blockchain

Auto Added by WPeMatico

Auto Added by WPeMatico

A year ago I felt a panic that still reverberates in me today. Hackers swapped my T-Mobile SIM card without my approval and methodically shut down access to most of my accounts and began reaching out to my Facebook friends asking to borrow crypto. Their social engineering tactics, to be clear, were laughable but they could have been catastrophic if my friends were less savvy.

Flash forward a year and the same thing happened to me again – my LTE coverage winked out at about 9pm and it appeared that my phone was disconnected from the network. Panicked, I rushed to my computer to try to salvage everything I could before more damage occurred. It was a false alarm but my pulse went up and I broke out in a cold sweat. I had dealt with this once before and didn’t want to deal with it again.

Sadly, I probably will. And you will, too. The SIM card swap hack is still alive and well and points to one and only one solution: keeping your crypto (and almost your entire life) offline.

Stories about massive SIM-based hacks are all over. Most recently a crypto PR rep and investor, Michael Terpin, lost $24 million to hackers who swapped his AT&T SIM. Terpin is suing the carrier for $224 million. This move, which could set a frightening precedent for carriers, accuses AT&T of “fraud and gross negligence.”

From Krebs:

Terpin alleges that on January 7, 2018, someone requested an unauthorized SIM swap on his AT&T account, causing his phone to go dead and sending all incoming texts and phone calls to a device the attackers controlled. Armed with that access, the intruders were able to reset credentials tied to his cryptocurrency accounts and siphon nearly $24 million worth of digital currencies.

While we can wonder in disbelief at a crypto investor who keeps his cash in an online wallet secured by text message, how many other services do we use that depend on emails or text messages, two vectors easily hackable by SIM spoofing attacks? How many of us would be resistant to the techniques that nabbed Terpin?

Another crypto owner, Namek Zu’bi, lost access to his Coinbase account after hackers swapped his SIM, logged into his account, and changed his email while attempting direct debits to his bank account.

“When the hackers took over my account they attempted direct debits into the account. But because I blocked my bank accounts before they could it seems there are bank chargebacks on that account. So Coinbase is essentially telling me sorry you can’t recover your account and we can’t help you but if you do want to use the account you owe $3K in bank chargebacks,” he said.

Now Zu’bi is facing a different issue: Coinbase is accusing him of being $3,000 in arrears and will not give him access to his account because he cannot reply from the hacker’s email.

“I tried to work with coinbase hotline who is supposed to help with this but they were clueless even after I told them that the hackerchanged email address on my original account and then created a new account with my email address. Since then I’ve been waiting for a ‘specialist’ to email me (was supposed to be 4 business days it’s been 8 days) and I’m still locked out of my account because Coinbase support can’t verify me,” he said.

It has been a frustrating ride.

“As an avid supporter and investor in crypto it baffles me how one of the market leaders who just supposedly launched institutional grade custody solutions can barely deal with a basic account take-over fraud,” Zu’bi said.

I’ve been using Trezor hardware wallets for a while, storing them in safe places outside of my home and maintaining a separate record of the seeds in another location. I have very little crypto but even for a fraction of a few BTC it just makes sense to practice safe storage. Ultimately, if you own crypto you are now your own bank. That you would trust anyone – including a fiat bank – to keep your digital currency safe is deeply delusional. Heck, I barely trust Trezor and they seem like the only solution for safe storage right now.

When I was first hacked I posted recommendations by crypto exchange Kraken. They are still applicable today:

Call your telco and:

Set a passcode/PIN on your account

- Make sure it applies to ALL account changes

- Make sure it applies to all numbers on the account

- Ask them what happens if you forget the passcode

- Ask them what happens if you lose that too

Institute a port freeze

Institute a SIM lock

Add a high-risk flag

Close your online web-based management account

Block future registration to online management system

Hack yo’ self

See what information they will leak

See what account changes you can make

They also recommend changing your telco email to something wildly inappropriate and using a burner phone or Google Voice number that is completely disconnected from your regular accounts as a sort of blind for your two factor texts and alerts.

Sadly, doing all of these things is quite difficult. Further, carriers don’t make it easy. In May a 27-year-old man named Paul Rosenzweig fell victim to a SIM-swapping hack even though he had SIM lock installed on his account. A rogue T-Mobile employee bypassed the security, resulting in the loss of a unique three character Twitter and Snapchat account.

Ultimately nothing is secure. The bottom line is simple: if you’re in crypto expect to be hacked and expect it to be painful and frustrating. What you do now – setting up real two-factory security, offloading your crypto onto physical hardware, making diligent backups, and protecting your keys – will make things far better for you in the long run. Ultimately, you don’t want to wake up one morning with your phone off and all of your crypto siphoned off into the pocket of a college kid like Joel Ortiz, a hacker who is now facing jail time for “13 counts of identity theft, 13 counts of hacking, and two counts of grand theft.” Sadly, none of the crypto he stole has surfaced after his arrest.

