Column

Auto Added by WPeMatico

Auto Added by WPeMatico

API publishers among Postman’s community of more than 15 million are working toward more seamless and integrated developer experiences for their APIs. Distilled from hundreds of one-on-one discussions, I recently shared a study on increasing adoption of an API with a public workspace in Postman. One of the biggest reasons to use a public workspace is to enhance developer onboarding with a faster time to first call (TTFC), the most important metric you’ll need for a public API.

If you are not investing in TTFC as your most important API metric, you are limiting the size of your potential developer base throughout your remaining adoption funnel.

To understand a developer’s journey, let’s first take a look at factors influencing how much time and energy they are willing to invest in learning your technology and making it work.

With that context in mind, the following stages describe the developer journey of encountering a new API:

A developer browses your website and documentation to figure out what your API offers. Some people gloss over this step, preferring to learn what your tech offers interactively in the next steps. But judgments are formed at this very early stage, likely while comparing your product among alternatives. For example, if your documentation and onboarding process appears comparatively unorganized and riddled with errors, perhaps it is a reflection of your technology.

Signing up for an account is a developer’s first commitment. It signals their intent to do something with your API. Frequently going hand-in-hand with the next step, signing up is required to generate an API key.

Making the first API call is the first payoff a developer receives and is oftentimes when developers begin more deeply understanding how the API fits into their world. Stripe and Algolia embed interactive guides within their developer documentation to enable first API calls. Stripe and Twitter also use Postman public workspaces for interactive onboarding. Since many developers already use Postman, experiencing an API in familiar territory gets them one step closer to implementation.

Powered by WPeMatico

Digital technologies have disrupted the structure of markets with unprecedented breadth and scale. Today, there is yet another wave of innovation emerging, and that is the decarbonization of the global economy.

While governments still lack the conviction necessary to truly fight the climate crisis, the overall direction is clear. The carbon price in Europe rose from below $10 to over $50 per ton. Shell was handed a resounding defeat by a Dutch court. The major blackout in Texas at the beginning of the year revealed the fragility of the existing energy supply even in a highly industrialized country. We must urgently invest more into developing and deploying reliable, clean electricity generation technologies to make decarbonization a reality.

Forward-thinking investors understand this. Global investment in low-carbon technologies climbed to $500 billion in 2020, according to Bloomberg. Renewable energy accounted for around $300 billion of that, followed by electrification of transport ($140 billion) and heating ($50 billion).

However, we remain far from the finish line. According to the International Energy Agency, global emissions of CO2 this year are set to jump 1.5 billion tons over 2020 levels. And more than 80% of global energy consumption is still made up of coal, oil and gas.

Fusion, the process that powers the stars, could be the cleanest energy source for humanity.

That’s why we need to continue backing new technologies with breakthrough potential. Of particular promise is nuclear fusion. Fusion, the process that powers the stars, could be the cleanest energy source for humanity. We are already indirectly harvesting the power of fusion through solar energy. Being able to build fusion reactors would give us an “always on” version, independent of weather conditions.

But why fund fusion at all, given that we don’t yet know how to do it? First, this isn’t an either-or proposition. We can afford to build out renewable energy and investigate new forms of energy production at the same time because the latter — at least at this early stage of development — will require a comparatively trivial amount of money. The U.S. government’s latest plan is to spend $174 billion over 10 years on the electrification of car transport alone, so to invest $2 billion to create a fusion power plant seems doable.

Second, we are about to need a lot more electricity than we ever have. The global demand for carbon-free energy sources is set to triple by 2050, driven by increasing urbanization, the electrification of industrial processes, the loss of biodiversity and the increase in energy consumption in emerging markets.

Third, there’s been tremendous progress in the necessary supporting technologies. Superconducting magnets for the magnetic-confinement approach to fusion have become much cheaper, lasers for inertial confinement fusion have become much more powerful, and breakthroughs in material science have made nanostructured targets available, which enable the use of completely new approaches to fusion, such as the low-neutronic fuel pB11.

Thankfully, there is a growing number of entrepreneurial efforts from world-class teams to try and build fusion. At least 25 startups around the world are targeting fusion right now, approaching the problem with a wide range of technologies. The amount invested in private fusion companies across the world increased tenfold to almost $1 billion in 2020, according to Crunchbase.

