Column

Auto Added by WPeMatico

Auto Added by WPeMatico

There’s no shortage of commentary around the chief marketing officer title these days, and certainly no lack of opinions about the role’s responsibilities and meaning within a company. There’s a reason for that. CMO is the shortest tenured C-suite role — the average tenure of a CMO is the lowest of all C-suite titles at 3.5 years.

CMOs either produce the numbers or we find another job.

That’s because the chief marketing officer’s role is increasingly complex. Qualifications require broad, strategic thinking while also maintaining tactical acumen across several functions. There’s a big disparity in what companies expect from CMOs. Some want a strategist with an eye for go-to-market planning, while others want a focus on close alignment with sales in addition to brand awareness, content strategy and lead generation.

Still other companies want their CMO to emphasize product marketing and management. Ask 10 CMOs how they define their role and you’ll get 10 different answers.

So, I’m sharing my honest, straight from the mouth of a tenured CMO take on what the role actually means, plus the key attributes of today’s modern CMO.

Hat tip to “The Lego Movie” for this analogy. Today’s marketing executives must bring functions and teams together. From sales and marketing alignment to product and everything in between, chief marketers are the connective tissue between every function. Driving alignment between these functions is table stakes.

Same goes for people teams and culture — I’ve experienced an increase in CMOs serving as the linchpin of a company’s culture. My CEO lives by the famous phrase “culture eats strategy for breakfast” and driving culture alignment now sits squarely on marketing’s shoulders.

Ah, demand generation. Driving new opportunity creation will continue to be a top priority for CMOs, of course. I’m not sharing anything new here, but the stakes are higher. CMOs either produce the numbers or we find another job. Doesn’t get any more straightforward than that. But, simply generating leads to check a box doesn’t cut it in board rooms anymore.

Powered by WPeMatico

It’s an entrepreneur’s market in digital health today, with startups raising record-breaking funding at soaring valuations and debuting on public markets to eager investors.

According to CB Insights, as of March 3, 2021, there are 51 healthcare unicorns — “startups” — worth $1 billion or more around the world. Global venture capital funding, including private equity and corporate VC, into digital health was the highest ever in the first quarter 2021 at $7.2 billion, according to Mercom Capital Group.

The massive influx of capital to healthcare should not be surprising; the pandemic has made it starkly clear that digital health is the future of healthcare. To that end, we should anticipate additional healthcare exits worth more than $1 billion in the near term. Which again, is great for entrepreneurs — as long as they understand how hard it is to build a unicorn in healthcare. Today, becoming a unicorn requires founders who are long on vision and operational experience.

Today, becoming a unicorn requires founders who are long on vision and operational experience.

Company founders most often turn to veteran investors for help with grand-slam strategies to create the next healthcare unicorn. That’s why many of them seek counsel from the Merck Global Health Innovation Fund: Because we have the experience, resources, successful track record and networks to build real scale in digital health.

During the pandemic, lots of investors jumped in to invest in digital health for the first time. But we’ve been investing for more than a decade. Two of our portfolio companies, Preventice Solutions and Livongo, exited last year as unicorns, rounding out the $6.2 billion in digital health market value MGHIF has exited over the last two years. And we are expecting two more unicorn exits in 2021. But we’re not stopping there; we’ll be investing our $500 million fund in drone-supported supply chain technologies, telehealth, AI, digital pathology, remote clinical trials and Internet of Medical Things (IoMT).

Given our success, here are four instrumental strategies to building a unicorn in digital health that we know work.

We often ask entrepreneurs: Would you rather own 20% of a $50 million company or 5% of a $1 billion company? To most, the answer is obvious. In our experience, too many entrepreneurs worry about dilution and never raise the right amount of capital.

It’s well known that companies with rapidly growing revenues are valued at a premium — but it’s important to remember that this is hard to do in healthcare. Getting to scale takes time because healthcare is so complicated and involves so many stakeholders.

Powered by WPeMatico

Here’s another edition of “Dear Sophie,” the advice column that answers immigration-related questions about working at technology companies.

“Your questions are vital to the spread of knowledge that allows people all over the world to rise above borders and pursue their dreams,” says Sophie Alcorn, a Silicon Valley immigration attorney. “Whether you’re in people ops, a founder or seeking a job in Silicon Valley, I would love to answer your questions in my next column.”

Extra Crunch members receive access to weekly “Dear Sophie” columns; use promo code ALCORN to purchase a one- or two-year subscription for 50% off.

