blockchain

Auto Added by WPeMatico

Auto Added by WPeMatico

Blok.Party, the company that built the upcoming PlayTable game console, announced today it raised $10 million in new funding. It’s also unveiling a big content partnership, where Blok.Party will create its own version of the popular board game Settlers of Catan.

I first wrote about Blok.Party and PlayTable earlier this year, when co-founder and CEO Jimmy Chen first laid out his vision to use blockchain technology to build a console that can recognize real-world objects (like figurines and cards), creating a hybrid between tabletop and video gaming.

The idea may have sounded a little abstract at the time, but it got a lot clearer when Chen dropped by the TechCrunch New York office to play a couple rounds of Catan with me.

I’ll admit that I hadn’t played in a while, but it was clear from the start that PlayTable saved us some setup time — instead of putting all the pieces of the physical board together, you play on a digital representation of the board. Most of the pieces are digitized too, and we used and traded our cards using smartphones. But there is a physical “robber” piece, because Chen said this allows the robber’s movement to remain “a very visceral experience … that a digital version can’t ever capture.”

It may not be too long before you get to try this out for yourself, at least if you’re among the 10,000 pre-orders Blok.Party has received so far. Chen said the company will start shipping its first devices this fall.

He added that Catan, like many of the other games built for PlayTable, will be priced at around $20.

“For us, it’s not about trying to compete based on price,” Chen said. “We’re trying to compete based on experience.”

The new funding comes from crypto fund JRR Capital and other investors. Chen said the company will use the money to continue scaling the product, including further software development and building out the library of games.

At the same time, he emphasized that although Blok.Party is manufacturing the initial devices, his vision is to achieve real scale through partnerships with hardware manufacturers, who will build their own PlayTable consoles. Apparently, some of those discussions are already underway.

“Our strategy is to always have [our own] hardware program running to continually do research,” Chen said. “What I’ve discovered is that keeping a hardware program running is not that expensive. The expensive part is when you try to scale the program.”

Powered by WPeMatico

Cryptocurrency speculation is over. That’s why I’m excited to announce that Vinay Gupta will join us at TechCrunch Disrupt Berlin to talk about cool use cases that could make blockchain projects useful, beyond financial services.

Gupta worked on the initial release of Ethereum back in 2015. He contributed when it comes to project management. He then worked with the Consensys team on other cryptocurrency projects.

But he’s now 100 percent focused on his own project — Mattereum. As the name suggests, it’s all about bringing physical objects to the blockchain.

For instance, if you buy an expensive painting, you want to make sure that you sign a contract with the previous owner that says that you now own this painting.

Mattereum helps you set up self-executing smart contracts to transfer digital assets (including tokens that could prove the ownership of a painting).

But if you want to combine smart contracts with good old legal contracts, Mattereum has also worked on Ricardian contracts so that those contracts have a legal value. Finally, Mattereum also worked on a decentralized dispute resolution platform that can be enforced in a national court.

If you want to listen to Gupta talk about Mattereum himself, then you should come to Disrupt Berlin.

Buy your ticket to Disrupt Berlin to listen to this discussion and many others. The conference will take place on November 29-30.

In addition to fireside chats and panels, like this one, new startups will participate in the Startup Battlefield Europe to win the highly coveted Battlefield cup.

Founder, Mattereum Ltd.

Vinay Gupta is a technologist and policy analyst with a particular interest in how specific technologies can close or create new avenues for decision makers. This interest has taken him through cryptography, energy policy, defence, security, resilience and disaster management arenas.

He is the founder of Hexayurt.Capital, a fund which invests in creating the Internet of Agreements . Mattereum is the first Internet of Agreements infrastructure project, bringing legally-enforceable smart contracts, and enabling the sale, lease, and transfer of physical property and legal rights.

. Mattereum is the first Internet of Agreements infrastructure project, bringing legally-enforceable smart contracts, and enabling the sale, lease, and transfer of physical property and legal rights.

He is known for his work on the hexayurt, a public domain disaster relief shelter designed to be build from commonly-available materials, and with Ethereum, a distributed network designed to handle smart contracts.

Powered by WPeMatico

When Circle raised its $110 million funding round, the company used this opportunity to talk about its stablecoin — USD Coin, or USDC for short. And you can now buy, sell and send USD Coins on Circle Trade and Circle’s exchange Poloniex.

But what is a stablecoin? As the name suggests, 1 USDC is worth 1 USD. Unlike traditional cryptocurrencies, you can be sure that the value of USDC isn’t going to fluctuate like crazy.

There are multiple reasons why you’d want to use stablecoins. First, if you want to short cryptocurrencies without cashing out, you can convert your bitcoins or ethers to USDC. This way, it’ll be easier to buy cryptocurrencies again in the future.

Second, if you want to avoid traditional financial institutions, you can send USDC to other people without going through a bank. Sending USDC is like sending any other token — you just need to tell your recipient to get a wallet and ask for their wallet address.

Third, I’m sure many people are going to use stablecoins to avoid taxation issues. It’s easier to hide a bunch of tokens than a big wire transfers hitting your bank statement.

Many people living in countries suffering from hyperinflation or chronic inflation, such as Venezuela or Turkey, could also rely on USDC to convert some of their savings. This way, you don’t have to open a bank account in another country.

