Banking

Auto Added by WPeMatico

Auto Added by WPeMatico

Less than a decade ago IPOs, acquisitions and global expansion by African startups were more possibility than reality. March saw all three from the continent’s tech scene.

Pan-African e-commerce company Jumia filed for an IPO on the New York Stock Exchange, per SEC documents and confirmation from chief executive Sacha Poignonnec.

In an updated filing, (since the March 12 original) Jumia indicated it will offer 13,500,000 ADR shares, for an offering price of $13 to $16 per share to trade under the ticker symbol “JMIA.” The IPO could raise up to $216 million for Jumia.

Since our first story (and reflected in the latest SEC docs), Mastercard Europe agreed upfront to buy $50 million in Jumia ordinary shares.

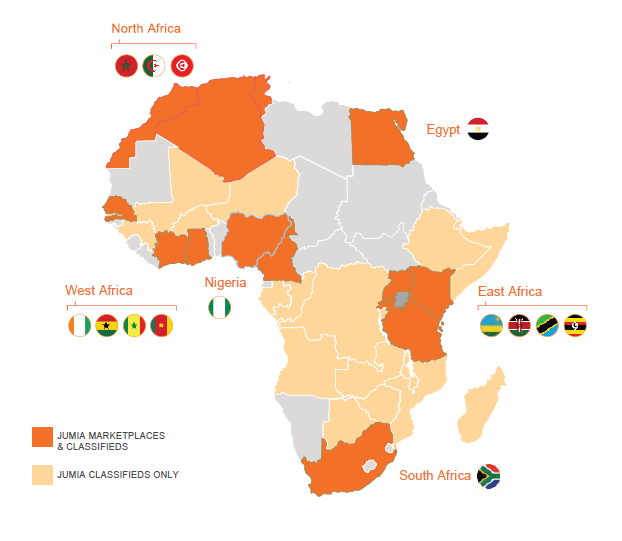

With a smooth filing process, Jumia will become the first African startup to list on a major global exchange. The company is incorporated in Germany, but maintains its headquarters in Nigeria, and operates exclusively in Africa, with 4,000 employees on the continent.

The pending IPO creates another milestone for Jumia. The venture became the first African startup unicorn in 2016, achieving a $1 billion valuation after a funding round that included Goldman Sachs, AXA and MTN.

Founded in Lagos in 2012 with Rocket Internet backing, Jumia now operates multiple online verticals in 14 African countries. Goods and services lines include Jumia Food (an online takeout service), Jumia Flights (for travel bookings) and Jumia Deals (for classifieds). Jumia processed more than 13 million packages in 2018, according to company data. The company has started to generate annual revenues over $100 million, but like many burn-rate startups, has done so while racking up big losses.

There’ll be a lot more to cover, analyze and debate pre and post Jumia’s NYSE bell toll — which could happen in coming weeks or months. For example, can Jumia generate a profit; is it really an African startup; will Jumia become an acquisition target for a big outside name or an acquirer of smaller startups in African e-commerce? Stay tuned for continuing TechCrunch coverage.

On the acquisition front, Lagos-based online lending startup OneFi bought Nigerian payment solutions company Amplify for an undisclosed amount.

OneFi is taking over Amplify’s IP, team and client network of more than 1,000 merchants to which Amplify provides payment processing services, OneFi CEO Chijioke Dozie told TechCrunch.

The purchase of Amplify caps off a busy period for OneFi. Over the last seven months the Nigerian venture secured a $5 million lending facility from Lendable, announced a payment partnership with Visa and became one of the first (known) African startups to receive a global credit rating. OneFi is also dropping the name of its signature product, Paylater, and will simply go by OneFi (for now).

Collectively, these moves represent a pivot for OneFi away from operating primarily as a digital lender, toward becoming an online consumer finance platform.

“We’re not a bank but we’re offering more banking services…Customers are now coming to us not just for loans but for cheaper funds transfer, more convenient bill payment, and to know their credit scores,” said Dozie.

OneFi will add payment options for clients on social media apps, including WhatsApp, this quarter — something in which Amplify already holds a specialization and client base. Through its Visa partnership, OneFi will also offer clients virtual Visa wallets on mobile phones and start providing QR code payment options at supermarkets, on public transit and across other POS points in Nigeria.

On the back of the acquisition, OneFi is in the process of raising a round and will look to expand internationally, considering Senegal, Côte d’Ivoire, DRC, Ghana and Egypt and Europe for Diaspora markets.

On African startups expanding globally, FlexClub — a South African venture that matches investors and drivers to cars for ride-hailing services — announced it will expand in Mexico in a partnership with Uber after closing a $1.2 million seed round led by CRE Venture Capital.

The move comes as Africa’s tech-transit space continues to produce unique mobility solutions shaped around local needs.

FlexClub touts itself as a “gig economy investment platform” that is creating new asset classes in emerging markets, according to chief executive and co-founder Tinashe Ruzane.

That asset class, for now, is ride-hail vehicles. FlexClub allows investors to go on the site and purchase a car (ultimately managed and serviced by FlexClub). The startup then connects that car to an Uber driver who uses earnings to pay a weekly rental charge.

Those fees generate monthly fixed-rate interest income for the investor. The driver has the option of buying the car after 12 months, with a descending purchase price over time.

FlexClub’s platform manages the investment, rental income and disbursement of funds across all parties. The startup also handles insurance, maintenance and upkeep of the cars.