Dear Sophie,

I’ve been working for a large tech company on an H-1B visa for about a year and a half. I’d like to establish my own company while maintaining my current, secure job.

Can I keep working on the H-1B, found my own company, and then have my startup sponsor me for an H-1B or another visa?

— Scrappy in Santa Clara

Hi Scrappy,

You need to be very careful while navigating this process because there are many different legal requirements that you need to pay careful attention to so you comply with U.S. immigration laws. But yes, it is possible for you to own a portion of a business on H-1B, and it is possible for a founder to obtain an H-1B transfer to work at the startup.

Take a listen to a recent podcast episode in which I discuss having two H-1B jobs — or concurrent H-1Bs. Concurrent H-1Bs enable your second employer — in this case, your startup — to avoid having to go through the H-1B lottery process because you have already gone through that process with your current employer.

Be kind to your attorneys — you will need their support to navigate this process! Before you embark on creating your startup, you should review and discuss your employment contract and NDA with an employment lawyer.

Big companies often require employees to obtain their consent prior to forming a startup. You should also consult with an experienced immigration attorney when considering embarking on this path and determining how to structure your startup. The H-1B has specific requirements that you and your startup must meet to qualify.

As you probably already know, the H-1B visa allows you to work for a specific employer in a specific job at a specific location. That means you cannot work for or at your startup under your current H-1B. Therefore, we often advise clients not to found any startup as a sole proprietorship. There will probably need to be a corporation or a limited liability company.

You may be advised to find a co-founder or two. One of the key requirements for the H-1B that you need to keep in mind is your startup and you must have an employer-employee relationship. That means someone at your startup, such as a co-founder, must have the ability to hire you, supervise you, hold you accountable for poor job performance, and fire you, according to the terms and conditions of the H-1B.

Also, you may need to work with a corporate attorney to draft certain bylaws, and it can be helpful if you personally own less than 50% of your startup. All of these things depend on the specific details of your situation, so definitely talk to experienced attorneys to guide you through, step by step!

Image Credits: Joanna Buniak / Sophie Alcorn (opens in a new window)

Your position and your startup must meet other requirements for an H-1B. To qualify for an H-1B, the future position must meet the definition of a “specialty occupation.” That means your position requires theoretical and practical application of highly specialized knowledge.

It also means you must have at least a bachelor’s degree or equivalent experience in a field that’s directly related to the position.

Moreover, your startup must be able to pay you the prevailing wage for the position and for the location where your startup or the position is based. Prevailing wages, which are determined by the U.S. Department of Labor, are broken down into four levels based on experience, with Level I being an entry-level position and Level IV being the most experienced.

Before filing an H-1B petition on your behalf to U.S. Citizenship and Immigration Services (USCIS), your startup’s immigration attorney will have to first submit a Labor Condition Application (LCA) for certification by the Department of Labor. An LCA seeks to ensure that the wages and working conditions of American workers are not negatively impacted by an H-1B position.

Equity in a company and stock options are not considered wages in the H-1B context. Therefore, your startup will need to show that it can afford to pay you the prevailing wage as well as support business operations.

If you’re pre-revenue, this can be shown by a business plan plus your bank statements showing your runway from an initial investment. The amounts required depend on the details of your company’s situation.

There are no restrictions on the number of hours an individual on an H-1B must work. An H-1B position can be full time or part time or involve working just a few hours a week. Take a listen to my podcast on best practices for submitting a strong H-1B petition.

Concurrent H-1B employment can last as long as the original H-1B with your large tech employer. If you want to remain permanently in the United States, you or one of the companies sponsoring your H-1B should apply for a green card at least a year before your sixth year on the H-1B. (If you apply for a green card before your sixth year on an H-1B, the sponsoring employer can continue to extend your H-1B beyond six years until you receive your green card so you don’t have to leave the United States to apply at a U.S. embassy in your home country).

If you want to apply for a green card on your own, consider the EB-1A green card for individuals with extraordinary ability or the EB-2 NIW (National Interest Waiver) for individuals with exceptional ability.

Other employment-based green cards, such as the EB-2 green card for professionals holding advanced degrees and EB-3 for skilled workers and professionals, require an employer to sponsor you as well as the PERM process, which can be challenging if you own substantial equity in the company.

Check with your current employer to find out if the company is willing to sponsor you for a green card. Depending on the timing, you might be able to bypass a second H-1B completely, avoiding the employer-employee relationship restrictions with your startup venture.

