blockchain

Auto Added by WPeMatico

Auto Added by WPeMatico

To paraphrase a saying popularized by countless dorm room stoners: “First they ignore you, then they laugh at you, then they fight you, then you use the hype around decentralized crypto economies to sell bacon.” The latest example of this age-old adage comes to us from Oscar Meyer and involves their exciting new cryp-faux-currency, Bacoin.

The currency can be redeemed for bacon and you “mine” it by sharing the good news of bacoin with your friends. Instead of taking up massive amounts of electricity, the production of the final store of value – pig parts – requires only a massive agricultural system dedicated to the wholesale destruction of mammals that are as smart as dogs and, in the right context, quite cute. The end product, bacon, is considered by many to be far more interesting than anything Vitalik created. In short, it’s a win-win.

How does it work? It’s basically a sweepstakes. From the rules and regulations:

The value of the Bacoin is tied to overall sharing meaning that the more people who share via the Website (as outlined above), the higher the value of the Bacoin. If overall sharing is slow, the value of the Bacoin will decrease. If sharing is slow and the value of the Bacoin is low, Sponsor may increase value of Bacoin in its sole discretion. The current value of the Bacoin will be displayed on the Website. Once the Bacoin is at a value you want, follow the instructions to “cash out” and you will receive a coupon with the corresponding value (all possible values of the Bacoin coupon are outlined in Section 4 below).

The current value of a single mined bacoin is about 28 slices of bacon and the more you share the more you mine. Given that it is in no way a decentralized cryptocurrency and has nothing to do with anything technical at all I’m hard pressed to find a reason to post this here except to admire the sheer chutzpah of a company who knows exactly what breed of Reddit-loving bacon eater will jump at a chance to Tweet about pork products. To paraphrase another saying by my friend Nicholas Deleon: I hope the asteroid they promised comes for us all soon.

Bacoin. Yeah.

Powered by WPeMatico

Mike Cagney, who was ousted last summer from the lending company he founded, is back with a new startup and a whole lot of funding from at least one of his previous investors.

According to a new report in Bloomberg, Cagney, who earlier this year formed a new lending startup called Figure, has raised $50 million to grow the company, which plans to use the blockchain to facilitate loan approvals in minutes instead of days.

According to the company’s site, its lending products will include home equity lines of credit, home improvement loans and home buy-lease back offerings for retirement.

The round was led by DCM Ventures and Ribbit Capital and included participation from Mithril Capital Management, Cagney confirmed to Bloomberg.

Ribbit Capital in Palo Alto, Calif., has been leading investments in the world of fintech and digital currencies since its founding nearly six years ago. Others of its many bets include the online consumer lending company Affirm, and Point, a startup that buys equity in U.S. homes.

Mithril, co-founded by Peter Thiel, prides itself on funding companies that take time to build, with funds that have longer investing timelines than do most traditional venture vehicles.

The cross-border firm DCM Ventures, meanwhile, is perhaps the most interesting participant in this round. The reason: Back in 2012, DCM began investing in Social Finance, or SoFi, the company that Cagney founded previously.

It isn’t uncommon for VCs to invest in founders with whom they’ve worked before, of course. And SoFi has grown by leaps and bounds since its August 2011 launch. Though it initially focused on refinancing student loans, today it provides personal and mortgage loans and wealth management services, and it appears to be pushing further into other bank-like services.

But Cagney was forced out of the company last summer, not long after a sexual harassment lawsuit was filed by a former employee who claimed he’d witnessed female employees being harassed by managers and was fired after he reported it.

Another former employer who’d been stationed at SoFi’s office in Healdsburg, Calif., told The New York Times that her work environment had been akin to a “frat house,” with employees “having sex in their cars and in the parking lot.” That same story, based on conversations with 30 then-current and former employees, also reported that Cagney himself had raised questions with staff because of his own behavior, including bragging about his sexual conquests.

Evidently, DCM and Figure’s other backers were able to brush aside concerns about anything of the sort happening again at Figure. (We’ve reached out to Cagney and Figure’s investors for more information.)

Employees are also flocking for Figure with the belief, ostensibly, that Cagney is well-positioned to create another financial services juggernaut. According to Bloomberg, the company has already quietly assembled a team of 56 people. Among its new hires is the former chief risk officer of LendingHome, Cynthia Chen, and the former chief legal counsel of PeerStreet, Sara Priola.

