sequoia capital

Auto Added by WPeMatico

Auto Added by WPeMatico

In the days leading up to TechCrunch Disrupt SF 2018, The Economist published the cover story, ‘Why Startups Are Leaving Silicon Valley.’

The author outlined reasons why the Valley has “peaked.” Venture capital investors are deploying capital outside the Bay Area more than ever before. High-profile entrepreneurs and investors, Peter Thiel, for example, have left. Rising rents are making it impossible for new blood to make a living, let alone build businesses. And according to a recent survey, 46 percent of Bay Area residents want to get the hell out, an increase from 34 percent two years ago.

Needless to say, the future of Silicon Valley was top of mind on stage at Disrupt.

“It’s hard to make a difference in San Francisco as a single entrepreneur,” said J.D. Vance, the author of ‘Hillbilly Elegy’ and a managing partner at Revolution’s Rise of the Rest Fund, which backs seed-stage companies based outside Silicon Valley. “It’s not as a hard to make a difference as a successful entrepreneur in Columbus, Ohio.”

In conversation with Vance, Revolution CEO Steve Case said he’s noticed a “mega-trend” emerging. Founders from cities like Pittsburgh, Detroit or Portland are opting to stay in their hometowns instead of moving to U.S. innovation hubs like San Francisco.

“The sense that you have to be here or you can’t play is going to start diminishing.”

“We are seeing the beginnings of a slowing of what has been a brain drain the last 20 years,” Case said. “It’s not just watching where the capital flows, it’s watching where the talent flows. And the sense that you have to be here or you can’t play is going to start diminishing.”

J.D. Vance says that most entrepreneurs don’t need to move to Silicon Valley.

Here’s why. #TCDisrupt pic.twitter.com/0mFPeTuHLe

— TechCrunch (@TechCrunch) September 6, 2018

Farewell, San Francisco

“It’s too expensive to live here,” said Aileen Lee, the founder of seed-stage VC firm Cowboy Ventures, amid a conversation with leading venture capitalists Spark Capital general partner Megan Quinn and Benchmark general partner Sarah Tavel .

“I know that there are a lot of people in the Bay Area that are trying to work on that problem and I hope that they are successful,” Lee added. “It’s an amazing place to live and we’ve made it really challenging for people to live here and not worry about making ends meet.”

One of Cowboy’s portfolio companies opted to relocate from Silicon Valley to Colorado when it came time to scale their business. That kind of move would’ve historically been seen as a failure. Today, it may be a sign of strong business acumen.

Quinn said that of all 28 of Spark’s growth-stage portfolio companies, Raleigh, North Carolina-based Pendo has the easiest time recruiting folks locally and from the Bay Area.

She advises her Bay Area-based late-stage companies to open a second office outside of the Valley where lower-cost talent is available.

“We often say go to [flySFO.com], draw a three-hour circle around San Francisco where they have direct flights, find a city that has a university and open up a second office as quickly as possible,” Quinn said.

Still, all three firms invest in a lot of companies based in San Francisco. Of Benchmark’s 10 most recent investments, for example, eight were based in SF, according to Crunchbase.

“I used to believe really strongly if you wanted to build a multi-billion dollar company you had to be based here,” Tavel said. “I’ve stopped giving that soap speech.”

Aileen Lee (Cowboy Ventures), Megan Quinn (Spark Capital), and Sarah Tavel (Benchmark Capital) on whether or not Silicon Valley is on the wane for investors #TCDisrupt pic.twitter.com/SOpn7p0eNQ

— TechCrunch (@TechCrunch) September 5, 2018

Underestimated talent

A lot of Bay Area VCs have been blind to the droves of tech talent located outside the region. Believe it or not, there are great engineers in America’s small- and medium-sized markets too.

At Disrupt, Backstage Capital founder Arlan Hamilton announced the firm would launch an accelerator to further amplify companies led by underestimated founders. The program will have cohorts based in four cities; San Francisco was noticeably absent from that list.

Instead, the firm, which invests in underrepresented founders and recently raised a $36 million fund, will work with companies in Philadelphia, Los Angeles, London and one more city, which will be determined by a public vote. Aniyia Williams, the founder of Tinsel and Black & Brown Founders, will spearhead the Philadelphia effort.

“For us, it’s about closing that wealth gap to address inequity in tech,” Williams said. “There needs to be more active participation from everyone.”

Hamilton added that for her, the tech talent in LA and London is undeniable.

“There is a lot of money and a lot of investors … it reminds me of three years ago in Silicon Valley,” Hamilton said.

Silicon Valley vs. China

Silicon Valley’s demise may not be just as a result of increased costs of living or investors overlooking talent in other geographies. It may be because of heightened competition abroad.

