Banking

Auto Added by WPeMatico

Auto Added by WPeMatico

Japanese messaging app company Line is pumping 20 billion JPY ($182 million) into its mobile payment business as it tries to turn things around following a challenging year in 2018.

The company announced the infusion into Line Pay, a subsidiary that it fully owns, in a filing that stated the new capital is “necessary funds for its future business operation.” No further details were provided.

The investment comes on the heels of Line’s latest financial report which saw it post a 5.79 billion JPY loss as revenue grew by 24 percent to reach 207.18 billion JPY in 2018. Line has long been a top money maker in the App Store, but its efforts to build out content around its messaging platform and games division have turned out to be expensive, with a job service, manga platform and e-commerce business among its ventures.

In addition to more content, payments are also seen as “glue” that can increase engagement within the Line ecosystem and its main messaging app.

The company is going after the cashless opportunity in Japan, where it is the dominant chat app with an estimated 50 million registered users. The country is notable for its continued use of cash, but the government is using the upcoming 2020 Olympic Games as an opportunity to move toward a digital future. Aside from its core Line Pay service, which sits inside the Line chat app, Line is introducing its own credit card with Visa and has gone after Chinese tourists through a tie-in with Tencent, the internet giant behind China’s top messaging app WeChat.

Outside of Japan, Line Pay is also available in Thailand (where it works with the Bangkok metro provider), Taiwan (where it counts two banks as partners) and Indonesia, which Line says are its next three largest markets in terms of user numbers. Together, across those four countries, Line claims it has 165 million monthly active users and 40 million registered Line Pay users. Line said GMV reached 55 billion JPY ($482 million) per month back in November 2017; there’s been no update since.

The service was launched more widely but it has shuttered in other markets, including Singapore where it was ended in February 2018.

Beyond payment, Line is also moving into banking and financial services. It is working to launch a digital bank in Japan and last year it announced plans to investigate the potential to roll out loans, insurance and other services backed by its own cryptocurrency. While it didn’t hold an ICO — its “Link” token is earned or can be bought on exchanges — Line did dive into crypto in a major way, opening its own exchange and starting a crypto investment fund, too. With the bear market in full effect, and token valuations dropping by 90 percent across the board, we haven’t heard too much more from Line regarding its crypto plans.

Powered by WPeMatico

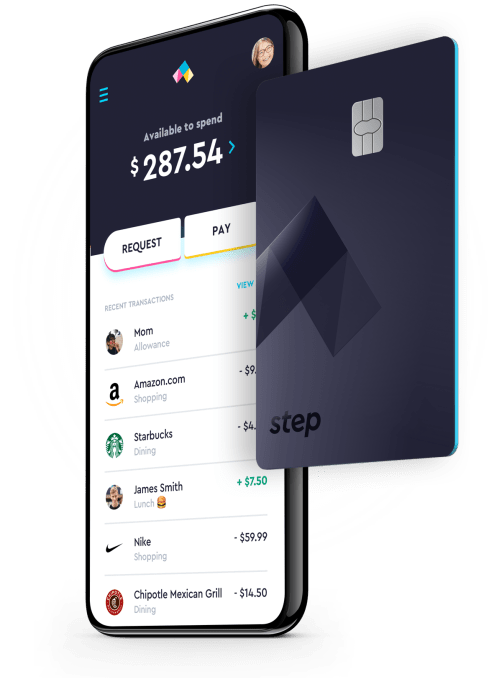

A new mobile banking startup called Step wants to help bring teenagers and other young adults into the cashless era. Today, cash is used less often, as more consumers shop online and send money to one another through payment apps like Venmo. But teenagers in particular are still heavily burdened with cash — even though they, too, want to spend their money on things that require a payment card, like Amazon.com purchases or mobile gaming, for example.

That’s where Step comes in.

The company aims to address the needs of what it believes is an underserved market in mobile banking — the 75 million children and young adults under the age of 21 in the U.S., who are still being forced to use cash.

This market isn’t the “unbanked,” it’s the “pre-banked,” explains Step CEO CJ MacDonald, whose previous startup, mobile gift card platform Gyft, sold to First Data several years ago.

Above: Step CEO, CJ MacDonald

“We’re building an all-in-one banking solution that primarily focuses on teens and parents,” he says. “We want it to be a teen’s first bank account. We want to be a teen’s first spending card. And we want to teach financial literacy and responsibility firsthand.”

MacDonald, along with CTO Alexey Kalinichenko, previously of Square and financial services startup Token, founded Step in May 2018. The 10-person team also includes several prior Gyft employees.

