Column

Auto Added by WPeMatico

Auto Added by WPeMatico

No single question bedevils American energy and environmental policy more than nuclear waste. No, not even a changing climate, which may be a wicked problem but nonetheless receives a great deal of counter-bedeviling attention.

It’s difficult to paint the picture with a straight face. Let’s start with three main elements of the story.

First, nuclear power plants in the United States generate about 2,000 metric tons of nuclear waste (or “spent fuel”) per year. Due to its inherent radioactivity, it is carefully stored at various sites around the country.

Second, the federal government is in charge of figuring out what to do with it. In fact, power plant operators have paid over $40 billion into the Nuclear Waste Fund so that the government can handle it. The idea was to bury it in the “deep geological repository” embodied by Yucca Mountain, Nevada, but this has proved politically impossible. Nevertheless, $15 billion was spent on the scoping.

Third, due to the Energy Department’s inability to manage this waste, it simply accumulates. According to that agency’s most recent data release, some 80,000 metric tons of spent fuel—hundreds of thousands of fuel assemblies containing millions of fuel rods—is waiting for a final destination.

And here’s the twist ending: those nuclear plant operators sued the government for breach of contract and, in 2013, they won. Several hundred million dollars is now paid out to them each year by the U.S. Treasury, as part of a series of settlements and judgments. The running total is over $8 billion.

I realize this story sounds a little crazy. Am I really saying that the U.S. government collected billions of dollars to manage nuclear waste, then spent billions of dollars on a feasibility study only to stick it on the shelf, and now is paying even more billions of dollars for this failure? Yes, I am.

Fortunately, all of the aggregated waste occupies a relatively small area and temporary storage exists. Without an urgent reason to act, policymakers generally will not.

While attempts to find long-term storage will continue, policymakers should look towards recycling some of this “waste” into usable fuel. This is actually an old idea. Only a small fraction of nuclear fuel is consumed to generate electricity.

Proponents of recycling envision reactors that use “reprocessed” spent fuel, extracting energy from the 90% of it leftover after burn-up. Even its critics admit that the underlying chemistry, physics, and engineering of recycling are technically feasible, and instead assail the disputable economics and perceived security risks.

So-called Generation IV reactors come in all shapes and sizes. The designs have been around for years—in some respects, all the way back to the dawn of nuclear energy—but light-water reactors have dominated the field for a variety of political, economic, and strategic reasons. For example, Southern Company’s twin conventional pressurized water reactors under construction in Georgia each boast a capacity of just over 1,000-megawatt (or 1 gigawatt), standard for Westinghouse’s AP 1000 design.

In contrast, next-generation plant designs are a fraction of the size and capacity, and also may use different cooling systems: Oregon-based NuScale Power’s 77-megawatt small modular reactor, San Diego-based General Atomics’ 50-megawatt helium-cooled fast modular reactor, Alameda-based Kairos Power’s 140-megawatt molten fluoride salt reactor, and so on all have different configurations that can fit different business and policy objectives.

Many Gen-IV designs can either explicitly recycle used fuel or be configured to do so. On June 3, TerraPower (backed by Bill Gates), GE Hitachi, and the State of Wyoming announced an agreement to build a demonstration of the 345-megawatt Natrium design, a sodium-cooled fast reactor.

Natrium is technically capable of recycling fuel for generation. California-based Oklo has already reached an agreement with Idaho National Laboratory to operate its 1.5-megawatt “microreactor” off of used-fuel supplies. In fact, the self-professed “preferred fuel” for New York-based Elysium Industries’ molten salt reactor design is spent nuclear fuel and Alabama-based Flibe Energy advertises the waste-burning capability of its thorium reactor design.

Whether advanced reactors rise or fall does not depend on resolving the nuclear waste deadlock. Though such reactors may be able to consume spent fuel, they don’t necessarily have to. Nonetheless, incentivizing waste recycling would improve their economics.

“Incentivize” here is code for “pay.” Policymakers should consider ways that Washington can make it more profitable for a power plant to recycle fuel than to import it—from Canada, Kazakhstan, Australia, Russia, and other countries.

Political support for advanced nuclear technology, including recycling, is deeper than might be expected. In 2019, the Senate confirmed Dr. Rita Baranwal as the Assistant Secretary for Nuclear Energy at the Department of Energy (DOE). A materials scientist by training, she emerged as a champion of recycling.

The new Biden administration has continued broadly bipartisan support for advanced nuclear reactors in proposing in its Fiscal Year 2022 Budget Request to increase funding for the DOE’s Office of Nuclear Energy by nearly $350 million. The proposal includes specific funding increases for researching and developing reactor concepts (plus $32 million), fuel cycle R&D (plus $59 million), and advanced reactor demonstration (plus $120 million), and tripling funding for the Versatile Test Reactor (from $45 million to $145 million, year over year).

In May, the DOE’s Advanced Research Projects Agency-Energy (ARPA-E) announced a new $40 million program to support research in “optimizing” waste and disposal from advanced reactors, including through waste recycling. Importantly, the announcement explicitly states that the lack of a solution to nuclear waste today “poses a challenge” to the future of Gen-IV reactors.

