cloud

Auto Added by WPeMatico

Auto Added by WPeMatico

Conventional wisdom over the last year has suggested that the pandemic has driven companies to the cloud much faster than they ever would have gone without that forcing event, with some suggesting it has compressed years of transformation into months. This quarter’s cloud infrastructure revenue numbers appear to be proving that thesis correct.

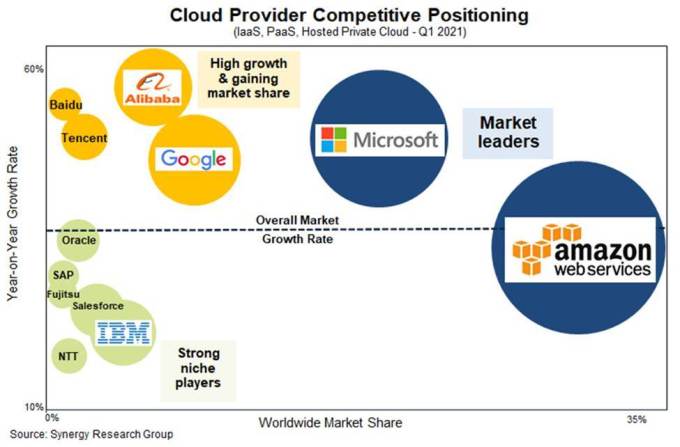

With The Big Three — Amazon, Microsoft and Google — all reporting this week, the market generated almost $40 billion in revenue, according to Synergy Research data. That’s up $2 billion from last quarter and up 37% over the same period last year. Canalys’s numbers were slightly higher at $42 billion.

As you might expect if you follow this market, AWS led the way with $13.5 billion for the quarter, up 32% year over year. That’s a run rate of $54 billion. While that is an eye-popping number, what’s really remarkable is the yearly revenue growth, especially for a company the size and maturity of Amazon. The law of large numbers would suggest this isn’t sustainable, but the pie keeps growing and Amazon continues to take a substantial chunk.

Overall AWS held steady with 32% market share. While the revenue numbers keep going up, Amazon’s market share has remained firm for years at around this number. It’s the other companies down market that are gaining share over time, most notably Microsoft, which is now at around 20% share — good for about $7.8 billion this quarter.

Google continues to show signs of promise under Thomas Kurian, hitting $3.5 billion, good for 9% as it makes a steady march toward double digits. Even IBM had a positive quarter, led by Red Hat and cloud revenue, good for 5% or about $2 billion overall.

Image Credits: Synergy Research

John Dinsdale, chief analyst at Synergy, says that even though AWS and Microsoft have firm control of the market, that doesn’t mean there isn’t money to be made by the companies playing behind them.

“These two don’t have to spend too much time looking in their rearview mirrors and worrying about the competition. However, that is not to say that there aren’t some excellent opportunities for other players. Taking Amazon and Microsoft out of the picture, the remaining market is generating over $18 billion in quarterly revenues and growing at over 30% per year. Cloud providers that focus on specific regions, services or user groups can target several years of strong growth,” Dinsdale said in a statement.

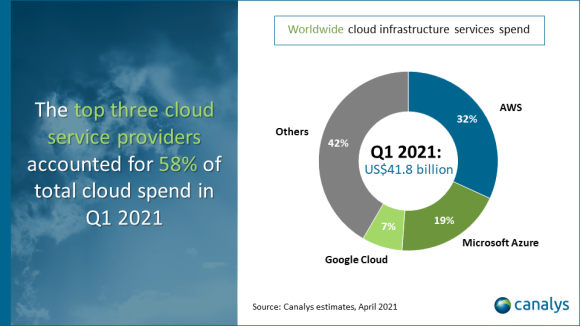

Canalys, another firm that watches the same market as Synergy, had similar findings with slight variations, certainly close enough to confirm one another’s findings. They have AWS with 32%, Microsoft 19% and Google with 7%.

Image Credits: Canalys

Canalys analyst Blake Murray says that there is still plenty of room for growth, and we will likely continue to see big numbers in this market for several years. “Though 2020 saw large-scale cloud infrastructure spending, most enterprise workloads have not yet transitioned to the cloud. Migration and cloud spend will continue as customer confidence rises during 2021. Large projects that were postponed last year will resurface, while new use cases will expand the addressable market,” he said.

