Robinhood

Auto Added by WPeMatico

Auto Added by WPeMatico

The venture capital world is constantly changing, and its evolution can sometimes flip pieces of conventional wisdom on their heads. For example, a recent flurry of extension rounds from Silicon Valley’s hottest startups like Stripe and Robinhood seem to signal that the investment type has suddenly become cool.

Extensions evolving from unloved to hot is not the first time that a type of VC deal has gained, or lost luster. In past times, for example, raising consecutive rounds from the same lead investor was often perceived as a negative signal; why couldn’t the startup find a new, different lead investor? Today, in contrast, venture capitalists are using inside rounds to double-down on winning startups, a way of helping ensure returns for their own backers.

The recent phenomenon of extensions becoming vogue is a tale of the times, in which the best startups get to play offense, and startups that can’t show accelerating growth are left behind. Let’s explore what has changed.

TechCrunch first wrote about the new extension-round trend after seeing what felt like a wave of the deals crop up. Some were large, like MariaDB’s huge $25 million add-on to its Series C, or Robinhood’s biblical $320 million addition to its Series F.

But most were smaller events like Sayari adding $2.5 million to its Series B, or CALA adding $3 million to its seed round. Even more recently, Eterneva raised another $3 million on top of its seed round, and also out this week was a million pounds more for Edinburgh-based Machine Labs’ seed round.

One reason for the growth of extension rounds in 2020 has been runway — making sure that a startup has enough. Upstarts often raise on an 18-month cadence. But because of COVID-19 and its constituent economic disruptions, many have reduced costs in a bid to bolster how long they have until their cash stores reach zero.

Powered by WPeMatico

The stakes keep getting higher for American discount brokerage Robinhood, which today disclosed that it has added hundreds of millions of dollars to its previously disclosed funding round.

Including the $280 million that the company had already announced, Robinhood said that it was “pleased to share” that it “raised an additional $320 million in subsequent closings.” Its now $600 million funding round brings its post-money valuation to $8.6 billion. Fortune first reported the news.

(A detail, but the new capital is part of the same round as it was raised at the same price. TechCrunch reported when the company’s $280 million round was announced, the fintech company was worth $8.3 billion. Another $300 million in capital at a flat share price means that the company’s valuation should have risen by only the dollar amount added. As it did.)

Robinhood has had a good business year, even if some of its practices have come under fire. The company pledged to tighten up parts of its platform relating to more exotic trading after the suicide of one of its users, for example; a topic that TechCrunch discussed at length last week.

What is inescapable is that Robinhood is having one hell of a year. When it might go public isn’t clear, especially as the private company is having no problem raising capital without an IPO. But as its value continues to rise, it becomes an increasingly remote acquisition target.

Powered by WPeMatico

Consumer fintech startups were massively successful in 2019, attracting millions of new users and disrupting traditional retail banks and financial services with mobile-first, consumer-oriented products. Despite the economic downturn in public markets and the massive wave of cuts at public and private companies in recent weeks, fintech startups have been raising a ton of money.

It feels like they’re all building a war chest to survive the economic winter as traditional banks continue to iterate so they can catch up and offer more user-friendly services. This is not the time to raise fees, slow down on product development or plans to acquire new users.

Back in January, I looked at challenger banks and their growth trajectories, but since then, they have managed to attract even more customers. According to the most recent figures:

And that’s without mentioning Starling Bank, Atom Bank, Bunq, Bnext, Paysend, etc. At some point, there will be as many challenger banks as non-challenger banks — perhaps we shouldn’t call them challenger banks anymore.

Beyond these startups, trading app Robinhood recently reached 13 million users, international payments startup TransferWise has 7 million customers and cryptocurrency exchange Coinbase has 30 million users.

Powered by WPeMatico

As expected, Robinhood has closed a new round of capital. The late-stage, consumer investing app announced today that it has closed a $280 million Series F funding at an $8.3 billion valuation. This closely tracks prior coverage that the firm was hunting for a nine-figure round at a valuation of around $8 billion.

Robinhood raised capital several times in 2019, including a $323 million mid-year Series E that valued the firm at around $7.6 billion, counting the value of the investment.

The valuation gains that the Menlo Park, Calif.-based unicorn has enjoyed over time are slowing. The firm’s 2017 Series C valued it at around $1.3 billion. That rose to around $5.6 billion the next year when it raised $363 million in its Series D. The firm’s Series E’s $7.6 billion valuation was strong, then, but a deceleration. And today’s $8.3 billion valuation brings its slimmest valuation gain in years.

It seems likely that Robinhood is growing into its valuation as it scales. According to its blog post, Robinhood has added 3 million accounts this year.

