cloud

Auto Added by WPeMatico

Auto Added by WPeMatico

When Amazon announced last month that Jeff Bezos was moving into the executive chairman role, and AWS CEO Andy Jassy would be taking over the entire Amazon operation, speculation began about who would replace Jassy.

People considered a number of internal candidates viable, such as Peter DeSantis, vice president of global infrastructure at AWS and Matt Garman, who is vice president of sales and marketing. Not many would have chosen Tableau CEO Adam Selipsky, but sure enough he is returning home to run the division he left in 2016.

In an email to employees, Jassy wasted no time getting to the point that Selipsky was his choice, saying that the former employee helped launch the division when they hired him in 2005, then spent 11 years helping Jassy build the unit before taking the job at Tableau. Through that lens, the choice makes perfect sense.

“Adam brings strong judgment, customer obsession, team building, demand generation, and CEO experience to an already very strong AWS leadership team. And, having been in such a senior role at AWS for 11 years, he knows our culture and business well,” Jassy wrote in the email.

Jassy has run AWS since its earliest days, taking it from humble beginnings as a kind of internal experiment on running a storage web service to building a mega division currently on a $51 billion run rate. It is that juggernaut that will be Selipsky’s to run, but he seems well-suited for the job.

He is a seasoned executive, and while he’s been away from AWS since before it really began to grow into a huge operation, he should still understand the culture well enough to step smoothly into the role. At the same time, he’s leaving Tableau, a company he helped transform from a desktop software company into one firmly based in the cloud.

Salesforce bought Tableau in June 2019 for a cool $15.7 billion and Selipsky has remained at the helm since then, but perhaps the lure of running AWS was too great and he decided to take the leap to the new job.

When we wrote a story at the end of last year about Salesforce’s deep bench of executive talent, Selipsky was one of the CEOs we pointed at as a possible replacement should CEO and chairman Marc Benioff step down. But with it looking more like president and COO Bret Taylor would be the heir apparent, perhaps Selipsky was ready for a new challenge.

Selipsky will make his return to AWS on May 17th and spend a few weeks with Jassy in a transitional time before taking over the division to run on his own. As Jassy slides into the Amazon CEO role, it’s clear the two will continue to work closely together, just as they did for over a decade.

Powered by WPeMatico

ServiceNow became the latest company to take the robotic process automation (RPA) plunge when it announced it was acquiring Intellibot, an RPA startup based in Hyderabad, India. The companies did not reveal the purchase price.

The purchase comes at a time where companies are looking to automate workflows across the organization. RPA provides a way to automate a set of legacy processes, which often involve humans dealing with mundane repetitive work.

The announcement comes on the heels of the company’s no-code workflow announcements earlier this month and is part of the company’s broader workflow strategy, according to Josh Kahn, SVP of Creator Workflow Products at ServiceNow.

“RPA enhances ServiceNow’s current automation capabilities including low code tools, workflow, playbooks, integrations with over 150 out of the box connectors, machine learning, process mining and predictive analytics,” Kahn explained. He says that the company can now bring RPA natively to the platform with this acquisition, yet still use RPA bots from other vendors if that’s what the customer requires.

“ServiceNow customers can build workflows that incorporate bots from the pure play RPA vendors such as Automation Anywhere, UiPath and Blue Prism, and we will continue to partner with those companies. There will be many instances where customers want to use our native RPA capabilities alongside those from our partners as they build intelligent, end-to-end automation workflows on the Now Platform,” Kahn explained.

The company is making this purchase as other enterprise vendors enter the RPA market. SAP announced a new RPA tool at the end of December and acquired process automation startup Signavio in January. Meanwhile Microsoft announced a free RPA tool earlier this month, as the space is clearly getting the attention of these larger vendors.

ServiceNow has been on a buying spree over the last year or so buying five companies including Element AI, Loom Systems, Passage AI and Sweagle. Kahn says the acquisitions are all in the service of helping companies create automation across the organization.

“As we bring all of these technologies into the Now Platform, we will accelerate our ability to automate more and more sophisticated use cases. Things like better handling of unstructured data from documents such as written forms, emails and PDFs, and more resilient automations such as larger data sets and non-routine tasks,” Kahn said.