Powered by WPeMatico

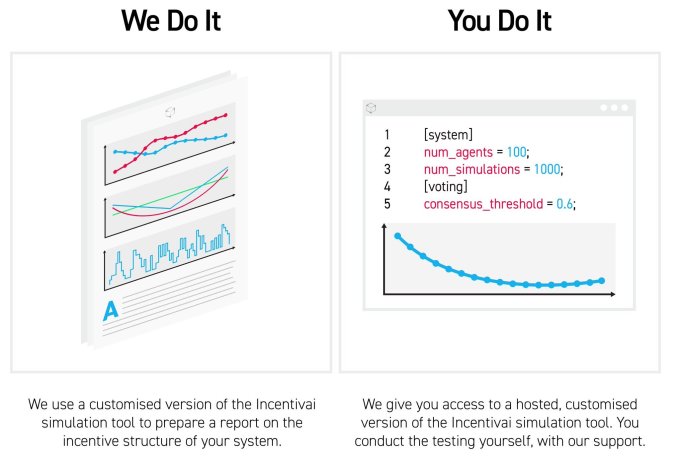

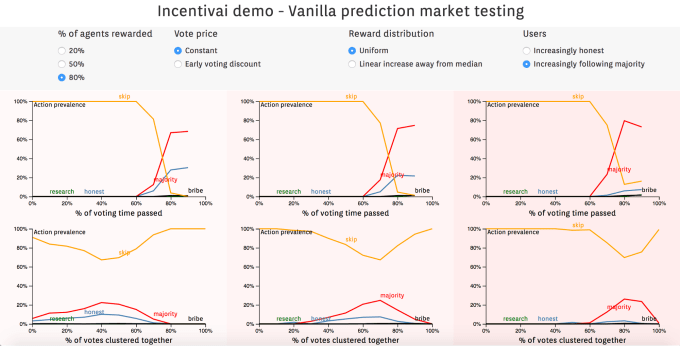

Cryptocurrency projects can crash and burn if developers don’t predict how humans will abuse their blockchains. Once a decentralized digital economy is released into the wild and the coins start to fly, it’s tough to implement fixes to the smart contracts that govern them. That’s why Incentivai is coming out of stealth today with its artificial intelligence simulations that test not just for security holes, but for how greedy or illogical humans can crater a blockchain community. Crypto developers can use Incentivai’s service to fix their systems before they go live.

“There are many ways to check the code of a smart contract, but there’s no way to make sure the economy you’ve created works as expected,” says Incentivai’s solo founder Piotr Grudzień. “I came up with the idea to build a simulation with machine learning agents that behave like humans so you can look into the future and see what your system is likely to behave like.”

Incentivai will graduate from Y Combinator next week and already has a few customers. They can either pay Incentivai to audit their project and produce a report, or they can host the AI simulation tool like a software-as-a-service. The first deployments of blockchains it’s checked will go out in a few months, and the startup has released some case studies to prove its worth.

“People do theoretical work or logic to prove that under certain conditions, this is the optimal strategy for the user. But users are not rational. There’s lots of unpredictable behavior that’s difficult to model,” Grudzień explains. Incentivai explores those illogical trading strategies so developers don’t have to tear out their hair trying to imagine them.

There’s no rewind button in the blockchain world. The immutable and irreversible qualities of this decentralized technology prevent inventors from meddling with it once in use, for better or worse. If developers don’t foresee how users could make false claims and bribe others to approve them, or take other actions to screw over the system, they might not be able to thwart the attack. But given the right open-ended incentives (hence the startup’s name), AI agents will try everything they can to earn the most money, exposing the conceptual flaws in the project’s architecture.

“The strategy is the same as what DeepMind does with AlphaGo, testing different strategies,” Grudzień explains. He developed his AI chops earning a masters at Cambridge before working on natural language processing research for Microsoft.

Here’s how Incentivai works. First a developer writes the smart contracts they want to test for a product like selling insurance on the blockchain. Incentivai tells its AI agents what to optimize for and lays out all the possible actions they could take. The agents can have different identities, like a hacker trying to grab as much money as they can, a faker filing false claims or a speculator that cares about maximizing coin price while ignoring its functionality.

Incentivai then tweaks these agents to make them more or less risk averse, or care more or less about whether they disrupt the blockchain system in its totality. The startup monitors the agents and pulls out insights about how to change the system.