According to Bloomberg, which broke the news of the firm’s then-impending funding round, Robinhood recorded around $60 million in revenue this March, three times its February result. It is unclear if the firm can continue that pace of revenue generation during the remainder of 2020, but Robinhood’s trailing valuation multiple would decline sharply if the feat was possible. (Revenue multiples are broadly contracting as the economy slows, and investors project slower growth amongst startups.)

But while Robinhood is caught in an updraft that is lifting the fortunes of many savings and investing apps, its road has not been entirely smooth this year.

Robinhood made headlines in March with less fortuitous news: three outages in two weeks. An outage, in the company’s case, means that consumers were unable to trade during specific hours due to technical difficulties. As the financial services startup handles people’s money — often tied to specific market movements — making any disruption to its operations the opposite of good news.

The stability of apps that handle your money is especially important right now, as people try to get their financial health in order amid rising unemployment and an uncertain future economy at large, let alone the stock market.

We don’t know whether the round was closed before the outages and before COVID-19, but we wouldn’t be surprised if discussions were underway months earlier. (We asked; Robinhood declined to comment.)

It’s worth noting that when Robinhood suffered its first massive outage, its co-CEOs noted that the cause was largely due to a stress on infrastructure due to an unprecedented load of usage.

Robinhood has spent time in the last few weeks figuring out how to handle another increases in usage — sensibly, the new capital will be used to build out capabilities and prevent future crashes. (The company said in its announcement that it intends to “continue to invest in scaling our platform.”)

It’s going to need that platform stability if the market keeps moving as swiftly toward its portion of the fintech world as it has in the last few months.

Robinhood’s citing of “unprecedented load” as part of the cause of its difficulties drove some snark. It’s hard to fit a small brag into an apology, after all. But one thing TechCrunch has learned is that individuals are investing and saving during the pandemic.

Data for this abounds. Acorns, a savings and investing app, saw a record of signups on March 19, the same day that the company noted the stock market recorded their second-worst day of trading since 1987.

We’ve collected further data in the same vein, with Public (another free stock-trading app) reporting surging usage, and other fintech providers telling TechCrunch that more folks than ever are looking to save and buy stocks. Indeed, Robinhood later said that in March it saw “more than 10x net deposits” when compared to the monthly average it set in the last quarter of 2019.

The company, then, raised around a usage high. This makes its failure to generate a larger valuation premium nearly confusing; after all, when would there be a better time for it to raise? The answer appears to be that the same market dynamic that gave it a surge in demand (the pandemic) is likely also the reason that its valuation gains were slight (falling revenue multiples and falling private investor sentiment).

Sequoia Capital led the round, which saw participation from NEA, fintech-focused Ribbit and smaller firms 9Yards Capital and Unusual Ventures.

Other companies are riding the same fundraising wave. Last week, investing app Stash raised a $112 million round led by LendingTree. In its most recent quarter Stash claims it had an over 100% increase in weekly customer deposits across banking and investing.

There are no shortages of other investing platforms for consumers during this time, even if that looks like a traditional incumbent bank. With a new nine-figure round, Robinhood will have to prove that it is competitive, and more importantly, reliable.

