cloud

Auto Added by WPeMatico

Auto Added by WPeMatico

It’s a busy day in IPO-land: Olo has raised its IPO range and DigitalOcean is giving us a first look at what it may be worth when it debuts.

That Olo raised its IPO price is not a huge surprise, given the software company’s rapid growth and profits. In the case of DigitalOcean, we have more work to do as its approach to growth is a bit different.

Let’s explore both companies’ pricing intervals through our usual lens of revenue multiples, market comps and general SaaS sass. We’ll do this in alphabetical order, which puts the cloud infra company up first.

According to its S-1/A filing, DigitalOcean expects its IPO to price between $44 and $47 per share. The price range is a coup for the company’s private investors, who as recently as the company’s 2020 Series C paid about $10.59 each for the company’s shares. Andreessen Horowitz is going to do very well, having led the company’s Series A at a per-share price of just more than $2. IA Ventures, which led DigitalOcean’s seed round, according to Crunchbase, paid just $0.26 per share back in the 2012-2013 time frame. That’s going to convert well.

In valuation terms, the company’s simple share count post-IPO will be 105,303,340, or 107,778,340 if its underwriters purchase their option. At $44 to $47 per share, DigitalOcean is worth $4.72 billion to $5.07 billion, including shares designated for its underwriters.

The company’s fully diluted valuation is higher. At midpoint, Renaissance Capital estimates DigitalOcean’s diluted valuation is $5.6 billion. That works out to a little under $5.8 billion at $47 per share.

Taking a look at DigitalOcean’s Q4 2020 revenue of $87.5 million, the company closed last year on a run rate of $350 million. Or a revenue multiple of 14.5x at the upper end of its nondiluted valuation, and around 16.5x at the upper bound of its diluted worth.

Powered by WPeMatico

DeepSee.ai, a startup that helps enterprises use AI to automate line-of-business problems, today announced that it has raised a $22.6 million Series A funding round led by led by ForgePoint Capital. Previous investors AllegisCyber Capital and Signal Peak Ventures also participated in this round, which brings the Salt Lake City-based company’s total funding to date to $30.7 million.

The company argues that it offers enterprises a different take on process automation. The industry buzzword these days is “robotic process automation,” but DeepSee.ai argues that what it does is different. I describe its system as “knowledge process automation” (KPA). The company itself defines this as a system that “mines unstructured data, operationalizes AI-powered insights, and automates results into real-time action for the enterprise.” But the company also argues that today’s bots focus on basic task automation that doesn’t offer the kind of deeper insights that sophisticated machine learning models can bring to the table. The company also stresses that it doesn’t aim to replace knowledge workers but helps them leverage AI to turn into actionable insights the plethora of data that businesses now collect.

Image Credits: DeepSee.ai

“Executives are telling me they need business outcomes and not science projects,” writes DeepSee.ai CEO Steve Shillingford. “And today, the burgeoning frustration with most AI-centric deployments in large-scale enterprises is they look great in theory but largely fail in production. We think that’s because right now the current ‘AI approach’ lacks a holistic business context relevance. It’s unthinking, rigid and without the contextual input of subject-matter experts on the ground. We founded DeepSee to bridge the gap between powerful technology and line-of-business, with adaptable solutions that empower our customers to operationalize AI-powered automation — delivering faster, better and cheaper results for our users.”

To help businesses get started with the platform, DeepSee.ai offers three core tools. There’s DeepSee Assembler, which ingests unstructured data and gets it ready for labeling, model review and analysis. Then, DeepSee Atlas can use this data to train AI models that can understand a company’s business processes and help subject-matter experts define templates, rules and logic for automating a company’s internal processes. The third tool, DeepSee Advisor, meanwhile focuses on using text analysis to help companies better understand and evaluate their business processes.

Currently, the company’s focus is on providing these tools for insurance companies, the public sector and capital markets. In the insurance space, use cases include fraud detection, claims prediction and processing, and using large amounts of unstructured data to identify patterns in agent audits, for example.

That’s a relatively limited number of industries for a startup to operate in, but the company says it will use its new funding to accelerate product development and expand to new verticals.

“Using KPA, line-of-business executives can bridge data science and enterprise outcomes, operationalize AI/ML-powered automation at scale, and use predictive insights in real time to grow revenue, reduce cost and mitigate risk,” said Sean Cunningham, managing director of ForgePoint Capital. “As a leading cybersecurity investor, ForgePoint sees the daily security challenges around insider threat, data visibility and compliance. This investment in DeepSee accelerates the ability to reduce risk with business automation and delivers much-needed AI transparency required by customers for implementation.”

