brazil

Auto Added by WPeMatico

Auto Added by WPeMatico

Creditas, the Brazilian lending business, has raised $255 million in new financing as financial services startups across Latin America continue to attract massive amounts of cash.

The company’s credit portfolio has crossed 1 billion reals ($196.66 million) and the new round will value the company at $1.75 billion thanks to $570 million raised in outside financing over five rounds.

Creditas is the latest company to benefit from a boom in financial services startup investing across the region. As the year dawned, venture investments into fintech startups in Latin America had grown from $50 million in 2014 to top $2.1 billion in 2020 across 139 deals, according to a report from CB Insights.

Investors in the round include new investors like LGT Lightstone, Tarsadia Capital, Wellington Management, e.ventures and an affiliate of Advent International, Sunley House Capital. Previous investors including SoftBank Vision Fund 1, SoftBank Latin America DFund, VEF, Kaszek and Amadeus Capital Partners also returned to put more money into the company.

“Creditas is still in the early innings of penetrating the huge untapped secured lending market in Brazil and Mexico” says Paulo Passoni, managing partner of SoftBank Latam fund, in a statement.

The company’s growth is a testament both to the need for new lending products across Latin America and the perspicacity of investors like Kaszek Ventures, whose portfolio has included several massive wins from bets on startups tackling financial services in Latin America.

“The journey since our investment in the Series A has been absolutely extraordinary. The team has executed on its vision, and Creditas has evolved into an asset-light ecosystem that resolves key financial needs of its customers throughout their lifetimes,” says Nicolas Szekasy, managing partner of Kaszek Ventures, in a statement.

Another big winner is Redpoint’s e.ventures fund, which has focused on investments in Latin America for the last several years.

“By empowering Brazilians to take control of their lending needs at reasonable rates, Creditas creates a beloved consumer product that will drive significant value for customers and investors. Having been involved since the seed stage through Redpoint e.ventures, we’re thrilled to support the company with our Global Growth Fund as well, as they change the Brazilian fintech landscape,” said Mathias Schilling, co-founder and managing partner of e.ventures.

Creditas has plans to use the cash to expand its home and auto lending as well as a payday lending service based on customers’ salaries and a retail option to sell through buy now, pay later loans based on a customer’s salary.

The company is also looking to expand to other markets, with an eye toward establishing a foothold in the Mexican market.

Founded in 2012, when the founders worked out of a five-square-meter office on Berrini Avenue in São Paulo, the company now boasts a robust business with hundreds of employees and a business resting on a secured lending marketplace and independent home and auto lending operations.

The company also released quarterly results for the first time, showing losses narrowing from 74.9 million Brazilian reals to 40.5 million reals in the year ago quarter.

Powered by WPeMatico

With nearly half a million customers across Mexico and a network of 30,000 retail locations where representatives can take deposits, the challenger bank albo is already on its way to becoming a dominant player in Mexico’s emerging fintech industry.

And the company has recently raised another $45 million to consolidate its position.

“When your mission is to build the biggest bank in Mexico, you will need a ton of money,” said albo founder Angel Sahagún.

The company received its license to operate as a full depository bank in Mexico, and is slowly working toward being the premier internet-based financial services provider for Mexico’s large and growing middle class, Sahagún said.

“We are targeting a similar target market to Chime,” the albo founder and chief executive said. “We are targeting people who are underbanked and don’t have access to all the financial products in the market.”

Sahagún said the money will be used to expand into lending and insurance products the range of services albo offers. That’s a path that has already produced one multi-billion-dollar business in Nubank, Brazil’s wildly successful fintech company, which planted a flag for a new generation of Latin American startups.

While many challenger banks in the region pursued a strategy targeting upper-class and upper-middle-class consumers, Sahagún said his service had chosen a different path.

The company is trying to bring the middle and low-income Mexican consumers into the banking system by making it easy for them to move from a cash-based world to a digital one. “Where 90% of transactions are cash-based you need a value proposition that fits very well on that cash-based society,” Sahagún said.

It’s why the company set up a network of 30,000 locations, including convenience stores and drug stores, so that it can accept deposits at the places where its customers frequent.

That growth, and the company’s 40% share of the digital banking market in Mexico, according to data from Apptopia cited by the company, is why investors like Valar Ventures, Greyhound Capital, Mountain Nazca and Flourish Ventures were willing to invest as part of the $45 million round.

“albo has proven its ability to drive sustainable growth and is leading the market. This is the team that is going to transform banking in the region and we are proud to be supporting them in that,” said James Fitzgerald of Valar Ventures, in a statement.

Powered by WPeMatico

Since 2007, the number of publicly listed companies in Brazil has decreased from 400 to just a little over 300.