Intellibot was founded in 2015 and will provide the added bonus of giving ServiceNow a stronger foothold in India. The companies expect to close the deal no later than June.

Early Stage is the premier ‘how-to’ event for startup entrepreneurs and investors. You’ll hear first-hand how some of the most successful founders and VCs build their businesses, raise money and manage their portfolios. We’ll cover every aspect of company-building: Fundraising, recruiting, sales, product market fit, PR, marketing and brand building. Each session also has audience participation built-in – there’s ample time included for audience questions and discussion. Use code “TCARTICLE” at checkout to get 20 percent off tickets right here.

Powered by WPeMatico

Orca Security, an Israeli cybersecurity startup that offers an agent-less security platform for protecting cloud-based assets, today announced that it has raised a $210 million Series C round at a $1.2 billion valuation. The round was led by Alphabet’s independent growth fund CapitalG and Redpoint Ventures. Existing investors GGV Capital, ICONIQ Growth and angel syndicate Silicon Valley CISO Investment also participated. YL Ventures, which led Orca’s seed round and participated in previous rounds, is not participating in this round — and it’s worth noting that the firm recently sold its stake in Axonius after that company reached unicorn status.

If all of this sounds familiar, that may be because Orca only raised its $55 million Series B round in December, after it announced its $20.5 million Series A round in May. That’s a lot of funding rounds in a short amount of time, but something we’ve been seeing more often in the last year or so.

Orca Security co-founders Gil Geron (left) and Avi Shua (right). Image Credits: Orca Security

As Orca co-founder and CEO Avi Shua told me, the company is seeing impressive growth and it — and its investors — want to capitalize on this. The company ended last year beating its own forecast from a few months before, which he noted was already aggressive, by more than 50%. Its current slate of customers includes Robinhood, Databricks, Unity, Live Oak Bank, Lemonade and BeyondTrust.

“We are growing at an unprecedented speed,” Shua said. “We were 20-something people last year. We are now closer to a hundred and we are going to double that by the end of the year. And yes, we’re using this funding to accelerate on every front, from dramatically increasing the product organization to add more capabilities to our platform, for post-breach capabilities, for identity access management and many other areas. And, of course, to increase our go-to-market activities.”

Shua argues that most current cloud security tools don’t really work in this new environment. Many, because they are driven by metadata, can only detect a small fraction of the risks, and agent-based solutions may take months to deploy and still not cover a business’ entire cloud estate. The promise of Orca Security is that it can not only cover a company’s entire range of cloud assets but that it is also able to help security teams prioritize the risks they need to focus on. It does so by using what the company calls its “SideScanning” technology, which allows it to map out a company’s entire cloud environment and file systems.

“Almost all tools are essentially just looking at discrete risk trees and not the forest. The risk is not just about how pickable the lock is, it’s also where the lock resides and what’s inside the box. But most tools just look at the issues themselves and prioritize the most pickable lock, ignoring the business impact and exposure — and we change that.”

It’s no secret that there isn’t a lot of love lost between Orca and some of its competitors. Last year, Palo Alto Networks sent Orca Security a sternly worded letter (PDF) to stop it from comparing the two services. Shua was not amused at the time and decided to fight it. “I completely believe there is space in the markets for many vendors, and they’ve created a lot of great products. But I think the thing that simply cannot be overlooked, is a large company that simply tries to silence competition. This is something that I believe is counterproductive to the industry. It tries to harm competition, it’s illegal, it’s unconstitutional. You can’t use lawyers to take your competitors out of the media.”

Currently, though, it doesn’t look like Orca needs to worry too much about the competition. As GGV Capital managing partner Glenn Solomon told me, as the company continues to grow and bring in new customers — and learn from the data it pulls in from them — it is also able to improve its technology.

“Because of the novel technology that Avi and [Orca Security co-founder and CPO] Gil [Geron] have developed — and that Orca is now based on — they see so much. They’re just discovering more and more ways and have more and more plans to continue to expand the value that Orca is going to provide to customers. They sit in a very good spot to be able to continue to leverage information that they have and help DevOps teams and security teams really execute on good hygiene in every imaginable way going forward. I’m super excited about that future.”

