brazil

Auto Added by WPeMatico

Auto Added by WPeMatico

As we mentioned in part 1 of this EC-1, David Velez had two key co-founding roles he needed to fill to get started building Nubank. For one, he needed a CTO to lead the engineering side of the business, as Velez didn’t have an engineering background.

Edward Wible, an American computer science graduate who spent most of his career in private equity, would take that responsibility. He didn’t bring years of coding experience, but he had qualities that Velez considered more important: A strong belief in the potential of the product and an equally intense commitment to working on it.

Given the occasionally hostile reaction of most incumbent banks to their customers in Brazil, Nubank’s starkly contrasting openness and transparency has garnered a huge following.

That left an even more important role to fill — one that was much harder to define. This other co-founder would need to blend knowledge of the Brazilian market and local savvy with expertise in banking, all while embodying a Silicon Valley ethos of focusing on customers. This person would also have to work in São Paulo for minimal wages out of a small office with just one bathroom, all in the belief that their equity (both stock and sweat) would one day be worth it.

Velez would eventually stumble upon Cristina Junqueira, who was qualified to do all this, and much, much more.

“Once someone said I was the glue of the operation, and that someone else was the brains. And I said, ‘No, I’m the glue and the brains, and I bet my brain is even better than his,”’ Junqueira said.

Junqueira didn’t just lead Nubank’s drive into the Brazilian market, she also upended age-old notions of what it means to be a 21st-century bank. Her inspiration was nothing short of Disney, and her mission was to create a bank as popular as the magical kingdom itself.

A bank. As popular as Disney. Sounds like a fairy tale, frankly.

Unlike her co-founders Velez and Wible, Junqueira grew up in Nubank’s home market of Brazil. The eldest of four sisters, she remembers her parents — both dentists — always assiduously working to maintain their practice.

Their work ethic trickled down, but so did responsibility. As the oldest at home, she was forced to grow up quickly and take on responsibilities from an early age. “I remember being 11 years old and doing grocery shopping for the month,” she said. “I did everything very young.”

Powered by WPeMatico

As we saw in parts 1 and 2 of this EC-1, by mid-2013, Nubank CEO David Velez had most of what he needed to get started. He’d brought on two co-founders, assembled ambitious engineering and operations teams, raised $2 million in seed funding from Sequoia and Kaszek, rented a tiny office in São Paulo, and was armed with a mission to deliver the kind of banking services that customers in a market as large and lucrative as Brazil’s should expect.

Despite being named Nubank, however, the startup couldn’t actually be a bank: Brazil’s laws made it illegal at the time for a foreigner-run company to operate a bank. That restriction required the team to develop an inventive product strategy to find a foothold in the market while they waited for a license directly from the country’s president.

Nubank was so adamant about differentiating itself from other banks that it chose Barney purple for its brand color and first credit card.

Nubank therefore pursued a credit card as its first offering, but it had to race against a clock counting quickly down to zero. At the time, Brazil didn’t have ownership restrictions on this product segment like it did with banking, but new rules were coming into force in just a few months in May 2014 that would block a company like Nubank from launching.

The company needed to execute rapidly over the next eight months if it wanted to be grandfathered into the existing regulations. The speed of operations was frantic to say the least, and the company would go on to work even faster, ultimately propelling itself into the stratosphere of fintech startups.

It’s easy to assume that the name Nubank refers to “new bank,” but that’s not really what the founders were going for. The word “nu” in Portuguese means “naked,” and Velez and his team wanted the name to reflect their vision: To build a 21st-Century bank without any of the shackles imposed by the traditional banks in Brazil.

The team wanted to offer services to as many people as possible, as there is a huge wealth gap in Brazil, where the minimum wage is around $200 a month.

Launching with just a credit card was both a strategic and practical business decision. Credit cards were widely used in the country, and everyone understood how they worked. Additionally, you could only use credit cards to shop online in Brazil, because debit cards weren’t accepted.

Powered by WPeMatico

Nubank’s first office, on California Street in the Brooklin neighborhood of São Paulo, makes for a great beginning to the company’s story. It wasn’t a Silicon Valley garage, but this tiny, one-bathroom rented house, where 30 people worked insane hours to push out the company’s debut credit card, lends just as well to an image of entrepreneurial spirit and drive.

