Banking

Auto Added by WPeMatico

Auto Added by WPeMatico

Bitcoin turned 10 years old, a milestone for a technology that few have used and even fewer understand. Ultimately, the blockchain it wrought could be the biggest change to banking, finance and politics ever — or it could be a dud. The jury is still out, but let’s take a walk down memory lane and see just how the product grew from White Paper to world beater.

Powered by WPeMatico

Nearly a year after German fintech startup N26 announced that it would launch its service in the U.K., the company is launching in the U.K. N26 is already quite popular in the Eurozone, with more than 1.5 million customers. In this new market, it will face tough competition from existing players, such as Revolut, Monzo, Starling and many others.

N26 is going to roll out its product in multiple phases. Some lucky few will be able to open an account right away. The startup will then go through its waiting list — 50,000 people already left their email addresses to express interest. After that, anybody will be able to download the app and sign up.

This might sound like a convoluted process, but N26 expects a full public launch in just a few weeks. So it should be quite quick if everything goes as planned.

So what can you expect exactly? British customers will get all the basic N26 stuff with one killer feature — U.K. account numbers and sort codes. This way, customers will be able to receive payments and share banking information with their utility providers just like they would with a regular Barclays or Lloyds account.

When you open an N26 account, you get a true bank account and a MasterCard. Basic accounts are free, and N26 has a proper banking license — your deposits up to €100,000 are guaranteed by the European deposit guarantee scheme. You can then send and receive money and pay with your card. Sending money to other N26 users is instantaneous (they call it MoneyBeam).

N26 recently launched Spaces, a new feature that lets you create sub accounts and put some money aside. It’s still limited, but the company plans to add more features.

Your MasterCard works like any other challenger bank. Every time you use it, you receive a push notification. You can set payment and withdrawal limits, lock your card if you lose it and reset your PIN code. N26 will also bring Black and Metal plans to the U.K.

Let’s be honest, the elephant in the room is Revolut . The company has hundreds of thousands (if not over a million) customers in the U.K. N26 lets you do many of the things you can already do with your Revolut account.

So let me point out a few differences. As I noted, N26 has a banking license and U.K. banking information. N26 cards work in Apple Pay and Google Pay.

When it comes to international payments, N26 lets you pay with your card anywhere in the world without any additional fee. The company uses MasterCard’s conversion rates. Revolut first converts the money with its forex feature and then lets you spend your money.

There are an infinite number of forum posts about the exchange rates you’ll get. Sometimes Revolut is cheaper, sometimes N26 is cheaper. It mostly depends on the day of the week (Revolut conversion rates are more expensive on the weekend) and the currency. Unless you plan to spend tens of thousands of GBP during your vacation, you won’t see a huge difference on your bank statement.

Revolut also has many more features than N26. You can insure your phone, buy bitcoins, buy travel insurance, create virtual cards and more. It’s clear that N26 and Revolut have two different styles.

Revolut has a bigger user base than N26. But it’s always been a bit hard to compare them, as N26 wasn’t available in the U.K. Of course, they will both say there are tens of millions of people relying on old banks — multiple challenger banks can grow at the same time if they capture market share from those aging players. Still, the battle between N26 and Revolut is on.

Powered by WPeMatico

French startup Qonto has raised a $23 million funding round for its fintech product. The company is trying to make business banking cheaper, faster and more efficient.

Existing investors Valar Ventures and Alven are once again leading the round. The European Investment Bank Group is also participating.

If you are running a small company or work as a freelancer, Qonto wants to replace your professional bank account. When you sign up, you get a French IBAN, one or multiple debit cards and the ability to send and receive money.

And then, it works pretty much like any challenger bank. You can create virtual cards, order more cards for your team, get real time notifications and freeze cards. This is a breath of fresh air compared to traditional business banks and their time-consuming processes.

You can then sync your transactions with accounting and invoicing services, and grant access to your accountant. Premium plans let you select multiple administrators and create a validation workflow to approve expensive transfers for instance.

