brazil

Auto Added by WPeMatico

Auto Added by WPeMatico

Ebanx, the newly minted Brazilian financial services unicorn, expects to process $2 billion in payments by the end of the year and is looking to expand its offerings into domestic payments as it grows.

Since its launch in 2012, Ebanx has primarily focused on helping international merchants sell locally in Brazil. The Brazilian business accounts for nearly 90% of the company’s revenue, but as it expands into other markets the company is also broadening its suite of services.

The company moved into local payment processing in Brazil in April of this year, and recently closed on a new financing round from previous investors FTV and Endeavor Catalyst that values the company north of $1 billion, according to chief executive Alphonse Voigt.

The money will be used to continue an aggressive hiring push in new markets and the launch of the company’s local payment services in other geographies, beginning with Colombia in the new year.

As credit cards penetrate the Latin American market, approval rates for local companies are increasing, which represents an attractive new source of revenue, Voigt says.

In addition to the local payment processing, Ebanx recently announced that it became a payment partner for the Uber Pay ecosystem in Latin America and would start processing cash voucher and bank transfer payments for Uber in Brazil and across Latin America. The company also inked deals with Coursera, Scribd, Trip.com and Shopify throughout Latin America. Finally, the company partnered with Mastercard on an initiative to increase electronic payments in the Brazilian state of Parana.

Powered by WPeMatico

SoftBank did not let up the flow of capital to Brazil this month, staying busy despite the WeWork debacle. With two more $100 million-plus rounds in QuintoAndar and MadeiraMadeira, the Japanese investor has funded at least one more unicorn in the Brazilian ecosystem. Their investments in Brazil from the past two months alone far outstrip Latin America’s venture capital funding in all of 2016.

In early September, SoftBank backed QuintoAndar for a $250 million Series D round alongside Dragoneer, General Atlantic and Kaszek Ventures, which recently made headlines for raising $600 million to invest in Latin America. QuintoAndar is a real estate rental startup that simplifies the process of locating and renting an apartment in Brazil. Although the startup only has 2% of the rentals market share in Brazil, QuintoAndar’s tech solution enabled them to scale rapidly, beating out traditional incumbents in the region’s bureaucratic rental structure.

QuintoAndar’s founders ideated the business model while they were struggling to find an apartment in São Paulo after finishing their MBAs at Stanford. They have seen property rentals grow 5x on their platform since raising a $70 million Series C just nine months ago.

SoftBank stayed bullish in Brazil with a $110 million investment in home goods marketplace Madeira Madeira, which has been described as the “Wayfair of Brazil.” This drop-shipping business has grown to sell thousands of products online with a relatively capital-light model that connects buyers directly with warehouses, saving on overhead costs. The SoftBank investment dwarfs all of Madeira Madeira’s previous capital raised — $38.8 million — by almost a factor of three.

Madeira Madeira plans to use the capital to expand across Latin America, as well as improve logistics and customer service.

David Arana, Konfio founder and CEO

Konfio provides unsecured loans to small and medium businesses in Mexico that are currently underserved by the traditional banking sector. Goldman Sachs contributed up to $100 million in secured credit to Konfio to allow them to make up to $250 million in loans to 25,000 companies over the next 12 months. Victory Park Capital also contributed to this debt round, bringing Konfio’s total raised to $43 million in equity and $260 million in debt.

This capital mints Konfio as one of the largest fintech startups in the region. It will also allow them to take on larger loan sizes. Konfio’s average loan size hovers around $20,000. Konfio uses credit ratings to calculate risk and disburse loans within 24 hours, and at half the rate of a traditional bank loan.

To date Konfio has served over 1 million clients in what is currently a $100 billion market in Mexico. Mexico’s access to credit is still significantly lower than the rest of Latin America, so Konfio is well-placed to grow within this market, especially with this new funding.

Mexican challenger bank Klar, a Chime clone, recently raised over $57.5 million in debt and equity in one of Mexico’s largest seed rounds. The $50 million credit line came from San Francisco’s Arc Labs, while Quona Capital led the $7.5 million equity round with support from Santander InnoVentures, aCrew Capital, FJ Labs and Western Technology Investment.

