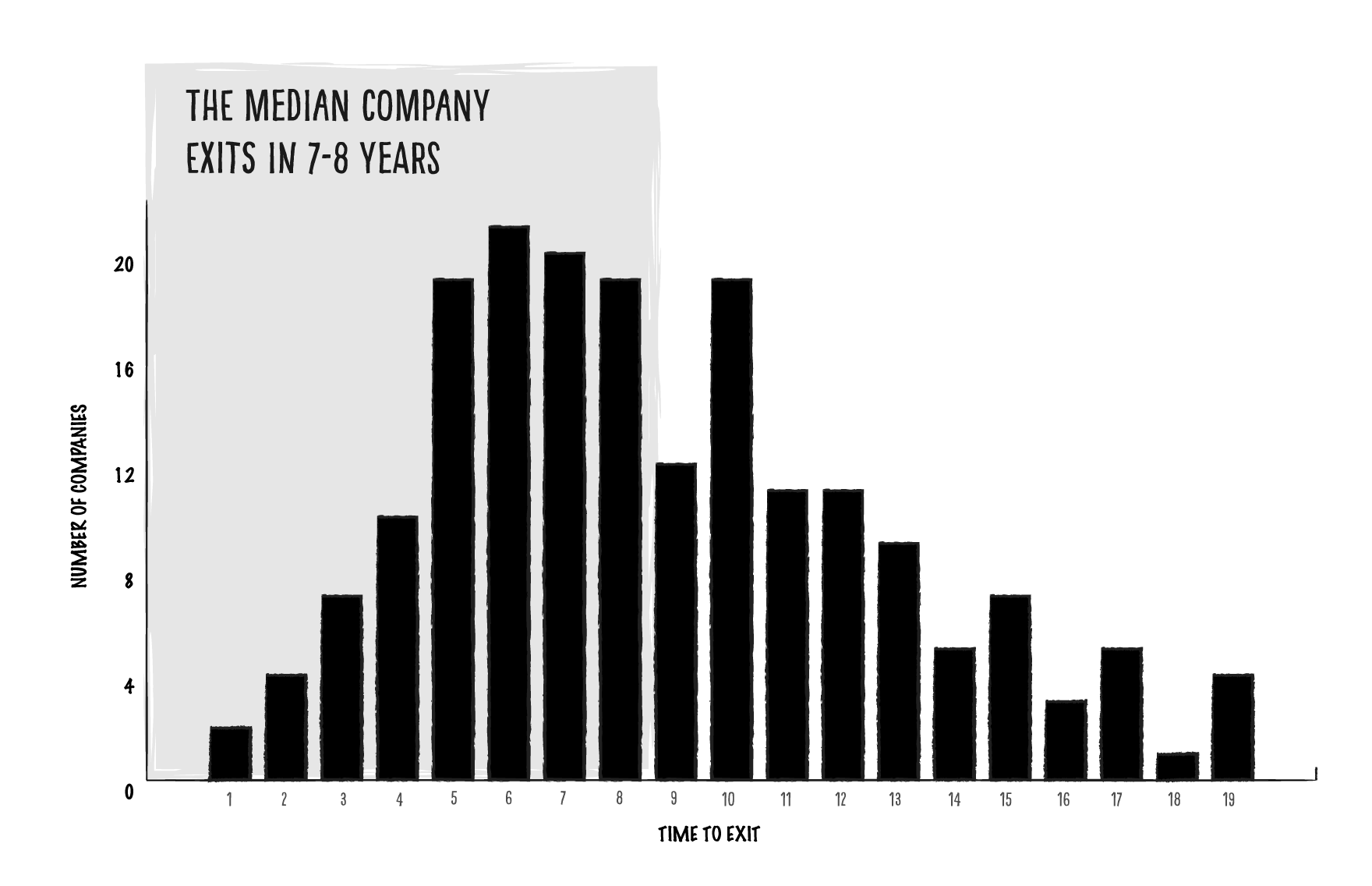

Does it really take an average of seven to eight years for a successful startup to exit? What can early-stage founders do to accelerate outcomes?

