Column

Auto Added by WPeMatico

Auto Added by WPeMatico

The pandemic forced companies around the world to adjust to a “new normal,” which caused many leaders to pivot their business strategies and adopt new technologies to continue operations. In a time of chaos and change, there is no senior leader that can navigate this sort of change better than a CTO.

Not only do CTOs understand the ever-changing tech landscape, they also provide invaluable insights to help organizations go beyond traditional IT conversations and leverage technology to successfully scale businesses.

Boards are facing pressure to be strategic and thoughtful on how to evolve in the rapidly iterating world of technology, and a CTO is uniquely positioned to address specific challenges.

There are now more reasons than ever to consider adding a CTO to your board. As a CTO myself, I know how important and impactful it can be to have technical-minded leaders on a company’s board of directors. At a time when companies are accelerating their digital transformation, it’s critical to have diverse technical perspectives and people from varying backgrounds, as transformations are a mix of people, process and technology.

Drawing on my experience on Lightbend’s board of directors, here are five hidden benefits of making space at the table for a CTO.

Currently, most boards of directors are composed of former CEOs, CFOs and investors. While such executives bring vast experience, they have very specific expertise, and that frequently does not include technical proficiency. In order for a company to be successful, your board needs to have people with different backgrounds and expertise.

Inviting different perspectives forces companies out of the groupthink mentality and find new, creative solutions to their problems. Diverse perspectives aren’t just about the title –– racial ethnicity and gender diversity are clearly a play here as well.

For a product-led company, having a CTO who has been close to product development and innovation can bring deep insights and understanding to the boardroom. Boards are facing pressure to be strategic and thoughtful on how to evolve in the rapidly iterating world of technology, and a CTO is uniquely positioned to address specific challenges.

Powered by WPeMatico

Software as a service has been thriving as a sector for years, but it has gone into overdrive in the past year as businesses responded to the pandemic by speeding up the migration of important functions to the cloud. We’ve all seen the news of SaaS startups raising large funding rounds, with deal sizes and valuations steadily climbing. But as tech industry watchers know only too well, large funding rounds and valuations are not foolproof indicators of sustainable growth and longevity.

Failing to come across as a unique, differentiated company will likely mean settling for an exit that feels mediocre instead of incredible.

To scale sustainably, grow its customer base and mature to the point of an exit, a SaaS startup needs to stand apart from the herd at every phase of development. Failure to do so means a poor outcome for founders and investors.

As a founder who pivoted from on-premise to SaaS back in 2016, I have focused on scaling my company (most recently crossing 145,000 customers) and in the process, learned quite a bit about making a mark. Here is some advice on differentiation at the various stages in the life of a SaaS startup.

Differentiation is crucial early on, because it’s one of the only ways to attract customers. Customers can help lay the groundwork for everything from your product roadmap to pricing.

The more you know about your target customers’ pain points with current solutions, the easier it will be to stand out. Take every opportunity to learn about the people you are aiming to serve, and which problems they want to solve the most. Analyst reports about specific sectors may be useful, but there is no better source of information than the people who, hopefully, will pay to use your solution.

The key to success in the SaaS space is solving real problems. Take DocuSign, for example — the company found a way to simply and elegantly solve a niche problem for users with its software. This is something that sounds easy, but in reality, it means spending hours listening to the customer and tailoring your product accordingly.

Powered by WPeMatico

It was August 2019, and the fundraising process was not going well.

My co-founder and I had left our product management jobs at New Relic several months prior, deciding to finally plunge into building Reclaim after nearly a year of late nights and weekends spent prototyping and iterating on ideas. We had bits and pieces of a product, but the majority of it was what we might call “slideware.”

When you can’t raise big on the vision, you need to raise big on the proof. And the proof comes from building, learning, iterating and getting traction with your first few hundred users.

When we spoke to many other founders, they all told us the same thing: Go raise, raise big, and raise now. So we did that, even though we were puzzled as to why anyone would give us money with little more than a slide deck to our names. We spent nearly three months pitching dozens of VCs, hoping to raise $3 million to $4 million in a seed round to hire our founding team and build the product out.

Initially, we were excited. There was lots of inbound interest, and we were starting to hear a lot of crazy numbers getting thrown around by a lot of Important People. We thought for sure we were maybe a week away from term sheets. We celebrated preemptively. How could it possibly be this easy?