Powered by WPeMatico

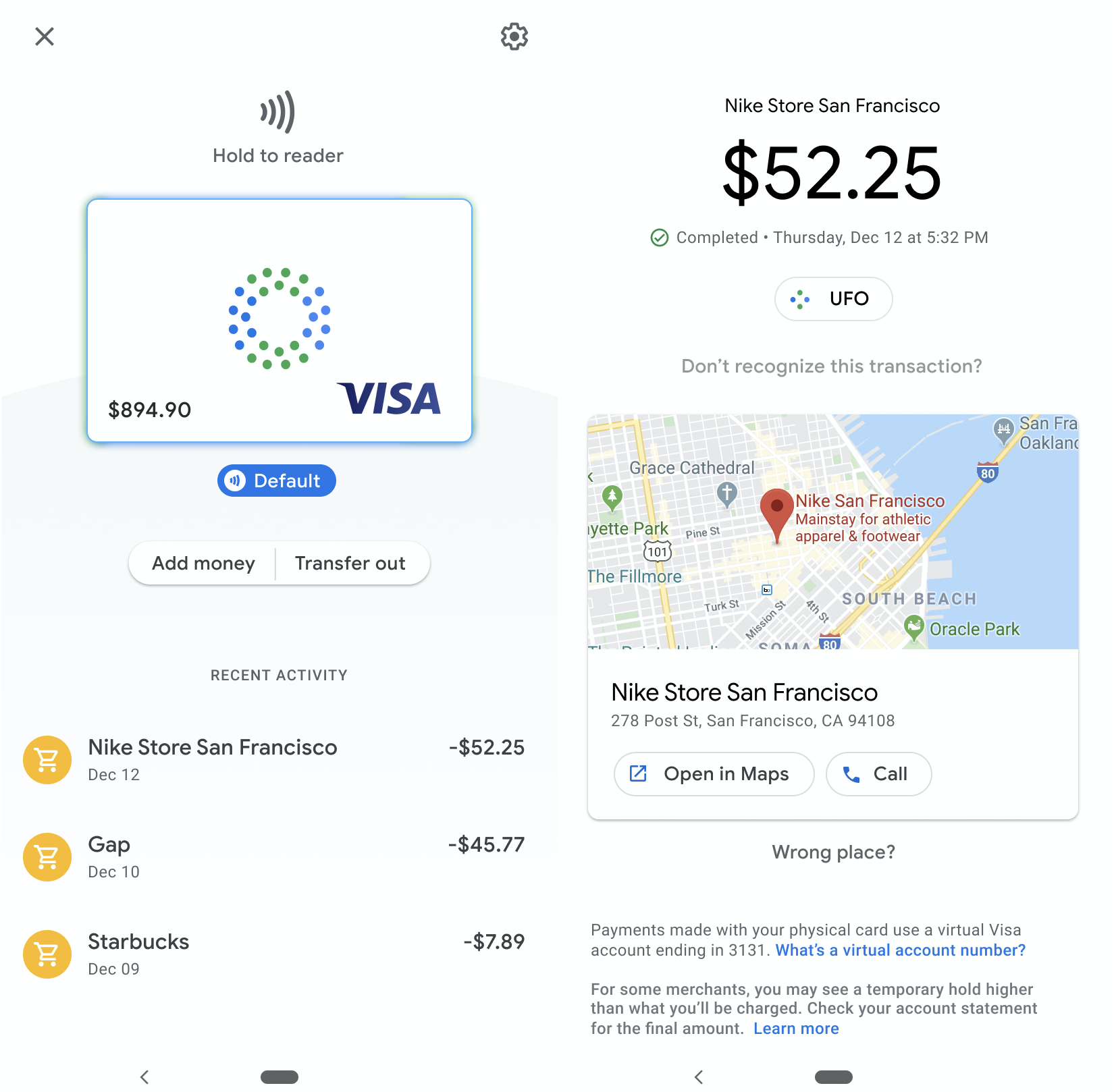

Would you pay with a “Google Card?” TechCrunch has obtained imagery that shows Google is developing its own physical and virtual debit cards. The Google card and associated checking account will allow users to buy things with a card, mobile phone or online. It connects to a Google app with new features that let users easily monitor purchases, check their balance or lock their account. The card will be co-branded with different bank partners, including CITI and Stanford Federal Credit Union.

A source provided TechCrunch with the images seen here, as well as proof that they came from Google. Another source confirmed that Google has recently worked on a payments card that its team hopes will become the foundation of its Google Pay app — and help it rival Apple Pay and the Apple Card. Currently, Google Pay only allows online and peer-to-peer payments by connecting a traditionally issued payment card. A “Google Pay Card” would vastly expand the app’s use cases, and Google’s potential as a fintech giant.

By building a smart debit card, Google has the opportunity to unlock new streams of revenue and data. It could potentially charge interchange fees on purchases made with the card or other checking account fees, and then split them with its banking partners. Depending on its privacy decisions, Google could use transaction data on what people buy to improve ad campaign measurement or even targeting. Brands might be willing to buy more Google ads if the tech giant can prove they drive a sales lift.

The long-term implications are even greater. While once the industry joke was that every app eventually becomes a messaging app, more recently it’s been that every tech company eventually becomes a financial services company. A smart debit card and checking accounts could pave the way for Google offering banking, stock brokerage, financial advice or robo-advising, accounting, insurance or lending.

Image Credits: jossnatu / Getty Images

Google’s vast access to data could allow it to more accurately manage risk than traditional financial institutions. Its deep connection to consumers via apps, ads, search and the Android operating system gives it ample ways to promote and integrate financial services. With the COVID-19 downturn taking shape, high-margin finance products could help Google develop efficient revenue opportunities and build its share price back up.

When TechCrunch asked Google for confirmation, it did not dispute our findings or assertions. The company offered us a statement it provided reporters following a November story, wherein Google told The Wall Street Journal’s Peter Rudegeair and Liz Hoffman it was experimenting in the checking account space. TechCrunch is the first to report Google’s debit card plans:

We’re exploring how we can partner with banks and credit unions in the US to offer smart checking accounts through Google Pay, helping their customers benefit from useful insights and budgeting tools, while keeping their money in an FDIC or NCUA-insured account. Our lead partners today are Citi and Stanford Federal Credit Union, and we look forward to sharing more details in the coming months.

For now, Google’s strategy is to let partnered banks and credit unions provide the underlying financial infrastructure and navigate regulation while it builds smarter interfaces and user experiences. It’s forseeable that one day Google might cut out the banks and take all the spoils for itself. Google launched a Wallet debit card in 2013 as an extension of its old payment app Google Wallet, but shut the card down in 2016. Given Google’s penchant for renaming or shutting down then reviving products, building a new debit card feels on-brand.