In the past six years there were only 21 IPOs — an average of just 3.5 public exits per year; by 2019, even Iran had more listed companies than Brazil. Global capital markets are heated given pandemic stimulus packages and low interest rates worldwide, but in Brazil the boom comes with a special feature: in Q3 2020, there were 25 primary and secondary equity offerings, and this year is on track to be the most active in history both in number of deals and dollar volume.

The most important event, however, is not necessarily the reversal of a shrinking public market but the fact that startups are issuing stocks for the first time, a dramatic change for a market previously dominated by industries like commodities and utilities.

Not only is Brazil’s IPO market roaring, the waitlist is even more impressive: More than 47 companies have filed at CVM (equivalent to the the Securities and Exchange Commission) to issue equity and are waiting for approval. In other words, the IPO is equivalent to more than 15% of the number of publicly listed companies. In the first half of October, six companies were approved to issue equity. Obviously construction and retail names are still predominant as they take advantage of the lower rates, but the main novelty are new entrants in internet and technology.

In the past decade, there were 56 IPOs in Brazil and only two were in the software space, both in 2013. That is a reflection of the profile of the investors who dominate local markets, which are used to allocating assets to companies in sectors like oil, paper and cellulose, mining or utilities. Historically, publicly listed companies in the country were value plays, as few of them had significant exposure to the domestic market and derived a significant share of revenue from commodities and exports.

As a result, companies that focused on the domestic market or on growth were never quite embraced by local investors. Many investors deploying capital in Brazil were mostly foreign and very risk-averse to the dynamics of the domestic market; in 2007, when Brazil went through a similar IPO boom, 70 percent of the demand for equity offerings came from foreign investors.

Along with an undervalued currency, growth companies struggled to find attractive valuations on the local exchange. As a result, growth companies such as Stone Payments, Netshoes, PagSeguro, Arco Educação and XP Investimentos did their IPOs in New York where they attained higher valuations. It’s ironic that there were three times more IPOs of Brazilian growth companies in the U.S. in the past five years than there were in the domestic market in the last decade.

Powered by WPeMatico

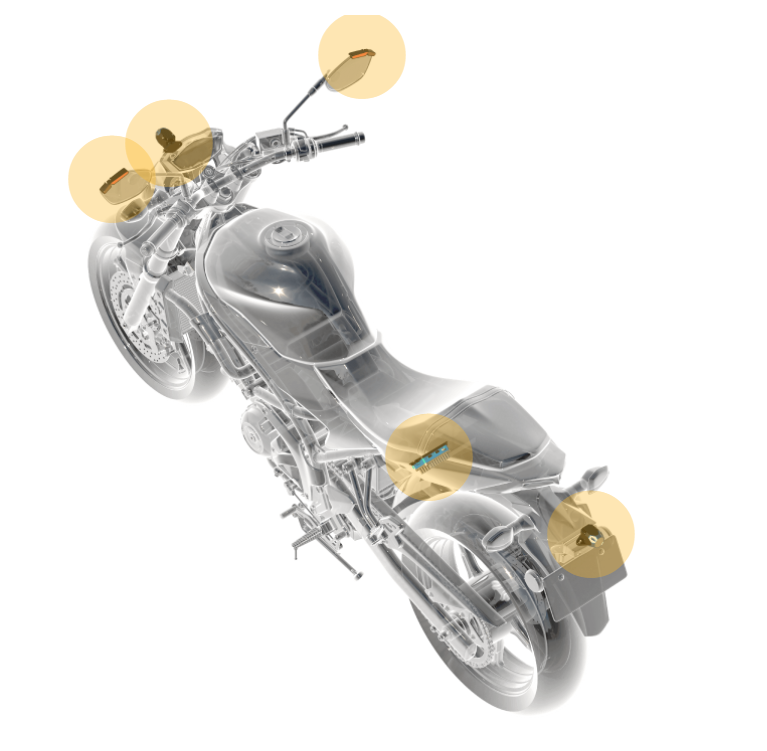

Ride Vision, an Israeli startup that is building an AI-driven safety system to prevent motorcycle collisions, today announced that it has raised a $7 million Series A round led by crowdsourcing platform OurCrowd. YL Ventures, which typically specializes in cybersecurity startups but also led the company’s $2.5 million seed round in 2018, Mobilion VC and motorcycle mirror manufacturer Metagal also participated in this round. The company has now raised a total of $10 million.

In addition to this new funding round, Ride Vision also today announced a new partnership with automotive parts manufacturer Continental .

“As motorcycle enthusiasts, we at Ride Vision are excited at the prospect of our international launch and our partnership with Continental,” Uri Lavi, CEO and co-founder of Ride Vision, said in today’s announcement. “This moment is a major milestone, as we stride toward our dream of empowering bikers to feel truly safe while they enjoy the ride.”