Then in July, almost in an instant, everything started to dry up. The verbal offers for term sheets didn’t materialize into real offers. We had term sheets, but they were from investors that didn’t seem to care much about what we were building or what problems we wanted to solve. We quickly realized that we hadn’t really built momentum around the product or the vision, but were instead caught up in what we later learned to be “deal flow.”

Basically, investors were interested because other investors were interested. And once enough of them weren’t, nobody was.

Fortunately, as I write this today, Reclaim has raised a total of $6.3 million on great terms across a group of incredible investors and partners. But it wasn’t easy, and it required us to embrace our failure and learn three important lessons that I believe every founder should consider before they decide to go out and pitch investors.

In 2019, we were hunting for what some referred to as a “mango seed” — that is, a seed round that was large enough that it was perceptibly closer to a light Series A financing. Being pre-product at the time, we had to lean on our experience and our vision to drive conviction and urgency among investors. Unfortunately, it just wasn’t enough. Investors either felt that our experience was a bad fit for the space we were entering (productivity/scheduling) or that our vision wasn’t compelling enough to merit investment on the terms we wanted.

When we did get offers, they involved swallowing some pretty bitter pills: We would be forced to take bad terms that were overly dilutive (at least from our perspective), work with an investor who we didn’t think had high conviction in our product strategy, or relinquish control in the company from an extremely early stage. None of these seemed like good options.

Powered by WPeMatico

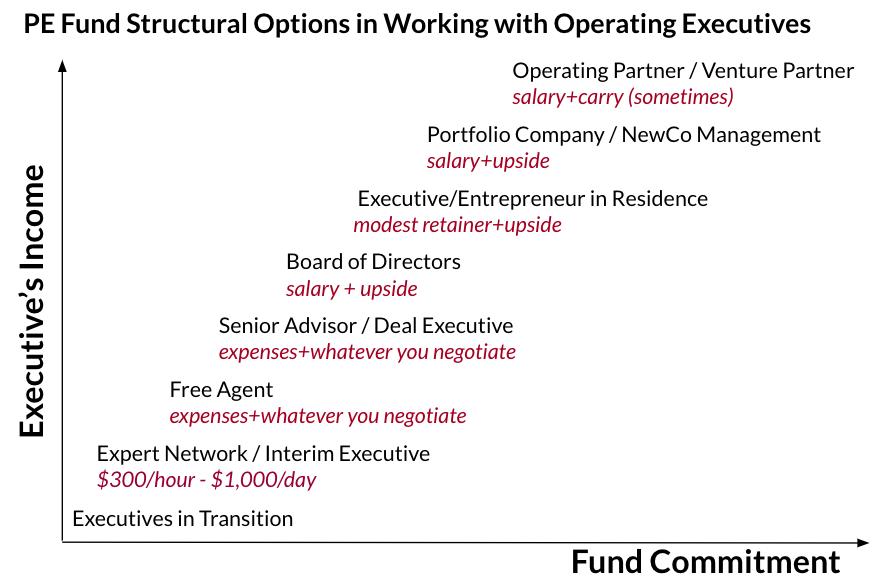

Would you like to work with private equity and venture capital funds?

There are relatively few jobs directly inside private equity and venture capital funds, and those jobs are highly competitive. However, there are many other ways you can work and earn money within the industry — as a consultant, an interim executive, a board member, a deal executive partnering to buy a company, an executive in residence or as an entrepreneur in residence.

Venture capitalists often have an operations background. However, historically most private equity professionals were former investment bankers and other finance professionals. Then private equity players gradually realized that value cannot be created through financial engineering alone. A BCG study of 121 investments found that operational improvement drives 48% of value creation in PE-backed companies. PE funds now almost always require an upgrade in management and change management teams if necessary.

Not surprisingly, the tighter your relationship with the firm, the more money you will earn:

Image Credits: David Teten

At Versatile VC, we’ve used all these models. We are soon launching Founders’ Next Move, a selective, free community for founders researching their next move, which will be a key tool for working with outside talent.