The numbers we see are hardly a surprise anymore, and as companies push more workloads into the cloud, the numbers will continue to impress. The only question now is if Microsoft can continue to close the market share gap with Amazon.

Powered by WPeMatico

IBM today made another acquisition to deepen its reach into providing enterprises with AI-based services to manage their networks and workloads. It announced that it is acquiring Turbonomic, a company that provides tools to manage application performance (specifically resource management), along with Kubernetes and network performance — part of its bigger strategy to bring more AI into IT ops, or as it calls it, AIOps.

Financial terms of the deal were not disclosed, but according to data in PitchBook, Turbonomic was valued at nearly $1 billion — $963 million, to be exact — in its last funding round in September 2019. A report in Reuters rumoring the deal a little earlier today valued it at between $1.5 billion and $2 billion. A source tells us the figure is accurate.

The Boston-based company’s investors included General Atlantic, Cisco, Bain, Highland Capital Partners and Red Hat. The last of these, of course, is now a part of IBM (so it was theoretically also an investor), and together Red Hat and IBM have been developing a range of cloud-based tools addressing telco, edge and enterprise use cases.

This latest deal will help extend that further, and it has more generally been an area that IBM has been aggressive in recently. Last November IBM acquired another company called Instana to bring application performance management into its stable, and it pointed out today that the Turbonomic deal will complement that and the two technologies’ tools will be integrated together, IBM said.

Turbonomic’s tools are particularly useful in hybrid cloud architectures, which involve not just on-premise and cloud workloads, but workloads that typically are extended across multiple cloud environments. While this may be the architecture people apply for more resilience, reasons of cost, location or other practicalities, the fact of the matter is that it can be a challenge to manage. Turbonomic’s tools automate management, analyse performance and suggest changes for network operations engineers to make to meet usage demands.

“Businesses are looking for AI-driven software to help them manage the scale and complexity challenges of running applications cross-cloud,” said Ben Nye, CEO, Turbonomic, in a statement. “Turbonomic not only prescribes actions, but allows customers to take them. The combination of IBM and Turbonomic will continuously assure target application response times even during peak demand.”

The bigger picture for IBM is that it’s another sign of how the company is continuing to move away from its legacy business based around servers, movinh deeper into services, and specifically services on the infrastructure of the future, cloud-based networks.

“IBM continues to reshape its future as a hybrid cloud and AI company,” said Rob Thomas, SVP, IBM Cloud and Data Platform, in a statement. “The Turbonomic acquisition is yet another example of our commitment to making the most impactful investments to advance this strategy and ensure customers find the most innovative ways to fuel their digital transformations.”

A large part of the AI promise in the world of network operations and IT ops is how it will afford companies to rely more on automation, another area where IBM has been very active. (In a very different application of this technology — in business services — this month, it acquired MyInvenio in Italy to bring process mining technology in house.)

The promise of automation, meanwhile, is lower operation costs, a critical issue for managing network performance and availability in hybrid cloud deployments.

“We believe that AI-powered automation has become inevitable, helping to make all information-centric jobs more productive,” said Dinesh Nirmal, general manager, IBM Automation, in a statement. “That’s why IBM continues to invest in providing our customers with a one-stop shop of AI-powered automation capabilities that spans business processes and IT. The addition of Turbonomic now takes our portfolio another major step forward by ensuring customers will have full visibility into what is going on throughout their hybrid cloud infrastructure, and across their entire enterprise.”

Powered by WPeMatico

Taking on Amazon S3 in the cloud storage game would seem to be a fool-hearty proposition, but Wasabi has found a way to build storage cheaply and pass the savings onto customers. Today the Boston-based startup announced a $112 million Series C investment on a $700 million valuation.

Fidelity Management & Research Company led the round with participation from previous investors. It reports that it has now raised $219 million in equity so far, along with additional debt financing, but it takes a lot of money to build a storage business.

CEO David Friend says that business is booming and he needed the money to keep it going. “The business has just been exploding. We achieved a roughly $700 million valuation on this round, so you can imagine that business is doing well. We’ve tripled in each of the last three years and we’re ahead of plan for this year,” Friend told me.

