cloud

Auto Added by WPeMatico

Auto Added by WPeMatico

For IBM, much of the last eight years simply posting positive revenue growth was a challenge. In fact, the company had a period between 2013 and 2018 when it experienced an astonishing 22 straight quarters of negative revenue growth. So when Big Blue reported yesterday that revenue was up slightly, I’m sure the company took that as a win. Investors appear to be happy with the results, with the stock up 4.73% this morning as of publication.

Consider that over the last eight quarters encompassing FY2019 and FY2020, the company had only one positive revenue quarter when it was up 0.1% in Q42019. It had had five losing quarters prior to that one. When you look at yesterday’s report in that light, and combine it with growth in the Cloud and Cognitive Services group, it adds up to a decent quarter for IBM, one it badly needed after another negative report in the prior quarter.

Looking back at the January report, the company reported Cloud and Cognitive Services revenues down 4.5% at $6.8 billion, which was a big blow, considering the company has been betting much of its future on those very areas, fueled in large part by the $34 billion Red Hat acquisition in 2018.

Its most recent quarterly report proved much better, with the company reporting Cloud and Cognitive Services revenues of $5.4 billion, up 3.8% YoY. Interestingly quarter-on-quarter revenue for the segment was down, but rose on a year-over-year basis. Perhaps a year-end enterprise revenue push could account for the difference between Q4 2020 and Q1 2021.

At any rate, IBM CEO Arvind Krishna saw today’s report as a positive sign that his attempts to push the company toward a future focused on hybrid computing and AI were starting to take root. He also saw enough in the report to predict some growth this year.

“In our last call, we shared our financial expectations for the year, revenue growth and $11 billion to $12 billion of adjusted free cash flow. While it’s still early in the year and a lot remains to be done, we are confident enough to say that we are on track,” Krishna said in the earnings call with analysts yesterday.

The company has made a number of smaller acquisitions over the last year, including a couple of consulting companies, which should help as they try to work with customers around the transition to hybrid computing and artificial intelligence, both of which tend to require a lot of hand-holding to get done.

At the same time, of course, the company is continuing apace with its spin out of the legacy infrastructure services division, which it announced last year. The plan at this point is to rename the company Kyndryl (an unfortunate choice) and complete the spin out by year’s end.

CFO Jim Kavanaugh also sees the modestly positive quarter as something the company can build on. “…in fact we are even more confident in the position we put in place with regards to our two most important measures, one, revenue growth, and second, adjusted free cash flow, which is going to provide the fuel for the investments needed for us to capture that hybrid cloud $1 trillion TAM,” Kavanaugh said in the earnings call with analysts.

All of this is being pushed by Red Hat, which grew revenue 15% in the most recent quarter, something the company is banking will continue to advance it deeper into positive territory throughout the rest of 2021.

Krishna is not looking for booming growth by any means. He just wants growth, and even sustained single-digit top line expansion will make him happy. “Our systems if I take a two-year to three-year view kind of flattish, but in any given year it might increase or decrease but not by a whole lot. It doesn’t impact the top line a lot and that’s how sort of we get to the mid-single-digit sustainably,” Krishna said in the call.

The CEO simply wants to bring some long-term stability back to the company it has been sadly lacking in recent years. Of course, it’s hard to know if this quarter was a temporary upward blip on IBM’s earnings chart, one of those fluctuations up or down he spoke of, or if it is the corner the company has been looking to turn for years. Only time will tell whether IBM can sustain the modest revenue goals Krishna has set for the organization, or if it will fall back into the revenue doldrums that have plagued the company for the last eight years.

Powered by WPeMatico

When Zoom launched Zoom Apps and the Marketplace as a place to sell them last year, it was a big signal that the company wanted to be more than just a popular video conferencing application. It wanted to be a platform, which developers could use to build applications on top of Zoom.

Today the company announced a $100 million investment fund to encourage the most promising startups using the Zoom toolset to launch a business by giving them funding, while using that as a springboard to encourage other developers to take advantage of the tooling on the platform.

“We’re looking for companies with a viable product and early market traction, and a commitment to developing on and investing in the Zoom ecosystem,” Zoom’s Colin Born wrote in a blog post announcing the new program.

The company’s corporate development team, with heavy involvement from the Zoom executive team, will be in charge of selecting and managing the portfolio companies. The company plans to invest between $250,000 and $2.5 million in each startup in the portfolio.

“A big part of this is helping facilitate those early companies and giving them the access to resources and connections within Zoom, so that they can grow and succeed,” Zoom CTO Brendan Ittelson told me.

While the company wants to invest successfully, a big part of this is using the fund to encourage developers to take advantage of the platform offerings from Zoom. “We feel we’ll help [these startups] build these valuable and engaging experiences and by having that and by investing, we’re helping bring solutions and further expand the ecosystem and our customers should benefit from that,” he said.

Zoom has a number of developer tools that budding entrepreneurs can use to build applications that take advantage of Zoom functionality. In March the company introduced an SDK (software development kit) designed to help programmers embed Zoom functionality inside other applications.

The company also provides tools for embedding an application inside of Zoom, such as one designed for a specific purpose, like education or healthcare, and it has created a centralized place to learn about all of them at developer.zoom.us.