With today’s funding round, the company plans to double the size of the team and create its own payment infrastructure. Qonto currently relies heavily on Treezor for the back end. The startup also plans to expand to Germany, Italy and Spain in 2019.

Qonto now has 90 employees and 25,000 clients. The company has managed $2 billion in total transaction volume so far. The fact that the same VC funds keep investing more money into Qonto is a great vote of confidence.

Powered by WPeMatico

Watching the current price madness is scary. Bitcoin is falling and rising in $500 increments with regularity and Ethereum and its attendant ICOs are in a seeming freefall with a few “dead cat bounces” to keep things lively. What this signals is not that crypto is dead, however. It signals that the early, elated period of trading whose milestones including the launch of Coinbase and the growth of a vibrant (if often shady) professional ecosystem is over.

Crypto still runs on hype. Gemini announcing a stablecoin, the World Economic Forum saying something hopeful, someone else saying something less hopeful – all of these things and more are helping define the current market. However, something else is happening behind the scenes that is far more important.

As I’ve written before, the socialization and general acceptance of entrepreneurs and entrepreneurial pursuits is a very recent thing. In the old days – circa 2000 – building your own business was considered somehow sordid. Chancers who gave it a go were considered get-rich-quick schemers and worth of little more than derision.

As the dot-com market exploded, however, building your own business wasn’t so wacky. But to do it required the imprimaturs and resources of major corporations – Microsoft, Sun, HP, Sybase, etc. – or a connection to academia – Google, Netscape, Yahoo, etc. You didn’t just quit school, buy a laptop, and start Snapchat.

It took a full decade of steady change to make the revolutionary thought that school wasn’t so great and that money was available for all good ideas to take hold. And take hold it did. We owe the success of TechCrunch and Disrupt to that idea and I’ve always said that TC was career pornography for the cubicle dweller, a guilty pleasure for folks who knew there was something better out there and, with the right prodding, they knew they could achieve it.

So in looking at the crypto markets currently we must look at the dot-com markets circa 1999. Massive infrastructure changes, some brought about by Y2K, had computerized nearly every industry. GenXers born in the late 70s and early 80s were in the marketplace of ideas with an understanding of the Internet the oldsters at the helm of media, research, and banking didn’t have. It was a massive wealth transfer from the middle managers who pushed paper since 1950 to the dot-com CEOs who pushed bits with native ease.

Fast forward to today and we see much of the same thing. Blockchain natives boast about having been interest in bitcoin since 2014. Oldsters at banks realize they should get in on things sooner than later and price manipulation is rampant simply because it is easy. The projects we see now are the Kozmo.com of the blockchain era, pie-in-the-sky dream projects that are sucking up millions in funding and will produce little in real terms. But for every hundred Kozmos there is one Amazon .

And that’s what you have to look for.

Will nearly every ICO launched in the last few years fail? Yes. Does it matter?

Not much.

The market is currently eating its young. Early investors made (and probably lost) millions on early ICOs but the resulting noise has created an environment where the best and brightest technical minds are faced with not only creating a technical product but also maintaining a monetary system. There is no need for a smart founder to have to worry about token price but here we are. Most technical CEOs step aside or call for outside help after their IPO, a fact that points to the complexity of managing shareholder expectations. But what happens when your shareholders are 16-year-olds with a lot of Ethereum in a Discord channel? What happens when little Malta becomes the de facto launching spot for token sales and you’re based in Nebraska? What happens when the SEC, FINRA, and Attorneys General from here to Beijing start investigating your hobby?

Basically your hobby stops becoming a hobby. Crypto and blockchain has weaponized nerds in an unprecedented way. In the past if you were a Linux developer or knew a few things about hardware you could build a business and make a little money. Now you can build an empire and make a lot of money.