USDC is an ERC-20 token, which means that it’s easy to add support for USDC if you’re running an exchange or a wallet. But Circle wants to make sure that issuers are not just printing money without any actual USD in their bank accounts.

Multiple companies partnered to create CENTRE, a consortium that is going to define policies around stablecoins and governance. If you want to issue USDC, you have to comply with a bunch of rules. In particular, you have to send monthly audited reports proving that you have as many USD on deposit as issued tokens.

Multiple companies have already announced that they will begin trading USDC soon, such as DigiFinex, CoinEx, KuCoin, OKCoin, Coinplug and XDAEX. On the wallet front, BitGo, Cobo, Coinbase Wallet, CoolWallet S, Elph, imToken, Ledger, Status and Trust will add native USDC support soon.

Powered by WPeMatico

Walmart has been working with IBM on a food safety blockchain solution and today it announced it’s requiring that all suppliers of leafy green vegetable for Sam’s and Walmart upload their data to the blockchain by September 2019 .

Most supply chains are bogged down in manual processes. This makes it difficult and time consuming to track down an issue should one like the E. coli romaine lettuce problem from last spring rear its head. By placing a supply chain on the blockchain, it makes the process more traceable, transparent and fully digital. Each node on the blockchain could represent an entity that has handled the food on the way to the store, making it much easier and faster to see if one of the affected farms sold infected supply to a particular location with much greater precision.

Walmart has been working with IBM for over a year on using the blockchain to digitize the food supply chain process. In fact, supply chain is one of the premiere business use cases for blockchain (beyond digital currency). Walmart is using the IBM Food Trust Solution, specifically developed for this use case.

“We built the IBM Food Trust solution using IBM Blockchain Platform, which is a tool or capability that IBM has built to help companies build, govern and run blockchain networks. It’s built using Hyperledger Fabric (the open source digital ledger technology) and it runs on IBM Cloud,” Bridget van Kralingen, IBM’s senior VP for Global Industries, Platforms and Blockchain explained.

Before moving the process to the blockchain, it typically took approximately 7 days to trace the source of food. With the blockchain, it’s been reduced to 2.2 seconds. That substantially reduces the likelihood that infected food will reach the consumer.

Photo: Shana Novak/Getty Images

One of the issues in a requiring the suppliers to put their information on the blockchain is understanding that there will be a range of approaches from paper to Excel spreadsheets to sophisticated ERP systems all uploading data to the blockchain. Walmart spokesperson Molly Blakeman says that this something they worked hard on with IBM to account for. Suppliers don’t have to be blockchain experts by any means. They simply have to know how to upload data to the blockchain application.

“IBM will offer an onboarding system that orients users with the service easily. Think about when you get a new iPhone – the instructions are easy to understand and you’re quickly up and running. That’s the aim here. Essentially, suppliers will need a smart device and internet to participate,” she said.

After working with it for a year, the company things it’s ready for broader implementation with the goal ultimately being making sure that the food that is sold at Walmart is safe for consumption, and if there is a problem, making auditing the supply chain a trivial activity.

“Our customers deserve a more transparent supply chain. We felt the one-step-up and one-step-back model of food traceability was outdated for the 21st century. This is a smart, technology-supported move that will greatly benefit our customers and transform the food system, benefitting all stakeholders,” Frank Yiannas, vice president of food safety for Walmart said in statement.

In addition to the blockchain requirement, the company is also requiring that suppliers adhere to one of the Global Food Safety Initiative (GFSI), which have been internationally recognized as food safety standards, according to the company.

Powered by WPeMatico

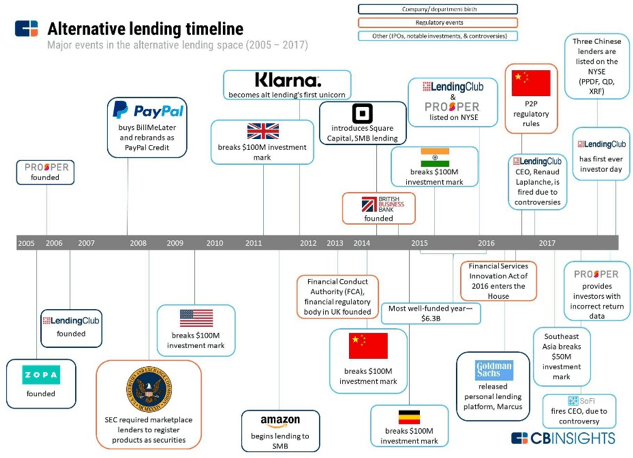

Renaud Laplanche spent ten years building LendingClub. In the process, he created an industry from scratch. Circumventing conventional banking channels for consumer credit began in 1996 when Chris Larsen started E-LOAN, which ultimately led to Prosper Marketplace. But LendingClub, which Laplanche founded in 2007, was and remains the poster child for the business of marketplace lending. The industry’s short history has been volatile, characterized by both triumphant hype and utter lack of confidence.

History of the Marketplace Lending Industry, CB Insights

While LendingClub has struggled in the public markets since their late 2014 IPO, they have managed to propel their industry into significance, while rapidly expanding their share of the personal loan market to 10%.