Klar was founded less than 10 months ago to help Mexicans access free and fair financial services through digital banking. Currently Klar offers a debit and a credit product with transparent fees; today, only 15% of Mexicans have access to credit cards, most of which have +60% interest rates and a lot of hidden fees. Klar wants to make banking accessible for everyone in Mexico through their free digital platform.

This startup will be one to watch over the coming months as it competes with Nubank and other local neobanks to bank Mexico’s unbanked.

Mexican property-tech startup Flat is taking the Opendoor model to Latin America. This startup raised an unprecedented $4.6 million in their pre-seed round led by ALL VP, with support from Liquid2 Ventures, Next Billion, Picus Capital and angels.

Besides Mexican e-scooter giant, Grin, Flat’s pre-seed is the largest ever for Mexico. Flat’s founders, Victor Noguera and Bernardo Cordero, are betting on a $25 billion home sales market in Mexico that is currently stuck in the 20th century. Flat will allow homeowners and buyers to gain access to accurate information about home prices (think Zillow in the U.S.), as well as managing the slow process of notarizing the purchase after the fact. With Flat, the startup manages everything from valuation to ownership transfer, all through their platform, and within 72 hours of purchase.

Flat will use this investment to vertically integrate within the Mexican market, rather than expanding across Latin America.

Powered by WPeMatico

Another day, another mega round for a fintech startup. And this one is mega-mega.

Brazil-based Nubank, which offers a suite of banking and financial services for Brazilian consumers, announced today that it has raised a $400 million Series F round of venture capital led by Woody Marshall of TCV. The growth-stage fund is best known for its investment in Netflix but has also made fintech a high priority, with over $1.5 billion in investments in the space. According to Nubank, the company has now raised $820 million across seven venture rounds.

Katie Roof and Peter Rudegeair of The Wall Street Journal reported this morning that the company secured a valuation above $10 billion, potentially making it one of a short list of startup decacorns. That’s up from the $4 billion valuation we wrote about back in October 2018.

Part of the reason for that big-ticket round is the company’s growth. Nubank said in a statement that it has now reached 12 million customers for its various products, making it the sixth-largest financial institution by customer count within its home market. Brazil has a population of roughly 210 million people — indicating that there is still a lot of local growth potential even before the company begins to consider its international expansion options. Nubank announced a few weeks ago that it will start to expand its offerings to Mexico and Argentina.

Over the past year, the company has expanded its product offerings to include personal loans and cash withdrawal options as part of its digital savings accounts.

As I wrote earlier this week, part of the reason for these fintech mega-rounds is that the cost of acquiring a financial customer is critical to the success of these startups. Once a startup has a customer for one financial product — say, a savings account — it can then upsell customers to other products at a very low marketing cost. That appears to be the strategy at Nubank as well, with its quickly expanding suite of products.

As my colleague Jon Shieber discussed last month, critical connections between Stanford, Silicon Valley and Latin America have forged a surge of investment from venture capitalists into the region, as the continent experiences the same digital transformation seen elsewhere throughout the world. As just one example from the healthcare space, Dr Consulta raised more than nine figures to address the serious healthcare needs of Brazilian consumers. Additionally, SoftBank’s Vision Fund, which was rumored to be investing in Nubank earlier this year, has vowed to put $5 billion to work in the region and recently invested $231 million in fintech startup Creditas.

In an email from TCV, Woody Marshall said that, “Leveraging unique technology, David Vélez and his team are continuously pushing the boundaries of delivering best in class financial services, grounded in a culture of tech and innovation. Nubank has all the core tenets of what TCV looks for in preeminent franchise investments.”

NuBank was founded in 2013 by co-founders Adam Edward Wible, Cristina Junqueira, and David Velez. In addition to TCV, existing backers Tencent, DST Global, Sequoia Capital, Dragoneer, Ribbit Capital and Thrive Capital also participated in the round.

Powered by WPeMatico

Nowports, a developer of software and services to track freight shipments from ports to destinations across Latin America, has aims to become the regional answer to Flexport’s billion-dollar digital shipping business.

Almost 54 million containers are imported and exported from Latin America each year, and nearly half of them are either delayed or lost due to mismanagement.

Nowports is pitching shippers on its digital management software to keep track of each container, and has signed on a number of leading venture capital firms to fulfill its mission.