Powered by WPeMatico

Google Cloud today announced the launch of a new support option for its Premium Support customers that run mission-critical services on its platform. The new service, imaginatively dubbed Mission Critical Services (MCS), brings Google’s own experience with Site Reliability Engineering to its customers. This is not Google completely taking over the management of these services, though. Instead, the company describes it as a “consultative offering in which we partner with you on a journey toward readiness.”

Initially, Google will work with its customers to improve — or develop — the architecture of their apps and help them instrument the right monitoring systems and controls, as well as help them set and raise their service-level objectives (a key feature in the Site Reliability Engineering philosophy).

Later, Google will also provide ongoing check-ins with its engineers and walk customers through tune-ups architecture reviews. “Our highest tier of engineers will have deep familiarity with your workloads, allowing us to monitor, prevent, and mitigate impacts quickly, delivering the fastest response in the industry. For example, if you have any issues–24-hours-a-day, seven-days-a-week–we’ll spin up a live war room with our experts within five minutes,” Google Cloud’s VP for Customer Experience, John Jester, explains in today’s announcement.

This new offering is another example of how Google Cloud is trying to differentiate itself from the rest of the large cloud providers. Its emphasis today is on providing the high-touch service experiences that were long missing from its platform, with a clear emphasis on the needs of large enterprise customers. That’s what Thomas Kurian promised to do when he became the organization’s CEO and he’s clearly following through.

Early Stage is the premier ‘how-to’ event for startup entrepreneurs and investors. You’ll hear first-hand how some of the most successful founders and VCs build their businesses, raise money and manage their portfolios. We’ll cover every aspect of company-building: Fundraising, recruiting, sales, product market fit, PR, marketing and brand building. Each session also has audience participation built-in – there’s ample time included for audience questions and discussion. Use code “TCARTICLE at checkout to get 20 percent off tickets right here.

Powered by WPeMatico

Last month Jeff Bezos announced he would step down as CEO of Amazon later this year, moving into the executive chairman role, while passing the baton to AWS CEO Andy Jassy. Could Marc Benioff, co-founder, chairman and CEO at Salesforce be the next big-name executive to make a similar move?

A Reuter’s story published on Monday suggested that could be the case. Citing unnamed sources, the story indicated that Benioff’s CEO exit could happen this year. Further those same sources suggested that current Salesforce president and COO Bret Taylor is the likely heir apparent.

We wrote a story at the end of last year speculating on possible successors to Benioff, were he to step away from the CEO role. There were a number of worthy candidates, several of whom, like Taylor, came to the company via an acquisition. All the same, we thought that Taylor seemed to be the most likely candidate to replace Benioff.

We asked Salesforce for a comment on the Reuter’s story. A company spokesperson told us that the company doesn’t comment on rumors or speculation.

While the entire scenario fits firmly in the rumor and speculation column, it is not entirely unlikely either. What would it mean if Benioff stepped away and what if Taylor was truly the next in line? And how would that swap compare with the Bezos decision were it to happen?

Salesforce and Amazon are both companies founded in the 1990s, each looking to shake up its industry.

For Amazon, it was changing the way goods (starting with books) were bought and sold. And for Benioff the goal was changing the way software was sold. Bezos famously founded his company in his garage. Benioff built his in a rented apartment. From these humble beginnings both have built iconic companies and accumulated enormous wealth. You could understand why either could be ready to step away from the daily grind of running a company after all these years.

Bezos announced that veteran executive Andy Jassy, who runs the company’s cloud arm, would be his replacement when the handoff comes. Jassy knows the organization’s priority mix as he’s been working at the company for more than two decades. He’s locked into the culture and helped take AWS from idea to $50 billion juggernaut.

While Benioff hasn’t made any actual firm pronouncement, we have seen Bret Taylor — who joined the company in 2016 when Salesforce purchased his startup Quip for $750 million — move quickly up the ladder.

Laurie McCabe, co-founder and analyst at SMB Group, who has been following Salesforce since its earliest days, says that if Benioff were to leave, he would obviously leave big shoes to fill. But she agreed that everything seems to point to Taylor as his successor should that happen.

“Salesforce has been grooming Taylor for awhile. He has some stellar credentials both at Salesforce, his own start-up, Quip, that Salesforce acquired, and at Facebook. There’s no doubt in my mind he can lead Salesforce forward, but he’ll bring a different more low-key style to the role. And I’m sure Benioff will stay very involved […],” McCabe said.