The general idea here is pretty straightforward and comparable with the blind-spot monitoring system in your car. Using computer vision, Ride Vision’s system, the Ride Vision 1, analyzes the traffic around a rider in real time. It provides forward collision alerts and monitors your blind spot, but it can also tell you when you’re following another rider or car too closely. It can also simply record your ride and, coming soon, it’ll be able to make emergency calls on your behalf when things go awry.

The general idea here is pretty straightforward and comparable with the blind-spot monitoring system in your car. Using computer vision, Ride Vision’s system, the Ride Vision 1, analyzes the traffic around a rider in real time. It provides forward collision alerts and monitors your blind spot, but it can also tell you when you’re following another rider or car too closely. It can also simply record your ride and, coming soon, it’ll be able to make emergency calls on your behalf when things go awry.

As the company argues, the number of motorcycles (and other motorized two-wheeled vehicles) has only increased during the pandemic, as people started avoiding public transport and looked for relatively affordable alternatives. In Europe, sales of two-wheeled vehicles increased by 30% during the pandemic.

The hardware on the motorcycle itself is pretty straightforward. It includes two wide-angle cameras (one each at the front and rear), as well as alert indicators on the mirrors, as well as the main computing unit. Ride Vision has patents on its human-machine warning interface and vision algorithms.

It’s worth noting that there are some blind-spot monitoring solutions for motorcycles on the market already, including those from Innovv and Senzar. Honda also has patents on similar technologies. These do not provide the kind of 360-degree view that Ride Vision is aiming for.

Ride Vision says its products will be available in Italy, Germany, Austria, Spain, France, Greece, Israel and the U.K. in early 2021, with the U.S., Brazil, Canada, Australia, Japan, India, China and others following later.

Powered by WPeMatico

Started as a side project by its founders, Warren is now helping regional cloud infrastructure service providers compete against Amazon, Microsoft, IBM, Google and other tech giants. Based in Tallinn, Estonia, Warren’s self-service distributed cloud platform is gaining traction in Southeast Asia, one of the world’s fastest-growing cloud service markets, and Europe. It recently closed a $1.4 million seed round led by Passion Capital, with plans to expand in South America, where it recently launched in Brazil.

Warren’s seed funding also included participation from Lemonade Stand and angel investors like former Nokia vice president Paul Melin and Marek Kiisa, co-founder of funds Superangel and NordicNinja.

The leading global cloud providers are aggressively expanding their international businesses by growing their marketing teams and data centers around the world (for example, over the past few months, Microsoft has launched a new data center region in Austria, expanded in Brazil and announced it will build a new region in Taiwan as it competes against Amazon Web Services).

But demand for customized service and control over data still prompt many companies, especially smaller ones, to pick local cloud infrastructure providers instead, Warren co-founder and chief executive officer Tarmo Tael told TechCrunch.

“Local providers pay more attention to personal sales and support, in local language, to all clients in general, and more importantly, take the time to focus on SME clients to provide flexibility and address their custom needs,” he said. “Whereas global providers give a personal touch maybe only to a few big clients in the enterprise sectors.” Many local providers also offer lower prices and give a large amount of bandwidth for free, attracting SMEs.

He added that “the data sovereignty aspect that plays an important role in choosing their cloud platform for many of the clients.”

In 2015, Tael and co-founder Henry Vaaderpass began working on the project that eventually became Warren while running a development agency for e-commerce sites. From the beginning, the two wanted to develop a product of their own and tested several ideas out, but weren’t really excited by any of them, he said. At the same time, the agency’s e-commerce clients were running into challenges as their businesses grew.

Tael and Vaaderpass’s clients tended to pick local cloud infrastructure providers because of lower costs and more personalized support. But setting up new e-commerce projects with scalable infrastructure was costly because many local cloud infrastructure providers use different platforms.

“So we started looking for tools to use for managing our e-commerce projects better and more efficiently,” Tael said. “As we didn’t find what we were looking for, we saw this as an opportunity to build our own.”

After creating their first prototype, Tael and Vaaderpass realized that it could be used by other development teams, and decided to seek angel funding from investors, like Kiisa, who have experience working with cloud data centers or infrastructure providers.

Southeast Asia, one of the world’s fastest-growing cloud markets, is an important part of Warren’s business. Warren will continue to expand in Southeast Asia, while focusing on other developing regions with large domestic markets, like South America (starting with Brazil). Tael said the startup is also in discussion with potential partners in other markets, including Russia, Turkey and China.

Warren’s current clients include Estonian cloud provider Pilw.io and Indonesian cloud provider IdCloudHost. Tael said working with Warren means its customers spend less time dealing with technical issues related to infrastructure software, so their teams, including developers, can instead focus on supporting clients and managing other services they sell.