As for this funding round, Shua noted that he found CapitalG to be a “huge believer” in this space and an investor that is looking to invest into the company for the long run (and not just trying to make a quick buck). The fact that CapitalG is associated with Alphabet was obviously also a draw.

“Being associated with Alphabet, which is one of the three major cloud providers, allowed us to strengthen the relationship, which is definitely a benefit for Orca,” he said. “During the evaluation, they essentially put Orca in front of the security leadership at Google. Definitely, they’ve done their own very deep due diligence as part of that.”

Early Stage is the premier ‘how-to’ event for startup entrepreneurs and investors. You’ll hear first-hand how some of the most successful founders and VCs build their businesses, raise money and manage their portfolios. We’ll cover every aspect of company-building: Fundraising, recruiting, sales, product market fit, PR, marketing and brand building. Each session also has audience participation built-in – there’s ample time included for audience questions and discussion. Use code “TCARTICLE” at checkout to get 20 percent off tickets right here.

Powered by WPeMatico

Shares of Box, a well-known content-and-collaboration company that went public in 2015, rose today after Reuters reported that the company is exploring a sale. TechCrunch previously discussed rising investor pressure for Box to ignite its share price after years in the public-market wilderness.

At the close today Box’s equity was worth $23.65 per share, up around 5% from its opening value, but lower than its intraday peak of $26.47, reached after the news broke. The company went public a little over five years ago at $14 per share, only to see its share price rise to around the same level it returned today during its first day’s trading.

Box, famous during its startup phase thanks in part to its ubiquitous CEO and co-founder Aaron Levie, has continued to grow while public, albeit at a declining pace. Dropbox, a long-term rival, has also seen its growth rate decline since going public. Both have stressed rising profitability over revenue expansion in recent quarters.

But the problem that Box has encountered while public, namely hyper-scale platform companies with competing offerings, could also prove a lifeline; Google and Microsoft could be a future home for Levie’s company, after years of the duo challenging Box for deals.

As recently as last week, Box announced a deal for tighter integration with Microsoft Office 365. Given the timing of the release, it was easy to speculate the news could be landing ahead of a potential deal. The Reuters article adds fuel to the possibility.

While we can’t know for sure if the Reuters article is accurate, the possible sale of Box makes sense.

The article indicated that one of the possible acquisition options for Box could be taking it private again via private equity. Perhaps a firm like Vista or Thoma Bravo, two firms that tend to like mature SaaS companies with decent revenue and some issues, could swoop in to buy the struggling SaaS company. By taking companies off the market, reducing investor pressure and giving them room to maneuver, software companies can at times find new vigor.

Consider the case of Marketo, a company that Vista purchased in 2016 for $1.6 billion before turning it around and selling to Adobe in 2018 for $4.75 billion. The end result generated a strong profit for Vista, and a final landing for Marketo as part of a company with a broader platform of marketing tools.

If there are expenses at Box that could be trimmed, or a sales process that could be improved, is not clear. But Box’s market value of $3.78 billion could put it within grasp of larger private-equity funds. Or well within the reaches of a host of larger enterprise software companies that might covet its list of business customers, technology or both.

If the rumors are true, it could be a startling fall from grace for the company, moving from Silicon Valley startup darling to IPO to sold entity in just six years. While it’s important to note these are just rumors, the writing could be on the wall for the company, and it could just be a matter of when and not if.

Powered by WPeMatico

There has been a growing industry trend in recent years for large-scale companies to build their own chips. As part of that, Google announced today that it has hired long-time Intel executive Uri Frank as vice president to run its custom chip division.

“The future of cloud infrastructure is bright, and it’s changing fast. As we continue to work to meet computing demands from around the world, today we are thrilled to welcome Uri Frank as our VP of Engineering for server chip design,” Amin Vahdat, Google Fellow and VP of systems infrastructure wrote in a blog post announcing the hire.

With Frank, Google gets an experienced chip industry executive, who spent more than two decades at Intel rising from engineering roles to corporate vice president at the Design Engineering Group, his final role before leaving the company earlier this month.

Frank will lead the custom chip division in Israel as part of Google. As he said in his announcement on LinkedIn, this was a big step to join a company with a long history of building custom silicon.