Doug Leone, an early- and growth-stage investor at Sequoia Capital, said at Disrupt that he’s noticed a very different work ethic in China.

Chinese entrepreneurs, he explained, are more ruthless than their American counterparts and they’re putting in a whole lot more hours.

Doug Leone of Sequoia Capital says founders in the US and China both want to change the world, but Chinese founders are a little more desperate (and you see it in the crazy work ethic they have).#TCDisrupt pic.twitter.com/dPxsRTbJoq

— TechCrunch (@TechCrunch) September 6, 2018

“I’ve had dinner in China until after 10 p.m. and people go to work after 10 p.m.,” Leone recalled.

“We don’t see that in the U.S. I’m not saying the U.S. founders oughta do that but those are the differences. They are similar in character. They are similar in dreams. They are similar in how they want to change the world. They are ultra-driven … The Chinese founders have a half other gear because I think they are a little more desperate.”

Much of this, however, has been said before and still, somehow, Silicon Valley remained the place to be for investors and startup entrepreneurs.

The reality is, those engaged in tech culture are always anxiously awaiting for the bubble to pop, the market to crash and for “peak Valley” to finally arrive.

Maybe, just maybe, Silicon Valley is forever.

Here’s more of our coverage of Disrupt 2018.

Powered by WPeMatico

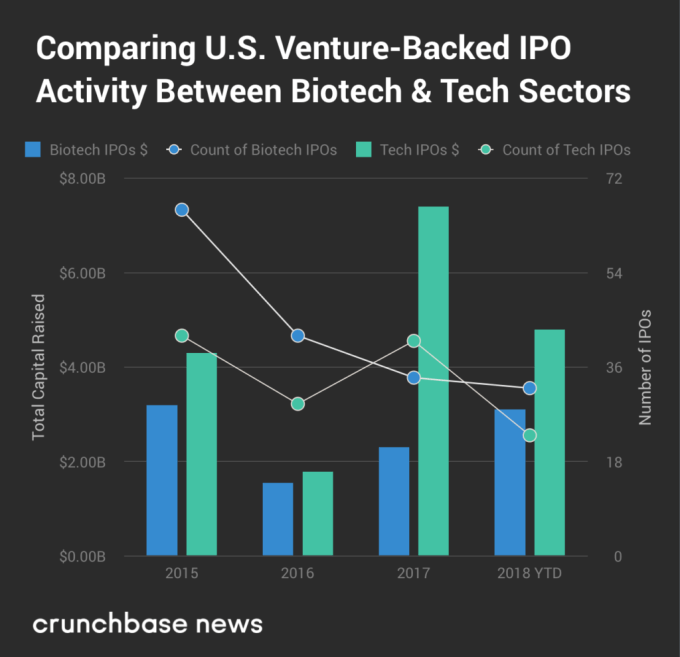

For people who make investment decisions based on revenues and projected earnings, biotech IPOs are kind of a non-starter. Not only are new market entrants universally unprofitable, most have zero revenue. Going public is mostly a means to raise money for clinical trials, with red ink expected for years to come.

That pattern may be one reason the venture capital press, Crunchbase News included, tends to devote a disproportionately small portion of coverage to biotech IPOs. It’s more exciting to watch a big-name internet company pop in first-day trading or poke fun at an underperforming dud.

But with our fixation on all things tech, we’re missing out on the big picture. There are actually a lot more biotech and healthcare startup IPOs than tech offerings. In the second quarter of this year, for instance, at least 16 U.S. venture-backed biotech and healthcare companies went public, compared to just 11 tech startups. In three of the past four years, bio offerings outnumbered tech IPOs, according to Crunchbase data.

In the following analysis, we attempt to get up to speed on the pace of biotech offerings, assess where we are in the cycle and spotlight some of the rising stars.

As mentioned above, U.S. bio IPOs outnumber tech offerings in most years. However, the bio cohort raises less total capital, partly because the largest technology IPOs tend to be much bigger than the largest bio IPOs. In the chart below, we compare the two sectors over the past four years.

Globally, the numbers are much higher. Using Crunchbase data, we’ve put together a chart looking at global VC-backed biotech and healthcare IPOs over the past four years. While we’re just over halfway through 2018, biotech and health IPOs have already raised more money than in any of the prior three full calendar years.

It’s pretty clear we’re in an upcycle for all things startup-related. VCs are flush with cash, late-stage rounds are ballooning in size and IPO and M&A action is picking up, too.

So what does that mean for bio IPOs? Is the uptick in the pace and size of offerings mostly a result of bullish market conditions? Or is the current slate of pre-IPO candidates more compelling than in the past?