For example, Incentivai might learn that uneven token distribution leads to pump and dump schemes, so the developer should more evenly divide tokens and give fewer to early users. Or it might find that an insurance product where users vote on what claims should be approved needs to increase its bond price that voters pay for verifying a false claim so that it’s not profitable for voters to take bribes from fraudsters.

Grudzień has done some predictions about his own startup too. He thinks that if the use of decentralized apps rises, there will be a lot of startups trying to copy his approach to security services. He says there are already some doing token engineering audits, incentive design and consultancy, but he hasn’t seen anyone else with a functional simulation product that’s produced case studies. “As the industry matures, I think we’ll see more and more complex economic systems that need this.”

Powered by WPeMatico

Coinbase wants to be Facebook Connect for crypto. The blockchain giant plans to develop “Login with Coinbase” or a similar identity platform for decentralized app developers to make it much easier for users to sign up and connect their crypto wallets. To fuel that platform, today Coinbase announced it has acquired Distributed Systems, a startup founded in 2015 that was building an identity standard for dApps called the Clear Protocol.

The five-person Distributed Systems team and its technology will join Coinbase. Three of the team members will work with Coinbase’s Toshi decentralized mobile browser team, while CEO Nikhil Srinivasan and his co-founder Alex Kern are forming the new decentralized identity team that will work on the Login with Coinbase product. They’ll be building it atop the “know your customer” anti-money laundering data Coinbase has on its 20 million customers. Srinivasan tells me the goal is to figure out “How can we allow that really rich identity data to enable a new class of applications?”

Distributed Systems had raised a $1.7 million seed round last year led by Floodgate and was considering raising a $4 million to $8 million round this summer. But Srinivasan says, “No one really understood what we’re building,” and it wanted a partner with KYC data. It began talking to Coinbase Ventures about an investment, but after they saw Distributed Systems’ progress and vision, “they quickly tried to move to find a way to acquire us.”

Distributed Systems began to hold acquisition talks with multiple major players in the blockchain space, and the CEO tells me it was deciding between going to “Facebook, or Robinhood, or Binance, or Coinbase,” having been in formal talks with at least one of the first three. Of Coinbase the CEO said, they “were able to convince us they were making big bets, weaving identity across their products.” The financial terms of the deal weren’t disclosed.

Coinbase’s plan to roll out the Login with Coinbase-style platform is an SDK that others apps could integrate, though that won’t necessarily be the feature’s name. That mimics the way Facebook colonized the web with its SDK and login buttons that splashed its brand in front of tons of new and existing users. This turned Facebook into a fundamental identity utility beyond its social network.

Developers eager to improve conversions on their signup flow could turn to Coinbase instead of requiring users to set up whole new accounts and deal with crypto-specific headaches of complicated keys and procedures for connecting their wallet to make payments. One prominent dApp developer told me yesterday that forcing users to set up the MetaMask browser extension for identity was the part of their signup flow where they’re losing the most people.

This morning Coinbase CEO Brian Armstrong confirmed these plans to work on an identity SDK. When Coinbase investor Garry Tan of Initialized Capital wrote that “The main issue preventing dApp adoption is lack of native SDK so you can just download a mobile app and a clean fiat to crypto in one clean UX. Still have to download a browser plugin and transfer Eth to Metamask for now Too much friction,” Armstrong replied “On it :)”

On it 🙂

— Brian Armstrong (@brian_armstrong) August 15, 2018

In effect, Coinbase and Distributed Systems could build a safer version of identity than we get offline. As soon as you give your Social Security number to someone or it gets stolen, it can be used anywhere without your consent, and that leads to identity theft. Coinbase wants to build a vision of identity where you can connect to decentralized apps while retaining control. “Decentralized identity will let you prove that you own an identity, or that you have a relationship with the Social Security Administration, without making a copy of that identity,” writes Coinbase’s PM for identity B. Byrne, who’ll oversee Srinivasan’s new decentralized identity team. “If you stretch your imagination a little further, you can imagine this applying to your photos, social media posts, and maybe one day your passport too.”

Considering Distributed Systems and Coinbase are following the Facebook playbook, they may soon have competition from the social network. It’s spun up its own blockchain team and an identity and single sign-on platform for dApps is one of the products I think Facebook is most likely to build. But given Coinbase’s strong reputation in the blockchain industry and its massive head start in terms of registered crypto users, today’s acquisition well position it to be how we connect our offline identity with the rising decentralized economy.

Powered by WPeMatico

Facebook is invading the blockchain, but how? Back in May, Facebook formed a cryptocurrency team to explore the possibilities, and today it removed a roadblock to revealing its secret plans.

Former head of Messenger David Marcus, who leads the Facebook Crypto team, today announced he was stepping down from the board of Coinbase, the biggest crypto startup. Marcus was formerly the president of PayPal and helped Facebook Messenger adopt chatbot commerce and peer-to-peer payments, so he was both a natural choice for Coinbase’s board and Facebook’s blockchain skunklabs.