The company’s goal is to give local cloud infrastructure providers the ability to meet increasing demand, and eventually expand internationally, with tools to handle more installations and end users. These include features like automated maintenance and DevOps processes that streamline feature testing and handling different platforms.

Ultimately, Warren wants to connect providers in a network that end users can access through a single API and user interface. It also envisions the network as a community where Warren’s clients can share resources and, eventually, have a marketplace for their apps and services.

In terms of competition, Tael said local cloud infrastructure providers often turn to OpenStack, Virtuozzo, Stratoscale or Mirantis. The advantage these companies currently have over Warren is a wider network, but Warren is busy building out its own. The company will be able to connect several locations to one provider by the first quarter of 2021. After that, Tael said, it will “gradually connect providers to each other, upgrading our user management and billing services to handle all that complexity.”

Powered by WPeMatico

Over the last five years, Brazil has witnessed a startup boom.

The main startups hubs in the country have traditionally been São Paulo and Belo Horizonte, but now a new wave of cities are building their own thriving local startup ecosystems, including Recife with Porto Digital hub and Florianópolis with Acate. More recently, a “Black Silicon Valley” is beginning to take shape in Salvador da Bahia.

While finance and media are typically concentrated in São Paulo and Rio de Janeiro, Salvador, a city of three million in the state of Bahia, is considered one of Brazil’s cultural capitals.

With an 84% Afro-Brazilian population, there are deep, rich and visible roots of Africa in the city’s history, music, cuisine and culture. The state of Bahia is almost the size of France and has 15 million people. Bahia’s creative legacy is quite clear, given that almost all the big Brazilian cultural patrimonies have their roots here, from samba and capoeira to various regional delicacies.

Many people are unaware that Brazil has the largest Black population in any country outside of Africa. Like counterparts in the U.S. and across the Americas, Afro-Brazilians have long struggled for socio-economic equity. As with counterparts in the United States, Brazil’s Black founders have less access to capital.

According to research by professor Marcelo Paixão for the Inter-American Development Bank, Afro-Brazilians are three times more likely to have their credit denied than their white counterparts. Afro-Brazilians also have over twice the poverty rates of white Brazilians and only a handful of Afro-Brazilians have held legislative positions, despite comprising more than 50% of the population. Not to mention, they make up less than 5% of the top level of the top 500 companies. Compared with countries like the United States or the United Kingdom, the racial funding gap is even more stark as more than 50% of Brazil’s population is classified as Afro-Brazilian.

Salvador (Bahia’s capital) is the natural birthplace of Brazil’s Black Silicon Valley, which largely centers around a local ecosystem hub, Vale do Dendê.

Vale do Dendê coordinates with local startups, investors and government agencies to support entrepreneurship and innovation and runs startup acceleration programs specifically focusing on supporting Afro-Brazilian founders. The Vale do Dendê Accelerator organization has already been in the spotlight at international and national publications because of its innovative work in bringing startup and tech education from mainstream to traditionally underserved communities.

In almost three years, the accelerator has supported 90 companies directly that cut across various industries, with high representation from the creative and social impact sectors. Almost all of the companies have achieved double-digit growth and various companies have gone on to raise further funding or corporate backing. One of the first portfolio companies, TrazFavela, a delivery app that focuses on linking customers and goods from traditionally marginalized communities, was supported by the accelerator in 2019. Despite the lockdown, the business grew 230% between the period of March and May after incubation and recently signed an agreement for further support and investment from Google Brasil.

There is a clear recognition of the business case for Afro-Brazilian businesses. Another company supported in the beginning with mentoring by Vale do Dendê is Diaspora Black (which focuses on Black culture in the tourism sectors). It attracted backing from Facebook Brasil and grew 770% in 2020.

The same is true for AfroSaúde, a health tech company focused on low-income communities with a new service to prevent COVID-19 in favelas (urban slums, which incidentally have high Black representation). The app now has more than 1,000 Black health professionals on its platform, creating jobs while addressing a health crisis that had been tremendously racialized.

Despite Brazil’s challenging economic situation, large national and global companies and investors are taking notice of this startup boom. Major IT company Qintess has come on board as a major sponsor to help Salvador become the leading Black tech hub in Latin America.

The company announced an investment of around 10 million reais (nearly $2 million USD) over the next five years in Black startups, including a collaboration with Vale do Dendê to train around 2,000 people in tech and accelerate more than 500 startups led by Black founders. Also, in September, Google launched a 5 million reais (around $1 million USD) Black Founders Fund with the support of Vale do Dendê to boost the Afro-Brazilian startup ecosystem.