We turned to Bob Nelsen, co-founder of ARCH Venture Partners, one of the top-performing biotech investors, for his take, which is that it’s a “fundamentals driven, cycle amplified” IPO boomlet.

More companies are launching well-received IPOs because the pace of startup innovation is faster than in the past. Nelson calls it “the result of the previous 30 years of investment and innovation in biotech that has finally led to essentially data-driven innovation.” That’s leading to more curative treatments, disease-modifying therapies and preventative technologies.

Yet we’re also in a bullish segment of the market cycle for biotech. That’s prompting companies that might have stayed private under other conditions to give going public a shot. It’s also providing bigger outcomes for emerging companies that were already on the IPO track.

The latest example of a big outcome IPO is Rubius Therapeutics, which develops drugs based on genetically engineered red blood cells. This week, the five-year-old company raised $241 million at an initial valuation of over $2 billion, making it the largest bio offering of 2018. The Cambridge, Mass. company, which previously raised nearly a quarter-billion-dollars in venture funding, is still in the pre-clinical trial phase.

This year has delivered several other good-sized offerings as well, including drug developers Eidos Therapeutics and Homology Medicines, recently valued around $800 million each, along with Tricida, valued around $1.2 billion. (See the full list of 2018 global bio and health offerings here.)

As for aftermarket performance, that’s been up and down, but includes some big ups. Last year, biotech led the pack for best-performing IPOs on U.S. exchanges. The sector accounted for four of the six top spots, according to Renaissance Capital, led by drug developers AnaptysBio, Argenx and UroGen, along with Calyxt, an agbio startup.

While things are already up, bio VCs, generally an optimistic bunch, see several reasons why bio IPOs could go higher.

Nelson points to what he sees as the lagging pace of in-house innovation at big pharma and biotech players. Increasingly, they need to acquire startups and recently public companies to stay competitive and build out new product pipelines.

There is also tons of fresh capital earmarked for healthcare startups. In the U.S. in 2017, healthcare-focused venture capitalists raised $9.1 billion. That figure was up 26 percent from 2016, per Silicon Valley Bank.

More dollars also are flowing from venture firms that invest in a mix of tech and life sciences through a single fund. That list includes well-established VCs with dry powder to invest, including Polaris Partners, Founders Fund, Kleiner Perkins and Sequoia Capital.

Still, Nelson observes, deep into an IPO bull market, the average quality of offerings does tend to decline. That said, he’s been through similar inflection points in previous cycles and “for the same point in the cycle, the quality is markedly higher.”

Powered by WPeMatico

Yesterday, we learned that 18-month-old, Bay Area-based electric scooter rental company Lime is joining forces with the ride-hailing giant Uber, which is both investing in the company as part of a $335 million round and planning to promote Lime in its mobile app. According to Bloomberg, Uber also plans to plaster its logo on Lime’s scooters.

Lime isn’t being acquired outright, in short, but it looks like it will be. At least, Uber struck a similar arrangement with the electric bike company JUMP bikes before spending $200 million to acquire the company in spring.

There are as many questions raised by this kind of tie-up as answered, but the biggest may be what the impact means for Lime’s fiercest rival in the e-scooter wars, 15-month-old L.A.-based Bird, which several sources tell us also discussed a potential partnership with Uber.

Despite recently raising $300 million in fresh capital at a somewhat stunning $2 billion valuation, could its goose be, ahem, cooked?

At first glance, it would appear so. Uber’s travel app is the most downloaded in the U.S. by a wide margin, despite gains made last year by its closest U.S. competitor, Lyft, as Uber battled one scandal after another. It’s easy to imagine that Lime’s integration with Uber will give it the kind of immediate brand reach that most founders can only dream about.

A related issue for Bird is its relationship with Lyft, which . . . isn’t great. Bird’s founder and CEO, Travis VanderZanden, burned that bridge when, not so long after Lyft acqui-hired VanderZanden from a small startup he’d launched and made him its COO, he left to join rival Uber.

Lyft, which sued VanderZanden for allegedly breaking a confidentiality agreement when he joined Uber, later settled with him for undisclosed terms. But given their history, it’s hard to imagine Lyft — which also has a much smaller checkbook than Uber — paying top dollar to acquire his company.

Where that leaves Bird is an open question, but people familiar with both Bird and Lime suggest the e-scooter war is far from over.

For example, though Uber sees its partnership with Lime as “another step towards our vision of becoming a one-stop shop for all your transportation needs,” two sources familiar with Bird’s thinking are quick to underscore its plans to expand internationally quickly and not merely fight a turf war in the U.S. (It already has one office in China.)