The simplest path forward is to identify funds in your industry of expertise and reach out. You can explore all of the models below with them. First, start by identifying the firms that invest in companies that you’ve worked with. Then, more broadly, look for investors in the industries in which you have expertise. You can identify institutional investors through one of multiple online databases:

| All investors | Private equity | Venture capital |

| Preqin (free demo)

Grey House (free demo) |

PitchBook (free trial)

PrivateEquityFirms.com |

AngelList (free)

CrunchBase (free) PWC MoneyTree (free) VentureDeal (free trial) Asian Venture Capital Journal (free trial) |

Let’s take a look at the different ways you can work with the investment community.

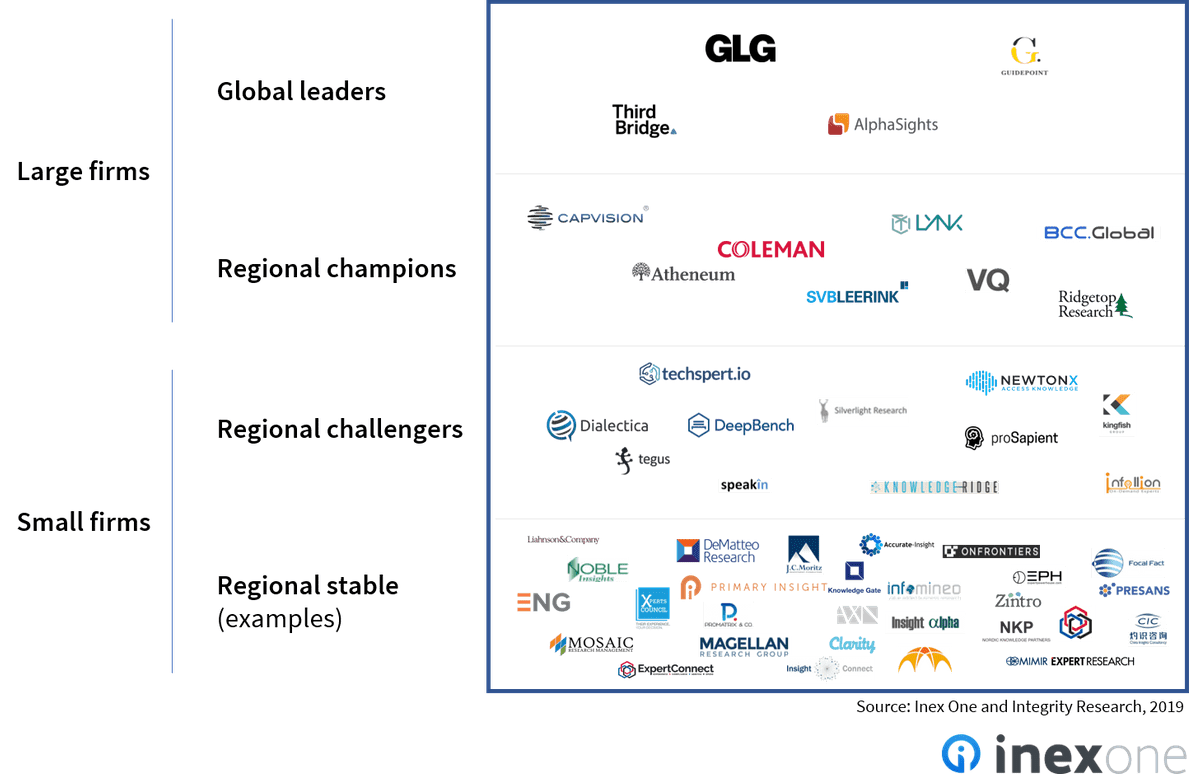

Expert network firms source subject matter experts from various domains and pair them with clients seeking topical or industry insights. They typically charge clients up to $1,200 per hour, and pay the expert $100 to $500 an hour. I founded Circle of Experts, an expert network that I sold to Evalueserve.

The expert network industry has grown an average 4.5% annually between 2015 and 2020, its market size topping $1.3 billion in 2020. While the major clients were initially hedge funds and private equity firms, consulting firms now comprise 32% of total demand for expert network services.

Inex One, an expert network marketplace, has compiled a list of 80 expert networks, summarized in the graphic below:

Image Credits: Inex One and Integrity Research

The largest expert networks include: GLG, which accounts for approximately 50% of the industry’s revenue; AlphaSights is the second biggest generalist expert network; Guidepoint services six major categories of clients globally across several industries; and Third Bridge hires and retains talent to “democratize the world’s human insights and upend the traditional research model.”

