Column

Auto Added by WPeMatico

Auto Added by WPeMatico

Last year was a record 12 months for venture-backed biotech and pharma companies, with deal activity rising to $28.5 billion from $17.8 billion in 2019. As vaccines roll out, drug development pipelines return to normal, and next-generation therapies continue to hold investor interest, 2021 is on pace to be another blockbuster year.

The median step up in valuations from seed to Series A is now 2x, higher than in all later rounds. As a result, biotech startups will continue to attract more investment at earlier stages from a larger, more diverse pool of venture capitalists.

This may also change the nature of biotech founders themselves: As a blog post from Y Combinator suggests, these founders are trending younger and perhaps less willing to cede control to VCs and hired executives than they might have in years past (i.e., via the “venture creation” model so predominant among early-stage biotech companies).

Founders are some of the most creative people out there, but legal documentation should be anything but.

As longtime members of the biotech startup community — as executives, entrepreneurs, advisors and legal counsel — we’ve seen our fair share of founder missteps early in the fundraising journey result in severe consequences.

In this exciting moment, when younger founders will likely receive more attention, capital and control than ever, it’s crucial to avoid certain pitfalls.

Founders are some of the most creative people out there, but legal documentation should be anything but. Keep it as simple and clear as possible. That means using National Venture Capital Corporation documents that everyone knows and understands, as well as keeping organized documentation for employee intellectual property (IP) assignment and NDAs, option grants, independent contractor agreements, tax documents and other key contracts and paperwork.

Powered by WPeMatico

The clock begins ticking on a startup the day the doors open. Regardless of a young company’s struggles or success, sooner or later the question of when, how or whether to sell the enterprise presents itself. It’s possibly the biggest question an entrepreneur will face.

For founders who self-funded (bootstrapped) their startup, a boardroom full of additional factors come into play. Some are the same as for investor-funded firms, but many are unique.

Put happiness at the center of the decision, and let your intuition — the instincts that made you the person you are today — be your guide.

After 18 years of bootstrapping a BI software firm into a business that now serves 28,000 companies and three million users in 75 countries, here’s what I’ve learned about myself, my company, about entrepreneurship and about when to grab for that brass ring.

Starting a software company 7,900 miles southwest of Silicon Valley requires some forethought and not a small amount of crazy. When we opened, it didn’t occur to us that one could have an idea and then go knock on someone’s door and ask for money.

Bootstrapping forced us to be a bit more creative about how we would go about building our company. In the early days, it was a distraction to growth, because we were doing other revenue-generating activities like consulting, development work, whatever we could find to keep ourselves afloat while we built Yellowfin. It meant we couldn’t be 100% focused on our idea.

However, it also meant we had to generate income from our new company from Day One — something funded companies don’t have to do. We never got into the mindset that it was okay to burn lots of cash and then cross our fingers and hope that it worked.

Powered by WPeMatico

When the world flipped upside down last year, nearly every company in every industry was forced to implement a remote workforce in just a matter of days — they had to scramble to ensure employees had the right tools in place and customers felt little to no impact. While companies initially adopted solutions for employee safety, rapid response and short-term air cover, they are now shifting their focus to long-term, strategic investments that empower growth and streamline operations.

As a result, categories that make up productivity infrastructure — cloud communications services, API platforms, low-code development tools, business process automation and AI software development kits — grew exponentially in 2020. This growth was boosted by an increasing number of companies prioritizing tools that support communication, collaboration, transparency and a seamless end-to-end workflow.

Productivity infrastructure is on the rise and will continue to be front and center as companies evaluate what their future of work entails and how to maintain productivity, rapid software development and innovation with distributed teams.

According to McKinsey & Company, the pandemic accelerated the share of digitally enabled products by seven years, and “the digitization of customer and supply-chain interactions and of internal operations by three to four years.” As demand continues to grow, companies are taking advantage of the benefits productivity infrastructure brings to their organization both internally and externally, especially as many determine the future of their work.

Developers rely on platforms throughout the software development process to connect data, process it, increase their go-to-market velocity and stay ahead of the competition with new and existing products. They have enormous amounts of end-user data on hand, and productivity infrastructure can remove barriers to access, integrate and leverage this data to automate the workflow.