Last summer, Step closed on $3.8 million in seed funding from Sesame Ventures, Crosslink Capital and Collaborative Fund. Crosslink general partner Eric Chin sits on the board.

While there are a number of mobile banking apps out there today — like Chime, Monzo, Simple, Revolut and others — Step will specifically target teens, 13 and up, and other young adults with its marketing. Teens under 18 still need parents’ approval to sign up, of course. But the goal is to encourage the teens to bring the idea to their parents — not the other way around.

Step’s focus on this younger demographic puts it in a different space, where there are fewer competitors. Its more direct rivals are not the bigger mobile banks, but rather startups like teen debit card and bank app Current, or the parent-managed debit card for kids from Greenlight.

Step’s focus on this younger demographic puts it in a different space, where there are fewer competitors. Its more direct rivals are not the bigger mobile banks, but rather startups like teen debit card and bank app Current, or the parent-managed debit card for kids from Greenlight.

The mobile banking service Step provides will also aim to be more comprehensive than just a debit card. It will offer a combination of checking, savings and a Visa card that works as both credit and debit.

The card includes Visa’s Zero Liability Protection on all purchases from unauthorized use, and allows parents to set spending limits.

Parents will also be able to connect their own bank accounts to Step to instantly transfer in funds, which can then be distributed to kids’ accounts for things like allowances and chores, or other everyday spending needs. Step’s bank account itself is backed by Evolve Bank, so it’s FDIC-insured up to $250,000.

Unlike Current, which charges a subscription to use its service, Step aims to be a fee-free bank for consumers. Users don’t have to pay for their account, and there are no fees for things like overdrafts. Instead, Step’s plan is to generate revenue through traditional means — like interchange fees and by way of lending practices, once it has established a deposit base.

The company pays a 2.5 percent interest rate on deposits, offers a round-up savings feature and a range of budgeting tools and supports free instant transfers between Step accounts. It also provides access to a network of 35,000 ATMs with no fees.

The company pays a 2.5 percent interest rate on deposits, offers a round-up savings feature and a range of budgeting tools and supports free instant transfers between Step accounts. It also provides access to a network of 35,000 ATMs with no fees.

Beyond simply facilitating mobile banking, Step’s bigger goal is to teach teens to become financially responsible.

“Schools do not teach kids about money. A lot of families don’t talk about money. And it’s a crucial life skill that’s not really addressed properly when people are growing up,” says MacDonald, who says he was lacking in life skills in this area, even as a young college grad.

“There were ‘Money 101’ skills that I had not learned — that no one had talked to me about. Things like building credit, how many credit cards you should have, debt to income ratio,” he continues. “A lot of people get released into the real world without experience [in those areas],” he says.

Long-term, after solving the needs associated with everyday banking transactions, Step wants to layer on other products and services — like tools that allow a family to save together for college, for example.

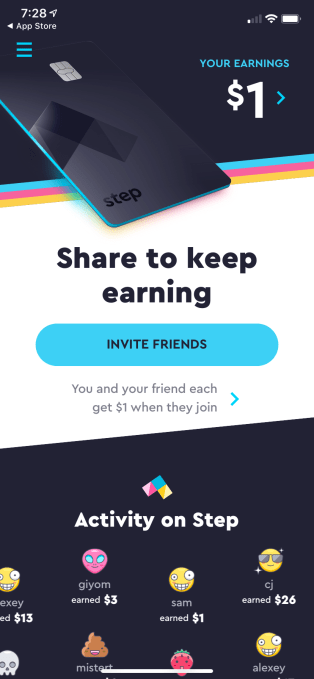

The company is launching the banking service under an invite-only system to scale up.

Today, it’s opening a waitlist and referral program. When you invite a friend, you each receive one dollar. Access will then be rolled out on a first-come, first-serve basis this spring. Users can join Step through the website, iOS or Android application.

Powered by WPeMatico

India’s largest bank has secured an unprotected server that allowed anyone to access financial information on millions of its customers, like bank balances and recent transactions.

The server, hosted in a regional Mumbai-based data center, stored two months of data from SBI Quick, a text message and call-based system used to request basic information about their bank accounts by customers of the government-owned State Bank of India (SBI), the largest bank in the country and a highly ranked company in the Fortune 500.

But the bank had not protected the server with a password, allowing anyone who knew where to look to access the data on millions of customers’ information.

It’s not known for how long the server was open, but long enough for it to be discovered by a security researcher, who told TechCrunch of the leak, but did not want to be named for the story.