As Nubank continues to make international waves, more and more VC investors are taking a look at the Brazilian ecosystem and could potentially fund other upstarts in the years to come.

But as Nubank’s story continued, the team eventually had to move out of that early office, and the next several offices, too. Eventually Nubank had to relocate to an eight-story building in São Paulo, which houses a large part of the company’s now 3,000-person team.

The startup reached decacorn status in far less than a decade, and it is growing faster than ever. When I interviewed CEO David Velez back in January to discuss Nubank’s $400 million Series G, he said, “We’ve gone from 12 million customers in 2019 to 34 million solely based on word of mouth.” By September last year, the company was onboarding 41,000 new customers per day.

In the five months since our interview, Nubank has managed to rope in a whopping 6 million customers to reach 40 million. It’s now valued at $30 billion.

Nubank’s present day headquarters in São Paulo, Brazil. Image Credits: NELSON ALMEIDA/AFP / Getty Images

Getting there hasn’t been easy. The company’s three co-founders, Velez, Edward Wible and Cristina Junqueira, had to make key strategic decisions about how to scale themselves to retain the company’s lead in the neobanking market. That lead is getting tougher to sustain every day. Nubank’s proliferating offerings and broader geographical remit has painted a massive target on its back, and a wide number of competitors have cropped up to run on the paths it pioneered.

Like most Disney films, a fairy-tale ending seems in order, but it’ll take a few more rotations of the film wheel to get to the ending.

For the co-founding trio, it became increasingly clear that Nubank’s growing scale demanded critical strategic decisions on how to bring order to the company.

By 2018, the company had thousands of employees, millions of customers, and they still didn’t have a head of HR. Growth until then had been somewhat unstructured. According to Junqueira, waiting so long to hire a head of HR was one of their early mistakes, because it stunted their ability to grow. “[Good] people continue to be our biggest bottleneck,” she says.

Powered by WPeMatico

Microsoft will soon launch a dedicated device for game streaming, the company announced today. It’s also working with a number of TV manufacturers to build the Xbox experience right into their internet-connected screens and Microsoft plans to bring cloud gaming to the PC Xbox app later this year, too, with a focus on play-before-you-buy scenarios.

It’s unclear what these new game streaming devices will look like. Microsoft didn’t provide any further details. But chances are we’re talking about either a Chromecast-like streaming stick or a small Apple TV-like box. So far, we also don’t know which TV manufacturers it will partner with.

It’s no secret that Microsoft is bullish about cloud gaming. With Xbox Game Pass Ultimate, it’s already making it possible for its subscribers to play more than 100 console games on Android, streamed from the Azure cloud, for example. In a few weeks, it’ll open cloud gaming in the browser on Edge, Chrome and Safari, to all Xbox Game Pass Ultimate subscribers (it’s currently in limited beta). And it is bringing Game Pass Ultimate to Australia, Brazil, Mexico and Japan later this year, too.

In many ways, Microsoft is unbundling gaming from the hardware — similar to what Google is trying with Stadia (an effort that, so far, has fallen flat for Google) and Amazon with Luna. The major advantage Microsoft has here is a large library of popular games, something that’s mostly missing on competing services, with the exception of Nvidia’s GeForce Now platform — though that one has a different business model since its focus is not on a subscription but on allowing you to play the games you buy in third-party stores like Steam or the Epic store.

What Microsoft clearly wants to do is expand the overall Xbox ecosystem, even if that means it sells fewer dedicated high-powered consoles. The company likens this to the music industry’s transition to cloud-powered services backed by all-you-can-eat subscription models.

“We believe that games, that interactive entertainment, aren’t really about hardware and software. It’s not about pixels. It’s about people. Games bring people together,” said Microsoft’s Xbox head Phil Spencer. “Games build bridges and forge bonds, generating mutual empathy among people all over the world. Joy and community — that’s why we’re here.”

It’s worth noting that Microsoft says it’s not doing away with dedicated hardware, though, and is already working on the next generation of its console hardware — but don’t expect a new Xbox console anytime soon.

Powered by WPeMatico

Just about every week there’s a blockbuster round coming out of South America, but in certain countries such as Ecuador, things have been more hush-hush. However, Kushki, a Quito-based fintech, is bringing attention to the region with today’s announcement of an $86 million Series B and a $600 million valuation.