Other notable expert networks include Atheneum Partners, Coleman Research Group, Dialectica, ENG, Lynk Global, Mosaic, PreScouter, ProSapient and Tegus. There are also expert networks with sector or geography specialization. For example, SERMO is a global social media network for physicians to exchange knowledge and share challenging patient cases, and Clarity.fm connects startups to experts in building new businesses.

Powered by WPeMatico

Customers have been “experiencing” business since the ancient Romans browsed the Forum for produce, pottery and leather goods. But digitization has radically recalibrated the buyer-seller dynamic, fueling the rise of one of the most talked-about industry acronyms: CX (customer experience).

Part paradigm, part category and part multibillion-dollar market, CX is a broad term used across a myriad of contexts. But great CX boils down to delighting every customer on an emotional level, anytime and anywhere a business interaction takes place.

Great CX boils down to delighting every customer on an emotional level, anytime and anywhere a business interaction takes place.

Optimizing CX requires a sophisticated tool stack. Customer behavior should be tracked, their needs must be understood, and opportunities to engage proactively must be identified. Wall Street, for one, is taking note: Qualtrics, the creator of “XM” (experience management) as a category, was spun-out from SAP and IPO’d in January, and Sprinklr, a social media listening solution that has expanded into a “Digital CXM” platform, recently filed to go public.

Thinking critically about customer experience is hardly a new concept, but a few factors are spurring an inflection point in investment by enterprises and VCs.

Firstly, brands are now expected to create a consistent, cohesive experience across multiple channels, both online and offline, with an ever-increasing focus on the former. Customer experience and the digital customer experience are rapidly becoming synonymous.

The sheer volume of customer data has also reached new heights. As a McKinsey report put it, “Today, companies can regularly, lawfully, and seamlessly collect smartphone and interaction data from across their customer, financial, and operations systems, yielding deep insights about their customers … These companies can better understand their interactions with customers and even preempt problems in customer journeys. Their customers are reaping benefits: Think quick compensation for a flight delay, or outreach from an insurance company when a patient is having trouble resolving a problem.”

Moreover, the app economy continues to raise the bar on user experience, and end users have less patience than ever before. Each time Netflix displays just the right movie, Instagram recommends just the right shoes, or TikTok plays just the right dog video, people are being trained to demand just a bit more magic.

Powered by WPeMatico

When it comes to meeting compliance standards, many startups are dominating the alphabet. From GDPR and CCPA to SOC 2, ISO27001, PCI DSS and HIPAA, companies have been charging toward meeting the compliance standards required to operate their businesses.

Today, every healthcare founder knows their product must meet HIPAA compliance, and any company working in the consumer space would be well aware of GDPR, for example.

But a mistake many high-growth companies make is that they treat compliance as a catchall phrase that includes security. Thinking this could be an expensive and painful error. In reality, compliance means that a company meets a minimum set of controls. Security, on the other hand, encompasses a broad range of best practices and software that help address risks associated with the company’s operations.

It makes sense that startups want to tackle compliance first. Being compliant plays a big role in any company’s geographical expansion to regulated markets and in its penetration to new industries like finance or healthcare. So in many ways, achieving compliance is a part of a startup’s go-to-market kit. And indeed, enterprise buyers expect startups to check the compliance box before signing on as their customer, so startups are rightfully aligning around their buyers’ expectations.

One of the best ways startups can begin tackling security is with an early security hire.

With all of this in mind, it’s not surprising that we’ve witnessed a trend where startups achieve compliance from the very early days and often prioritize this motion over developing an exciting feature or launching a new campaign to bring in leads, for instance.

Compliance is an important milestone for a young company and one that moves the cybersecurity industry forward. It forces startup founders to put security hats on and think about protecting their company, as well as their customers. At the same time, compliance provides comfort to the enterprise buyer’s legal and security teams when engaging with emerging vendors. So why is compliance alone not enough?

First, compliance doesn’t mean security (although it is a step in the right direction). It is more often than not that young companies are compliant while being vulnerable in their security posture.

What does it look like? For example, a software company may have met SOC 2 standards that require all employees to install endpoint protection on their devices, but it may not have a way to enforce employees to actually activate and update the software. Furthermore, the company may lack a centrally managed tool for monitoring and reporting to see if any endpoint breaches have occurred, where, to whom and why. And, finally, the company may not have the expertise to quickly respond to and fix a data breach or attack.