The debate is a reminder that recycling in general is a very messy process. It is chemical-, machine-, and energy-intensive. Recycling of all kinds, from critical minerals to plastic bottles, produces new waste, too. Today, federal and state governments are quite active in recycling these other waste streams, and they should be equally involved in nuclear waste.

Powered by WPeMatico

“Who should my first marketing hire be?”

This is (by far) the most common question I’ve received since starting as Fuel’s CMO, and for good reason. Your first marketer will have an outsized impact on team dynamics as well as the overall strategic direction of the brand, product and company.

The nature of the marketing function has expanded significantly over the past two decades. So much so that when founders ask this question, it immediately prompts multiple new ones: Should I hire a brand or growth marketer? An offline or an online marketer? A scientific or a creative marketer?

Once upon a time, the number of marketing channels was fairly limited, which meant the function itself fit into a neater, tighter box. The number of ways to reach customers has since grown exponentially, as has the scope of the marketing role. Today’s startups require at least four broad functions under the umbrella of “marketing,” each with its own array of subfunctions.

The reality is that anyone who excels across all marketing functions is a unicorn and nearly impossible to find.

Here’s a sample of the marketing functions at a typical early-stage startup:

Brand marketing: Brand strategy, positioning, naming, messaging, visual identity, experiential, events, community.

Product marketing: UX copy, website, email marketing, customer research and segmentation, pricing.

Communications: PR and media relations, content marketing, social media, thought leadership, influencer.

Growth marketing: Direct response paid acquisition, funnel optimization, retention, lifecycle, engagement, reporting and attribution, word of mouth, referral, SEO, partnerships.

Have you worked with a talented individual or agency who helped you find and keep more users?

Respond to our survey and help us find the best startup growth marketers!

As you can imagine, that’s a lot for one person to manage, let alone be an expert in. What’s more, the skill set and experience required to excel in growth marketing is quite different from the skill set required to succeed in brand marketing. The reality is that anyone who excels across all marketing functions is a unicorn and nearly impossible to find.

Unless you’re lucky enough to nab that unicorn, your first hire should be a generalist who can tend to the full stack of the marketing function, learn what they don’t know, and roll up their sleeves to get things done. Someone smart, savvy and super scrappy who understands how to experiment across marketing channels until they find the right mix.

But this utility player should also bring deeper expertise in one of the big marketing functions: brand, product, communications or growth. Before making this key hire, you need to figure out which marketing priorities are most urgent and, consequently, which marketing “persona” is most appropriate for your business at the earliest stages.

To figure out which skill set you need most in-house, consider these five questions:

If you’ve done some marketing experimentation previously, have there been any bright spots? Which channels are proving the most efficient from a customer acquisition, conversion, retention, engagement, whatever your key KPI is, perspective? If you find a promising area, find a candidate that has expertise in it. For example, if you are seeing good results with Instagram ads, hiring a candidate who has expertise in growth marketing makes sense.

If you don’t have much data from channel testing, consider how your target customers are currently finding competitive products or services. At TaskRabbit, we knew from early customer research that clients were finding help with home services either through recommendations from friends or by asking Google (i.e., SEO and SEM).

So, that was a natural place for us to start. Our focus from a resource and staffing perspective in the early days was on growth marketing — driving more word of mouth, plus optimizing our SEO and SEM.

How competitive is the category you’re playing in? Are there dominant players with strong brands? Do these brands have endless marketing budgets? Are CACs exorbitant because well-capitalized competitors are outbidding each other? If so, you might want to focus on building an exceptional brand and product/customer experience.

That means disseminating a unique story through organic channels (word of mouth, PR, influencers and organic social media). A brand marketer or someone with deep PR and communications experience makes sense in this scenario.

Another aspect to consider is the skills the founder(s) — or other members of the founding/early team — bring to the table. If a founder has a strong vision for the brand and extensive experience building brands, then focus less on a brand marketing hire and rather supplement the branding skill set with another marketing priority (i.e., product marketing). Likewise, if a founder has a strong vision for the brand but no one on the team knows how to build one, that’s a skill gap that your first marketing hire should fill.

Trust building has become an increasingly important aspect for brands as customers become more and more discerning. But trust building tends to be more critical in certain areas than others: New, nascent industries or markets, sectors with a lot of human interaction (services businesses, dating platforms, etc.), industries that are fundamentally changing consumer behavior (ride-sharing in its earliest days), or industries where the stakes or cost is relatively high (luxury goods).

If trust building is critical, consider a branding expert who understands how to build trust and credibility, and build an experience that consumers are passionate about. This person will likely have deep expertise in PR and brand building, as these channels tend to inspire the most trust among consumers.

Once you’ve answered these five questions, you should have a pretty good idea of the type of marketing experience you want. But just how much experience should that person have? I typically recommend that seed-stage founders look for senior manager or director-level candidates at midsized companies.