After his well-publicized departure in May 2016, Laplanche got started on his next venture in a hurry. Just a few months later he started Credify, ultimately renamed to Upgrade, a company that bears a striking resemblance to LendingClub. In just two years Upgrade has raised $142 million in funding, while originating more than $1 billion in loans since August 2017.

With Upgrade, Laplanche has the opportunity to start fresh with the benefit of hindsight. The initial promise of LendingClub and their competitors was unbundling the banks. Now, to persist and grow, marketplace lenders have realized they need to rebundle, providing an array of bank-like services to better serve their end customers. This post explores what Laplanche is doing differently this time with Upgrade.

There has been a general recognition across many fintech businesses that marketplace business models aren’t enough. The mutually-beneficial arrangement of marketplace lending is a perfect example. Superior customer experience, expedited loan decision, quick receipt of funds, and lower operational costs without legacy infrastructure were the selling points. Charles Moldow famously called it a “trillion-dollar opportunity” in 2014.

He may still be right, but in order to realize the opportunity, marketplace lenders need to capture a larger, more regular share of borrower’s attention. Loans may be high-volume purchases, but they’re not high-frequency transactions. So when a platform like LendingClub facilitates a loan so someone can refinance their outstanding credit card debt, is there really a relationship with the customer there? Capital is provided, customer service is available, and monthly payments are made. That’s all there is to it.

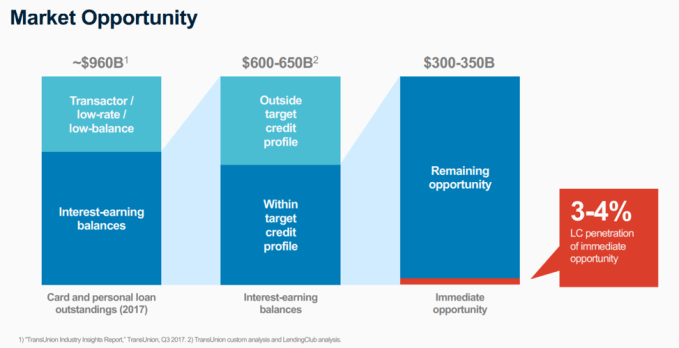

Total addressable market (TAM) is frequently used to assess opportunity. A critical part of the TAM estimation process might have been overlooked in the early assessments of the alternative lending industry. The large numbers in the figure below reflect an alluring market that LendingClub, Prosper, Avant, Upstart, OneMain, Best Egg and others have attempted to capitalize upon.

The notion of a replacement cycle, which I’ll borrow from Michael Mauboussin, is an important consideration here, particularly in a high volume, low frequency transaction relationship such as consumer lending. Just because a borrower refinances their credit card debt with a loan from LendingClub, there’s little guarantee that all of the money spent on acquiring that customer will lead to future transactions with that customer. Yet, in order for these companies to succeed, the average revenue per user (ARPU) is going to have to rise through some combination of repeat customers and complementary services to deepen the relationship and create new revenue channels.

The market opportunity for marketplace Lenders, LendingClub Investor Day 2017

With this realization in mind, fintech players across the board have focused on deepening relationships with customers to drive sales and lower SG&A costs. Customer acquisition is a major component of the income statement for these companies. The more engagement a lender has with their end customer, the greater the chance they stand to not only be called upon when a borrower needs to borrow again, but ultimately pinpoint opportunities for product recommendations.

And that’s exactly what Upgrade is doing. In many ways, they’re quite similar to LendingClub. Upgrade offers personal loans between $1,000 and $50,000 over three-to-five-year repayment periods at rates competitive with major banks. LendingClub varies a bit in the principal amount offerings and APRs, but they essentially do the same thing. Loans are originated through WebBank, the partner bank that also works with LendingClub. Operationally, there’s a blockchain component for data remediation and security purposes. However, the extent and value of this application are unclear.

The notion of financial wellness is increasingly popular among consumer fintech companies, as well as incumbent financial institutions. It reflects a transition away from a purely transactional relationship to a fiduciary one, as we’ve also seen in the wealth management industry. The tricky thing about this is that although it may be the right thing to do, late fees and overdraft penalties make up a sizeable portion of traditional bank revenue.

Where Upgrade differs from LendingClub is in their customer engagement model. Upgrade provides several features to customers that resemble a conventional personal financial management (PFM) app. Their Credit Health service offers free advice and monitoring tools, personalized recommendations, and customized updates for individual credit scores and underlying rationale. Additionally, they offer a financial education tool open to the public called Credit Health Insights, which offers tips and tricks for debt management and financial wellness. At the surface, there’s little differentiation here. A free credit score is becoming table stakes for any financial institution, and personalized insights are to be expected.

Upgrade’s borrower value proposition, LendIt 2018 Conference

In Upgrade’s case, however, the framing of the dual service is compelling. Typically, online lenders only approve 10-15% of applicants. While the credit underwriting models are looking for the most compelling borrower profiles who will pay back their loans, the majority of interested borrowers are sent back to the drawing board.

A major focus of Upgrade is to build the credit of the other 85-90% of applicants who are typically rejected so that they improve their profile and obtain a loan in the future. Credit repair and financial wellness are underserved markets today, although companies like Bloom Credit are working to change the record. This product combination helps to unify the interests of Upgrade and borrowers, both approved and rejected.