That Sequoia Capital led Bird’s most recent round of funding helps on this front, given Sequoia Capital China’s growing dominancein the country and the relationships that go with it. Then again, Sequoia is also an investor in Uber, having acquired a stake in the company earlier this year. And alliances are generally temperamental in this brave new world of transportation. In just the latest unexpected twist, Lime’s newest round included not only Uber but also GV, the venture arm of Alphabet, which only recently resolved a lawsuit with Uber.

Another wrinkle to consider is the exposure that Lime receives from Uber, which could prove double-edged, given the company’s ups and downs. Uber’s new CEO, Dara Khosrowshahi, appears determined to steer the company to a smooth and decidedly undramatic public offering in another year or so. But for a company of Uber’s scale and scope, that’s a challenge, to say the least. (Its newest hire, Scott Schools — a former top attorney at the U.S. Justice Department and now Uber’s chief compliance officer — will undoubtedly be tasked with minimizing the odds of things going astray.)

Lime’s arrangement with Uber could potentially create other opportunities for Bird. First, by agreeing to allow Uber to apply its branding to its scooters, Lime will be diluting its own brand. Even if Uber never acquires the company, riders may well associate Lime with Uber and think, for better or worse, that it’s a subsidiary.

Further, Uber does not appear to have made any promises to Lime in terms of how prominently its app is featured within its own mobile app, which already crams in quite a lot, from offering free ride coupons to featuring local offers to promoting its Uber Eats business.

Consider that in January 2017, Google added to both the Android and iOS versions of its Google Maps service the ability to book an Uber ride. Uber might have thought that a coup, too, at the time. But last summer, Google quietly removed the feature from its iOS app, and it removed the service from Android just last month. If there wasn’t much outrage over the decision, likely it’s because so few users of Google Maps noticed the feature in the first place.

Lime’s arrangement could prove more advantageous than that. Only time will tell. But everything considered, whether or not Bird flies away with this competition will likely owe less to Lime’s new arrangement with Uber than with its own ability to execute. That includes making its own mobile app the kind of go-to destination that Uber’s has become.

Certainly, that’s what Bird’s flock would argue will happen. Yesterday afternoon, Roelof Botha, a partner at Sequoia and a Bird board member, declined to discuss the Lime deal, instead emailing one short observation seemingly designed to say it all: “Travis [VanderZanden] is far more customer obsessed than competitor obsessed. That is a quality we look for in great founders.”

A Bird spokesperson offered an equally sanguine quote, saying that Bird is “happy to see our friends in the ride-sharing industry coalesce on the pressing need to offer a sustainable and affordable alternative to car trips.”

Powered by WPeMatico

And there we have it: Bird, one of the emerging massively hyped Scooter startups, has roped in its next pile of funding by picking up another $300 million in a round led by Sequoia Capital.

The company announced the long-anticipated round this morning, with Sequoia’s Roelof Botha joining the company’s board of directors. This is the second round of funding that Bird has raised over the span of a few months, sending it from a reported $1 billion valuation in May to a $2 billion valuation by the end of June. In March, the company had a $300 million valuation, but the Scooter hype train has officially hit a pretty impressive inflection point as investors pile on to get money into what many consider to be the next iteration of resolving transportation at an even more granular level than cars or bikes. New investors in the round include Accel, B Capital, CRV, Sound Ventures, Greycroft and e.ventures; previous investors Craft Ventures, Index Ventures, Valor, Goldcrest, Tusk Ventures and Upfront Ventures are also in the round. (So, basically everyone else who isn’t in competitor Lime.)

Scooter mania has captured the hearts of Silicon Valley and investors in general — including Paige Craig, who actually jumped from VC to join Bird as its VP of business — with a large amount of capital flowing into the area about as quickly as it possibly can. These sort of revolving-door fundraising processes are not entirely uncommon, especially for very hot areas of investment, though the scooter scene has exploded considerably faster than most. Bird’s round comes amid reports of a mega-round for Lime, one of its competitors, with the company reportedly raising another $250 million led by GV, and Skip also raising $25 million.

“We have met with over 20 companies focused on the last-mile problem over the years and feel this is a multi-billion dollar opportunity that can have a big impact in the world,” CRV’s Saar Gur, who did the deal for the firm, said. “We have a ton of conviction that this team has original product thought (they created the space) and the execution chops to build something extremely valuable here. And we have been long-term focused, not short-term focused, in making the investment. The ‘hype’ in our decision (the non-zero answer) is that Bird has built the best product in the market and while we kept meeting with more startups wanting to invest in the space — we kept coming back to Bird as the best company. So in that sense, the hype from consumers is real and was a part of the decision. On unit economics: We view the first product as an MVP (as the company is less than a year old) — and while the unit economics are encouraging, they played a part of the investment decision but we know it is not even the first inning in this market.”