Zoom is not alone in investing in companies building applications on its platform. Firms like Sequoia, Maven Ventures and Emergence Capital have already started investing in startups building companies on top of Zoom, including Mmhmm, Docket and ClassEdu.

The fund gives startup founders one more option to get some funding to get their idea off the ground. Ittelson says all of the investments will be seed-level investments for starters, and they will be providing developer and business resources to help the young startups build and distribute their products.

While he says the company will be on the lookout for promising startups to bring into the portfolio, interested entrepreneurs can apply directly at zoom.com/fund.

Powered by WPeMatico

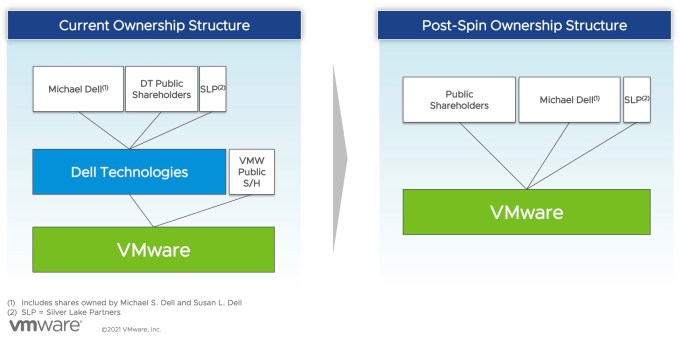

TechCrunch has spilled much digital ink tracking the fate of VMware since it was brought to Dell’s orbit thanks to the latter company’s epic purchase of EMC in 2016 for $58 billion. That transaction saddled the well-known Texas tech company with heavy debts. Because the deal left VMware a public company, albeit one controlled by Dell, how it might be used to pay down some of its parent company’s arrears was a constant question.

Dell made its move earlier this week, agreeing to spin out VMware in exchange for a huge one-time dividend, a five-year commercial partnership agreement, lots of stock for existing Dell shareholders and Michael Dell retaining his role as chairman of its board.

So, where does the deal leave VMware in terms of independence, and in terms of Dell influence? Dell no longer will hold formal control over VMware as part of the deal, though its shareholders will retain a large stake in the virtualization giant. And with Michael Dell staying on VMware’s board, it will retain influence.

Here’s how VMware described it to shareholders in a presentation this week. The graphic shows that under the new agreement, VMware is no longer a subsidiary of Dell and will now be an independent company.

Image Credits: VMware

But with VMware tipped to become independent once again, it could become something of a takeover target. When Dell controlled VMware thanks to majority ownership, a hostile takeover felt out of the question. Now, VMware is a more possible target to the right company with the right offer — provided that the Dell spinout works as planned.

Buying VMware would be an expensive effort, however. It’s worth around $67 billion today. Presuming a large premium would be needed to take this particular technology chess piece off the competitive board, it could cost $100 billion or more to snag VMware from the public markets.

So VMware will soon be more free to pursue a transaction that might be favorable to its shareholders — which will still include every Dell shareholder, because they are receiving stock in VMware as part of its spinout — without worrying about its parent company simply saying no.

Powered by WPeMatico

When Dell announced it was spinning out VMware yesterday, the move itself wasn’t surprising; there had been public speculation for some time. But Dell could have gone a number of ways in this deal, despite its choice to spin VMware out as a separate company with a constituent dividend instead of an outright sale.

The dividend route, which involves a payment to shareholders between $11.5 billion and $12 billion, has the advantage of being tax-free (or at least that’s what Dell hopes as it petitions the IRS). For Dell, which owns 81% of VMware, the dividend translates to somewhere between $9.3 billion and $9.7 billion in cash, which the company plans to use to pay down a portion of the huge debt it still holds from its $58 billion EMC purchase in 2016.

Dell hopes to have its cake and eat it too with this deal: It generates a large slug of cash to use for personal debt relief while securing a five-year commercial deal that should keep the two companies closely aligned.

VMware was the crown jewel in that transaction, giving Dell an inroad to the cloud it had lacked prior to the deal. For context, VMware popularized the notion of the virtual machine, a concept that led to the development of cloud computing as we know it today. It has since expanded much more broadly beyond that, giving Dell a solid foothold in cloud native computing.

Dell hopes to have its cake and eat it too with this deal: It generates a large slug of cash to use for personal debt relief while securing a five-year commercial deal that should keep the two companies closely aligned. Dell CEO Michael Dell will remain chairman of the VMware board, which should help smooth the post-spinout relationship.

But could Dell have extracted more cash out of the deal?

Patrick Moorhead, principal analyst at Moor Insights and Strategies, says that beyond the cash transaction, the deal provides a way for the companies to continue working closely together with the least amount of disruption.

“In the end, this move is more about maximizing the Dell and VMware stock price [in a way that] doesn’t impact customers, ISVs or the channel. Wall Street wasn’t valuing the two companies together nearly as [strongly] as I believe it will as separate entities,” Moorhead said.

Powered by WPeMatico

Dell announced this afternoon that it’s spinning out VMware, a move that has been suspected for some time. Dell acquired VMware as part of the massive $58 billion EMC acquisition (announced as $67 billion) in 2015.