“We never thought that we would return home [from the U.S.] and build a company that was more valuable in Ecuador than we had built in the U.S.,” said Aron Schwarzkopf, CEO and co-founder of Kushki.

Schwarzkopf and his business partner, Sebastián Castro, previously built and sold a fintech called Leaf in the U.S. in 2014. The two are originally from Ecuador but moved to Boston for college, where they met watching soccer.

Unlike many other fintechs in LatAm that are out to help the unbanked, Kushki works behind the scenes building the tech infrastructure that companies like Nubank use to transfer money. Some of the functionalities they build enable both local and cross-border payment players in credit and debit cards, bank transfers, digital cash, mobile wallets and other alternative payment methods.

“We realized there was a gigantic opportunity to democratize and create infrastructure to move money,” Schwarzkopf told TechCrunch.

The company, which was founded in 2017, already has operations in Mexico, Colombia, Ecuador, Peru and Chile. The Series B will be used to accelerate growth and expand to Brazil and nine other markets in Central America.

Generally, expanding to Brazil is an expensive proposition, and therefore not a path that all companies can take, even though it can be an extremely profitable move if done right. Some of the challenges include the need to translate everything into Portuguese followed by the varying financial regulations.

That’s why Kushki’s approach has to be somewhat custom in each country.

“We focus on going into the markets and we basically rebuild an entire infrastructure, so we put everything into one API,” said Schwarzkopf.

Products similar to Kushki have been successful in other regions around the world, such as in India with Pine Labs, Africa with Flutterwave and Checkout.com, which now has 15 international offices.

To build all this infrastructure, Kushki, which means “cash” in a native Andes dialect, has raised a total of $100 million from SoftBank and an undisclosed global growth equity firm, as well as previous investors including DILA Capital, Kaszek Ventures, Clocktower Ventures and Magma Partners.

“From now until 2060, people will need servers and ways to move money, and we knew that the existing payment infrastructure couldn’t support that,” said Schwarzkopf.

Powered by WPeMatico

Here in the U.S. the concept of using a driver’s data to decide the cost of auto insurance premiums is not a new one.

But in markets like Brazil, the idea is still considered relatively novel. A new startup called Justos claims it will be the first Brazilian insurer to use drivers’ data to reward those who drive safely by offering “fairer” prices.

And now Justos has raised about $2.8 million in a seed round led by Kaszek, one of the largest and most active VC firms in Latin America. Big Bets also participated in the round, along with the CEOs of seven unicorns, including Assaf Wand, CEO and co-founder of Hippo Insurance; David Vélez, founder and CEO of Nubank; Carlos Garcia, founder and CEO of Kavak; Sergio Furio, founder and CEO of Creditas; Patrick Sigrist, founder of iFood and Fritz Lanman, CEO of ClassPass. (There’s a seventh CEO who wishes to remain anonymous). Senior executives from Robinhood, Stripe, Wise, Carta and Capital One also put money in the round.

Serial entrepreneurs Dhaval Chadha, Jorge Soto Moreno and Antonio Molins co-founded Justos, having most recently worked at various Silicon Valley-based companies including ClassPass, Netflix and Airbnb.

“While we have been friends for a while, it was a coincidence that all three of us were thinking about building something new in Latin America,” Chadha said. “We spent two months studying possible paths, talking to people and investors in the United States, Brazil and Mexico, until we came up with the idea of creating an insurance company that can modernize the sector, starting with auto insurance.”

Ultimately, the trio decided that the auto insurance market would be an ideal sector considering that in Brazil, an estimated more than 70% of cars are not insured.

The process to get insurance in the country, by any accounts, is a slow one. It takes up to 72 hours to receive initial coverage and two weeks to receive the final insurance policy. Insurers also take their time in resolving claims related to car damages and loss due to accidents, the entrepreneurs say. They also charge that pricing is often not fair or transparent.

Justos aims to improve the whole auto insurance process in Brazil by measuring the way people drive to help price their insurance policies. Similar to Root here in the U.S., Justos intends to collect users’ data through their mobile phones so that it can “more accurately and assertively price different types of risk.” This way, the startup claims it can offer plans that are up to 30% cheaper than traditional plans, and grant discounts each month, according to the driving patterns of the previous month of each customer.