With people around the world suddenly more concerned about their finances amidst the coronavirus economic disaster, a debit card with more transparency and controls could be appealing.

Traditional banking products can be clunky, often requiring phone communication with customer service or sifting through cluttered websites to address security issues. Google hopes to make financial management as intuitive as its email and mapping apps. The card and app designs shown here are not final, and it’s unclear when Google’s debit card may launch. But let’s take a look at what these internal Google materials reveal about its ambitions for its payment instrument.

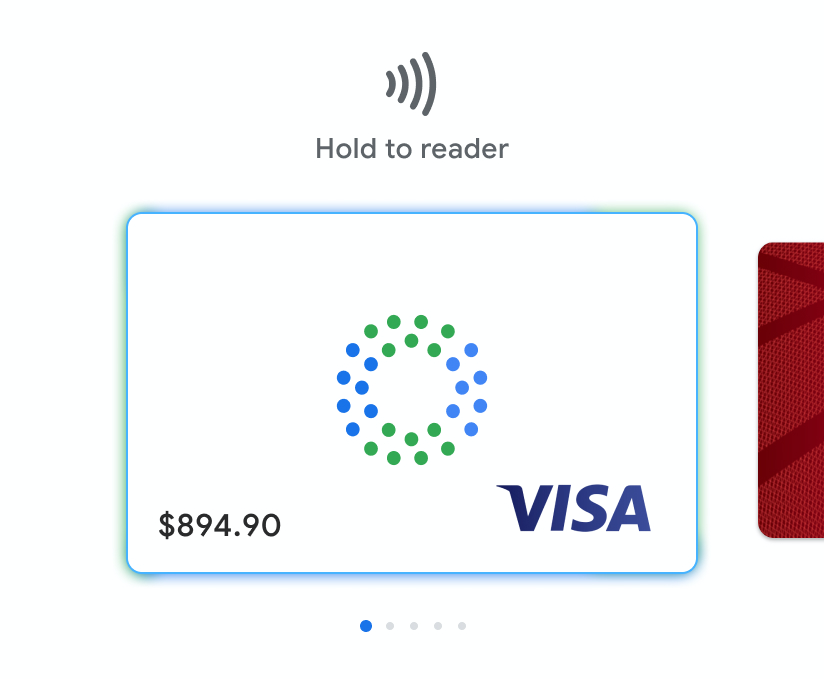

The Google debit card will come co-branded with the Google name and its partnered bank, though the exact name of the product is still unknown. In the designs, it’s a chip card on the Visa network, though Google could potentially support other networks like Mastercard. Users are able to add money or transfer funds out of their account from the connected Google app, which is likely to be Google Pay, and use a fingerprint and PIN for account security.

Once connected to their bank or credit union account, users could pay for purchases in retail stores with a physical Google debit card, including with contactless payments, by just holding it up to a card reader. A virtual version of the card that lives on a user’s phone can also be used for Bluetooth mobile payments. Meanwhile, a virtual card number can be used for online or in-app payments.

Users are shown a list of recent transactions, with each including the merchant name, date and price. They can dig into each transaction to see the location on a map, get directions or call the store. If users don’t recognize a transaction, it’s easy to protect themselves with the card’s vast security options.