“Google has designed and built some of the world’s largest and most efficient computing systems. For a long time, custom chips have been an important part of this strategy. I look forward to growing a team here in Israel while accelerating Google Cloud’s innovations in compute infrastructure,” Frank wrote.

Google’s history of building its own chips dates back to 2015 when it launched the first TensorFlow chips. It moved into video processing chips in 2018 and added OpenTitan , an open-source chip with a security angle in 2019.

Frank’s job will be to continue to build on this previous experience to work with customers and partners to build new custom chip architectures. The company wants to move away from buying motherboard components from different vendors to building its own “system on a chip” or SoC, which it says will be drastically more efficient.

“Instead of integrating components on a motherboard where they are separated by inches of wires, we are turning to “Systems on Chip” (SoC) designs where multiple functions sit on the same chip, or on multiple chips inside one package. In other words, the SoC is the new motherboard,” Vahdat wrote.

While Google was early to the “Build Your Own Chip” movement, we’ve seen other large scale companies like Amazon, Facebook, Apple and Microsoft begin building their own custom chips in recent years to meet each company’s unique needs and give more precise control over the relationship between the hardware and software.

It will be Frank’s job to lead Google’s custom chip unit and help bring it to the next level.

Powered by WPeMatico

Berlin-based y42 (formerly known as Datos Intelligence), a data warehouse-centric business intelligence service that promises to give businesses access to an enterprise-level data stack that’s as simple to use as a spreadsheet, today announced that it has raised a $2.9 million seed funding round led by La Famiglia VC. Additional investors include the co-founders of Foodspring, Personio and Petlab.

The service, which was founded in 2020, integrates with more than 100 data sources, covering all the standard B2B SaaS tools, from Airtable to Shopify and Zendesk, as well as database services like Google’s BigQuery. Users can then transform and visualize this data, orchestrate their data pipelines and trigger automated workflows based on this data (think sending Slack notifications when revenue drops or emailing customers based on your own custom criteria).

Like similar startups, y42 extends the idea data warehouse, which was traditionally used for analytics, and helps businesses operationalize this data. At the core of the service is a lot of open source and the company, for example, contributes to GitLabs’ Meltano platform for building data pipelines.

y42 founder and CEO Hung Dang. Image Credits: y42

“We’re taking the best of breed open-source software. What we really want to accomplish is to create a tool that is so easy to understand and that enables everyone to work with their data effectively,” Y42 founder and CEO Hung Dang told me. “We’re extremely UX obsessed and I would describe us as a no-code/low-code BI tool — but with the power of an enterprise-level data stack and the simplicity of Google Sheets.”

Before y42, Vietnam-born Dang co-founded a major events company that operated in more than 10 countries and made millions in revenue (but with very thin margins), all while finishing up his studies with a focus on business analytics. And that in turn led him to also found a second company that focused on B2B data analytics.

Image Credits: y42

Even while building his events company, he noted, he was always very product- and data-driven. “I was implementing data pipelines to collect customer feedback and merge it with operational data — and it was really a big pain at that time,” he said. “I was using tools like Tableau and Alteryx, and it was really hard to glue them together — and they were quite expensive. So out of that frustration, I decided to develop an internal tool that was actually quite usable and in 2016, I decided to turn it into an actual company. ”

He then sold this company to a major publicly listed German company. An NDA prevents him from talking about the details of this transaction, but maybe you can draw some conclusions from the fact that he spent time at Eventim before founding y42.

Given his background, it’s maybe no surprise that y42’s focus is on making life easier for data engineers and, at the same time, putting the power of these platforms in the hands of business analysts. Dang noted that y42 typically provides some consulting work when it onboards new clients, but that’s mostly to give them a head start. Given the no-code/low-code nature of the product, most analysts are able to get started pretty quickly — and for more complex queries, customers can opt to drop down from the graphical interface to y42’s low-code level and write queries in the service’s SQL dialect.

The service itself runs on Google Cloud and the 25-people team manages about 50,000 jobs per day for its clients. The company’s customers include the likes of LifeMD, Petlab and Everdrop.