“We measure how safely people drive using the sensors on their cell phones,” Chadha said. “This allows us to offer cheaper insurance to users who drive well, thereby reducing biases that are inherent in the pricing models used by traditional insurance companies.”

Justos also plans to use artificial intelligence and computerized vision to analyze and process claims more quickly and machine learning for image analysis and to create bots that help accelerate claims processing.

“We are building a design-driven, mobile first and customer experience that aims to revolutionize insurance in Brazil, similar to what Nubank did with banking,” Chadha told TechCrunch. “We will be eliminating any hidden fees, a lot of the small text and insurance-specific jargon that is very confusing for customers.”

Justos will offer its product directly to its customers as well as through distribution channels like banks and brokers.

“By going direct to consumer, we are able to acquire users cheaper than our competitors and give back the savings to our users in the form of cheaper prices,” Chadha said.

Customers will be able to buy insurance through Justos’ app, website or even WhatsApp. For now, the company is only adding potential customers to a waitlist but plans to begin selling policies later this year..

During the pandemic, the auto insurance sector in Brazil declined by 1%, according to Chadha, who believes that indicates “there is latent demand raring to go once things open up again.”

Justos has a social good component as well. Justos intends to cap its profits and give any leftover revenue back to nonprofit organizations.

The company also has an ambitious goal: to help make insurance become universally accessible around the world and the roads safer in general.

“People will face everyday risks with a greater sense of safety and adventure. Road accidents will reduce drastically as a result of incentives for safer driving, and the streets will be safer,” Chadha said. “People, rather than profits, will become the focus of the insurance industry.”

Justos plans to use its new capital to set up operations, such as forming partnerships with reinsurers and an insurance company for fronting, since it is starting as an MGA (managing general agent).

It’s also working on building out its products such as apps, its back end and internal operations tools, as well as designing all its processes for underwriting, claims and finance. Justos’ data science team is also building out its own pricing model.

The startup will be focused on Brazil, with plans to eventually expand within Latin America, then Iberia and Asia.

Kaszek’s Andy Young said his firm was impressed by the team’s previous experience and passion for what they’re building.

“It’s a huge space, ripe for innovation and this is the type of team that can take it to the next level,” Young told TechCrunch. “The team has taken an approach to building an insurance platform that blends being consumer-centric and data-driven to produce something that is not only cheaper and rewards safety but as the brand implies in Portuguese, is fairer.”

Powered by WPeMatico

Fintech and proptech are two sectors that are seeing exploding growth in Latin America, as financial services and real estate are two categories in particular dire need of innovation in a region.

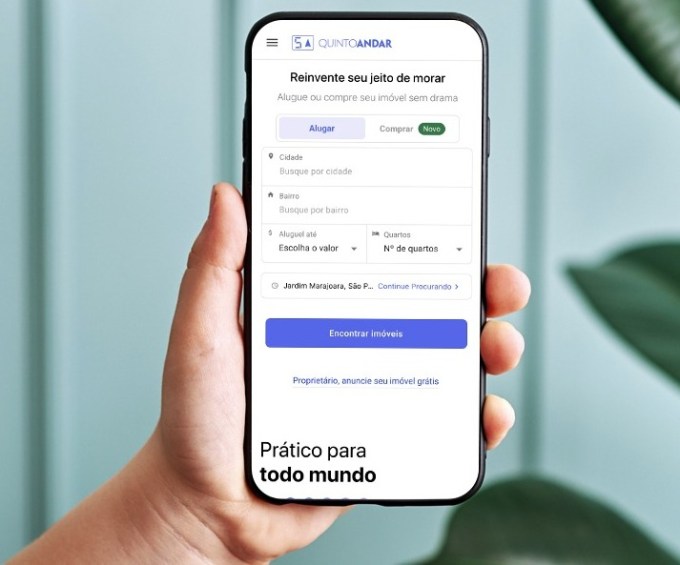

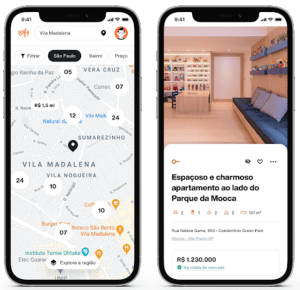

Brazil’s QuintoAndar, which has developed a real estate marketplace focused on rentals and sales, has seen impressive growth in recent years. Today, the São Paulo-based proptech has announced it has closed on $300 million in a Series E round of funding that values it at an impressive $4 billion.

