blockchain

Auto Added by WPeMatico

Auto Added by WPeMatico

The blockchain is in the middle of a major hype cycle at the moment, and that makes it hard for many people to take it seriously, but if you look at the core digital ledger technology, there is tremendous potential to change the way we think about trust in business. Yet these are still extremely early days and there are a number of missing pieces that need to be in place for the blockchain to really take off in the enterprise.

Suffice it to say that it has caught the fancy of major enterprise vendors with the likes of SAP, IBM, Oracle, Microsoft and Amazon all looking at providing some level of Blockchain as a service for customers.

While the level of interest in blockchain remains fluid, a July 2017 survey of 400 large companies by UK firm Juniper Research found 6 in 10 respondents were “either actively considering, or are in the process of, deploying blockchain technology.”

In spite of the growing interest we have seen over the last 12-18 months, blockchain lacks some basic underlying system plumbing, the kind any platform needs to thrive in an enterprise setting. Granted, some companies and the open source community are recognizing this as an opportunity and trying to build it, but many challenges remain.

Even though the blockchain clearly has many possible use cases, some people still have trouble separating it from its digital currency roots, and Joshua McKenty, who helped develop Open Stack while working at NASA and now is head of Cloud Foundry at Pivotal, sees this as a real problem, one that could hold back the progress of blockchain as an enterprise technology.

He believes that right now bitcoin and blockchain are akin to Napster and peer to peer (P2P) technology in the late 90s. When Napster made it easy to share MP3 files illegally on a P2P network, McKenty believes, it set back business usage of P2P for a decade because of the bad connotations associated with the popular use case.

“You couldn’t talk about Napster [and P2P] and have it be a positive conversation. Bitcoin has done that to blockchain. It will take us time to recover what bitcoin has done to get to something that is really useful [with blockchain],” he said.

Photo by Spencer Platt/Newsmakers – Getty Images

A recent survey by Deloitte of over 1000 participants in 7 countries found that outside the US in particular this perception held true. “When asked if they believed that blockchain was just “a database for money” with little application outside of financial services, just 18 percent of US respondents agreed with that statement versus 61 percent of respondents in France and the United Kingdom,” the report stated.

Richie Etwaru, founder and CEO at Hu-manity and author of the book, Blockchain Trust Companies sees it as a matter of trust. Companies aren’t used to dealing from a position of trust. In fact, his book argues that the entire contract system exists because of a total lack of it.

“The hurdle [to widespread blockchain adoption in the enterprise] is that those who have traditionally designed or transformed business models in large enterprise settings have systematically and habitually treated trust and transparency as second, sometimes third level characteristics of a business model. The raw material needed are the willingness and executive level alignment and harmonization around the notion that trust and transparency are the next differentiators,” Etwaru explained.

Blockchain was originally created as a system to track bitcoin (digital currency) ownership, and it’s still used extensively for that purpose, but a trusted and immutable record has great utility to track virtually anything of value and enforce a set of rules. We have seen companies like po.et trying to use it to enforce content ownership, Hu-manity, which wants to enforce data ownership, and the IBM TrustChain consortium to track the provenance of diamonds from mine to store.

Photo: LeoWolfert/Getty Images

Rob May, who is CEO at Talla and whose company helped launch a blockchain called BotChain to track the authenticity of bots, says finding good use cases could help ultimately determine the technology’s success or failure. “Blockchain has a bunch of different use cases, and they are usually either all lumped together or poorly understood separately,” May said.

He believes that in many instances today, companies don’t understand the advantages of blockchain, which he identifies as immutability, trust and tokenization, the latter of which can help finance blockchain initiatives (but which can also contribute to confusion with digital currency use cases).

“Right now, businesses are missing real blockchain opportunities and instead throwing blockchain in places where it doesn’t belong. For example, they are trying to use it for smart contracts, and that stuff isn’t ready. They also try to use it for cases that require a lot of speed, and again blockchains aren’t ready,” he said.

Finally, he says, if you don’t require immutability, trust and tokenization, you might want to consider a different approach other than blockchain.