He says that demand continues to grow and he’s been getting requests internationally. That was one of the primary reasons he went looking for more capital. What’s more, data sovereignty laws require that certain types of sensitive data like financial and healthcare be stored in-country, so the company needs to build more capacity where it’s needed.

He says they have nailed down the process of building storage, typically inside co-location facilities, and during the pandemic they actually became more efficient as they hired a firm to put together the hardware for them onsite. They also put channel partners like managed service providers (MSPs) and value added resellers (VARs) to work by incentivizing them to sell Wasabi to their customers.

Wasabi storage starts at $5.99 per terabyte per month. That’s a heck of a lot cheaper than Amazon S3, which starts at 0.23 per gigabyte for the first 50 terabytes or $23.00 a terabyte, considerably more than Wasabi’s offering.

But Friend admits that Wasabi still faces headwinds as a startup. No matter how cheap it is, companies want to be sure it’s going to be there for the long haul and a round this size from an investor with the pedigree of Fidelity will give the company more credibility with large enterprise buyers without the same demands of venture capital firms.

“Fidelity to me was the ideal investor. […] They don’t want a board seat. They don’t want to come in and tell us how to run the company. They are obviously looking toward an IPO or something like that, and they are just interested in being an investor in this business because cloud storage is a virtually unlimited market opportunity,” he said.

He sees his company as the typical kind of market irritant. He says that his company has run away from competitors in his part of the market and the hyperscalers are out there not paying attention because his business remains a fraction of theirs for the time being. While an IPO is far off, he took on an institutional investor this early because he believes it’s possible eventually.

“I think this is a big enough market we’re in, and we were lucky to get in at just the right time with the right kind of technology. There’s no doubt in my mind that Wasabi could grow to be a fairly substantial public company doing cloud infrastructure. I think we have a nice niche cut out for ourselves, and I don’t see any reason why we can’t continue to grow,” he said.

Powered by WPeMatico

DigitalOcean has emailed customers warning of a data breach involving customers’ billing data, TechCrunch has learned.

The cloud infrastructure giant told customers in an email on Wednesday, obtained by TechCrunch, that it has “confirmed an unauthorized exposure of details associated with the billing profile on your DigitalOcean account.” The company said the person “gained access to some of your billing account details through a flaw that has been fixed” over a two-week window between April 9 and April 22.

The email said customer billing names and addresses were accessed, as well as the last four digits of the payment card, its expiry date and the name of the card-issuing bank. The company said that customers’ DigitalOcean accounts were “not accessed,” and passwords and account tokens were “not involved” in this breach.

“To be extra careful, we have implemented additional security monitoring on your account. We are expanding our security measures to reduce the likelihood of this kind of flaw occuring [sic] in the future,” the email said.

DigitalOcean said it fixed the flaw and notified data protection authorities, but it’s not clear what the apparent flaw was that put customer billing information at risk.

In a statement, DigitalOcean’s security chief Tyler Healy said 1% of billing profiles were affected by the breach, but declined to address our specific questions, including how the vulnerability was discovered and which authorities have been informed.

Companies with customers in Europe are subject to GDPR and can face fines of up to 4% of their global annual revenue.

Last year, the cloud company raised $100 million in new debt, followed by another $50 million round, months after laying off dozens of staff amid concerns about the company’s financial health. In March, the company went public, raising about $775 million in its initial public offering.

Powered by WPeMatico

Red Hat CEO Paul Cormier runs the centerpiece of IBM’s transformation hopes. When Big Blue paid $34 billion for his company in 2018, it was because it believed it could be the linchpin of the organization’s shift to a focus on hybrid computing.

In its most recent earnings report, IBM posted positive revenue growth for only the second time in eight quarters, and it was Red Hat’s 15% growth that led the way. Cormier recognizes the role his company plays for IBM, and he doesn’t shy away from it.

As he told me in an interview this week ahead of the company’s Red Hat Summit, a lot of cloud technology is based on Linux, and as the company that originally made its name selling Red Hat Enterprise Linux (RHEL), he says that is a technology his organization is very comfortable working with. He sees the two companies working well together, with Red Hat benefitting from having IBM sell his company’s software, while remaining neutral technologically, something that benefits customers and pushes the overall IBM vision.