The round is notable for a few reasons. For one, the valuation — high by any standards but especially for a LatAm company — represents an increase of four times from when QuintoAndar raised a $250 million Series D in September 2019.

It’s also noteworthy who is backing the company. Silicon Valley-based Ribbit Capital led its Series E financing, which also included participation from SoftBank’s LatAm-focused Innovation Fund, LTS, Maverik, Alta Park, an undisclosed U.S.-based asset manager fund with over $2 trillion in AUM, Kaszek Ventures, Dragoneer and Accel partner Kevin Efrusy.

Having backed the likes of Coinbase, Robinhood and CreditKarma, Ribbit Capital has historically focused on early-stage investments in the fintech space. Its bet on QuintoAndar represents clear faith in what the company is building, as well as its confidence in the startup’s plans to branch out from its current model into a one-stop real estate shop that also offers mortgage, title, insurance and escrow services.

The latest round brings QuintoAndar’s total raised since its 2013 inception to $635 million.

Ribbit Capital Partner Nick Huber said QuintoAndar has over the years built “a unique and trusted brand in Brazil” for those looking for a place to call home.

“Whether you are looking to buy or to rent, QuintoAndar can support customers through the entire transaction process: from browsing verified inventory to signing the final contracts,” Huber told TechCrunch. “The ability to serve customers’ needs through each phase of life and to do so from start to finish is a unique capability, both in Brazil and around the world.”

QuintoAndar describes itself as an “end-to-end solution for long-term rentals” that, among other things, connects potential tenants to landlords and vice versa. Last year, it expanded also into connecting a home buyers to sellers.

Image Credits: QuintoAndar

TechCrunch spoke with co-founder and CEO Gabriel Braga and he shared details around the growth that has attracted such a bevy of high-profile investors.

Like most other businesses around the world, QuintoAndar braced itself for the worst when the COVID-19 pandemic hit last year — especially considering one core piece of its business is to guarantee rents to the landlords on its platform.

“In the beginning, we were afraid of the implications of the crisis but we were able to honor our commitments,” Braga said. “In retrospect, the pandemic was a big test for our business model and it has validated the strength and defensibility of our business on the credit side and reinforced our value proposition to tenants and landlords. So after the initial scary moments, we actually felt even more confident in the business that we are building.”

QuintoAndar describes itself as “a distant market leader” with more than 100,000 rentals under management and about 10,000 new rentals per month. Its rental platform is live in 40 cities across Brazil, while its home-buying marketplace is live in four. Part of its plans with the new capital is to expand into new markets within Brazil, as well as in Latin America as a whole.

The startup claims that, in less than a year, QuintoAndar managed to aggregate the largest inventory among digital transactional platforms. It now offers more than 60,000 properties for sale across Sao Paulo, Rio de Janeiro, Belho Horizonte and Porto Alegre. To give greater context around the company’s growth of that side of its platform: In its first year of operation, QuintoAndar closed more than 1,000 transactions. It has now surpassed the mark of 8,000 transactions in annualized terms, growing between 50% and 100% quarter over quarter.

As for the rentals side of its business, Braga said QuintoAndar has more than 100,000 rentals under management and is closing about 10,000 new rentals per month. The company is not profitable as it’s focused on growth, although it’s unit economics are particularly favorable in certain markets such as Sao Paulo, which is financing some of its growth in other cities, according to Braga.

Now, the 2,000-person company is looking to begin its global expansion with plans to enter the Mexican market later this year. With that, Braga said QuintoAndar is looking to hire “top-tier” talent from all over.

“We want to invest a lot in our product and tech core,” he said. “So we’re trying to bring in more senior people from abroad, on a global basis.”

CEO Braga and CTO André Penha came up with the idea for QuintoAndar after receiving their MBAs at Stanford University. As many startups do, the company was founded out of Braga’s personal “nightmare” of an experience — in this case, of trying to rent an apartment in Sao Paulo.

The search process, he recalls, was difficult as there was not enough information available online and renters were forced to provide a guarantor, or co-signer, from the same city or pay rent insurance, which Braga described as “very expensive.”