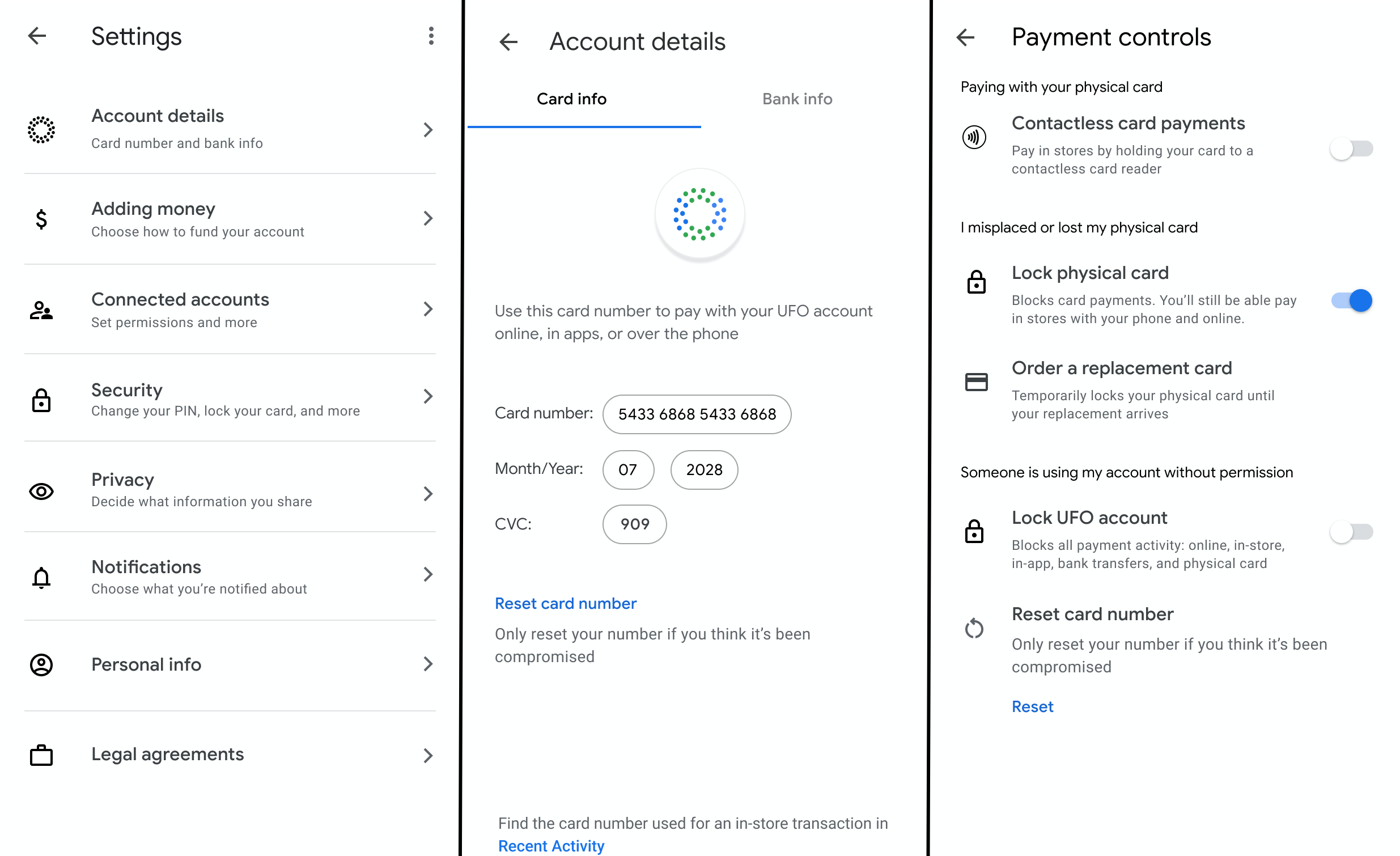

If a customer suspects foul play because they lost their card, they can lock it and optionally order a replacement while still being able to pay with their phone or online, thanks to Google’s virtual card number system that’s different than the one on their physical card. If instead they suspect their virtual card number was stolen by a hacker, they can quickly reset it. And if they believe someone has gained unauthorized access to their account, they can lock it entirely to block all types of payments and transfers.

The settings reveal options for notifications and privacy controls to “decide what information you share,” though we don’t have imagery of what’s contained in those menus. It’s unclear how much power Google will give customers to limit the company or merchant’s data access. Google’s decisions there could impact how transaction data might fuel its other businesses.

Google is a relative late-comer to offering its own card. Apple launched its Apple Card in August, offering a slickly designed titanium Mastercard credit card backed by Goldman Sachs. It charges minimal customer fees, comes with a virtual card for use through Apple Pay and generates interest.

Apple Card

Apple does collect interchange fees from merchants, though, which Google could similarly gather to earn revenue. Last month, Apple changed the Card’s privacy settings to share more data with Goldman Sachs that might also help the two provide additional financial services. Apple Pay now accounts for 5% of global card transactions, and is forecast to hit 10% by 2024, according to Bernstein research. The underlines the gigantic market Google is gunning for here.

The stock brokerage and robo-advisor apps have also joined the payments race. Wealthfront launched cash accounts and debit cards last February, bringing in $1 billion in assets in two months and doubling the company’s total holdings to $20 billion by September. Betterment launched its checking product in October 2019 with a Visa debit card, but it doesn’t generate interest.

Robinhood botched the December 2018 launch of its checking accounts due to ineligible insurance, but relaunched in October 2019 with debit card withdrawls from 75,000 ATMs and a solid interest rate. It’s unclear how Google’s card will work with ATMs or how its checking accounts will generate interest.

Robinhood’s debit cards

The appeal for Google and the rest is clear. It seems whenever companies help move people’s money around, some of it inevitably “falls off the truck” and lands in their pockets. Financial services are typically low-overhead ways to generate revenue. That could be especially enticing, as Google has found many of its side hustle “other bets” to be unsustainable. It’s moved to prune some of these tertiary projects, such as its Makani wind energy kites.

Google may never find businesses as lucrative as its core in search and advertising, but it has the advantages to become a serious player in fintech. Its vast sums of cash, deep bench of engineering talent, experience building complex utilities, numerous consumer touch points and near-bottomless well of data could give it an edge over stodgier old banks and scrappier startups. And while Facebook slams into regulatory scrutiny and is forced to scale back its Libra cryptocurrency, Google’s more familiar approach via debit cards could pay off.