Powered by WPeMatico

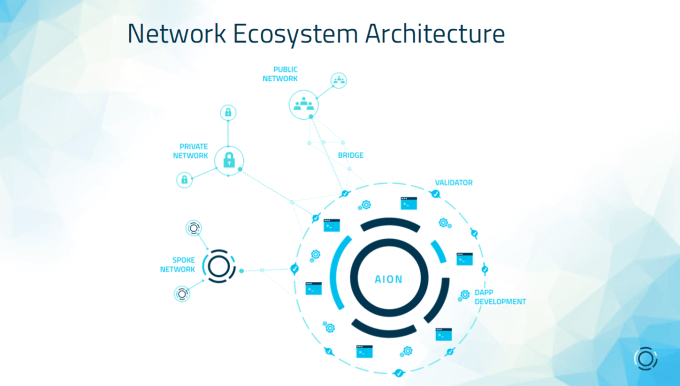

If you believe blockchains will proliferate in the coming years, it stands to reason that you will need some sort of mechanism to move information between them — a network of blockchains with bridges and processes for sharing information between entities. That is exactly what The Aion Network is providing with a new blockchain network released today.

The company wants to be the underlying infrastructure for a network of blockchains in a similar way that TCP/IP drove the proliferation of the internet. To that end, the company, which originally began as a for-profit startup called Nuco, has decided to become a not-for-profit organization with the goal of setting up protocols for a set of interconnected blockchains. They now see their role as something akin to the Linux Foundation, helping third-party companies build products and creating an ecosystem around their base technology.

Graphic: Aion Networks

“The core design of network we have been building is to connect various networks, and route data and transactions through a public network. We are launching that network today. It allows you to build bridges to other blockchain networks. That public network acts as relayer between blockchains,” Matthew Spoke, CEO and co-founder at Aion Networks told TechCrunch.

While there clearly could be security concerns with a public by-way for blockchain data moving between systems, Spoke says that can be minimized. Instead of transmitting a medical record between a hospital and insurance company, you send a proof that the person had an operation, which the insurance company can check against the coverage rules it has created for that individual and vice versa.

The idea behind this venture is to provide the underlying plumbing to encourage more highly scalable blockchain use cases. Spoke and his team once ran the blockchain practice at Deloitte before starting this venture, and they saw roadblocks to scaling first-hand. “When we were doing enterprise projects, our biggest realization was that the plumbing wasn’t sophisticated enough. The scaling wasn’t meeting specs that enterprise companies would need long-term. Because of that, we were not seeing anyone moving beyond proof of concept projects. What we are doing is trying to mature the possible use cases,” he said.

In order to drive adoption, the company is introducing a token or cryptocurrency to be used to move data across the network and build in a level of trust. Spoke believes if the users have skin in the game in the form of tokens, that could create a higher level of trust on the system.

“Instead of paying for infrastructure, you are going to pay to be part of a common trusted protocol. It comes down to the mechanism of consensus and being incentivized to do business in an honest way,” Spoke said

This is probably not something that will get adopted widely overnight. Just because they have built it, they still require a level of utilization for it to really take off, and that will require more blockchain projects. “We still need a few years of pure focus on infrastructure to make sure we are getting these layers right. Every time you move data of any kind there are security vulnerabilities, and we need to make sure there are good specs and comfort in using it,” he said.

Powered by WPeMatico

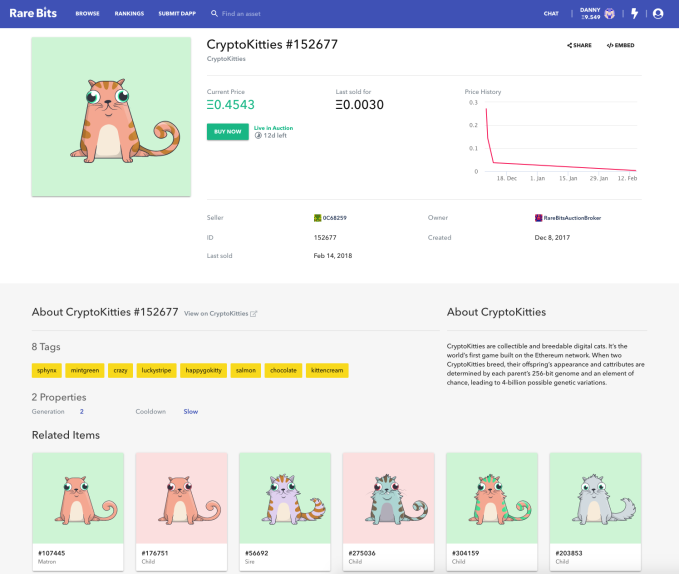

Rare Bits wants to be eBay for the blockchain, where you buy, sell and trade non-fungible crypto-goods. After CryptoKitties raised $12 million from Andreessen Horowitz last month for its digital collectibles game, there’s been an explosion of interest in the space. But without a popular marketplace, it’s hard to find the goods you want at the right price. Now a team of former Zynga staffers is building out the Rare Bits crypto-collectible auction and commerce site with a $6 million round led by Nabeel Hyatt at Spark Capital, and joined by First Round Capital, David Sacks’ Craft Ventures and SV Angel.

