Banking

Auto Added by WPeMatico

Auto Added by WPeMatico

Entering into the world of Anthemis is a bit like stepping into the frame of a Wes Anderson film. Eclectic, offbeat people situated in colorful interiors? Check. A muse in the form of a renowned British-Venezuelan economist? Check. A design-forward media platform to provoke deep thought? Check. An annual summer retreat ensconced in the French Alps? Bien sûr.

Sitting atop this most unusual fintech(ish) VC is its ponytailed founder and chairman Sean Park, whose difficult-to-place accent and Philosophy professor aura belie his extensive fixed income capital markets experience. He’s joined by founder and CEO Amy Nauiokas, who in addition to being one of Fintech’s most prominent female investors also owns a high-minded film and television production company.

When Arman Tabatabai and I recently sat down with Park and Nauiokas in their New York office, the firm’s leaders were in an upbeat mood, having blown past the temporary perception-setback associated with the abrupt resignation last year of Anthemis’ former CEO Nadeem Shaikh (for more on this, read TechCrunch writer Steve O’Hear’s coverage of the situation).

And as the conversation below demonstrates, Park and Nauiokas are well poised to bring the quirk into everything they touch, which these days runs the gamut from backing companies involved in sustainable finance, advancing their home-grown media platform and preparing a soon-to-be-announced initiative elevating female entrepreneurs.

Gregg Schoenberg: With the two of you now at the helm, how does Anthemis present itself today?

Sean Park: I’ll step back and say that when Amy and I were working at big financial institutions in the noughties, we saw that the industry was going to change and that existing business models were running into their natural diminishing returns.

We tried to bring some new ideas to the organizations we were working in, but we each had epiphany moments when we realized that big organizations weren’t built to do disruptive transformation — for bad reasons, but also good reasons, too.

GS: Let’s fast forward to today, where you have several strong Fintech VCs out there. But unlike others, Anthemis puts weirdness at the heart of its model.

Yes, you’ve backed some big names like Betterment and eToro, but you’ve done other things that are farther afield. What’s the underlying thesis that supports that?

Amy Nauiokas: Whatever we do at Anthemis has to be a non-zero-sum game. It has to be for good, not for evil. So that means that we aren’t looking in any place where you see predatory opportunities to make money.

Powered by WPeMatico

Just ahead of the launch of the Apple Card, a startup that has its own take on modernizing the credit card industry, Zero, is announcing the close of its $20 million Series A. The new round of funding was led by New Enterprise Associates (NEA), and brings Zero’s total raised to date to $35 million, including both equity and debt funding.

Other investors in the round include SignalFire, Eniac Ventures, Nyca Partners and some unnamed school endowments. Zero had previously announced an $8.5 million raise in fall 2017, led by Eniac, and had raised $7 million in venture debt from Silicon Valley Bank.

Zero has a clever idea that targets millennials’ hesitance to sign up for credit cards.

Today, only 33% of millennials have a major credit card, a Bankrate survey found — largely because they’re wary of falling into the vicious debt cycle. Instead, this younger demographic often only carries a debit card. But that also means they’re missing out on credit card benefits — like points, rewards and cash back.

Zero’s idea is to offer a rewards credit card that works like debit.