The way that the deal works is that Dell plans to offer VMware shareholders a special dividend of between $11.5 and $12 billion. As Dell owns approximately 81% of those shares that would work out to somewhere between $9.3 and $9.7 billion coming into Dell’s coffers when the deal closes later this year.

“By spinning off VMware, we expect to drive additional growth opportunities for Dell Technologies as well as VMware, and unlock significant value for stakeholders. Both companies will remain important partners, with a differentiated advantage in how we bring solutions to customers,” Dell CEO Michael Dell said in a statement.

While there is a fair amount of CEO speak in that statement, it appears to mean that the move is mostly administrative as the companies will continue to work closely together, even after the spin-off is official. Dell will remain as chairman of both companies.

In a presentation to investors, the companies indicated that the plan to work together is more than lip service. There is a five-year deal commercial agreement in place with plans to revisit that deal each year thereafter. In addition, there is a plan to sell VMware products through the Dell sales team and for VMware to continue to work with Dell Financial Services. Finally, there is a formalized governance process in place related to achieving the commercial goals under the agreement, so it’s pretty firm that these companies will continue to work closely together at least for another five years.

For its part, VMware said in a separate release that the deal will allow it “increased freedom to execute its strategy, a simplified capital structure and governance model and additional strategic, operational and financial flexibility, while maintaining the strength of the two companies’ strategic partnership.”

Dell shares are up more than 8% following the announcement. The company intends on using parts of its proceeds to deleverage, writing in a release that it will use “net proceeds to pay down debt, positioning the company well for Investment Grade ratings.” By that it means that Dell will reduce its net debt position and, it hopes, garner a stronger credit rating that will limit its future borrowing costs.

Even when it was part of EMC, VMware had a special status in that it operates as a separate entity with its own executive team and board of directors, and the stock has been sold separately as well.

The deal is expected to close at the end of this year, but it has to clear a number of regulatory hurdles first. That includes garnering a favorable ruling from the IRS that the deal qualifies for a tax-free spin-off, which could prove to be a considerable hurdle for a deal like this.

The transaction is not a surprise. The company has been open about its intention to shake up its broader corporate structure. And with Dell bloated in debt terms and, perhaps, in product scope as well, the VMware deal could be an intelligent way forward. Dell investors are more excited about the transaction than VMware shareholders, with the latter company’s stock is up a more modest 1.4%.

VMware’s most recent earnings release notes that it had $4.715 billion in “total cash, cash equivalents and short-term investments.” Perhaps its shareholders aren’t enthused at the prospect of levering VMware’s balance sheet to help Dell do the opposite.