Powered by WPeMatico

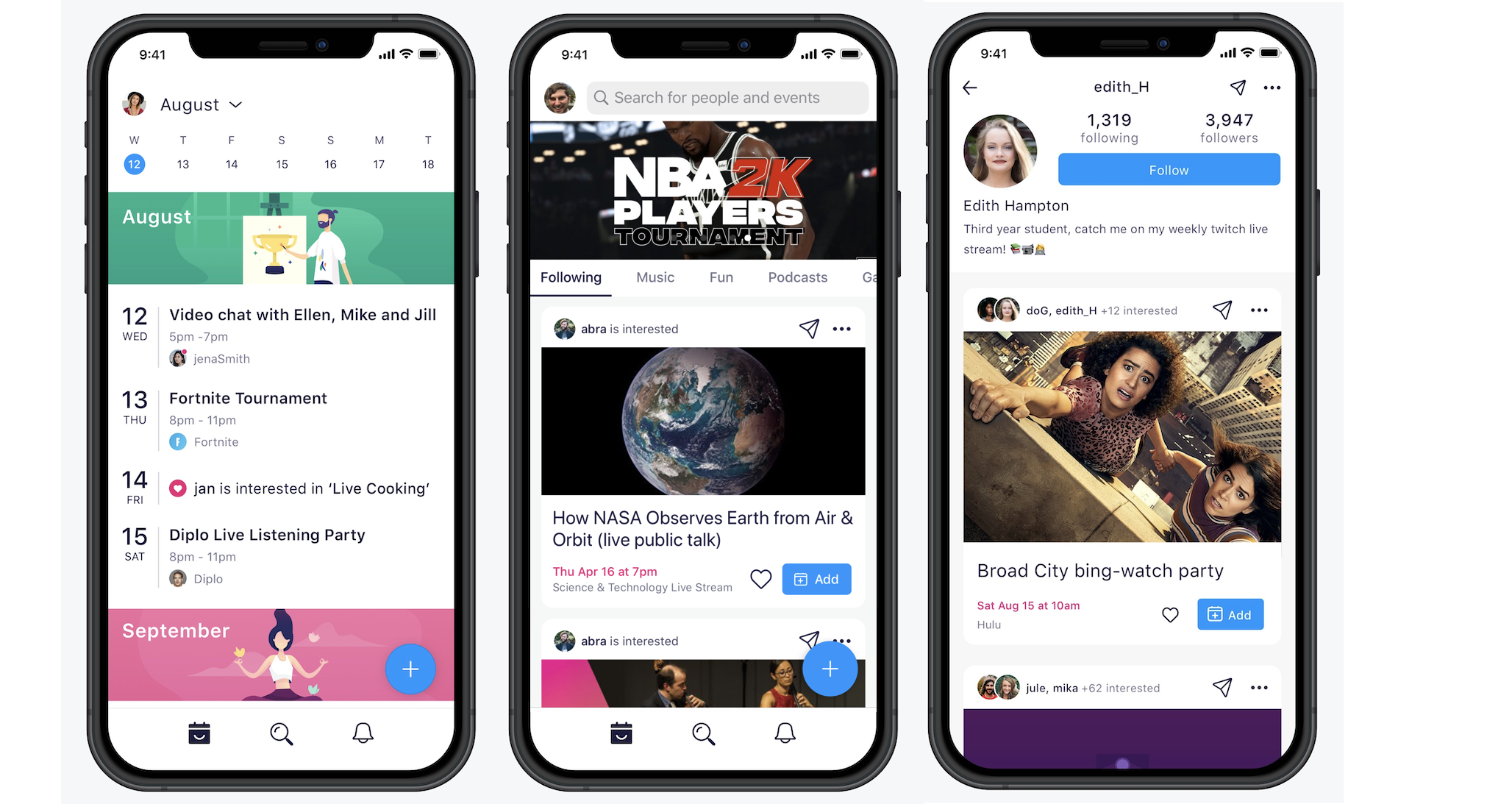

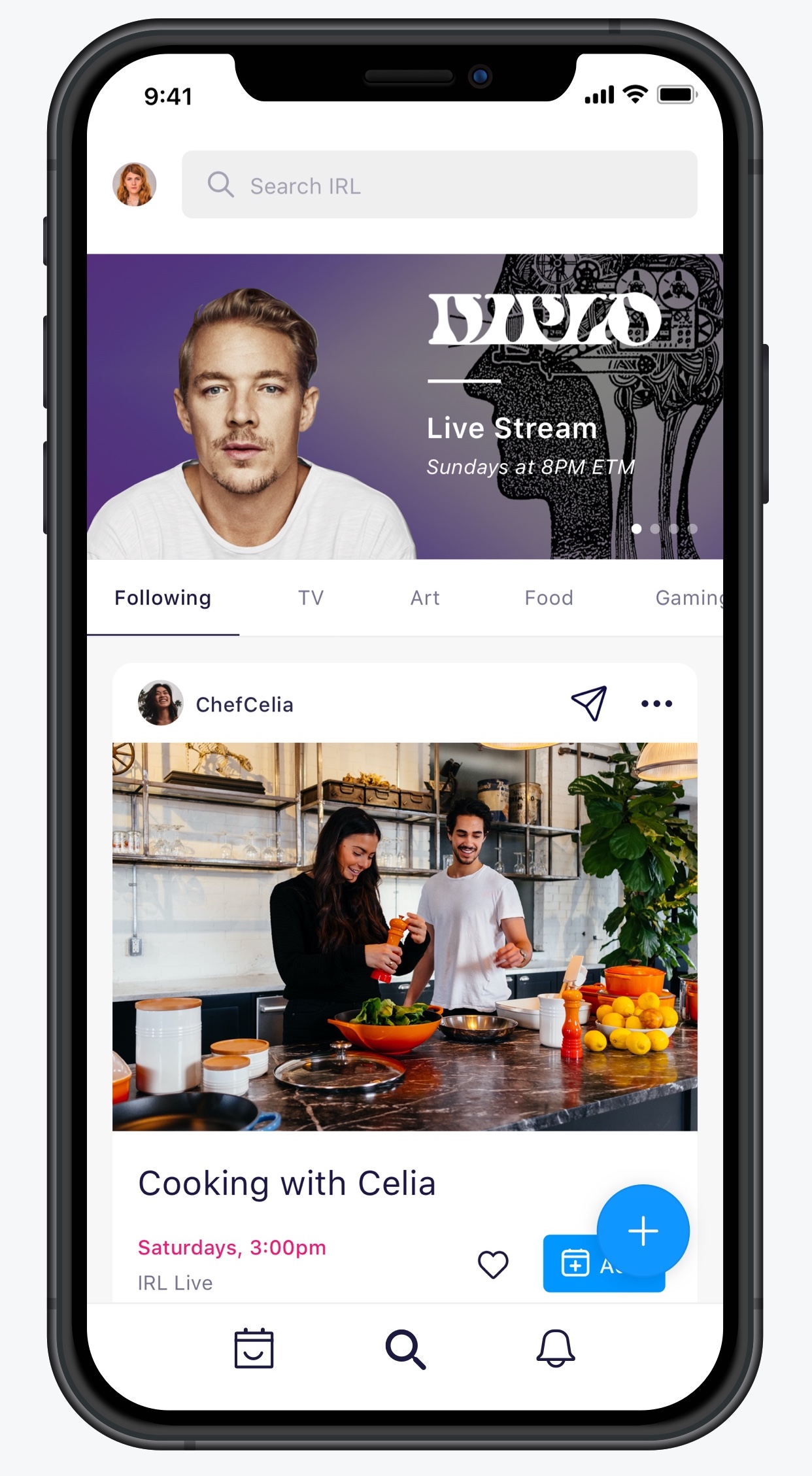

What do you do if you’re an event discovery startup and suddenly it’s illegal to attend events? You lean into the cultural shift and pivot. Today, $11 million-funded calendar app IRL is morphing from In Real Life to In Remote Life. It will now focus on helping people find, RSVP for, plan, share and chat about virtual events, from live-streamed concerts to esports tournaments to Zoom cocktail parties.

Coronavirus could make IRL relevant to a wider audience because before an event “only mattered if it was around you. But now with In Remote Life, content has no geographical limitations,” says IRL co-founder and CEO Abe Shafi. “The need is exponentially greater because everyone’s routines have been shattered.” IRL ranked No. 138 in the U.S. App Store today, making it the top calendar app, even above Google’s (No. 168).

IRL has some fresh product development talent to lead it through the transition. The startup has hired stock trading app Robinhood’s VP of Product Josh Elman . The former Greylock investor is well known for his product chops from jobs at Facebook, Twitter and LinkedIn. Elman joined Robinhood in early 2018 but left late last year, notably before its rash of recent outages that enraged users.

“I just realized more than anything that the company needed people who had 110% to give, and it wasn’t clear that was going to be me,” Elman said of Robinhood, now valued at $7.6 billion and struggling to scale. “My first passions and all the things I’ve talked about over the years have been social and media.”

“I just realized more than anything that the company needed people who had 110% to give, and it wasn’t clear that was going to be me,” Elman said of Robinhood, now valued at $7.6 billion and struggling to scale. “My first passions and all the things I’ve talked about over the years have been social and media.”

For now, IRL is a part-time gig, where he’ll be heading up a Secret Projects division. While most apps “try to suck more of our time,” he sees IRL as a chance to give this precious resource back to people. Though he insists “Robinhood’s great, I’m a very happy shareholder.”