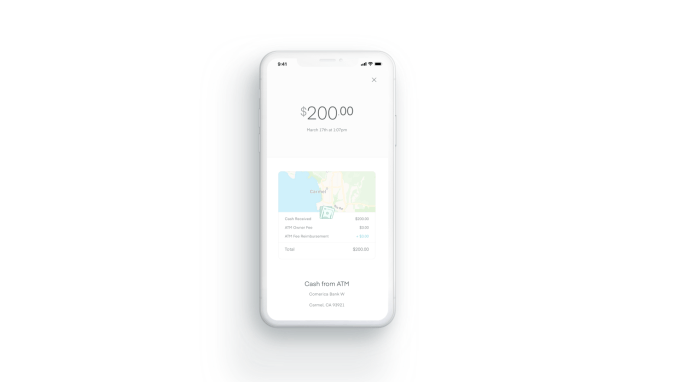

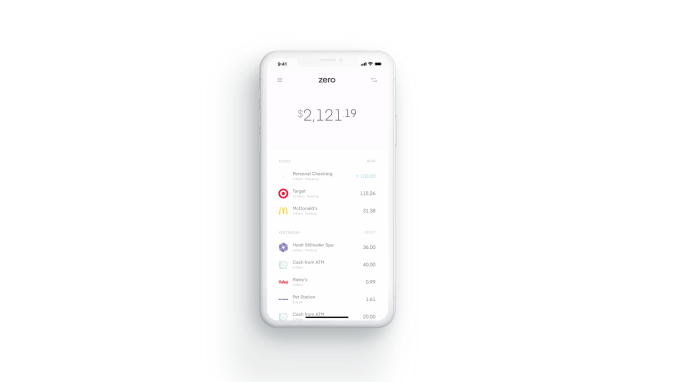

The Zerocard itself is a World Mastercard, so it earns credit card cash back. But unlike a traditional credit card, it’s combined with an FDIC-backed checking account called Zero Checking. That means Zerocard and Zero Checking work together in the app, allowing cardholders to see one net number they can spend from.

That way, they won’t make the mistake of accidentally going over budget, as is often the case with traditional credit cards, which then benefit from charging interest on the unpaid balance.

Zero co-founder and CEO Bryce Galen says he had always liked optimizing his personal finances, but didn’t see the value in overspending to chase rewards.

“People spend 10 to 15% more on average just because they’re putting it on a credit card, and not seeing where they stand all the time,” he says. “Spending 10 to 15% more to chase 1 to 2% in rewards doesn’t make sense.”

Plus, he adds, “half of all credit card points are never even redeemed.”

With Zerocard, the company does away with other credit card annoyances as well.

Zerocard doesn’t charge annual fees like many traditional credit cards do. And Zero Checking doesn’t add any additional ATM fees beyond what the ATM owner charges. It also does away with foreign transaction fees, minimum balance fees and overdraft fees — like many of today’s challenger banks.

Meanwhile, the Zero app is built with an eye toward what makes apps great.

Galen, who led product development for Zynga’s “Words with Friends” has experience in this department, while co-founder and COO Joel Washington previously co-founded car sales marketplace Shift. The executive team, combined, has backgrounds that include time at Affirm, Apple, Capital One, Dropbox, Google, Postmates, Silicon Valley Bank, Upgrade and Wells Fargo.

Overall, Zero’s design feels clean and simple, compared to the cluttered and dated apps from traditional banks. It has smart features, too, like a detailed transaction view that shows the vendor’s logo and location on a map to make it easier to recognize purchases.

“Zero creates an innovative debit-style experience, with an elegant design, and truly compelling rewards. It’s a fabulous banking experience,” said Hans Morris, managing partner of Nyca Partners and former president of Visa, Inc., in a statement. “Few people understand how complex it is to launch either a credit card or a checking account program, and I believe Zero is the first U.S. startup to launch both,” he said.

Zero launched in November 2018, but only to a small number of customers. Though officially open for business, it was functioning more like a public beta — though it didn’t call it that at the time. Meanwhile, its waitlist continued to grow.

Today, there are still 204,000 people waiting to be allowed in — something that Galen says is now going to happen.

“We haven’t launched to everyone on the waitlist yet, but we expect to within the next few weeks,” he says.

Another interesting twist on traditional credit cards is Zero’s path to card upgrades: it encourages but also rewards customers for telling their friends. By doing so, customers gain access to better-looking cards and higher cash-back percentages.

Zero customers start with a “Quartz” card offering 1% back on purchases. When a friend they refer joins, they receive a higher-level card called “Graphite” that offers 1.5% back. Two friends earns you the “Magnesium” card with 2% back and four friends gets you the “Carbon” card with 3% back. The Carbon card is also solid metal, capitalizing on the millennial trend of wanting their cards to look cool. And metal cards are in particular demand.

To receive the full cash-back rates, customers have to pay their balances in full by the due date, Zero says.

The company has partnered with Salt Lake City-based WebBank to issue the card, and deposits are held at Memphis-based Evolve Bank & Trust, an FDIC member. Zero makes money primarily on interchange and interest on deposits.

While some users may leave balances on the card that generate interest, Zero isn’t focused on that aspect of the business for revenue generation.

“Most companies in fintech today are launching undifferentiated debit cards as a feature or extension to their product for an additional engagement and monetization stream,” says Rick Yang, partner at NEA, as to why he invested.

“Zero is completely focused on their card programs and building a differentiated solution that actually provides a value proposition that resonates with consumers. We’ve also been fascinated by the growth of debit outpacing credit, and we think that our solution gives consumers the best of both worlds,” he adds.