Crypto is falling because the people in it for the short term are leaving. Long term players – the Amazons of the space – have yet to be identified. Ultimately we are going to face a compression in the ICO and, for a while, it’s going to be a lot harder to build an ICO. But give it a few years – once the various financial authorities get around to reading the Satoshi white paper – and you’ll see a sea change. Coverage will change. Services will change. And the way you raise money will change.

VC used to be about a team and a dream. Now it’s about a team, $1 million in monthly revenue, and a dream. The risk takers are gone. The dentists from Omaha who once visited accelerator demo days and wrote $25,000 checks for new apps are too shy to leave their offices. The flashy VCs from Sand Hill have to keep Uber and Airbnb’s plates spinning until they can cash out. VC is dead for the small entrepreneur.

Which is why the ICO is so important and this is why the ICO is such a mess right now. Because everybody sees the value but nobody – not the SEC, not the investors, not the founders – can understand how to do it right. There is no SAFE note for crypto. There are no serious accelerators. And all of the big names in crypto are either goldbugs, weirdos, or Redditors. No one has tamed the Wild West.

They will.

And when they do expect a whole new crop of Amazons, Ubers, and Oracles. Because the technology changes quickly when there’s money, talent, and a way to marry the two in which everyone wins.

Powered by WPeMatico

A stablecoin is a cryptocurrency pegged 1-to-1 with another “stable” currency. In most cases, these coins are pegged to the US dollar and, as such, allow for true transfers of actual fiat currencies between parties using the blockchain. If you’re nodding off right now thinking about this, I would posit that these moves, however minor right now, are an important step forward in cryptocurrency acceptance.

The latest stablecoin to hit the virtual streets is the Gemini Dollar. This coin comes on the heels of the much-ridiculed Tether, a stablecoin created in 2014 that has been the the brunt of much criticism including suggestions that the team has been artificially pumping the currency with wash trades.

The new currency by Winklevoss-run Gemini is pegged directly to the US dollar on the Ethereum blockchain. This means that for every Gemini Dollar there is one actual dollar in a bank account. The Gemini Trust Company holds the deposits and has been officially accepted by the New York Department of Financial Services, the regulatory body associated with banking and finance.

The GD, in other words, is the first stablecoin to gain a truly official imprimatur.

“As the financial technology marketplace continues to evolve, New York is committed to fostering innovation while ensuring responsible growth. These approvals demonstrate that companies can create change and strong standards of compliance within a strong state regulatory framework that safeguards regulated entities and protects consumers,” said Department of Financial Services Superintendent Maria T. Vullo.

From the release:

DFS issued a limited purpose trust company charter to Gemini in October 2015 to operate a virtual currency exchange through which it offers customers services for buying, selling, sending, receiving, and storing virtual currency. DFS issued a limited purpose trust company charter in May 2015 to itBit, now Paxos Trust Company, which operates the itBit exchange, to offer services for buying, selling, sending, receiving, and storing virtual currency.

The NYDFS requires that the Gemini dollars “are fully exchangeable for a U.S. dollar” and that Gemini will maintain records of their movement. The requirements also include controls including AML and OFAC controls to present money laundering or terrorist financing. An independent accountant will examine the fiat-holding bank account to ensure that all of the stable coins are accounted for. You can convert and withdraw Gemini Dollars directly onto the Ethereum blockchain.

What all this means is that there is now a stable, regulated coin that should offset some of the traditional volatility of crypto. It’s an interesting – if limited – move by a big player in the crypto space.

Powered by WPeMatico

If you want to convert Netflix gift cards into dollars on a PayPal account, you usually have to find someone willing to do the same transaction in the other direction. It can quickly go wrong if you never receive your money.

Meet AirTM, a service that makes it easier to convert any form of money into any other form of money. You can deposit money using banks, gift cards, cash through Western Union and other equivalent services, cryptocurrencies and more. You can withdraw money through any of those protocols as well. AirTM is raising a $7 million Series A with BlueYard leading the round.