Brent Leary, founder and principal analyst at CRM Essentials says that while he believes Taylor could be chosen as Benioff’s successor, and would be qualified to lead the company, he’s taken a very different path from Jassy.

“I think Benioff moving on could be different from Bezos in the sense that Jassy has been at Amazon for over 20 years and was there to basically see and be part of most of the story. […] But if Taylor were to succeed Benioff there’s not as much [history] at Salesforce with him not being on board until the Quip acquisition in 2016,” Leary said.

Leary wonders if this relatively short history with the company could create some political friction in the organization if he were chosen to succeed Benioff. “I’m not saying that this would happen, but choosing one of the many possible heirs that have come via a number of high profile acquisitions could possibly lead to high level turnover from those not picked to succeed Benioff,” he said.

But Holger Mueller, an analyst at Constellation Research says that if you look at the range of candidates available, he believes that Taylor would be the best choice. “I don’t expect any issue because there is no one with a similar or even better background, which is when there are problems — that or when people are in an open competition as it used to be at GE,” he said.

We don’t know for sure what the final outcome will be, but if Benioff does decide to join Bezos and takes the executive chairman mantle at the company, it makes sense that the person to replace him will be Taylor. But for now, it remains in the realm of speculation, and we’ll just to wait and see if that’s what comes to pass.

Powered by WPeMatico

Aqua Security, a Boston- and Tel Aviv-based security startup that focuses squarely on securing cloud-native services, today announced that it has raised a $135 million Series E funding round at a $1 billion valuation. The round was led by ION Crossover Partners. Existing investors M12 Ventures, Lightspeed Venture Partners, Insight Partners, TLV Partners, Greenspring Associates and Acrew Capital also participated. In total, Aqua Security has now raised $265 million since it was founded in 2015.

The company was one of the earliest to focus on securing container deployments. And while many of its competitors were acquired over the years, Aqua remains independent and is now likely on a path to an IPO. When it launched, the industry focus was still very much on Docker and Docker containers. To the detriment of Docker, that quickly shifted to Kubernetes, which is now the de facto standard. But enterprises are also now looking at serverless and other new technologies on top of this new stack.

“Enterprises that five years ago were experimenting with different types of technologies are now facing a completely different technology stack, a completely different ecosystem and a completely new set of security requirements,” Aqua CEO Dror Davidoff told me. And with these new security requirements came a plethora of startups, all focusing on specific parts of the stack.

Image Credits: Aqua Security

What set Aqua apart, Dror argues, is that it managed to 1) become the best solution for container security and 2) realized that to succeed in the long run, it had to become a platform that would secure the entire cloud-native environment. About two years ago, the company made this switch from a product to a platform, as Davidoff describes it.

“There was a spree of acquisitions by CheckPoint and Palo Alto [Networks] and Trend [Micro],” Davidoff said. “They all started to acquire pieces and tried to build a more complete offering. The big advantage for Aqua was that we had everything natively built on one platform. […] Five years later, everyone is talking about cloud-native security. No one says ‘container security’ or ‘serverless security’ anymore. And Aqua is practically the broadest cloud-native security [platform].”

One interesting aspect of Aqua’s strategy is that it continues to bet on open source, too. Trivy, its open-source vulnerability scanner, is the default scanner for GitLab’s Harbor Registry and the CNCF’s Artifact Hub, for example.

“We are probably the best security open-source player there is because not only do we secure from vulnerable open source, we are also very active in the open-source community,” Davidoff said (with maybe a bit of hyperbole). “We provide tools to the community that are open source. To keep evolving, we have a whole open-source team. It’s part of the philosophy here that we want to be part of the community and it really helps us to understand it better and provide the right tools.”

In 2020, Aqua, which mostly focuses on mid-size and larger companies, doubled the number of paying customers and it now has more than half a dozen customers with an ARR of over $1 million each.

Davidoff tells me the company wasn’t actively looking for new funding. Its last funding round came together only a year ago, after all. But the team decided that it wanted to be able to double down on its current strategy and raise sooner than originally planned. ION had been interested in working with Aqua for a while, Davidoff told me, and while the company received other offers, the team decided to go ahead with ION as the lead investor (with all of Aqua’s existing investors also participating in this round).