Even though Cormier has been with Red Hat for 20 years, he took over as its CEO after Arvind Krishna replaced Ginni Rometty as IBM’s chief executive and long-time Red Hat CEO Jim Whitehurst moved over to a role at IBM last April. Cormier stepped in as leader just as the pandemic hit the U.S. with its full force.

“Going into my first year of a pandemic, no one knew what the business was going to look like, and not that we’re completely out of the woods yet, but we have weathered that pretty well,” he said.

Part of the reason for that is because like many software companies, he has seen his customers shifting to the cloud much faster than anyone thought previously. While the pandemic acted as a forcing event for digital transformation, it has left many companies to manage a hybrid on-prem and cloud environment, a place where Red Hat can help.

“Having a hybrid architecture brings a lot of value […], but it’s complex. It just doesn’t happen by magic, and I think we helped a lot of customers, and it accelerated a lot of things by years of what was going to happen anyways,” Cormier told me.

In terms of the workforce moving to work from home, Red Hat had 25% of its workforce doing that even before the pandemic, so the transition wasn’t as hard as you might think for a company of its size. “Most every meeting at Red Hat had someone on remotely [before the pandemic]. And so we just sort of flipped into that mode overnight. I think we had an easier time than others for that reason,” he said.

Red Hat’s 15% growth was a big reason for IBM showing modest revenue growth last quarter, something that has been hard to come by for the last seven years. At IBM’s earnings call with analysts, CEO Krishna and CFO Jim Kavanaugh both saw Red Hat maintaining that double digit growth as key to driving the company toward more stable positive revenue in the coming years.

Cormier says that he anticipates the same things that IBM expects — and that Red Hat is up to the task ahead of it. “We see that growth continuing to happen as it’s a huge market, and this is the way it’s really playing out. We share the optimism,” he explained.

While he understands that Red Hat must remain neutral and work with multiple cloud partners, IBM is free to push Red Hat, and having that kind of sales clout behind it is also helping drive Red Hat revenue. “What IBM does for us is they open the door for us in many more places. They are in many more countries than we were [prior to the acquisition], and they have a lot of high-level relationships where they can open the door for us,” he said.

In fact, Cormier points out that IBM salespeople have quotas to push Red Hat in their biggest accounts. “IBM sales is very incentivized to bring Red Hat in to help solve customer problems with Red Hat products,” he said.

When you’re being billed as a savior of sorts for a company as storied as IBM, it wouldn’t be surprising for Cormier to feel the weight of those expectations. But if he is he doesn’t seem to show it. While he acknowledges that there is pressure, he argues that it’s no different from being a public company, only the stakeholders have changed.

“Sure it’s pressure, but prior to [being acquired] we were a public company. I look at Arvind as the chairman of the board and IBM as our shareholders. Our shareholders put a lot of pressure on us too [when we were public]. So I don’t feel any more pressure with IBM and with Arvind than we had with our shareholders,” he said.

Although they represent only 5% of IBM’s revenue at present, Cormier knows it isn’t really about that number, per se. It’s about what his team does and how that fits in with IBM’s transformation strategy overall.

Being under pressure to deliver quarter after quarter is the job of any CEO, especially one that’s in the position of running a company like Red Hat under a corporation like IBM, but Cormier as always appears to be comfortable in his own skin and confident in his company’s ability to continue chugging along as it has been with that double-digit growth. The market potential is definitely there. It’s up to Red and Hat and IBM to take advantage.

Powered by WPeMatico

Five months ago, Adobe purchased (for $1.5 billion) Workfront, a company that helps build marketing department workflows. Today the company is officially announcing how it intends to use it. As marketing executives try to balance mapping strategy to the creative process while building customized experiences, a marketing workflow tool would fit neatly into Adobe Experience Manager (AEM), and that’s where it has landed.

Alex Shootman, who was CEO at Workfront and is now VP and GM of Adobe Workfront, told me they see the tool as the system of record for the marketing department inside of AEM. While there is more than a hint of marketing in that explanation, the data from Workfront’s workflows acts as a record of the creative process.

As part of Adobe, the company has built hooks into Experience Manager and Creative Cloud to enable marketing’s creative work to move through an organized and auditable process, leaving a data trail that lets management know exactly what happened — a marketing system of record.