At this experience level (six to 10 years), these candidates’ salaries tend to be more in line with a young company’s budget. Moreover, at this stage of their career, they tend to be both strategic and tactical. This means they can level up and think strategically about the business and the marketing function, but they are also happy to get their hands dirty and execute — actually dive into the Facebook platform and create ads, plan and host an event, or pitch a journalist.

Powered by WPeMatico

When I was at Open Market in the 1990s, our CEO gave out the recently published book “Crossing the Chasm” to the executive team and told us to read it to gain insight into why we had hit a speed bump in our scaling. We had gone from zero to $60 million in revenue in four years, went public at a billion-dollar market cap, and then stalled.

We found ourselves stuck in what author Geoffrey Moore called “the chasm,” a difficult transition from visionary early adopters who are willing to put up with an incomplete product and mainstream customers who demand a more complete product. This framework for marketing technology products has been one of the canonical foundational concepts to product-market fit for the three decades since it was first published in 1991.

Why is it that in recent years, wild-eyed optimistic VCs and entrepreneurs keep undershooting market size across the tech and innovation sector?

I have been reflecting on why it is that we venture capitalists and founders keep making the same mistake over and over again — a mistake that has become even more glaring in recent years. Despite our exuberant optimism, we keep getting the potential market size wrong. Market sizes have proven to be much, much larger than any of us had ever dreamed. The reason? Today, everyone aspires to be an early adopter. Peter Drucker’s mantra — innovate or die — has finally come to pass.

A glaring example in our investment portfolio is database software company MongoDB. Looking back at our Series A investment memo for this disruptive open-source, NoSQL database startup, I was struck that we boldly predicted the company had the opportunity to disrupt a subsegment of the industry and successfully take a piece of a market that could grow as large as $8 billion in annual revenue in future years.

Today, we realize that the company’s product appeals to the vast majority of the market, one that is forecast to be $68 billion in 2020 and approximately $106 billion in 2024. The company is projected to hit a $1 billion revenue run rate next year and, with that expanded market, likely has continued room to grow for many years to come.

Another example is Veeva, a vertical software company initially focused on the pharmaceutical industry. When we met the company for their Series A round, they showed us the classic hockey stick slide, claiming they would reach $50 million in revenue in five years.

We got over our concerns about market size when we and the founders concluded they could at least achieve a few hundred million in revenue on the backs of pharma and then expand to other vertical industries from there. Boy, were we wrong! The company filed their S-1 after that fifth year showing $130 million in revenue, and today the company is projected to hit $2 billion in revenue run rate next year, all while still remaining focused on just the pharma industry.

Veeva was a pioneer in “vertical SaaS” — software platforms that serve niche industries — which in recent years has become a popular category. Another vertical SaaS example is Squire, a company my partner Jesse Middleton angel invested in as part of a pre-seed round before he joined Flybridge.