“We want to grow from a product perspective, we want to grow from a go-to-market [perspective] and expand our geographical coverage — and we also want to be a little more acquisitive. That’s another direction we’re looking at because now we have the platform that allows us to do that. […] I feel we can take the company to great heights. That’s the plan. The market opportunity allows us to dream big.”

Powered by WPeMatico

Dropbox announced today that it plans to acquire DocSend for $165 million. The company helps customers share and track documents by sending a secure link instead of an attachment.

“We’re announcing that we’re acquiring DocSend to help us deliver an even broader set of tools for remote work, and DocSend helps customers securely manage and share their business-critical documents, backed by powerful engagement analytics,” Dropbox CEO Drew Houston told me.

When combined with the electronic signature capability of HelloSign, which Dropbox acquired in 2019, the acquisition gives the company an end-to-end document-sharing workflow it had been missing. “Dropbox, DocSend and HelloSign will be able to offer a full suite of self-serve products to help our millions of customers manage the entire critical document workflows and give more control over all aspects of that,” Houston explained.

Houston and DocSend co-founder and CEO Russ Heddleston have known each for other years, and have an established relationship. In fact, Heddleston worked for Dropbox as a summer in intern in 2010. He even ran the idea for the company by Houston prior to launching in 2013, who gave it his seal of approval, and the two companies have been partners for some time.

“We’ve just been following the thread of external sending, which has just kind of evolved and opened up into all these different workflows. And it’s just really interesting that by just being laser-focused on that we’ve been able to create a really differentiated product that users love a ton,” Heddleston said.

Those workflows include creative, sales, client services or startups using DocSend to deliver proposals or pitch decks and track engagement. In fact, among the earliest use cases for the company was helping startups track engagement with their pitch decks at VC firms.

The company raised a modest amount of the money along the way, just $15.3 million, according to Crunchbase, but Heddleston says that he wanted to build a company that was self-sufficient and raising more VC dollars was never a priority or necessity. “We had [VCs] chase us to give us more money all the time, and what we would tell our employees is that we don’t keep count based on money raised or headcount. It’s just about building a great company,” he said.

That builder’s attitude was one of the things that attracted Houston to the company. “We’re big believers in the model of product growth and capital efficiency, and building really intuitive products that are viral, and that’s a lot of what what attracted us to DocSend,” Houston said. While DocSend has 17,000 customers, Houston says the acquisition gives the company the opportunity to get in front of a much larger customer base as part of Dropbox.

It’s worth noting that Box offers a similar secure document-sharing capability enabling users to share a link instead of using an attachment. It recently bought e-signature startup SignRequest for $55 million with an eye toward building more complex document workflows similar to what Dropbox now has with HelloSign and DocSend. PandaDoc is another competitor in this space.

Both Dropbox and DocSend participated in the TechCrunch Disrupt Battlefield, with Houston debuting Dropbox in 2008 at the TechCrunch 50, the original name of the event. Meanwhile, DocSend participated in 2014 at TechCrunch Disrupt in New York City.

DocSend’s approximately 50 employees will be joining Dropbox when the deal closes, which should happen soon, subject to standard regulatory oversight.

Powered by WPeMatico

Each of the big three cloud vendors — Amazon, Microsoft and Google — has a marketplace where software vendors can sell their wares. It seems like an easy enough proposition to throw your software up there and be done with it, but it turns out that it’s not quite that simple, requiring a complex set of business and technical tasks.

Tackle, a startup that wants to help ease the process of getting a product onto one of these marketplaces, announced a $35 million Series B today. Andreessen Horowitz led the investment with help from existing investor Bessemer Venture Partners. The company reports it has now raised $48.5 million.

Company founder Dillon Woods says that at previous jobs, he found that it took several months with a couple of engineers dedicated to the task to get a product onto the AWS marketplace, and he noticed that it was a similar set of tasks each time.

“What I saw [in my previous jobs] was that we were kind of redoing the same work. And I thought everybody out there was probably reinventing the same wheel. And so when I started Tackle, my goal was to create a software platform that would take that time down to one or two days. So it’s really a no-code solution, and it makes it much more of a business decision, rather than this big technical integration project,” Woods told me.

While you may think it’s a pretty simple task to put an app on one of these marketplaces, Woods points out that the AWS user guide explaining the ins and outs is a 700-page pdf. He says that it’s not just the technical complexity of setting up the various API calls to get it connected, there is also the business side of selling in the marketplace, and that requires additional APIs.

“There’s not just the initial sale. There could be things later like upgrades, refunds, cancellations — maybe you need to do overage charges against that same contract. And so there are all of these downstream things that happen that all require API integration, and Tackle takes care of all of that for you,” Woods explained.