Like any network, identity will be at the core of any blockchain network because it is imperative that you understand whom you are communicating with. Charles Francis, a senior analyst at Accenture says for now blockchains will remain private for the most part, but authentication will become increasingly important as we eventually have blockchain-to-blockchain communications.

Photo: NicoElNino/Getty Images

“Initially blockchain-to-blockchain connections will be manually set up and you will manage your network in a private model and bad actors will be immediately obvious,” he explained. But he believes that we will require a system in place to ensure we are authentically who we say we are as we move beyond private networks.

Jerry Cuomo, IBM Fellow and VP of Blockchain says that there will come a time when there are multiple networks and we will need to set up systems for them to communicate. “There won’t be one blockchain network to rule them all. It’s a very safe bet. Once you make that statement, these systems need to work together,” he said. “All [the different pieces of networks] need identity and the identity better play across networks. My identity on one network better be the same on another network,” he explained.

For Etwaru it comes back to trust, and a trusted identity would be a natural extension of that. “Transformational blockchain use cases require a network of trading partners to start to operate in a more trusted and transparent way, not just one individual,” he said.

All this said, there is still a steady march toward adoption in the enterprise. As Talla’s May says, there may be open questions, but that just represents a big opportunity for smart companies. “If you are interacting with a network instead of a single company, whose throat do you choke when something goes wrong? I think you will see many companies in the blockchain space do what Red Hat did for Linux. Enterprises need consulting help and better frameworks to think about how [blockchain] networks will work, since Ethereum isn’t a product per se in the traditional sense,” he said.

Gil Perez, SVP for products and innovation, as well as head of digital customer initiatives at SAP says he’s seeing companies with real projects in production. “It is beyond just wanting to do something. We’re doing large scale implementations and pilots. For example, we did one in the pharmaceutical industry with over a billion transactions,” he said.

In fact, SAP has a total of 65 companies working on various projects at different stages of progress at the moment. Perez says the next level of adoption will require a way to involve multiple parties, not just a single company, as with a supply chain example, which involves moving goods and paperwork across multiple countries involving many individuals.

Photo: allanswart

He also points out the importance of making sure there is good data because ultimately, if you have bad data in an immutable record, that is going to be a serious problem. That requires the companies involved to come together and agree to a common system to enter and agree upon each piece of information that moves through the system and that is a work in progress.

May sees blockchain technology transforming the way we do business in the future and providing a more standard way of interacting than today’s hodgepodge of vendor approaches.

“Now that blockchain is here, what if we could launch a standard and have shared marketplace by all apps in a space? So as a developer, you write your [application] add-on one time and it works with any [similar application] that supports that standard, and they share one giant marketplace. But how do you get them to share a marketplace? Blockchain and tokens provide decentralization and incentives such that, if you set the right rules, maybe you could do it. That could be transformational,” he said.

As with any new technology, the more it scales the more the tools and adjacent technologies are required. We are still in the early stages of discovering what those are, and before the technology can take off in a big way, we will need more underlying infrastructure in place. If that happens, blockchain could be just as transformational as May suggests.

Powered by WPeMatico

Another day, another blockchain project. This time sources are reporting that Knotel – an office space rental service in Manhattan – has acquired 42Floors, a commercial real estate search engine in order to, according to founder Amol Sarva, get “access to data and technology on over 10 billion square feet of office space, driving further liquidity to Knotel’s marketplace while also accelerating its plans for a blockchain platform.”

The deal is not yet complete.

Knotel is building the Agile HQ platform, a way to rent office space for a few hours or a few months without getting stuck in a lease. The company has 1 million square feet of space in New York, San Francisco, London, and Berlin and it raised $100 million in funding. The company claims it has more has more buildings in New York than WeWork.

“42Floors built a powerful tool to organize a dark market that hasn’t changed in a hundred years,” said Amol Sarva, CEO of Knotel. “It’s still backroom and bilateral while the rest of the world is becoming digital and standardized. This is what leads to transactions that take months to close with a dozen middlemen – no reliable information. You can buy a house faster than you can rent a floor. Partnering together will help give owners and customers what they both want: truth.”

The reported 42Floors acquisition enables the company to bring new properties onto its platform and could let non-blockchain-based contracts move to the blockchain.