We wanted to know if founding teams can execute faster with a higher degree of success if they’re able to take advantage of relevant executive expertise. After all, that’s the thesis we built our venture model around — we purposefully designed M13 so that early-stage founders get access to experienced executives they wouldn’t otherwise have the money to hire or the time to vet, onboard and manage.

Even if companies are doing everything right, they still reduce time to exit when they have multiple founders with prior relevant experience as a senior leader or operator.

We looked at years of data from hundreds of successful startups. As it turns out, the impact of relevant executive expertise is even greater than we had anticipated — to the tune of doubling the rate of return on a venture investment.

When it comes to measuring leadership experience, information about an individual executive’s experience — for example, how long they’ve been an exec — is publicly available. Unfortunately, there isn’t readily available structured data around a founding team’s seniority and how early the founders bring on people with more experience as an operator or leader.

To find out if leadership experience significantly impacts startups’ success, we analyzed nearly 800 executives at more than 200 companies that reached a sizable exit (greater than or equal to a $500 million valuation) via an IPO on a U.S. exchange or an exit via M&A from 2004-2019. About 70% of the companies in our dataset exited between 2016-2019, including notable IPOs like Spotify, Zoom, Uber and Peloton. We decided to exclude companies in the biotech/life sciences space because these companies follow a different growth trajectory than consumer tech and B2B tech and traditionally exit via IPO or M&A at a much earlier stage.

Here’s what our analysis of startups with successful exits revealed.

While there are other intangible variables for startup success, the basic equation is the time and capital required to achieve an exit and the size of that exit.

Our dataset validates the widely accepted statement that successful exits take about seven to eight years:

Image Credits: M13

But could a variable like relevant leadership experience actually accelerate the time to exit? We wondered: Beyond time and capital, are there any factors — like experience as a leader or operator — that can have an exponential impact on the exit outcome? And when is the right time for those human capital resources to be introduced to make that impact?

Powered by WPeMatico

As the price of bitcoin hits record highs and cryptocurrencies become increasingly mainstream, the industry’s expanding carbon footprint becomes harder to ignore.

Just last week, Elon Musk announced that Tesla is suspending vehicle purchases using bitcoin due to the environmental impact of fossil fuels used in bitcoin mining. We applaud this decision, and it brings to light the severity of the situation — the industry needs to address crypto sustainability now or risk hindering crypto innovation and progress.

The market cap of bitcoin today is a whopping $1 trillion. As companies like PayPal, Visa and Square collectively invest billions in crypto, market participants need to lead in dramatically reducing the industry’s collective environmental impact.

As the price of bitcoin hits record highs and cryptocurrencies become increasingly mainstream, the industry’s expanding carbon footprint becomes harder to ignore.

The increasing demand for crypto means intensifying competition and higher energy use among mining operators. For example, during the second half of February, we saw the electricity consumption of BTC increase by more than 163% — from 265 TWh to 433 TWh — as the price skyrocketed.

Sustainability has become a topic of concern on the agendas of global and local leaders. The Biden administration rejoining the Paris climate accord was the first indication of this, and recently we’ve seen several federal and state agencies make statements that show how much of a priority it will be to address the global climate crisis.

A proposed New York bill aims to prohibit crypto mining centers from operating until the state can assess their full environmental impact. Earlier this year, the U.S. Securities and Exchange Commission put out a call for public comment on climate disclosures as shareholders increasingly want information on what companies are doing in this regard, while Treasury Secretary Janet Yellen warned that the amount of energy consumed in processing bitcoin is “staggering.” The United Kingdom announced plans to reduce greenhouse gas emissions by at least 68% by 2030, and the prime minister launched an ambitious plan last year for a green industrial revolution.

Crypto is here to stay — this point is no longer up for debate. It is creating real-world benefits for businesses and consumers alike — benefits like faster, more reliable and cheaper transactions with greater transparency than ever before. But as the industry matures, sustainability must be at the center. It’s easier to build a more sustainable ecosystem now than to “reverse engineer” it at a later growth stage. Those in the cryptocurrency markets should consider the auto industry a canary: Carmakers are now retrofitting lower-carbon and carbon-neutral solutions at great cost and inconvenience.