Until raising this round, Dang self-funded the company and had also raised some money from angel investors. But La Famiglia felt like the right fit for y42, especially due to its focus on connecting startups with more traditional enterprise companies.

“When we first saw the product demo, it struck us how on top of analytical excellence, a lot of product development has gone into the y42 platform,” said Judith Dada, general partner at LaFamiglia VC. “More and more work with data today means that data silos within organizations multiply, resulting in chaos or incorrect data. y42 is a powerful single source of truth for data experts and non-data experts alike. As former data scientists and analysts, we wish that we had y42 capabilities back then.”

Dang tells me he could have raised more but decided that he didn’t want to dilute the team’s stake too much at this point. “It’s a small round, but this round forces us to set up the right structure. For the Series A, which we plan to be towards the end of this year, we’re talking about a dimension which is 10x,” he told me.

Powered by WPeMatico

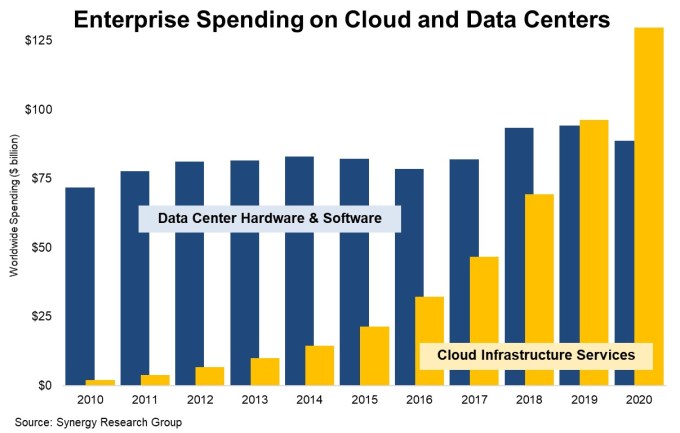

There is a prevailing notion that while the cloud infrastructure market is growing fast, the vast majority of workloads remain on premises. While that could be true, new research from Synergy Research Group found that cloud infrastructure spending surpassed on-prem spending for the first time in 2020 — and did so by a wide margin.

“New data from Synergy Research Group shows that enterprise spending on cloud infrastructure services continued to ramp up aggressively in 2020, growing by 35% to reach almost $130 billion. Meanwhile enterprise spending on data center hardware and software dropped by 6% to under $90 billion,” the firm said in a statement.

While the numbers have been trending toward the cloud for a decade, the spending favored on-prem software until last year when the two numbers pulled even, according to Synergy data. John Dinsdale, chief analyst and research director at Synergy says that this new data shows that CIOs have shifted their spending to the cloud in 2020.

“Where the rubber meets the road is what are companies spending their money on, and that is what we are covering here. Quite clearly CIOs are choosing to spend a lot more money on cloud services and are severely crimping their spend on on-prem (or collocated) data center assets,” Dinsdale told me.

Image Credits: Synergy Research Group

The total for on-prem spending includes servers, storage, networking, security and related software required to run the hardware. “The software pieces included in this data is mainly server OS and virtualization software. Comparing SaaS with on-prem business apps software is a whole other story,” Dinsdale said.

As we see on-prem/cloud numbers diverging in this way, it’s worth asking how these numbers compare to research from Gartner and others that the cloud remains a relatively small percentage of global IT spend. As workloads move back and forth in today’s hybrid world, Dinsdale says that makes it difficult to quantify where it lives at any given moment.

“I’ve seen plenty of comments about only a small percentage of workloads running on public clouds. That may or may not be true (and I tend more toward the latter), but the problem I have with this is that the concept of ‘workloads’ is such a fungible issue, especially when you try to quantify it,” he said.

It’s worth noting that the pandemic has led to companies moving to the cloud much faster than they might have without a forcing event, but Dinsdale says that the trend has been moving this way over years, even if COVID might have accelerated it.

Whatever numbers you choose to look at, it’s clear that the cloud infrastructure market is growing much faster now than its on-premises counterpart, and this new data from Synergy shows that CIOs are beginning to place their bets on the cloud.