Facebook told CoinDesk this was to avoid the appearance of a conflict of interest, which is exactly what it was. Marcus provided a statement to TechCrunch explaining he was stepping down “because of the new group I’m setting up at Facebook around blockchain,” noting that “Getting to know Brian [Armstrong, CEO of Coinbase], who’s become a friend, and the whole Coinbase leadership team and board has been an immense privilege. I’ve been thoroughly impressed by the talent and execution the team has demonstrated during my tenure, and I wish the team all the success it deserves going forward.”

Now Facebook is cleared to start publicly talking about its plans, though it hasn’t yet. “We are still in the very early stages and we are considering a number of different applications for the blockchain. But we don’t have anything else to share at this time,” a Facebook spokesperson tells me. So what could Facebook be building? I see three main consumer-facing opportunities.

Facebook could build a cryptocurrency wallet with its own token that people could use to pay for things with partnered businesses or that they discover through Facebook ads. Because blockchain can make transactions free or very cheap, Facebook and its partners could sidestep the typical credit card processing fees. That would potentially allow Facebook to offer users “3% off purchases made with FaceCoin” or a similar promotion.

Discounts like this could draw users into Facebook’s cryptocurrency feature. It’s well-positioned to run such a scheme thanks to its extensive connections with more than six million advertisers and 65 million businesses that have Facebook Pages. The social network could eat the costs of running the program, passing the transaction fee savings on to the users, while touting partnerships with Facebook Crypto as ways to boost sales for businesses. That could in turn get clients to spend more money on Facebook ads, as the discounts would enhance conversion rates and drive sales.

One thing we know for sure is that Facebook won’t be building on the Stellar protocol. Facebook debunked a Business Insider report saying it was, telling TechCrunch it was not in talks with Stellar or planning to build on it.

Facebook already lets you send friends money through Messenger for free, but only with a connected debit card or PayPal account. Facebook could offer cryptocurrency-based payments between friends to let a wider range of users settle debts for shared dinners or taxis through Messenger. Users might fund their Facebook Crypto wallet once with a payment, possibly with a one-time transaction fee, and then they could send and receive the tokens for free from then on. Blockchain becoming the backbone of peer-to-peer payments could further increase engagement with Messenger for its 1.3 billion users.

Meanwhile, Facebook could also potentially use cryptocurrency to let fans send micropayments to their favorite creators, like video stars and game streamers. Facebook recently debuted its own virtual (not crypto) currency, called Facebook Stars, that users can buy and send to creators, who can then cash them out for one cent each. Facebook takes an undisclosed cut, but gives to the creator the majority of what users spend on Stars.

Facebook could potentially undergird this system with cryptocurrency to alleviate transaction fees and let people tip creators smaller amounts of cash for exclusive content or just to show their appreciation. Facebook started with a minimum of $3 tips at a time so that transaction fees wouldn’t be too high of a percentage of the total purchase. A cryptocurrency solution could let users efficiently tip much smaller amounts, which could lure people toward the behavior. The more money Facebook can deliver to internet celebrities, the more popular ones it can recruit to live on its platform and the more content they’ll produce.

Facebook Stars. Image via KiwiFarm

A top problem in the world of decentralized blockchain apps is how you bring your identity with you. Securely connecting your wallet, blockchain-based virtual goods and biographical info to new dApps can be a laborious process. Users typically have to type in long, complicated alphanumeric keys that are tough to remember and annoying to input. User experience design around identity in the blockchain space lags far behind what we’re used to with mainstream social apps like Facebook Connect, which uses a OAuth single sign-on to let you instantly join apps without creating a new username and password, or filling out a profile and uploading a photo.

Facebook could use its expertise in operating a popular identity platform to ease login to dApps. While the company has faced plenty of privacy issues and attacks on election integrity, Facebook has a strong record of not being traditionally hacked. It hasn’t suffered a massive user data breach like LinkedIn, Twitter and other social networks. Using an overtly centralized identity system to connect with decentralized apps might be counterintuitive, but Facebook could deliver the UX convenience necessary to unlock a new wave of blockchain utility.

For now it’s unclear if Facebook will end up directly competing with Coinbase in the exchange and wallet space, or if it might instead partner with the blockchain mainstay to accelerate its efforts. And on the enterprise engineering side, Facebook could build some decentralized storage infrastructure to cut its massive server bills. But with deep pockets, tons of tech talent and ubiquity amongsts social networkers and businesses, Facebook Crypto’s primary limits are its ambitions and the extent of user trust.