Zero is currently iOS-only, but is working on an Android version that is expected to be ready in August.

Powered by WPeMatico

To become a global fintech player, locate your company in San Francisco and Africa.

That’s the approach of payments company Flutterwave, digital lending startup Mines, and mobile-money venture Chipper Cash—Africa-founded ventures that maintain headquarters in San Francisco and operations in Africa to tap the best of both worlds in VC, developers, clients, and the frontier of digital finance.

This arrangement wasn’t exactly coordinated across the ventures, but TechCrunch coverage picked up the trend and some common motives among these rising fintech firms.

Founded in 2016 by Nigerians Iyinoluwa Aboyeji and Olugbenga Agboola, Flutterwave has positioned itself as a global B2B payments solutions platform for companies in Africa to pay other companies on the continent and abroad.

Clients can tap its APIs and work with Flutterwave developers to customize payments applications. Existing customers include Uber, Booking.com and African e-commerce unicorn Jumia.com.

The Y-Combinator backed company is headquartered in San Francisco, runs its operations center in Nigeria, and plans to add offices in South Africa and Cameroon.

Flutterwave opened an office in Uganda in June and raised a $10 million Series A round in October. The company also plugged into ledger activity in 2018, becoming a payment processing partner to the Ripple and Stellar blockchain networks.

Powered by WPeMatico

OpenFin, the company looking to provide the operating system for the financial services industry, has raised $17 million in funding through a Series C round led by Wells Fargo, with participation from Barclays and existing investors including Bain Capital Ventures, J.P. Morgan and Pivot Investment Partners. Previous investors in OpenFin also include DRW Venture Capital, Euclid Opportunities and NYCA Partners.

Likening itself to “the OS of finance,” OpenFin seeks to be the operating layer on which applications used by financial services companies are built and launched, akin to iOS or Android for your smartphone.

OpenFin’s operating system provides three key solutions which, while present on your mobile phone, has previously been absent in the financial services industry: easier deployment of apps to end users, fast security assurances for applications and interoperability.

Traders, analysts and other financial service employees often find themselves using several separate platforms simultaneously, as they try to source information and quickly execute multiple transactions. Yet historically, the desktop applications used by financial services firms — like trading platforms, data solutions or risk analytics — haven’t communicated with one another, with functions performed in one application not recognized or reflected in external applications.

“On my phone, I can be in my calendar app and tap an address, which opens up Google Maps. From Google Maps, maybe I book an Uber . From Uber, I’ll share my real-time location on messages with my friends. That’s four different apps working together on my phone,” OpenFin CEO and co-founder Mazy Dar explained to TechCrunch. That cross-functionality has long been missing in financial services.

As a result, employees can find themselves losing precious time — which in the world of financial services can often mean losing money — as they juggle multiple screens and perform repetitive processes across different applications.

Additionally, major banks, institutional investors and other financial firms have traditionally deployed natively installed applications in lengthy processes that can often take months, going through long vendor packaging and security reviews that ultimately don’t prevent the software from actually accessing the local system.

OpenFin CEO and co-founder Mazy Dar (Image via OpenFin)

As former analysts and traders at major financial institutions, Dar and his co-founder Chuck Doerr (now president & COO of OpenFin) recognized these major pain points and decided to build a common platform that would enable cross-functionality and instant deployment. And since apps on OpenFin are unable to access local file systems, banks can better ensure security and avoid prolonged yet ineffective security review processes.

And the value proposition offered by OpenFin seems to be quite compelling. OpenFin boasts an impressive roster of customers using its platform, including more than 1,500 major financial firms, almost 40 leading vendors and 15 of the world’s 20 largest banks.

More than 1,000 applications have been built on the OS, with OpenFin now deployed on more than 200,000 desktops — a noteworthy milestone given that the ever-popular Bloomberg Terminal, which is ubiquitously used across financial institutions and investment firms, is deployed on roughly 300,000 desktops.

Since raising their Series B in February 2017, OpenFin’s deployments have more than doubled. The company’s headcount has also doubled and its European presence has tripled. Earlier this year, OpenFin also launched it’s OpenFin Cloud Services platform, which allows financial firms to launch their own private local app stores for employees and customers without writing a single line of code.

To date, OpenFin has raised a total of $40 million in venture funding and plans to use the capital from its latest round for additional hiring and to expand its footprint onto more desktops around the world. In the long run, OpenFin hopes to become the vital operating infrastructure upon which all developers of financial applications are innovating.