UPDATE – Text changed to reflect the type of business and ICO plans.

Powered by WPeMatico

Imagine a world where you could sell your medical information to a drug company on your terms for a specific purpose like a drug trial. Then imagine you could restrict the company from using that data for anything else, including selling it to other medical data brokers, and enforcing those ownership rules on the blockchain.

That’s what Hu-manity.co, a data ownership startup wants to do and they are putting the pieces in place to create a data marketplace. This is not an easy problem to solve, but co-founder and CEO Richie Etwaru, sees it as a crucial cultural shift in how we treat data.

Etwaru, who wrote a book on using the blockchain and smart contracts in a business context called Blockchain Trust Companies, sees the blockchain as just a small piece of a much broader solution. It can provide a rules engine and enforcement mechanism, but he doesn’t see this as the gist of the company at all.

For Etwaru and Hu-manity it’s about viewing your data as your property, and giving you legal control of it. “We’re starting with the idea that your data is your digital property, and we are allowing you to have the equivalent of a title, like you have for your car,” he explained.

You may be wondering how they can bring this notion to business, which after all has been allowed to use your data for some time without your explicit permission, never mind pay you for it under a set of specific contractual terms. To achieve that, Hu-manity wants to create large pools of users that would make it attractive to the data buyers.

“We are pooling large communities together to be able to notify corporations that don’t respect digital data streams of property, because they take a very business centric view of regulations to opt out, then invite them back into a property centric view of data within the new terms and conditions defined by the marketplace,” he said.

They are starting with health data because Etwaru says that this data is often sold for medical studies, whether you know it or not — albeit with PII removed. The other thing besides market pressure, which could drive companies like big pharma to make contracts with individuals to buy their data, is that they get much better data when they understand the whole patient. Even if they could figure out who the patient is, and it’s becoming increasingly possible with digital fingerprinting, they are legally prohibited from contacting an individual to correct the record or to get a better understanding of their history.

Hu-manity plays a couple of roles here according to Etwaru, For starters, they are attaching a traceable title number to the data. Then they plan to set up the marketplace and help put the seller and buyer together, all the while providing a track and trace mechanism that allows the data owner to ensure their data is being used in a way they wish. In that sense, they are acting as a broker between buyer and seller.

Interestingly, Etwaru admits there is no set market value for this data, at least as of yet, although he believes an individual’s medical data sets could sell for between $200-$400. For now, the company is working with a group of economists to determine the best way to approach pricing. He doesn’t believe it’s a good idea for individuals to negotiate their own terms, and that we should let these market cooperatives determine the value. His company will take 25 percent of the selling price as a brokerage fee, regardless of how it ultimately works.

The company was founded last spring and has raised $5.5 million on a $50 million valuation. There are many issues to work out before that happens, and many ways to stumble along the way, but the company has a compelling vision and it will be interesting to see if it can pull this together and gain market traction.

Powered by WPeMatico

Centralized crypto exchanges like Coinbase are easy but expensive because they introduce a middleman. Not-for-profit project 0x allows any developer to quickly build their own decentralized cryptocurrency exchange and decide their own fees. It acts like Craigslist, connecting traders without ever holding the tokens itself. And instead of having to bootstrap their way to enough users trading tokens on their app alone so that there’s liquidity, 0x offers cross-platform liquidity between users on the different projects it powers.

The problem is the user experience of decentralized apps is often crappy compared to the consumer apps we’re used to across the rest of tech. From sign-in to recovering accounts to conducting transactions, it’s a lot more complicated than Facebook Login, PayPal, or Shopify. Bitcoin and Ethereum prices remain well below half their peaks because it’s difficult to do much with cryptocurrency right now. Until the decentralized infrastructure improves, the dreams of how blockchains can improve the world remain distant.

0x is trying to fix that by ensuring developers all don’t have to reinvent the exchange wheel.

It began as a for-profit exchange before the team recognized the massive usability gap. So instead it became a decentralized exchange protocol, and raised $24 million in an ICO for its ZRX token. That’s how relayers — the apps who use it to build exchanges for ERC20 tokens atop the Ethereum blockchain — can charge fees. It also gives those who collect the most a say in the governance of the protocol.