Powered by WPeMatico

Audius wants to cut the middlemen out of music streaming so artists get paid their fair share. Coming out of stealth today led by serial entrepreneur and DJ Ranidu Lankage, Audius is building a blockchain-based alternative to Spotify or SoundCloud.

Users will pay for Audius tokens or earn them by listening to ads. Their wallet will then pay out a fraction of a cent per song to stream from decentralized storage across the network, with artists receiving roughly 85 percent — compared to roughly 70 percent on the leading streaming apps. The rest goes to compensating whomever is hosting that song, as well as developers of listening software clients, one of which will be built by Audius.

Audius plans to launch its open-sourced product in beta later this year. But it’s already found some powerful investors that see SoundCloud as vulnerable to the cryptocurrency revolution. Audius has raised a $5.5 million Series A led by General Catalyst and Lightspeed, with participation from Kleiner Perkins, Pantera Capital, 122West and Ascolta Ventures. They’re betting that Audius’ token will grow in value, making the stockpile it keeps worth a fortune. It could then sell chunks of its tokens to earn revenue instead of charging artists directly.

Audius co-founders (from left): head of product Forrest Browning, CEO Ranidu Lankage, CTO Roneil Rumburg

“The biggest problem in the music industry is that streaming is taking off and artists aren’t necessarily earning a lot of money. And it can take three months, or up to 18 months for unsigned artists, to get paid for streams,” says Lankage. “That’s what crypto really solves. You can pay artists in near real-time and make it fully transparent.”

The big question will be whether Audius can use the token economy to crack the chicken-and-egg problem of getting its first creators and listeners on a platform that might be less functionally robust than its traditional competitors. There are a lot of moving parts to decentralize, but there are also plenty of disgruntled musicians out there waiting for something better.

Most startup guys don’t have Billboard charting singles on their bio, but Lankage does. Born in Sri Lanka, his hip-hop songs in his native tongue of Sinhalese were the first of the language to be played on the BBC and MTV. He got signed to Sony and even went platinum, but left the label seeking greater control over his work. After going to Yale, he applied his music business knowledge to build a Reddit for dance music called The Drop with Twitch’s Justin Kan back in 2015.

The two teamed up again on a video version of Q&A app Quora called Whale, but that fizzled out too. Lankage’s next venture Polly, a polling tool built as a complement to Snapchat, inspired the now super-popular Instagram Stories polls and questions stickers. But after an acqui-hire by Reddit fell through, he returned to his first love: music.

“I’ve always been passionate about building tools for creators,” says Lankage. But this time, he wanted to focus on helping them turn their art into a profession. He teamed up with CTO Roneil Rumburg, an engineering partner at Kleiner Perkins who’d build a crypto wallet called Backslash, and head of product Forrest Browning, who’d sold his software metering startup StacksWare to Avi Networks.

Their goal is to build a blockchain streaming music service where listeners don’t have to understand blockchains. “A user wouldn’t even know that they have a wallet,” says Rumburg. They’ll just hear an ad every once in a while, get a subscription, or pay per stream. Since Audius is open sourced, developers will be able to build their own listening clients on top, which could specialize in discovery of certain types of music or offer their own payment schemes.

“I have known Ranidu, Forrest and Roneil for a long time, and have always been impressed with their ability to blend art, technology and business together,” says investor Niko Bonatsos of General Catalyst. “In Audius, they bring together all three skills, with a deep technical heart and a compelling solution for a very big marketplace.”

For starters, Audius is focusing on signing up independent electronic musicians. These are the types that might be popular on SoundCloud but actually have to pay for hosting there while not getting much back due to the platform’s weak monetization options. Don’t expect U2 and Ariana Grande on Audius, at least not yet. But the startup could differentiate by offering access to content you can’t find elsewhere.

To get artists on board, Lankage tells me Audius plans “to use token incentives.” Those willing to jump on first before there are many listeners could get a bonus allotment of tokens that might be worth more if they help popularize the service. And where artists go, their fans will follow. Audius is hoping artists will share its links first because that’s where they’ll earn the most money.

![]() Audius has also lined up a legion of big-name advisors to help it develop its blockchain product and artist relationships. Those include Augur co-founder Jeremy Gardner, EDM artist 3LAU, EA co-founder Bing Gordon and more it can’t announce just yet.

Audius has also lined up a legion of big-name advisors to help it develop its blockchain product and artist relationships. Those include Augur co-founder Jeremy Gardner, EDM artist 3LAU, EA co-founder Bing Gordon and more it can’t announce just yet.

The linchpin of Audius will be the user experience. If the system feels too complicated, listeners and artists will stay elsewhere. A DJ might earn more per stream from Audius, but if Spotify or SoundCloud offer better ways for fans to subscribe to them and generate more plays long-term, they’ll still direct supporters there. But if Audius can hide the nerdy bits while solving the music industry’s problems, it has the potential to be one of the first mainstream consumer blockchain projects that treats the tech as a utility, not just a new stock market to bet on.