The work permit that comes in the I-485 adjustment of status process is unrestricted as to the type of employment in which you can engage!

Wishing you the best on your journey,

Sophie

Have a question for Sophie? Ask it here. We reserve the right to edit your submission for clarity and/or space.

The information provided in “Dear Sophie” is general information and not legal advice. For more information on the limitations of “Dear Sophie,” please view our full disclaimer. You can contact Sophie directly at Alcorn Immigration Law.

Sophie’s podcast, Immigration Law for Tech Startups, is available on all major platforms. If you’d like to be a guest, she’s accepting applications!

Powered by WPeMatico

Domm Holland, co-founder and CEO of e-commerce startup Fast, appears to be living a founder’s dream.

His big idea came from a small moment in his real life. Holland watched as his wife’s grandmother tried to order groceries, but she had forgotten her password and wasn’t able to complete the transaction.

“I just remember thinking it was preposterous,” Holland said. “It defied belief that some arbitrary string of text was a blocker to commerce.”

So he built a prototype of a passwordless authentication system where users would fill out their information once and would never need to do so again. Within 24 hours, tens of thousands of people had used it.

Nothing beats building human networks. That’s the way that you’re going to get this done in terms of fundraising.

Shoppers weren’t the only ones on board with this idea. In less than two years, Holland has raised $124 million in three rounds of fundraising, bringing on partners like Index Ventures and Stripe.

Although the success of Fast’s one-click checkout product has been speedy, it hasn’t been effortless.

For one thing, Holland is Australian, which means he started out as a Silicon Valley outsider. When he arrived in the U.S. in the summer of 2019, he had exactly one Bay Area contact in his phone. He built his network from the ground up, a strategic process he credits to one thing: hard work.

On an episode of the “How I Raised It” podcast, Holland talks about how he built his network, why it’s important — not just for fundraising but for building the entire business — and how to avoid the mistakes he sees new founders make.

Holland’s primary strategy in building networks sounds like an obvious one — reach out to relevant people.

“When I first got to the States, I wanted to build networks,” Holland said, “but I didn’t really know anyone here in the Bay Area. So I spent a lot of time reaching out to relevant people — people working in payments, people working in technology, people working in identity authentication — just really relevant people in the space working in Big Tech who were building large-scale networks.”

One of the people Holland connected with was Allison Barr Allen, then the head of global product operations at Uber. Barr Allen managed her own angel investment fund, but Holland wasn’t actually looking for money when he reached out to her. He was much more interested in her perspective as the leader of an enormous financial services operation.

Powered by WPeMatico

With an increasing number of enterprise systems, growing teams, a rising proliferation of the web and multiple digital initiatives, companies of all sizes are creating loads of data every day. This data contains excellent business insights and immense opportunities, but it has become impossible for companies to derive actionable insights from this data consistently due to its sheer volume.

According to Verified Market Research, the analytics-as-a-service (AaaS) market is expected to grow to $101.29 billion by 2026. Organizations that have not started on their analytics journey or are spending scarce data engineer resources to resolve issues with analytics implementations are not identifying actionable data insights. Through AaaS, managed services providers (MSPs) can help organizations get started on their analytics journey immediately without extravagant capital investment.

MSPs can take ownership of the company’s immediate data analytics needs, resolve ongoing challenges and integrate new data sources to manage dashboard visualizations, reporting and predictive modeling — enabling companies to make data-driven decisions every day.

AaaS could come bundled with multiple business-intelligence-related services. Primarily, the service includes (1) services for data warehouses; (2) services for visualizations and reports; and (3) services for predictive analytics, artificial intelligence (AI) and machine learning (ML). When a company partners with an MSP for analytics as a service, organizations are able to tap into business intelligence easily, instantly and at a lower cost of ownership than doing it in-house. This empowers the enterprise to focus on delivering better customer experiences, be unencumbered with decision-making and build data-driven strategies.

Organizations that have not started on their analytics journey or are spending scarce data engineer resources to resolve issues with analytics implementations are not identifying actionable data insights.

In today’s world, where customers value experiences over transactions, AaaS helps businesses dig deeper into their psyche and tap insights to build long-term winning strategies. It also enables enterprises to forecast and predict business trends by looking at their data and allows employees at every level to make informed decisions.