There is no doubt that the new wave of innovation will come from the emerging markets, and the African Diaspora can play an important role. With the world’s largest African diaspora population in the hemisphere, Brazil can be a major leader on this. Vale do Dendê is keen to build partnerships to make Brazil and Latin America a more representative startup and creative economy ecosystem.

Powered by WPeMatico

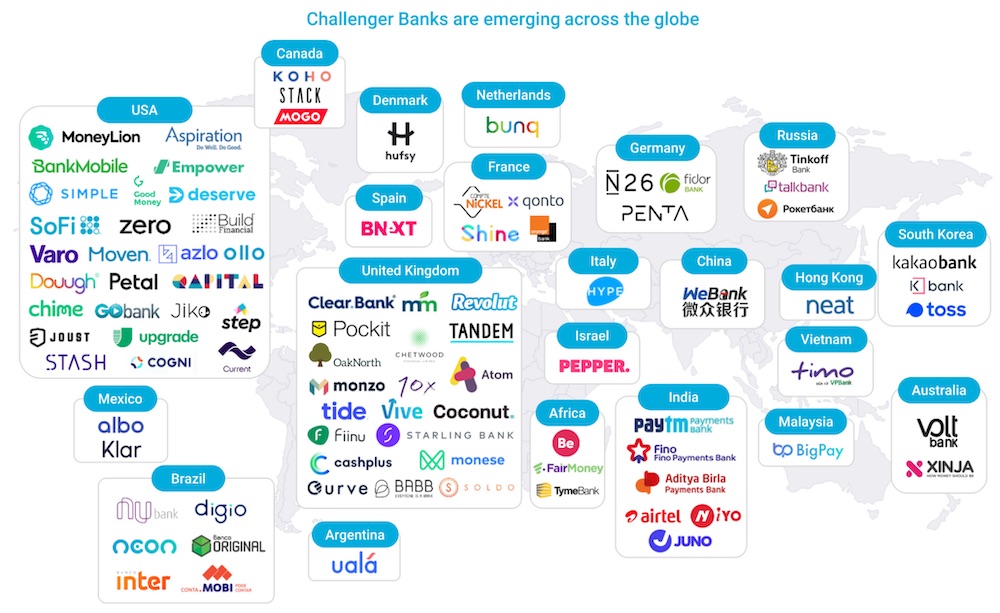

The neobank, or digital bank, phenomenon continues to take the world by storm, with global winners, from Brazil’s Nubank valued at $10 billion and Berlin’s N26 valued at $3.5 billion, to Chime, now valued at $14.5 billion as the most valuable consumer fintech in the United States.

Neobanks have led the charge of the $3.6 billion in venture capital funding for consumer fintech startups this year. And as the coronavirus-fueled acceleration of digital transformation continues, it seems the digital bank is here to stay, with some estimates pointing to neobanks reaching 60 million customers in North America and Europe by the end of 2020, and surpassing 145 million by 2024.

The space is also becoming more crowded, a trend which will only accelerate with fintech eating the world and creating greater infrastructure that enables any company to include a bank account as a product extension.

FT Partners Fintech Industry Research, January 2020

As a result, neobanks are not a monolithic model and not all are created equal. Looking underneath the hood of business models across the globe reveals remarkable operational differences and highlights specific features that are more likely to succeed in the long-term.

Today there are five distinct models that are leading globally:

Interchange-led: Relies on payments revenue, sourced through interchange as the revenue driver. Every time a customer uses the neobank’s card as a payment method they get paid [e.g. Chime / US; Neon (hybrid of 1 & 2) / Brazil].

Credit-led: Leverages a credit-first model, starting off with a credit card or similar offering, and later providing a bank account [e.g. Nubank, Neon (hybrid of 1 & 2) / Brazil].

Powered by WPeMatico

As two female investors who themselves identify as hypercultural (HC) Latinx, we see much potential for brands and startups that invest in this demographic.

For the purpose of this article, we will focus on 13-to-25-year-old individuals who can trace their heritage to a Latin American country who have spent the majority of their lifetime in the U.S. Whether they were born in the U.S. doesn’t matter as much as how much time they have spent immersed in mainstream American culture. This is important to note because this demographic is largely defined by always having one foot in their parents’ native country and another in the United States.

In simplest terms: A Latinx person has origins from a country in Latin America, like Mexico or Brazil, while a Hispanic person has origins from a country where Spanish is the dominant language, such as Mexico or Spain. A Pew Research study found that one in four people who describe themselves as Hispanic or Latino have heard of the non-gendered “Latinx,” but only 3% of them use the term in everyday life.

So what makes the hypercultural Latinx so unique and worthy of pursuit? It’s not a secret that they have massive purchasing power behind them (a collective $1.9 trillion to be exact). However, they are also different from their mostly white counterparts in the way they vigorously engage with technology, their obsession with being online at all times and their unique shopping habits.