Market participants need to actively work together to realize a low-emissions future powered by clean, renewable energy. Last month, the Crypto Climate Accord (CCA) launched with over 40 supporters — including Ripple, World Economic Forum, Energy Web Foundation, Rocky Mountain Institute and ConsenSys — and the goal to enable all of the world’s blockchains to be powered by 100% renewables by 2025.

Some industry participants are exploring renewable energy solutions, but the larger industry still has a long way to go. While 76% of hashers claim they are using renewable energy to power their activities, only 39% of hashing’s total energy consumption comes from renewables.

To make a meaningful impact, the industry needs to come up with a standard that’s open and transparent to measure the use of renewables and make renewable energy accessible and cheap for miners. The CCA is already working on such a standard. In addition, companies can pay for high-quality carbon offsets for remaining emissions — and perhaps even historical ones.

While the industry works to become more sustainable long term, there are green choices that can be made now, and some industry players are jumping on board. Fintechs like Stripe have created carbon renewal programs to encourage its customers and partners to be more sustainable.

Companies can partner with organizations, like Energy Web Foundation and the Renewable Energy Business Alliance, to decarbonize any blockchain. There are resources for those who want to access renewable energy sources and high-quality carbon offsets. Other options include using inherently low-carbon technologies, like the XRP Ledger, that don’t rely on proof-of-work (which involves mining) to help significantly reduce emissions for blockchains and cryptofinance.

The XRP Ledger is carbon-neutral and uses a validation and security algorithm called Federated Consensus that is approximately 120,000 times more energy-efficient than proof-of-work. Ethereum, the second-largest blockchain, is transitioning off proof-of-work to a much less energy-intensive validation mechanism called proof-of-stake. Proof-of-work systems are inefficient by design and, as such, will always require more energy to maintain forward progress.

The devastating impact of climate change is moving at an alarming speed. Making aspirational commitments to sustainability — or worse, denying the problem — isn’t enough. As with the Paris agreement, the industry needs real targets, collective action, innovation and shared accountability.

The good news? Solutions can be practical, market-driven and create value and growth for all. Together with climate advocates, clean tech industry leaders and global finance decision-makers, crypto can unite to position blockchain as the most sustainable path forward in creating a green, digital financial future.

Powered by WPeMatico

In 2011, a product developer named Fred Davison read an article about inventor Ken Yankelevitz and his QuadControl video game controller for quadriplegics. At the time, Yankelevitz was on the verge of retirement. Davison wasn’t a gamer, but he said his mother, who had the progressive neurodegenerative disease ALS, inspired him to pick up where Yankelevitz was about to leave off.

Launched in 2014, Davison’s QuadStick represents the latest iteration of the Yankelevitz controller — one that has garnered interest across a broad range of industries.

“The QuadStick’s been the most rewarding thing I’ve ever been involved in,” Davison told TechCrunch. “And I get a lot of feedback as to what it means for [disabled gamers] to be able to be involved in these games.”

Erin Muston-Firsch, an occupational therapist at Craig Hospital in Denver, says adaptive gaming tools like the QuadStick have revolutionized the hospital’s therapy team.

Six years ago, she devised a rehabilitation solution for a college student who came in with a spinal cord injury. She says he liked playing video games, but as a result of his injury could no longer use his hands. So the rehab regimen incorporated Davison’s invention, which enabled the patient to play World of Warcraft and Destiny.