Powered by WPeMatico

In the early 2000s, Jeff Bezos gave a seminal TED Talk titled “The Electricity Metaphor for the Web’s Future.” In it, he argued that the internet will enable innovation on the same scale that electricity did.

We are at a similar inflection point in healthcare, with the recent movement toward data transparency birthing a new generation of innovation and startups.

Those who follow the space closely may have noticed that there are twin struggles taking place: a push for more transparency on provider and payer data, including anonymous patient data, and another for strict privacy protection for personal patient data. What’s the main difference?

This sector is still somewhat nascent — we are in the first wave of innovation, with much more to come.

Anonymized data is much more freely available, while personal data is being locked even tighter (as it should be) due to regulations like GDPR, CCPA and their equivalents around the world.

The former trend is enabling a host of new vendors and services that will ultimately make healthcare better and more transparent for all of us.

These new companies could not have existed five years ago. The Affordable Care Act was the first step toward making anonymized data more available. It required healthcare institutions (such as hospitals and healthcare systems) to publish data on costs and outcomes. This included the release of detailed data on providers.

Later legislation required biotech and pharma companies to disclose monies paid to research partners. And every physician in the U.S. is now required to be in the National Practitioner Identifier (NPI), a comprehensive public database of providers.

All of this allowed the creation of new types of companies that give both patients and providers more control over their data. Here are some key examples of how.

This is a key capability of patients’ newly found access to health data. Think of how often, as a patient, providers aren’t aware of treatment or a test you’ve had elsewhere. Often you end up repeating a test because a provider doesn’t have a record of a test conducted elsewhere.

Powered by WPeMatico

Why can we see all our bank, credit card and brokerage data on our phones instantaneously in one app, yet walk into a doctor’s office blind to our healthcare records, diagnoses and prescriptions? Our health status should be as accessible as our checking account balance.

The liberation of financial data enabled by startups like Plaid is beginning to happen with healthcare data, which will have an even more profound impact on society; it will save and extend lives. This accessibility is quickly approaching.

As early investors in Quovo and PatientPing, two pioneering companies in financial and healthcare data, respectively, it’s evident to us the winners of the healthcare data transformation will look different than they did with financial data, even as we head toward a similar end state.

For over a decade, government agencies and consumers have pushed for this liberation.

This push for greater data liquidity coincides with demand from consumers for better information about cost and quality.