Hypercultural Latinx consumers are accustomed to being early adopters of new technology: 81% of them say they like to learn about the latest technology (overindexing their white counterparts by 36%). Latino households are filled with the latest gadgets and smart tech toys. Although we assume most Gen Zers and young millennials love technology, HC Latinx love tech at astronomical rates and shell out more dollars than their white, mostly monocultural counterparts.

This makes sense given that 60% of HC Latinx grew up in the internet age versus only 40% of their white counterparts. Across levels of HC Latinx income (or their parents’), there is always a budget for technology. In my own Mexican household (Ilse), I grew up prioritizing tech over other (sometimes more important) categories like books or vacations.

The online lives of the HC Latinx can be summed up by one statistic: 24% spend three hours or more on social media per day. compared to only 13% of their white counterparts. So much time is spent online by this Latinx youth that they are able to create a digital comunidad where they thrive socially and intellectually. This comunidad has so much influence in how the HC Latinx thinks about what they purchase and how loyal they are to the brands they buy from.

Powered by WPeMatico

In May 2020, Intel announced its purchase of Moovit, a mobility as a service (MaaS) solutions company known for an app that stitched together GPS, traffic, weather, crime and other factors to help mass transit riders reduce their travel times, along with time and worry.

According to a release, Intel believes combining Moovit’s data repository with the autonomous vehicle solution stack for its Mobileye subsidiary will strengthen advanced driver-assistance systems (ADAS) and help create a combined $230 billion total addressable market for data, MaaS and ADAS .

Before he was a member of Niantic’s executive team, private investor Omar Téllez was president of Moovit for the six years leading up to its acquisition. In this guest post for Extra Crunch, he offers a look inside Moovit’s early growth strategy, its efforts to achieve product-market fit and explains how rapid growth in Latin America sparked the company’s rapid ascent.

In late 2011, Uri Levine, a good friend from Silicon Valley and founder of Waze, asked me to visit Israel to meet Nir Erez and Roy Bick, two entrepreneurs who had launched an application they had called “the Waze of public transportation.”

By then, Waze was already in conversations to be sold (Google would finally buy it for $1.1 billion) and Uri was thinking about his next step. He was on the board of directors of Moovit (then called Tranzmate) and thought they could use a lot of help to grow and expand internationally, following Waze’s path.

At the time, I was part of Synchronoss Technologies’ management team. After Goldman Sachs and Deutsche Bank took us public in 2006, AT&T and Apple presented us with an idea that would change the world. It was so innovative and secret that we had to sign NDAs and personal noncompete agreements to work with them. Apple was preparing to launch the first iPhone and needed a system where users could activate devices from the comfort of their homes. As such, Synchronoss’ stock became very attractive to the capital markets and ours became the best public offering of 2006.

After six years with Synchronoss while also making some forays into the field of entrepreneurship, I was ready for another challenge. With that spirit in mind, I got on the plane for Israel.

I will always remember the landing at Ben Gurion airport. After 12 hours traveling from JFK, I was called to the front of the immigration line:

“Hey! The guy in the Moovit T-shirt, please come forward!”

For a second, I thought I was in trouble, but then the immigration officer said, “Welcome to Israel! We are proud of our startups and we want the world to know that we are a high-tech powerhouse,” before he returned my passport and said goodbye.

I was completely amazed by his attitude and wondered if I really knew what I was getting into.