Powered by WPeMatico

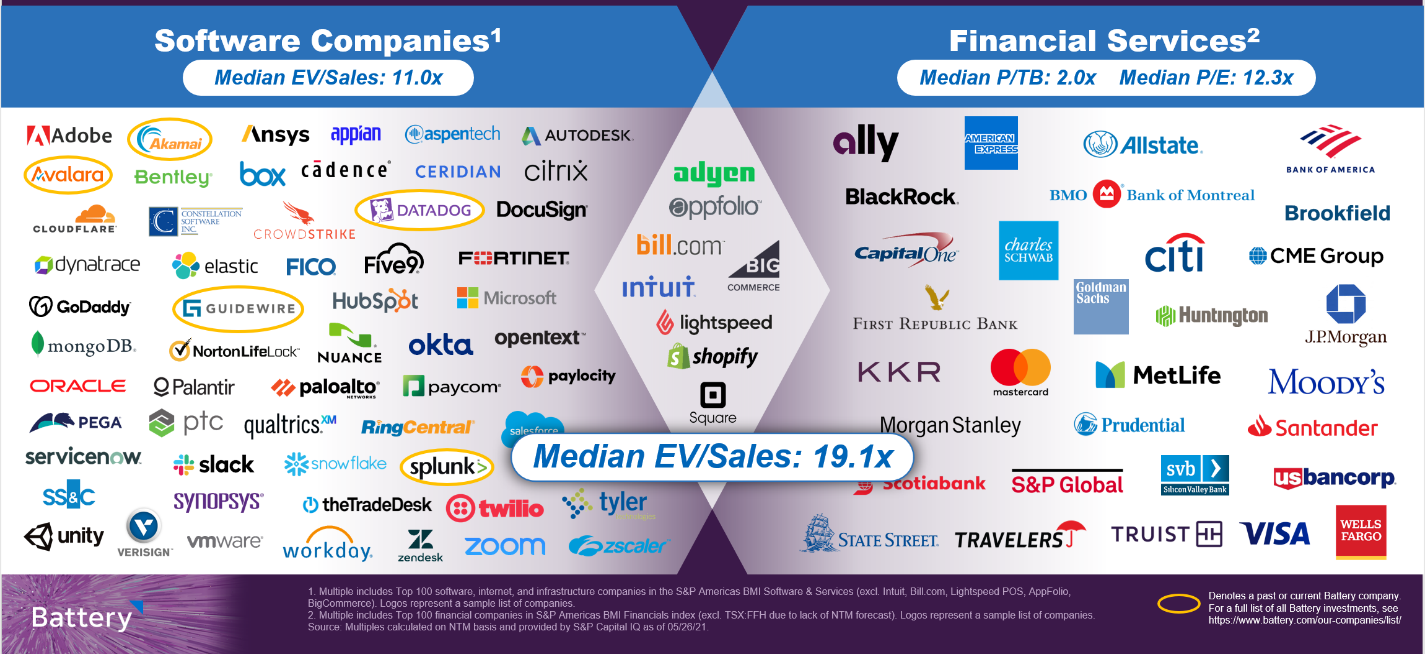

If money is the ultimate commodity, how can fintechs — which sell money, move money or sell insurance against monetary loss — build products that remain differentiated and create lasting value over time?

And why are so many software companies — which already boast highly differentiated offerings and serve huge markets— moving to offer financial services embedded within their products?

A new and attractive hybrid category of company is emerging at the intersection of software and financial services, creating buzz in the investment and entrepreneurial communities, as we discussed at our “Fintech: The Endgame” virtual conference and accompanying report this week.

These specialized companies — in some cases, software companies that also process payments and hold funds on behalf of their customers, and in others, financial-first companies that integrate workflow and features more reminiscent of software companies — combine some of the best attributes of both categories.

Image Credits: Battery Ventures

From software, they design for strong user engagement linked to helpful, intuitive products that drive retention over the long term. From financials, they draw on the ability to earn revenues indexed to the growth of a customer’s business.

Fintech is poised to revolutionize financial services, both through reinventing existing products and driving new business models as financial services become more pervasive within other sectors.

The powerful combination of these two models is rapidly driving both public and private market value as investors grant these “super” companies premium valuations — in the public sphere, nearly twice the median multiple of pure software companies, according to a Battery analysis.

The near-perfect example of this phenomenon is Shopify, the company that made its name selling software to help business owners launch and manage online stores. Despite achieving notable scale with this original SaaS product, Shopify today makes twice as much revenue from payments as it does from software by enabling those business owners to accept credit card payments and acting as its own payment processor.

The combination of a software solution indexed to e-commerce growth, combined with a profitable payments stream growing even faster than its software revenues, has investors granting Shopify a 31x multiple on its forward revenues, according to CapIQ data as of May 26.

Before even talking about how investors should value these hybrid companies, it’s worth making the point that in both private and public markets, fintechs have been notoriously hard to value, fomenting controversy and debate in the investment community.

Powered by WPeMatico

On Earth Day, April 22, SOSV published the SOSV Climate Tech 100, a list of the best startups that we’ve supported from their earliest stages to address climate change. There are always valuable insights embedded in a list like the 100. A TechCrunch story captured the investment perspective, and an SOSV post went deeper into the companies’ category breakdown and founder profiles.