The Monterrey, Mexico-based company raised $5.3 million in its seed round of financing. The round was led by Base10 and Monashees, with participation from Y Combinator and additional investors like Broadhaven, Soma Capital, Partech, Tekton and Paul Buchheit.

“In Nowports we saw a very strong combination: well prepared and ambitious team using technology to help thousands of customers to improve their importing and exporting processes. By adding efficiency, reliability, and transparency to change a multi-billion dollar industry, Nowports has been able to attract many clients that saw significant improvements in their daily routines by using the solution” said Caio Bolognesi, general partner from Monashees, in a statement.

The company said it would use the money to expand into new markets, grow its team and integrate with more companies involved in the (very fragmented) Latin American logistics industry. It’s a market that needs a range of better logistics technologies.

“Even though over 90% of the world’s trade is carried by sea, the most cost-effective way to move goods en masse, there has yet to be a solution that’s able to connect suppliers, customs brokers, carriers and transportation companies to provide an efficient and reliable service,” said Maximiliano Casal, founder and chief executive of Nowports, in a statement. “This is why we launched Nowports, combining our 10 years of industry expertise to fill this void and are currently working with over 40 customers in the region and growing.”

The company now has offices in Chile and Uruguay, and is planning to expand to Brazil, Colombia and Peru.

“With platforms, algorithms with AI and integrations, our platform allows companies to take control of their shipments and plan and predict the best timing to move the freight based on the needs of their own company,” said Alfonso De Los Rios, founder and CTO of Nowports.

As the company looks to expand, it has a strategic road map it can follow in the growth of Flexport, the Silicon Valley startup that has become a billion-dollar business by applying technology to the outdated shipping industry.

The two co-founders of Nowports met at a program at Stanford University, with De Los Rios hailing from a family with deep ties to the shipping industry. He and Casal linked up and the two began plotting a way to make the deeply inefficient industry more modern and transparent. To familiarize himself with the market for which he’d be developing a technology, Casal worked in a freight forwarder in Kansas City that had been operating for more than 30 years.

In all, freight providers are getting paid nearly $40 billion per year to move freight into Latin America.

“Alfonso and Max are the ideal founders we look to invest in as they are industry experts and passionate about evolving the industry using technology and automation,” said Adeyemi Ajao, general partner from Base10. “We are proud to be investors in Nowports alongside our friends at Monashees and look forward to watching the company’s continued growth.”

Powered by WPeMatico

Andreessen Horowitz <3 Latin American startups.

Latin America is the only region outside of the U.S. where the venture firm is routinely investing capital, and it just made another commitment, doubling down on its early-stage support for the point-of-sale lending startup ADDI.

ADDI picked up $12.5 million in new financing in April of this year as the company looks to expand its lending services online.

For an American audience, the closest corollary to what ADDI is up to is likely Affirm, the point-of-sale lender that’s raised a ton of cash and come in for some (valid) criticism for its basic business model.

Like Affirm, ADDI lets its borrowers apply for credit at the moment of purchase. The company likens its service to the layaway and credit plans that already exist in Colombia — but involve pretty onerous requirements to use. Company co-founder Santiago Suarez and Andreessen Horowitz general partner Angela Strange both commented on how, in some cases, Colombian shoppers have to have three people vouch for a borrower before a store will issue credit or agree to a layaway plan.

The difference between an ADDI loan — or any loan — and layaway is that an installment payment plan doesn’t charge interest (and even with the fees that installment plans do charge, they are often still cheaper than taking out a loan).

But financial products are coming for consumers in Latin America whether those buyers like it or not — and for the most part, it seems they do like it.

Historically, only the wealthiest clientele in Latin America received anything resembling the kinds of financial products that are more widely available in the United States, according to Strange. And the investment in ADDI is just part of her firm’s thesis in trying to make more services more broadly available in a region where a technological transformation is creating unprecedented opportunities for challengers.

That assessment is what drew Santiago Suarez back to Latin America only two years ago. A former executive at Lending Club who previously had worked as the head of New Product Development and Emerging Services at J.P. Morgan, Suarez saw the tremendous growth happening in Latin America and returned to Colombia to see if he could bring some much needed services to his home country.