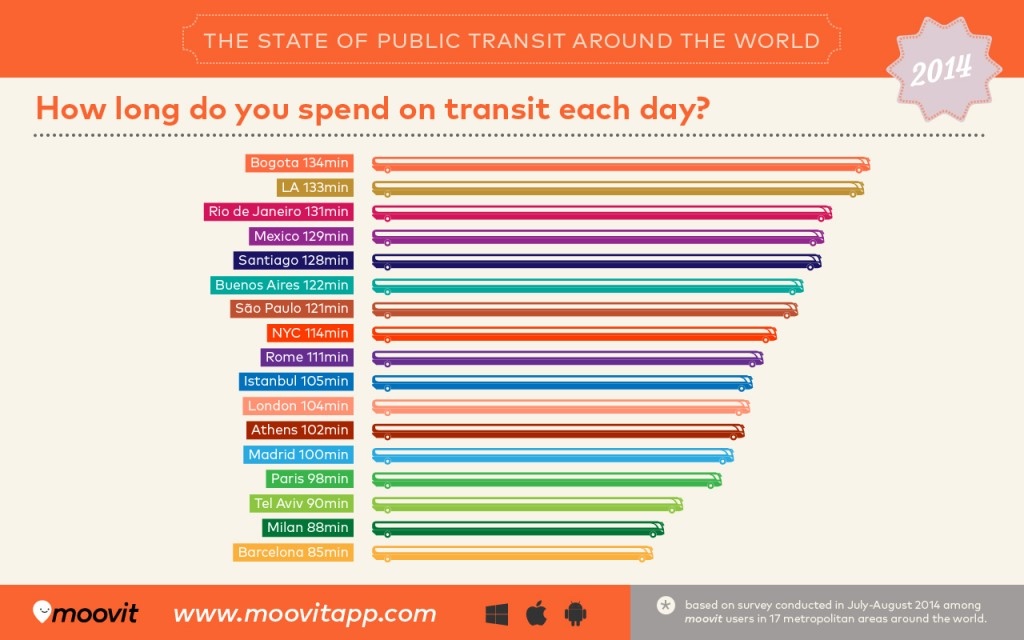

At first glance, the numbers seemed very attractive. In 2012, there were roughly seven billion people in the world and only a billion vehicles. Thus, many more people used mass public transport than private and users had to face not only the uncertainty of when a transport would arrive, but also what might happen to them while waiting (e.g., personal safety issues, weather, etc.). Adding more uncertainty: Many people did not know the fastest way to get from point A to point B. As designed, mass public transport was a real nightmare for users.

Uri advised us to “fall in love with the problem and not with the solution,” which is what we tried to do at Moovit. Although Waze had spawned a new transportation paradigm and helped reduce traffic in big cities, mass transit was a much bigger monster that consumed an average of two hours of each day for some people, which adds up to 37 days of each year*!

What would you do if someone told you that in addition to your vacation days, an app could help you find 18 extra days off work next year by cutting your transportation time in half?

* Assumes 261 working days a year, 14 productive hours per day.

Image Credits: Moovit (opens in a new window)

Powered by WPeMatico

Mobile device maker HMD Global has announced a $230M Series A2 — its first tranche of external funding since a $100M round back in 2018 when it tipped over into a unicorn valuation. Since late 2016 the startup has exclusively licensed Nokia’s brand for mobile devices, going on to ship some 240M devices to date.

Its latest cash injection is notable both for its size (HMD claims it as the third largest funding round in Europe this year); and the profile of the strategic investors ploughing in capital — namely: Google, Nokia and Qualcomm.

Though whether a tech giant (Google) whose OS dominates the world’s smartphone market (Android) becoming a strategic investor in Europe’s last significant mobile OEM (HMD) catches the attention of regional competition enforcers remains to be seen. Er, vertical integration anyone? (To wit: It’s a little over two years since Google was slapped with a $5BN penalty by EU regulators for antitrust violations related to how it operates Android — and the Commission has said it continues to monitor the market ‘remedies’.)

In a further quirk, when we spoke to HMD Global CEO, Florian Seiche, ahead of today’s announcement, he didn’t expect the names of the investors to be disclosed — but a press spokesperson had already shared them with us so he duly confirmed the trio are investors in the round. (But wouldn’t be drawn on how much equity Google is grabbing.)

HMD’s smartphones run on Google’s Android platform, which gives the tech giant a firm business reason for supporting the mobile maker in growing the availability of Google-packed hardware in key growth markets around the world.

And while HMD likens its consistent (and consistently updated) flavor of Android to the premium ‘pure’ Android experience you get from Google’s own-brand Pixel smartphones, the difference is the Finnish company offers devices across the range of price points, and targets hardware at mobile users in developing markets.

The upshot is relatively little overlap with Google’s Pixel hardware, and still plenty of business upside for Google should HMD grow the pipeline of Google services users (as it makes money by targeting ads).

Connoisseurs of mobile history may see more than a little irony in Google investing into Nokia branded smartphones (via HMD), given Android’s role in fatally disrupting Nokia’s lucrative smartphone business — knocking the Finnish giant off its perch as the world’s number one mobile maker and ushering in an era of Android-fuelled Asian mobile giants. But wait long enough in tech and what goes around oftentimes comes back around.

“We’re extremely excited,” said Seiche, when we mention Google’s pivotal role in Nokia’s historical downfall in smartphones. “How we are going to write that next chapter on smartphones is a critical strategic pillar for the company and our opportunity to team up so closely with Google around this has been a very, very great partnership from the beginning. And then this investment definitely confirms that — also for the future.”

“It’s a critical time for the industry therefore having a clear strategy — having a clear differentiation and a different point of view to offer, we believe, is a fantastic asset that we have developed for ourselves. And now is a great moment for us to double down on this,” he added.