The upside of successful fusion is nearly unlimited. The clean energy generation market represents a trillion-dollar opportunity. An estimated 26 TW of primary energy capacity needs to be built globally from 2030 to 2050 to serve the rising global energy needs, according to Materials Research Society. Just 1 TW of capacity will generate $300 billion in revenue, and a 15% market share from 2030 to 2050 would yield more than $1 trillion in annual revenue.

We need many shots on goal here, which is why Susan Danziger and I have personally invested in three different fusion startups already (Zap Energy and Avalanche in the United States and Marvel Fusion in Germany).

But it is not primarily the potential for financial upside that motivates us: There is an opportunity to make an indelible difference in the trajectory of human history. If even a small fraction of the large wealth accumulated by entrepreneurs and investors in the last couple of decades is invested here, the likelihood of successful fusion rises dramatically. That, in turn, will unlock much more investment from both venture funds and governments.

Now is the time to go all-in on decarbonization. Funding fusion with its breakthrough potential must be part of that effort.

Powered by WPeMatico

One of VR’s prospective revenue streams is ad placement. The thought is that its levels of immersion can engender high engagement with various flavors of display ads. Think billboards in a virtual streetscape or sporting venue. Art imitates life, and all that.

This topic reemerged recently in the wake of Facebook’s experimental ads in Blaston VR. As TechCrunch’s Lucas Matney observed, it didn’t go too well. The move triggered a resounding backlash, followed by the game publisher, Resolution Games, backing out of the trial.

This chain of events underscored Facebook’s headwinds in VR ad monetization, which stem from its broader ad issues. In fairness, this was an experimental move to test the VR advertising waters … which Facebook accomplished, though it didn’t get the result it wanted.

VR advertising is a bit of a double-edged sword. It could take several years for VR usage to reach requisite levels for meaningful ad monetization.

Regardless, we’ve taken this opportunity to revisit our ongoing analysis and market sizing of VR advertising in general. The short version: There are pros and cons on both qualitative and quantitative levels.

VR advertising’s opportunity goes back to factors noted above: potentially high ad engagement given inherent levels of immersion. On that measure, VR exceeds all other media, which can mean higher-quality impressions, brand recall and other common display-ad metrics.

Historical evidence also suggests that VR could follow a path toward ad monetization. VR shows similar patterns to media that were increasingly ad supported as they matured. These include video, social media, mobile apps and games (just ask Unity).

To put some numbers behind that, 75% of apps in the Apple App Store’s first year were paid apps — similar to VR today. That figure declined to 15% in 2014 and hovers around 10% today. Over time, developers learned they could reach scale through free downloads.

Prevalent revenue models today include in-app purchases — especially in mobile gaming — and advertising. The question is whether VR will follow a similar path as developers learn that they can reach scale faster through free apps that employ “back-end monetization” like ad support.

This trend also follows audience dynamics: Early adopters are more likely to pay for content and experiences. But as a given technology or media matures, its transition to mainstream audiences requires different business models with less upfront commitment and friction.

“Today, there are only about 18% of applications in VR stores such as Steam and Oculus that are free,” Admix CEO Samuel Huber said. “This is fine for now because we are still very early in the market and most of these users are early adopters. They are willing to pay for content, just like they were willing to pay for prototype unproven hardware and generally, they have higher purchasing power than the average person.”

Considering the above advantages, VR advertising is a bit of a double-edged sword (or beat saber). Those advantages are counterbalanced by a few practical disadvantages in the medium’s early stage. Much of this comes down to the requirement for scale.

Powered by WPeMatico

Understanding what you will change is most important to achieve a long-lasting and successful robotic process automation transformation. There are three pillars that will be most impacted by the change: people, process and digital workers (also referred to as robots). The interaction of these three pillars executes workflows and tasks, and if integrated cohesively, determines the success of an enterprisewide digital transformation.

Robots are not coming to replace us, they are coming to take over the repetitive, mundane and monotonous tasks that we’ve never been fond of. They are here to transform the work we do by allowing us to focus on innovation and impactful work. RPA ties decisions and actions together. It is the skeletal structure of a digital process that carries information from point A to point B. However, the decision-making capability to understand and decide what comes next will be fueled by RPA’s integration with AI.