Suarez partnered with his childhood friend, Elmer Ortega, who was working as the chief technology officer of the local hedge fund where he had previously been employed as a derivatives trader before learning how to code.

Together, the two men, who had known each other since they were five years old, set out to transform how credit was offered in retail shops. It’s an industry that Suarez had known well since his parents had owned stores.

“In the U.S. there are all of these gaps that fintech companies are filling,” says Suarez. “But the gaps in Latin America are bigger.”

Suarez and Ortega incorporated the company in September 2018, around the same time they raised $2.3 million from the regional investment firm, Monashees, Andreessen and Village Global . They then raised another $1.5 million in an internal round of financing before closing the most recent funding.

The company offers loans at annual percentage rates ranging from 19.99% to 28.90%. The company started with a digital solution for brick and mortar retailers because 90% of retail in Colombia still happens offline.

Although it’s in its early days, the company has already originated 10,000 borrowers and typically loans out roughly $500 since it launched on February 22, according to Suarez. He declined to comment on the company’s default rate on loans.

Now with 40 employees on staff, the company is looking to bring its lending tool to more e-commerce and physical retailers, according to Suarez. And despite the threat of cyclical political turmoil, Suarez says there’s no better time to be investing in Colombia.

“It’s the most stable country outside of Chile… Way more stable than Brazil, way more stable than Argentina and way more stable than Mexico,” Suarez says. “What we’re looking at is more than cyclical instability… those things go beyond that. Nubank was able to build a multibillion business in the worst political and economic crisis in Brazil’s history. I think Colombia is an incredibly attractive space with a deep talent pool.”

Powered by WPeMatico

Brex, the fintech business that’s taken the startup world by storm with its sought after corporate card tailored for entrepreneurs, is raising millions in Series D funding less than a year after it launched, TechCrunch has learned.

Bloomberg reports Brex is raising at a $2 billion valuation, though sources tell TechCrunch the company is still in negotiations with both new and existing investors. Brex didn’t immediately respond to requests for comment.

Kleiner Perkins is leading the round via former general partner Mood Rowghani, who left the storied venture capital fund last year to form Bond alongside Mary Meeker and Noah Knauf. As we’ve previously reported, the Bond crew is still in the process of deploying capital from Kleiner’s billion-dollar Digital Growth Fund III, the pool of capital they were responsible for before leaving the firm.

Bond, which recently closed on $1.25 billion for its debut effort and made its first investment, is not participating in the round for Brex, sources confirm to TechCrunch. Bond declined to comment.

Brex, a graduate of Y Combinator’s winter 2017 cohort, has raised $182 million in VC funding, reaching a valuation of $1.1 billion in October 2018 three months after launching its corporate card for startups and less than a year after completing YC’s accelerator program.

Most recently, Brex attracted a $125 million Series C investment led by Greenoaks Capital, DST Global and IVP. The startup is also backed by PayPal founders Peter Thiel and Max Levchin, and VC firms such as Ribbit Capital, Oneway Ventures and Mindset Ventures, according to PitchBook.

The company’s pace of growth is unheard of, even in Silicon Valley where inflated valuations and outsized rounds are the norm. Why? Brex has tapped into a market dominated by legacy players in dire need of technological innovation and, of course, startup founders always need access to credit. That, coupled with the fact that it’s capitalized on YC’s network of hundreds of startup founders — i.e. Brex customers — has accelerated its path to a multi-billion-dollar price tag.

Brex doesn’t require any kind of personal guarantee or security deposit from its customers, allowing founders near-instant access to credit. More importantly, it gives entrepreneurs a credit limit that’s as much as 10 times higher than what they would receive elsewhere.

Investors may also be enticed by the fact the company doesn’t use third-party legacy technology, boasting a software platform that is built from scratch. On top of that, Brex simplifies a lot of the frustrating parts of the corporate expense process by providing companies with a consolidated look at their spending.

“We have a very similar effect of what Stripe had in the beginning, but much faster because Silicon Valley companies are very good at spending money but making money is harder,” Brex co-founder and chief executive officer Henrique Dubugras told me late last year.

Stripe, for context, was founded in 2010. Not until 2014 did the company raise its unicorn round, landing a valuation of $1.75 billion with an $80 million financing. Today, Stripe has raised a total of roughly $1 billion at a valuation north of $20 billion.