Access to rich interaction data combined with pre-trained ML models, automated workflows and configurable front-end components enables developers to drastically shorten development cycles. Through enhanced data protection and compliance, productivity infrastructure safeguards critical data and mitigates risk while reducing time to ROI.

As the post-pandemic workplace begins to take shape, how can productivity infrastructure support enterprises where they are now and where they need to go next?

Powered by WPeMatico

The tidal wave of growth is upon us — an unprecedented economic boom that will manifest later this year, bringing significant investments, acquisitions and customer growth. But most tech companies and startups are not adequately prepared to capitalize on the opportunity that lies ahead.

Here’s how marketing in tech will shift — and what you need to know to reach more customers and accelerate growth in 2021.

First and foremost, differentiation is going to be imperative. It’s already hard enough to stand out and get noticed, and it’s about to get much more difficult as new companies emerge and investments and budgets balloon in the latter half of the year. Virtually all major companies are increasing budgets to pre-pandemic levels, but will delay those investments until the second half of the year. This will result in an increased intensity of competition that will drown out any undifferentiated players.

The second half of 2021 will bring incredible growth, the likes of which we haven’t seen in a long time.

Additionally, tech companies need to be mindful not to ignore the most important part of the ecosystem: people. Technology will only take you so far, and it’s not going to be enough to survive the competition. Marketing is about people, including your customers, team, partners, investors and the broader community.

Understanding who your people are and how you can use their help to build a strong foundation and drive exponential growth is essential.

Tactically, the most successful tech companies will embrace video and experimentation in their marketing — two components that will catapult them ahead of the competition.

Ignoring these predictions, backed by empirical evidence, will be detrimental and devastating. Fasten your seatbelts: 2021 is going to be a turbocharged year of growth opportunities for marketing in tech.

The explosion of tech companies and startups seeking to be the next big thing isn’t over yet. However, many of them are indistinguishable from each other and lack a compelling value proposition. Just one look at the websites of new and existing tech companies will reveal a proliferation of buzzwords and conceptual illustrations, leaving them all looking and sounding alike.

The tech companies that succeed are those that embrace one of the fundamentals of effective marketing — positioning.

In the ’80s, Al Ries and Jack Trout published “Positioning: The Battle For Your Mind” and coined the term, which documented the best-known approach to standing out in a noisy marketplace. As the market heats up, companies will realize the need to sharpen their positioning and dial in their focus to break through the noise.

To get attention and build traction, companies need to establish a position they can own. The mashup method — “Netflix but for coding lessons” — is not real positioning; it’s simply a lazy gimmick.

It is imperative to identify who your ideal customer is and not just who could use your product. Focusing on a segment of the market rather than the whole is, perhaps counterintuitively, the most effective approach to capturing the larger market.

Powered by WPeMatico

Many emerging and mature organizations survive or die based on their ability to scale. Scale quicker. Scale cheaper. Scale right.

Typically the IT team bears that burden — on top of countless other demands. IT teams move mountains for their organizations while scaling the tech platform as fast as possible, putting out the latest infrastructure fire and responding to countless day-to-day requests.

The most helpful gift any chief information officer or chief technology officer can give their IT teams is more time. Many people think that means adding another team member. Maybe it does in some cases (if you can find a developer in this tough job market), but giving my team Boomi’s low-code integration platform was one of the best strategic moves for HealthBridge.

The best time to use low-code is when you need to add something to your organization that isn’t unique or doesn’t drive significant business value.

As the least skilled coder on the team, low-code let me develop and deliver four customer-centric self-service portals a year ahead of schedule while my team focused on building and scaling our revenue-driving, custom platform by hand-writing code.

Low-code is quickly becoming commonplace and a popular topic among IT decision-makers. Over the last few years, the market has exploded. Gartner expects it to total $13.8 billion in 2021. That means low-code technology, which we’ve been hearing about for years, is ready for widespread adoption. Today, low-code enables you to streamline (and scale) everything from integration to artificial intelligence.

It’s a secret only some organizations are clued in on, but it’s a great way to scale fast, save on resources and give your team more time. Here’s how.

The best time to use low-code is when you need to add something to your organization that isn’t unique or doesn’t drive significant business value.