SBI Quick allows SBI’s banking customers to text the bank, or make a missed call, to retrieve information back by text message about their finances and accounts. It’s ideal for millions of the banking giant’s customers who don’t use smartphones or have limited data service. By using predefined keywords, like “BAL” for a customer’s current balance, the service recognizes the customer’s registered phone number and will send back the current amount in that customer’s bank account. The system can also be used to send back the last five transactions, block an ATM card and make inquiries about home or car loans.

It was the back-end text message system that was exposed, TechCrunch can confirm, storing millions of text messages each day.

A redacted example of some of the banking and credit information found in the database (Image: TechCrunch)

The passwordless database allowed us to see all of the text messages going to customers in real time, including their phone numbers, bank balances and recent transactions. The database also contained the customer’s partial bank account number. Some would say when a check had been cashed, and many of the bank’s sent messages included a link to download SBI’s YONO app for internet banking.

The bank sent out close to three million text messages on Monday alone.

The database also had daily archives of millions of text messages each, going back to December, allowing anyone with access a detailed view into millions of customers’ finances.

We verified the data by asking India-based security researcher Karan Saini to send a text message to the system. Within seconds, we found his phone number in the database, including the text message he received back.

“The data available could potentially be used to profile and target individuals that are known to have high account balances,” said Saini in a message to TechCrunch. Saini previously found a data leak in India’s Aadhaar, the country’s national identity database, and a two-factor bypass bug in Uber’s ridesharing app.

Saini said that knowing a phone number “could be used to aid social engineering attacks — which is one of the most common attack vectors in the country with regard to financial fraud,” he said.

SBI claims more than 500 million customers across the glob,e with 740 million accounts.

Just days earlier, SBI accused Aadhaar’s authority, UIDAI, of mishandling citizen data that allowed fake Aadhaar identity cards to be created, despite numerous security lapses and misuse of the system. UIDAI denied the report, saying there was “no security breach” of its system. (UIDAI often uses the term “fake news” to describe coverage it doesn’t like.)

TechCrunch reached out to SBI and India’s National Critical Information Infrastructure Protection Centre, which receives vulnerability reports for the banking sector. The database was secured overnight.

Despite several emails, SBI did not comment prior to publication.

Powered by WPeMatico

After spending eight months in an immigration facility in the United States, Abimael Hernandez made the tough decision to return to Mexico.

He had spent 14 years in Florida and was leaving behind his wife and three children to return to Mexico so he could go through the process of returning to the United States legally.

Hernandez didn’t want to live in fear of being pulled over by police; he longed to own a car in his name and he didn’t want his immigration status to be illegal any longer.

Upon his return to Mexico, Hernandez had worked in construction, call centers and sold CDs before finally being given an opportunity that made a return to the United States less appealing. Hernandez now works as a software developer at Ignite Commerce in Mexico and has integrated well into the country that he at first struggled to identify as home.

Hernandez’s struggle to adjust and adapt to life in a new country mirrors that of other migrants who are returning to Mexico. And ongoing U.S. government attempts to put an end to the DACA program instituted under President Barack Obama, an initiative which protected as many as 800,000 unauthorized migrants that had come to the United States as children, are pushing many others along the same path.

For the people facing an increasingly hostile environment for migrants who choose — or are forced — to return to Latin America, little support awaits.

What tends to lie in store for these deportees and returnees in Mexico is usually low-paying service employment. For those with an undocumented status especially, no collateral in Mexico leads to problems in accessing finances, whilst having spent the majority of their lives in the United States, barriers in the Spanish language mean some returnees fail to be accepted into the Mexican education system.

Though there are some government initiatives aimed at supporting deportees by providing shelter and food, this usually bilingual cohort is prone to unemployment, as well as the mental struggle assigned to the frustrations of reintegrating into a country with which many can’t identify.

It is the hardship of reintegration that inspired the foundation of Hola Code, the only Mexican startup of its kind that currently runs in the country. Founded by CEO Marcela Torres just last year, Hola Code is coined as hackers without borders and is a startup that offers a coding bootcamp for migrants, ensuring that this young generation, new to Mexico, does not slip under the radar.

Geared at supporting the integration of deportees, the startup is prepping Mexicans to enter into a high-demand sector through an intensive five-month software development training program that gives the students qualification, even though many have started from scratch.

‘‘We don’t know of any social enterprises or even regular startups that are actually tackling migration in Mexico,’’ Torres recently told TechCrunch. Although migration and deportations continue to make headlines, it appears that Hola Code might be the only Mexican startup trying to do anything about it.

Backed by San Francisco-based Hack Reactor, the Mexican organization costs nothing until graduates have secured a full-time job, and pays their students a monthly stipend without any bureaucratic red tape.