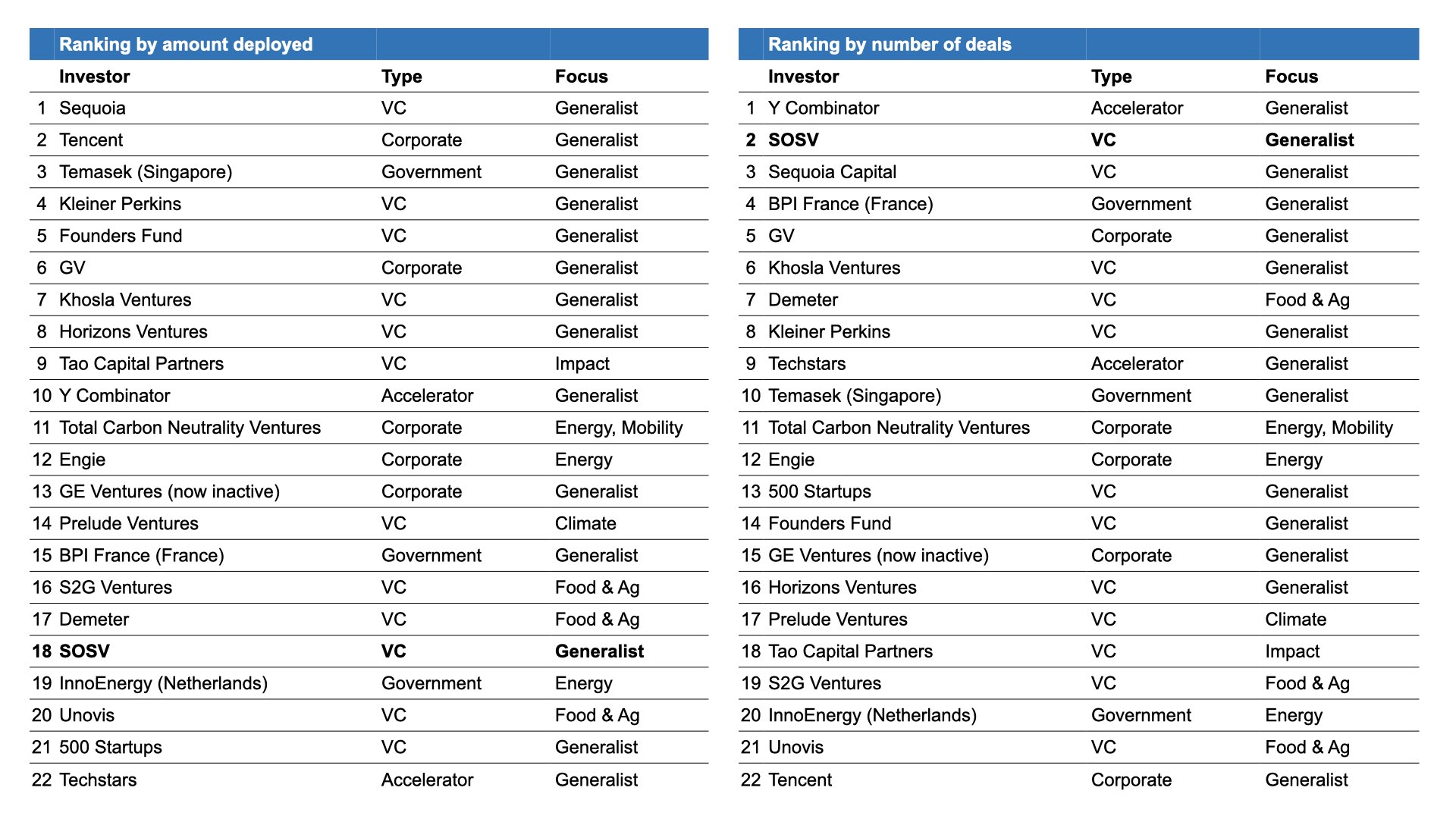

But what can founders learn from the list about climate tech investors? In other words, who invested in the Climate Tech 100? We dug into the “who’s who” of the list, which had more than 500 investors, and here’s what we found.

If you think 500 investors in 100 companies is a lot of investors, you’re right. There are clearly a lot of investors interested in climate tech, and most are generalists just testing the waters. For the Climate Tech 100, about 10% of investors put their money in more than one startup and only seven (less than 2%) wrote a check to four or more. These included Blue Horizon, CPT Capital, EF, Fifty Years, Hemisphere Ventures and Horizons Ventures.

That pattern tracks well with data from PwC, which found that 2,700 unique investors had backed 1,200 startups in its State of Climate Tech 2020 report covering the 2013-2019 period. The report found that only 10 firms out of 2,700 made four or more climate tech deals per year, on average, over the 2013-2019 period. The most active firms are listed in the table below.

Image Credits: PwC, 2020; additional research by SOSV

Capital deployed in climate tech grew at five times the venture capital overall growth rate over the 2013-2019 period.

There is reason to believe that the fragmentation will diminish with the launch of more funds focused on climate tech. Four funds worth more than a billion dollars each have launched since 2020 that fit the description (see chart below).

It’s also encouraging to see that capital deployed in climate tech grew at five times the venture capital overall growth rate over the 2013-2019 period.

Even so, climate tech still only represented 6% of total venture capital deployed in 2019, so there is plenty of room to grow.

Powered by WPeMatico

Running a startup can be a complicated, difficult process fraught with pitfalls and ample opportunities to make mistakes. But the logistics of setting up a startup should be simple, because over the long run, complicated equity setups and cap tables cost more money in legal fees and administration time.

The logistics of setting up a startup should be simple, because over the long run, complicated equity setups and cap tables cost more money in legal fees and administration time.

My company, Pulley, has helped more than a thousand founders build their cap table and equity structure.

Here’s a tactical guide to get your startup running in just four days.

It is now standard to incorporate your company at the seed stage itself. In the U.S., startups incorporate as Delaware C Corporations with 10 million authorized shares. This is the standard setup when you use services like Stripe Atlas or Clerky.

Post incorporation, you need to answer a few questions on how to grant equity to founders and future employees.

First, you should determine how you want to split the equity between the founders. There is no standard for doing so — some founders split shares equally, while others do 49/51 splits for control. Some founders even may have an 80/20 equity split because one founder spent an extra year on the idea.

At the end of the day, a good equity split is one that all founders find fair. If you can’t agree on a structure, you should have a deeper discussion on whether this is the right team to work with for the next decade or more.

Powered by WPeMatico

Every time there is a rumor of a Google algorithm update, a general panic ripples through the SEO community. There is a collective holding of breath while the numbers are analyzed and then a sigh of relief (hopefully) when they survive the algorithm update unscathed.

After the update is released, and especially if it is confirmed by Google, a slew of articles and pundit analyses attempt to dissect what Google changed and how to win in the new paradigm.

I believe all this angst is entirely misplaced.

The Google algorithm is made out to be some sort of mystical secret recipe cooked up in a lab designed to simultaneously rob and reward sites at the whims of a magical, all-knowing wizard. In this outdated schema, the goal of every SEO and webmaster is to dupe this wizard and come out on the winning side of every update.