“Apple and Google’s mobile operating systems and app stores have enabled more than a million apps that have fundamentally changed how we live,” said Dar. “OpenFin OS and our new app store services enable the next generation of desktop apps that are transforming how we work in financial services.”

Powered by WPeMatico

SoFi is one of the leading fintech startups to emerge from San Francisco and breach the financial markets. Originally started as a way to better finance student debt, it has since expanded to include products targeted at personal loans and home loans.

Today, the company announced a new exchange-traded fund (ETF) product focused on the gig economy. GIGE, which trades on Nasdaq, is an actively managed fund advised by Toroso Investments that allows investors to capitalize on this hot sector of the economy. Toroso offers a range of services around creating and managing ETFs.

The company also announced the creation of an ETF focused on high-growth stocks. That ETF, which trades as SFYF on the NYSE, is designed to identify and capture the growth of the top 50 of the 1,000 largest publicly traded issues.

It has formerly used that growth focus to create two ETFs, targeting 500 high-growth companies under the trading name SFY and a product it called “SoFi Next 500 ETF,” which trades under SFYX, both of which have no management fees.

SoFi’s SFYF fund is composed specifically of public companies that show the strongest growth on three key metrics: top-line revenue growth, net income growth and forward-looking consensus estimates of net income growth.

For its GIGE fund, SoFi defines the “gig economy” as a group of companies that “embrace and support the workforce in which employment is based around short-term engagements that allow for flexibility and personal freedom and temporary contracts.”

SoFi’s new funds add value to investors primarily through providing 1) access to industry disruptors at 2) an earlier-stage point in their growth cycle.

In recent years, more and more investors have been trying to get a piece of the hottest tech companies earlier with a growing number of traditional institutional investors now dipping their toes into startup and tech investing.

Furthermore, a number of platforms and funds were launched to support the high-demand for access to some of the top public and private companies and major disruptive trends, including funds focused on themes such as artificial intelligence, big data, cybersecurity or the next manufacturing revolution.

SoFi argues that its GIGE fund offers compelling value due to the speed at which it offers investors access to new equity issues, as the fund is structured so that most post-IPO companies can join the GIGE within 31 days of IPO, relative to the 60-90 days traditional passive funds that often have to wait to add a newly IPO’d company.

Additionally, because SoFi’s GIGE fund is actively managed, SoFi is also offering fund investors access to experienced asset managers and an alternative to algorithmic, machine-led passive funds that have increasingly dominated the capital markets.

“Our members are excited by high-growth and gig economy companies because these companies are in many cases part of their lives,” said SoFi CEO Anthony Noto in a press release. “We’re giving our members a way to get started investing by buying what they know and investing in themselves.”

The announcement is the company’s latest step in its attempt to further establish itself under the new guard of CEO Anthony Noto, formerly of Goldman Sachs, who replaced former head Michael Cagney in 2018, as the company looks to move further away from dark clouds in its past established by lawsuits, sexual harassment claims, FTC penalties and chunky rounds of layoffs. In the past week, the company also announced that CMO and former COO, Joanne Bradford, will be leaving the company at the end of May, though the split was reportedly long-planned and amicable.

The launch of SoFi’s new investment products also comes just weeks after the company was reportedly in discussions to raise $500 million from the Qatar Investment Authority.

To date, SoFi has raised roughly $2 billion in venture capital, according to data from Crunchbase, with backing from a number of Silicon Valley and Wall Street heavy hitters, including SoftBank, Silver Lake Partners, Morgan Stanley, Founders Fund and a host of others.

Already at a valuation of nearly $4.5 billion, according to PitchBook, SoFi appears well on its way to an eventual IPO. Noto, however, noted in a recent interview with Yahoo Finance that “an IPO is not a priority at this point” for SoFi as the company remains focused on executing on a high-quality sustainable growth path.

Powered by WPeMatico

You probably haven’t heard of Checkout, a digital payments processing company that was founded in 2012 in London. Apparently, however, investors have been keeping tabs on the low-flying company and like what they see. Today, Checkout announced that it has raised $230 million in Series A funding at a valuation just shy of $2 billion co-led by Insight Partners and DST Global, with participation from GIC, the Singaporean sovereign-wealth fund, Blossom Capital, Endeavor Catalyst and other, unnamed strategic investors.

It’s the first institutional round for the company; it’s also one of the biggest Series A rounds ever for a European company.