For instance, a customer portal is not unique; don’t waste time hand-coding it.

While it’s certainly an extremely helpful feature for our customers, it’s unlikely to drive significant shareholder or investor value. However, it’s key for scaling. Using low-code for a must-have but undifferentiated feature will allow your team to work on more important projects while scaling.

When we started working on the timeline for a customer portal project at HealthBridge, we estimated it would take several sprints per portal to develop, but more pressing development work kept pushing it down the list in our backlog. Waiting a year for a basic feature didn’t seem reasonable to me, so we looked for a workaround.

Powered by WPeMatico

By 2025, 463 exabytes of data will be created each day, according to some estimates. (For perspective, one exabyte of storage could hold 50,000 years of DVD-quality video.) It’s now easier than ever to translate physical and digital actions into data, and businesses of all types have raced to amass as much data as possible in order to gain a competitive edge.

However, in our collective infatuation with data (and obtaining more of it), what’s often overlooked is the role that storytelling plays in extracting real value from data.

The reality is that data by itself is insufficient to really influence human behavior. Whether the goal is to improve a business’ bottom line or convince people to stay home amid a pandemic, it’s the narrative that compels action, rather than the numbers alone. As more data is collected and analyzed, communication and storytelling will become even more integral in the data science discipline because of their role in separating the signal from the noise.

Data alone doesn’t spur innovation — rather, it’s data-driven storytelling that helps uncover hidden trends, powers personalization, and streamlines processes.

Yet this can be an area where data scientists struggle. In Anaconda’s 2020 State of Data Science survey of more than 2,300 data scientists, nearly a quarter of respondents said that their data science or machine learning (ML) teams lacked communication skills. This may be one reason why roughly 40% of respondents said they were able to effectively demonstrate business impact “only sometimes” or “almost never.”

The best data practitioners must be as skilled in storytelling as they are in coding and deploying models — and yes, this extends beyond creating visualizations to accompany reports. Here are some recommendations for how data scientists can situate their results within larger contextual narratives.

Ever-growing datasets help machine learning models better understand the scope of a problem space, but more data does not necessarily help with human comprehension. Even for the most left-brain of thinkers, it’s not in our nature to understand large abstract numbers or things like marginal improvements in accuracy. This is why it’s important to include points of reference in your storytelling that make data tangible.

For example, throughout the pandemic, we’ve been bombarded with countless statistics around case counts, death rates, positivity rates, and more. While all of this data is important, tools like interactive maps and conversations around reproduction numbers are more effective than massive data dumps in terms of providing context, conveying risk, and, consequently, helping change behaviors as needed. In working with numbers, data practitioners have a responsibility to provide the necessary structure so that the data can be understood by the intended audience.

Powered by WPeMatico

If the definition of insanity is doing the same thing over and over and expecting a different outcome, then one might say the cybersecurity industry is insane.

Criminals continue to innovate with highly sophisticated attack methods, but many security organizations still use the same technological approaches they did 10 years ago. The world has changed, but cybersecurity hasn’t kept pace.

Distributed systems, with people and data everywhere, mean the perimeter has disappeared. And the hackers couldn’t be more excited. The same technology approaches, like correlation rules, manual processes and reviewing alerts in isolation, do little more than remedy symptoms while hardly addressing the underlying problem.

The current risks aren’t just technology problems; they’re also problems of people and processes.

Credentials are supposed to be the front gates of the castle, but as the SOC is failing to change, it is failing to detect. The cybersecurity industry must rethink its strategy to analyze how credentials are used and stop breaches before they become bigger problems.

Compromised credentials have long been a primary attack vector, but the problem has only grown worse in the midpandemic world. The acceleration of remote work has increased the attack footprint as organizations struggle to secure their network while employees work from unsecured connections. In April 2020, the FBI said that cybersecurity attacks reported to the organization grew by 400% compared to before the pandemic. Just imagine where that number is now in early 2021.

It only takes one compromised account for an attacker to enter the active directory and create their own credentials. In such an environment, all user accounts should be considered as potentially compromised.