Therefore, although compliance standards are met, several security flaws remain. The end result is that startups can suffer security breaches that end up costing them a bundle. For companies with under 500 employees, the average security breach costs an estimated $7.7 million, according to a study by IBM, not to mention the brand damage and lost trust from existing and potential customers.

Second, an unforeseen danger for startups is that compliance can create a false sense of safety. Receiving a compliance certificate from objective auditors and renowned organizations could give the impression that the security front is covered.

Once startups start gaining traction and signing upmarket customers, that sense of security grows, because if the startup managed to acquire security-minded customers from the F-500, being compliant must be enough for now and the startup is probably secure by association. When charging after enterprise deals, it’s the buyer’s expectations that push startups to achieve SOC 2 or ISO27001 compliance to satisfy the enterprise security threshold. But in many cases, enterprise buyers don’t ask sophisticated questions or go deeper into understanding the risk a vendor brings, so startups are never really called to task on their security systems.

Third, compliance only deals with a defined set of knowns. It doesn’t cover anything that is unknown and new since the last version of the regulatory requirements were written.

For example, APIs are growing in use, but regulations and compliance standards have yet to catch up with the trend. So an e-commerce company must be PCI-DSS compliant to accept credit card payments, but it may also leverage multiple APIs that have weak authentication or business logic flaws. When the PCI standard was written, APIs weren’t common, so they aren’t included in the regulations, yet now most fintech companies rely heavily on them. So a merchant may be PCI-DSS compliant, but use nonsecure APIs, potentially exposing customers to credit card breaches.

Startups are not to blame for the mix-up between compliance and security. It is difficult for any company to be both compliant and secure, and for startups with limited budget, time or security know-how, it’s especially challenging. In a perfect world, startups would be both compliant and secure from the get-go; it’s not realistic to expect early-stage companies to spend millions of dollars on bulletproofing their security infrastructure. But there are some things startups can do to become more secure.

One of the best ways startups can begin tackling security is with an early security hire. This team member might seem like a “nice to have” that you could put off until the company reaches a major headcount or revenue milestone, but I would argue that a head of security is a key early hire because this person’s job will be to focus entirely on analyzing threats and identifying, deploying and monitoring security practices. Additionally, startups would benefit from ensuring their technical teams are security-savvy and keep security top of mind when designing products and offerings.

Another tactic startups can take to bolster their security is to deploy the right tools. The good news is that startups can do so without breaking the bank; there are many security companies offering open-source, free or relatively affordable versions of their solutions for emerging companies to use, including Snyk, Auth0, HashiCorp, CrowdStrike and Cloudflare.

A full security rollout would include software and best practices for identity and access management, infrastructure, application development, resiliency and governance, but most startups are unlikely to have the time and budget necessary to deploy all pillars of a robust security infrastructure.

Luckily, there are resources like Security 4 Startups that offer a free, open-source framework for startups to figure out what to do first. The guide helps founders identify and solve the most common and important security challenges at every stage, providing a list of entry-level solutions as a solid start to building a long-term security program. In addition, compliance automation tools can help with continuous monitoring to ensure these controls stay in place.

For startups, compliance is critical for establishing trust with partners and customers. But if this trust is eroded after a security incident, it will be nearly impossible to regain it. Being secure, not only compliant, will help startups take trust to a whole other level and not only boost market momentum, but also make sure their products are here to stay.

So instead of equating compliance with security, I suggest expanding the equation to consider that compliance and security equal trust. And trust equals business success and longevity.

Powered by WPeMatico

For many VCs, the exit is the endgame; you cash in and move on. But as we know, the startup world is evolving, and that means the impact of investment is no longer limited to how much money is made.

As investors, we’re looking further into what each investment means to human beings, at interlinking our mission with our money. And yet, one of the events that generates the most momentum for long-term impact — the successful exit of a portfolio company — is not being harnessed.

When leveraged properly, an exit can be the beginning of a firm’s true impact, especially when we’re talking about giving all founders equal opportunities and empowering the best ideas. The investment sphere is slowly shaking off its “America first” approach as foreign products take the world by storm and international businesses become the norm.

When leveraged properly, an exit can be the beginning of a firm’s true impact, especially when we’re talking about giving all founders equal opportunities and empowering the best ideas.