While many of you probably don’t see why you’d use a service like this, AirTM’s users in Venezuela are willing to pay high fees to convert their bolívars into anything else. Multiple years of hyperinflation have turned everyone’s savings into piles of bills that are worth close to nothing.

AirTM accounts aren’t bank accounts. When you create an account, you get an e-wallet in AirUSD. You can deposit and withdraw money as well as send and receive money. Depending on your payment method, you’ll get different fees.

For instance, there’s a huge supply of money from PayPal, which means that you’ll pay quite a lot to deposit money using PayPal and convert it into AirUSD.

While AirTM sounds great for money laundering, the company is a registered money service business and follow anti-money laundering and know-your-customer requirements. The company is just getting started as it manages $9 million in monthly transaction volume with 4,000 daily active users. But it’s clear that it has the potential of creating an alternative to traditional banking in countries with volatile currencies.

Powered by WPeMatico

Backlash swelled this morning after Facebook’s aspirations in financial services were blown out of proportion by a Wall Street Journal report that neglected how the social network already works with banks. Facebook spokesperson Elisabeth Diana tells TechCrunch it’s not asking for credit card transaction data from banks and it’s not interested in building a dedicated banking feature where you could interact with your accounts. It also says its work with banks isn’t to gather data to power ad targeting, or even personalize content such as which Marketplace products you see based on what you buy elsewhere.

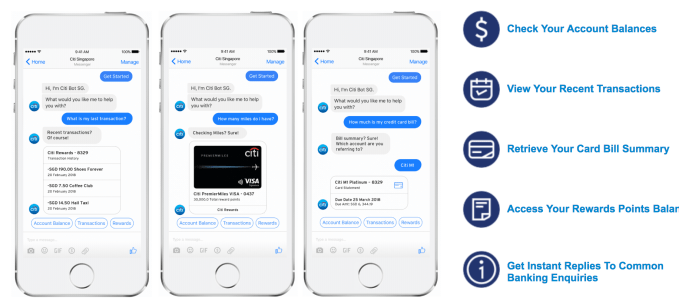

Instead, Facebook already lets Citibank customers in Singapore connect their accounts so they can ping their bank’s Messenger chatbot to check their balance, report fraud or get customer service’s help if they’re locked out of their account without having to wait on hold on the phone. That chatbot integration, which has no humans on the other end to limit privacy risks, was announced last year and launched this March. Facebook works with PayPal in more than 40 countries to let users get receipts via Messenger for their purchases.

Expansions of these partnerships to more financial services providers could boost usage of Messenger by increasing its convenience — and make it more of a centralized utility akin to China’s WeChat. But Facebook’s relationships with banks in the current form aren’t likely to produce a steep change in ad targeting power that warrants significant heightening of its earning expectations. The reality of today’s news is out of step with the 3.5 percent share price climb triggered by the WSJ’s report.

“A recent Wall Street Journal story implies incorrectly that we are actively asking financial services companies for financial transaction data – this is not true. Like many online companies with commerce businesses, we partner with banks and credit card companies to offer services like customer chat or account management. Account linking enables people to receive real-time updates in Facebook Messenger where people can keep track of their transaction data like account balances, receipts, and shipping updates,” Diana told TechCrunch. “The idea is that messaging with a bank can be better than waiting on hold over the phone – and it’s completely opt-in. We’re not using this information beyond enabling these types of experiences – not for advertising or anything else. A critical part of these partnerships is keeping people’s information safe and secure.”

Diana says banks and credit card companies have also approached it about potential partnerships, not just the other way around as the WSJ reports. She says any features that come from those talks would be opt-in, rather than happening behind users’ backs. The spokesperson stressed these integrations would only be built if they could be privacy safe. For example, signing up to use the Citibank Messenger chatbot requires two-factor authentication through your phone.

But renewed interest in Facebook’s dealings with banks comes at a time when many are pointing to its poor track record with privacy following the Cambridge Analytica scandal, where people were duped into volunteering the personal info of them and their friends. Facebook hasn’t had a big traditional data breach where data was outright stolen, as has befallen LinkedIn, eBay, Yahoo [part of TechCrunch’s parent company] and others. But users are rightfully reluctant to see Facebook ingest any more of their sensitive data for fear it could leak or be misused.