Nearly all of the hundreds of breach reports I’ve read have involved compromised credentials. More than 80% of hacking breaches are now enabled by brute force or the use of lost or stolen credentials, according to the 2020 Data Breach Investigations Report. The most effective and commonly-used strategy is credential stuffing attacks, where digital adversaries break in, exploit the environment, then move laterally to gain higher-level access.

Powered by WPeMatico

Data is the most valuable asset for any business in 2021. If your business is online and collecting customer personal information, your business is dealing in data, which means data privacy compliance regulations will apply to everyone — no matter the company’s size.

Small startups might not think the world’s strictest data privacy laws — the California Consumer Privacy Act (CCPA) and Europe’s General Data Protection Regulation (GDPR) — apply to them, but it’s important to enact best data management practices before a legal situation arises.

Data compliance is not only critical to a company’s daily functions; if done wrong or not done at all, it can be quite costly for companies of all sizes.

For example, failing to comply with the GDPR can result in legal fines of €20 million or 4% of annual revenue. Under the CCPA, fines can also escalate quickly, to the tune of $2,500 to $7,500 per person whose data is exposed during a data breach.

If the data of 1,000 customers is compromised in a cybersecurity incident, that would add up to $7.5 million. The company can also be sued in class action claims or suffer reputational damage, resulting in lost business costs.

It is also important to recognize some benefits of good data management. If a company takes a proactive approach to data privacy, it may mitigate the impact of a data breach, which the government can take into consideration when assessing legal fines. In addition, companies can benefit from business insights, reduced storage costs and increased employee productivity, which can all make a big impact on the company’s bottom line.

Data compliance is not only critical to a company’s daily functions; if done wrong or not done at all, it can be quite costly for companies of all sizes. For example, Vodafone Spain was recently fined $9.72 million under GDPR data protection failures, and enforcement trackers show schools, associations, municipalities, homeowners associations and more are also receiving fines.

GDPR regulators have issued $332.4 million in fines since the law was enacted almost two years ago and are being more aggressive with enforcement. While California’s attorney general started CCPA enforcement on July 1, 2020, the newly passed California Privacy Rights Act (CPRA) only recently created a state agency to more effectively enforce compliance for any company storing information of residents in California, a major hub of U.S. startups.

That is why in this age, data privacy compliance is key to a successful business. Unfortunately, many startups are at a disadvantage for many reasons, including:

Powered by WPeMatico

More than half a decade ago, my Battery Ventures partner Neeraj Agrawal penned a widely read post offering advice for enterprise-software companies hoping to reach $100 million in annual recurring revenue.

His playbook, dubbed “T2D3” — for “triple, triple, double, double, double,” referring to the stages at which a software company’s revenue should multiply — helped many high-growth startups index their growth. It also highlighted the broader explosion in industry value creation stemming from the transition of on-premise software to the cloud.

Fast forward to today, and many of T2D3’s insights are still relevant. But now it’s time to update T2D3 to account for some of the tectonic changes shaping a broader universe of B2B tech — and pushing companies to grow at rates we’ve never seen before.

One of the biggest factors driving billion-dollar B2Bs is a simple but important shift in how organizations buy enterprise technology today.