From a strategic standpoint, success measures for automating, optimizing and redesigning work should not be solely centered around metrics like decreasing fully loaded costs or FTE reduction, but should put the people at the center.

We are seeing software vendors adopt vertical technology capabilities and offer a wide range of capabilities to address the three pillars mentioned above. These include powerhouses like UiPath, which recently went public, Microsoft’s Softomotive acquisition, and Celonis, which recently became a unicorn with a $1 billion Series D round. RPA firms call it “intelligent automation,” whereas Celonis targets the execution management system. Both are aiming to be a one-stop shop for all things related to process.

We have seen investments in various product categories for each stage in the intelligent automation journey. Process and task mining for process discovery, centralized business process repositories for CoEs, executives to manage the pipeline and measure cost versus benefit, and artificial intelligence solutions for intelligent document processing.

For your transformation journey to be successful, you need to develop a deep understanding of your goals, people and the process.

From a strategic standpoint, success measures for automating, optimizing and redesigning work should not be solely centered around metrics like decreasing fully loaded costs or FTE reduction, but should put the people at the center. To measure improved customer and employee experiences, give special attention to metrics like decreases in throughput time or rework rate, identify vendors that deliver late, and find missed invoice payments or determine loan requests from individuals that are more likely to be paid back late. These provide more targeted success measures for specific business units.

The returns realized with an automation program are not limited to metrics like time or cost savings. The overall performance of an automation program can be more thoroughly measured with the sum of successes of the improved CX/EX metrics in different business units. For each business process you will be redesigning, optimizing or automating, set a definitive problem statement and try to find the right solution to solve it. Do not try to fit predetermined solutions into the problems. Start with the problem and goal first.

To accomplish enterprise digital transformation via RPA, executives should put people at the heart of their program. Understanding the skill sets and talents of the workforce within the company can yield better knowledge of how well each employee can contribute to the automation economy within the organization. A workforce that is continuously retrained and upskilled learns how to automate and flexibly complete tasks together with robots and is better equipped to achieve transformation at scale.

Powered by WPeMatico

There’s a lot wrapped up in a name: feelings, emotions, connotation, unconscious bias, personal history. It’s an identity — it gives something meaning and importance.

In leading marketing and brand at High Alpha, I think about naming quite a bit. As a venture studio, we co-found and launch five to 10 new software startups every year. It is my team’s responsibility to create and build out the brands for all the new companies we start, including everything from naming and domain acquisition to brand identity and websites. Over the past five years, we’ve named more than 30 software startups at High Alpha.

Over the past five years, we’ve named more than 30 software startups.

As a soon-to-be first-time parent, the idea of naming has taken on a whole new meaning and importance in my life. Even though I help name new companies for a living, I now fully understand the paralysis that often comes when faced with the task of deciding the name for someone or something that’s especially important to you.

Because of this, I’ve always tried to take an objective, pragmatic approach to naming a company with our CEOs and other startups. Naming is an incredibly difficult and nuanced process. It’s fraught with subjectiveness and personal preference. And to top it all off, most founders have zero (or very little) experience in naming.

The truth is that business names fall on a bell curve — you have a small number of outliers that actively contribute to your success and a small number of outliers that actively impair your ability to succeed. The vast majority, though, fall somewhere in the middle in their impact on your business.

So, how should a founder go about effectively naming their baby startup and not picking a name that will hurt them? I’m sharing my own criteria and lessons for how to go about naming your startup, how to evaluate a company name and what makes for a good company name.

As a founder, one of the first criteria to look at is ownability and URL availability. Nowadays, you’ll be hard-pressed to find a name where the .com is still available. I oftentimes will look at .io, .co, get_______.com, or _____hq.com as my top alternatives to a .com, but I always still prefer if the .com is potentially attainable in the future. It may be parked by a domain investor or someone asking a ridiculous price, but that’s always better than an established business using your .com. If not, you will always be fighting a search battle with some other brand that owns your .com.

This goes much further than just the availability of the coveted .com domain, though. You should evaluate the competitiveness and search congestion around your branded keywords. A company named “Apple” or “Lumber” is going to have a really hard time competing for search placements, even if they don’t sell computers or building supplies. An established name and word is also going to come with existing connotations and previous experiences in your audience’s mind. You want a name free from as much baggage as possible so you can easily build your own connotations and memories.