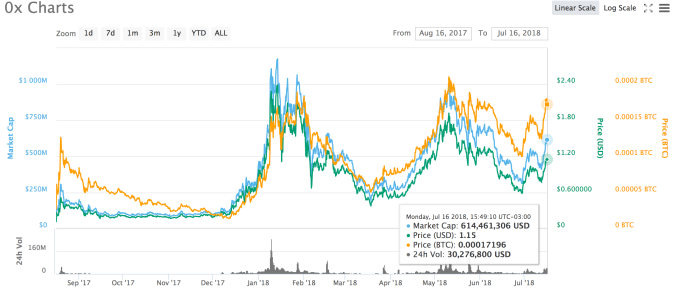

Some of the top projects on 0x like Augur and Dydx are going strong. Last week Coinbase announced it was exploring whether it might list ZRX and several other currencies for trade on its exchange, helping perk up the price after declines since the new year.

0x’s ZRX token price, via CoinMarketCap

Now 0x is putting some of its $24 million to work. It just hired former Facebook designer Chris Kalani to help it improve the usability of its APIs and the products built on top of them. His skills helped Facebook embrace mobile around its 2012 IPO. He then built Wake, raising $3.8 million for the design prototype sharing tool that let teams get instant feedback on their works-in-progress. Kalani sold Wake to design platform InVision in April, and after a few months assisting the transition, he’s joined 0x.

“There are very few designers involved in the [blockchain] space” Kalani tells me. “There’s not a lot of people who had worked on anything at a large-scale or from the consumer perspective. We’re focused on making crypto more approachable.”

After talking to four leaders in different parts of the blockchain industry, the consensus was that 0x was an elegant protocol for spawning decentralized exchanges. But the question kept coming up about whether the project will be sustainable. The company doesn’t have to earn enormous amounts of revenue, but concerns about its longevity could scare away developers. One, who asked to remain anonymous, described 0x saying, “the best analogy is trying to monetize Linux.”

After talking to four leaders in different parts of the blockchain industry, the consensus was that 0x was an elegant protocol for spawning decentralized exchanges. But the question kept coming up about whether the project will be sustainable. The company doesn’t have to earn enormous amounts of revenue, but concerns about its longevity could scare away developers. One, who asked to remain anonymous, described 0x saying, “the best analogy is trying to monetize Linux.”

0x is open source, so it could be forked so developers can sidestep ZRX. 0x hopes that the shared liquidity feature will keep developers in line. It only works with the unforked version, and is now being used by 0x-powered projects, including Radar Relay, ERC dEX, Shark Relay, Bamboo Relay and LedgerDex.

While some centralized exchanges have suffered security troubles and hacks, those with stronger records like Coinbase continue to thrive while banking off high fees. That in turn lets them offer better liquidity and invest more in the user experience, widening the gap versus decentralized apps. “People trust Coinbase with large amounts of capital but they wouldn’t trust themselves,” Kalani admits. But he thinks it’s early in the game, and as users become more knowledgeable and comfortable with holding their own tokens for use on decentralized exchanges, 0x and ZRX will thrive.

There’s also competition within the decentralized exchange space from Kyber’s liquidity network, and AirSwap’s peer-to-peer exchange marketplace. But for any of these to thrive, the mainstream crypto owner will have to get better educated. That could fall to 0x.

One alternative path for the not-for-profit would be selling developer services and consulting to those building on top of it. Or it could always do another ICO. But for now, there are a lot of projects out there that don’t want to foot the upfront cost to build their own secure and compliant exchange from scratch. Kalani concludes, “The way Stripe allowed developers and businesses to build on top of it, and not have to worry about regulatory issues and all the infrastructure necessary to take payments, I think 0x is going to do something similar with exchanges for crypto.”

Powered by WPeMatico

The team at Dirt Protocol is using blockchain technology to create a new approach to verify information.

The startup doesn’t plan to launch its platform until later this year, but it announced today that it has raised $3 million in seed funding from General Catalyst, Greylock, Lightspeed, Pantera Capital, Digital Currency Group, SV Angel, Avichal Garg, Elad Gil, Fred Ehrsam, Linda Xi and others.