Powered by WPeMatico

Maybe a year and a half after Russian interference was believed to have a key impact on the election of a U.S. president isn’t the best time to be floating new voting technologies. Not if you’re looking to avoid some major skepticism, at least.

But West Virginia is going ahead with plans to allow some limited voting through a smartphone app called Voatz, nonetheless. The plan, spearheaded by West Virginia Secretary of State Mac Warner, will utilize the Boston-based startup’s technology to allow troops stationed abroad to vote in the upcoming November midterm.

Both Voatz and Warner, naturally, tout the security of the app. Indentification requires a user to take a selfie, which is matched with a state I.D. using facial recognition. Ballots are then anonymous and recorded with blockchain tech.

Naturally, not everyone is thrilled about the idea.

“Mobile voting is a horrific idea,” the Center for Democracy and Technology’s Joseph Lorenzo Hall, told CNN. “It’s internet voting on people’s horribly secured devices, over our horrible networks, to servers that are very difficult to secure without a physical paper record of the vote.”

Not a fan, apparently.

The state has been testing the tech, and Warner says that paper will still be an option for those serving abroad, even as it offers access to smartphone voting. The lack of paper trail for electronic voting, however, is generally considered a bit of a nonstarter, and recent events will likely only make security experts more wary of adopting new tech.

Powered by WPeMatico

Sometimes smart contracts can be pretty dumb.

All of the benefits of a cryptographically secured, publicly verified, anonymized transaction system can be erased by errant code, malicious actors or poorly defined parameters of an executable agreement.

Hoping to beat back the tide of bad contracts, bad code and bad actors, Sagewise, a new Los Angeles-based startup, has raised $1.25 million to bring to market a service that basically hits pause on the execution of a contract so it can be arbitrated in the event that something goes wrong.

Co-founded by a longtime lawyer, Amy Wan, whose experience runs the gamut from the U.S. Department of Commerce to serving as counsel for a peer-to-peer real estate investment platform in Los Angeles, and Dan Rice, a longtime entrepreneur working with blockchain, Sagewise works with both Ethereum and the Hedera Hashgraph (a newer distributed ledger technology, which purports to solve some of the issues around transaction processing speed and security which have bedeviled platforms like Ethereum and Bitcoin).

The company’s technology works as a middleware, including an SDK and a contract notification and monitoring service. “The SDK is analogous to an arbitration clause in code form — when the smart contract executes a function, that execution is delayed for a pre-set amount of time (i.e. 24 hours) and users receive a text/email notification regarding the execution,” Wan wrote to me in an email. “If the execution is not the intent of the parties, they can freeze execution of the smart contract, giving them the luxury of time to fix whatever is wrong.”

Sagewise approaches the contract resolution process as a marketplace where priority is given to larger deals. “Once frozen, parties can fix coding bugs, patch up security vulnerabilities, or amend/terminate the smart contract, or self-resolve a dispute. If a dispute cannot be self-resolved, parties then graduate to a dispute resolution marketplace of third party vendors,” Wan writes. “After all, a $5 bar bet would be resolved differently from a $5M enterprise dispute. Thus, we are dispute process agnostic.”

Wavemaker Genesis led the round, which also included strategic investments from affiliates of Ari Paul (Blocktower Capital), Miko Matsumura (Gumi Cryptos), Youbi Capital, Maja Vujinovic (Cipher Principles), Jordan Clifford (Scalar Capital), Terrence Yang (Yang Ventures) and James Sowers.

“Smart contracts are coded by developers and audited by security auditing firms, but the quality of smart contract coding and auditing varies drastically among service providers,” said Wan, the chief executive of Sagewise, in a statement. “Inevitably, this discrepancy becomes the basis for smart contract disputes, which is where Sagewise steps in to provide the infrastructure that allows the blockchain and smart contract industry to achieve transactional confidence.”

In an email, Wan elaborated on the thesis to me, writing that, “smart contracts may have coding errors, security vulnerabilities, or parties may need to amend or terminate their smart contracts due to changing situations.”

Contracts could also be disputed if their execution was triggered accidentally or due to the actions of attackers trying to hack a platform.

“Sagewise seeks to bring transactional confidence into the blockchain industry by building a smart contract safety net where smart contracts do not fulfill the original transactional intent,” Wan wrote.

Powered by WPeMatico

Crypto skeptics rejoice! A new way to short the cryptocurrency market is coming from dYdX, a decentralized financial derivatives startup. In two months it will launch its protocol for creating short and leverage positions for Ethereum and other ERC20 tokens that allow investors to amp up their bets for or against these currencies.