There’s certainly an argument to be made for Bird, whose scooters you’ll see pretty much all over the place in cities like Los Angeles. For trips that are just a few miles down wide roads or sidewalks, where you aren’t likely to run into anyone, a quick scan of a code and a hop on a Bird may be worth the few bucks in order to save a few minutes crossing those considerably long blocks. Users can grab a bird that they see and start going right away if they are running late, and it does potentially alleviate the pressure of calling a car for short distances in traffic, where a scooter may actually make more sense physically to get from point A to point B than a car.

There are some considerable hurdles going forward, both theoretical and in effect. In San Francisco, though just a small slice of the United States metropolitan area population, the company is facing significant pushback from the local government, and scooters for the time being have been kicked off the sidewalks. There’s also the looming shadow of what may happen regarding changes in tariffs, though Gur said that it likely wouldn’t be an issue and “the unit economics appear to be viable even if tariffs were to be added to the cost of the scooters.” (Xiaomi is one of the suppliers for Bird, for example.)

Powered by WPeMatico

Ethos, the company that bills itself as making life insurance accessible, affordable and simple, has officially come out of stealth with an $11.5 million investment led by one of the world’s top venture firms, Sequoia Capital, and additional participation from the family offices of Hollywood’s biggest stars and an NBA all-star.

Jay Z’s Roc Nation, and the family funds of Kevin Durant, Robert Downey Jr. and Will Smith, all participated in the new round for Ethos, and Sequoia Partner Roelof Botha is taking a seat on the company’s board. Because nothing says star power like a life insurance startup.

The life insurance market is one that’s been attracting interest from venture investors for a little over a year now. Companies like England’s Anorak, HealthIQ, Ladder, Mira Financial, and France’s Alan, which is backed by Partech Investments (among others), Fabric and Quilt, are all pitching life insurance products as well.

Ethos is licensed in 49 states, which is pretty comparable to the offering from providers like Haven Life, the Mass Mutual-backed life insurance product.

What has made the life insurance market interesting for investors is the fact that consumers’ interest in it continues to decline. Whether it’s because no one trusts insurers to actually pay out, or because Americans are putting their faith in the anti-aging technologies from funds like the Longevity Fund, folks just aren’t buying insurance products the way they used to.

So when investors see the numbers of users of a formerly ubiquitous product decline from 77 percent in 1989 to below 60 percent in 2018, the assumption is that there’s room for new companies to come in and provide better service.

Scads of investors have taken the same bet, which makes Ethos a marketing play as much as anything else. In the company’s press release it touts the fast, easy and inexpensive process for getting a quote.

The initial process requires only four questions to get a quote and a 10 minute survey to get a policy (in most cases). The company says 99 percent of its applicants don’t need a medical exam or blood test to get a policy.

What may have been most interesting to investors is the pedigree of the company’s co-founders. Peter Colis and Lingke Wang have both worked in the insurance industry before. They previously co-founded a life insurance marketplace called, Ovid Life.

“Life insurance is critical for families, but the process is broken for those who want and need it,” said Peter Colis. “We are consumer advocates, intensely focused on expanding life insurance accessibility to the millions of U.S. families who have college debt, mortgages, spouses and children to care for, and who want to be financially empowered to live their lives without worry.”

Ethos founders Lingke Wang and Peter Colis

Powered by WPeMatico

San Jose-based Cohesity has closed an oversubscribed $250M Series D funding round led by SoftBank’s Vision Fund, bringing its total raised to date to $410M. The enterprise software company offers a hyperconverged data platform for storing and managing all the secondary data created outside of production apps.

In a press release today it notes this is only the second time SoftBank’s gigantic Vision Fund has invested in an enterprise software company. The fund, which is almost $100BN in size — without factoring in all the planned sequels, also led an investment in enterprise messaging company Slack back in September 2017 (also a $250M round).

“Cohesity pioneered hyperconverged secondary storage as a first stepping stone on the path to a much larger transformation of enterprise infrastructure spanning public and private clouds. We believe that Cohesity’s web-scale Google-like approach, cloud-native architecture, and incredible simplicity is changing the business of IT in a fundamental way,” said Deep Nishar, senior managing partner at SoftBank Investment Advisers, in a supporting statement.

Also participating in the financing are Cohesity’s existing strategic investors Cisco Investments, Hewlett Packard Enterprise (HPE), and Morgan Stanley Expansion Capital, along with early investor Sequoia Capital and others.