“Because of the Ethereum ledger, for the first time, users can truly own their digital items,” says co-founder Amitt Mahajan. “Previously in mobile or social games, virtual items earned through play or by spending money were actually owned by the company operating the game. If they shut down their servers, the items would go away and users would be out of luck. We believe this new asset class represents a paradigm shift in digital property whereby centralized assets will be moved onto decentralized systems.”  For now, Rare Bits isn’t slapping any extra fees on its marketplace, compared to paying up to 1 percent on other marketplaces like Open Sea, or even more elsewhere. Instead, if a crypto-item developer charges a fee on secondary sales, say 5 percent, they’ll split that with Rare Bits for arranging the transaction.

For now, Rare Bits isn’t slapping any extra fees on its marketplace, compared to paying up to 1 percent on other marketplaces like Open Sea, or even more elsewhere. Instead, if a crypto-item developer charges a fee on secondary sales, say 5 percent, they’ll split that with Rare Bits for arranging the transaction.

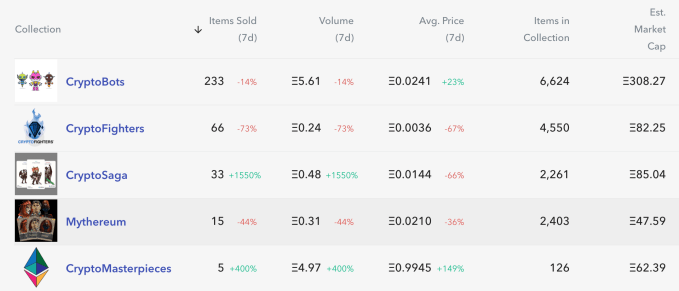

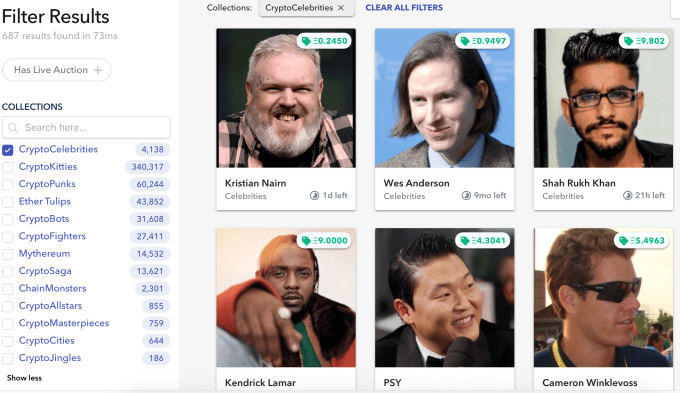

Rare Bits lists more than 500,000 items from a dozen games, including CryptoPunks, Ether Tulips, CryptoBots, CryptoFighters, Mythereum and CryptoCelebrities. Users get the benefit of having all their crypto-collectibles in a single wallet. They can see historical pricing before they buy anything thanks to the transparency of the Ethereum ledger, whether they want to “Buy Now” or win an auction. The collectors can also see related items rather than transacting in a vacuum. One item sold for more than $10,000, and sales in the 5-10ETH range ($555 each today) aren’t uncommon.

Rare Bits founders from left: Danny Lee, Payom Dousti, Dave Pekar and Amitt Mahajan

Mahajan, Danny Lee and Dave Pekar all met after selling their gaming startups to Zynga . [Disclosure: I know Pekar from college.] Their fourth co-founder, Payom Dousti, worked at fintech VC fund 1/0 Capital and sold his sports analytics startup numberFire to FanDuel. With experience across the gaming, virtual goods and crypto space, Mahajan tells me, “We thought long and hard about potentially building blockchain-based games ourselves, but ultimately decided that there was a larger opportunity in focusing on crypto-based property as a whole.” The Rare Bits exchange launched in February and did more than $100,000 in transactions in its first month.