What’s so special about Checkout that investors felt compelled to write such big checks? In a sea filled with fintech startups, it’s hard to know at first glance what differentiates it — or whether investors merely spy a huge opportunity, particularly given the company’s recent revenue numbers.

Checkout helps businesses — including Samsung, Adidas, Deliveroo and Virgin, among others — to accept a range of payment types across their online stores around the world. According to the WSJ, the fees from these services are adding up, too. It says Checkout’s European business generated $46.8 million in gross revenue and $6.7 million in profit in 2017, information it dug up through Companies House, the United Kingdom’s registrar of companies.

Checkout also plays into two huge trends that seem to be lifting all boats — the ongoing boom in online shopping, and the growing number of businesses using online payments. Little wonder that investors poured into payments startups last year more than four times what they invested in them in 2017 ($22 billion, according to Dow Jones VentureSource data cited by the WSJ).

Little wonder, too, that payments startups that have gone public are faring well, including the global payments company Adyen, which IPO’d on the Euronext in June of last year and has mostly seen its shares move in one direction since. Indeed, the company, valued at $2.3 billion by investors in 2015, is now valued at nearly $21 billion.

Though Checkout’s Series A is stunning for its size, according to Dealroom data, it isn’t the largest for a European company. Among other giant rounds, the U.K.-based biotech company Immunocore closed on $320 million in Series A funding in 2015. In 2017, another U.K. fintech, OakNorth, a digital bank that focuses on loans for small and medium enterprises, raised $200 million in Series A funding. (It has gone on to raise roughly $850 million altogether.)

More recently, TradePlus24, a two-year-old, Zurich, Switzerland-based fintech company that insures against default the accounts receivables of small and mid-size businesses, also raised a healthy amount: $120 million in Series A funding. Its backers include Credit Suisse and the insurance broker Kessler.

Powered by WPeMatico

Just five months after announcing £85 million in Series E funding, Monzo is already gearing up to raise additional funding, which would almost double its valuation.

As reported in the Sunday Times yesterday, the U.K. challenger bank is close to raising £100 million in further funding in a new round led by an unnamed U.S. investor. If the deal goes through, it will reportedly give Monzo a pre-money valuation of close to £2 billion, up from £1 billion in October.

Now TechCrunch has learned that the new U.S. backer is Y Combinator.

According to multiple sources within investor circles on both sides of the pond, the Silicon Valley accelerator and venture capital fund plans to invest in Monzo out of its growth fund, the vehicle it typically uses to double down on fast-growing companies within its alumni.

Notably, Monzo isn’t a graduate of YC. However, Monzo co-founder Tom Blomfield’s previous startup, the payments company GoCardless, did go through the accelerator program, making Blomfield himself an alumni.

Monzo declined to comment. Y Combinator couldn’t be reached at the time of publication and I’ll update this post should I hear back.

Meanwhile, the news that Y Combinator is lining up to invest in Monzo makes a lot of sense in a number of ways beyond Blomfield’s previous ties to the accelerator. The challenger bank already boasts a plethora of U.S. investors, such as U.S. venture capital firm General Catalyst, Thrive Capital and Stripe.

And, as TechCrunch reported exclusively, Monzo has quietly begun working on a U.S. launch. This includes setting up a small team states-side to begin laying the groundwork to bring a version of Monzo to North America. It will initially be powered by a U.S. banking partner while Monzo works on the necessary regulatory licenses to go it alone.

Monzo continues to grow at a clip here in the U.K., too. To date, the challenger bank claims more than 1.7 million customers since it launched in 2015.

Powered by WPeMatico

During my recent conversation with Peter Kraus, which was supposed to be focused on Aperture and its launch of the Aperture New World Opportunities Fund, I couldn’t help veering off into tangents about the market in general. Below is Kraus’ take on the availability of alpha generation, the Fed, inflation versus Amazon, housing, the cross-ownership of U.S. equities by a few huge funds and high-frequency trading.

Gregg Schoenberg: Will alpha be more available over the next five years than it has been over the last five?

To think that at some point equities won’t become more volatile and decline 20% to 30%… I think it’s crazy.

Peter Kraus: Do I think it’s more available in the next five years than it was in the last five years? No. Do I think people will pay more attention to it? Yes, because when markets are up to 30 percent, if you get another five, it doesn’t matter. When markets are down 30 percent and I save you five by being 25 percent down, you care.

GS: Is the Fed’s next move up or down?

PK: I think the Fed does zero, nothing. In terms of its next interest rate move, in my judgment, there’s a higher probability that it’s down versus up.