Collectively venturing into Mexican society with peers in a similar position, most Hola Code students also don’t plan to return to the United States and want to use their skill set in the ever-growing Mexican tech ecosystems. For former student Hernandez, he remains grateful for the support network that Hola Code became for him.

‘‘If Mexico had more opportunities like Hola Code I think returnees would definitely think about not going back to the United States and other countries,’’ he said.

The question now remains as to how international policies will continue to affect Latin American families in the future.

‘‘You create the program in the hopes that one day that you will run out of work,’’ CEO and co-founder Marcela Torres ambitiously explained.

MISSION, TX – JUNE 12: A Central American immigrant stands at the U.S.-Mexico border fence after crossing into Texas on June 12, 2018 near Mission, Texas. U.S. Customs and Border Protection (CBP) is executing the Trump administration’s zero tolerance policy towards undocumented immigrants. U.S. Attorney General Jeff Sessions also said that domestic and gang violence in immigrants’ country of origin would no longer qualify them for political-asylum status. (Photo by John Moore/Getty Images)

The bittersweet reality is that Hola Code has, in fact, blossomed within the past year, with now more than 400 monthly applications from Mexicans and Central American migrants that are seeking refuge in the country. Although the organization celebrates the achievements of their alumni, who tend to quickly ascend into well-paid tech jobs across Mexico, the coding bootcamp is never short of work, and is now looking to open an office in Tijuana to be closer to the border.

The journey for the startup’s female founder, one of a small number of women in Mexican tech leadership, has also not been an easy feat.

‘‘It’s very difficult for a woman that has designed a business plan and has ideas to be taken seriously,’’ Torres explains. ‘‘It took me a long time to find the original investors that would believe in my idea and in my capacity, as well, to run the organization because this is the first startup that I have executed.’’

The cultural burdens that still exist in Mexico is a reality that deters many women from entering into the entrepreneurial scene within the country. From finding investors to promoting an idea, it is the issue of being taken seriously that is most effective at stalling Mexico’s female entrepreneurs.

‘‘I think that it’s important for younger women to start seeing us out there trying to take risks and thinking that they can do it as well. Even if they’re not successful, that it’s something that is available and achievable for them.’’

Confronted by her own hurdles in becoming the tech leader of Hola Code today, however, her organization does much more than just in-depth coding. From encouraging young Mexican women to leap into business and tech, to helping each student find a job, Torres speaks of the hope, security and routine that every Hola Coder gathers as they become immersed in Mexican life through this community.

‘‘Helping them navigate the expectations of how to start a career in tech is one of the things that we work on and therefore it means that they develop the right skill set, and once they finish the program, to be able to successfully jump into big areas such as banking.’’

MCALLEN, TX – JUNE 12: Central American asylum seekers wait for transport while being detained by U.S. Border Patrol agents near the U.S.-Mexico border on June 12, 2018 in McAllen, Texas. The group of women and children had rafted across the Rio Grande from Mexico and were detained before being sent to a processing center for possible separation. Customs and Border Protection (CBP) is executing the Trump administration’s “zero tolerance” policy towards undocumented immigrants. U.S. Attorney General Jeff Sessions also said that domestic and gang violence in immigrants’ country of origin would no longer qualify them for political asylum status. (Photo by John Moore/Getty Images)

Former student Miriam Alvarez is now a software engineer for SegundaMano. Growing up in the United States, Mexican Universities did not accept her U.S. documents and she too began working in a call center before hearing about the project, applying just days before the application deadline. ‘‘It’s OK to not know everything, but you should always be open to trying new things and learning something new,’’ Alvarez said, speaking of the broader messages that Hola Code delivers.

The overwhelming lessons that all Hola Code’s alumni praise is how the bootcamp delivers more than just coding, but also important life skills that allow for the transition to Mexico to be easier. Through reasoning and problem solving, many are grateful for the structure and direction that Hola Code provides Mexicans new to the country.

Though many of their students had joined Hola Code feeling “American,” the values that the group provides adds to the larger picture of Mexico’s growing tech scenes.

‘‘The biggest challenge for the tech sector in the country is access to human capital and the second one is retaining the talent.’’ By fine-tuning the country’s coding talent pools with bicultural young developers that speak English, Spanish and also JavaScript, the organization contributes to growing tech hubs such as Tijuana, Guadalajara and Mexico City, which are increasingly gaining global attention.

Hola Code is one of just a few life-changing organizations filling the gap in an immigration story that is seldom covered by the media.

Providing social mobility to people that have been forced to return through education, employment and exposure to tech pioneers, Hola Code’s alumni are spreading the message of integration through education far and wide across the globe.