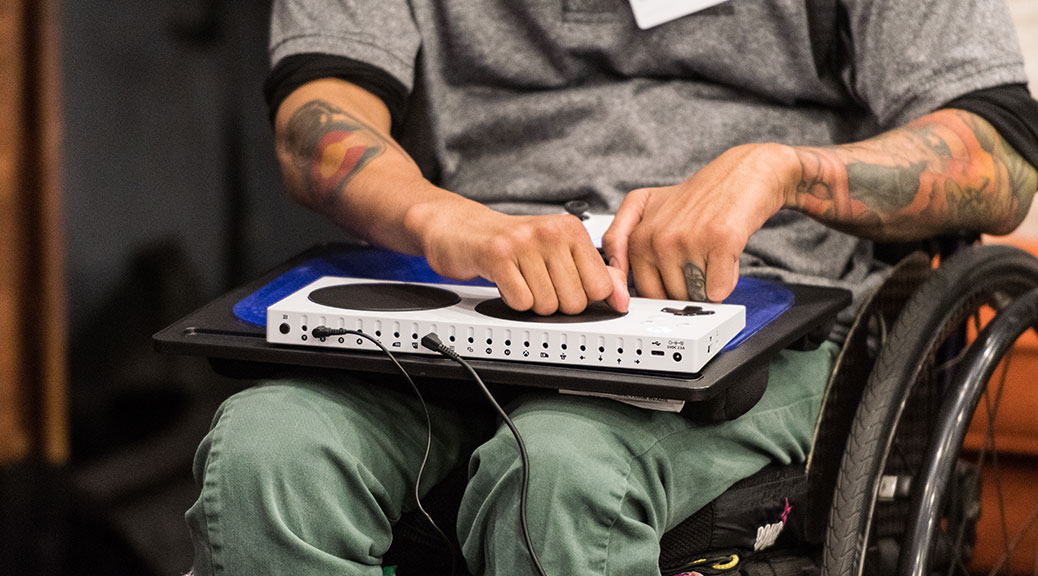

QuadStick

Jackson “Pitbull” Reece is a successful Facebook streamer who uses his mouth to operate the QuadStick, as well as the XAC, (the Xbox Adaptive Controller), a controller designed by Microsoft for use by people with disabilities to make user input for video games more accessible.

Reece lost the use of his legs in a motorcycle accident in 2007 and later, due to an infection, his hands and legs were amputated. He says he remembers able-bodied life as one filled with mostly sports video games. He says being a part of the gaming community is an important part of his mental health.

Fortunately there is an atmosphere of collaboration, not competition, around the creation of hardware for gamers within the assistive technology community.

But while not every major tech company has been proactive about accessibility, after-market devices are available to create customized gaming experiences for disabled gamers.

At its Hackathon in 2015, Microsoft’s Inclusive Lead Bryce Johnson met with disabled veterans’ advocacy group Warfighter Engaged.

“We were at the same time developing our views on inclusive design,” Johnson said. Indeed, eight generations of gaming consoles created barriers for disabled gamers.

“Controllers have been optimized around a primary use case that made assumptions,” Johnson said. Indeed, the buttons and triggers of a traditional controller are for able-bodied people with the endurance to operate them.

Besides Warfighter Engaged, Microsoft worked with AbleGamers (the most recognized charity for gamers with disabilities), Craig Hospital, the Cerebral Palsy Foundation and Special Effect, a U.K.-based charity for disabled young gamers.

Xbox Adaptive Controller

The finished XAC, released in 2018, is intended for a gamer with limited mobility to seamlessly play with other gamers. One of the details gamers commented on was that the XAC looks like a consumer device, not a medical device.

“We knew that we couldn’t design this product for this community,” Johnson told TechCrunch. “We had to design this product with this community. We believe in ‘nothing about us without us.’ Our principles of inclusive design urge us to include communities from the very beginning.”