Investors will be driving forces in enabling the highest-potential companies to build products that countries everywhere will benefit from — no matter where they were conceived. The way they play the game can transform the industry into one in which a founder from across the ocean has as much of a chance to change the world as one from next door.

We know the basics of how to do this with cash: Investing in underrepresented founders is a necessary first step. But who’s talking about the power of exits to change the playing field for diverse founders? We must consider the psychological motivation of seeing a huge buyout on other entrepreneurs, what that startup’s ex-team members go on to build, and what the achievements of one citizen does for that nation’s reputation.

Last year, 41 venture-backed companies saw a billion-dollar exit, totaling over $100 billion, the highest numbers in a decade. We have an unprecedented amount of clout to do something with those power moves and four ways to turn them into a domino effect.

When a foreign entrepreneur raises money from U.S. firms and sells to a U.S. company, other immigrants see that. Regardless of how groundbreaking their product idea might be, immigrant Americans will always be more wary of putting their eggs into the entrepreneurship basket, at least as long as 93% of all VC money continues to be controlled by white men.

This, despite research suggesting that immigrants contribute 40% more to innovation than local inventors.

What these foreign entrepreneurs most need is confidence, role models and success stories proving other people who look like them have made it, especially when those founders are making waves in the same industry as them.

So a big, well-publicized exit will create momentum in the industry for other foreign founders to give fuel to their venture and seek to take it to the next stage. Not only that, it will instill more self-assurance when it comes to fundraising, and investors will value that.

I was inspired to write this column after Returnly, a fintech founded by a fellow immigrant from Spain based in San Francisco — which, for full transparency, I invested in as an angel investor, and then for Series B and C via my fund — was acquired for $300 million by Affirm.

While there was undoubtedly a personal financial gain worth celebrating, the success of a foreign founder who persevered against the odds in such a competitive ecosystem as Silicon Valley, raised large rounds from U.S.-based investors, and was finally acquired by a U.S. company served as a moment of inspiration for other diverse founders around the world. We saw this in the amount of media attention it received in both business and mainstream press in Spain and the floods of connect requests and congratulations that followed on LinkedIn.

The impact of an exit is greater when it shows foreign entrepreneurs that there are globally minded organizations helping startups like theirs get equal access to funding. That means having VC firms that spotlight international entrepreneurship and foster global expert networks.

As investors, we can maximize the impact of our exits in the industry by highlighting the foreign origins of our founders in a big way when it comes to promoting the exit, including narrating the challenges and opportunities they encountered on their journey. We can use the victory to drive the point home to our fellow investors that diverse and international entrepreneurship is an undervalued gem. We can personally take the win to boost our brand as one that empowers foreign entrepreneurs in that niche, attracting more to seek funding with us in a positive reinforcement cycle.

The windfall from a big exit puts all previous investors in a privileged position, and it’s unlikely that money will sit around for long. They’ll look to reinvest in other high-potential companies — probably ones that look a lot like the one that was just sold.

But in addition to those investors multiplying the positive impact in their own portfolio, they will rally other investors to behave in a similar way.

Each exit — good or bad — sets a precedent for that niche and that type of company. Other investors will follow suit if they sense that one of their peers is onto a cash cow. Because foreign and ethnic minority founders are still underrepresented in startup funding, it makes this field less competitive while harboring huge potential. VCs who have an eye out for unique opportunities will spot when an investor has made a hefty profit from an unconventional startup, especially if they continue to invest in others in that same field.

To help this along, angels and VCs who’ve been behind a recent exit and are reinvesting in similar founders should publicize those knock-on investments, explaining how their previous success motivated them to support similar ventures. They can also be vocal within their network about their decision to raise up certain entrepreneurs because they’ve seen it works.

Returnly’s founder recently offered to put some of his earnings back into our fund, enabling more foreign entrepreneurs like himself to access capital. If as investors we foster meaningful relationships with our funders and truly care about empowering diverse entrepreneurs, we’ll see more of that wealth circle back into our mission.

The PayPal Mafia is a set of former PayPal executives and employees — such as Elon Musk, a South African, and Peter Thiel, a German American — who have gone on to seriously disrupt not one but multiple industries across tech. Among the companies they’ve founded are YouTube, LinkedIn, Yelp and Tesla, and they’ve even been named U.S. ambassadors. That’s just one company. Imagine what other diverse and driven teams can do with the influx of cash and inspiration that comes with a big exit. There will be a ripple effect of team members eager to start out on their own who feel empowered by the success of someone who believed in them.