Powered by WPeMatico

Snowflake announced earlier this month that it would give up its dual-class shareholder structure, a corporate governance setup that often gives founders and executives superior voting rights, typically involving 10 times as many votes for their own shares as others receive. The mechanism can enable founders to maintain control despite later dilution and may sometimes even grant ironclad control to an individual in perpetuity.

For many companies, these supervoting shares represent a highly powerful tool, allowing founders to have their cake and eat it, too — to go public and receive the advantages of being a public company while limiting the power of external shareholders to influence how they run the company once it floats.

Some founders and their investors argue that these preferred shares protect them from the short-term whims of the market, but the perspective isn’t universally accepted.

Some founders and their investors argue that these preferred shares protect them from the short-term whims of the market, but the perspective isn’t universally accepted. Dual-class shares are a controversial governance structure, and some wonder if they are setting up an unfair playing field by allowing a cabal to wield outsized power.

Why would Snowflake give up such a powerful tool a mere six months after it went public? We decided to look at the notion of dual-class shares and why Snowflake may have been willing to let them go.

If one of the primary purposes of dual-class shares is to consolidate CEO power, then perhaps Snowflake felt they weren’t necessary, given the history of CEO-shuffling at the company. While Snowflake’s founders are still part of the organization, they hired Sutter Hill investor Mike Speiser to be their first CEO, followed by former Microsoft exec Bob Muglia before finally bringing in veteran CEO Frank Slootman to take their company public.

Without an all-powerful CEO founder in place, perhaps the company felt that supervoting shares weren’t necessary. Regardless, Snowflake CFO Mike Scarpelli framed the move as a decision that works for all parties when he announced that his company would abandon the special shares during its earnings call earlier this month.

“Today, we announced that on March 1st, 2021, our Class B shareholders in accordance with our governing documents converted all of our Class B common stock to Class A common stock, eliminating the dual-class structure of our common stock and ensuring that each share has an equal vote. We view this as operationally beneficial to the company and our shareholders,” Scarpelli said during the call.