Founder Yin Wu previously created lockscreen startup Echo (acquired by Microsoft in 2015) and laundry startup Prim. She told me that after becoming interested in the cryptocurrency industry, she was concerned about the fear, uncertainty and doubt around coin offerings — after all, we’ve covered several ICOs where companies appear to have disappeared with people’s money.

“The market today is still unregulated, with high incentive for people to spread misinformation for personal gain,” Wu said.

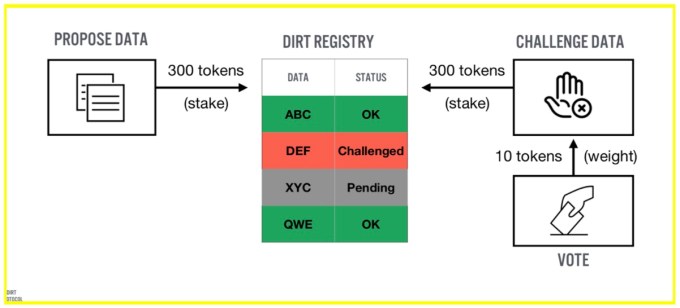

Her solution? Build databases where anyone can contribute information, but where they have “skin in the game,” so there’s a financial penalty if they’re not truthful.

Dirt Protocol isn’t trying to create a single, definitive data repository, but rather to provide the tools for developers to build their own databases. Those databases might focus on things like ICOs (providing information like the team, the investors and the number of tokens in circulation), or online publishers (to help advertisers avoid bots), or professional listings and membership lists.

There will be a single token that works across the Dirt platform. Users will need to stake tokens to add new information to databases, to challenge an entry or to vote in disputes — you’ll be penalized (by losing tokens) for adding misinformation and rewarded for weeding it out.

While that should create an economic incentive for people to not just avoid inaccuracies but also to actively remove them, it doesn’t fully address the question of determining the truth — who, ultimately, gets to decide whether an entry is accurate? Wu said Dirt will support a variety of different “governance structures,” whether that’s centralized moderation, free-for-all voting or a system where votes are weighted by reputation.

Wu also suggested that the system is designed in a way to discourage concerted misinformation campaigns. For one thing, hoaxers will probably want to target the more popular databases, but those are also the ones that should attract more active moderation. Plus, she said, “The more valuable the network, the more people are contributing information, the more expensive [it becomes to contribute].”

A recurring theme in our conversation was the advantage of a “decentralized” approach to data verification. Wu said that isn’t always the right way to go, but she said it makes sense when there’s a big platform with a centralized vetting process that works too slowly, or in situations where “you can’t trust the curator” of information, or with data sets that are just proprietary and expensive to access — while you have to buy tokens to contribute information, Wu said that Dirt Protocol data sets should be freely accessible, and “no single party owns that information and can shut off access.”

In a similar vein, she said Dirt Protocol isn’t currently focused on making money. Ultimately, the business model will probably involve some combination of giving the software away for free and charging for additional services.

“We’re focused on creating this open data set that anyone can use,” Wu said. “If we achieve that goal, I’m confident that some monetization will arise.”

Powered by WPeMatico

HTC isn’t gone just yet. Granted, it’s closer than it’s ever been before, with a headcount of fewer than 5,000 employees worldwide — that’s down from 19,000 in 2013. But in spite of those “market competition, product mix, pricing, and recognized inventory write-downs,” the company’s still trucking on.

And while its claim to being “the leading innovator in smart phone devices,” is up for debate, the Taiwanese manufacturer has never shied away from a compelling gimmick. Announced earlier this year, the Exodus definitely fits the bill. The “world’s first major blockchain phone” is still shrouded in mystery, though the company did reveal a couple of key details this week at RISE in Hong Kong intended to keep folks interested while it irons out the rest of the product’s hiccups.

Chief among the reveals is an admittedly nebulous release date of Q3 this year. It’s hardly specific, but it does make the phone a little bit more real — unlike the images, which are still limited to the above blueprint picture at press time.

Here’s a quote from the company’s chief crypto officer, a position that really exists.