Dubugras and Brex co-founder Pedro Franceschi, 23-year-old entrepreneurs, relocated from Brazil to Stanford in the fall of 2016 to attend the university. They dropped out upon getting accepted into YC, which they applied to with a big dreams for a virtual reality startup called Beyond. Beyond quickly became Brex, a name in which Dubugras recently told TechCrunch was chosen because it was one of few four-letter word domains available.

Brex’s funding history

March 2017: Brex graduates Y Combinator

April 2017: $6.5M Series A | $25M valuation

April 2018: $50M Series B | $220M valuation

October 2018: $125M Series C | $1.1B valuation

May 2019: undisclosed Series D | ~$2B valuation

In April, Brex secured a $100 million debt financing from Barclays Investment Bank. At the time, Dubugras told TechCrunch the business would not seek out venture investment in the near future, though he did comment that the debt capital would allow for a significant premium when Brex did indeed decide to raise capital again.

In 2019, Brex has taken steps several steps toward maturation.Recently, it launched a rewards program for customers and closed its first notable acquisition of a blockchain startup called Elph. Shortly after, Brex released its second product, a credit card made specifically for ecommerce companies.

Its upcoming infusion of capital will likely be used to develop payment services tailored to Fortune 500 business, which Dubugras has said is part of Brex’s long term plan to disrupt the entire financial technology space.