Ruzane envisions this as a model to finance multiple asset classes in emerging markets — where lending options are fewer for individuals who may not have credit histories.

“Our goal is to make this completely passive… where investors can invest in different kinds of assets on our platform, login to a dash, and see this is how my five cars in South Africa are doing, my vans in Mexico, my motorbikes in Indonesia — with a diversified portfolio around the world,” he explained.

FlexClub will begin work matching investors to cars and Uber drivers in Mexico in April. The startup sees opportunities to move into other mobility classes, such as Africa’s ride-hail motorcycle taxi and three-wheel tuk-tuk market, CEO Tinashe Ruzane told TechCrunch in this feature.

And finally, francophone Africa will see a boost in funds and support for startups. The Dakar Network Angels group launched last month, making its first investment to cleantech venture Coliba — an Ivorian startup that uses a mobile app to coordinate waste recycling

The deal is part of Dakar Network Angels’ mission of convening experts and capital to bridge the resource gap for startups in French-speaking Africa — or 24 of the continent’s 54 countries.

The organization — which goes by DNA for short — will offer seed fund investments of between $25,000 to $100,000 to early-stage ventures with high growth potential. These rounds will come with the entrepreneurial guidance of DNA’s angel network.

Launched in Senegal, the organization’s founder Marieme Diop — a VC investor at Orange Digital Ventures — named the goal of bridging VC disparities between francophone and non-francophone Africa as the primary driver for DNA. She pointed to funding data by Partech, indicating that 76 percent of investment to African startups goes to three English-speaking countries — Nigeria, Kenya and South Africa.

To gain consideration for DNA investment, startups must gain referral by a member. DNA will take a minority stake (less than 10 percent) in ventures that receive seed funds and provide program mentorship until exits, Diop told TechCrunch.

To become an angel, members must commit to investing a minimum of $10,000 a year (for those coming on as individuals), $20,000 (for corporates) and be on hand to support the portfolio startups, according to DNA’s Corporate Membership Charter.

More Africa Related Stories @TechCrunch

African Tech Around The Net

Powered by WPeMatico

The internet is often lauded for the potential to increase the impact of a range of primary services in emerging markets, including education, commerce, banking and healthcare. While many of those platforms are now being built, a few are finding that a hybrid approach combining online and offline is advantageous.

That’s exactly what Jio Health, a “full stack” (forgive the phrase) healthcare startup is bringing to consumers in Southeast Asia, starting in Vietnam.

The company started as a U.S.-based venture that worked with healthcare providers around the “Obamacare” initiative, before sensing the opportunity overseas and relocating to Vietnam, the Southeast Asian market of 95 million people and a fast-growing young population.

Today, it operates an online healthcare app and a physical facility in Saigon; it also has licenses for prescriptions and over the counter drug sales. The serviced launched nearly a year ago; already the company has some 130 staff, including 70 caregivers — including doctors — and a tech team of 30.

The idea is to offer services digitally, but also provide a physical location for when it is needed. Therein, the company ensures that “every element of that journey” is controlled and of the required standard; that’s in contrast to services that partner with hospitals or other care centers.

The scope of Jio Health’s services range from pediatrics to primary care, chronic disease management and ancillary services, which will soon cover areas like eye care, dermatology and cancer.

“Our initial research [before moving] found that healthcare in Vietnam was unlike the U.S.,” Raghu Rai, founder and CEO of Jio Health, told TechCrunch in an interview. “Spending is primarily driven by the consumer (out of pocket) and there’s no real digital infrastructure to speak of.”

Rai — a U.S. citizen — said doctors typically “have minutes per patient” and get through “hundreds” of consultations in every morning shift. That gave him an idea to make things more efficient.

“We can probably address north of 80 percent of consumers’ health needs,” he said of Jio Health,” but we also have referral partnerships with certain hospitals.”

Raghu Rai is CEO and founder of Jio Health

The process begins when a consumer downloads the Jio Health app and inputs primary information. A representative is then dispatched to visit the consumer in person, potentially within “hours” of the submission of information, according to Rai.

He believes that Jio Health can save its users money and time by using remote consultancy for many diagnoses. The company also works with health insurance companies for areas like annual checkups, and Rai said that McDonald’s and 7-Eleven are among the corporations that offer Jio Health among the providers for their staff; they’re not exclusive.

This week, Jio Health announced that it has closed a $5 million Series A funding from Southeast Asia’s Monk’s Hill Ventures . Rai said the company plans to use the capital for expansion. In particular, he said, the company is adding new care categories this month — including eye care and dermatology — and it is working toward expanding its brand through marketing.

Further down the line, Rai said the company hopes to expand to Hanoi before the end of this year. While there is interest in moving into other markets within Southeast Asia, that isn’t about to happen soon.

“We have begun to investigate other markets, but at this point feel the market in Vietnam is substantial in itself,” he told TechCrunch. “It’s very plausible that we’d be looking at international expansion plans in 2020… we’re going to be focused on Southeast Asia.”

Powered by WPeMatico

Social investing and trading platform eToro announced that it has acquired Danish smart contract infrastructure provider Firmo for an undisclosed purchase price.