With some CryptoKitties selling elsewhere for as much as $200,000, investors liked the idea of taking a cut of everyone’s transactions rather than just launching another digital trading card. That led Rare Bits to raise a $1 million seed from Macro Ventures and angels like Steve Jang and Robin Chan. As scaling issues threaten to prevent the Bitcoin and Ethereum blockchains from supporting micropayments and mainstream commerce, new use cases like crypto-collectibles are taking the spotlight.

Now with the $6 million Series A, Rare Bits is bringing in some heavyweight angels from the world of gaming. That includes Emmet Shear and Justin Kan, the co-founders of Twitch. Former Dropbox execs and married couple Ruchi Sanghvi and Aditya Agrawal are also in the round, alongside Greenoaks Captial MD Neil Mehta and Channel Factory CEO Tony Chen.

The team hopes the runway will help it secure partnerships with developers and creatives to publish new collectibles for the blockchain that have a home on Rare Bits. Mahajan says, “People are viewing these items as assets that can be invested in instead of liabilities that are one way transfers of value towards the developer, it’s one of the major changes in this ecosystem versus traditional virtual items.”

Rare Bits will have to deal with the inherent scaling troubles of the Ethereum blockchain it operates on. For now, it’s refunding users the “gas” it costs to execute purchases and sales on its marketplace in a timely manner. Those range from a few cents to a few dollars, depending on network congestion. But Rare Bits could be looking at a steep bill or be forced to push those fees onto users if it gets popular enough.

There’s always the danger that CryptoKitties and the like are just the new Beanie Babies — valued today, but worthless when the fad dies. Rare Bits benefits from getting to follow the trend to whatever crypto-collectible is in vogue, and just has to hope the whole concept doesn’t fade.

But Rare Bits has a hedge against that. “While today most of these items are items from games and collectibles, we envision that we will see licenses, tickets, rights, even tokenized physical goods represented as digital assets,” Mahajan tells us. It’s now building a Fan Bits feature that will let YouTube creators, Twitch streamers and Instagram celebrities create crypto-based collectibles “to engage with their audience and let their fans support them,” he explains. You might one day be able to buy and resell a meet-and-greet pass for your favorite band.

“Our ultimate goal is to convince millions of new people to begin owning and transacting crypto-based property,” says Mahajan. But the founders will probably be okay regardless. “Like anyone crazy enough to start a crypto app company this early, we started buying and HODLing BTC and ETH years ago.”

Powered by WPeMatico

It looks like at least one major news publisher is on-board with Brave, the ad-blocking web browser founded by former Mozilla CEO Brendan Eich.

Brave Software and Dow Jones Media Group announced today they will be partnering in a deal that will bring Media Group content (specifically, full access to Barrons.com or a premium MarketWatch newsletter) to “a limited number of users who download the Brave browser on a first-come, first-serve basis.”

In addition, Barron’s and MarketWatch are becoming verified publishers on Brave’s Basic Attention Token (BAT) platform, a blockchain-based system that will allow consumers and eventually advertisers to pay publishers. (Brave had a hugely successful initial coin offering last year.)

And the companies said they will be working together to experiment with different ways to use blockchain technology in media and advertising.

“As global digital publishers, we believe it is important to continually explore new and emerging technologies that can be used to build quality customer experiences,” said Barron’s Senior Vice President Daniel Bernard in the announcement.

To be clear, the partnership just involves the Dow Jones Media Group, not the larger Dow Jones organization (which is best-known for publishing The Wall Street Journal). And the language that the companies are using suggests that they’re very much approaching this as an experiment.

But it’s certainly a dramatic change in tone from the way most publishers talk about ad-blockers. In fact, a group of newspapers (including the Journal) published a letter two years stating that Brave’s business model was “indistinguishable from a plan to steal our content to publish on your own website.”

Brave also recently announced the launch of a referral program that rewards creators with BAT when they convince their fans to switch over to the browser. In the same announcement, the company said it has 2 million monthly active users.

Update: The headline and story have been rewritten to clarify the distinction between the Dow Jones Media Group and the larger Dow Jones organization.

Powered by WPeMatico

things")

Startup life is full of quick, lateral thinking. “Move fast and break things” is the mantra. However, with the rise of token sales – essentially vehicles for untested startups to raise millions in a few minutes – lots of stuff gets broken and little gets fixed.

Take BCT – the Blockchain Terminal – for example. This frothy project led by Bob Bonomo, a former hedge fund guy turned Blockchain guru, features some interesting breakages.