In the new internet age people are generally more conscious about their data, this a perfect opportunity to empower the user to start owning their digital identity. The Exodus is a great place to start because the phone is the most personal device, and it is also the place where all your data originates from. I’m excited about the opportunity it brings to decentralize the internet and reshape it for the modern user.

Prior to the launch, the company is partnering with the popular blockchain title, CryptoKitties. The game will be available on a small selection of the company’s handsets starting with the U12+. “This is a significant first step in creating a platform and distribution channel for creatives who make unique digital goods,” the company writes in a release tied to the news. “Mobile is the most prevalent device in the history of humankind and for digital assets and dapps to reach their potential, mobile will need to be the main point of distribution. The partnership with Cryptokitties is the beginning of a non fungible, collectible marketplace and crypto gaming app store.”

The company says the partnership marks the beginning of a “platform and distribution channel for creatives who make unique digital goods.” In other words, it’s attempting to reintroduce the concept of scarcity through these decentralized apps. HTC will also be partnering with Bitmark to help accomplish this.

If HTC is looking for the next mainstream play to right the ship, this is emphatically not it. That said, it could be compelling enough to gain some adoption among those heavily invested enough in the crypto space to pick up a handset built around the technology.

HTC promises more information on the device in “the coming months.”

Powered by WPeMatico

What a day. Yesterday, hundreds of people gathered in Zug, Switzerland for TechCrunch Sessions: Blockchain. In addition to some of the key people of the Ethereum Foundation, the team interviewed the entrepreneurs behind Binance, Coinbase, ConsenSys, CryptoKitties and many other organizations.

The event was packed with interesting content. But if you couldn’t be there in person, don’t worry as you can watch everything that happened in Zug:

Disclosure: I own small amounts of various cryptocurrencies.

Powered by WPeMatico

The Securities and Exchange Commission, the federal agency responsible for protecting investors and maintaining fair and orderly functioning of our securities markets, has 11 regional offices, including in Miami, New York, Boston and Chicago.

None has quite the workload as the SEC’s San Francisco regional office, where a major area of focus in recent years has been investor fraud in pre-IPO companies, particularly the many startups that in an earlier era would have either have gone public or else out of business, but which today linger as privately held outfits because there’s so much money sloshing around.

Among the companies to find themselves in the SEC’s sights in recent years is HR software outfit Zenefits and its founder, Parker Conrad; they were fined $1 million last October as part of a settlement over charges that they’d misled investors. In March, the online personal finance company Credit Karma also settled SEC charges; it had been accused of unlawfully offering securities to its employees — then failing to provide them with timely financial statements and risk disclosures.

Of course, the best-known SEC case to date has centered on the blood-testing company Theranos, which was charged with massive fraud in March, along with the company’s founder, Elizabeth Holmes, and its former president, Sunny Balwani.

Leading the charge in each of these cases and many more: Jina Choi, a graduate of Oberlin and Yale Law School who worked as a lawyer for the Justice Department in Washington before heading to San Francisco and the SEC’s enforcement division in 2000.

Five years ago, Choi was promoted to director of that office, where she has since overseen enforcement and examinations in Northern California and the Pacific Northwest, despite critics who believe the SEC should keep its eye on public companies alone. (“If no one is policing private markets, that’s a problem,” Choi said at a public forum in May.)

In an age of initial coin offerings, cryptocurrencies and mushrooming numbers of blockchain-related projects, Choi and her colleagues have their hands particularly full, so you can imagine how excited we are that Choi is coming to Disrupt to discuss some of those challenges, as well as the agency’s victories. We’re also looking forward to learning more about how decisions are made in Choi’s office and back in Washington.

If you’re interested in learning more about the SEC’s ever-evolving approach to Silicon Valley startups — and why you shouldn’t expect its interest to dissipate any time soon — you really won’t want to miss this conversation.

You can buy tickets to the show, taking place in San Francisco September 5th through September 7th, right here.