Their ventures will be more likely to “pass it on” when it comes to giving equal opportunities to people regardless of origin and will generate more jobs for people with their mission. Take Thiel, who has to date backed over 40 companies in Europe alone.

As VCs, we can capitalize on this team effect by keeping our eye on any spinoff ventures that arise and supporting them when possible (with experience and contacts, if not with capital). But beyond this, you can also consider encouraging these people to join the investment sphere, maybe even within your firm. Many successful startup founders and executives go on to become investors — the PayPal Mafia has contributed to some of the most notorious funds out there today. The origin story of these former team members will make them more prone to supporting underrepresented founders they can get behind. In turn, new entrepreneurs will draw more value from their personal experiences.

Although Returnly is headquartered in San Francisco, its founder is Spanish and many of its employees were based in Spain.

That means that the impact of Returnly’s exit will be felt on the other side of the Atlantic as well as among co-nationals in the United States. The same is true of other notable sales, like AlienVault, which was founded in Spain and had multiple offices there. AlienVault was acquired by U.S. telecommunications giant AT&T for $900 million. Or IPOs — earlier this month, the Spanish-origin payments company Flywire filed for an IPO that could value the company at $3 billion. One startup’s success boosts the reputation of its entire team, and with it other founders and talent with their same country of origin, background, education and drive.

It follows that investors and other stakeholders will be more inclined to back opportunities among founders from the same home country if it says something about the mission, expertise and culture they bring to their startup.

At the same time, growing startups will be more interested in hiring the talent of evidently successful teams. That doesn’t just mean hiring more foreign experts in the United States, but seeking to outsource farther afield. We’re already becoming far more comfortable with remote teams, and it’s more capital-efficient for one half of the team to be working while the other half sleeps. But founders will always gravitate more to countries where local talent and innovation is already seen to be thriving. Open up that conversation with your portfolio companies.

VCs have the power to change an industry forever, to connect startup ecosystems across continents and to see startups expand worldwide. But this is about staying relevant as an investor as much as it’s about ensuring this next stage in the startup world is a positive one.

Investors who don’t recognize that the future of startups is global and diverse in nature won’t be in sync with the best opportunities — and won’t be selected by the best founders. Rather than trying to play catchup, help build that ecosystem.

Powered by WPeMatico

Netflix has two CEOs: Co-founder Reed Hastings oversees the streaming side of the company, while Ted Sarandos guides Netflix’s content.

Warby Parker has co-CEOs as well — its co-founders went to college together. Other companies like the tech giant Oracle and luggage maker Away have shifted from having co-CEOs in recent years, sparking a wave of headlines suggesting that the model is broken.

It’s impossible to be in two places at once or clone yourself. With co-CEOs, you can effectively do just that.

While there isn’t a lot of research on companies with multiple CEOs, the data is more promising than the headlines would suggest. One study on public companies with co-CEOs revealed that the average tenure for co-CEOs, about 4.5 years, was comparable to solitary CEOs, “suggesting that this arrangement is more stable than previously believed.”

The study’s authors also found that co-CEOs were spread across industry types and that splitting the role can “complement each other in terms of educational background or executive responsibilities.”

I serve as co-CEO of an organic meal delivery company with my sister Laureen. Having two CEOs has helped us take Fresh n’ Lean to new heights. We closed 2020 with $87 million in revenue, more than double from the year before, and project similar growth this year.

We complement each other well, and the results bear that out. During the decade that we’ve served as co-CEOs, the company has grown from a very small team to 475 full-time employees and 40 part-time employees. We’ve delivered more than 17 million meals, launched four different meal lines, expanded our retail offerings, partnered with some great names in sports and fitness, and saw our annual revenues climb exponentially.

The leadership structure isn’t for every company, but it’s been a great fit for Fresh n’ Lean. Here’s why.

Laureen launched the company in 2010 out of her one-bedroom apartment.

“Those early years were especially tough,” she said. “I consistently worked 20-hour days as I performed just about every role — cooking dishes, preparing labels, making deliveries and performing customer service duties. I was devoting so much energy into product, packaging and logistics, but in order for the company to grow, I needed help with marketing, tech and finance.”