Powered by WPeMatico

A CEO’s fiduciary duties to their company and its shareholders do not end when they are off the clock — they must always act in good faith. However, navigating the boundaries between a company’s official communications and a personal voice can be difficult in today’s social-media-connected environment.

What a CEO posts on Twitter can raise not only serious reputational issues for themselves and their companies but posting the wrong things at the wrong time can also cause breach of fiduciary duties and may even run afoul of securities laws.

Reputation and goodwill take a long time to build and are difficult to maintain, but it only takes one tweet to destroy it all.

Fiduciary duties can be divided into three buckets: (1) duty of care — CEOs must act in good faith with the care of a reasonable person in a like position with a reasonable belief that their decisions are in furtherance of their company’s best interest; (2) duty of loyalty — CEOs must put the interest of shareholders and the company above their own self-interest; and (3) duty of good faith — CEOs must act with honesty and fairness to shareholders and the company.

There is no denying that Twitter can be leveraged as a powerful tool. Used appropriately, it can fortify the reputation of a company and its CEO, forge stronger consumer relationships and drive business profits. For example, Tim Cook’s habit of tweeting about his interactions with Apple customers demonstrates his customer-service values and effort to connect with consumers, which can potentially lead to a bigger and more loyal following.

Lately, more and more CEOs are communicating their stance on issues that are important to their consumer base to exhibit authenticity, relatability and demonstrate their personal and corporate values through social media. Following last year’s murder of George Floyd and rise of the Black Lives Matter movement, nearly 60% of all S&P 100 tech CEOs, unicorn CEOs, and Fortune 500 CEOs tweeted, “Black Lives Matter.” This was the first time CEOs active on Twitter overwhelmingly voiced their position on racial and social justice issues.

Twitter can also be an opportunity to show transparency in policy. CEOs can use social media to announce new management initiatives, capability expansions and new investments in employees (diversity initiatives, new roles for women, organizational changes) that are positive in tone and speak about the future direction of the company. These can have a positive correlation with stock prices.

It wasn’t that long ago that the world was fixated on Donald Trump’s Twitter posts and their correlation with the stock market. Words have permanence and their impact can be catastrophic. Given their elevated role as a leader and representative of the company and the fiduciary duties they owe, CEOs must watch what they say and when they say it. What it all boils down to is awareness, common sense and the law.

For U.S. publicly traded companies, SEC Regulation Fair Disclosure (Reg FD) says that “an issuer may not disclose material nonpublic information to certain groups, either intentionally or unintentionally, without disclosing the same information to the entire marketplace.” If companies use social media to announce key information, to comply, they must alert investors that social media will be used to disseminate such information.

Regardless of whether it is a public or private company, CEOs are corporate officers and owe fiduciary duties to their companies and their shareholders. Fiduciary duty requires CEOs to act in good faith, apply their best business judgment and to act in the best interest of the company. This is true whether they are in the boardroom or on Twitter.