Facebook has recently cracked down on the use of data brokers that suck in public and purchased data sets for ad targeting. It no longer lets data brokers upload Managed Custom Audience lists of user contact info or power Partner Categories for targeting ads based on interests. It also more adamantly demands that advertisers have the consent of users whose email addresses or phone numbers they upload for Custom Audience targeting, though Facebook does little to verify that consent and advertisers could still buy data sets from brokers and upload them themselves

Facebook has recently cracked down on the use of data brokers that suck in public and purchased data sets for ad targeting. It no longer lets data brokers upload Managed Custom Audience lists of user contact info or power Partner Categories for targeting ads based on interests. It also more adamantly demands that advertisers have the consent of users whose email addresses or phone numbers they upload for Custom Audience targeting, though Facebook does little to verify that consent and advertisers could still buy data sets from brokers and upload them themselves

Facebook’s statement today shows more scruples than Google, which last year struck ad measurement data deals with data brokers that have access to 70 percent of credit and debit card transactions in the U.S. That led to a formal complaint to the FTC from the Electronic Privacy Information Center. [Correction: Google tells us the deals are for ad measurement data, not ad targeting as we originally published. It only learns the aggregate purchase value, not what the items were bought, and the data is encrypted.]

Cambridge Analytica has brought on an overdue era of scrutiny regarding privacy and how internet giants use our data. Practices that were overlooked, accepted as industry standard or seen as just the way business gets done are coming under fire. Internet users aren’t likely to escape ads, and some would rather have those they see be relevant thanks to deep targeting data. But the combination of our offline purchase behavior with our online identities seems to trigger uproar absent from sites using cookies to track our web browsing and buying.

Facebook’s probably better off backing away from anything that involves sensitive data like checking account balances until Cambridge Analytica blows over and it’s proven its newfound sense of responsibility translates into a safer social networking. But at least for now, it’s not slurping up our banking data wholesale.

Powered by WPeMatico

In emerging market countries where economic volatility is a way of life, there aren’t a lot of relatively safe options for members of the burgeoning middle class to park their money.

For instance, countries like Nigeria have experienced a tremendous growth in the number of citizens entering the middle class, which now accounts for about 23 percent of the population (it’s around 50 percent in the U.S.), according to a recent article citing the African Development Bank.

While Nigeria now faces some significant headwinds from a weak domestic currency (the naira), high interest rates and a manufacturing recession, there are ways that local investment can both protect the wealth that’s been created and encourage investment domestically to potentially spur development.

At least, that’s the conclusion that college friends Razaq Ahmed and Edward Popoola came to while they were thinking about opportunities for new financial services options in their home country of Nigeria.

The two men, Ahmed with a background in finance and Popoola in computer science, are launching a company called CowryWise that gives Nigerian investors a way to save their money by investing in high-yield government bonds. The rates on those products are high enough to absorb the wild swings in value of the naira and still provide a healthy return for investors, according to Ahmed.

Set to present at this year’s demo day from Y Combinator, CowryWise is one of a number of startups that Y Combinator has backed coming from the African continent, and an example of the wellspring of entrepreneurial talent that is flourishing in sub-Saharan Africa.

Using CowryWise, a customer would just have to sign up with their email address and phone number and link their bank account up to the CowryWise platform.

There are already roughly 57 million savings accounts in Nigeria and 32 million unique bank users. By investing in the bonds, these savers gain access to interest rates that range between 10 percent and 17 percent, according to Ahmed.

“The bonds… are similar to the treasuries issued by the U.S. government, which is A-rated,” says Ahmed. Even if there were foreign currency risk from investing in the naira, the inflation rate is currently around 11 percent, according to Ahmed. Given that most of the bonds are yielding interest rates on the higher end, it’s just a better deal for consumers, he said.