Shootman says having this system of record in place allows marketing teams to do several things. For starters, it lets them connect strategy to execution. “If you think about a CMO, he or she and their team is developing the key priorities for decisions for the year or for the quarter [and this helps them] take those key priorities and make sure that they are driving the activities within the marketing organization,” he said.

He says that involves connecting the people, processes and data within marketing into a single system where teams can iteratively plan on the work as changes arise. That’s where Workfront comes into play.

Brent Leary, lead analyst at CRM Essentials, says the approach makes a great deal of sense. “Creating enough personalized content at scale to stay connected with customers as their needs evolve over time is a team sport. That calls for tighter collaboration throughout the creation process, and Workfront within the AEM brings a sophisticated project management capability to the creative process,” Leary said.

During the pandemic, that became imperative as the majority of sales moved online. That increased the need for speed and agility. Having this workflow tool in place inside the Adobe Experience Manager means it’s not only allowing marketing to build customized experiences for its customers, it also enables them to automate the workflows behind those customizations.

The way this could work in practice is a marketing team creates a campaign and maps it out in Workfront. From there, creatives get assigned tasks and these tasks show up in Creative Cloud. When they complete the assignment, it automatically goes back into Workfront where it will be reviewed, eventually get approved and get published to the Digital Asset Management (DAM) tool where it will be available for use by the entire marketing team.

When it comes to acquisitions, it’s hard to know how well they’ll turn out, but Workfront seems particularly well suited to the Adobe ecosystem, a tool that can help bring a missing workflow automation component to the entire creative process, while allowing marketing execs to see exactly how their strategy played out.

Powered by WPeMatico

Getting actionable business information into the hands of users who need it has always been a challenge. If you have to wait for experts to help you find the answers, chances are you’re going to be too late. Enter Tellius, an early-stage startup building a solution to help business users find the information they need when they need it.

Today the company announced an $8 million Series A led by Sands Capital Ventures, with participation from Grotech. Today’s investment brings the total raised to $17 million, according to the company.

CEO and founder Ajay Khanna says the company is attempting to marry two technologies that have traditionally lived in silos: business intelligence and artificial intelligence. He believes that bringing them together can lead to greater wisdom and help close the insight gap.

“Tellius is an AI-driven decision intelligence platform, and what we do is we combine machine learning — AI-driven automation — with a Google-like natural language interface, so combining the left brain and the right brain to enable business teams to get insights on the data,” Khanna told me.

The idea is to let the machine learning teams and the business analysts continue to do their thing, but provide an application where business users can put all of that to work. “We believe that to go from data to decisions, you need to know not only what happened, but why things change and how you can improve your company,” he said.

The product takes aim at three employee groups. The first is the business user, who can simply query the data with a natural language question to get results. The second is a data analyst, who can get more granular by choosing a specific model to base the query on, and finally a data scientist who can enhance the query with Python or Spark code.

It connects to various data sources, including Salesforce and Google Analytics, data lakes like Snowflake, csv files to take advantage of Excel data or cloud storage tools like Amazon S3. It comes in two versions: one that the customer can connect to the cloud infrastructure provider of choice, and one which they run as a service and manage for the customers.

Khanna says that as companies struggled to change the way they do business during the pandemic, they needed the kind of insights his company provides, and business grew 300% last year as a result.

The startup launched in 2016 after Khanna sold a previous company, which allowed him to bootstrap while in stealth. They spent a couple of years building the product and brought the first version of Tellius to market in Q3 2018. That’s when they took a $7.5 million seed round.

Powered by WPeMatico

Google today announced a sizable update to its Anthos multicloud platform that lets you build, deploy and manage containerized applications anywhere, including on Amazon’s AWS and (in preview) on Microsoft Azure.

Version 1.7 includes new features like improved metrics and logging for Anthos on AWS, a new Connect gateway to interact with any cluster right from Google Cloud and a preview of Google’s managed control plane for Anthos Service Mesh. Other new features include Windows container support for environments that use VMware’s vSphere platform and new tools for developers to make it easier for them to deploy their applications to any Anthos cluster.

Today’s update comes almost exactly two years after Google CEO Sundar Pichai originally announced Anthos at its Cloud Next event in 2019 (before that, Google called this project the “Google Cloud Services Platform,” which launched three years ago). Hybrid and multicloud, it’s fair to say, takes a key role in the Google Cloud roadmap — and maybe more so for Google than for any of its competitors. Recently, Google brought on industry veteran Jeff Reed to become the VP of Product Management in charge of Anthos.