At the LendIt Conference in 2017, Laplanche concluded his presentation with a reference to the Wright Brothers. He discussed how he was enamored with their ability to combine two things to create something entirely new, which in their case was “wheeling and flying.” A year later, he returned to LendIt with a new product release that borrowed from the innovation strategy of Orville and Wilbur.

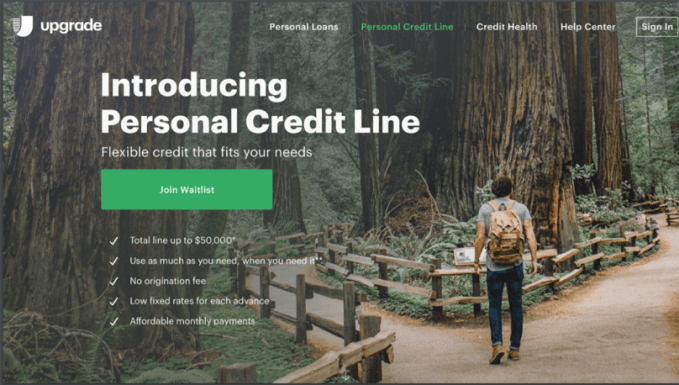

Upgrade launched a first of its kind product, a Personal Credit Line, a hybrid of a credit card and an unsecured loan. Here’s how it works: customers get approved for up to $50,000 in credit, from which they can draw down as needed. They only pay interest on what’s borrowed, over the course of a 12-60-month timeframe. The interest rate is also fixed over the term of the loan.

Upgrade’s Personal Credit Line, a hybrid of a personal loan and a credit card, Upgrade

The product is built on the premise that the level of innovation in the origination of consumer credit has been somewhat limited. Laplanche attempted to reinvent it once with the creation of LendingClub. In some ways, it worked. Personal loans originated by fintech lenders account for roughly a third of outstanding consumer loans according to Transunion. Now he’s trying to do it again.

When I first read the press release for the Personal Credit Line, I thought it was a very compelling way to expand the menu of options to qualified consumers. It puts more control in the hands of the borrower, so they can avoid the vicious cycle of consumer debt. I was also reminded of a comment made by Josh Brown, CEO of Ritholtz Wealth Management, after Wealthfront released their “Portfolio Line of Credit” product in April 2017. He said that while it might sound flashy, there’s nothing holding Schwab or Fidelity back from offering the same product tomorrow.

What’s so challenging about consumer-facing fintech companies is that customers are expensive to acquire, they’re difficult to keep, and products are easy to replicate. Providing a free credit score is easily accessible through a partnership with Equifax or Experian. It’s commoditized. The situation is similar with personal financial management tools. This Personal Credit Line seems awfully similar. What’s to stop Chase or Goldman’s Marcus from offering an identical product, perhaps with even better rates? U.S. Bank just launched a similar product, albeit for a different use case, called Simple Loan. It’s a $100 to $1,000 loan marketed as a payday lending alternative, with a roughly 20% lower interest rate than typical payday lender offers.

There is something to be said for being first to market, but ease of replication limits the defensibility of that position. There is a clear interest in an expansion into new products, which will continue to help Upgrade to differentiate the value proposition to consumers, and maybe one day small businesses. The unfortunate reality is that bigger players with an existing customer base and a lower cost of capital are on their tail.

Renaud Laplanche rings the bell with his team at LendingClub (DON EMMERT/AFP/Getty Images)

The real insight that distinguishes Upgrade from LendingClub is the profile of the users. On the supply side of the marketplace, Upgrade only welcomes institutional investors. LendingClub was, and still is, marketed to individuals and institutions.

The peer-to-peer model turned out to be a little too idealistic to serve as the foundation for a business. The concept of a marketplace is really attractive – the ability to invest in others, as cliché as that may sound, has a philanthropic twist to it that even implies a social good. Or, at the very least, an alignment of interests. Except interests aren’t aligned because of the mercurial nature of retail investors, which makes for unstable sources of capital.

LendingClub’s original business model, in the pure P2P form, was reliant on the ability to create a new asset class. The notion of investing in consumer credit may sound compelling, and return prospects may be even more appealing. But, you can’t bootstrap an asset class and base a business model around retail adoption. LendingClub had to solve for distribution of their service, as well as the dissemination of the broader concept of unsecured consumer lending as an asset class.

On Laplanche’s second go around with Upgrade, there’s no more promise of democratization of a new asset class. Instead, large multi-billion-dollar credit investors own the supply side of the marketplace. As a result, there’s a more stable capital base of institutional investors who know what they’re investing in and the reason why they’re investing in it.

What Laplanche did this time around was base his business model around stability. In this market it can pay to be a follower. LendingClub touts the notion that they have “brought a new asset class to investors,” but that education campaign came at a serious cost. It also invited boiler room-like sales behavior from competitors. Upgrade is stepping in after a decade of marketing to scale an untested industry to the masses. Fortunately, a lot of the work has already been done for them.

Upgrade is led by as experienced and forward-thinking of a leader as they come in the marketplace lending industry. They expect to originate over $2 billion loans in 2018 and hit profitability by year-end as well. They’re redefining convention when it comes to consumer credit products.