Powered by WPeMatico

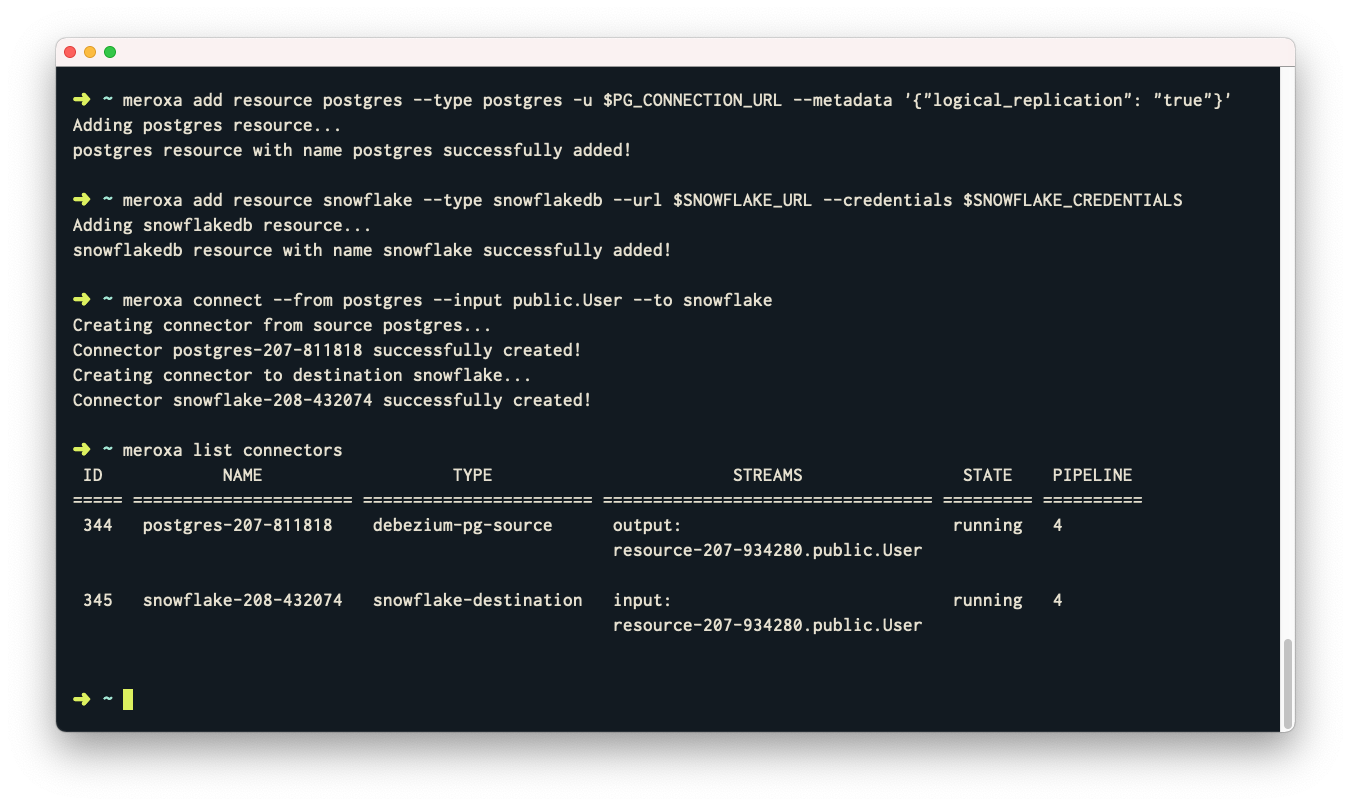

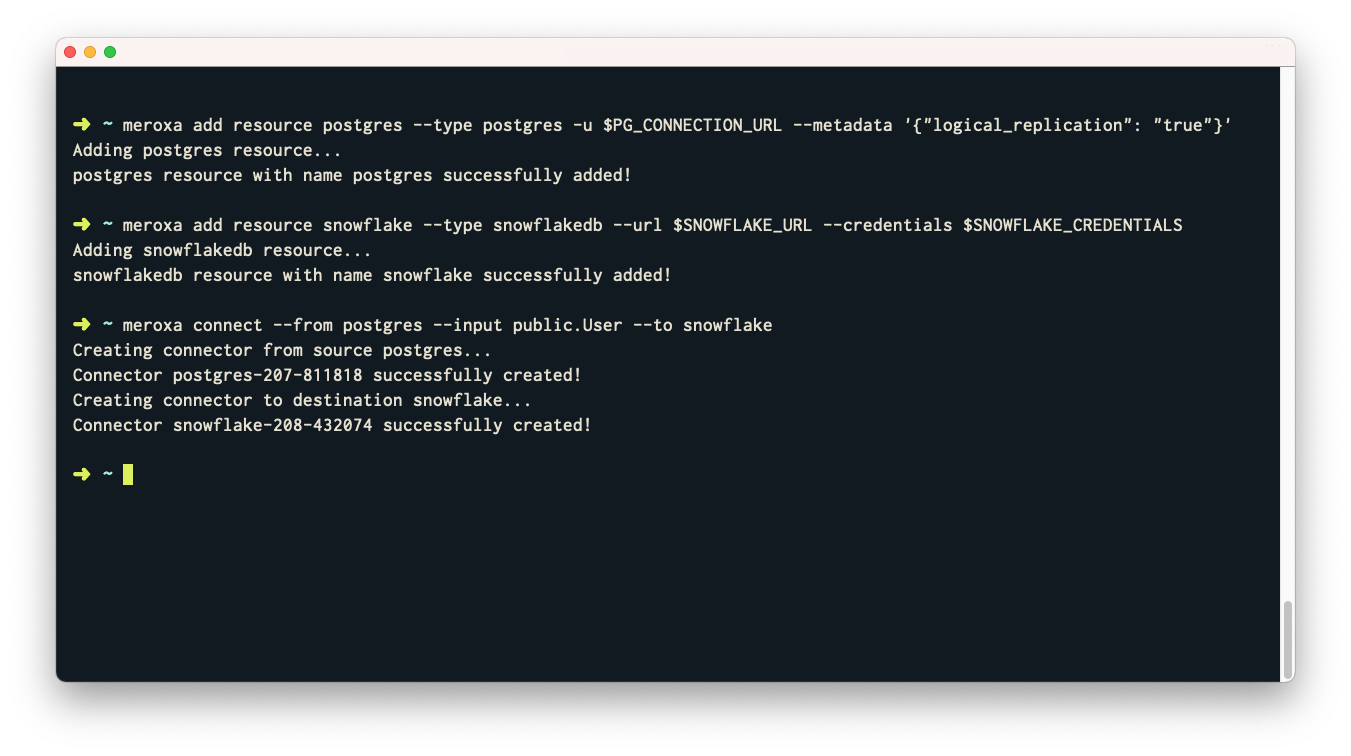

Meroxa, a startup that makes it easier for businesses to build the data pipelines to power both their analytics and operational workflows, today announced that it has raised a $15 million Series A funding round led by Drive Capital. Existing investors Root, Amplify and Hustle Fund also participated in this round, which together with the company’s previously undisclosed $4.2 million seed round now brings total funding in the company to $19.2 million.

The promise of Meroxa is that businesses can use a single platform for their various data needs and won’t need a team of experts to build their infrastructure and then manage it. At its core, Meroxa provides a single software-as-a-service solution that connects relational databases to data warehouses and then helps businesses operationalize that data.