Firmo’s platform enables exchanges to execute smart financial contracts across various assets, including crypto derivatives, and across all major blockchains. Firmo founder and CEO Dr. Omri Ross described the company’s mission as “…enabl[ing] our users to trade any asset globally with instant settlement by tokenizing assets and executing all essential trade processes on the blockchain.” Firmo’s only disclosed investment, according to data from Pitchbook, came in the form of a modest pre-seed round from the Copenhagen Fintech Lab accelerator.

Firmo’s mission aligns well with that of eToro — which is equal parts trading platform, social network and educational resource for beginner investors — with the company having long communicated hopes of making the capital markets more open, transparent and accessible to all users and across all assets. By gobbling up Firmo, eToro will be able to accelerate its development of offerings for tokenized assets.

The acquisition represents the latest step in eToro’s broader growth plan, which has ramped up as of late. Earlier in March, the company launched a crypto-only version of its platform in the US, as well as a multi-signature digital wallet where users can store, send and receive cryptocurrencies.

The Firmo deal and eToro’s other expansion activities fit squarely into the company’s belief in the tokenization of assets and the immense, sector-defining opportunity that it creates. Etoro believes that asset tokenization and the movement of financial services onto the blockchain are all but inevitable and the company has employed the long-tailed strategy of investing heavily in related blockchain and crypto technologies despite the ongoing crypto winter.

“Blockchain and the tokenization of assets will play a major role in the future of finance,” said eToro co-founder and CEO Yoni Assia. “We believe that in time all investible assets will be tokenized and that we will see the greatest transfer of wealth ever onto the blockchain.” Assia expressed a similar sentiment in a recent conversation with TechCrunch, stating “We think [the tokenization of assets] is a bigger opportunity than the internet…”

After the acquisition, Firmo will operate as an internal R&D arm within eToro focused on developing blockchain-oriented trade execution and the infrastructure behind the digital representation of tokenized assets.

“The Firmo team has done ground-breaking work in developing practical applications for blockchain technology which will facilitate friction-less global trading,” said Assia.

“The adoption of smart contracts on the blockchain increases trust and transparency in financial services. We are incredibly proud and excited that [Firmo] will be joining the eToro family. We believe that together we have a very bright future and look forward to pursuing our shared goal to become the first truly global service provider allowing people to trade, invest and save.”

Powered by WPeMatico

Atlanta-based Movius, a company that allows companies to assign a separate business number for voice calls and texting to any phone, today announced that it has raised a $45 million Series D round led by JPMorgan Chase, with participation from existing investors PointGuard Ventures, New Enterprise Associates and Anschutz Investment company. With this, the company has now raised a total of $100 million.

In addition to the new funding, Movius also today announced that it has brought on former Adobe and Sun executive John Loiacono as its new CEO. Loiacono was also the founding CEO of network analytics startup Jolata.

“The Movius opportunity is pervasive. Almost every company on planet Earth is mobilizing their workforce but are challenged to find a way to securely interact with their customers and constituents using all the preferred communication vehicles – be that voice, SMS or any other channel they use in their daily lives,” said Loiacono. “I’m thrilled because I’m joining a team that features highly passionate and proven innovators who are maniacally focused on delivering this very solution. I look forward to leading this next chapter of growth for the company.”

Sanjay Jain, the chief strategy officer at Hyperloop Transportation Technologies, and Larry Feinsmith, the head of JPMorgan Chase’s Technology Innovation, Strategy & Partnerships office, are joining the company’s board.

Movius currently counts more than 1,400 businesses as its customers, and its carrier partners include Sprint, Telstra and Telefonica. What’s important to note is that Movius is more than a basic VoIP app on your phone. What the company promises is a carrier-grade network that allows businesses to assign a second number to their employees’ phones. That way, the employer remains in charge, even as employees bring their own devices to work.

Powered by WPeMatico

Stash, the fintech startup and app that aims to introduce new people to the world of investing, is unveiling some interesting new services while also announcing that it has raised more funding to expand its business. The company is introducing mobile-based banking accounts from Green Dot Bank, and, alongside it, a new rewards program called “Stock-Back.” When users spend money using their Stash accounts, they get “points” — which are either stocks in the companies where they are buying goods, or shares in ETFs approved by Stash. On top of that, Stash also said it raised a Series E of $65 million that it will be using to grow its business on the back of these two launches.

A spokesperson for the company said that Stash is not disclosing the full round of investors in this round. For context, Stash was valued at $350 million post-money in its Series D, according to figures from PitchBook, and a source says the valuation is now “much higher” than $400 million.

But from the looks of it, the $65 million appears to include participation from Breyer Capital, a previous investor whose founder Jim Breyer has heartily endorsed the new Stock-Back service and accompanying loyalty program that’s tied in with it, which was tested early with companies like Netflix, T-Mobile and Chipotle all offering stock when people used their Stash accounts to pay for goods and services at the companies.

“I have invested in and served on the Board of many leading companies, and it’s clear how a program like Stock-Back can power immense brand loyalty,” he said in a statement today. “The early data shows unequivocally that share ownership drives increased sales and customer appreciation. This innovative new technology from STASH will have CEOs and CMOs knocking on their door.”

From what we understand, the round was led by a private institutional investor and includes 40 percent existing and 60 percent new investors. Previous backers in addition to Breyer include Union Square Ventures, Coatue Management, Entree, Goodwater and Valar. “We’re really excited and proud to be working with this incredible group of VCs,” the spokesperson noted.