Powered by WPeMatico

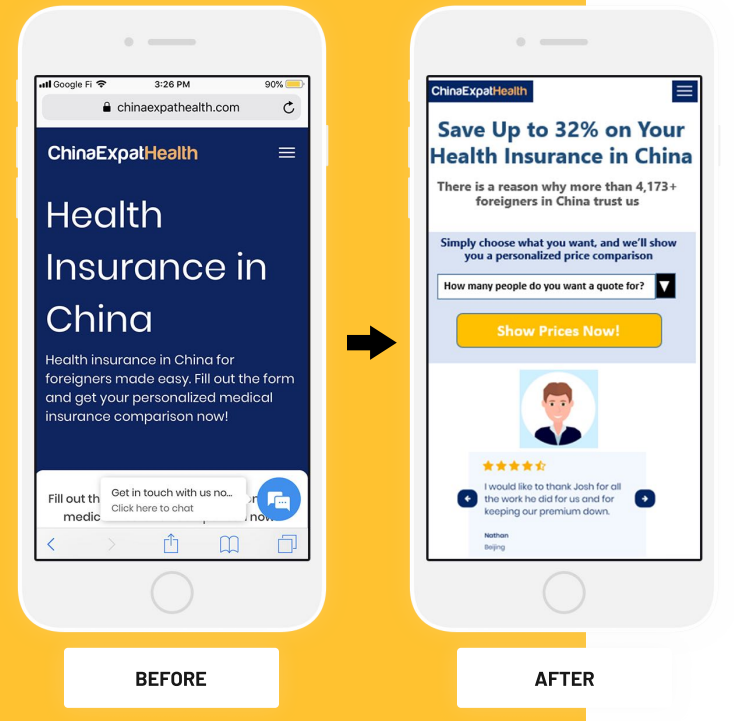

In this case study, we’ll show how we used research-driven CRO (conversion rate optimization) techniques to increase lead conversion rate by 79% for China Expat Health, a lead generation company.

Help TechCrunch find the best growth marketers for startups.

Provide a recommendation in this quick survey and we’ll share the results with everybody.

In the image below, the mobile site view on the left, labeled “before,” is the control ( “A” version) while that on the right, labeled “after,” is the optimized page (“B” version). We conducted a split test aka A/B test, directing half of the traffic to each version, and the result attained 95% statistical significance. Read on for a description of the key changes made.

Image Credits: Jasper Kuria

The headline on the control version is “Health Insurance in China.” If I am an expat looking for health insurance in China, at least I know I am in the right place but I don’t immediately have a reason to choose you. I have to scroll and infer this from multiple elements.

For revenue-generating landing pages it is best to always follow the Bauhaus design aesthetic (from architecture). Form follows function, ornament is evil!

The winning version instantly conveys a compelling value proposition: “Save Up to 32% on Your Health Insurance in China,” accompanied by “evidentials” to support this claim — the number of past customers and a relevant testimonial with a 4.5 star rating (by the way, it is better to use a default static testimonial rather than a moving carousel).

As the famed old-school direct response marketer John Caples taught us, “The reader’s attention is yours only for a single instant. They will not spend their valuable time trying to figure out what you mean.” What was true in Caples’ 1920s heyday is doubly so in the mobile age, when attention spans are shorter than a fruit fly’s!

Powered by WPeMatico

Let’s play out this scenario. Your deck is ready and you’re just about to start reaching out. What does conventional wisdom say that you should send? A three-paragraph overview, four bullet points outlining the problem, and three bullet points on how you solve it and why you’re the best. You went through all that work … but who is going to read it? A junior person. Not even a senior VC.

Even if you do end up with a meeting, odds are that your deck didn’t even get read. The biggest lie in venture capital is: “Yes, I read through your deck.” Because those words are immediately followed by, “ … but why don’t you run us through it from the beginning?”

At that point, it’s safe to assume that no one has actually taken the time to read through what you sent, the junior guy thought it would be an interesting meeting considering the fund’s current themes of interest, and no one objected to taking the meeting. But no one has really taken the time to read through your deck.

Even if the only benefit was that other investment committee members heard the story direct from the founder, that alone would make your video pitch worth it.

According to DocSend, the average pitch deck review time over the last 20 weeks is less than three minutes. Let’s break down how much time you’ll be given for a 12-page deck (a very concise deck):

That also includes time for that critical-to-understand diagram that illustrates and distills your unique system or view of the world. Do you think 25 seconds is long enough to fully comprehend that diagram and connect the dots with your value prop? Not likely.

Don’t send cold decks, ever. Instead, you should be video pitching — this is a video walkthrough of your deck, with your face in a camera bubble talking through it and giving added color in a video no longer than six-and-a-half minutes. Your objective for this video: Get in, provide a basis of understanding, and get out with a punchy CTA. Nothing flashy, nothing fancy.

More investors are embracing video pitches (prime example: Ashton Kutcher’s Sound Ventures), and in the age of the Zoom-based pitch meeting, it’s quickly becoming the standard.

The rapid but notable shift is because in video pitching, founders get to showcase the preparedness, commitment and passion VCs are looking for, all while telling their story. None of that is effectively transmitted in a cold pitch deck. Further, it allows you to create a deeper connection even before a meeting ever takes place. In a sense, it allows you and the investor to skip a step in the relationship-building process.

Cold decks get blown out of the water when compared with the benefits of the video pitch:

Powered by WPeMatico

Last week was a good one for edtech in Europe.