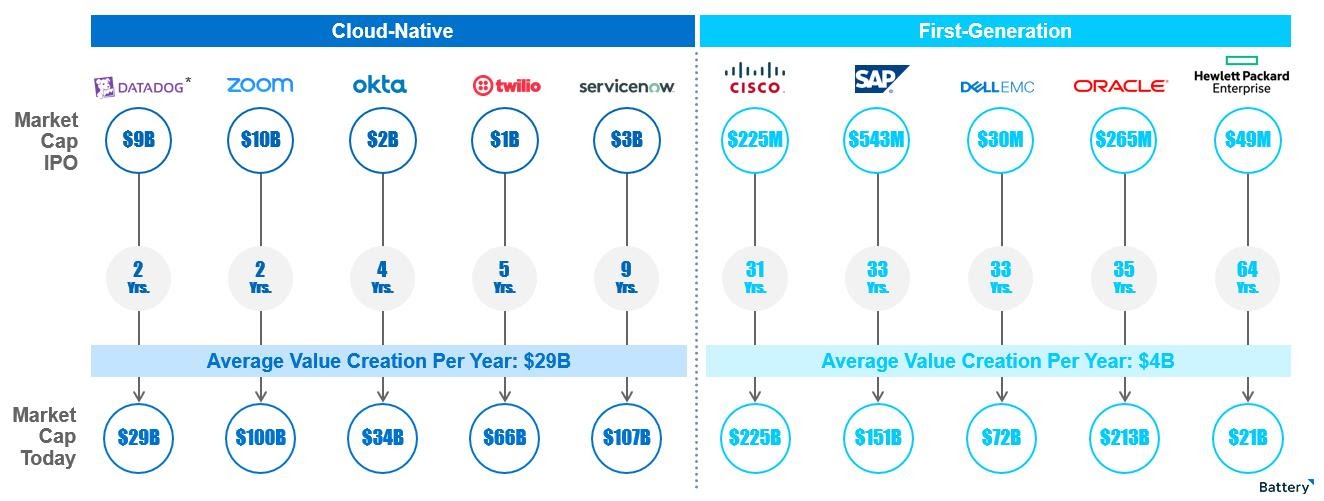

I call this new paradigm “billion-dollar B2B.” It refers to the forces shaping a new class of cloud-first, enterprise-tech behemoths with the potential to reach $1 billion in ARR — and achieve market capitalizations in excess of $50 billion or even $100 billion.

In the past several years, we’ve seen a pioneering group of B2B standouts — Twilio, Shopify, Atlassian, Okta, Coupa*, MongoDB and Zscaler, for example — approach or exceed the $1 billion revenue mark and see their market capitalizations surge 10 times or more from their IPOs to the present day (as of March 31), according to CapIQ data.

More recently, iconic companies like data giant Snowflake and video-conferencing mainstay Zoom came out of the IPO gate at even higher valuations. Zoom, with 2020 revenue of just under $883 million, is now worth close to $100 billion, per CapIQ data.

Image Credits: Battery Ventures via FactSet. Note that market data is current as of April 3, 2021.

In the wings are other B2B super-unicorns like Databricks* and UiPath, which have each raised private financing rounds at valuations of more than $20 billion, per public reports, which is unprecedented in the software industry.

Powered by WPeMatico

More individuals than ever are donning the investor cap. Almost a fifth of U.S. equity trading in 2020 was driven by mom-and-pop investors — up from around 15% in the previous year. With such impressive returns to be made, many are deciding to set up a full-fledged investment business.

With the fundraising world becoming more democratic and accessible, we should help people find the right path to setting up a venture capital firm and also make sure the right people are entering the VC sphere. Startups are changing, and any new investment manager will have to adapt to the shifting landscape. VCs today have to provide more than money to get the best portfolio, and they must have a strong focus on impact to get the best institutional investors into their funds.

Startup investors can be the financial backbone for mass disruption. That’s why, at Founder Institute, we believe in the need for more VCs with strong values: Because they will prop up the companies that will build a brighter future for humanity. We’re not the only ones — our first “accelerator for ethical VCs” was oversubscribed.

VCs today have to provide more than money to get the best portfolio, and they must have a strong focus on impact to get the best institutional investors into their funds.

So if you want to lead your own VC fund in 2021, here are the main questions aspiring investors need to ask themselves.

Investing in startups is not just about making money. In selecting the startups that will become future industry leaders, VCs have a lot more power than most to do good (or harm). If you’re only interested in money, you likely won’t go too far. Identifying the greatest businesses means seeing beyond their capital into the longevity of their vision, their real-life impact on society, and how much consumers will love or hate them.

After all: Most startup founders pour their blood, sweat and tears into building a business not just to make money, but also to make an impact on the world and build products that align with their mission. Any new venture capitalist looking to attract the best founders needs to think about the vision and mission of their fund in the same terms.

Although VC firms have been slow on the uptake when it comes to environmental, social and governance (ESG) goals, there are signs that times are changing. Some firms are forming a community around implementing ESG, not only because of the external impact but because it furthers their business goals. To help accelerate this trend, we asked our VC Lab participants to take The Mensarius Oath (Latin for “banker” or “financier”), a professional code of conduct for finance professionals to create an ethical, prosperous and healthy world.