The Green Dot-powered banking service comes with the core features that will sound familiar to those who have used or looked at next-generation banking services before. It will include a debit card-based account, no overdraft or monthly maintenance fees, access to a network of ATMs that can be used for free and direct deposit services, as well as “personal guidance” for their financial planning activities, from saving to investing.

Stash is part of a wave of fintech startups — others include the likes of Robinhood, Acorns, YieldStreet, Revolut and many others — that have tapped into the popularity of apps and the advent of new financial services technology to democratise how individuals can save, spend, invest, borrow and lend money, moving many of those operations and transactions out of the hands of the big incumbent players who used to control them.

The average age of a Stash user is 29 and average income is less than $50,000 per year, and tying in transactions made using Stash’s banking service — by way of reward points that are being picked up incidentally — will make it even more seamless for these users to take some of their money and invest with it, while at the same time demystifying some of the process and making it more likely that those users will choose to invest even more down the line.

The idea of tying investments to what you are actually purchasing is a clever one. For a startup whose user base includes no-nonsense professionals from fields like teaching, nursing and retail, this is the embodiment of putting your money where your mouth is — literally speaking, as the investments can include things like shares in Chipotle each time you buy food there, and T-Mobile every time you pay your phone bill for all the talking you do.

Stash is positioning Stock-Back as a rewards program, with the percentages varying by business or brand and going as high as five percent in Stock-Back in some cases — as is the case, at launch, when people use their Stash debit cards to pay their Spotify and Netflix dues.

Ultimately, the aim of this is to present a way for ordinary, modestly-salaried people not only to potentially make money, but to be better engaged in how financial systems work, and how their daily actions impact that — the idea being that this knowledge can only help them in the long run.

“80% of Americans are living paycheck-to-paycheck. Stock-Back is our way of utilizing STASH’s smart, patent-pending technology to help people build better financial habits and invest in their future,” said co-founder and president, Ed Robinson, in a statement. “Our ability to give customers the opportunity to save and build portfolios that mirror their spending behavior and preferences is incredibly powerful.”

Powered by WPeMatico

San Francisco-based mobile banking startup Chime announced this morning it has raised an additional $200 million in Series D financing led by DST Global, valuing its business at $1.5 billion. The oversubscribed round also included participation from new investors Coatue, General Atlantic, ICONIQ Capital and Dragoneer Investment Group, along with existing investors Menlo Ventures, Forerunner Ventures, Cathay Innovation and others.

To date, Chime has raised approximately $300 million, including last year’s $70 million Series C, which then saw the company valued at $500 million.

With the new funding, Chime has now raised the most funding and has the highest valuation among other U.S. challenger banks.

The company is now one of several going after a younger, millennial audience who no longer sees the need for banks with physical branches, and who are sick of being nickel-and-dimed by bigger banks’ numerous fees. Like others in this space, Chime offers a “no fees” bank account, which won’t penalize users for things like dropping below a minimum balance or even overdrafts.

On top of this is a modern-day banking app with features that make it look like it was actually built by a technology company — not a traditional bank. That’s because its team’s background is a mix of both tech and finance. Chime’s co-founder and CEO Chris Britt previously worked at Flycast, was an early comScore employee and worked at Visa and Green Dot; co-founder and CTO Ryan King spent time at Plaxo and Comcast before Chime.

Chime also includes a couple of innovative features that help differentiate it from the other mobile banking apps on the market. This includes an automatic savings feature that rounds up purchases to pocket the change; another feature that automatically saves 10 percent of your paycheck into Chime’s savings account; and one that offers a no-fee paycheck advance that makes your money available sooner.

To date, customers have opened more than 3 million FDIC-insured bank accounts on Chime, which makes it the largest brand in its category, the company claims. (This appears to be true. SoFi had 500,000 members as of last year. Simple doesn’t disclose its account base beyond “hundreds of thousands.” Moven and Varo Money are smaller, according to American Banker’s round-up.)

Its size, scale and growth trajectory, perhaps, have aided Chime in poaching a few execs from its other fintech businesses — including rivals. For example, the company recently added Chime VP, Risk Brian Mullins, who was the former head of Risk Ops at Square; and Chime GM, Lending Aaron Plante, who was the former Business Unit leader for Student Loans at SoFi.

The company says it plans to use the new investment to continue to accelerate growth and launch new products, including those in lending and credit. It also plans to double its San Francisco-based team to more than 200 employees and expand its leadership.

“We’re excited to welcome some of the world’s leading growth investors to Chime,” said Britt in a statement about the funding. “Banking should be free, helpful and easy to use but traditional banks are reluctant to embrace this reality. We aim to set a new standard in the industry by using technology to create services that are truly aligned with the best interests of consumers.”

Powered by WPeMatico

Figure, a 13-month-old, San Francisco-based company that says it uses blockchain technology to provide home equity loans online in as little as five days, has raised a whole lot of money in not a lot of time: $120 million to date, including $65 million in fresh funding from RPM Ventures and partners at DST Global, with participation from DCG, Nimble Ventures, Morgan Creek and earlier investors Ribbit Capital and DCM.

The money isn’t entirely surprising, given who founded the company — Mike Cagney, who founded SoFi and built it into a major player in student loan refinancing in the U.S. before leaving amid allegations of sexual harassment and an anything-goes corporate culture that saw at least two former employees sue the company.

Today, SoFi has moved on under the leadership of CEO Anthony Noto, a former Twitter executive who is working to reshape SoFi from a lending company into more of a full-fledged financial services company, with savings and checking accounts, as well as exchange-traded funds, all with the aim of making its platform stickier than in the past.