“There’s more value in keeping the money in government treasury bills” than in the bank, says Ahmed.

For Ahmed and Popoola, the decision to launch CowryWise was a way to bring investment opportunities to a retail investor that hadn’t been able to access the best that the financial system in Nigeria had to offer.

To target these retail investors meant leveraging technology to scale quickly and cheaply across the country. The two men started developing their service in January and tested it in February and March with friends and family.

CowryWise isn’t without competitors. Another Nigerian company, Piggybank, recently raised $1.1 million for its own automated savings solution. Like CowryWise, Piggybank also taps into government bonds to offer better rates to its investors.

That company already has 53,000 registered users — who have saved in excess of $5 million since 2016, according to a release.

There are subtle differences between the two. Piggybank touts its ability to save through bonds, but it is primarily working with banks to get Nigerians saving money. CowryWise is using Meristem Financial (Ahmed’s old employer) as the asset manager for its investments into the bond market.

Another difference is the time customers’ funds are locked up. Piggybank has a three-month savings period required before investors can withdraw funds, while CowryWise will let its customers withdraw cash immediately, according to this teardown of the two services.

Ultimately, there’s a large enough market for multiple players, and a need for better financial services, according to Ahmed.

“We kept having interest from retail investors on why they want to do micro-savings and micro-investment, but they didn’t have the required capital,” Ahmed says. “That was the major reason for staring the company. Why not democratize the assets? And make them available in investments and savings in this traditional instrument?”

Powered by WPeMatico

The working class of the United States doesn’t get many breaks these days. It’s not just a function of low pay and long hours, but also the incredible uncertainty of income and expenses that makes surviving week-to-week so challenging. One in five Americans have a negative net wealth, even in an economy where the unemployment rate is the lowest in almost two decades. Banks, meanwhile, are actively dissuading the working class from banking with them, creating a permanent class of unbanked and underbanked citizens.

For Jon Schlossberg, CEO and co-founder of Even.com, improving the plight of ordinary Americans and their finances is a deeply personal and professional mission. And now that mission has a huge new bucket of capital behind it, with Keith Rabois of Khosla Ventures leading a $40 million Series B round into the Oakland-based startup. Rabois is a return investor, having previously backed the company in its late 2014 seed round. With this latest round of capital, Even.com has now raised $50.5 million.

When Even.com first launched its eponymous app, the goal was to offer income smoothing for workers, helping them avoid usurious payday loans to make ends meet. Since that first launch several years ago, Schlossberg and his team learned that the only way to improve the finances for the working class is to help them budget better — ending the need for loans in the first place. “To do anything with your life, unless you are just born to the right family, you need to spend your money wisely, but we never teach you how to do that,” Schlossberg explained to me.

Last year, Even.com announced that it had stopped evening through its Pay Protection product. Instead, Schlossberg said that Even.com has evolved and wanted to “build a new kind of financial institution with products that fit your life.” It still has a feature it brands as Instapay, which allows users to request their earned pay in advance of their payday.

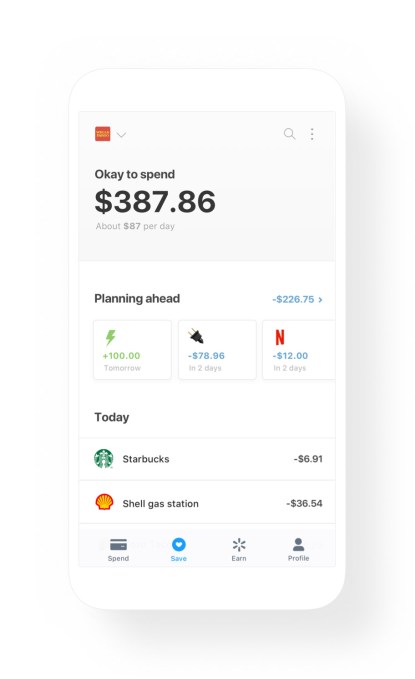

But Even.com is increasingly focused on improving the quality of its intelligent budgeting feature. Using artificial intelligence models honed over the past few years, the company now gives users of its Even app an “Okay to spend” figure that helps them think through their cash flow. By giving a predictive figure rather than a checking account balance, Even can help its users avoid sudden surprise expenses that can trigger the kind of financial death spiral that has become a familiar story in America. The company will also soon launch an automatic savings feature similar to Digit or Acorns that helps people build up regular savings.