The number of VCs are growing and the industry is increasingly becoming concentrated. This means that simply offering large sums of money won’t get you traction with the best startups. Founders are looking for value over volume — they usually want mission alignment, connections, value-added services and industry expertise more than a blank check.

Remember that the best founders get to choose their VCs from a menu of options, not the other way around. To convince them that you’re the right match, you’ll need a proven track record in the same industry (or transferable experience from another industry) and referrals from credible people. You’ll also need a strong value proposition or niche that sets you apart from other funds. For example, Untapped Capital invests in “unexpected” and “undernetworked” founders, while R42 Group invests in AI and longevity-focused businesses.

If you don’t think you’ve got the profile to offer value to founders just yet, it’s worth taking some time to lay out exactly who you are. That is: what you hope to achieve as a fund manager, the vision you have for your portfolio companies and how you alone can help them get there.

As a new VC fund without historical data points, limited partners (LPs) will naturally be cautious to invest in your fund. So, you have to build a brand that tells your story and proves your reputation.

Go back to the basics and pinpoint exactly what your strengths are. If you’re having trouble finding inspiration, use statements like, “I can get the best deal because I have X,” or, “I help grow my portfolio companies by X” to get the ball rolling. Be wary of saying that the amount of money you have is your strength — at this stage, your bank balance isn’t your competitive edge. Focus instead on what makes you unique, credible and relevant. Having a high number of strategic contacts, extensive industry experience or a backsheet of successful exits could be your secret ingredients. For extra guidance, check out this resource my team put together to help fund managers consolidate their niche in an “investment thesis.”

Once you have a list, choose your top three strengths and write a followup sentence detailing how each of them can be enriched by your network and expertise. Ideally, share these with a test group (friends, family or fellow entrepreneurs) and ask them which is the most compelling. If there’s a general consensus toward one point, you know to make that a large chunk of your VC fund’s thesis.

Who you know is just as important as what you know, and the most prominent VCs tend to be in the middle of a flow of information and people. Your network tells founders that you’re respected and reassures them that they will probably be brought into the fold to connect with future mentors, customers, investors or hires.

If you’re a thought leader, the alumni of a well-known company like Uber or PayPal, or if you’ve started a community around an emerging vertical, you’re more likely to form a positive deal flow. But this status and these relationships have to be established before you launch your fund — if you try to network from zero, you’ll be spinning too many plates and won’t have the social proof to back yourself up.

Don’t just rely on your gut to tell you whether your network is satisfactory. Map out your personal ecosystem, sorting people based on familiarity (close contacts or acquaintances) and defining characteristics (consumers, finance, ex-CEOs, etc.). That “map” can be as basic as an Excel sheet with a column for each category, or you could use more attractive visual tools like Canva — great for sharing with your future team and encouraging them to fill any network gaps.

A VC fund runs like any other business — you have to develop a vision, recruit a team, form an entity, raise money, deliver value and report to stakeholders. To kick things off, you need to consider what size fund you want, and then secure significant commitments from LPs — at least 10% of your total fund. LPs can be corporations, entrepreneurs, government agencies and other funds.

Also keep in mind that most LPs will want you to personally invest at least 1% of the total fund size so that you have “skin in the game.”

For that reason especially, it’s best to start small, somewhere between $5 million and $20 million, and use this “training fund” to demonstrate returns and create a launchpad for bigger raises to follow.

Your partnership with companies will be for the long haul, so you can’t rely just on offering value when you wire the money. Founders need consistent support across the full startup lifecycle, meaning you need to be conscious not to overpromise and fail to deliver. Think of the startups you’d most like to work with: How could you help them now? How could you help them in the future? And how could you help them exit?

You can take a skills-centric approach, where you reserve different resources and connections based on marketing, hiring, fundraising and culture-creation that can be applied as the startup grows. Alternatively, you might want to make sprint-like plans, where you check in with founders on a repeating basis and iterate the support you offer based on their progress. Whatever way you chose to structure your support, ensure that you’re realistic about what you can bring to the table, your availability, preferred involvement and how you’ll document it.

The future of VC will be driven by venture capitalists with strong values who have built funds with the new needs of founders in mind. VC may once have been exclusive and mysterious, but 2021 could be the year VC becomes a more open and fair space for businesses and investors alike.

Powered by WPeMatico