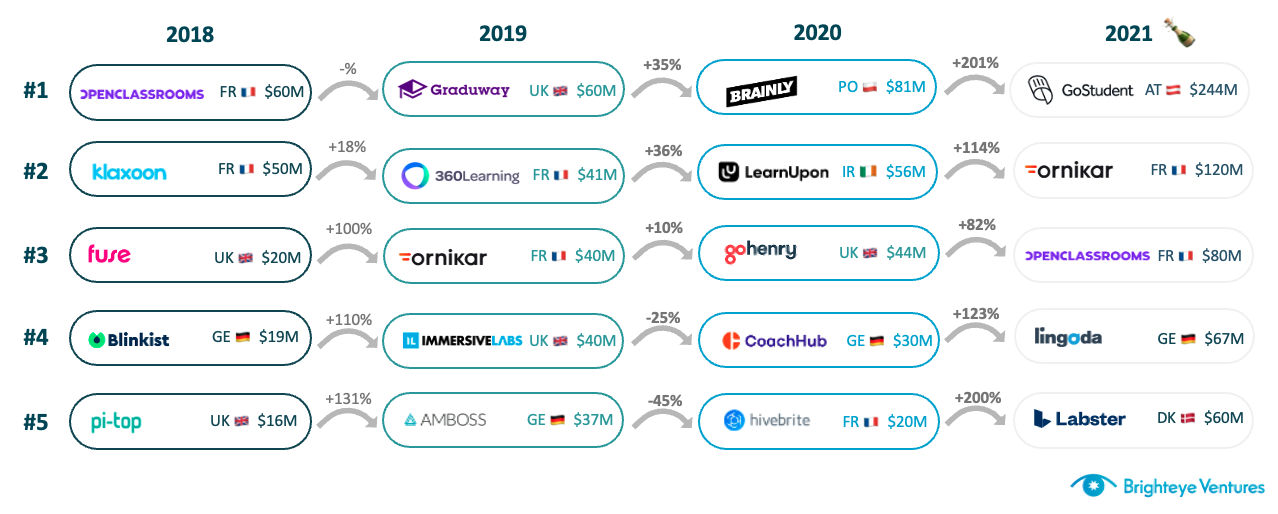

GoStudent became Europe’s first edtech unicorn (IPO’d companies aside), raising its third round in 12 months and the biggest ever in the sector in Europe. Brighteye Ventures’ analysis showed that VC investments in European edtech had breached $1 billion in a calendar year for the first time, even without GoStudent’s mega-round, with six months left to go.

Edtech deal flow in 2021 looks set to match or even outpace 2020 levels, per the report: At $9.4 million, average deal size is triple 2020 levels; seven companies have raised $50 million in five different markets; and the U.K. has more than three times as many deals as the next individual market.

Deal-size progression in edtech over the years. Image Credits: Brighteye Ventures

It’s interesting that we are not seeing enormous increases in deal count. The $1.05-billion mark in the report is spread across 111 transactions — there were 237 in 2020, so we could expect a similar total this year. More funding and stable deal count of course means that we are seeing significant increases in deal size.

It seems generalist investors are recognizing that edtech investments can reap outsized returns, similar to sectors like deep tech, health tech and fintech.

We can draw a few conclusions from this. We can construe that companies created last year and in previous years matured significantly during the pandemic due to increased demand. Moreover, this rapid natural selection process provided insights on verticals and possible winners.

Lastly, it seems generalist investors are recognizing that edtech investments can reap outsized returns, similar to sectors like deep tech, health tech and fintech.

This is contributing to larger early rounds than we have seen in previous years — investors can’t pick the winner, but they can slant the playing field instead. We therefore expect to see a surge in the number of pre-seed, seed and Series A rounds in the second half of 2021, as companies founded during the pandemic begin to raise meaningful funding.