To get the startup there, dYdX recently closed a $2 million seed round led by Andreessen Horowitz and Polychain, and joined by Kindred and Abstract plus angels, including Coinbase CEO Brian Armstrong and co-founder Fred Ehrsam, and serial investor Elad Gil.

“The main use for cryptocurrency so far has been trading and speculation — buying and holding. That’s not how sophisticated financial institutions trade,” says dYdX founder Antonio Juliano. “The derivatives market is usually an order of magnitude bigger than the spot trading or buy/sell market. The cryptocurrency market is probably on the order of $5 billion to $10 billion in volume, so you’d expect the derivatives market would be 10X bigger. I think there’s a really big opportunity there.”

The idea is that you buy the short Ethereum token with ETH or a stable coin from an exchange or dYdX. The short Ethereum’s token price is inversely pegged to ETH, so it goes up in value when ETH goes down and vice versa. You can then sell the short Ethereum token for a profit if you correctly predicted an ETH price drop.

On the backend, lenders earn an interest rate by providing ETH as collateral locked into smart contracts that back up the short Ethereum tokens. Only a small number of actors have to work with the smart contract to mint or close the short Tokens. Meanwhile, dYdX also offers leveraged Ethereum tokens that let investors borrow to boost their profits if ETH’s price goes up.

The plan is to offer short and leveraged tokens for any ERC20 currency in the future. dYdX is building its own user-facing application for buying the tokens, but is also partnering with exchanges to offer the margin tokens “where people are already trading,” says Juliano.

“We think of it as more than just shorting your favorite shitcoin. We think of them as mature financial products.”

Coinbase has proven to be an incredible incubator for blockchain startup founders. Juliano was employed there as a software engineer after briefly working at Uber and graduating in computer science from Princeton in 2015. “The first thing I started was a search engine for decentralized apps. I worked for months on it full-time, but nobody was building decentralized apps so no one was searching for them. It was too early,” Juliano explains.

But along the way he noticed the lack of financial instruments for decentralized derivatives despite exploding consumer interest in buying and selling cryptocurrencies. He figured the big hedge funds would eventually come knocking if someone built them a bridge into the blockchain world.

But along the way he noticed the lack of financial instruments for decentralized derivatives despite exploding consumer interest in buying and selling cryptocurrencies. He figured the big hedge funds would eventually come knocking if someone built them a bridge into the blockchain world.

Juliano built dYdX to create a protocol to first begin offering margin tokens. It’s open source, so technically anyone can fork it to issue tokens themselves. But dYdX plans to be the standard-bearer, with its version offering the maximum liquidity to investors trying to buy or sell the margin tokens. His five-person team in San Francisco with experience from Google, Bloomberg, Goldman Sachs, NerdWallet and ConsenSys is working to find as many investors as possible to collateralize the tokens and exchanges to trade them. “It’s a race to build liquidity faster than anyone else,” says Juliano.

So how will dYdX make money? As is common in crypto, Juliano isn’t exactly sure, and just wants to build up usage first. “We plan to capture value at the protocol level in the future likely through a value adding token,” the founder says. “It would’ve been easy for us to rush into adding a questionable token as we’ve seen many other protocols do; however, we believe it’s worth thinking deeply about the best way to integrate a token in our ecosystem in a way that creates rather than destroys value for end users.”

“Antonio and his team are among the top engineers in the crypto ecosystem building a novel software system for peer-to-peer financial contracts. We believe this will be immensely valuable and used by millions of people,” says Polychain partner Olaf Carlson-Wee. “I am not concerned with short-term revenue models but rather the opportunity to permanently improve global financial markets.”

With the launch less than two months away, Juliano is also racing to safeguard the protocol from attacks. “You have to take smart contract security extremely seriously. We’re almost done with the second independent security audit,” he tells me.

The security provided by decentralization is one of dYdX’s selling points versus centralized competitors like Poloniex that offer margin trading opportunities. There, investors have to lock up ETH as collateral for extended periods of time, putting it at risk if the exchange gets hacked, and they don’t benefit from shared liquidity like dYdX will.

The security provided by decentralization is one of dYdX’s selling points versus centralized competitors like Poloniex that offer margin trading opportunities. There, investors have to lock up ETH as collateral for extended periods of time, putting it at risk if the exchange gets hacked, and they don’t benefit from shared liquidity like dYdX will.

It also could compete for crypto haters with the CBOE that now offers Bitcoin futures and margin trading, though it doesn’t handle Ethereum yet. Juliano hopes that since dYdX’s protocol can mint short tokens for other ERC20 tokens, you could bet for or against a certain cryptocurrency relative to the whole crypto market by mixing and matching. dYdX will have to nail the user experience and proper partnerships if it’s going to beat the convenience of centralized exchanges and the institutional futures market.