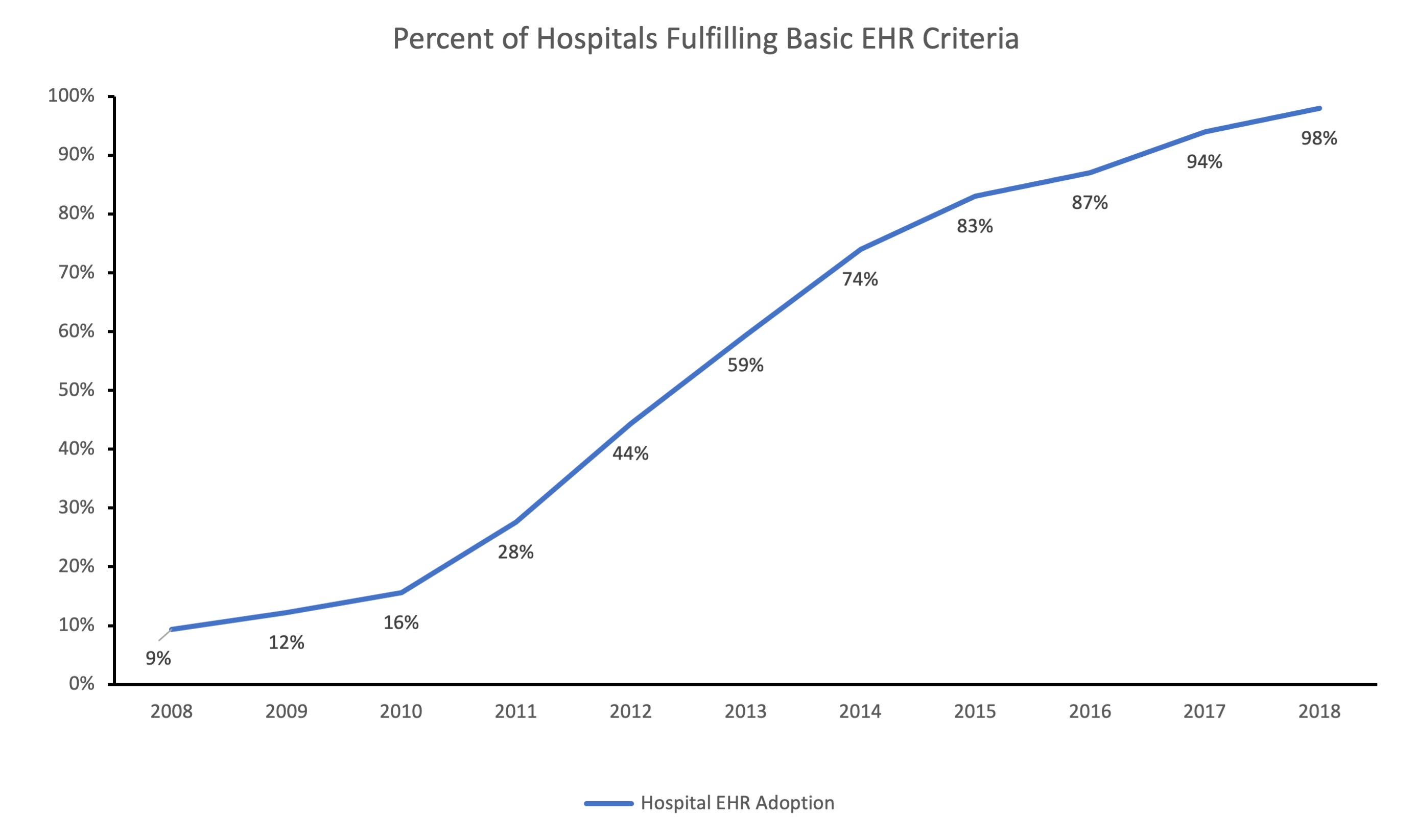

In 2009, the Health Information Technology for Economic and Clinical Health Act (HITECH) gave the first big industry push, catalyzing a wave of digitization through electronic health records (EHR). Today, over 98% of medical records are digitized. This market is dominated by multibillion‐dollar vendors like Epic, Cerner and Allscripts, which control 70% of patient records. However, these giant vendors have yet to make these records easily accessible.

A second wave of regulation has begun to address the problem of trapped data to make EHRs more interoperable and valuable. Agencies within the Department of Health and Human Services have mandated data sharing among payers and providers using a common standard, the Fast Healthcare Interoperability Resources (FHIR) protocol.

Image Credits: F-Prime Capital

This push for greater data liquidity coincides with demand from consumers for better information about cost and quality. Employers have been steadily shifting a greater share of healthcare expenses to consumers through high-deductible health plans — from 30% in 2012 to 51% in 2018. As consumers pay for more of the costs, they care more about the value of different health options, yet are unable to make those decisions without real-time access to cost and clinical data.

Image Credits: F-Prime Capital

Tech startups have an opportunity to ease the transmission of healthcare data and address the push of regulation and consumer demands. The lessons from fintech make it tempting to assume that a Plaid for healthcare data would be enough to address all of the challenges within healthcare, but it is not the right model. Plaid’s aggregator model benefited from a relatively high concentration of banks, a limited number of data types and low barriers to data access.

By contrast, healthcare data is scattered across tens of thousands of healthcare providers, stored in multiple data formats and systems per provider, and is rarely accessed by patients directly. Many people log into their bank apps frequently, but few log into their healthcare provider portals, if they even know one exists.

HIPPA regulations and strict patient consent requirements also meaningfully increase friction to data access and sharing. Financial data serves mostly one-to-one use cases, while healthcare data is a many-to-many problem. A single patient’s data is spread across many doctors and facilities and is needed by just as many for care coordination.

Because of this landscape, winning healthcare technology companies will need to build around four propositions:

Powered by WPeMatico

Almost two centuries ago, gold prospectors in California set off one of the greatest rushes for wealth in history. Proponents of socially conscious investing claim fund managers will start a similar stampede when they discover that environmental, social and governance (ESG) insights can yield treasure in the form of alternative data that promise big payoffs — if only they knew how to mine it.

First, let’s be clear: ESG is not on the fringe.

There may be some truth to that line of thinking if you take some of the rhetoric and advertising out of the equation.

First, let’s be clear: ESG is not on the fringe. The European Union has implemented new financial regulations via the Sustainable Finance Disclosure Regulation (SFDR). These improve ESG disclosures and considerations and help to direct capital toward products and companies that benefit people and the planet. As we write, the U.S. Securities and Exchange Commission is also considering drafting and implementation of ESG-related regulations.