Yesterday at about 3pm Eastern Time the company’s FAQ – which has since been updated but is still hidden here – read something like this:

While this sort of techno greeking is fine if you’re sending mock-ups back and forth, the token sale had been running since April 1st, a fact that was baffling to me and another reporter. Was this an April Fool’s joke? No, because when I visited the sale’s Telegram room I found a group of happy buyers asking questions about their future tokens.

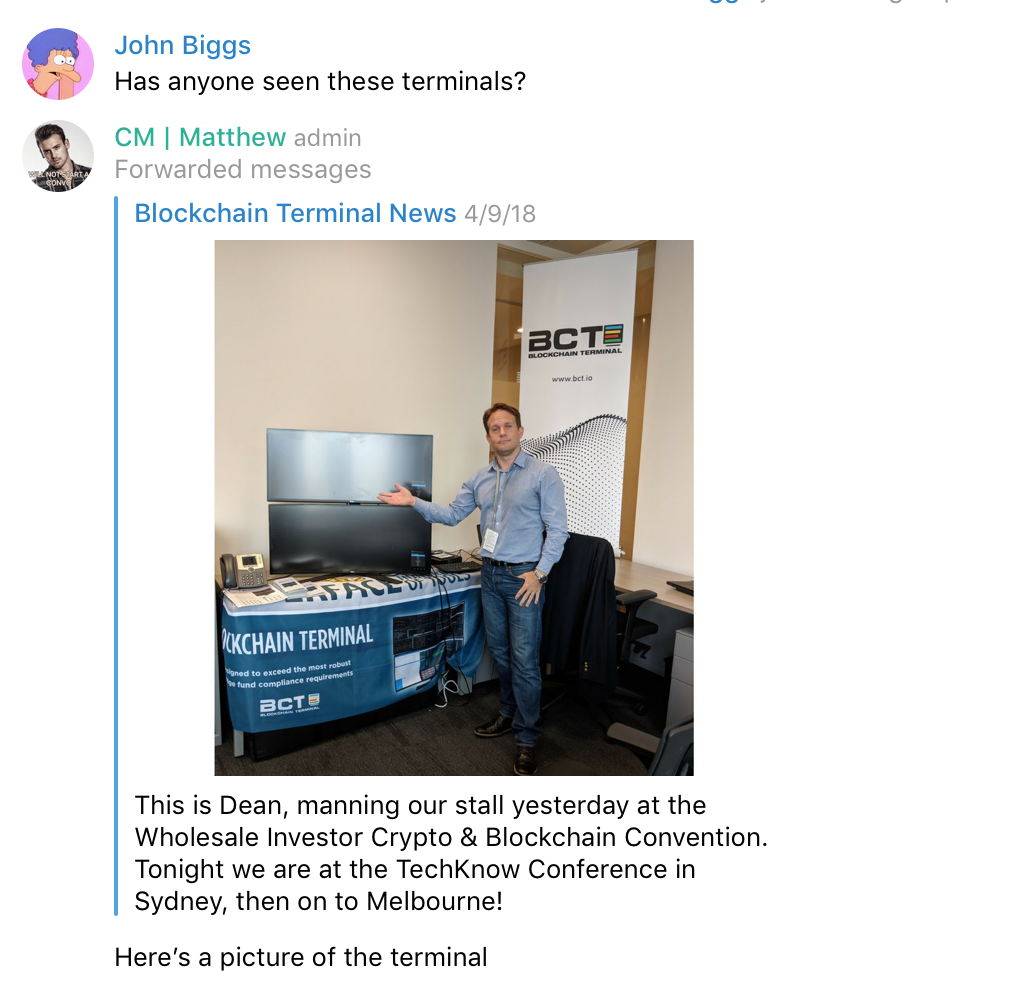

Ever the reporter, I asked if anyone had seen the terminals and a community manager sent me this:

Interesting… blank screens at a demo event. The other CM, quicker on the draw, sent this:

Fair enough. In fact, crypto needs a product like this to legitimize it with Wall Street. But clearly they were moving so fast that the wheels were falling off.