If all goes well, dYdX wants to move into offering options or swaps. “Those derivatives are more often traded by sophisticated traders. We don’t think there are too many traders like that in the market right now,” Juliano explains. “The other types of derivatives that we’ll move to in the future will be really big once the market matures.” That “once the market matures” refrain is one sung by plenty of blockchain projects. The question is who’ll survive long enough to see that future, if it ever arrives.

[Featured Image via Nuzu and Bryce Durbin]

Powered by WPeMatico

Meet Radar Relay, a cryptocurrency startup that just raised $10 million from Blockchain Capital and other investors. The company is taking advantage of the 0x protocol to change your tokens into other tokens without going through a traditional exchange.

Centralized exchanges have been one of the main weaknesses of the cryptocurrency industry for years. A centralized exchange can get hacked or shut down. Malicious users can also hijack your account and transfer all your tokens.

“I definitely hope centralized exchanges go burn in hell as much as possible,” Vitalik Buterin said in a recent TechCrunch interview.

So what is the solution? Decentralized exchanges that never hold your tokens on their wallets. As TechCrunch’s Josh Constine wrote, 0x is a protocol that makes this possible. 0x connects traders so that you can swap tokens without going through a centralized marketplace. It leverages smart contracts so that you don’t end up sending the tokens first and waiting for the other person to send you back their tokens — the transaction happens simultaneously.

Many companies are building projects on top of the 0x protocol, and Radar Relay is one of them. As the name suggests, Radar Relay helps you find other traders who are interested in your order.

For instance, if you want to exchange 10 MLN for 162 ZRX, you need to publicize your order somewhere so that other users can find it. If another Radar Relay user wants to make a similar transaction, but in the other direction, then the trade occurs.

Users connect wallet addresses on Radar Relay so that you stay in control of your tokens at all times. For instance, if you use a Ledger wallet, you can exchange tokens from one address on your Ledger to another. In the future, you can imagine integrations with wallet makers so that you can submit an order from your wallet directly.

In addition to leaving you in control of your tokens, you don’t need to create an account to use a decentralized exchange. Radar Relay is only compatible with ERC20 tokens as 0x has been designed for ERC20 tokens specifically. Since October, users have traded the equivalent of $150 million in 170 tokens.

While Blockchain Capital is leading the round, a ton of investors have put money in Radar Relay — Tusk Ventures, Distributed Global, Reciprocal Ventures, Collaborative Fund, Distributed Global, Reciprocal Ventures, Collaborative Fund, Elefund, Slow Ventures, SV Angel, Kindred Ventures, Breyer Capital, Digital Currency Group, V1.VC, Kokopelli, Village Global and Chapter One.

It’s an impressive list of investors. So let’s see if decentralized exchanges can shake up the big exchanges that everybody uses today.

Powered by WPeMatico

Xage (pronounced Zage), a blockchain security startup based in Silicon Valley, announced a $12 million Series A investment today led by March Capital Partners. GE Ventures, City Light Capital and NexStar Partners also participated.

The company emerged from stealth in December with a novel idea to secure the myriad of devices in the industrial internet of things on the blockchain. Here’s how I described it in a December 2017 story:

Xage is building a security fabric for IoT, which takes blockchain and synthesizes it with other capabilities to create a secure environment for devices to operate. If the blockchain is at its core a trust mechanism, then it can give companies confidence that their IoT devices can’t be compromised. Xage thinks that the blockchain is the perfect solution to this problem.

It’s an interesting approach, one that attracted Duncan Greatwood to the company. As he told me in December his previous successful exits — Topsy to Apple in 2013 and PostPath to Cisco in 2008 — gave him the freedom to choose a company that really excited him for his next challenge.

When he saw what Xage was doing, he wanted to be a part of it, and given the unorthodox security approach the company has taken, and Greatwood’s pedigree, it couldn’t have been hard to secure today’s funding.

The Industrial Internet of Things is not like its consumer cousin in that it involves getting data from big industrial devices like manufacturing machinery, oil and gas turbines and jet engines. While the entire Internet of Things could surely benefit from a company that concentrates specifically on keeping these devices secure, it’s a particularly acute requirement in industry where these devices are often helping track data from key infrastructure.

GE Ventures is the investment arm of GE, but their involvement is particularly interesting because GE has made a big bet on the Industrial Internet of Things. Abhishek Shukla of GE Ventures certainly saw the connection. “For industries to benefit from the IoT revolution, organizations need to fully connect and protect their operation. Xage is enabling the adoption of these cutting edge technologies across energy, transportation, telecom, and other global industries,” Shukla said in a statement.

The company was founded just last year and is based in Palo Alto, California.

Powered by WPeMatico