Powered by WPeMatico

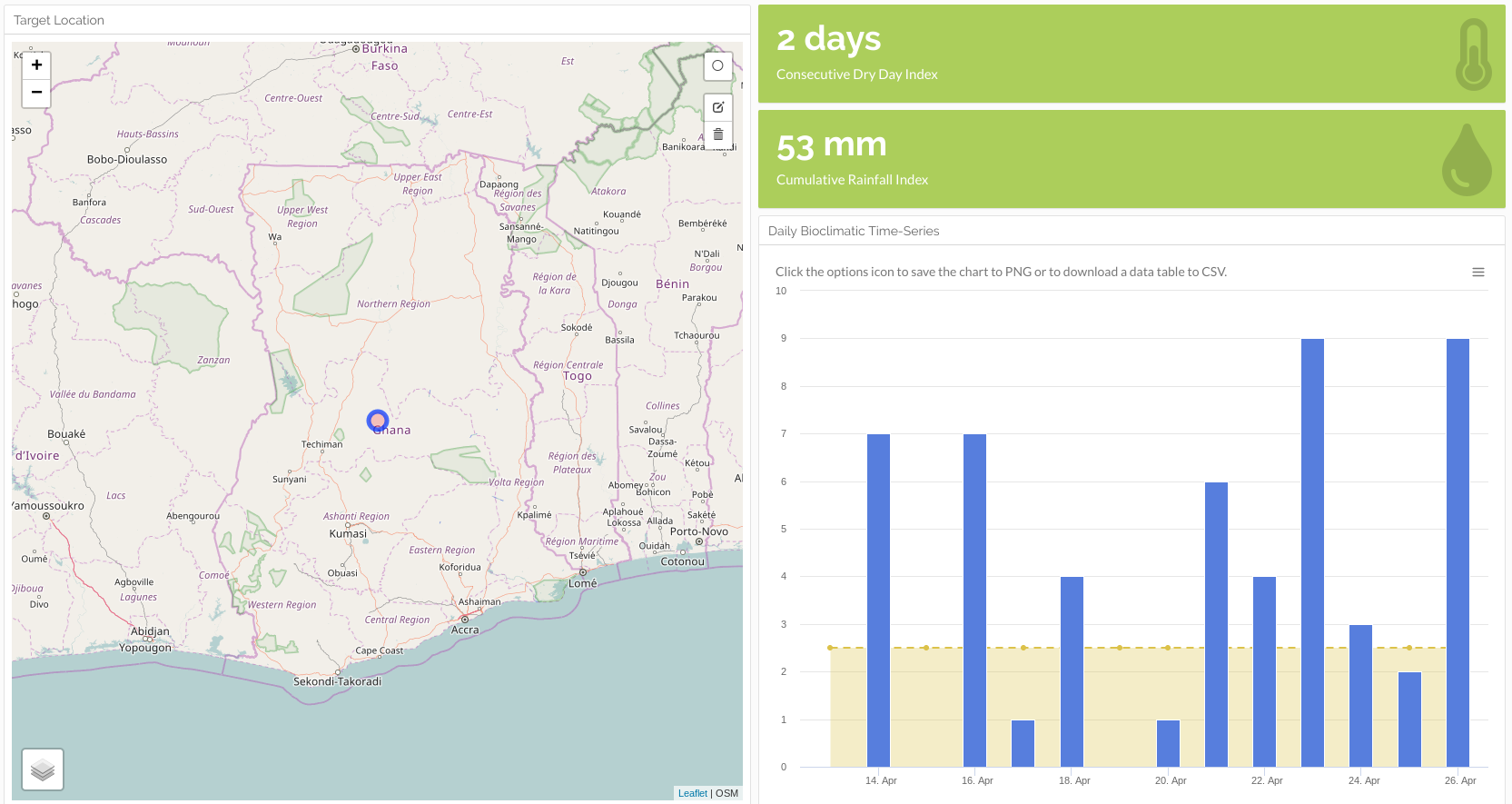

WorldCover, a New York and Africa-based climate insurance provider to smallholder farmers, has raised a $6 million Series A round led by MS&AD Ventures.

Y Combinator, Western Technology Investment and EchoVC also participated in the round.

WorldCover’s platform uses satellite imagery, on-ground sensors, mobile phones and data analytics to create insurance options for farmers whose crop yields are affected adversely by weather events — primarily lack of rain.

The startup currently operates in Ghana, Uganda and Kenya . With the new funding, WorldCover aims to expand its insurance offerings to more emerging market countries.

“We’re looking at India, Mexico, Brazil, Indonesia. India could be first on an 18-month timeline for a launch,” WorldCover co-founder and chief executive Chris Sheehan said in an interview.

The company has served more than 30,000 farmers across its Africa operations. Smallholder farmers are those earning all or nearly all of their income from agriculture, farming on 10-20 acres of land and earning around $500 to $5,000, according to Sheehan.

Farmers connect to WorldCover by creating an account on its USSD mobile app. From there they can input their region and crop type and determine how much insurance they would like to buy and use mobile money to purchase a plan. WorldCover works with payments providers such as M-Pesa in Kenya and MTN Mobile Money in Ghana.

The service works on a sliding scale, where a customer can receive anywhere from 5x to 15x the amount of premium they have paid. If there is an adverse weather event, namely lack of rain, the farmer can file a claim via mobile phone. WorldCover then uses its data-analytics metrics to assess it, and, if approved, the farmer will receive an insurance payment via mobile money.

Common crops farmed by WorldCover clients include maize, rice and peanuts. It looks to add coffee, cocoa and cashews to its coverage list.

For the moment, WorldCover only insures for events such as rainfall risk, but in the future it will look to include other weather events, such as tropical storms, in its insurance programs and platform data analytics.

For the moment, WorldCover only insures for events such as rainfall risk, but in the future it will look to include other weather events, such as tropical storms, in its insurance programs and platform data analytics.

The startup’s founder clarified that WorldCover’s model does not assess or provide insurance payouts specifically for climate change, though it does directly connect to the company’s business.

“We insure for adverse weather events that we believe climate change factors are exacerbating,” Sheehan explained. WorldCover also resells the risk of its policyholders to global reinsurers, such as Swiss Re and Nephila.

On the potential market size for WorldCover’s business, he highlights a 2018 Lloyd’s study that identified $163 billion of assets at risk, including agriculture, in emerging markets from negative, climate change-related events.

“That’s what WorldCover wants to go after…These are the kind of micro-systemic risks we think we can model and then create a micro product for a smallholder farmer that they can understand and will give them protection,” he said.

With the round, the startup will look to possibilities to update its platform to offer farming advice to smallholder farmers, in addition to insurance coverage.

WorldCover investor and EchoVC founder Eghosa Omoigui believes the startup’s insurance offerings can actually help farmers improve yield. “Weather-risk drives a lot of decisions with these farmers on what to plant, when to plant, and how much to plant,” he said. “With the crop insurance option, the farmer says, ‘Instead of one hector, I can now plant two or three, because I’m covered.’ ”

Insurance technology is another sector in Africa’s tech landscape filling up with venture-backed startups. Other insurance startups focusing on agriculture include Accion Venture Lab-backed Pula and South Africa based Mobbisurance.