Join us on Thursday, June 10 at 12:30 p.m. PDT/3:30 p.m. EDT for a Twitter Spaces chat with author Eli Schwartz.

We’ll discuss SEO and growth marketing, so bring your questions!

This idea is rooted in a fundamental misunderstanding of what happens in a Google algorithm update — and a fundamental misunderstanding of Google. The reality is, algorithms are not your enemy. They are designed to help create a better, more accurate user experience. Here are a few pieces of perspective that should help reframe your relationship with algorithms.

Google’s algorithms are extensive and complex software programs that constantly need to be updated based on real scenarios.

First, let’s establish this: Google is only trying to help. The company wants to ensure a pleasurable, high-quality user experience for the searcher. Nothing more, nothing less. It is not a wizard, and its system is not meant to rob and reward sites arbitrarily.

Keep that in mind as we continue.

Google’s algorithms are extensive and complex software programs that constantly need to be updated based on real scenarios. Otherwise, they would be totally arbitrary. Just as bugs are reported and fixed in a software program, search engines must discover what’s not working and create solutions.

Google, like any other software company, releases updates with big leaps forward to its products and services. However, in Google’s case, they are called “major algorithm updates” instead of just product updates.

You are now armed with the knowledge of exactly what a Google algorithm update is. Is it not, then, gratifying to know there is never a reason to panic?

Have you worked with a talented individual or agency who helped you find and keep more users?

Respond to our survey and help us find the best startup growth marketers!

If a site experiences a drop in search traffic after a major algorithm update, it is rarely because the entire site was targeted. Typically, while one collection of URLs may be demoted in search rankings, other pages likely improved.

Seeing the improved pages requires taking a deep dive into Google Search Console to drill into which URLs saw drops in traffic and which witnessed gains. While a site can certainly see a steep drop off after an update, it is usually because they had more losers than winners.

Any drop is most definitely not because the algorithm punished the site.

If you see a drop, in many cases, your site might not have even lost real traffic; often, the losses represent only lost impressions already not converting into clicks. With a recent update, Google removed the organic listing of sites that had a featured snippet ranking. I saw steep drops in impressions, but the clicks were virtually unchanged. Gather and study your granular data for a clearer rendering of information rather than assuming the site has become a winner or loser after an update.

Websites that focus on providing an amazing and high-quality experience for users shouldn’t fear algorithm updates. In fact, updates can provide the needed impetus to excel. The only websites that have something to fear are those that should not have had high search visibility in the first place because of a poor user experience.

If your website provides a great experience for users, updates are actually likely to help you because they winnow those poorer quality sites out of the running.

If you focus on a good user experience, there will be pages that may lose some traffic in algorithm updates, but in aggregate, the site will typically gain traffic in most scenarios. Digging into the granular data of what changed will likely support the idea that websites do not suffer or benefit from algorithm updates — only specific URLs do.

Google will, and should, continuously update its algorithms. Google’s primary motivation is to have an evolving product that will continue to please and retain its users.

Consider that if Google leaves its algorithm alone, it risks being overrun by spammers that take advantage of loopholes. A search function that provides too many spammy results will soon go the way of AOL, Excite, Yahoo and every other search engine that is functionally no longer in existence. Google stays relevant by updating algorithms.

Updates are a part of search life.

Instead of chasing the algorithm, which will inevitably change, I believe that every website that relies on organic search should train its focus somewhere more important: on the user experience.

The user is the ultimate customer of search. If your site serves the user, it will be immunized from algorithm updates designed to protect the search experience. There is no algorithm wizard — only SEO masters who have figured out how to apply best processes, best procedures and actions for your website.

Algorithms and updates have only one purpose: help a user find exactly what they seek. Period. If you are helpful to the user, you have nothing to fear.

This post is an excerpt from “Product-Led SEO: The Why Behind Building Your Organic Growth Strategy.”

Powered by WPeMatico

Here’s another edition of “Dear Sophie,” the advice column that answers immigration-related questions about working at technology companies.

“Your questions are vital to the spread of knowledge that allows people all over the world to rise above borders and pursue their dreams,” says Sophie Alcorn, a Silicon Valley immigration attorney. “Whether you’re in people ops, a founder or seeking a job in Silicon Valley, I would love to answer your questions in my next column.”

Extra Crunch members receive access to weekly “Dear Sophie” columns; use promo code ALCORN to purchase a one- or two-year subscription for 50% off.

Dear Sophie,

I started a tech company about two years ago, and ever since I’ve dreamed of expanding my company in the United States.

I would love to have a green card. Someone mentioned that I should apply for a diversity green card. Would you please provide me with more details about it and how to apply?

— Technical in Tanzania

Dear Technical,

As a startup founder from Tanzania, you have several immigration options available to you, including the Diversity Immigrant Visa (green card) Program.

My law partner, Anita Koumriqian, and I recently discussed the Diversity Immigrant Visa Program (DV Program) on a podcast episode. Take a listen for how to apply and tips for applying. Each year, the U.S. Department of State, which oversees the DV Program, reserves 50,000 green cards for individuals born in countries that have low rates of immigration to the United States. The State Department publishes instructions each year, which includes the countries whose natives are eligible to register for the annual diversity lottery. Here is the latest version.