Powered by WPeMatico

Pressure is steadily mounting on U.S. lawmakers to implement comprehensive cannabis banking reform at the federal level, and that pressure is coming from all directions.

Rapid shifts in public opinion and a rising number of states with legal medical and adult-use cannabis sales have laid bare an obvious need to update our banking laws to meet the age of regulated cannabis markets. And earlier this month, Congress tackled the issue head on in a widely anticipated hearing that had huge implications for the future of banking for America’s legal cannabis industry.

The Secure and Fair Enforcement (SAFE) Banking Act was among the most notable topics discussed during the House Financial Services Committee hearing February 13, which was titled “Challenges and Solutions: Access to Banking Services for Cannabis-Related Businesses.”

The legislation, which would provide safe harbor to banks working with state-legal cannabis businesses, counts a large and diverse group of lawmakers, regulators, law enforcement professionals, financial institutions, businesses interests and trade organizations among its supporters.

House Financial Services Committee member Rep. Ed Perlmutter (D-CO), along with Rep. Denny Heck (D-WA), introduced the SAFE Banking Act in the last Congress, with 95 co-sponsors — including 13 Republicans — signing on. Twenty bipartisan co-sponsors signed onto the companion bill, introduced in the Senate by Jeff Merkley (D-OR). The two bills drew some heavyweight co-sponsors from both sides of the aisle, including Sen. Rand Paul (R-KY), Sen. Elizabeth Warren (D-MA), Sen. Cory Gardner (R-CO), Sen. Kamala Harris (D-CA) and Sen. Cory Booker (D-NJ), and in the House, Rep. Beto O’Rourke (D-TX), Rep. David Joyce (R-OH), Rep. Tulsi Gabbard (D-HI) and Rep. Adam Schiff (D-CA).

And a bipartisan group of 19 state attorneys general came together last year to urge Congress to advance legislation that would allow state-legal cannabis businesses to utilize traditional banking services available to every other legal industry in the United States.

Groups like the Credit Union National Association, the Independent Community of Bankers of America, American Bankers Association and the National Cannabis Industry Association are also vocal advocates for the measure.

As the U.S. cannabis industry continues along its steady growth trajectory, access to banking services is perhaps the most critical challenge facing operators.

And that wasn’t the first attempt in the House to address the cannabis banking problem. In 2014, House lawmakers passed an amendment to an appropriations bill (228-195) that, much like the SAFE Banking Act, would have extended legal protections to financial institutions working with state-regulated cannabis businesses. The measure failed to move through the Senate, however.

But much has changed since 2014. Ten states and Washington, DC, have now legalized cannabis for adult use; 33 states have legalized comprehensive medical cannabis programs; two in three Americans now support legalizing cannabis nationwide for recreational use, according to Gallup polling data; and a majority of older Americans — a formidable voting bloc — now supports legalization. Momentum around cannabis reform is spreading across the globe as well, with cannabis now legally available to adults for recreational use in both Canada and Uruguay, and numerous countries mulling similar reforms.

A brand new multi-billion-dollar industry has risen up in a few short years, and yet, most financial institutions in the U.S. remain reluctant to work with cannabis businesses due to fears of violating federal money laundering laws. That fear has forced the majority of cannabis businesses to operate on a cash-only basis — creating massive security risks, logistical nightmares and regulatory headaches for all parties involved.

As the U.S. cannabis industry continues along its steady growth trajectory, access to banking services is perhaps the most critical challenge facing operators. The recent House Financial Services Subcommittee hearing represents the committee’s first-ever hearing on this issue — a promising first step toward passing the SAFE Banking Act.

Sixty-seven percent of Americans across the political spectrum want Congress to enact legislation allowing financial institutions to do business with legal cannabis operators, according to polling data from think tank Third Way.

With this new Congress, there may finally be progress. Rep. Perlmutter and Rep. Heck plan to re-introduce the SAFE Banking Act in the House, and Sen. Merkley is expected to re-introduce a similar measure in the Senate. Now we need House lawmakers to prioritize this issue and move these measures through the legislature, so they can become the law of the land.