As long as the fragility of migration continues to be tested, however, Torres and her team have work to do in their mission to produce Mexico’s next pioneering coding generation.

Powered by WPeMatico

French startup Shine wants to be the only professional bank account you need if you’re a freelancer. So far, 25,000 people have signed up to the service, and the company recently raised a $9.3 million funding round.

Shine wants to help freelancers in France all steps of the way. After signing up, the app helps you fill out all the paperwork to create your freelancer status. You then get a card and banking information.

This way, you can generate invoices, accept payments and also pay for stuff. Creating an account and basic transactions have been free so far, but starting on January 21st, freelancers will have to pay €4.90 to €7.90 per month depending on their status.

Freelancers who generate less than €70,000 (so-called “auto-entrepreneurs”) will pay €4.90 per month, while others will pay more. This is still cheaper than most professional bank accounts. Existing users won’t have to pay anything.

The company mentioned premium plans in the past, but Shine now wants to create a single plan with a unified feature set for everyone. If you’re more serious about your indie lifestyle and generate a lot of revenue, you’ll pay a bit more.

In addition to that change, the startup is working on some new features. Soon, you’ll be able to generate better exports for accounting purposes. You’ll be able to deposit checks, control your account from a web browser, generate better invoices and more.

But Shine doesn’t just want to build an endless list of bullet points with as many features as possible. The company wants to create the best banking assistant for freelancers. You get notifications for admin tasks and you can ask the support team any question you have when it comes to the administrative part of your work.

It’s not just customer support for the product — it’s customer support for French paperwork. And that has some value by itself.

Powered by WPeMatico

B-Social, a London fintech that currently offers a “social finance” app and beta debit Mastercard, has raised £3.2 million in seed-round funding from undisclosed high-net-worth individuals. However, the fundraise is just the first step in a journey in which B-Social wants to eventually become a fully licensed bank that reimagines banking around everyday social interactions.

As it exists today, the B-Social app and accompanying card enables users to have control over everyday spending, track expenditures and create groups between friends to split bills and record settlements. It’s currently in the hands of a limited number of beta testers, spanning employees, investors, friends and family, with plans for a wider U.K. launch in February next year.

“We recognise that almost all financial transactions are inherently social,” B-Social co-founder and CEO Nazim Valimahomed tells me. “We want to change the relationship people have with money by helping them overcome the anxiety, awkwardness and wasted time when they engage with their social finances. We are doing that by building a digital bank that truly accommodates the way people live their lives and is dedicated to connecting a person’s finances to their social world.”

The idea was born in part out of Valimahomed’s own frustrations and is informed by his belief that individuals are often a bank themselves, lending and borrowing to friends and family by making shared purchases and then getting paid back.

“A simple example might be that you pay for flights for two or more people and then get paid back individually,” he says. “For multiple transactions, this becomes complex, often resulting in the trip organiser having to create a spreadsheet to work out what people owe across multiple transactions.”

To simplify this problem, B-Social wants to let you to make purchases with your card, which are flagged as an expense on behalf of a group of individuals. From here the bank to be will enable all members of a group — and where groups can be ad hoc and temporary or more long-term — to continuously see who is owed how much and to get paid back easily within the app and record settlements.

Dubbing this future proposition as the seeds of a “social bank,” the B-Social CEO cites competitors as traditional high-street banks that currently dominate the U.K. consumer market (the so-called big 5 have around 87 percent market share in the U.K.).

“We are aiming at winning a part of their market share by targeting customers looking for a bank as social as they are that offers a unique digital experience in order to help change the banking ecosystem forever,” Valimahomed tells me, although he also concedes that challengers such as Monzo, N26, Starling and Revolut have also built some basic social features into their apps.

“Our entire technology and product focus is to build a bank from scratch through a social lens,” he says.

Powered by WPeMatico

Robinhood is undercutting the big banks by forgoing brick-and-mortar branches with its new zero-fee checking and savings account features. With no overdraft or monthly fees, a juicy 3 percent interest rate and a claim of more U.S. ATMs than the five biggest banks combined, Robinhood is using the scalability of software to pass impressive perks on to customers. The free stock trading app already used that approach to attack brokers like E*Trade and Charles Schwab that charge a per-trade fee. Now it’s breaking into the larger financial services market with a model that could put the squeeze on Wells Fargo, Chase and Bank of America.