You must register online in the fall — usually from early October through early November — for the annual random lottery by completing the Electronic Diversity Visa Entry Form (DS-5501). There is no cost to register for the lottery, but be aware that you will be automatically disqualified if you register yourself more than once, and incomplete forms will not be accepted.

Once you complete the online registration form, you will get a confirmation number. Do not lose this number! It is the only way to access the online system that will tell you whether you were selected in the lottery and are eligible to submit a green card application. In May, registrants can log into the online system to find out whether they’ve been selected. No notification will be sent by email or snail mail; checking online by entering your confirmation code is the only way to find out. After you enter your confirmation code online, you will receive a diversity visa number, which you will use to determine when you can file your green card application.

Powered by WPeMatico

Ending years of debates over environmental sustainability, the United States officially declared a climate crisis earlier this year, deeming climate considerations an “essential element” of foreign policy and national security. After recommitting the U.S. to the Paris Agreement, President Joseph R. Biden announced an aggressive new goal for reducing U.S. greenhouse gas emissions and pushed world leaders to collectively “step up” their fight against climate change.

At the same time, consumers are increasingly looking to do business with brands that align with their growing environmental values, rather than ignoring the climate consequences of their consumption. Even without regulation as a stick, consumer demand is now serving as a carrot to increase sustainability’s impact on public companies’ agendas.

Startups have already followed suit. Investors today view sustainability as an important pillar of any business model and are looking for entrepreneurs who “get it” from the beginning to build and scale next-generation companies. Startups interested in thriving cannot treat sustainability as an afterthought and should be prepared to enter the public eye with a plan for sustainable growth.

Today, companies of all sizes are being held to a higher standard by consumers, employees, potential partners and the media.

So what exactly do founders need to put in place to demonstrate that they’re on the right track when it comes to sustainability? Here are five attributes that investors are looking for.

It’s fairly easy for any company to claim that it understands customers’ wants and needs, but it’s challenging to have the tech stack in place to prove a company actually listens to customer feedback and meets those expectations.

Investors now expect startups to have both platforms and solutions — social listening channels, relationship management tools, surveying programs and review forums — that allow them to hear and act on the needs of their customers. Without the proper communications tools and actual people using them, your eco-friendly efforts will likely appear to be merely lip service.

Take the example of TemperPack, which manufactures recyclable insulated packaging solutions for shipments of cold, perishable foods and pharmaceuticals. The direct relationship between a packager like TemperPack and the end consumer is often invisible. But as we were looking into investing in the company, some of its life sciences customers told us about comments they had received from end users — people who were receiving medicine twice per day. Another supplier’s packaging required them to visit a recycler for disposal, a real-world pain point that was causing them to consider switching to a different medication.

Revolution Growth decided to add TemperPack as a portfolio company after directly seeing its customer feedback loop in action: End-user requests informed product development, proving both a market need and customer demand on the sustainability front. This firsthand example demonstrates how an investor, a packaging maker, a life sciences company and an end user are now interconnected in one relationship while underscoring how end-user feedback can connect the dots for sustainable product development.

Over the past several years, we have seen millennials and Gen Z consumers demand transparency in sustainability efforts. As these generations grow in purchasing power, investors will look for startups that make their commitments to eco-friendly goals as transparent as possible to satisfy shrewd consumer needs.

For many VCs, making public commitments to sustainability goals is a sign that your startup is working toward becoming a next-generation company. Investors will look for goals that are thoughtful, with a clear understanding of where your company will have agency and influence, and that are S.M.A.R.T (Specific, Measurable, Achievable, Realistic and Timely). They will also expect regular reports on progress.

Although a company’s management establishes these goals, its board should play a behind-the-scenes role in driving the goals forward, keeping leadership on track and setting the playing field so executives understand that they’re being evaluated on criteria transcending positive EBIDTA.

Taking these steps will ensure goals are responsible and ambitious while also holding the company accountable to consumers and stakeholders to see the initiatives through to completion.

Even the best-laid sustainability goals will go unmet without a strong culture designed to guarantee leadership and employee alignment. Sustainability must be ingrained in a startup’s culture — from the top down and bottom up — and there’s a lot at stake if it’s not.

Another Revolution Growth portfolio company, the global fintech-revolutionizing startup Tala, demonstrates how young companies can imbue their cultures with purpose-driven values. While Tala’s mission is to provide credit to the unbanked, the company believes that the consumer’s best interests should always come first. During 2019’s holiday season, Tala contrasted with businesses fueling consumption by instead urging customers in Kenya to not take out loans, protecting them from predatory unregulated lenders amid a lack of functioning credit bureaus and loan-stacking databases. This forward-looking approach ultimately safeguarded Tala’s customers and its vibrant digital lending industry.