Powered by WPeMatico

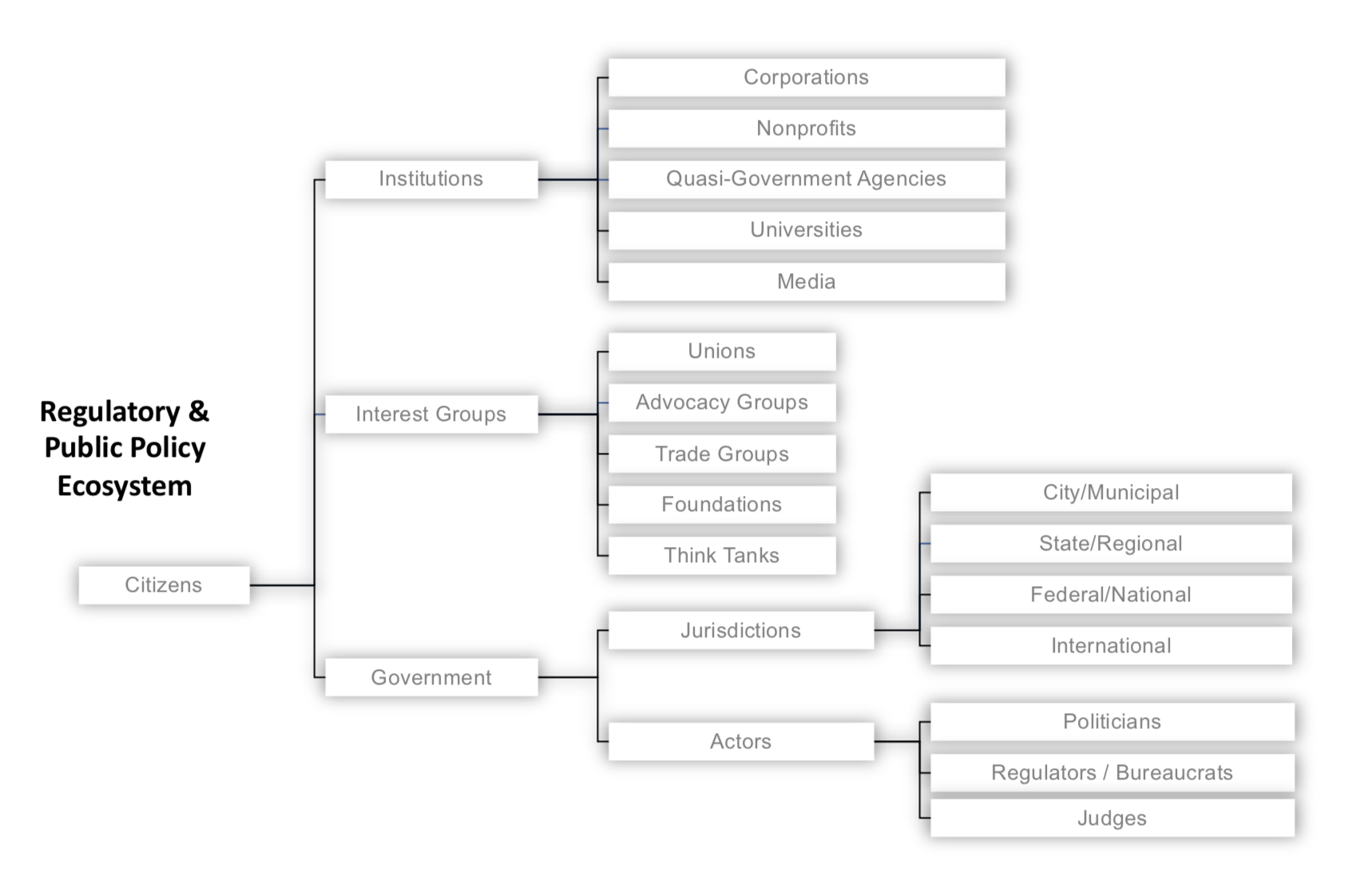

Startups are but one species in a complex regulatory and public policy ecosystem. This ecosystem is larger and more powerfully dynamic than many founders appreciate, with distinct yet overlapping laws at the federal, state and local/city levels, all set against a vast array of public and private interests. Where startup founders see opportunity for disruption in regulated markets, lawyers counsel prudence: regulations exist to promote certain strongly-held public policy objectives which (unlike your startup’s business model) carry the force of law.

Snapshot of the regulatory and public policy ecosystem. Image via Law Office of Daniel McKenzie

Although the canonical “ask forgiveness and not permission” approach taken by Airbnb and Uber circa 2009 might lead founders to conclude it is strategically acceptable to “move fast and break things” (including the law), don’t lose sight of the resulting lawsuits and enforcement actions. If you look closely at Airbnb and Uber today, each have devoted immense resources to building regulatory and policy teams, lobbying, public relations, defending lawsuits, while increasingly looking to work within the law rather than outside it – not to mention, in the case of Uber, a change in leadership as well.