Image Credits: Meroxa

“The interesting thing is that we are focusing squarely on relational and NoSQL databases into data warehouse,” Meroxa co-founder and CEO DeVaris Brown told me. “Honestly, people come to us as a real-time FiveTran or real-time data warehouse sink. Because, you know, the industry has moved to this [extract, load, transform] format. But the beautiful part about us is, because we do change data capture, we get that granular data as it happens.” And businesses want this very granular data to be reflected inside of their data warehouses, Brown noted, but he also stressed that Meroxa can expose this stream of data as an API endpoint or point it to a Webhook.

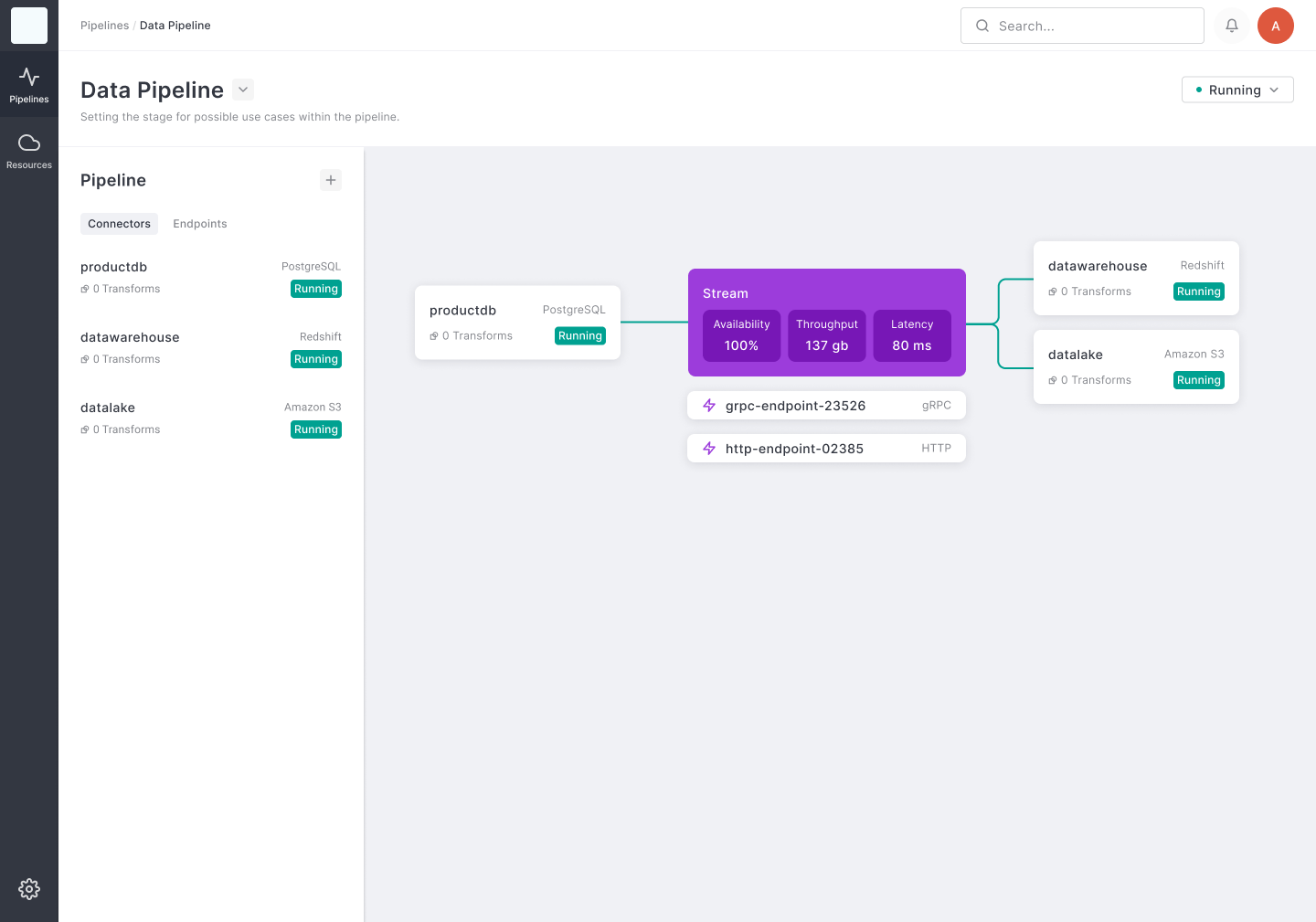

The company is able to do this because its core architecture is somewhat different from other data pipeline and integration services that, at first glance, seem to offer a similar solution. Because of this, users can use the service to connect different tools to their data warehouse but also build real-time tools on top of these data streams.

Image Credits: Meroxa

“We aren’t a point-to-point solution,” Meroxa co-founder and CTO Ali Hamidi explained. “When you set up the connection, you aren’t taking data from Postgres and only putting it into Snowflake. What’s really happening is that it’s going into our intermediate stream. Once it’s in that stream, you can then start hanging off connectors and say, ‘Okay, well, I also want to peek into the stream, I want to transfer my data, I want to filter out some things, I want to put it into S3.’ ”

Because of this, users can use the service to connect different tools to their data warehouse but also build real-time tools to utilize the real-time data stream. With this flexibility, Hamidi noted, a lot of the company’s customers start with a pretty standard use case and then quickly expand into other areas as well.