Reed told me that he believes that there are a lot of factors right now that are putting Anthos in a good position. “The wind is at our back. We bet on Kubernetes, bet on containers — those were good decisions,” he said. Increasingly, customers are also now scaling out their use of Kubernetes and have to figure out how to best scale out their clusters and deploy them in different environments — and to do so, they need a consistent platform across these environments. He also noted that when it comes to bringing on new Anthos customers, it’s really those factors that determine whether a company will look into Anthos or not.

He acknowledged that there are other players in this market, but he argues that Google Cloud’s take on this is also quite different. “I think we’re pretty unique in the sense that we’re from the cloud, cloud-native is our core approach,” he said. “A lot of what we talk about in [Anthos] 1.7 is about how we leverage the power of the cloud and use what we call “an anchor in the cloud” to make your life much easier. We’re more like a cloud vendor there, but because we support on-prem, we see some of those other folks.” Those other folks being IBM/Red Hat’s OpenShift and VMware’s Tanzu, for example.

The addition of support for Windows containers in vSphere environments also points to the fact that a lot of Anthos customers are classical enterprises that are trying to modernize their infrastructure, yet still rely on a lot of legacy applications that they are now trying to bring to the cloud.

Looking ahead, one thing we’ll likely see is more integrations with a wider range of Google Cloud products into Anthos. And indeed, as Reed noted, inside of Google Cloud, more teams are now building their products on top of Anthos themselves. In turn, that then makes it easier to bring those services to an Anthos-managed environment anywhere. One of the first of these internal services that run on top of Anthos is Apigee. “Your Apigee deployment essentially has Anthos underneath the covers. So Apigee gets all the benefits of a container environment, scalability and all those pieces — and we’ve made it really simple for that whole environment to run kind of as a stack,” he said.

I guess we can expect to hear more about this in the near future — or at Google Cloud Next 2021.

Powered by WPeMatico

After an upward revision, UiPath priced its IPO last night at $56 per share, a few dollars above its raised target range. The above-range price meant that the unicorn put more capital into its books through its public offering.

For a company in a market as competitive as robotic process automation (RPA), the funds are welcome. In fact, RPA has been top of mind for startups and established companies alike over the last year or so. In that time frame, enterprise stalwarts like SAP, Microsoft, IBM and ServiceNow have been buying smaller RPA startups and building their own, all in an effort to muscle into an increasingly lucrative market.

In June 2019, Gartner reported that RPA was the fastest-growing area in enterprise software, and while the growth has slowed down since, the sector is still attracting attention. UIPath, which Gartner found was the market leader, has been riding that wave, and today’s capital influx should help the company maintain its market position.

It’s worth noting that when the company had its last private funding round in February, it brought home $750 million at an impressive valuation of $35 billion. But as TechCrunch noted over the course of its pivot to the public markets, that round valued the company above its final IPO price. As a result, this week’s $56-per-share public offer wound up being something of a modest down-round IPO to UiPath’s final private valuation.

Then, a broader set of public traders got hold of its stock and bid its shares higher. The former unicorn’s shares closed their first day’s trading at precisely $69, above the per-share price at which the company closed its final private round.

So despite a somewhat circuitous route, UiPath closed its first day as a public company worth more than it was in its Series F round — when it sold 12,043,202 shares sold at $62.27576 apiece, per SEC filings. More simply, UiPath closed today worth more per-share than it was in February.

How you might value the company, whether you prefer a simple or fully-diluted share count, is somewhat immaterial at this juncture. UiPath had a good day.

While it’s hard to know what the company might do with the proceeds, chances are it will continue to try to expand its platform beyond pure RPA, which could become market-limited over time as companies look at other, more modern approaches to automation. By adding additional automation capabilities — organically or via acquisitions — the company can begin covering broader parts of its market.

TechCrunch spoke with UiPath CFO Ashim Gupta today, curious about the company’s choice of a traditional IPO, its general avoidance of adjusted metrics in its SEC filings, and the IPO market’s current temperature. The final question was on our minds, as some companies have pulled their public listings in the wake of a market described as “challenging”.

Powered by WPeMatico