Those areas happened to be my strengths. There was too much for one person to oversee as CEO and not enough hours in the day. But given the equal challenges that both sides of the company presented and the trust we shared, it made sense for us to be side by side on the organizational chart.

Powered by WPeMatico

Venture capitalists add value in a number of ways. For example, one of my business’ backers has a deep tech “pod” that generates events and content we are always welcomed to be a part of. Another one of our investors gives us full commercial support through its network of mentors that are there to support the business, not the VC.

Due diligence works both ways, and entrepreneurs shouldn’t be in a rush to take investment from anyone that offers it.

I might not expect that from every VC, but if they promise those “assets” by saying that they are here to drive innovation and growth, then I expect them to deliver, just as I have to back up the claim of having a team of supersmart machine learning researchers.

They might know the forks in the road, directions to take, and who to speak to based on having been through the process with similar companies. They might have venture partners that can mentor you and a network of investors that can participate in follow-on rounds. That is where they add value.

The best ones will seek to connect with you personally. They’ll have prepared thoroughly beforehand and are brimming with questions. While they may have preconceived and potentially ill-informed ideas, they demonstrate enthusiasm by starting sentences with “what if,” and they leave me emboldened but contemplative. I fully expect to be provoked in the right way.

However, some also play God. One experience offered up a major warning sign, one that would make me walk on by.

I’m pleased to say my business has some outstanding investors who totally get it. Our investors’ head of investment told representatives at one of New York’s top funds that one of their leading deep tech portfolio companies was coming to town for a “blitz meeting session.” They announced that they were committing to the round I was raising and that we were looking for a new lead investor.

So, put it this way: I wasn’t a guy who walked off the street with a crazy idea, but you might have thought otherwise, given the experience that followed. To be clear, I don’t expect all VCs to open their arms and embrace everyone, but there are rules of engagement.

After a very positive morning meeting, I’d scheduled a couple of hours for a quick chance to grab a breather at my hotel. Flicking through my phone, an email from the associate at the VC I was due to meet next pinged into my inbox.

“Hey Ofri, it’s Jessica [not her real name], really sorry, I’m not feeling great so am thinking I might cut the day short. I know you’re only in New York the next two days, so let’s catch up later on a call and next time you’re over I’m sure we can revisit.”

I started composing a polite response: “Really sorry to hear that. Absolutely fine to reschedule. Let me know your availability, etc., etc.” In truth, I was irritated — this had been in the diary for two months and was one of six meetings scheduled. I was not sorry; I was annoyed.

Powered by WPeMatico

Every company wants to be innovative, but innovation comes with its share of difficulties. One key challenge for early-stage companies that are disrupting a particular space or creating a new category is figuring out how to sell a unique product to customers who have never bought such a solution.

This is especially the case when a solution doesn’t have many reference points and its significance may not be obvious.

My view is simple — some buyers could use a walkthrough of the buying process. If you are building a singular product in a nascent market that necessitates forward-looking customers and want to drastically shorten sales cycles, I have a proposal: Create a buyer’s guide.

A buyer’s guide is essentially a prescriptive summary that provides an understandable overview of how a customer may buy your solution.

A buyer’s guide is essentially a prescriptive summary that provides an understandable overview of how a customer may buy your solution. What does your product actually do? Is it secure? How would you implement the technology? What does it replace, if anything? It should be short, simple and speak the customer’s language. It also acts as a sales-enabling tool. Sales teams, especially at smaller startups, can review the guide quarterly and analyze what is and isn’t working as the company goes to market.

Here is how to put together a buyer’s guide, including what to sort out before you type a single word.

From the start, it’s important to think about who the stakeholders are for your product’s buying cycle. One typical issue with early-stage startups is they meet with an enthusiastic buyer — a CIO, CTO or VP of product — but neglect to include the other stakeholders who should be part of the conversation. More importantly, a lot of companies don’t realize the impact of their product on a group or team that they would not typically sell to.

For example, target the security team as an early stakeholder, because they’re probably going to review your product. If the solution is focused toward, say, integration, then hone in on who would be owning the integration process on the buyer’s team.

If you’re selling a martech solution, on a business level, you have to consider a finance business partner for marketing. Think about the problems your customers face and also how others in their company relate to them.

Powered by WPeMatico