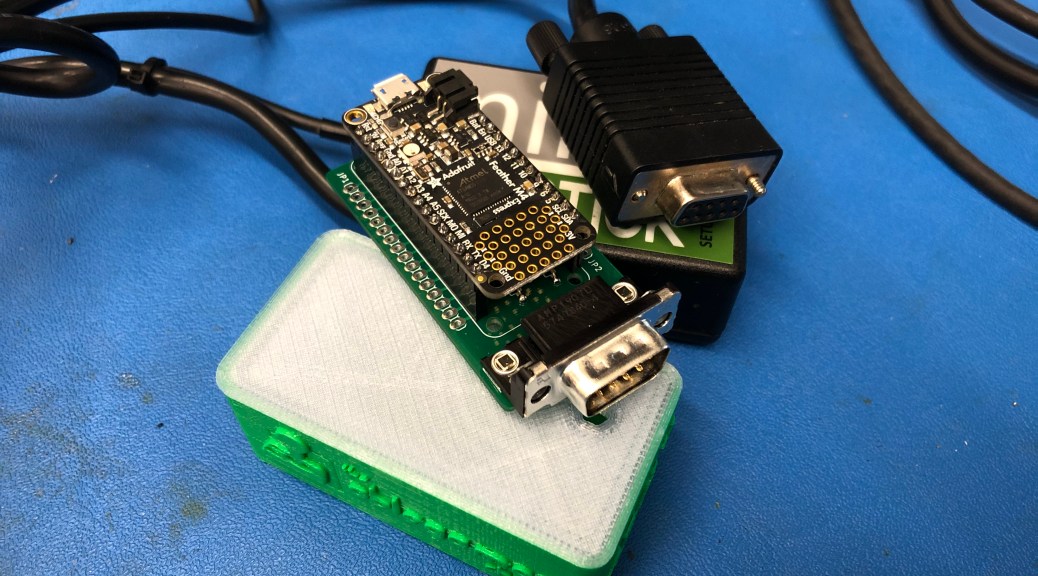

There were others getting involved. Like many inventions, the creation of the Freedom Wing was a bit of serendipity.

At his booth at an assistive technology (AT) conference, ATMakers‘ Bill Binko showcased a doll named “Ella” using the ATMakers Joystick, a power-chair device. Also in attendance was Steven Spohn, who is part of the brain trust behind AbleGamers.

Spohn saw the Joystick and told Binko he wanted a similar device to work with the XAC. The Freedom Wing was ready within six weeks. It was a matter of manipulating the sensors to control a game controller instead of a chair. This device didn’t require months of R&D and testing because it had already been road tested as a power-chair device.

ATMakers Freedom Wing 2

Binko said mom-and-pop companies are leading the way in changing the face of accessible gaming technology. Companies like Microsoft and Logitech have only recently found their footing.

ATMakers, QuadStick and other smaller creators, meanwhile, have been busy disrupting the industry.

“Everybody gets [gaming] and it opens up the ability for people to engage with their community,” Binko said. “Gaming is something that people can wrap their heads around and they can join in.”

As the technology evolves, so do the obstacles to accessibility. These challenges include lack of support teams, security, licensing and VR.

Binko said managing support teams for these devices with the increase in demand is a new hurdle. More people with the technological skills are needed to join the AT industry to assist with the creation, installation and maintenance of devices.

Security and licensing is out of the hands of small creators like Davison because of financial and other resources needed to work with different hardware companies. For example, Sony’s licensing enforcement technology has become increasingly complex with each new console generation.

With Davison’s background in tech, he understands the restrictions to protect proprietary information. “They spend huge amounts of money developing a product and they want to control every aspect of it,” Davison said. “Just makes it tough for the little guy to work with.”

And while PlayStation led the way in button mapping, according to Davison, the security process is stringent. He doesn’t understand how it benefits the console company to prevent people from using whichever controller they want.

“The cryptography for the PS5 and DualSense controller is uncrackable so far, so adapter devices like the ConsoleTuner Titan Two have to find other weaknesses, like the informal ‘man in the middle’ attack,” Davison said.

The technique allows devices to utilize older-gen PlayStation controllers as a go-between from the QuadStick to the latest-gen console, so disabled gamers can play the PS5. TechCrunch reached out to Sony’s accessibility division, whose representative said there are no immediate plans for an adaptable PlayStation or controller. However, they stated their department works with advocates and gaming devs to consider accessibility from day one.

In contrast, Microsoft’s licensing system is more forgiving, especially with the XAC and the ability to use older-generation controllers with newer systems.

“Compare the PC industry to the Mac,” Davison said. “You can put together a PC system from a dozen different manufacturers, but not for the Mac. One is an open standard and the other is closed.”

In November, Japanese controller company HORI released an officially licensed accessibility controller for the Nintendo Switch. It’s not available for sale in the United States currently, but there are no region restrictions to purchase one online. This latest development points toward a more accessibility-friendly Nintendo, though the company has yet to fully embrace the technology.

Nintendo’s accessibility department declined a full interview but sent a statement to TechCrunch. “Nintendo endeavors to provide products and services that can be enjoyed by everyone. Our products offer a range of accessibility features, such as button-mapping, motion controls, a zoom feature, grayscale and inverted colors, haptic and audio feedback, and other innovative gameplay options. In addition, Nintendo’s software and hardware developers continue to evaluate different technologies to expand this accessibility in current and future products.”