The question, however, remains: how long can the novelty last? Consumer fintech is fiercely competitive. It’s also increasingly occupied by incumbents with far lower costs of capital, large existing customer bases, and the ability to experiment in a way that a startup cannot. The unsecured consumer lending space has attracted mountains of capital in the past five years, but the opportunity is clearly defined. The number of lenders issuing more than 10,000 personal loans per year has more than doubled since 2011.

There’s a network effect component to marketplace lending businesses, particularly as lenders are able to maintain more connected relationships with consumers. But when it comes to standing apart from the rest of the pack, a differentiated product offering isn’t a very wide moat.

Powered by WPeMatico

Earlier this year we saw the headlines of how the users of popular voice assistants like Alexa and Siri and continue to face issues when their private data is compromised, or even sent to random people. In May it was reported that Amazon’s Alexa recorded a private conversation and sent it to a random contact. Amazon insists its Echo devices aren’t always recording, but it did confirm the audio was sent.

The story could be a harbinger of things to come when voice becomes more and more ubiquitous. After all, Amazon announced the launch of Alexa for Hospitality, its Alexa system for hotels, in June. News stories like this simply reinforce the idea that voice control is seeping into our daily lives.

The French startup Snips thinks it might have an answer to the issue of security and data privacy. Its built its software to run 100% on-device, independently from the cloud. As a result, user data is processed on the device itself, acting as a potentially stronger guarantor of privacy. Unlike centralized assistants like Alexa and Google, Snips knows nothing about its users.

Its approach is convincing investors. To date, Snips has raised €22 million in funding from investors like Korelya Capital, MAIF Avenir, BPI France and Eniac Ventures. Created in 2013 by 3 PhDs, and now employing more than 60 people in Paris and New York, Snips offers its voice assistant technology as a white-labelled solution for enterprise device manufacturers.

It’s tested its theories about voice by releasing the result of a consumer poll. The survey of 410 people found that 66% of respondents said they would be apprehensive of using a voice assistant in a hotel room, because of concerns over privacy, 90% said they would like to control the ways corporations use their data, even if it meant sacrificing convenience.

“Сonsumers are increasingly aware of the privacy concerns with voice assistants that rely on cloud storage — and that these concerns will actually impact their usage,” says Dr Rand Hindi, co-founder and CEO at Snips. “However, emerging technologies like blockchain are helping us to create safer and fairer alternatives for voice assistants.”

Indeed, blockchain is very much part of Snip’s future. As Hindi told TechCrunch in May, the company will release a new set of consumer devices independent of its enterprise business. The idea is to create a consumer business that will prompt further enterprise development. At the same time, they will issue a cryptographic token via an ICO to incentivize developers to improve the Snips platform, as an alternative to using data from consumers. The theory goes that this will put it at odds with the approach used by Google and Amazon, who are constantly criticised for invading our private lives merely to improve their platforms.

As a result Hindi believes that as voice-controlled devices become an increasingly common sight in public spaces, there could be a significant shift in public opinion about how their privacy is being protected.

In an interview conducted last month with TechCrunch, Hindi told me the company’s plans for its new consumer product are well advanced, and will be designed from the beginning to be improved over time using a combination of decentralized machine learning and cryptography.

By using blockchain technology to share data, they will be able to train the network “without ever anybody sending unencrypted data anywhere,” he told me.

And ‘training the network” is where it gets interesting. By issuing a cryptographic token for developers to use, Hindi says they will incentivize devs to work on their platform and process data in a decentralized fashion. They are starting from a good place. He claims they already have 14,000 developers on the platform who will be further incentivized by a token economy.

“Otherwise people have no incentive to process that data in a decentralized fashion, right?” he says.

“We got into blockchain because we’re trying to find a way to get people to participate in decentralized machine learning. We’ve been wanting to get into consumer [devices] for a couple of years but didn’t really figure out the end goal because we had always had this missing element which was: how do you keep making it better over time.”

“This is the main argument for Google and Amazon to pretend that you need to send your data to them, to make the service better. If we can fix this [by using blockchain] then we can offer a real alternative to Alexa that guarantees Privacy by Design,” he says.

“We now have over 14000 developers building for us and that’s really completely organic growth, zero marketing, purely word of mouth, which is really nice because it shows that there’s a very big demand for decentralized voice assistance, effectively.”

It could be a high-risk strategy. Launching a voice-controlled device is one thing. Layering it with applications produced by developed supposedly incentivized by tokens, especially when crypto prices have crashed, is quite another.

It does definitely feel like a moonshot idea, however, and we’ll really only know if Snips can live up to such lofty ideals after the launch.

Powered by WPeMatico

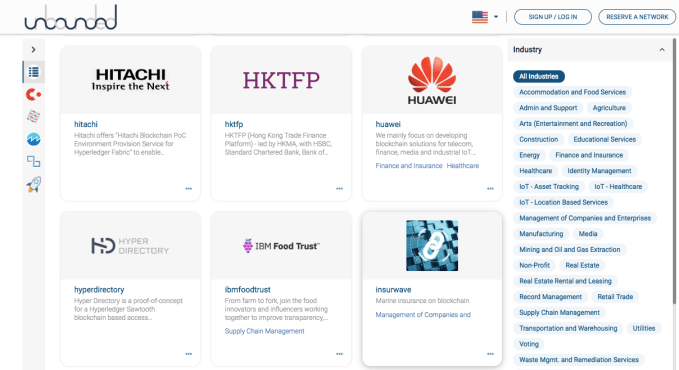

In the 1990s when the web was young, companies like Yahoo, created directories of web pages to help make them more discoverable. Hacera wants to bring that same idea to blockchain, and today it announced the launch of the Hacera Network Registry.