Whether enacted or currently under consideration, these rules encourage fund managers to integrate sustainability risks into their business processes, report on them publicly, stamp out greenwashing, and promote transparency and knowledge among investors. Accordingly, it will become easier to compare firms’ sustainability efforts, too, allowing stakeholders from all corners to make more informed decisions.

Incorporating ESG factors into investment strategies is not new, of course. The world’s largest asset managers have been practicing it for years. According to the Governance & Accountability Institute, 90% of companies listed on the S&P 500 now produce sustainability reports, an increase of 70 percentage points from more than a decade ago.

Yet some are still groaning about adopting an ESG investing mindset; they see ESG as a nuisance that detracts from their mission of earning high returns. But could this mindset mean they are missing important opportunities?

Waiting for new mandatory ESG reporting and compliance framework standards in the U.S. puts Americas-focused managers at a significant disadvantage. Fund managers can start gaining insights today from alternative data originating in ESG-related data stemming from climate change, natural disasters, harassment and discrimination lawsuits, and other events and information that can be mined.

Powered by WPeMatico

Let’s be clear: The venture capital industry has lacked diversity. The good news is the industry is working to improve itself.

To begin with, as an industry, venture capital can only improve what we measure. In 2016, we set out to develop a rigorous methodology for tracking progress on diversity, equity and inclusion (DEI) in venture capital, and to measure and benchmark those data through our biennial VC Human Capital Survey.

The goals of the survey — powered by the National Venture Capital Association, Venture Forward and Deloitte — are to collect demographic data on the VC workforce across all firm types, sizes, stages, sectors and geographies, as well as trends on firm talent management and recruitment practices. We’ve learned that progress can be slow and seem discouraging, but we’ve also captured evidence that diversity (and firm practices to advance diversity) is increasing in some areas, even as other areas have unfortunately not seen the same pace of change.

To begin with, as an industry, venture capital can only improve what we measure.

We fielded the survey in 2016, 2018 and 2020, and released the outcomes of the third edition last month, featuring data (as of June 30, 2020) collected from 378 firms, a marked increase from 203 participating firms in 2018. Furthermore, more than 145 firms signed the #VCHumanCapital pledge to publicly commit to submitting their DEI data.

At a high level, the data showed that improvements in diversity among investment partners have largely been driven by the hiring and advancement of female investors, while there has been little progress in the equitable representation of Black or Hispanic investment partners.

However, the demographic composition of junior investment professionals reflects greater diversity and wider adoption of diversity-focused talent management and recruitment practices suggest some cause for optimism. The industry still has a long way to go, but here are some of the key insights and changes we identified from the latest survey.

More firms are explicitly assigning responsibility for promoting diversity and inclusion internally — 50% of firms have a staff person or team tasked with this responsibility (compared with 34% in 2018 and 16% in 2016). Simultaneously, diversity and inclusion strategies have become more widespread; 43% of firms have implemented a diversity strategy (against 32% in 2018 and 24% in 2016), while 41% have an inclusion strategy (versus 31% in 2018 and 17% in 2016).

This intentionality translates to improved diversity outcomes. Firms with dedicated DEI staff, strategies and programs achieve greater gender and racial diversity on investment teams and among investment partners. The increased emphasis on DEI is also a broader ecosystem trend. More firms report that limited partners and portfolio companies have requested their DEI details over the past 12 months.

Venture firms are relatively small and turnover is generally low, but 21% of firms in 2020 reported their number of senior-level investment positions had increased, while 43% said their number of junior-level positions had expanded. Meanwhile, the demographic composition of junior investment professionals reflects higher gender and racial diversity, a positive leading indicator for the diversity of future investment partners.

As overall DEI strategies have become increasingly widespread, more firms have also developed DEI-focused recruitment and hiring programs — 33% of firms have formal programs, while 74% have informal programs, both reflecting steady increases from 2016. Firms were also more likely to report that they typically seek external candidates for open positions than they did in 2018.

However, firms continue to largely rely on internal networks for recruitment, which often encourages homogeneous hiring outcomes. Between the 2018 and 2020 surveys, there was little change shown in the use of narrow recruitment methods to find external candidates; notifying peers in the VC industry (78%) and notifying the firm internally (59%) were the strategies cited most often. The exception was posting on third-party websites like LinkedIn or in newsletters, a strategy reported by 54% of firms in 2020 (a substantial increase from 37% in 2018), which presents one avenue to reach a broader audience of candidates outside of existing networks.