Brown and Hamidi met during their time at Heroku, where Brown was a director of product management and Hamidi a lead software engineer. But while Heroku made it very easy for developers to publish their web apps, there wasn’t anything comparable in the highly fragmented database space. The team acknowledges that there are a lot of tools that aim to solve these data problems, but few of them focus on the user experience.

Image Credits: Meroxa

“When we talk to customers now, it’s still very much an unsolved problem,” Hamidi said. “It seems kind of insane to me that this is such a common thing and there is no ‘oh, of course you use this tool because it addresses all my problems.’ And so the angle that we’re taking is that we see user experience not as a nice-to-have, it’s really an enabler, it is something that enables a software engineer or someone who isn’t a data engineer with 10 years of experience in wrangling Kafka and Postgres and all these things. […] That’s a transformative kind of change.”

It’s worth noting that Meroxa uses a lot of open-source tools but the company has also committed to open-sourcing everything in its data plane as well. “This has multiple wins for us, but one of the biggest incentives is in terms of the customer, we’re really committed to having our agenda aligned. Because if we don’t do well, we don’t serve the customer. If we do a crappy job, they can just keep all of those components and run it themselves,” Hamidi explained.

Today, Meroxa, which the team founded in early 2020, has more than 24 employees (and is 100% remote). “I really think we’re building one of the most talented and most inclusive teams possible,” Brown told me. “Inclusion and diversity are very, very high on our radar. Our team is 50% black and brown. Over 40% are women. Our management team is 90% underrepresented. So not only are we building a great product, we’re building a great company, we’re building a great business.”

Powered by WPeMatico

Workflow automation has been one of the key trends this year so far, and Zoho, a company known for its suite of affordable business tools has joined the parade with a new low code workflow product called Qntrl (pronounced control).

Zoho’s Rodrigo Vaca, who is in charge of Qntrl’s marketing says that most of the solutions we’ve been seeing are built for larger enterprise customers. Zoho is aiming for the mid-market with a product that requires less technical expertise than traditional business process management tools.

“We enable customers to design their workflows visually without the need for any particular kind of prior knowledge of business process management notation or any kind of that esoteric modeling or discipline,” Vaca told me.

While Vaca says, Qntrl could require some technical help to connect a workflow to more complex backend systems like CRM or ERP, it allows a less technical end user to drag and drop the components and then get help to finish the rest.

“We certainly expect that when you need to connect to NetSuite or SAP you’re going to need a developer. If nothing else, the IT guys are going to ask questions, and they will need to provide access,” Vaca said.

He believes this product is putting this kind of tooling in reach of companies that may have been left out of workflow automation for the most part, or which have been using spreadsheets or other tools to create crude workflows. With Qntrl, you drag and drop components, and then select each component and configure what happens before, during and after each step.

What’s more, Qntrl provides a central place for processing and understanding what’s happening within each workflow at any given time, and who is responsible for completing it.

We’ve seen bigger companies like Microsoft, SAP, ServiceNow and others offering this type of functionality over the last year as low code workflow automation has taken center stage in business.

This has become a more pronounced need during the pandemic when so many workers could not be in the office. It made moving work in a more automated workflow more imperative, and we have seen companies moving to add more of this kind of functionality as a result.

Brent Leary, principal analyst at CRM Essentials, says that Zoho is attempting to remove some the complexity from this kind of tool.

“It handles the security pieces to make sure the right people have access to the data and processes used in the workflows in the background, so regular users can drag and drop to build their flows and processes without having to worry about that stuff,” Leary told me.

Qntrl is available starting today starting at just $7 per user month.

Powered by WPeMatico

When Microsoft announced it was acquiring Nuance Communications this morning for $19.7 billion, you could be excused for doing a Monday morning double take at the hefty price tag.

That’s surely a lot of money for a company on a $1.4 billion run rate, but Microsoft, which has already partnered with the speech-to-text market leader on several products over the last couple of years, saw a company firmly embedded in healthcare and decided to go all in.

And $20 billion is certainly all in, even for a company the size of Microsoft. But 2020 forced us to change the way we do business, from restaurants to retailers to doctors. In fact, the pandemic in particular changed the way we interact with our medical providers. We learned very quickly that you don’t have to drive to an office, wait in waiting room, then in an exam room, all to see the doctor for a few minutes.

Instead, we can get on the line, have a quick chat and be on our way. It won’t work for every condition, of course — there will always be times the physician needs to see you — but for many meetings such as reviewing test results or for talk therapy, telehealth could suffice.

Microsoft CEO Satya Nadella says that Nuance is at the center of this shift, especially with its use of cloud and artificial intelligence, and that’s why the company was willing to pay the amount it did to get it.

“AI is technology’s most important priority, and healthcare is its most urgent application. Together, with our partner ecosystem, we will put advanced AI solutions into the hands of professionals everywhere to drive better decision-making and create more meaningful connections, as we accelerate growth of Microsoft Cloud in Healthcare and Nuance,” Nadella said in a post announcing the deal.