With its new round and plans for global expansion, WorldCover joins a growing list of startups that have developed business models in Africa before raising rounds toward entering new markets abroad.

In 2018, Nigerian payment startup Paga announced plans to move into Asia and Latin America after raising $10 million. In 2019, South African tech-transit startup FlexClub partnered with Uber Mexico after a seed raise. And Lagos-based fintech startup TeamAPT announced in Q1 it was looking to expand globally after a $5 million Series A round.

Powered by WPeMatico

Rappi represents a new era for Latin American technology startups.

Based in Bogotá, Colombia, the on-demand delivery startup has taken the region by storm, attracting a record amount of venture capital funding in mere months. Today marks the beginning of a new round of explosive growth as SoftBank, the Japanese telecom giant and prolific Silicon Valley tech investor, has confirmed a $1 billion investment in the business.

The king-sized financing comes two months after SoftBank announced its Innovation Fund, a new pool of capital committed to spending billions on the growing tech ecosystem in Central and South America.

VC funding in Latin America catapulted to new heights in 2018. Startups located across Argentina, Brazil, Chile, Colombia and more have secured nearly $2.5 billion since the beginning of 2018, according to PitchBook, up from less than $1 billion invested in 2017.

SoftBank plans to transfer the Rappi investment to the Innovation Fund “upon the fund’s establishment,” according to a press release. For now, the SoftBank Group and affiliated Vision Fund will each invest $500 million in the company. Jeffrey Housenbold, a managing director at SoftBank responsible for investments in Brandless, Opendoor and DoorDash, will join Rappi’s board of directors.

“SoftBank’s vision of accelerating the technology revolution deeply resonated with our mission of improving how people live through digital payments and a super-app for everything consumers need,” Rappi co-founder Sebastian Mejia said in a statement. “We will continue to focus on building innovations for couriers, restaurants, retailers and start-ups that translate into new sources of growth.”

Mejia, Simón Borrero and Felipe Villamarin launched Rappi in 2015, graduating from the Y Combinator startup accelerator the following year. It didn’t take long for the business to capture the attention of American VCs, including the likes of Andreessen Horowitz, DST Global and Sequoia Capital .

The latest round, the largest ever for a Latin American tech startup, brings Rappi’s total raised to date to a whopping $1.2 billion. The company was valued at more than $1 billion last year with a $200 million financing.

Rappi is among few venture-backed “unicorns” based in Latin America. São Paulo-based Nubank, a fast-growing fintech startup, garnered a $4 billion valuation last year with a $180 million investment.

Rappi didn’t immediately respond to a request for comment.

Powered by WPeMatico

Madrid-based micromobility startup Movo has closed a €20 million (~$22.5M) Series A funding round to accelerate international expansion.

The 2017-founded Spanish startup targets cities in its home market and in markets across LatAm, offering last-mile mobility via rentable electric scooters (e-mopeds and e-scooters) plotted on an app map. It’s a subsidiary of local ride-hailing firm Cabify, which provided the seed funding for the startup.

Movo’s Series A round is led by two new investors: Insurance firm Mutua Madrileña, doubtless spying strategic investment potential in helping diversify its business by growing the market for humans to scoot around cities on two wheels — and VC fund Seaya Ventures, an early investor in Cabify.

Both Mutua Madrileña and Seaya Ventures are now taking a seat on Movo’s board.

Commenting on the Series A in a statement, Javier Mira, general director of Mutua Madrileña, said: “The equity investment in Movo reflects Mutua Madrileña’s aspiration to respond to the new mobility needs that are emerging, and to the economic and social changes that are occurring and that are transforming our life habits.”

Movo currently operates in six cities across five countries — Spain, México, Colombia, Perú and Chile.

It first launched an e-moped service in Madrid a year ago, according to a spokeswoman, and has since expanded domestic operations to the southern Spanish coastal city of Malaga, as well as riding into Latin America.

The new funding is mostly pegged for further international expansion, with a plan to expand into new markets in LatAm, including Argentina, Brazil and Uruguay. Movo is targeting operating in a total of 10 countries by the end of 2019.