Today Robinhood launches checking and savings accounts in the U.S. with a Mastercard debit card issued through Sutton Bank that starts shipping December 18th. Users earn 3 percent on all the dough they keep with Robinhood, yet there’s no minimum balance or fees for monthly membership, overdrafts, foreign transactions or card replacements. That’s a pretty sweet deal compared to the other leading banks that all charge for some of that or offer much lower interest rates. The trade-off is that while customers get 24/7 live text chat support, they won’t be able to walk into a local bank branch. Users who want early access can sign up here.

Robinhood expects to turn a profit thanks to a lean 300-employee operation, earning a margin on investing your money in U.S. treasuries and a revenue share with Mastercard on interchange fees charged to merchants when you swipe. The launch could be critical to keeping Robinhood worthy of its $5.6 billion valuation from when it took a $363 million Series D in March just a year after raising at a $1.3 billion valuation. The 6 million-user app invested in launching a free cryptocurrency trading exchange early this year only to see coin prices plummet and mainstream interest fall off. But with banks hammering users with surprise fees and mediocre user experience, there’s a huge opportunity for a mobile-first startup to disrupt how we store money.

“Brick-and-mortar locations are costly. Our goal with this product was to build a completely digital experience so we can reduce our overhead so we can pass more of the value back to customers,” Robinhood co-CEO Baiju Bhatt tells me. [Disclosure: I know Bhatt and co-CEO Vlad Tenev from college.] “Saving accounts in the U.S. pay on average 0.09 percent and we all know the banks are making far more than that from the deposits. With Robinhood you earn 3 percent off all of your money. Mental math is hard, so if you look at the median U.S. household that has about $8,000 in liquid savings, they’d earn $240 a year.”

Robinhood will be sending invites to users in January for the new feature that they can use exclusively or alongside their existing bank. Anyone approved to use Robinhood’s stock brokerage is eligible, but users can also sign up directly for checking and savings with no obligation to trade stocks. Robinhood claims signing up won’t impact your credit score. Users get to customize a Robinhood-branded debit card that’s accepted wherever Mastercard is. Because the feature is run within Robinhood’s brokerage, it’s ensured by the SIPC instead of the FDIC, but you still get the same insurance on up to $250,000 cash.

One of the most appealing features of Robinhood checking and savings is getting access to 75,000 free-to-use ATMs in places like Target, Walgreens and 7-Eleven. Users won’t be able to tell just by looking at an ATM whether it’s in the network, but the Robinhood app features a map for finding the nearest one. You can deposit checks via Robinhood’s app too, and if you need to send a check, you can just tell the startup how much to deliver to whom and it will mail the check for you.

“These fees like overdraft fees — they’re not fees millionaires are paying. It’s ordinary folks paying. It’s actually more expensive for those that have less money and it’s cheaper for those that have more money. We think that isn’t right and we think that’s bad business,” Bhatt gripes. Because Robinhood built its own clearing house for moving money, and it lacks the overhead of traditional banks, it’s able to save enough money to make its no-fee structure work. “We want to build a financial services company that democratizes America’s financial system.”

Robinhood will have to convince users it’s worthy of their trust, as a security breach could be disastrous. There’s also the question of whether people are ready to ditch their bank branch. “Behaviors about and going into a branch are definitely changing,” says Bhatt. My biggest concern was not having any consistency in who I talk to when I need banking help. Bhatt tells me the company plans to roll out more personalized customer service features in the coming months, but there may always be edge cases that make the lack of in-person support annoying.

Getting into banking could open a lucrative revenue stream for Robinhood as it charts its path to IPO. The startup recently hired Jason Warnick, a 20-year veteran of Amazon, to be its CFO and get it prepped to go public. Wall Street will want to see a more robust business that’s not as vulnerable to foes like stock brokerage Charles Schwab, which is already lowering fees to stay competitive with Robinhood. Not only will checking and savings see users move more money into their Robinhood accounts that it can invest to earn a profit, but it also poises the startup to tackle more financial services in the future. More lucrative products like loans could make paying 3 percent much easier for Robinhood to handle.

Powered by WPeMatico

N26 announced today that it now has more than 2 million customers — up from 1.5 million in October.

The German fintech startup’s CEO Valentin Stalf was interviewed onstage at Disrupt Berlin with Tandem CEO Ricky Knox, where they discussed the growth of what are sometimes called challenger banks or neobanks — new banks that are taking on the incumbents by focusing on digital tools.

Stalf said N26 is seeing more than €1.5 billion in transactions each month, with €1 billion in deposits. He also discussed the company’s recent launch in the United Kingdom — he didn’t know the exact number of U.K. users, but estimated that the company has tens of thousands of U.K. accounts, with between 1,500 and 2,000 new signups on a single day three days ago.