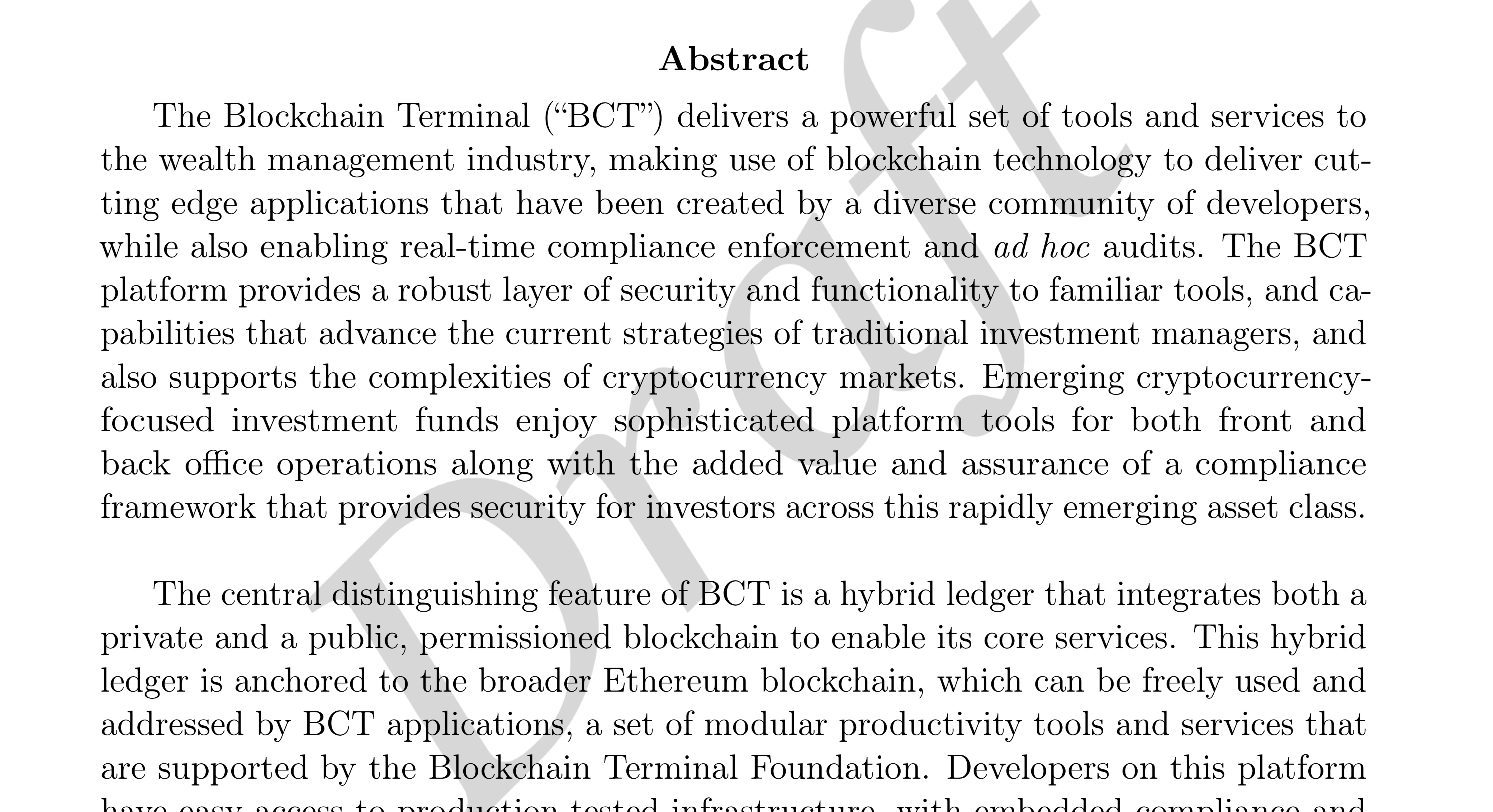

Finally I did the obvious thing: visit the white paper. There we find that the Terminal is being built in conjunction with FactSet, a venerable research company that has seen all the vicissitudes of financial data. In fact, the paper is a tour-de-force on par with the best of the white papers I’ve seen. But we also discover that the white paper is a draft.

In short, BCT wouldn’t pass the average human investor sniff test but is definitely well on the way to completing its token sale. This is a problem.

BCT is not alone. I’ve spoken to development houses working with founders who barely understand cryptocurrency let alone understand their own token sales. I’ve seen founders’ eyes light up like the Big Bad Wolf eyeing Porky Pig when they talk about all the capital they will unlock. And I spoke to a founder on stage who said he would be very careful with the $80 million they raised for a company designed to raise money for ICOs. Greed is clouding this market in ways that are at once dangerous and comical.

There is precedent for this. In the early days of the Internet and even the frothiest dot-com days you could see the avarice in the eyes of Pets.com and Cisco executives who knew that big money was just around the corner. And we can’t begrudge these founders their excitement. What founder wouldn’t want the sweet feeling of being fully funded for, we presume, the next decade?