CEO Jonathan Levi says that blockchains being established today risk being isolated because people simply can’t find them. If you have a project like the IBM -Maersk supply chain blockchain announced last month, how does an interested party like a supplier or customs authority find it and ask to participate? Up until the creation of this registry, there was no easy way to search for projects.

Early participants include heavy hitters like Microsoft, Hitachi, Huawei, IBM, SAP and Oracle, who are linking to projects being created on their platforms. The registry supports projects based on major digital ledger communities including Hyperledger, Quorum, Cosmos, Ethereum and Corda. The Hacera Network Registry is built on Hyperledger Fabric, and the code is open source. (Levi was Risk Manager for Hyperledger Fabric 1.0.)

Hacera Network Registry page

While early sponsors of the project include IBM and Hyperledger Fabric, Levi stressed the network is open to all. Blockchain projects can create information pages, not unlike a personal LinkedIn page, and Hacera verifies the data before adding it to the registry. There are currently more than 70 networks in the registry, and Hacera is hoping this is just the beginning.

Jerry Cuomo, VP of blockchain technologies at IBM, says for blockchain to grow it will require a way to register, lookup, join and transact across a variety of blockchain solutions. “As the number of blockchain consortiums, networks and applications continues to grow we need a means to list them and make them known to the world, in order to unleash the power of blockchain,” Cuomo told TechCrunch. Hacera is solving that problem.

This is exactly the kind of underlying infrastructure that the blockchain requires to expand as a technology. Cuomo certainly recognizes this.”We realized from the start that you cannot do blockchain on your own; you need a vibrant community and ecosystem of like-minded innovators who share the vision of helping to transform the way companies conduct business in the global economy,” he said.

Hacera understands that every cloud vendor wants people using their blockchain service. Yet they also see that to move the technology forward, there need to be some standard ways of conducting business, and they want to provide that layer. Levi has a broader vision for the network beyond pure discoverability. He hopes eventually to provide the means to share data through the registry.

Powered by WPeMatico

Let the computers do the legal busy work so attorneys can focus on complex problem solving for their clients. That’s the lucrative idea behind Atrium LTS, Twitch co-founder Justin Kan’s machine learning startup that digitizes legal documents and builds applications on top to speed up fundraising, commercial contracts, equity distribution and employment issues. For example, one of its apps automatically turns startup funding documents into Excel cap tables.

Automating expensive legal labor has led to a rapid rise to 110 employees and 250 clients for Atrium, including startups like Bird and MessageBird. Atrium only came of stealth a year ago with a $10.5 million party round before going into Y Combinator last winter. Today it announces it’s raised a $65 million round led by Andreessen Horowitz.

In characteristic dude fashion, Kan tells me “I’m pretty stoked about that because of having more resources for Atrium.” The venture firm’s partner Andrew Chen is taking a board seat and famed co-founder Marc Andreessen is joining as a board observer. “I wanted a visionary who’s always going to be pushing us to build something really big,” Kan says. General Catalyst, YC’s Continuity Fund and Ashton Kutcher’s Sound Ventures are also joining the round.

With the massive influx of cash, Atrium will be able to develop more internal tools it can use to crank out client work faster than its traditional competitors. “We can ultimately be this platform on top of which you’re building these legal businesses and eventually other professional services and software services,” Kan explains.”They’re all sitting on top of the platform that understands legal documents.”

In more Atrium news, Y Combinator’s leading partner Michael Seibel will join the startup’s board, too. And it’s acquired Tetra, a YC artificial intelligence startup that had raised $1.5 million to analyze voice, “to help us build our platform that understands and structures data,” Kan tells me.

What Kan didn’t initially mention is that two of Atrium’s co-founders, CTO Chris Smoak and legal partner BeBe Chueh, have left. He later admitted they had transitioned out of the company several months before the new funding. “BeBe wanted to spend time working on family (she just got engaged); Chris and I disagreed on his job role” regarding the definition of the CTO position, Kan tells me. He’ll now be running Atrium with remaining co-founder Augie Rakow, formerly of mega-law firm Orrick, and Kan’s long-term business partner and former McKinsey analyst Nick Cortes.

Justin Kan (Atrium) at TechCrunch Disrupt SF 2017

The law firm business model has left the door open for disruption by technology companies like Atrium. “Law firms generate revenue from hourly billing, and lack an incentive to vastly improve efficiency,” Chen writes. “Many law firms dividend out all their profits at the end of each year, making it hard to invest in the expensive investment of building software. Software is hard to build inside a software company, much less a law firm.”

But Atrium is an engineering company with a legal clientele. It takes the most common and time-consuming activities — often related to ingesting mountains of documents — and builds machine learning workarounds. Atrium’s lawyers can focus on advising their clients on what to do, rather than burning the midnight oil doing it as they look for tiny quirks in the paperwork. The legal services get faster, cheaper and more predictable, so Atrium can offer upfront pricing. It’s been using fundraising workshops and other educational materials to drum up leads.