Meanwhile, Knox said Tandem now has nearly half a million users in the U.K. (“This year, we’re seeing everybody’s growing really quickly.”) He also noted that because Tandem allows users to aggregate different accounts, he’s noticed some of those users are starting to become more focused on individual services.

“What tends to happen, particularly with the early adopter audience, is they will open [an] account with everybody because they want to check it out, they want to get the best product,” he said. “And then what you’ll see is over time, them kind of picking a horse — depending on the functionality they like, depending on, you know, the service they’re getting there — and settling in.”

Tandem is also expanding geographically, specifically to Hong Kong through a deal with Convoy Global Holdings. Asked why he’s making the leap to Asia before launching in other European markets, Knox said, “There are a load of massive Asian markets … The exciting thing here is the opportunity, as I said, for a global bank, and some of these Asian markets are really ripe for disruption.”

In discussing the different models for challenger banks, Knox warned against the dangers of the “marketplace bank” model, where banks make money by connecting customers to third-party services.

“What we found is, the more we try and push revenue in that area there, the less customers love it,” he said. “That’s the challenge with marketplaces: If you build your business model around it, you’ve got an inherent contradiction between customers loving you less when you make more money.”

Instead, Knox argued that customers have a better experience if the bank is willing to recommend free or low-priced services: “And actually at the backend, we’re still making money the same way the bank makes money. So we’re able to fund, if you like, all this great customer stuff at the front end.”

Moderator Romain Dillet quickly pointed out that Stalf was shaking his head while Knox was making his arguments.

“What we see with our customers is, I think if we have a great product, they’re normally also willing to pay a little bit for it,” Stalf said. “It needs to be transparent, and it needs to be a good value to consumers. But I think it’s untrue that customers are always not choosing a product if you price it.”

As for whether we’ll be seeing consolidation in the industry over the next few years, Knox argued, “I’d say there’s plenty of room for the existing cadre of neobanks to be incredibly successful on a global basis without any mergers or acquisitions.” He suggested it’s more likely that the established banks start trying to acquire the challengers, although he said, “That’s not a route we want to take.”

“I think there’s a couple players that are set for being a global bank, and I think we are trying to take the shot to be a global bank,” Stalf added. “I think it’s about building up 50 to 100 million users in the next couple years.”

Powered by WPeMatico

The Morgan Stanley Multicultural Innovation Lab, Morgan Stanley’s in-house accelerator focused on companies founded by multicultural and female entrepreneurs, hosted its second Annual Showcase and Demo Day. The event also featured companies from accelerators HearstLab, Newark Venture Partner Labs and PS27 Ventures. (Note: I was formerly employed by Morgan Stanley and have no financial ties.)

The showcase represented the culmination of the program’s second year, which followed an initial five company class that has already seen two acquisitions. Through the six-month program, Morgan Stanley provides early-stage companies with a wide range of benefits including an equity investment from Morgan Stanley, office space at Morgan Stanley headquarters, access to Morgan Stanley’s extensive network, and others. Applications are now open for its third cohort of companies with the application window closing on January 4th, 2019.

The 16 presenting startups, all led by a female or multicultural founder, offered solutions to structural inefficiencies across a wide array of categories including fintech, developer tools, and health. Though all of the companies offered impressive presentations and strong value propositions, here are three of the companies that stood out to us.

In hopes of democratizing software and app development, Hatch Apps provides a platform that allows users and companies to build iOS, Android and web applications without any code through pre-built templates and custom plug-and-play functions. In essence, Hatch Apps provides a solution for application building similar to what Squarespace or Wix provide for websites.

In the modern economy, every company is in one way or another a tech or tech-enabled company. Now the demand for strong engineers has made the fight for talent increasingly competitive and has made engineering quite costly, even when only needed for simple tasks.

For an implementation and subscription fee, Hatch Apps allows companies with less sophisticated engineering DNA to reduce entering costs by launch native apps on their own, across platforms, and often on faster timelines than those seen through third-party developers. Once an app is launched, Hatch Apps provides customers with detailed analytics and allows them to send targeted push notifications, export data and make in-app changes that can automatically go live in app stores.

The company initially took a bootstrapping approach to financing and raised funds by selling a 2016 election-themed “Cards Against Humanity”-style game created on the platform. Since then, Hatch Apps has already received funding from the Y Combinator Fellowship, Morgan Stanley, and a number of other investors.

While estate planning is a topic many don’t like to think about, it’s a critical issue for managing cross-generational wealth. But will drafting can often be very complex, time-consuming, and costly, requiring hours of legal consultation and coordination between various parties.