Once talent has come on board, inclusive culture and retention become key metrics of DEI progress. More firms are implementing programs dedicated to leadership development, mentorship and retention, with about two-thirds reporting informal versions of such programs (20 percentage points higher than in 2016) and 20% of firms reporting formal programs.

Assessing inclusion through the VC Human Capital Survey is challenging because we survey one representative per firm, and one person cannot speak to the degree of inclusion felt by others. However, we added a new question to the 2020 survey to gauge how firms themselves are assessing inclusion. While 41% of firms reported having an inclusion strategy, only 26% said they conduct surveys of their employees to assess inclusion.

Well-structured, consistently applied policies for career advancement are critical to ensuring that diverse talent reaches the most senior decision-making levels of the industry. About 20% of firms reported having formal DEI programs focused on promotion (up from 5% in 2016), while 65% of firms have informal programs (compared with 39% in 2016).

Although DEI programs focused on the promotion of employees are more widespread, subjective factors remain a key consideration for promotion decisions, which can lead to unequal and biased outcomes.

Almost all firms reported that “contributions to the performance of the fund” (90%) and “deal origination” (82%) were very important or important factors in considering promotions. However, the factor most often rated highly was “soft skills,” with 94% of firms saying it was very important or important. These types of subjective factors present significant opportunity for unconscious bias to creep in and can detract from the weight given to objective measures more demonstrably relevant to performance.

The results of the third edition of our survey are timely, coming on the heels of a year in which social justice and racial equity have been the subjects of sharp national focus, policymakers have sought to increase access to capital for underserved communities, and the VC industry has shown a renewed focus on DEI. The survey shows where the VC industry’s efforts should be focused and also serves as an important reminder of the intersectional needs of DEI-focused initiatives.

The data show that progress within one demographic element can be more nuanced when considering people who represent multiple marginalized communities (e.g., the percentage of investment partners who are women has steadily increased, but the percentage of investment partners who are women of color has not).

The pace of DEI progress has been slow and uneven in some areas, but there are reasons for optimism. On April 6, NVCA, Venture Forward and Deloitte hosted a discussion with industry leaders to further examine the latest survey results and to address DEI challenges, opportunities and strategies for the industry. More firms are prioritizing these constructive conversations, both within their firms and publicly with industry peers. More firms are acting in a collaborative spirit, adopting thoughtful and concrete DEI strategies and acting with intentionality and urgency.

If the industry can continue to build upon this momentum and commitment around DEI efforts, we can reach a tipping point that will translate to meaningful progress reflected in future editions of the survey.

Powered by WPeMatico

There’s a disconnect between reality and the added value investors are promising entrepreneurs. Three in five founders who were promised added value by their VCs felt duped by their negative experience.

While this feels like a letdown by investors, in reality, it shows fault on both sides. Due diligence isn’t a one-way street, and founders must do their homework to make sure they’re not jumping into deals with VCs who are only paying lip service to their value-add.

Looking into an investor’s past, reputation and connections isn’t about finding the perfect VC, it’s about knowing what shaking certain hands will entail — and either being ready for it or walking away.

Entrepreneurs are increasingly demanding more than a blank check: They want mentorship, product understanding and emotional support, as well as industry connections and expertise. If VCs can’t bring that value, founders now have plenty of other funding routes to choose from, like crowdfunding, angel syndicates, tokenization and SPACs.

To stay competitive, VCs have to at least advertise that they have more than deep pockets. But what if it stops there? Founders have to know exactly what they’re looking for in a VC, which means looking past the front page and vetting their investors.

The ideal investor for modern startups is an operator VC — someone who was a founder or operator at a company before becoming an investor. But even then, ticking boxes isn’t enough to ensure the investor won’t come with their own challenges, like being too hands-on or less strategically minded.

Looking into an investor’s past, reputation and connections isn’t about finding the perfect VC, it’s about knowing what shaking certain hands will entail — and either being ready for it or walking away. There is no single solution to this issue, but here are my recommendations to founders seeking a successful investor relationship in 2021.

No founder-investor relationship can survive misalignment. Because you share responsibility on so many processes, both parties have to be on the same page. So before you even start fundraising, nail down the expectations you need your future investor to meet. What do you need the most? What does your dream investor look like?

Powered by WPeMatico