We also asked Seiche whether HMD has any interest in taking advantage of the European Commission’s Android antitrust enforcement decision — i.e. to fork Android and remove the usual Google services, perhaps swapping them out for some European alternatives, which is at least a possibility for OEMs selling in the region — but Seiche told us: “We have looked at it but we strongly believe that consumers or enterprise customers actually love [Google] services and therefore they choose those services for themselves.” (Millions of dollars of direct investment from Google also, presumably, helps make the Google services business case stack up.)

Nokia, meanwhile, has always had a close relationship with HMD — which was established by former Nokia execs for the sole purpose of licensing its iconic mobile brand. (The backstory there is a clause in the sale terms of Nokia’s mobile device division to Microsoft expired in 2016, paving the way for Nokia’s brand to be returned to the smartphone market without the prior Windows Mobile baggage.)

Its investment into HMD now looks like a vote of confidence in how the company has been executing in the fiercely competitive mobile space to date (HMD doesn’t break out a lot of detail about device sales but Seiche told us it sold in excess of 70M mobiles last year; that’s a combined figure for smartphones and feature phones) — as well as an upbeat assessment of the scope of the growth opportunity ahead of it.

On the latter front US-led geopolitical tensions between the West and China do look poised to generate a tail-wind for HMD’s business.

Mobile chipmaker Qualcomm, for example, is facing a loss of business, as US government restrictions threaten its ability to continue selling chips to Huawei; a major Chinese device maker that’s become a key target for US president Trump. Its interest in supporting HMD’s growth, therefore, looks like a way for Qualcomm to hedge against US government disruption aimed at Chinese firms in its mobile device maker portfolio.

While with Trump’s recent threats against the TikTok app it seems safe to assume that no tech company with a Chinese owner is safe.

As a European company, HMD is able to position itself as a safe haven — and Seiche’s sales pitch talks up a focus on security detail and overall quality of experience as key differentiating factors vs the Android hoards.

“We have been very clear and very consistent right from the beginning to pick these core principles that are close to our heart and very closely linked with the Nokia brand itself — and definitely security, quality and trust are key elements,” he told TechCrunch. “This is resonating with our carrier and retail customers around the world and it is definitely also a core fundamental differentiator that those partners that are taking a longer term view clearly see that same opportunity that we see for us going forward.”

HMD does use manufacturing facilities in China, as well as in a number of other locations around the world — including Brazil, India, Indonesia and Vietnam.

But asked whether it sees any supply chain risks related to continued use of Chinese manufacturers to build ‘secure’ mobile hardware, Seiche responded by claiming: “The most important [factor] is we do control the software experience fully.” He pointed specifically to HMD’s acquisition of Valona Labs earlier this year. The Finnish security startup carries out all its software audits. “They basically control our software to make sure we can live up to that trusted standard,” Seiche added.

Landing a major tranche of new funding now — and with geopolitical tension between the West and the Far East shining a spotlight on its value as alternative, European mobile maker — HMD is eyeing expansion in growth markets such as Africa, Brail and India. (Currently, HMD said it’s active in 91 markets across eight regions, with its devices ranged in 250,000 retail outlets around the world.)

It’s also looking to bring 5G to devices at a greater range of price-points, beyond the current flagship Nokia 8.3. Seiche also said it wants to do more on the mobile services side. HMD’s first 5G device, the flagship Nokia 8.3, is due to land in the US and Europe in a matter of weeks. And Seiche suggested a timeframe of the middle of next year for launching a 5G device at a mid tier price point.

“The 5G journey again has started, in terms of market adoption, in China. But now Europe, US are the key next opportunity — not just in the premium tier but also in the mid segment. And to get to that as fast as possible is one of our goals,” he said, noting joint-working with Qualcomm on that.

“We also see great opportunity with Nokia in that 5G transition — because they are also working on a lot of private LTE deployments which is also an interesting area since… we are also very strongly present in that large enterprise segment,” he added.

On mobile services, Seiche highlighted the launch of HMD Connect: A data SIM aimed at travellers — suggesting it could expand into additional connectivity offers in future, forging more partnerships with carriers.

“We have already launched several services that are close to the hardware business — like insurance for your smartphones — but we are also now looking at connectivity as a great area for us,” he said. “The first pilot of that has been our global roaming but we believe there is a play in the future for consumers or enterprise customers to get their connectivity directly with their device. And we’re partnering also with operators to make that happen.”

“You can see us more as a complement [to carriers],” he added, arguing that business “dynamics” for carriers have also changed substantially — and customer acquisition hasn’t been a linear game for some time.

“In a similar way when we talk about Google Pixel vs us — we have a different footprint. And again if you look at carriers where they get their subscribers from today is already today a mix between their own direct channels and their partner channels. And actually why wouldn’t a smartphone player be a natural good partner of choice also for them? So I think you’ll see that as a trend, potentially, evolving in the next couple of years.”

Powered by WPeMatico