Powered by WPeMatico

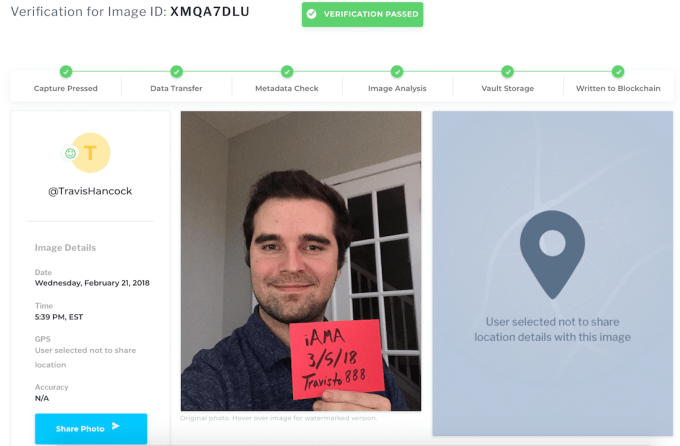

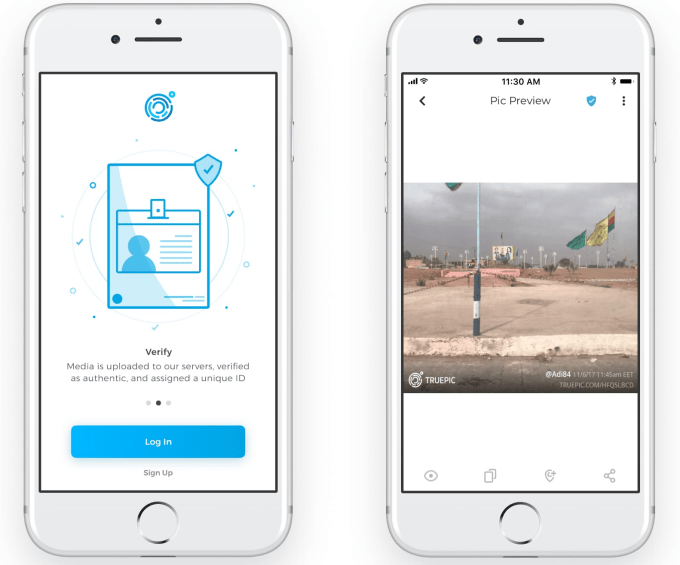

How can you be sure an image wasn’t Photoshopped? Make sure it was shot with Truepic. This startup makes a camera feature that shoots photos and adds a watermark URL leading to a copy of the image it saves, so viewers can compare them to ensure the version they’re seeing hasn’t been altered.

Now Truepic’s technology is getting its most important deployment yet as the way Reddit will verify that Ask Me Anything Q&As are being conducted live by the actual person advertised — oftentimes a celebrity.

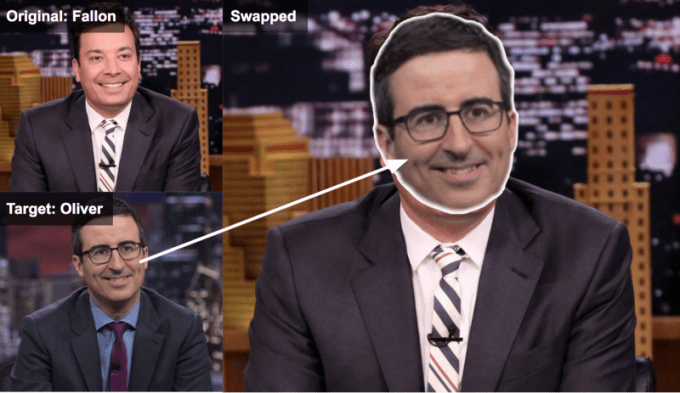

But beyond its utility for verifying AMAs, dating profiles and peer-to-peer e-commerce listings, Truepic is tackling its biggest challenge yet: identifying artificial intelligence-generated Deepfakes. These are where AI convincingly replaces the face of a person in a video with someone else’s. Right now the technology is being used to create fake pornography combining an adult film star’s body with an innocent celebrity’s face without their consent. But the big concern is that it could be used to impersonate politicians and make them appear to say or do things they haven’t.

The need for ways to weed out Deepfakes has attracted a new $8 million round for Truepic. The cash comes from untraditional startup investors, including Dowling Capital Partners, former Thomson Financial (which become Reuters) CEO Jeffrey Parker, Harvard Business school professor William Sahlman and more. The Series A brings Truepic to $10.5 million in funding.