The company says the investment will be put towards “large-scale global expansion” by selling more enterprises on the claimed cost and operational savings from consolidating multiple separate point solutions onto its hyperconverged platform. On the customer acquisition front it flags up support from its strategic investors, Cisco and HPE, to help it reach more enterprises.

Cohesity says it’s onboarded more than 200 new enterprise customers in the last two quarters — including Air Bud Entertainment, AutoNation, BC Oil and Gas Commission, Bungie, Harris Teeter, Hyatt, Kelly Services, LendingClub, Piedmont Healthcare, Schneider Electric, the San Francisco Giants, TCF Bank, the U.S. Department of Energy, the U.S. Air Force, and WestLotto — and says annual revenues grew 600% between 2016 and 2017.

In another supporting statement, CEO and founder Mohit Aron, added: “My vision has always been to provide enterprises with cloud-like simplicity for their many fragmented applications and data — backup, test and development, analytics, and more.

“Cohesity has built significant momentum and market share during the last 12 months and we are just getting started.”

Powered by WPeMatico

Robinhood started off as a dead-simple stock trading application that had no transaction fees — but since it’s continued to grow, and especially as it starts to dive into cryptocurrency, investors are getting pretty excited about its prospects and are pouring a ton of new funding into it.

And it’s that tantalizing prospect of creating a next generation way of trading assets and cryptocurrency that is now sending Robinhood to a $5.6 billion valuation in a new financing round that the company is announcing today. Robinhood says it’s closed a $363 million Series D financing round; DST Global led this new round and Iconiq, Kleiner Perkins, Sequoia and Capital G participated. Robinhood had a $1.3 billion valuation last year when it had around 2 million users, and the company says it now has 4 million users and has passed $150 billion in transaction volume.

“It’s the only place right now where you can trade crypto, stocks, and options all in one place,” CEO Vlad Tenev said. “For us to construct an experience that feels seamless and natural for customers, that for example want to sell an equity and use the proceeds to buy crypto, seamlessly, that’s been challenging not just from a product and design standpoint, but also infrastructure standpoint. There’s complexity under the hood, and our goal is to make it as seamless as possible in the process and make that complexity go away.”

Those 4 million users — and that valuation — indicates that Robinhood has clearly exposed a lot of demand for an easier way for users to dip their toes into financial services without having to work with firms that have trading fees like Scottrade or E*Trade. And while there are a lot of services that offer robo-advisory services like Betterment and Wealthront, which make it easier to start investing small amounts of money, Robinhood offers users the opportunity to do these things at a more granular level.

And, of course, there’s the cryptocurrency aspect that is clearly spurring a lot of interest in the company. At the time, 1 million users waitlisted for access in just the five days after Robinhood Crypto was announced. Robinhood has premium services like Robinhood Gold, where the company can find additional ways to generate revenue that offset the requirements of running a system that allows users to trade stocks for free. Robinhood has raised $539 million to date, as diving into financial services can be an expensive prospect, as well as getting enough users on board to the point that it can scale to a level that the business starts to increasingly make sense.

Robinhood’s crypto trading service came out in February and by today, the company says it’s available in 10 states. The company also rolled out a web version and stock option trading, trying to become a more robust financial services company that’s still tuned to a younger generation that wants an easier way to get into investing without needing a big balance to invest. Most of Robinhood’s users, too, aren’t so-called “day traders” and are instead holding stocks for a while after they buy them.

“If you look at the data and the statistics, people that are active day traders are actually a very small percentage of our space,” Tenev said. “People that are actually transacting on that cadence are the minority of our customers. Most of our customers engage in more of these buy and hold accumulation strategies. We really see a lot of unique things because we don’t charge trading commissions. There are customers that deposit money regularly twice or once a month and then buy stocks as soon as those deposits come in. We don’t see a lot of customers that are doing rapid buying and selling.”

Still, as it tries to further expand — especially into products like crypto and new regions — it’s going to increasingly find itself trying to jump hurdles that financial services companies find when going abroad. And there’s always a chance that the trading platforms will try to become a little more competitive (and companies like Square are even getting into Bitcoin trading). That’s going to require a robust amount of funding to try to outmaneuver well-capitalized companies that might already have those relationships in place to more easily expand.

“The political climate is uncertain, it sort of affects everyone, it doesn’t affect us uniquely,” Tenev said. “We’re a crypto business now. Not a lot of people have a ton of clarity on what that’s gonna look like in the future, it’s a new space that’s evolving really rapidly. I think that we’re confident we can adapt and evolve, and we’re operating the business in a responsible way. There’s only so much you can do, but I feel like we’ve done a lot to address any concerns.”