Holger Mueller, an analyst at Constellation Research, says that may be so, but he believes that Microsoft missed the boat with Cortana and this is about helping the company catch up on a crucial technology. “Nuance will be not only give Microsoft technology help in regards to neural network-based speech recognition, but also a massive improvement from vertical capabilities, call center functionality and the MSFT IP position in speech,” he said.

Microsoft sees this deal doubling what was already a considerable total addressable market to nearly $500 billion. While TAMs always tend to run high, that is still a substantial number.

It also fits with Gartner data, which found that by 2022, 75% of healthcare organizations will have a formal cloud strategy in place. The AI component only adds to that number and Nuance brings 10,000 existing customers to Microsoft, including some of the biggest healthcare organizations in the world.

Brent Leary, founder and principal analyst at CRM Essentials, says the deal could provide Microsoft with a ton of health data to help feed the underlying machine learning models and make them more accurate over time.

“There is going be a ton of health data being captured by the interactions coming through telemedicine interactions, and this could create a whole new level of health intelligence,” Leary told me.

That of course could drive a lot of privacy concerns where health data is involved, and it will be up to Microsoft, which just experienced a major breach on its Exchange email server products last month, to assure the public that their sensitive health data is being protected.

Leary says that ensuring data privacy is going to be absolutely key to the success of the deal. “The potential this move has is pretty powerful, but it will only be realized if the data and insights that could come from it are protected and secure — not only protected from hackers but also from unethical use. Either could derail what could be a game-changing move,” he said.

Microsoft also seemed to recognize that when it wrote, “Nuance and Microsoft will deepen their existing commitments to the extended partner ecosystem, as well as the highest standards of data privacy, security and compliance.”

Kate Leggett, an analyst at Forrester Research, thinks healthcare could be just the first step and once Nuance is in the fold, it could go much deeper than that.

“However, the benefit of this acquisition does not stop [with healthcare]. Nuance also offers market-leading customer engagement technologies, with deep expertise and focus in verticals such as financial services. As MSFT evolves their industry editions into other verticals, this acquisition will pay off for other industries. MSFT may also choose to fill in the gaps within their Dynamics solution with Nuance’s customer engagement technologies,” Leggett said.

We are clearly on the edge of a sea change when it comes to how we interact with our medical providers in the future. COVID pushed medicine deeper into the digital realm in 2020 out of simple necessity. It wasn’t safe to go into the office unless absolutely necessary.

The Nuance acquisition, which is expected to close some time later this year, could help Microsoft shift deeper into the market. It could even bring Teams into it as a meeting tool, but it’s all going to depend on the trust level people have with this approach, and it will be up to the company to make sure that both healthcare providers and the people they serve have that.

Powered by WPeMatico

LiquidStack does it. So does Submer. They’re both dropping servers carrying sensitive data into goop in an effort to save the planet. Now they’re joined by one of the biggest tech companies in the world in their efforts to improve the energy efficiency of data centers, because Microsoft is getting into the liquid-immersion cooling market.

Microsoft is using a liquid it developed in-house that’s engineered to boil at 122 degrees Fahrenheit (lower than the boiling point of water) to act as a heat sink, reducing the temperature inside the servers so they can operate at full power without any risks from overheating.

The vapor from the boiling fluid is converted back into a liquid through contact with a cooled condenser in the lid of the tank that stores the servers.

“We are the first cloud provider that is running two-phase immersion cooling in a production environment,” said Husam Alissa, a principal hardware engineer on Microsoft’s team for datacenter advanced development in Redmond, Washington, in a statement on the company’s internal blog.

While that claim may be true, liquid cooling is a well-known approach to dealing with moving heat around to keep systems working. Cars use liquid cooling to keep their motors humming as they head out on the highway.

As technology companies confront the physical limits of Moore’s Law, the demand for faster, higher performance processors mean designing new architectures that can handle more power, the company wrote in a blog post. Power flowing through central processing units has increased from 150 watts to more than 300 watts per chip and the GPUs responsible for much of Bitcoin mining, artificial intelligence applications and high end graphics each consume more than 700 watts per chip.

It’s worth noting that Microsoft isn’t the first tech company to apply liquid cooling to data centers and the distinction that the company uses of being the first “cloud provider” is doing a lot of work. That’s because bitcoin mining operations have been using the tech for years. Indeed, LiquidStack was spun out from a bitcoin miner to commercialize its liquid immersion cooling tech and bring it to the masses.

“Air cooling is not enough”

More power flowing through the processors means hotter chips, which means the need for better cooling or the chips will malfunction.

“Air cooling is not enough,” said Christian Belady, vice president of Microsoft’s datacenter advanced development group in Redmond, in an interview for the company’s internal blog. “That’s what’s driving us to immersion cooling, where we can directly boil off the surfaces of the chip.”

For Belady, the use of liquid cooling technology brings the density and compression of Moore’s Law up to the datacenter level

The results, from an energy consumption perspective, are impressive. The company found that using two-phase immersion cooling reduced power consumption for a server by anywhere from 5 percent to 15 percent (every little bit helps).

Microsoft investigated liquid immersion as a cooling solution for high performance computing applications such as AI. Among other things, the investigation revealed that two-phase immersion cooling reduced power consumption for any given server by 5% to 15%.