“We started Truepic long before manipulated images impacted democratic elections across the globe, digital evidence of atrocities and human rights abuses were regularly undermined, or online identities were fabricated to advance political agendas — but now we fully recognize its impact on society,” says Truepic founder and COO Craig Stack. “The world needs the Truepic technology to help right the wrongs that have been created by the abuse of digital imagery.”

Here’s how Truepic works:

For example, Reddit’s own Wiki recommends that AMA creators use the Truepic app to snap a photo of them holding a handwritten sign with their name and the date on it. “Truepic’s technology allows us to quickly and safely verify the identity and claims for some of our most eccentric guests,” says Reddit AMA moderator and Lynch LLP intellectual property attorney Brian Lynch. “Truepic is a perfect tool for the ever-evolving geography of privacy laws and social constructs across the internet.”

The abuses of image manipulation are evolving, too. Deepfakes could embarrass celebrities… or start a war. “We will be investing in offline image and video analysis and already have identified some subtle forensic techniques we can use to detect forgeries like deepfakes,” Truepic CEO Jeff McGregor tells me. “In particular, one can analyze hair, ears, reflectivity of eyes and other details that are nearly impossible to render true-to-life across the thousands of frames of a typical video. Identifying even a few frames that are fake is enough to declare a video fake.”

This will always be a cat and mouse game, but from newsrooms to video platforms, Truepic’s technology could keep content creators honest. The startup has also begun partnering with NGOs like the Syrian American Medical Society to help it deliver verified documentation of atrocities in the country’s conflict zone. The Human Rights Foundation also trained humanitarian leaders on how to use Truepic at the 2018 Freedom Forum in Oslo.

Throwing shade at Facebook, McGregor concludes that “The internet has quickly become a dumpster fire of disinformation. Fraudsters have taken full advantage of unsuspecting consumers and social platforms facilitate the swift spread of false narratives, leaving over 3.2 billion people on the internet to make self-determinations over what’s trustworthy vs. fake online… we intend to fix that by bringing a layer of trust back to the internet.”

Powered by WPeMatico

SAP announced today at its Sapphire customer conference it was making the SAP Leonardo Blockchain service generally available. The latter is a cloud service to help companies build applications based on digital ledger-style technology.

Gil Perez, senior vice president for product and innovation and head of digital customer initiatives at SAP, says most of the customers he talks to are still very early in the proof of concept stage, but not so early that SAP doesn’t want to provide a service to help move them along the maturity curve.

“We are announcing the general availability of the SAP Cloud Platform Blockchain Services.” This is a generalized service on top of which customers can begin building their blockchain projects. He says SAP is taking an agnostic approach to the underlying ledger technology whether it’s the open source Hyperledger project, where SAP is a platinum sponsor, MultiChain or any additional blockchain or decentralized distributed ledger technologies.

Perez said part of the reason for this flexibility is that blockchain technology is really still being defined and SAP doesn’t want to commit to any underlying ledger approach until the market decides which way to go. He says this should allow them to minimize the impact on customers as the technology evolves.

They join other enterprise companies like Oracle, IBM, Microsoft and Amazon who have previously released blockchains services for their customers. For SAP, which many companies use for the back-office management of everything from finance to logistics, the blockchain could present some interesting use cases for its customers such as supply chain management.

In this case, the blockchain could help reduce paperwork, bring products to market more quickly and provide an easy audit trail. Instead of requesting a scanned copy of a signed document, you could simply click on a node on the blockchain and see the approval (or denial) and follow the products through the shipping process to the marketplace.

But Perez stresses that just because it’s early doesn’t mean they aren’t working on some pretty substantial projects. He cited one with a pharmaceutical company to ensure the provenance of drugs that involved over a billion transactions already.

SAP is simply trying to keep up with what customers want. Prior to the GA announced today, the company conducted a survey of 250 customers and found, that although it was early days, there is enterprise interest in exploring blockchain technology. Whether this initiative can expand into a broader business is hard to say, but SAP sees blockchain as logical adjacent technology to their core offerings.

Powered by WPeMatico