It may be a bigger endeavor than Noto had realized. Though Cagney once predicted the company would IPO in 2018 or 2019, SoFi isn’t even considering a public offering this year, Noto told reporters earlier this week.

Cagney has meanwhile moved on, too, though he still seems set on taking on traditional banks. Indeed, while Figure is providing home loans today — it says it has provided more than 1,500 home equity lines to date — it’s also moving to diversify into new areas, including wealth management, unsecured consumer loans and checking accounts offered (for now) in partnership with an existing bank.

Interestingly, Figure, which employs 100 people, is targeting a very different demographic than did SoFi, as Cagney told American Banker recently. Whereas SoFi marketed to young people earning high salaries, Figure is going after older customers who may not be seeing much in the way of income but have much of their wealth tied up in their homes instead.

Given that older Americans are projected to outnumber children for the first time in history by 2030, according to U.S. census data, Cagney clearly sees the writing on the wall.

Unsurprisingly, he’s not the only one. Other startups trying to make it easier for Americans to borrow against their homes include Point, a roughly four-year-old startup that lends capital to people and receives partial ownership in their homes in return.

Cagney co-founded Figure with his wife, June Ou, who is the company’s chief operating officer. She was previously chief technology officer at SoFi.

As for its culture and lingering questions that customers and potential partners may have about what happened at SoFi, Cagney — who has said he had consensual sexual relationships with female subordinates at SoFi — insists that Figure is benefiting from lessons learned.

At SoFi, he told American Banker, “[W]e grew so fast and we never really understood what we were going to grow into, and culture never took a front seat.” Figure meanwhile has a “very clear adherence to a no-asshole policy.”

Powered by WPeMatico

Lunar Way, the Nordic banking app that’s riding new EU regulation to help inject more competition into the region, has raised €13 million in new funding. The round is led by SEED Capital, with participation from Greyhound Capital, Socii Capital and a number of individual investors from the financial services industry.

It also comes shortly after Lunar Way announced it had attained a PISP payments license, meaning that the fintech can offer a more comprehensive banking feature-set, including making payments out of third-party bank accounts on a user’s behalf.

This, says Lunar Way founder Ken Villum Klausen, also paves the way for the startup to crack open the “Nordic clearing system monopoly,” which has traditionally made it difficult for new banking entrants.

“The new payment license grants us the option to instruct underlying banks to do payments, pay bills or even pay in a retail environment from their accounts,” explains Klausen. “So when you sign up, you’re able to connect to an existing bank-account in the sign up flow. And after that control all your finances through our platform.”

In addition, Lunar Way has a PSD2 AISP license, so that it is regulated to “co-own the transaction data,” which Klausen says Lunar Way can use in the company’s PFM features and for new products.

“The [Lunar Way] product offers all the fundamentals from a banking app. You can pay bills, transfer money, set a budget, do saving-goals, manage your card etc. We also have a few subscription-based credit lines, where you pay a monthly fee [for credit],” he says.

In Denmark, Lunar Way also acts as a “NemKonto” — or national Danish account — a type of bank account that the Danish government stipulates by law that all citizens and businesses must have.

Adds Klausen: “It has taken a few years to build our app to suit the different demands of the Nordic countries, but now we are a serious competitor to traditional banks. Our aim is — and have always been — to fundamentally change the status quo of banking. We’re now welcoming more than 10,000 new users a month and counting, which is substantial considering the fact that the Nordics’ total addressable market is 27 million people.”

Meanwhile, Lunar Way says it will use the funding to help accelerate the banking app’s growth, in a bid to reach further scale across the Nordics. I also understand the fintech is already gearing up for a new funding round pegged for later this summer.

Powered by WPeMatico

It was the Lehman Brothers of blockchain. 850,000 Bitcoin disappeared when cryptocurrency exchange Mt. Gox imploded in 2014 after a series of hacks. The incident cemented the industry’s reputation as frighteningly insecure. Now a controversial crypto celebrity named Brock Pierce is trying to get the Mt. Gox flameout’s 24,000 victims their money back and build a new company from the ashes.

Pierce spoke to TechCrunch for the first interview about Gox Rising — his plan to reboot the Mt. Gox brand and challenge Coinbase and Binance for the title of top cryptocurrency exchange. He claims there’s around $630 million and 150,000 Bitcoin waiting in the Mt. Gox bankruptcy trust, and Pierce wants to solve the legal and technical barriers to getting those assets distributed back to their rightful owners.

The consensus from several blockchain startup CEOs I spoke with was that the plot is “crazy”, but that it also has the potential to right one of the biggest wrongs marring the history of Bitcoin.

But the story starts with Magic: The Gathering. Mt. Gox launched in 2006 as a place for players of the fantasy card game to trade monsters and spells before cryptocurrency came of age. The Magic: The Gathering Online eXchange wasn’t designed to safeguard huge quantities of Bitcoin from legions of hackers, but founder Jed McCaleb pivoted the site in 2010. Seeking to focus on other projects, he gave 88 percent of the company to French software engineer Mark Karpeles, and kept 12 percent. By 2013, the Tokyo-based Mt. Gox had become the world’s leading cryptocurrency exchange, handling 70 percent of all Bitcoin trades. But security breaches, technology problems, and regulations were already plaguing the service.