The Series A will also be used to grow its vehicle fleet in existing markets, it said.

“We are very excited to be able to offer a solution to the problems of mobility in cities, particularly for short distances in areas with high population density,” said CEO Pedro Rivas in a statement. “We are committed to working together with governments to complement mass public transport with these new micromobility alternatives, so that people can get around in a more sustainable and efficient way.”

Commenting on its investment in the Cabify subsidiary, Seaya Ventures’ Beatriz Gonzalez, founder and managing partner, said the fund is “committed to the evolution of mobility towards sustainable alternatives in the world’s major cities.”

“We want to be part of the transport revolution by promoting projects like Cabify and, of course, Movo,” she said in a statement, which seeks to paint micromobility as a solution for urban congestion and poor air quality. “We are motivated to continue to promote companies with which we share this sense of responsibility towards the development and improvement of people’s quality of life.”

Powered by WPeMatico

The San Francisco-based startup Branch International, which makes small personal loans in emerging markets, has raised $170 million and announced a partnership with Visa to offer virtual, pre-paid debit cards to Branch client networks in Africa, South-Asia and Latin America.

Branch — which has 150 employees in San Francisco, Lagos, Nairobi, Mexico City and Mumbai — makes loans starting at $2 to individuals in emerging and frontier markets. The company also uses an algorithmic model to determine credit worthiness, build credit profiles and offer liquidity via mobile phones.

“We’ll use [the money] to deepen existing business in Africa. Later this year we’ll announce high-yield savings accounts…in Africa,” says Branch co-founder and chief executive Matt Flannery.

The $170 million round from Foundation Capital and its new debit card partner, Visa, will support Branch’s international expansion, which could include Brazil and Indonesia, according to Flannery. Branch launched in Mexico and India within the last year. In Africa, it offers its services in Kenya, Nigeria and Tanzania.

A potential Branch customer

The Branch-Visa partnership will allow individuals to obtain virtual Visa accounts with which to create accounts on Branch’s app. This gives Branch larger reach in countries such as Nigeria — Africa’s most populous country with 190 million people — where cards have factored more prominently than mobile money in connecting unbanked and underbanked populations to finance.

Founded in 2015, Branch started operating in Kenya, where mobile money payment products such as Safaricom’s M-Pesa (which does not require a card or bank account to use) have scaled significantly. M-Pesa now has 25 million users, according to sector stats released by the Communications Authority of Kenya. Branch has more than 3 million customers and has processed 13 million loans and disbursed more than $350 million, according to company stats.

Branch has one of the most downloaded fintech apps in Africa, per Google Play app numbers combined for Nigeria and Kenya, according to Flannery.

Already profitable, Branch International expects to reach $100 million in revenues this year, with roughly 70 percent of that generated in Africa, according to Flannery.

In addition to Visa and Foundation Capital, the $170 Series C round included participation from Branch’s existing investors Andreessen Horowitz, Trinity Ventures, Formation 8, the IFC, CreditEase and Victory Park, while adding new investors Greenspring, Foxhaven and B Capital.

Branch last raised $70 million in 2018. The company’s overall VC haul and $100 million revenue peg register as pretty big numbers for a startup focused primarily on Africa. Pan-African e-commerce startup Jumia, which also announced its NYSE IPO last month, generated $140 million in revenue (without profitability) in 2018.

Startups building financial technologies for Africa’s 1.2 billion population have gained the attention of investors. As a sector, fintech (or financial inclusion) attracted 50 percent of the estimated $1.1 billion funding to African startups in 2018, according to Partech.

Startups building financial technologies for Africa’s 1.2 billion population have gained the attention of investors. As a sector, fintech (or financial inclusion) attracted 50 percent of the estimated $1.1 billion funding to African startups in 2018, according to Partech.

Branch’s recent round and plans to add countries internationally also tracks a trend of fintech-related products growing in Africa, then expanding outward. This includes M-Pesa, which generated big numbers in Kenya before operating in 10 countries around the world. Nigerian payments startup Paga announced its pending expansion in Asia and Mexico late last year. And payment services such as Kenya’s SimbaPay have also connected to global networks like China’s WeChat.

Powered by WPeMatico