Powered by WPeMatico

Why has San Francisco’s startup scene generated so many hugely valuable companies over the past decade?

That’s the question we asked over the past few weeks while analyzing San Francisco startup funding, exit, and unicorn creation data. After all, it’s not as if founders of Uber, Airbnb, Lyft, Dropbox and Twitter had to get office space within a couple of miles of each other.

We hadn’t thought our data-centric approach would yield a clear recipe for success. San Francisco private and newly public unicorns are a diverse bunch, numbering more than 30, in areas ranging from ridesharing to online lending. Surely the path to billion-plus valuations would be equally varied.

But surprisingly, many of their secrets to success seem formulaic. The most valuable San Francisco companies to arise in the era of the smartphone have a number of shared traits, including a willingness and ability to post massive, sustained losses; high-powered investors; and a preponderance of easy-to-explain business models.

No, it’s not a recipe that’s likely replicable without talent, drive, connections and timing. But if you’ve got those ingredients, following the principles below might provide a good shot at unicorn status.

First, lose money until you’ve left your rivals in the dust. This is the most important rule. It is the collective glue that holds the narratives of San Francisco startup success stories together. And while companies in other places have thrived with the same practice, arguably San Franciscans do it best.

It’s no secret that a majority of the most valuable internet and technology companies citywide lose gobs of money or post tiny profits relative to valuations. Uber, called the world’s most valuable startup, reportedly lost $4.5 billion last year. Dropbox lost more than $100 million after losing more than $200 million the year before and more than $300 million the year before that. Even Airbnb, whose model of taking a share of homestay revenues sounds like an easy recipe for returns, took nine years to post its first annual profit.

Not making money can be the ultimate competitive advantage, if you can afford it.

Industry stalwarts lose money, too. Salesforce, with a market cap of $88 billion, has posted losses for the vast majority of its operating history. Square, valued at nearly $20 billion, has never been profitable on a GAAP basis. DocuSign, the 15-year-old newly public company that dominates the e-signature space, lost more than $50 million in its last fiscal year (and more than $100 million in each of the two preceding years). Of course, these companies, like their unicorn brethren, invest heavily in growing revenues, attracting investors who value this approach.

We could go on. But the basic takeaway is this: Losing money is not a bug. It’s a feature. One might even argue that entrepreneurs in metro areas with a more fiscally restrained investment culture are missing out.

What’s also noteworthy is the propensity of so many city startups to wreak havoc on existing, profitable industries without generating big profits themselves. Craigslist, a San Francisco nonprofit, may have started the trend in the 1990s by blowing up the newspaper classified business. Today, Uber and Lyft have decimated the value of taxi medallions.

Not making money can be the ultimate competitive advantage, if you can afford it, as it prevents others from entering the space or catching up as your startup gobbles up greater and greater market share. Then, when rivals are out of the picture, it’s possible to raise prices and start focusing on operating in the black.

You can’t lose money on your own. And you can’t lose any old money, either. To succeed as a San Francisco unicorn, it helps to lose money provided by one of a short list of prestigious investors who have previously backed valuable, unprofitable Northern California startups.

It’s not a mysterious list. Most of the names are well-known venture and seed investors who’ve been actively investing in local startups for many years and commonly feature on rankings like the Midas List. We’ve put together a few names here.

You might wonder why it’s so much better to lose money provided by Sequoia Capital than, say, a lower-profile but still wealthy investor. We could speculate that the following factors are at play: a firm’s reputation for selecting winning startups, a willingness of later investors to follow these VCs at higher valuations and these firms’ skill in shepherding portfolio companies through rapid growth cycles to an eventual exit.

Whatever the exact connection, the data speaks for itself. The vast majority of San Francisco’s most valuable private and recently public internet and technology companies have backing from investors on the short list, commonly beginning with early-stage rounds.

Generally speaking, you don’t need to know a lot about semiconductor technology or networking infrastructure to explain what a high-valuation San Francisco company does. Instead, it’s more along the lines of: “They have an app for getting rides from strangers,” or “They have an app for renting rooms in your house to strangers.” It may sound strange at first, but pretty soon it’s something everyone seems to be doing.

It’s not a recipe that’s likely replicable without talent, drive, connections and timing.

A list of 32 San Francisco-based unicorns and near-unicorns is populated mostly with companies that have widely understood brands, including Pinterest, Instacart and Slack, along with Uber, Lyft and Airbnb. While there are some lesser-known enterprise software names, they’re not among the largest investment recipients.

Part of the consumer-facing, high brand recognition qualities of San Francisco startups may be tied to the decision to locate in an urban center. If you were planning to manufacture semiconductor components, for instance, you would probably set up headquarters in a less space-constrained suburban setting.