Powered by WPeMatico

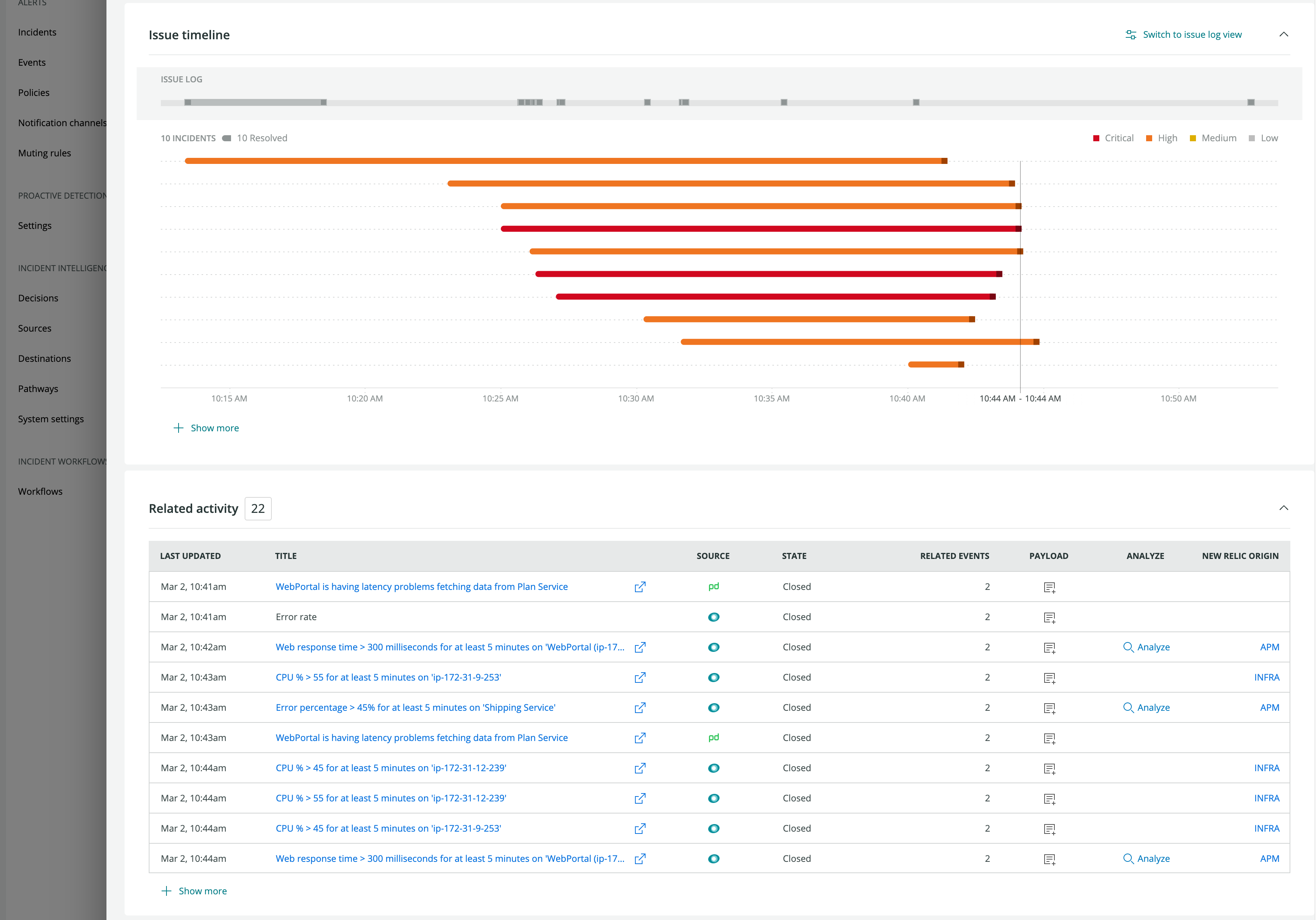

In recent years, the publicly traded observability service New Relic started adding more machine learning-based tools to its platform for AI-assisted incident response when things don’t quite go as planned. Today, it is expanding this feature set with the launch of a number of new capabilities for what it calls its “New Relic Applied Intelligence Service.”

This expansion includes an anomaly detection service that is even available for free users, the ability to group alerts from multiple tools when the models think it’s a single issue that is triggering all of these alerts and new ML-based root cause analysis to help eliminate some of the guesswork when problems occur. Also new (and in public beta) is New Relic’s ability to detect patterns and outliers in log data that is stored in the company’s data platform.

The main idea here, New Relic’s director of product marketing Michael Olson told me, is to make it easier for companies of all sizes to reap the benefits of AI-enhanced ops.

Image Credits: New Relic

“It’s been about a year since we introduced our first set of AIops capabilities with New Relic Applied Intelligence to the market,” he said. “During that time, we’ve seen significant growth in adoption of AIops capabilities through New Relic. But one of the things that we’ve heard from organizations that have yet to foray into adopting AIops capabilities as part of their incident response practice is that they often find that things like steep learning curves and long implementation and training times — and sometimes lack of confidence, or knowledge of AI and machine learning — often stand in the way.”

The new platform should be able to detect emerging problems in real time — without the team having to pre-configure alerts. And when it does so, it’ll smartly group all of the alerts from New Relic and other tools together to cut down on the alert noise and let engineers focus on the incident.

“Instead of an alert storm when a problem occurs across multiple tools, engineers get one actionable issue with alerts automatically grouped based on things like time and frequency, based on the context that they can read in the alert messages. And then now with this launch, we’re also able to look at relationship data across your systems to intelligently group and correlate alerts,” Olson explained.

Image Credits: New Relic

Maybe the highlight for the ops teams that will use these new features, though, is New Relic’s ability to pinpoint the probable root cause of a problem. As Guy Fighel, the general manager of applied intelligence and vice president of product engineering at New Relic, told me, the idea here is not to replace humans but to augment teams.

“We provide a non-black-box experience for teams to craft the decisions and correlation and logic based on their own knowledge and infuse the system with their own knowledge,” Fighel noted. “So you can get very specific based on your environment and needs. And so because of that and because we see a lot of data coming from different tools — all going into New Relic One as the data platform — our probable root cause is very accurate. Having said that, it is still a probable root cause. So although we are opinionated about it, we will never tell you, ‘hey, go fix that, because we’re 100% sure that’s the case.’ You’re the human, you’re in control.”