“Overall, I felt it was a very inefficient and fragmented process with no transparency or tech,” Braga told me at the time of the company’s last raise. “There was all this friction and high cost involved, just real tangible problems to solve.”

The concept for QuintoAndar (which can be translated literally to “Fifth Floor” in Portuguese) was born.

“Little by little, we created a platform that consolidated supply and inventory in a uniform way,” Braga said.

The company took the search phase online for the first time, according to Braga. It also eliminated the need for tenants to provide a guarantor, thereby saving them money. On the other side, QuintoAndar also works to help protect the landlord with the guarantee that they will get their rent “on time every month,” Braga said.

It’s been interesting watching the company evolve and grow over time, just as it’s been fascinating seeing the region’s startup scene mature and shine in recent years.

Powered by WPeMatico

Commission-free trading app Stake, which is available in the U.K., Brazil and New Zealand, has raised $30 million from Tiger Global and partners of London-based DST Global to expand into Europe.

Matt Leibowitz, founder and CEO of Stake said: “We’re really excited to get to this point but it’s just the start. We set out to change the game for retail investors and were self-funded for the first four years of our journey. We’ve proven the model and now have the chance to expand our product and bring our zero-brokerage service to more retail investors.”

Since launching in the U.K. in early 2020, Stake claims to have grown its total customer base more than six times over, with 25% month-on-month customer growth on average and hitting over 330,000 customers globally.

It was the first to offer commission-free access to the U.S. market in Australia, offering retail investors access to over 4,400 U.S. stocks & ETFs without a brokerage fee.

In the U.K. it competes with eToro, Libertex, Fineco, Plus500 and IG, among others.

Powered by WPeMatico

It looks like everyone and their mother is trying to reinvent the Brazilian banking system. Earlier this year we wrote about Nubank’s $400 million Series G, last month there was the PicPay IPO filing and today, alt.bank, a Brazilian neobank, announced a $5.5 million Series A led by Union Square Ventures (USV).

It’s no secret that the Brazilian banking system has been poised for disruption, considering the sector’s little attention to customer service and exorbitant fee structure that’s left most Brazilians unbanked, and alt.bank is just the latest company trying to take home a piece of the pie.

Following Nubank’s strategy of launching a bank with colors that are very un-bank-like, signaling that they do things differently, alt.bank similarly launched its first financial product in 2019 — a fluorescent-yellow debit card which the locals have endearingly dubbed, “o amarelinho,” meaning, “the little yellow card.”

The company, founded by serial entrepreneur Brad Liebmann, follows the founder’s $480 million exit of Simply Business, which was acquired by U.S. insurance giant Travelers in 2017.

Unlike many fintechs, alt.bank has a strong social mission and pays commissions for referrals that last for the customer’s lifetime.

“Most fintechs just help wealthy people get wealthier, so I thought let’s do something with a social mission,” Liebmann told TechCrunch in an interview.

To drive home the mission, and really target the unbanked, Liebman and his team of 80 employees have designed an app that can be used by the illiterate. Instead of words, users can follow color-coded prompts to complete a transaction. The company also plans to launch credit products soon.

According to the company, close to a million people have downloaded the android app since launch, but Liebman declined to disclose how many active users the company actually has.

Today, the company’s core offerings include the debit card, a prepaid credit card, Pix (similar to Zelle), a savings account and even telemedicine visits via a partnership with Dr. Consulta, a network of healthcare clinics throughout the country. The prepaid credit card is key because online stores in Brazil don’t accept debit card purchases.

In addition to the perk of ongoing commissions, alt.bank has also partnered with three major drugstores, allowing their users to get 5-30% off any item at the stores, including medication.

While the company is based in São Paulo and São Carlos, Liebmann and his family are currently based in London due to regulations around the pandemic.

The investment in alt.bank marks USV’s first investment in South America, solidifying a trend by other major U.S. investors such as Sequoia who only in the last several years have started looking to LatAm for deals.

“The bar was high for our first investment in South America,” said Union Square Ventures partner John Buttrick. “The combination of the alt.bank business model and world-class management team enticed us to expand our geographic focus to help build the leading digital bank targeting the 100 million Brazilians who are currently being neglected by traditional lenders,” he added in a statement.