While it can be frustrating to watch a company lurch from quarter to quarter without a profit in sight, there is ample evidence the approach can be wildly successful over time.

Seattle’s Amazon is probably the poster child for this strategy. Jeff Bezos, recently declared the world’s richest man, led the company for more than a decade before reporting the first annual profit.

These days, San Francisco seems to be ground central for this company-building technique. While it’s certainly not necessary to locate here, it does seem to be the single urban location most closely associated with massively scalable, money-losing consumer-facing startups.

Perhaps it’s just one of those things that after a while becomes status quo. If you want to be a movie star, you go to Hollywood. And if you want to make it on Wall Street, you go to Wall Street. Likewise, if you want to make it by launching an industry-altering business with a good shot at a multi-billion-dollar valuation, all while losing eye-popping sums of money, then you go to San Francisco.

Powered by WPeMatico

Square just announced that it’s reached an agreement to acquire Weebly for $365 million in cash and stock.

While Square is best known for its payment software and hardware, it’s also been expanding into other areas; for example, with the acquisition of food delivery service Caviar and corporate catering startup Zesty.

Weebly, meanwhile, offers easy-to-use website-building tools. While those tools can be used by individuals (my personal website is built on Weebly), the company has increasingly focused on serving small businesses and e-commerce companies.

Meanwhile, competitor Squarespace raised $200 million at a $1.7 billion valuation at the end of last year.

Square says that by acquiring Weebly, it can create “one cohesive solution” for entrepreneurs looking to build an online and offline business. And because 40 percent of Weebly’s 625,000 paid subscribers are outside the U.S., the deal will help Square expand globally.

“Square and Weebly share a passion for empowering and celebrating entrepreneurs,” said Square CEO Jack Dorsey in the acquisition release. “Square began its journey with in-person solutions while Weebly began its journey online. Since then, we’ve both been building services to bridge these channels, and we can go even further and faster together.”

Weebly was founded in 2007 by David Rusenko, Chris Fanini and Dan Veltr. (Rusenko, who’s still the company’s CEO, is pictured above.) According to Crunchbase, the company raised $35.7 million in funding from Sequoia Capital, Tencent Holdings, Baseline Ventures, Floodgate, Felicis, Ron Conway and Y Combinator.

Square says the acquisition price includes stock for Weebly founders and employees that will vest over a four-year period.

Update: During a conference call with reporters, Square executives were asked whether the company is becoming more acquisitive. CFO Sarah Friar said it was more a case of “serendipity.” In this instance, Square and Weebly had been working together for years now, and she said, “We love the way David and the company talk about the entrepreneur. Culturally, we feel very aligned.”

Friar cautioned against into reading this as a situation where Square “decided to wake up … and do a bunch of acquisitions.” For the most part, she said the company will stick to “a build path and a partner path.”

Most of the Weebly team will be joining Square. Rusenko added that he just finished the all-hands meeting where he announced the acquisition.

“There’s just a tremendous amount of excitement … a true shared and mutual respect,” he said. He also recalled telling his team, “I am very excited to continue working on this mission for a very long time.”

Powered by WPeMatico

When you’re raising venture capital, it helps if you’ve had “exits.” In other words, if your company has been acquired or you’ve taken one public, investors are more inclined to take a bet on anything you do.

Boston -based serial entrepreneur David Cancel has sold not just one, but four companies. And after a few years running product for HubSpot, he’s in the midst of building number five.

That startup, Drift, managed to raise $47 million in its first three years. Now it’s announcing another $60 million led by Sequoia Capital, with participation from existing investors CRV and General Catalyst. The valuation is undisclosed.

So what is Drift? It’s “changing the way businesses buy from businesses,” said Cancel. He wants to eventually build an alternative to Amazon to make it easier for companies to make large orders.

Currently, Drift subscribers can use chatbots to help turn web visits into sales. It has 100,000 clients including Zenefits, MongoDB, Zuora and AdRoll.

Drift “turns those conversations into customers,” Cancel explained. He said that technology is comparable to what is commonly used for customer service. It’s the “same messaging that was used for support, but used in the sales context.”

In the long-run, Cancel says he hopes Drift will expand its offerings to compete with Salesforce.

The company wouldn’t disclose revenue, but says it is ten times better compared to whatever it was in the past year. And it’s on track to grow another five times this year. This, of course, means little without hard numbers.

Yet we’re told that the new round means that Drift will have $90 million in the bank. It plans to use some of the funding to make acquisitions in voice and video technology. Drift also plans to expand its teams in both Boston and San Francisco, with new offices for both. The company presently has 130 employees.

Powered by WPeMatico