For now, Atrium’s tech is limited to a narrow band of use cases. But “over $300 billion is spent per year in the enterprise legal market,” Chen writes, so there’s plenty of room to grow now that Atrium is well capitalized. It will have to convince big corporations to ditch the old way and let computers lend a hand. Luckily, Atrium isn’t a SAAS company forcing clients to use the tech themselves. Done right, they shouldn’t even know that it’s machine vision software, not junior associates, pouring over their docs. It will have to out-match fellow legal tech startups like Ravel, CaseText, Judicata, Premonition and more, though they’re often just tools rather than software-equipped law firms.

Kan also cops to his lack of experience in legal. “I think for any full stack vertical startup started by a non-subject matter expert (i.e. me who is not a lawyer), there is a risk that you come in and are very prescriptive on how things work. Then you build software that says ‘the providers must do it this way!’,” Kan tells me. “But the practical reality is that it doesn’t work with the nuanced, non-linear workflows that providers already have. So the technology doesn’t get adopted and fails to provide value. That to me is the biggest upcoming risk.”

Justin Kan, from lifevlogger to legal giant

Yet if Atrium can ease clients into this new world service by service, it could generate network effects that fuel the whole business. It’s just a matter of prioritization. “One of the things I always need to be focused on is…focusing. That’s sometimes a blind spot.” From Justin.tv to Twitch to its acquisition by Amazon to his role as YC partner, Kan delivers, but can be frenetic. “As an entrepreneur, I have a tendency to take on too much.”

But after leaving YC because “I had felt like I’d stopped learning,” Kan has found the legal space so full of knowledge and opportunity that it can hold his attention. “Part of why I like this business is because it was so different. I didn’t think it was something that would be as easily competed with,” Kan recalls. “I had this calendar company and Google came out with something similar. I told [Twitch co-founder] Emmett ‘We have to do something no one can compete with. At least Google will never do this.’ Then they did.”

But unlike with that game streaming startup, Atrium doesn’t have to worry about beating or getting bought by some legal tech giant. Instead, it wants to become one.

Powered by WPeMatico

Brian Armstrong, the CEO of cryptocurrency trading platform Coinbase, wants to take his company public — maybe on the blockchain.

Onstage at TechCrunch Disrupt SF 2018, Armstrong dished on his ambitions for the future of Coinbase.

“We are self-sustaining,” Armstrong said. “You know, we’ve been profitable for quite a while. We don’t have any plans to raise additional capital at this point, but never say never … Someday I’d love to run a public company.”

Armstrong didn’t rule out going public on the blockchain. He said he’s even considered going public on his own platform.

“I think it would be very on mission for us to do that because, of course, we are creating an open financial system,” he said. “Companies could list their stock, which are really tokens, and instead of a cap table, you tokenize the cap table. But I don’t have any decisions on that to share at the moment.”

An innovative exit would be very on-brand for Coinbase. As one of the earliest players in crypto-mania, the company has certainly had to make things up as it goes. It’s worked, as Armstrong said; the company is profitable and was the first-ever cryptocurrency startup to garner a billion-dollar valuation.

Founded in 2012, Coinbase is backed by IVP, Spark Capital, Greylock Partners, Battery Ventures, Section 32, Draper Associates and more. The company was valued at $1.6 billion in August 2017 with a $100 million Series D last year. The financing was reportedly the largest-ever for a crypto startup.

Watch the full interview with Brian Armstrong below.