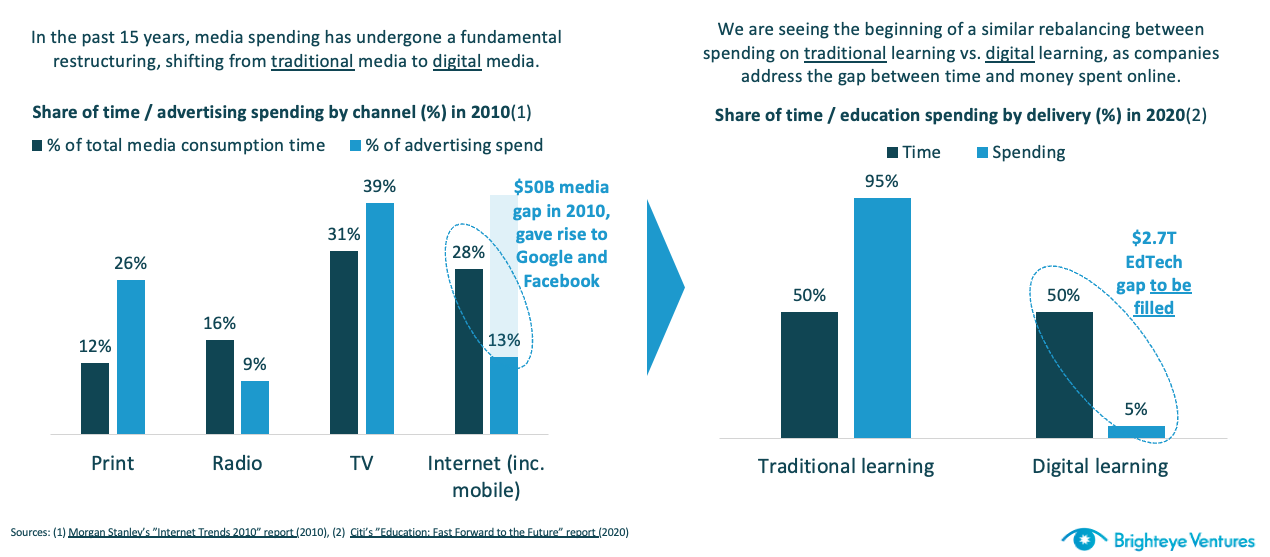

Another reason that edtech is being taken seriously by generalist investors is that the true size of the market (and the extent of digitization to come) is becoming more conceivable.

Edtech spending is growing like media spending did in the 2010s. Image Credits: Brighteye Ventures

Powered by WPeMatico

Data breaches have become a part of life. They impact hospitals, universities, government agencies, charitable organizations and commercial enterprises. In healthcare alone, 2020 saw 640 breaches, exposing 30 million personal records, a 25% increase over 2019 that equates to roughly two breaches per day, according to the U.S. Department of Health and Human Services. On a global basis, 2.3 billion records were breached in February 2021.

It’s painfully clear that existing data loss prevention (DLP) tools are struggling to deal with the data sprawl, ubiquitous cloud services, device diversity and human behaviors that constitute our virtual world.

Conventional DLP solutions are built on a castle-and-moat framework in which data centers and cloud platforms are the castles holding sensitive data. They’re surrounded by networks, endpoint devices and human beings that serve as moats, defining the defensive security perimeters of every organization. Conventional solutions assign sensitivity ratings to individual data assets and monitor these perimeters to detect the unauthorized movement of sensitive data.

It’s painfully clear that existing data loss prevention (DLP) tools are struggling to deal with the data sprawl, ubiquitous cloud services, device diversity and human behaviors that constitute our virtual world.

Unfortunately, these historical security boundaries are becoming increasingly ambiguous and somewhat irrelevant as bots, APIs and collaboration tools become the primary conduits for sharing and exchanging data.

In reality, data loss is only half the problem confronting a modern enterprise. Corporations are routinely exposed to financial, legal and ethical risks associated with the mishandling or misuse of sensitive information within the corporation itself. The risks associated with the misuse of personally identifiable information have been widely publicized.

However, risks of similar or greater severity can result from the mishandling of intellectual property, material nonpublic information, or any type of data that was obtained through a formal agreement that placed explicit restrictions on its use.

Conventional DLP frameworks are incapable of addressing these challenges. We believe they need to be replaced by a new data misuse protection (DMP) framework that safeguards data from unauthorized or inappropriate use within a corporate environment in addition to its outright theft or inadvertent loss. DMP solutions will provide data assets with more sophisticated self-defense mechanisms instead of relying on the surveillance of traditional security perimeters.

Powered by WPeMatico