Then everything fell apart. In February 2014, Mt. Gox halted withdrawls due to what it called a bug in Bitcoin, trapping assets in user accounts. Mt. Gox discovered that it had lost over 700,000 Bitcoins due to theft over the past few years. By the end of the month, it had suspended all trading and filed for bankruptcy protection, which would contribute to a 36 percent decline in Bitcoin’s price. It admitted that 100,000 of its own Bitcoin atop 750,000 owned by customers had been stolen.

Mt. Gox is now undergoing bankruptcy rehabilitation in Japan overseen by court-appointed trustee and veteran bankruptcy lawyer Nobuaki Kobayashi to establish a process for compensating the 24,000 victims who filed claims. There’s now 137,892 Bitcoin, 162,106 Bitcoin Cash, and some other forked coins in Mt. Gox’s holdings, along with $630 million from the sale of 25 percent of the Bitcoin Kobayashi handled at a precient price point above where it is today. But five years later, creditors still haven’t been paid back.

Brock Pierce, the eccentric crypto celebrity

Pierce had actually tried to acquire Mt. Gox in 2013. The child actor known from The Mighty Ducks had gone on to work with a talent management company called Digital Entertainment Network. But accusations of sex crime led Pierce and some team members to flee the US to Spain until they were extradited back. Pierce wasn’t charged and paid roughly $21,000 to settle civil suits, but his cohorts were convicted of child molestation and child pornography.

The situation still haunts Pierce’s reputation and makes some in the industry apprehensive to be associated with him. But he managed to break into the virtual currency business, setting up World Of Warcraft gold mining farms in China. He claims to have eventually run the world’s largest exchanges for WOW Gold and Second Life Linden Dollars.

Soon Pierce was becoming a central figure in the blockchain scene. He co-founded Blockchain Capital, and eventually the EOS Alliance as well as a “crypto utopia” in Puerto Rico called Sol. His eccentric, Burning Man-influenced fashion made him easy to spot at the industry’s many conferences.

As Bitcoin and Mt. Gox rose in late 2012, Pierce tried to buy it, but “my biggest investor was Goldman Sachs. Goldman was not a fan of me buying the biggest Bitcoin exchange” due to the regulatory issues, Pierce tells me. But he also suspected the exchange was built on a shaky technical foundation that led him to stop pursuing the deal. “I thought there was a big risk factor in the Mt. Gox back-end. That was may intuition and I’m glad I was because my intuition was dead right.”

After Mt. Gox imploded, Pierce claims his investment group Sunlot Holdings successfully bought founder McCaleb’s 12 percent stake for 1 Bitcoin, though McCaleb says he didn’t receive the Bitcoin and it’s not clear if the deal went through. Pierce also claims he had a binding deal with Karpeles to buy the other 88 percent of Mt. Gox, but that Karpeles tried to pull out of the deal that remains in legal limbo.

The Sunlot has since been trying to handle the bankruptcy proceedings, but that arrangement was derailed by a lawsuit from CoinLab. That company had partnered with Mt. Gox to run its North American operations but claimed it never received the necessary assets, and sued Mt. Gox for $75 million, though Mt. Gox countersued saying CoinLab wasn’t legally certified to run the exchange in the US and that it hadn’t returned $5.3 million in customer deposits. For a detailed account the tangle of lawsuits, check out Reuters’ deep-dive into the Mt. Gox fiasco.

CoinLab co-founder Peter Vessenes

This week, CoinLab co-founder Peter Vessenes increased the claim and is now seeking $16 billion. Pierce alleges “this is a frivolous lawsuit. He’s claiming if [the partnership with Mt. Gox] hadn’t been cancelled, CoinLab would have been Coinbase and is suing for all the value. He believes Coinbase is worth $16 billion so he should be paid $16 billion. He embezzled money from Mt. Gox, he committed a crime, and he’s trying to extort the creditors. He’s holding up the entire process hoping he’ll get a payday.” Later, Pierce reiterated that “Coinlab is the villain trying to take all the money and see creditors get nothing.” Industry sources I spoke to agreed with that characterization

Mt. Gox customers worried that they might only receive the cash equivalent of their Bitcoin according to the currency’s $486 value when Gox closed in 2014. That’s despite the rise in Bitcoin’s value rising to around 7X that today, and as high as 40X at the currency’s peak. Luckily, in June 2018 a Japanese District Court halted bankruptcy proceedings and sent Mt. Gox into civil rehabilitation which means the company’s assets would be distributed to its creditors (the users) instead of liquidated. It also declared that users would be paid back their lost Bitcoin rather than the old cash value.

Now Pierce and Sunlot are attempting another rescue of Mt. Gox’s $1.2 billion assets. He wants to track down the remaining cryptocurrency that’s missing, have it all fairly valued, and then distribute the maximum amount to the robbed users with Mt. Gox equity shareholders including himself receiving nothing. That’s a much better deal for creditors than if Mt. Gox paid out the undervalued sum, and then shareholders like Pierce got to keep the Bitcoins or proceeds of their sale at today’s true value. “I‘ve been very blessed in my life I did commit to giving my first billion away” Pierce notes, joking that this plan could account for the first $700 million he plans to ‘donate’.

“Like Game Of Thrones, the last season of Mt. Gox hasn’t been written” Pierce tells me, speaking in terms HBO’s Silicon Valley would be quick to parody. “What kind of ending do we want to make for it? I’m a Joseph Campbell fan so I’m obviously going to go with a hero’s journey, with a rise and a fall, and then a rise from the ashes like a phoenix.”