Powered by WPeMatico

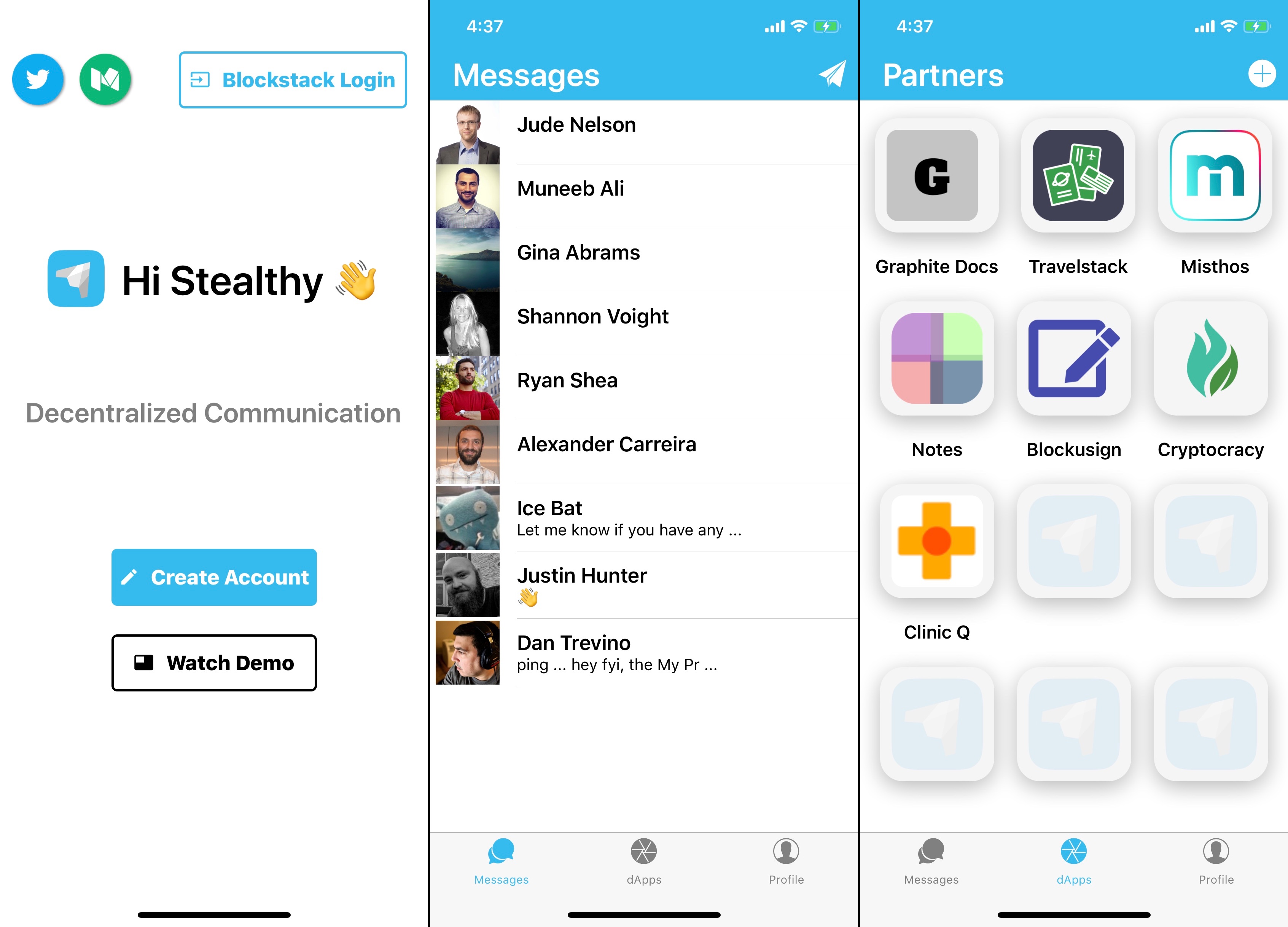

Meet Stealthy a new messaging app that leverages Blockstack’s decentralized application platform to build a messaging app. The company is participating in TechCrunch’s Startup Battlefield at Disrupt SF and launching its app on iOS and Android today.

On the surface, Stealthy works like many messaging apps out there. But it gets interesting once you start digging to understand the protocol behind it. Stealthy is a decentralized platform with privacy in mind. It could become the glue that makes various decentralized applications stick together.

“We started Stealthy because Blockstack had a global hackathon in December of last year,” co-founder Prabhaav Bhardwaj told me. “We won that hackathon in February.” After that, the #deletefacebook movement combined with the overall decentralization trend motivated Bhardwaj and Alex Carreira to ship the app.

Blockstack manages your identity. You get an ID and a 12-word passphrase to recover your account. Blockstack creates a blockchain record for each new user. You use your Blockstack ID to connect to Stealthy.

Stealthy users then choose how they want to store their messages. You can connect your account with Dropbox, Amazon Web Services, Microsoft Azure, etc.

Every time you message someone, the message is first encrypted on your device and sent to your recipient’s cloud provider. Your recipient can then open the Stealthy app and decrypt the message from their storage system.

All of this is seamless for the end user. It works like an iMessage conversation, which means that Microsoft or Amazon can’t open and read your messages without your private key. You remain in control of your data. Stealthy plans to open source their protocol and mobile product so that anybody can audit their code.

Some features require a certain level of centralization. For instance, Stealthy relies on Firebase for push notifications. If you’re uncomfortable with that, you can disable that feature.

The company also wants to become your central hub for all sorts of decentralized apps (or dapps for short). For instance, you can launch Graphite Docs or Blockusign from Stealty. Those dapps are built on top of Blockstack as well, but Stealthy plans to integrate with other dapps that don’t work on Blockstack.

“We have dapp integrations in place right now and we want to make it easier to add dapp integrations. If somebody wants to come in and start selling messaging stickers, you could do that. If you want to come in and implement a payment system to pay bloggers, you could do that,” Bhardwaj said. “Eventually, what we want to be is to make it as easy as submitting an app in the App Store.”

When you build a digital product, chances are you’ll end up adding a messaging feature at some point. You can chat in Google Docs, Airbnb, Venmo, YouTube… And the same is likely to be true with dapps. Stealthy believes that many developers could benefit from a solid communication infrastructure — this way, other companies can focus on their core products and let Stealthy handle the communication layer.

Stealthy is an ambitious company. In many ways, the startup is trying to build a decentralized WeChat with the encryption features of Signal. It’s a messaging app, but it’s also a platform for many other use cases.

A handful of messaging apps have become so powerful that they’ve become a weakness. Governments can block them or leverage them to create a social ranking. Authorities can get a warrant to ask tech companies to hand them data. And of course, the top tech companies have become too powerful. More decentralization is always a good thing.

Powered by WPeMatico