Powered by WPeMatico

Nearly exactly one month ago, digital real estate platform Loft announced it had closed on $425 million in Series D funding led by New York-based D1 Capital Partners. The round included participation from a mix of new and existing investors such as DST, Tiger Global, Andreessen Horowitz, Fifth Wall and QED, among many others.

At the time, Loft was valued at $2.2 billion, a huge jump from its being just near unicorn territory in January 2020. The round marked one of the largest ever for a Brazilian startup.

Now, today, São Paulo-based Loft has announced an extension to that round with the closing of $100 million in additional funding that values the company at $2.9 billion. This means that the 3-year-old startup has increased its valuation by $700 million in a matter of weeks.

Baillie Gifford led the Series D-2 round, which also included participation from Tarsadia, Flight Deck, Caffeinated and others. Individuals also put money in the extension, including the founders of Better (Zach Frenkel), GoPuff, Instacart, Kavak and Sweetgreen.

Loft has seen great success in its efforts to serve as a “one-stop shop” for Brazilians to help them manage the home buying and selling process.

Image Credits: Loft

In 2020, Loft saw the number of listings on its site increase “10 to 15 times,” according to co-founder and co-CEO Mate Pencz. Today, the company actively maintains more than 13,000 property listings in approximately 130 regions across São Paulo and Rio de Janeiro, partnering with more than 30,000 brokers. Not only are more people open to transacting digitally, more people are looking to buy versus rent in the country.

“We did more than 6x YoY growth with many thousands of transactions over the course of 2020,” Pencz told TechCrunch at the time of the company’s last raise. “We’re now growing into the many tens of thousands, and soon hundreds of thousands, of active listings.”

The decision to raise more capital so soon was due to a variety of factors. For one, Loft has received “overwhelming investor interest” even after “a very, very oversubscribed main round,” Pencz said.

“We have seen a continued acceleration in our market share growth, especially in São Paulo and Rio de Janeiro, the two markets we currently operate in,” he added. “We saw an opportunity to grow even faster with additional capital.”

Pencz also pointed out that Baillie Gifford has relatively large minimum check size requirements, which led to the extension being conducted at a higher price and increased the total round size “by quite a bit to be able to accommodate them.”

While the company was less forthcoming about its financials as of late, it told me last year that it had notched “over $150 million in annualized revenues in its first full year of operation” via more than 1,000 transactions.

The company’s revenues and GMV (gross merchandise value) “increased significantly” in 2020, according to Pencz, who declined to provide more specifics. He did say those figures are “multiples higher from where they were,” and that Loft has “a very clear horizon to profitability.”

Pencz and Florian Hagenbuch founded Loft in early 2018 and today serve as its co-CEOs. The aim of the platform, in the company’s words, is “bringing Latin American real estate into the e-commerce age by developing online alternatives to analogue legacy processes and leveraging data to create transparency in highly opaque markets.” The U.S. real estate tech company with the closest model to Loft’s is probably Zillow, according to Pencz.

In the United States, prospective buyers and sellers have the benefit of MLSs, which in the words of the National Association of Realtors, are private databases that are created, maintained and paid for by real estate professionals to help their clients buy and sell property. Loft itself spent years and many dollars in creating its own such databases for the Brazilian market. Besides helping people buy and sell homes, it offers services around insurance, renovations and rentals.

In 2020, Loft also entered the mortgage business by acquiring one of the largest mortgage brokerage businesses in Brazil. The startup now ranks among the top-three mortgage originators in the country, according to Pencz. When it comes to helping people apply for mortgages, he likened Loft to U.S.-based Better.com.

This latest financing brings Loft’s total funding raised to an impressive $800 million. Other backers include Brazil’s Canary and a group of high-profile angel investors such as Max Levchin of Affirm and PayPal, Palantir co-founder Joe Lonsdale, Instagram co-founder Mike Krieger and David Vélez, CEO and founder of Brazilian fintech Nubank. In addition, Loft has also raised more than $100 million in debt financing through a series of publicly listed real estate funds.

Loft plans to use its new capital in part to expand across Brazil and eventually in Latin America and beyond. The company is also planning to explore more M&A opportunities.

This article was updated post-publication to reflect accurate investor information.

Powered by WPeMatico