Founded by two former classmates at Stanford Business School, FreeWill looks to simplify the estate planning process by providing a free online platform that automates will drafting, in a similar function to what TurboTax does for taxes. Using FreeWill, users can quickly set allocations for their estate and select personal recipients, charitable donations, executor specifications, and other ancillary requests. The platform then creates a finalized legal document that is legally valid in all 50 states, which users can also quickly make changes to and replace without incurring expensive legal costs.

FreeWill is able to provide the platform to consumers for free due to the proceeds it receives from its non-profit customers, who pay to be featured on the platform as a partner organization. FreeWill offers a compelling value proposition for partnering companies. By acting as a channel to funnel user donations to listed organizations, FreeWill has been able to drive a 600% increase in charitable giving to partner organizations on average. FreeWill also provides partner organizations with backing analytics that allow non-profits to track bequests and donors through monthly reports.

FreeWill currently boasts an impressive roster of 75 paying non-profit partners that include American Red Cross, Amnesty International and many others. In the long-run hopes to be the go-to solution financial and legal end of life planning for investment advisors, life insurance and employee benefits providers.

Shoobs is looking to be the go-to platform for local “urban” events, which the company defined as events centered on local nightlife, comedy and concerts in the hip-hop, R&B, and reggae genres to name a few. But unlike the genre-agnostic, transaction-focused event management platforms that can make the space seem pretty crowded, Shoobs focused on providing genre-specific even discovery. Shoobs matches urban event goers with artists of their choice and related smaller scale events that can be harder to discover, acting as a form of curation, quality control and discovery.

For event organizers, Shoobs helps provide digital ticketing and promotion services, with event recommendation capabilities that target the most promising potential customers. Through its offering to event organizers, Shoobs is able to monetize its services through ticket sale commission, advertising and brand partnerships.

Since its initial launch in London, Shoobs notes it has become one of the top urban events platforms in the city, with an extensive base of recurring registered users and event organizers. After previously working with AEG for its London launch, Shoobs is looking to expand stateside with the help of organizers like Live Nation. Shoobs joins a long list of promising Y Combinator alumni companies with YC also acting as one of Shows initial investors

Morgan Stanley Multicultural Innovation Lab

Hearst Labs

Newark Venture Partners Labs

PS27 Ventures

Cleaning System — a water free, detergent free, and chemical free plasma device that cleans items that are extremely hard or impossible to clean with a washer and dryer.”

Cleaning System — a water free, detergent free, and chemical free plasma device that cleans items that are extremely hard or impossible to clean with a washer and dryer.”Powered by WPeMatico

Chris Hays and Mark Jeffrey wanted to create a way for everyone to be able to tell their loved ones if they were in trouble. Their first product, Guardian Circle, did just that, netting a mention a few years ago. Now the same team is truly decentralizing alerts with a new token called, obviously, Guardium.

The plan is to create an ad hoc network of helpers and first responders. “Guardium and Guardian Circle together open the emergency response grid to vetted citizens, private response and compatible devices for the very first time,” write the founders. “Providing an economic framework on our global distributed emergency response network; Guardium brings first responders to the 4 billion people on the planet without government-sponsored emergency response.”

Because the product already works, the team is taking on the token sale as a new challenge.

“We’re serial entrepreneurs — both of us have been venture-backed in the past by names like SoftBank and Intel, and we’ve been senior execs in companies backed by Sequoia and Elon Musk. Transitioning to the token sale-backed universe has been an interesting study in contrasts,” said Hays. “There are a number of ‘panic button apps’ — but without exception, all of them have forgotten ‘the second half of the problem’ — organizing the response. Getting people who do not know one another into instant communication and location sharing during an emergency — the importance of that cannot be overstated.”

The founders found that their idea wasn’t fundable in the valley. After all, what VC wants to help people when they can invest in Snapchat? Instead, Hays and Jeffrey are aiming bigger.

“We’re rebooting the world’s safety grid,” said Hays. “We’re creating a new global public utility. And we want it to service everyone, everywhere on earth. Although it is a very big vision, and it is a capitalist, multibillion dollar ecosystem that we’re chasing — it’s still a very different vision, and not the one venture capitalists are looking for.”

The token works to create a flash mob of help. Guard tokens pay first responders and dispatchers and “cities, campuses, and resorts stake $GUARD to access Alerts created within their geofenced borders,” allowing local folks to help immediately. They’ve sold half of their hard cap of $10 million thus far.

While tokens are always an iffy investment, this team has produced product and, more important, it’s clear they’ll never raise venture. A token, no matter how it’s used in the future, seems like a solid solution.

Powered by WPeMatico