Meanwhile, companies like Submer claim they reduce energy consumption by 50%, water use by 99%, and take up 85% less space.

For cloud computing companies, the ability to keep these servers up and running even during spikes in demand, when they’d consume even more power, adds flexibility and ensures uptime even when servers are overtaxed, according to Microsoft.

“[We] know that with Teams when you get to 1 o’clock or 2 o’clock, there is a huge spike because people are joining meetings at the same time,” Marcus Fontoura, a vice president on Microsoft’s Azure team, said on the company’s internal blog. “Immersion cooling gives us more flexibility to deal with these burst-y workloads.”

At this point, data centers are a critical component of the internet infrastructure that much of the world relies on for… well… pretty much every tech-enabled service. That reliance however has come at a significant environmental cost.

“Data centers power human advancement. Their role as a core infrastructure has become more apparent than ever and emerging technologies such as AI and IoT will continue to drive computing needs. However, the environmental footprint of the industry is growing at an alarming rate,” Alexander Danielsson, an investment manager at Norrsken VC noted last year when discussing that firm’s investment in Submer.

If submerging servers in experimental liquids offers one potential solution to the problem — then sinking them in the ocean is another way that companies are trying to cool data centers without expending too much power.

Microsoft has already been operating an undersea data center for the past two years. The company actually trotted out the tech as part of a push from the tech company to aid in the search for a COVID-19 vaccine last year.

These pre-packed, shipping container-sized data centers can be spun up on demand and run deep under the ocean’s surface for sustainable, high-efficiency and powerful compute operations, the company said.

The liquid cooling project shares most similarity with Microsoft’s Project Natick, which is exploring the potential of underwater datacenters that are quick to deploy and can operate for years on the seabed sealed inside submarine-like tubes without any onsite maintenance by people.

In those data centers nitrogen air replaces an engineered fluid and the servers are cooled with fans and a heat exchanger that pumps seawater through a sealed tube.

Startups are also staking claims to cool data centers out on the ocean (the seaweed is always greener in somebody else’s lake).

Nautilus Data Technologies, for instance, has raised over $100 million (according to Crunchbase) to develop data centers dotting the surface of Davey Jones’ Locker. The company is currently developing a data center project co-located with a sustainable energy project in a tributary near Stockton, Calif.

With the double-immersion cooling tech Microsoft is hoping to bring the benefits of ocean-cooling tech onto the shore. “We brought the sea to the servers rather than put the datacenter under the sea,” Microsoft’s Alissa said in a company statement.

Ioannis Manousakis, a principal software engineer with Azure (left), and Husam Alissa, a principal hardware engineer on Microsoft’s team for datacenter advanced development (right), walk past a container at a Microsoft datacenter where computer servers in a two-phase immersion cooling tank are processing workloads. Photo by Gene Twedt for Microsoft.

Powered by WPeMatico

Okta today announced it was expanding its platform into a couple of new areas. Up to this point, the company has been known for its identity access management product, giving companies the ability to sign onto multiple cloud products with a single sign on. Today, the company is moving into two new areas: privileged access and identity governance

Privileged access gives companies the ability to provide access on an as-needed basis to a limited number of people to key administrative services inside a company. This could be your database or your servers or any part of your technology stack that is highly sensitive and where you want to tightly control who can access these systems.

Okta CEO Todd McKinnon says that Okta has always been good at locking down the general user population access to cloud services like Salesforce, Office 365 and Gmail. What these cloud services have in common is you access them via a web interface.

Administrators access the speciality accounts using different protocols. “It’s something like secure shell, or you’re using a terminal on your computer to connect to a server in the cloud, or it’s a database connection where you’re actually logging in with a SQL connection, or you’re connecting to a container, which is the Kubernetes protocol to actually manage the container,” McKinnon explained.

Privileged access offers a couple of key features including the ability to limit access to a given time window and to record a video of the session so there is an audit trail of exactly what happened while someone was accessing the system. McKinnon says that these features provide additional layers of protection for these sensitive accounts.

He says that it will be fairly trivial to carve out these accounts because Okta already has divided users into groups and can give these special privileges to only those people in the administrative access group. The challenge was figuring out how to get access to these other kinds of protocols.

The governance piece provides a way for security operations teams to run detailed reports and look for issues related to identity. “Governance provides exception reporting so you can give that to your auditors, and more importantly you can give that to your security team to make sure that you figure out what’s going on and why there is this deviation from your stated policy,” he said.

All of this when combined with the $6.5 billion acquisition of Auth0 last month is part of a larger plan by the company to be what McKinnon calls the identity cloud. He sees a market with several strategic clouds and he believes identity is going to be one of them.

“Because identity is so strategic for everything, it’s unlocking your customer, access, it’s unlocking your employee access, it’s keeping everything secure. And so this expansion, whether it’s customer identity with zero trust or whether it’s doing more on the workforce identity with not just access, but privileged access and identity governance. It’s about identity evolving in this primary cloud,” he said.

While both of these new products were announced today at the company’s virtual Oktane customer conference, they won’t be generally available until the first quarter of next year.

Powered by WPeMatico