CEO John Jahnke says that the company usually starts with one product in one marketplace, which acts as a kind of proof of concept for the customer, then builds up from there. Once customers see what Tackle can do, they can expand usage.

It seems to be working, with the startup reporting that it tripled annual recurring revenue (ARR), although it didn’t want to share a specific number. It also doubled headcount and the number of customers and was responsible for over $200 million in transactions across the three cloud marketplaces.

Jahnke didn’t share the exact number of customers, but he said there were currently hundreds on the platform, including companies like Snowflake, GitHub, New Relic and PagerDuty.

The company currently has 67 employees spread across 25 states, with plans to almost double that by the end of 2021. He says that it’s essential to put systems in place to build a diverse company now.

“How we scale through this next 100% increase in headcount is going to define the mix of the company into the future. If we can get this right right now and continue to extend on the foundation for diversity and inclusion that we started and make it a real part of our conversation at some scale, we think we’ll be set up as we go from 100 employees to 1,000 employees over the long period of time to continue to grow and create opportunities for people wherever they are,” Jahnke said.

Martin Casado, general partner at lead investor a16z, says this type of selling has become essential for businesses and that’s why he wanted to invest in the company. “Cloud marketplaces have become a primary channel for selling software quickly and conveniently. Tackle is the leading player for enabling companies to sell software through the cloud,” he said.

Powered by WPeMatico

Snowflake reported earnings this week, and the results look strong with revenue more than doubling year-over-year.

However, while the company’s fourth quarter revenue rose 117% to $190.5 million, it apparently wasn’t good enough for investors, who have sent the company’s stock tumbling since it reported Wednesday after the bell.

It was similar to the reaction that Salesforce received from Wall Street last week after it announced a positive earnings report. Snowflake’s stock closed down around 4% today, a recovery compared to its midday lows when it was off nearly 12%.

Why the declines? Wall Street’s reaction to earnings can lean more on what a company will do next more than its most recent results. But Snowflake’s guidance for its current quarter appeared strong as well, with a predicted $195 million to $200 million in revenue, numbers in line with analysts’ expectations.

Sounds good, right? Apparently being in line with analyst expectations isn’t good enough for investors for certain companies. You see, it didn’t exceed the stated expectations, so the results must be bad. I am not sure how meeting expectations is as good as a miss, but there you are.

It’s worth noting of course that tech stocks have taken a beating so far in 2021. And as my colleague Alex Wilhelm reported this morning, that trend only got worse this week. Consider that the tech-heavy Nasdaq is down 11.4% from its 52-week high, so perhaps investors are flogging everyone and Snowflake is merely caught up in the punishment.

Snowflake CEO Frank Slootman pointed out in the earnings call this week that Snowflake is well positioned, something proven by the fact that his company has removed the data limitations of on-prem infrastructure. The beauty of the cloud is limitless resources, and that forces the company to help customers manage consumption instead of usage, an evolution that works in Snowflake’s favor.

“The big change in paradigm is that historically in on-premise data centers, people have to manage capacity. And now they don’t manage capacity anymore, but they need to manage consumption. And that’s a new thing for — not for everybody but for most people — and people that are in the public cloud. I have gotten used to the notion of consumption obviously because it applies equally to the infrastructure clouds,” Slootman said in the earnings call.

Snowflake has to manage expectations, something that translated into a dozen customers paying $5 million or more per month to Snowflake. That’s a nice chunk of change by any measure. It’s also clear that while there is a clear tilt toward the cloud, the amount of data that has been moved there is still a small percentage of overall enterprise workloads, meaning there is lots of growth opportunity for Snowflake.

What’s more, Snowflake executives pointed out that there is a significant ramp up time for customers as they shift data into the Snowflake data lake, but before they push the consumption button. That means that as long as customers continue to move data onto Snowflake’s platform, they will pay more over time, even if it will take time for new clients to get started.

So why is Snowflake’s quarterly percentage growth not expanding? Well, as a company gets to the size of Snowflake, it gets harder to maintain those gaudy percentage growth numbers as the law of large numbers begins to kick in.

I’m not here to tell Wall Street investors how to do their job, anymore than I would expect them to tell me how to do mine. But when you look at the company’s overall financial picture, the amount of untapped cloud potential and the nature of Snowflake’s approach to billing, it’s hard not to be positive about this company’s outlook, regardless of the reaction of investors in the short term.