Even’s Okay to spend feature gives insight into future cash flows before it is too late

While the company offers an increasingly comprehensive suite of financial tools, it has decided to avoid charging users specific use fees, opting instead for a subscription model. Schlossberg explained that “We are a mission-oriented company, but talk is cheap and where the rubber hits the road, it’s how you make money.” Even is free for users participating through partner employers, or $2.99 a month for individuals without a sponsor.

The company’s highest expense feature is Instapay due to underwriting, and so the company makes higher profits when fewer of its customers need access to payday credit. In other words, the better that its users budget, the fewer loans it will underwrite, and the more money the company makes. We are “directly incentivized to help people with their financial health,” Schlossberg noted.

Even has proven attractive to corporate customers, including Walmart, which partnered with the startup last December to offer its service to all 1.4 million employees at the retailer. Since the launch of that partnership, more than 200,000 Walmart employees regularly use the app, according to Even, and the typical active user checks their Okay to spend balance four times a week. A majority of active users have also taken out an Instapay through Even.

More interestingly, salaried employees at Walmart used the app slightly more than hourly workers, proving that just having a guaranteed income isn’t necessarily a panacea to financial trouble for many American households.

Even.com’s Series B round is all about expansion and growth for the company. Even intends to open an East Coast office this year, and intends to expand its product further into the Fortune 500 with partnerships similar to its Walmart deal. The company currently has 37 employees. In addition to Khosla, the startup raised funding from Valar Ventures, Allen & Company, Harrison Metal, SV Angel, Silicon Valley Bank and others.

Powered by WPeMatico

Fintech startup N26 is updating its N26 Metal product and launching it tomorrow. You might remember that the company first announced its premium card at TechCrunch Disrupt Berlin in December 2017. Shortly after the conference, the card was available in early access for existing N26 Black customers.

But the company had to go back to the drawing board and update the card design. N26 Metal customers had some complaints about the design of the card in particular.

While the original metal card was primarily made of a sheet of tungsten, the metallic part was still surrounded by plastic. Customers complained about scratches and the overall feel of the card.

It didn’t really feel like a metal card. It was more or less a heavy plastic card with a metal core. You could easily get scratches and the MasterCard logo was just a sticker.

@N26 such a shame my Metal card has a big scratch… it doesn’t even look like a scratch but something deeper under the plastic 🙁 pic.twitter.com/7qFTNEkqlH

— W Bonnaud-Dowell (@bonnaud_dowell) March 5, 2018

Even more surprising, some customers had some issues going through airport security because tungsten was an uncommon material.

Travelled 2 times since I have the @n26 metal card and get an extra security check each time because of this.

— Alex. Delivet (@alexd) May 14, 2018

At an event in Berlin, the company announced a revised version of N26 Metal. The front of the card is going to be made out of actual metal. The MasterCard logo will be engraved. And the name of the customer is moving to the back of the card.

You can join the waiting list now and customers will start getting the new metal card tomorrow. Everybody will be able to sign up next Tuesday.

But N26 Metal isn’t just a fancy card. For around €15 per month, you get all the advantages of N26 Black as well as partner offerings.

These offerings include the basic $45 per month WeWork subscription so that you can access a WeWork office for free for one day per month and pay for extra days. You also get 10 percent off hotel bookings on Hotels.com, promo codes for Drivy, Babbel and other services. The company says that there will be new offerings in the coming months.

Powered by WPeMatico