But to make this happen, Sunlot needs at least half of those Mt. Gox users seeking compensation, or roughly 12,000 that represent the majority of assets, to sign up to join a creditors committee. That’s where GoxRising.com comes in. The plan is to have users join the committee there so they can present a united voice to Kobayashi about how they want Mt. Gox’s assets distributed. “I think that would allow the process to move faster than it would otherise. Things are on track to be resolved in the next three to five years. If [a majority of creditors sign on] this could be resolved in maybe 1 year.

Beyond providing whatever the Mt. Gox estate pays out, Pierce wants to create a Gox Coin that gives original Mt Gox creditors a stake in the new company. He plans to have all of Mt. Gox’s equity wiped out, including his own. Then he’ll arrange to finance and tokenize an independent foundation governed by the creditors that will seek to recover additional lost Mt. Gox assets and then distribute them pro rata to the Gox Coin holders. There are plenty of unanswered questions about the regulatory status of a Gox Coin and what holders would be entitled to, Pierce admits.

Meanwhile, Pierce is bidding to buy the intangibles of Mt. Gox, aka the brand and domain. He wants to then relaunch it as a Gox or Mt. Gox exchange that doesn’t provide custody itself for higher security.

“We want to offer [creditors] more than the bankruptcy trustee can do on its own” Pierce tells me. He concedes that the venture isn’t purely altruistic. “If the exchange is very successful I stand to benefit sometime down the road.” Still, he stands by his plan, even if the revived Mt. Gox never rises to legitimately challenge Binance, Coinbase, and other leading exchanges. Pierce concludes, “Whether we’re successful or not, I want to see the creditors made whole.” Those creditors will have to decide for themselves who to trust.

Powered by WPeMatico

Many major companies, like Air Canada, Hollister and Expedia, are recording every tap and swipe you make on their iPhone apps. In most cases you won’t even realize it. And they don’t need to ask for permission.

You can assume that most apps are collecting data on you. Some even monetize your data without your knowledge. But TechCrunch has found several popular iPhone apps, from hoteliers, travel sites, airlines, cell phone carriers, banks and financiers, that don’t ask or make it clear — if at all — that they know exactly how you’re using their apps.

Worse, even though these apps are meant to mask certain fields, some inadvertently expose sensitive data.

Apps like Abercrombie & Fitch, Hotels.com and Singapore Airlines also use Glassbox, a customer experience analytics firm, one of a handful of companies that allows developers to embed “session replay” technology into their apps. These session replays let app developers record the screen and play them back to see how its users interacted with the app to figure out if something didn’t work or if there was an error. Every tap, button push and keyboard entry is recorded — effectively screenshotted — and sent back to the app developers.

Or, as Glassbox said in a recent tweet: “Imagine if your website or mobile app could see exactly what your customers do in real time, and why they did it?”