Powered by WPeMatico

We’re not digging into another IPO filing today. You can read all about AppLovin’s filing here, or ThredUp’s document here.

This morning, instead, we’re talking about an old favorite: software valuations. The folks over at Battery Ventures have compiled a lengthy dive into the 2020 software market that’s worth our time — you can read along here; I’ll provide page numbers as we go — because it helps explain some software valuations.

The Exchange explores startups, markets and money. Read it every morning on Extra Crunch, or get The Exchange newsletter every Saturday.

There’s little doubt that there is some froth in the software market, but it may not be where you think it is.

The Battery report has a lot of data points that we’ll also work through in this week’s newsletter, but this morning, let’s narrow ourselves to thinking about rising aggregate software multiples, the breakdown of multiples expansion through the lens of relative growth rates, and cap it off with a nibble on the importance, or lack thereof, of cash flow margins for the valuation of high-growth software companies.

We’ll look at the changing public market perspective, and then ask ourselves if the aggregate image that appears is good or not good for software startups.

We’ll look at the changing public market perspective, and then ask ourselves if the aggregate image that appears is good or not good for software startups.

I chatted through pieces of the report with its authors, Battery’s Brandon Gleklen and Neeraj Agrawal. So, we’ll lean on their perspective a little as we go to help us move quickly. This is our Friday treat. Or at least mine. Let’s get into it.

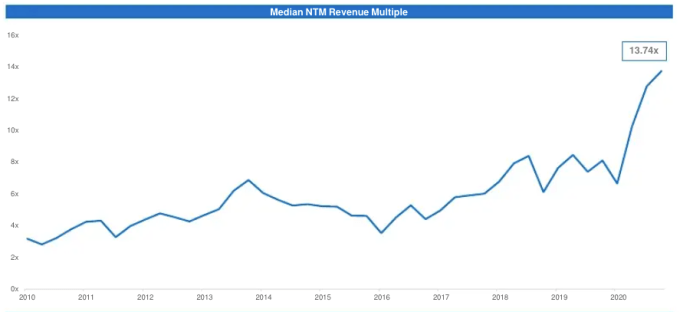

Let’s start with an affirmation. Yes, software valuations have risen to record-high multiples in recent years. Here’s the Battery chart that makes the change clear:

Page 31, Battery report. Image Credits: Battery Ventures

Powered by WPeMatico

Box could be facing troubled times if a Reuters story from last week is accurate. Activist investor Starboard Value took a 7.9% stake in the storage company in September 2019, and a year ago took three board seats as its involvement in the cloud company deepened. It seemed only a matter of time before another shoe dropped.

Activist investor Starboard Value is reportedly after three additional board seats.

That thunk you just heard could be said shoe as Starboard is reportedly after three additional board seats. Those include current CEO Aaron Levie’s and two independent board members, all of whom have their seats coming up for election in June. If the firm were to obtain three additional seats, it would control six of nine votes and could have its way with Box.

What could the future hold for the company given this development (assuming it’s true)? It seems changes are coming for Box.

Below, we’ll explore how Box got to this point. And if an acquisition is in Box’s future, just who might be in the market for a cloud-native content management company built to scale in the enterprise? There would very likely be multiple suitors.

Starboard may have reason to be frustrated by Box’s performance. The cloud company’s stock price and market cap remain stubbornly low. Its share price is mired around $18 a share, not much higher than the price it went public at in 2015 when it was valued at $14 per share. Its market cap today is $3 billion, which is lacking in comparison to fellow cloud stalwarts like Dropbox at $9 billion, Slack at $23 billion or Okta at $34 billion.

Remember back in March 2014 when Box announced it was going public? It then did something highly unusual, delaying the deed 10 months until January 2015. One thing or another kept the company from pulling the trigger and just doing it. Perhaps it was a sign.

Instead, Box raised $150 million more after its S-1 filing received a lackluster response from the market. Looking back, you could argue that the SaaS model was simply less well known in 2014 than it is today. Certainly public investors are more sympathetic to software companies that run deficits in the name of growth than they were back then.

But when Box did file again, finally pricing at $14 per share in 2015, it received a strong welcome. The company had priced above its $11 to $13 per-share IPO range as TechCrunch reported at the time and instantly shot higher. We wrote on its IPO day that the cloud company quickly “surged to over $20 a share and [was then] trading at $23.67.”

A year later, our continuing coverage had flipped with the share price stuck at $10 in January 2016.

Powered by WPeMatico