Beyond determining what they stand for, many of our portfolio companies face challenges securing talent. People have choices about where they want to work, and those with intrinsic motivations — such as concerns about the environment — will feel uncomfortable if their employers do not share their values. Regulatory risks and customer attrition pale in comparison to the human cost of losing star performers who seek other work cultures that better align with their values.

A clear values system should embed sustainability into the decision-making process, make obvious imperatives and empower employees to follow through.

Companies aren’t only judged by their own initiatives — they’re also judged by their partners. As startups build new relationships or expand to work with new suppliers, investors will be keen to know that these outside parties align with their stated sustainability philosophies.

Before becoming publicly involved with another company, a startup should gauge each new supplier’s reputation, including insights into their employment practices. Take leading Mediterranean fast-casual restaurant Cava or healthy-inspired salad-centric chain Sweetgreen, both Revolution Growth portfolio companies; neither will source proteins from farms with inhumane policies. If companies are not aware of these factors, their customers will eventually let them know, and likely hold them accountable for the oversight.

Think of it this way: If a diagram of your partnerships and supplier relationships was printed on the front page of The New York Times, would you be comfortable with what it shows the world? Today, companies of all sizes are being held to a higher standard by consumers, employees, potential partners and the media. It’s no longer possible to fly under the radar with relationships that are antithetical to a company’s sustainability goals. So take a hard look at your supplier and partner ecosystem, and make clear that you are bringing your green vision to life through every extension of your business.

Financial realism acknowledges that a company can want to do good, but unless they have the economics, they won’t survive to make an impact. For most startups, beginning with financial realism as a mindset and incrementalism as an approach will be key to success, enabling all businesses to contribute to a more resilient planet. For startups that prioritize environmentally friendly business practices alongside a product or service, this strategy can prevent goodness from becoming the enemy of greatness. Founders in this position can commit to a stage-by-stage sustainability plan, rather than expecting an overnight transformation. Investors understand the delicate balance between striving to meet green goals and keeping the lights on.

Entrepreneurs looking to build a business that not only adopts eco-friendly practices but also has sustainability at its heart may have to consider starting in a niche industry or market that is less price-sensitive and ready for a solution today. Once that solution is firmly established, the business can build upon what they’ve created, rather than going big with something that doesn’t scale — and failing fast. Without an initial set of customers that value and love what you’re doing, you won’t get to the bigger play.

As the public and private sectors continue to address the climate crisis, sustainability will increasingly become a mandate rather than an option, and funding will increasingly flow to startups that have addressed potential environmental concerns. Unfortunately, pressure for companies to meet sustainability demands has led to “greenwashing” — the deceptive use of green marketing to persuade consumers that a company’s products, aims and policies are environmentally friendly.

Greenwashing has forced investors to look beyond mere words for action. As we move toward a more sustainable future, startups pursuing VC funding will need to prove to investors that sustainability is a priority across their entire organizations, aligning their outreach, public commitments and cultures with accountability and concrete examples of sustainable activities. Even if those examples are just steps toward larger goals, they will show investors and customers that startups are ready today to contribute to a greener and better tomorrow.

Powered by WPeMatico

Hey, founders between gigs: What now?

If you exited your last company for airplane money and are now independently wealthy, congratulations! If you want to build another company, just self-fund. If you want outside capital, VCs will chase after you to invest.

Unfortunately, most founders are not in that position: nine out of 10 startups fail. Even if you achieve a high valuation, you might end up like FanDuel’s founders: Their investors got the benefit of a $465 million exit; the founders got zero.

As someone with “founder” on your resume, you face a greater challenge when trying to get a traditional salaried job. You’ve already shown that you really want to lead a company and not just rise up the ladder, which means some employers are less likely to hire you. One research paper found:

[F]ormer founders receive fewer callbacks than non-founders; however, all founders are not disadvantaged similarly. Former founders of successful ventures receive even fewer [emphasis added] callbacks than former founders of failed ventures. Through 20 interviews with technical recruiters, we highlight the mechanisms driving this founder-experience discount: concerns related to the applicant’s capability and ability to fit into and remain committed to the wage employment and the hiring firm.

At my prior firm, ff Venture Capital, we invested in a company co-founded by Nate Jenkins, who had a successful exit, but not quite enough to buy a private plane. He’s now researching his next opportunity and interviewing for some jobs. At the end of a recent interview, the interviewer summarized, “I’ll hire you, but is this what you really want to do?”

That said, Samuel Sabin, CEO of HireBlue, observed, “Some founders who work better with more resources at their disposal may be tapped for intrapreneurship roles. Also, some companies value a self-starter mentality.”

So what should you do? Especially if your life partner and/or bank account are burnt out on the income volatility of startups?

I’ve been in this situation myself when I shut down one startup and exited two others. I think you have six main options:

At Versatile VC, our new VC fund, we’re creating an online community just for founders who are in transition, Founders’ Next Move. We hope you will join us!

If you want to work on your startup idea, the bar for starting a company should always be very high. VCs have a diversified portfolio and most of their investments die. You don’t have a diverse portfolio and so you’re taking far more risk than the VCs. For free resources to help research your ideas, see What startup will you build? Identifying market white space.

Powered by WPeMatico