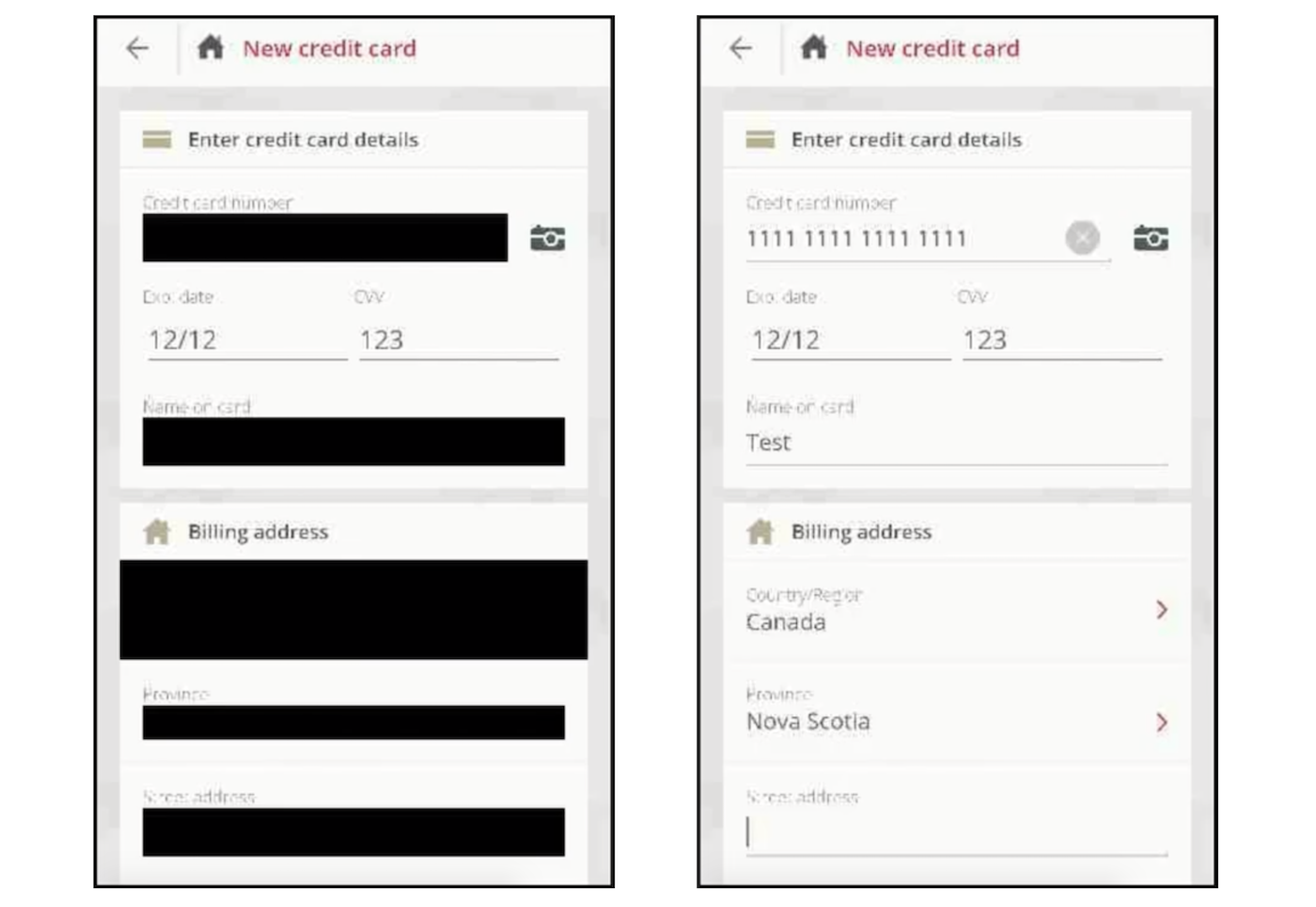

The App Analyst, a mobile expert who writes about his analyses of popular apps on his eponymous blog, recently found Air Canada’s iPhone app wasn’t properly masking the session replays when they were sent, exposing passport numbers and credit card data in each replay session. Just weeks earlier, Air Canada said its app had a data breach, exposing 20,000 profiles.

“This gives Air Canada employees — and anyone else capable of accessing the screenshot database — to see unencrypted credit card and password information,” he told TechCrunch.

In the case of Air Canada’s app, although the fields are masked, the masking didn’t always stick (Image: The App Analyst/supplied)

We asked The App Analyst to look at a sample of apps that Glassbox had listed on its website as customers. Using Charles Proxy, a man-in-the-middle tool used to intercept the data sent from the app, the researcher could examine what data was going out of the device.

Not every app was leaking masked data; none of the apps we examined said they were recording a user’s screen — let alone sending them back to each company or directly to Glassbox’s cloud.

That could be a problem if any one of Glassbox’s customers aren’t properly masking data, he said in an email. “Since this data is often sent back to Glassbox servers I wouldn’t be shocked if they have already had instances of them capturing sensitive banking information and passwords,” he said.

The App Analyst said that while Hollister and Abercrombie & Fitch sent their session replays to Glassbox, others like Expedia and Hotels.com opted to capture and send session replay data back to a server on their own domain. He said that the data was “mostly obfuscated,” but did see in some cases email addresses and postal codes. The researcher said Singapore Airlines also collected session replay data but sent it back to Glassbox’s cloud.

Without analyzing the data for each app, it’s impossible to know if an app is recording a user’s screens of how you’re using the app. We didn’t even find it in the small print of their privacy policies.

Apps that are submitted to Apple’s App Store must have a privacy policy, but none of the apps we reviewed make it clear in their policies that they record a user’s screen. Glassbox doesn’t require any special permission from Apple or from the user, so there’s no way a user would know.

Expedia’s policy makes no mention of recording your screen, nor does Hotels.com’s policy. And in Air Canada’s case, we couldn’t spot a single line in its iOS terms and conditions or privacy policy that suggests the iPhone app sends screen data back to the airline. And in Singapore Airlines’ privacy policy, there’s no mention, either.

We asked all of the companies to point us to exactly where in its privacy policies it permits each app to capture what a user does on their phone.

Only Abercombie responded, confirming that Glassbox “helps support a seamless shopping experience, enabling us to identify and address any issues customers might encounter in their digital experience.” The spokesperson pointing to Abercrombie’s privacy policy makes no mention of session replays, neither does its sister-brand Hollister’s policy.

“I think users should take an active role in how they share their data, and the first step to this is having companies be forthright in sharing how they collect their users data and who they share it with,” said The App Analyst.

When asked, Glassbox said it doesn’t enforce its customers to mention its usage in their privacy policy.

“Glassbox has a unique capability to reconstruct the mobile application view in a visual format, which is another view of analytics, Glassbox SDK can interact with our customers native app only and technically cannot break the boundary of the app,” the spokesperson said, such as when the system keyboard covers part of the native app, “Glassbox does not have access to it,” the spokesperson said.

Glassbox is one of many session replay services on the market. Appsee actively markets its “user recording” technology that lets developers “see your app through your user’s eyes,” while UXCam says it lets developers “watch recordings of your users’ sessions, including all their gestures and triggered events.” Most went under the radar until Mixpanel sparked anger for mistakenly harvesting passwords after masking safeguards failed.

It’s not an industry that’s likely to go away any time soon — companies rely on this kind of session replay data to understand why things break, which can be costly in high-revenue situations.

But for the fact that the app developers don’t publicize it just goes to show how creepy even they know it is.

Got a tip? You can send tips securely over Signal and WhatsApp to +1 646-755–8849. You can also send PGP email with the fingerprint: 4D0E 92F2 E36A EC51 DAAE 5D97 CB8C 15FA EB6C EEA5.

Powered by WPeMatico