Indeed, more recently, examples of founders and startups running into serious regulatory issues are commonplace: whether in healthcare, where CEO/Co-founder Conrad Parker was forced to resign from Zenefits and later fined approximately $500K; in the securities registration arena, where cryptocurrency startups Airfox and Paragon have each been fined $250K and further could be required to return to investors the millions raised through their respective ICOs; in the social media and privacy realm, where TikTok was recently fined $5.7 million for violating COPPA, or in the antitrust context, where tech giant Google is facing billions in fines from the EU.

Suffice it to say, regulation is not a low-stakes table game. In 2017 alone, according to Duff and Phelps, US financial regulators levied $24.4 billion in penalties against companies and another $621.3 million against individuals. Particularly in today’s highly competitive business landscape, even if your startup can financially absorb the fines for non-compliance, the additional stress and distraction for your team may still inflict serious injury, if not an outright death-blow.

The best way to avoid regulatory setbacks is to first understand relevant regulations and work to develop compliant policies and business practices from the beginning. This article represents a step in that direction, the fifth and final installment in Extra Crunch’s exclusive “Startup Law A to Z” series, following previous articles on corporate matters, intellectual property (IP), customer contracts and employment law.

Given the breadth of activities subject to regulation, however, and the many corresponding regulations across federal, state, and municipal levels, no analysis of any particular regulatory framework would be sufficiently complete here. Instead, the purpose of this article is to provide founders a 30,000-foot view across several dozen applicable laws in key regulatory areas, providing a “lay of the land” such that with some additional navigation and guidance, an optimal course may be charted.

The regulatory areas highlighted here include: (a) Taxes; (b) Securities; (c) Employment; (d) Privacy; (e) Antitrust; (f) Advertising, Commerce and Telecommunications; (g) Intellectual Property; (h) Financial Services and Insurance; and finally (i) Transportation, Health and Safety.

Of course, some regulations may touch on multiple regulatory areas, for example, the “Fair Credit Reporting Act” is a law ultimately about privacy, but it impacts many financial and employment-related services as well. Certain laws may therefore be cross-listed in more than one regulatory area. Also, since we can’t look at every U.S. state and city, this article will focus primarily on the federal and California state laws.

After you focus on the particular regulatory areas that may implicate your business, next reference the short quotations and links to relevant primary and secondary sources below, then work to identify the specific compliance risks you face. This is where other Extra Crunch resources can help. For example, the Verified Experts of Extra Crunch include some of the most experienced and skilled startup lawyers in practice today. Use these profiles to identify attorneys who are focused on serving companies at your particular stage and then seek out any further guidance you need to address the regulatory matters pertinent to your startup.

With that as context, the Startup Law A to Z – Regulatory Compliance checklist is below:

Before diving into further detail, it may be helpful for some readers to note the distinction between a law and a regulation. Simply put, regulations provide more detailed direction on how certain laws should be followed. So regulations are not technically laws, but they carry the force of law (including penalties for violation), since they are adopted by governmental agencies under authority granted by statute. Beyond that, understanding how laws and regulations are actually enacted is helpful to illustrate the extent to which the process is politically driven.

In the U.S., a bill must first pass both legislative branches of government, then, if signed by the executive branch, it will be codified in statute as law (Schoolhouse Rock anyone?). Once codified, the legislative branch will authorize the relevant executive department or agency to determine whether specific regulations are necessary to give the law effect. If so, those executive departments or agencies will determine what further rules are needed, and in turn, work to enforce them.

At the federal level, for example, proposed regulations are developed first through a “Notice of Proposed Rulemaking,” listed in the Federal Register and filed in the corresponding executive agency’s official docket (available at Regulations.gov). This affords the public an opportunity to comment on the regulations. After receiving comments, the filing agency may revise the proposed regulation before final rules are issued, which again will be published in the Federal Register and then filed in the agency’s official docket at Regulations.gov, before they are codified in the Code of Federal Regulations (CFR).

At nearly every step in this process then, institutions, government, and interest groups are working – sometimes at cross purposes – to shape what the law will be and how it will impact your startup.

The Startup Law A to Z – Regulatory Compliance reference guide is below:

Powered by WPeMatico