The AI system also asks users for feedback, so that the model gets refined with every new incident, too.

Fighel tells me that New Relic’s tools rely on a variety of statistical analysis methods and machine learning models. Some of those are unique to individual users while others are used across the company’s user base. He also stressed that all of the engineers who worked on this project have a background in site reliability engineering — so they are intimately familiar with the problems in this space.

With today’s launch, New Relic is also adding a new integration with PagerDuty and other incident management tools so that the state of a given issue can be synchronized bi-directionally between them.

“We want to meet our customers where they are and really be data source agnostic and enable customers to pull in data from any source, where we can then enrich that data, reduce noise and ultimately help our customers solve problems faster,” said Olson.

Early Stage is the premier “how-to” event for startup entrepreneurs and investors. You’ll hear firsthand how some of the most successful founders and VCs build their businesses, raise money and manage their portfolios. We’ll cover every aspect of company building: Fundraising, recruiting, sales, product-market fit, PR, marketing and brand building. Each session also has audience participation built-in — there’s ample time included for audience questions and discussion. Use code “TCARTICLE at checkout to get 20% off tickets right here.

Powered by WPeMatico

It was easy to wonder what would become of Docker after it sold its enterprise business in 2019, but it regrouped last year as a cloud native container company focused on developers, and the new approach appears to be bearing fruit. Today, the company announced a $23 million Series B investment.

Tribe Capital led the round with participation from existing investors Benchmark and Insight Partners. Docker has now raised a total of $58 million including the $35 million investment it landed the same day it announced the deal with Mirantis.

To be sure, the company had a tempestuous 2019 when they changed CEOs twice, sold the enterprise division and looked to reestablish itself with a new strategy. While the pandemic made 2020 a trying time for everyone, Docker CEO Scott Johnston says that in spite of that, the strategy has begun to take shape.

“The results we think speak volumes. Not only was the strategy strong, but the execution of that strategy was strong as well,” Johnston told me. He indicated that the company added 1.7 million new developer registrations for the free version of the product for a total of more than 7.3 million registered users on the community edition.

As with any open-source project, the goal is to popularize the community project and turn a small percentage of those users into paying customers, but Docker’s problem prior to 2019 had been finding ways to do that. While he didn’t share specific numbers, Johnston indicated that annual recurring revenue (ARR) grew 170% last year, suggesting that they are beginning to convert more successfully.

Johnston says that’s because they have found a way to turn a certain class of developer in spite of a free version being available. “Yes, there’s a lot of upstream open-source technologies, and there are users that want to hammer together their own solutions. But we are also seeing these eight to 10 person ‘two-pizza teams’ who want to focus on building applications, and so they’re willing to pay for a service,” he said.

That open-source model tends to get the attention of investors because it comes with that built-in action at the top of the sales funnel. Tribe’s Arjun Sethi, whose firm led the investment, says his company actually was a Docker customer before investing in the company and sees a lot more growth potential.

“Tribe focuses on identifying N-of-1 companies — top-decile private tech firms that are exhibiting inflection points in their growth, with the potential to scale toward outsized outcomes with long-term venture capital. Docker fits squarely into this investment thesis [ … ],” Sethi said in a statement.

Johnston says as they look ahead post-pandemic, he’s learned a lot since his team moved out of the office last year. After surveying employees, they were surprised to learn that most have been happier working at home, having more time to spend with family, while taking away a grueling commute. As a result, he sees going virtual first, even after it’s safe to reopen offices.

That said, he is planning to offer a way to get teams together for in-person gatherings and a full company get-together once a year.

“We’ll be virtual first, but then with the savings of the real estate that we’re no longer paying for, we’re going to bring people together and make sure we have that social glue,” he said.

Early Stage is the premier “how-to” event for startup entrepreneurs and investors. You’ll hear firsthand how some of the most successful founders and VCs build their businesses, raise money and manage their portfolios. We’ll cover every aspect of company building: Fundraising, recruiting, sales, product-market fit, PR, marketing and brand building. Each session also has audience participation built in — there’s ample time included for audience questions and discussion. Use code “TCARTICLE at checkout to get 20% off tickets right here.

Powered by WPeMatico