The push for more accessible hardware for disabled gamers hasn’t been smooth. Many of these devices were created by small business owners with little capital. In a few cases corporations with a determination for inclusivity at the earliest stages of development became involved.

Slowly but surely, however, assistive technology is moving forward in ways that can make the experience much more accessible for gamers with disabilities.

Powered by WPeMatico

Whether you’re building a company or thinking about investing, it’s important to understand your strategic advantage. In order to determine one, you should ask fundamental questions like: What’s the long-term, sustainable reason that the company will stay in business?

The most important elements for founders to consider when figuring out their strategic advantage(s) include one-sided or “direct” network effects (e.g., with social media sites like Facebook), marketplace network effects (e.g., with two-sided marketplaces like Uber), data moats, first mover and switching costs.

Let’s take a quick look at an example of one-sided network effects. At the very earliest stages of Facebook’s existence, it was just Mark Zuckerberg, a few friends and their basic profiles. The nascent social media platform wasn’t useful beyond a few dorm rooms. They needed a strategic advantage or the company would not make it beyond the edge of campus.

A successful startup without a strategic advantage is just a validated business model vulnerable to copycat companies looking for a market entry point.

In fact, Facebook only truly became a useful platform — and accelerated as a business — when more users came into the fold and more types of email addresses were accepted. Add to that the introduction of an ad marketplace revenue model and you have a clear strategic advantage — based on one-sided network effects — that gave Facebook a strategic edge over other early social media sites like MySpace.

These one-sided network effects are different from two-sided network effects.

Image Credits: Canvas Ventures

Two-sided network effects are most common in marketplace business models. In a two-sided network, supply and demand are matched, like Uber riders (demand) being matched with Uber drivers (supply). The Uber product is not necessarily more valuable just because more users (riders) join, the way Facebook is more valuable when more users join.

In fact, when more users (riders) join the demand side of the Uber network, it might actually be worse for the user experience — it’s harder to find a driver and wait times get longer. The demand side (riders) gets value from more supply (drivers) joining the platform and vice-versa. That’s why it’s called a two-sided network, or a marketplace.

Regardless of industry, a successful startup without a strategic advantage is just a validated business model vulnerable to copycat companies looking for a market entry point. Copycats can range in size from startups with similar grit to large companies like Facebook or Google that have limitless resources to drive competition into the market, and potentially run the startup with the original idea out of business. This vulnerability can prove fatal unless a startup’s founding team explores and embraces one or more strategic advantages.

Powered by WPeMatico

There’s a lot of noise out there. The ability to effectively communicate can make or break your launch. It will play a role in determining who wins a new space — you or a competitor.

Most people get that. I get emails every week from companies coming out of stealth mode, wanting to make a splash. Or from a Series B company that’s been around for a while and hopes to improve their branding/messaging/positioning so that a new upstart doesn’t eat their lunch.

You have to stop thinking that what you are up to is interesting.

How do you make a splash? How do you stay relevant?

Worth noting is that my area of expertise is in the DevOps space and that slant may crop up occasionally. But these five specific tips should be applicable to virtually any startup.

This is especially important if you are a small startup that not many people know about. Journalists don’t want to hear opinions from your head of marketing or product — they want to hear from the founders. What problems are they solving? What unique opinions do they have about the market? These are insights that mean the most coming from the people that started the company. So if you don’t have at least one founder that can dedicate time to being the face, then PR is going to be an uphill battle.

That doesn’t mean there isn’t plenty to do to support these efforts. Create a list of all the journalists that have written about your competitors. Read those articles. How can your founder add value to these conversations? Where should you be contributing thought leadership? What are the most interesting perspectives you can offer to those audiences?

This is legwork and research you can do before looping founders into the conversation. Getting your PR going can be like trying to push a broken-down car up the road: If the founders see you exerting effort to get things moving on your own, they’re more likely to get beside you and help.

Here’s an example: It may be unreasonable to ask a founder to sit down and write a 1,000-word thought leadership piece by the end of the week, but they very likely have 20 minutes to chat, especially if you make it clear that the contents of the conversation will make for great thought leadership pieces, social media posts, etc.

The flow looks like:

Powered by WPeMatico