I’ve been following token sales with great interest over the past few months for a few reasons. First, I understand the hype cycle. I’ve seen tactics used by token sellers used before by hardware sellers, most notably with flops like the Phantom gaming console and the Notion Ink Adam, and there is a stink that permeates projects that are, at best, half-baked.

I want token sales to thrive as a method to raise capital. I want small startups to be able to turn on a spigot previously available to the well-connected and well-heeled. But the exact opposite seems true. Bankers are moving into a technology space that they little understand while carpetbaggers – lawyers, PR folks, advisors – are working hard to extract cash out of these windfalls. In the end the token sale industry should formalize itself and become as boring as the VC industry. I just hope it survives long enough to get there.

Powered by WPeMatico

Sam Kim, co-founder and CEO of Lucidity, said blockchain technology offers a solution to cut down on fraud and bring more transparency to digital advertising.

Kim was previously chief operating officer at The Mobile Majority, a mobile ad company where he said he saw the challenges of reconciling the data used by different parts of the ad supply chain. So at Lucidity, his team has created technology on the Ethereum blockchain for smart contracts that track this data across the ecosystem.

“What we’ve built is a protocol for industry participants to come to a consensus about what events are valid and what are invalid,” he said. “We allow all the participants trafficking that ad to submit that data … so that basically becomes a single source of truth across the industry.”

On top of the protocol, Lucidity has created products focused on specific issues. There’s one around fee transparency, where every participant in the supply chain submits the information about the fee they charged and verification that they actually ran the impression, which Kim said could replace a drawn-out reconciliation process. And there’s another product for confirming publisher identity and flagging fake bid requests.

When I asked whether ad platforms and publishers will feel comfortable sharing this data in a new way, Kim said, “As an industry, there’s a lot of pressure from the advertisers to become more transparent.”

“The way we designed it, it will benefit those who are honest and transparent,” he added. “Those who aren’t, it’ll be harmful to them. We expect to see adoption from those who are completely transparent and honest, and hopefully drive the industry in that direction.”

As for potential privacy concerns, Kim noted that Lucidity doesn’t currently include consumer data. That could change in the future, but if it does, Kim said it would be done in a way that ensured “privacy was addressed.”

Lucidity has been in beta testing since earlier this year, and it’s already signed up partners from the ad world including Audience Group and Digital Remedy.

Kim said the goal is to get “the benefits of the blockchain — disintermediation, transparency and trust — but deployed in a way that’s not cumbersome and difficult for the current players.” So if you’re an advertiser, you don’t need to worry too much about the underlying technology; you just get a dashboard with the data you want.

At the same time, Kim said the company is using “cutting edge technology,” for example by implementing Plasma, a side-chain processing technology that’s supposed to address Ethereum’s speed and scaling issues. And it’s partnered with IAB Tech Lab’s Blockchain Working Group, the Enterprise Ethereum Association and Hyperledger.

The startup was previously known as Kr8os (from the Greek word kratos, which was one of the ingredients for democracy). Today it’s rebranding as Lucidity.

“We’d been thinking about the rebrand for some time,” Kim said. “Kr8os is a process we used to ultimately drive our vision for Lucidity.”

Powered by WPeMatico

Salesforce has always been a company that is looking ahead to the next big technology, whether that was mobile, social, internet of things or artificial intelligence. In an interview with Business Insider’s Julie Bort at the end of March, Salesforce co-founders Marc Benioff and Parker Harris talked about a range of subjects including how the company came to be working on one of the next hot technologies, a blockchain product.

Benioff told a story of being at the World Economic Forum in Switzerland where a bit of serendipity led him to start thinking about blockchain and how it could be used as part of the Salesforce family of products.

As it turned out, there was a crypto conference going on at the same time as the WEF and the two worlds collided at a Salesforce event at the Intercontinental Hotel. While there, one of the crypto conference attendees engaged Benioff in a conversation and it was the start of something.

“I had been thinking a lot about what is Salesforce’s strategy around blockchain, and what is Salesforce’s strategies around cryptocurrencies and how will we relate to all of these things,” Benioff said. He is actually a big believer in the power of serendipity, and he said just by having that conversation, it started him down the road to thinking more seriously about Salesforce’s role in this developing technology.

He said the more he thought about it, the more he believed that Salesforce could make use of Blockchain. Then suddenly something clicked for him and he saw a way to put blockchain and cryptocurrencies to work in Salesforce. “That’s kind of how it works and I hope by Dreamforce we will have a blockchain and cryptocurrency solution.”

Benioff is clearly a visionary and says a lot of that comes from simply paying attention as he did when he talked to this person in Davos, and recognizing an opportunity to expand Salesforce in a meaningful way. “A lot [these ideas] comes from paying attention, listening. There’s new ideas coming all the time,” he said. He recognizes that there are more ideas out there than they can possibly execute, but part of his job is understanding which ones are the most important for Salesforce customers.

Blockchain is the electronic ledger used to track Bitcoin or other digital currencies, but it also has a more general business role. As an irrefutable and immutable record, it can track just about anything of value.

Dreamforce is Salesforce’s enormous annual customer conference. It will be held this year from September 25-28 in San Francisco, and if it all works as planned, they could be announcing a blockchain product this year.

__

Check out the whole interview between Salesforce founders Parker Harris and Marc Benioff and Julie Bort from Business Insider:

Powered by WPeMatico

JPMorgan’s key blockchain executive is departing the bank for the world of startups, it has emerged.

Amber Baldet heads up JPMorgan’s Blockchain Center of Excellence, which explores the development of distributed ledger technology and use cases of blockchain technology across the firm’s business. A high-profile figure in the blockchain space in her own right, she is leaving to start her venture, according to Reuters.

Baldet set up JPMorgan’s blockchain strategy and headed up its enterprise-focused Quorum blockchain, which is reportedly being considered for a spinout. As Baldet’s six-year tenure at the bank ends, she will be replaced by Christine Moy, who led blockchain services across the bank’s Investor Services and Capital Markets segments, according to Fortune.

¯_(ツ)_/¯ https://t.co/5y02V30p2x

— Amber (@AmberBaldet) April 3, 2018

The exit is an example of a talent drain that is beginning to take shape in banking and financial services with engineers and business execs moving over to blockchain and crypto projects that are seen to have serious growth potential.

That’s despite a rocky year to date for crypto, at least in terms of valuations.

Bitcoin reached nearly $20,000 per coin in December but it spent much of March below $10,000. As of today, one bitcoin is worth $7,387, according to Coinmarketcap.com. Top tokens like Ethereum, Litecoin and Ripple are also down significantly on their record January-December prices.

There’s a strong case to be made that a more stable crypto market is for the best, even if there is a loss in value. High prices led to high transaction fees, which made life difficult for developers whilst also adding uncertainty for market speculators and token collectors.

Note: The author owns a small amount of cryptocurrency. Enough to gain an understanding, not enough to change a life. (That’s definitely the case lately.)

Powered by WPeMatico

I’ll be honest: When I first got the pitch for “the first blockchain-based video game console,” I assumed it must be some kind of gimmick.

But Jimmy Chen, co-founder and CEO of Blok.Party, said the Ethereum blockchain is “a critical part of this experience,” allowing his team to create “this seamless bridge between the digital and physical worlds.”

Today, Blok.Party is unveiling its PlayTable console, which combines elements of tabletop and console gaming.

This isn’t the first time someone’s tried to incorporate real-world objects into video games — for example, there was Disney Infinity, which shut down a couple of years ago. But by using blockchain technology, Chen said he can avoid many of the pitfalls that tripped up previous efforts.

For one thing, instead of manufacturing new toys and pieces for every game, PlayTable uses RFID tags, which can be attached to existing objects. So players can use the tags to incorporate their own toys and cards into the games.

“We’ve been trying to make toys smart for a very, very long time, but all we’ve been doing is stuffing resistors and transistors inside of them, making them incresingly more inaccessible,” Chen said. Blok.Party, in contrast, is “creating a data set that is inexpensive, that can easily attach to the physical object.”

He demonstrated PlayTable for me using Battlegrid, a card-based fantasy duel game developed by Blok.Party, which Chen described as “if Magic the Gathering, Hearthstone and Skylanders had a baby.” I won’t pretend that I followed all the ins and outs of the battle, but I saw that Chen could place different cards and pieces down and the table would recognize them and bring the related characters into play.

“The core of it, the physical manifestation of it that exists only in one space, has proven to be fairly difficult [in the past],” Chen added. “By creating that backend infrastructure, we can make the system a lot more successful. The element that blockchain really enables is this idea of having a truly unique, open dataset that people can contribute to and can build on top of.”

Chen said Blok.Party is working with third-party developers to create about 25 different titles, some of them based on classic games like poker and mah jong.

The PlayTable is currently available for pre-order at a discounted price of $349. (The company says the regular price will be $599.) The plan is to ship the console in the fourth quarter of this year.

Powered by WPeMatico