“We were on a tear, hitting a stride with usaging and growth related to real life events,” says Shafi. “Then this happened,” motioning on our Zoom call to the COVID-19 reality we’re now stuck in. “We realized we had to pull all of our content because it wasn’t happening.”

Today IRL’s iOS app launches a redesign of its Discover home screen content to center on virtual events people can attend from home. There’s now tabs for gaming, podcasts, TV and EDU, as well as music, food, lifestyle and a catch-all “fun” section. Each event can be added to your calendar that syncs with Google Cal, or Liked to add it to your profile that friends and fans can follow. You also can instantly launch a group chat about the event in IRL, or share it to Instagram Stories or another messaging app.

Today IRL’s iOS app launches a redesign of its Discover home screen content to center on virtual events people can attend from home. There’s now tabs for gaming, podcasts, TV and EDU, as well as music, food, lifestyle and a catch-all “fun” section. Each event can be added to your calendar that syncs with Google Cal, or Liked to add it to your profile that friends and fans can follow. You also can instantly launch a group chat about the event in IRL, or share it to Instagram Stories or another messaging app.

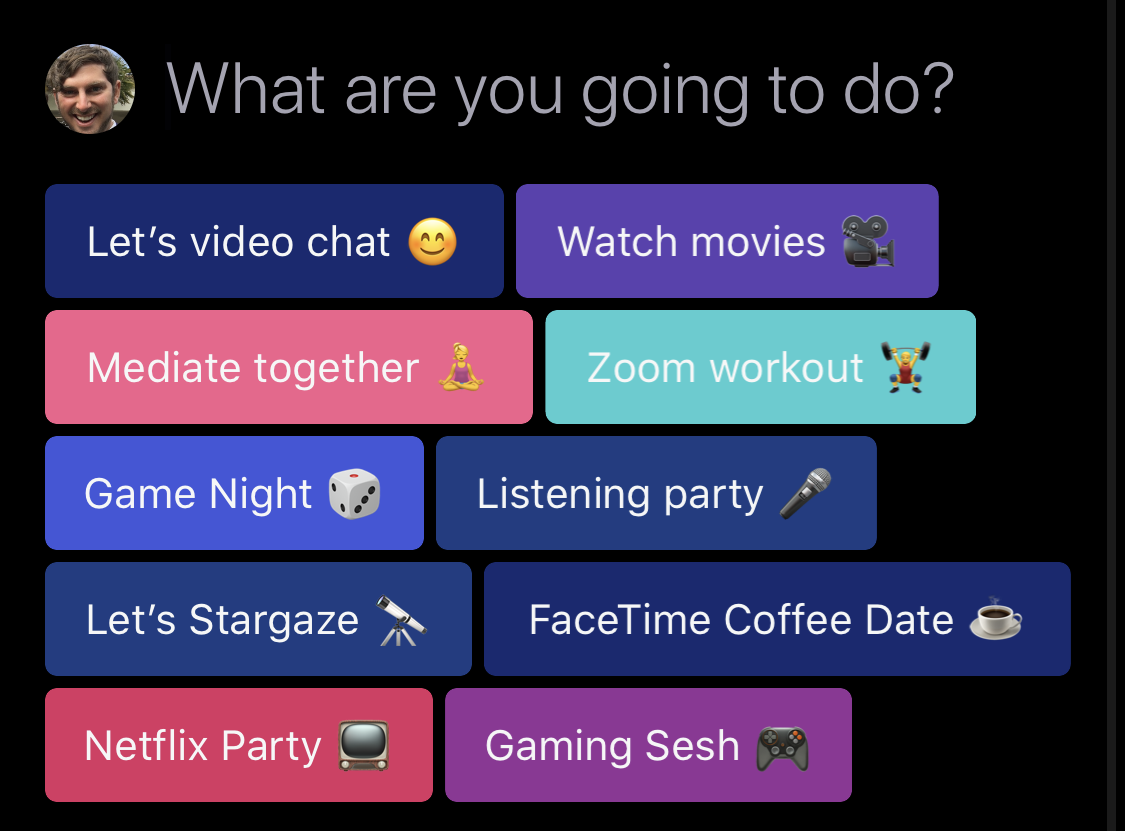

If you can’t find something public to do, you can make plans with friends using the composer with suggestions like “Let’s video chat,” “Zoom workout,” “gaming sesh” or “Netflix party.” That instantly sets up a calendar event you can invite people to. And if you’re not sure when you want to host, IRL’s “Soon” option lets you keep the schedule vague so you and friends can figure out when everyone’s available. Indeed, 50% of IRL plans start out as “Soon,” Shafi reveals, identifying a gap in rigid time/date calendars.

Beyond individual events, IRL also wants to make it easier to develop habits by letting you subscribe to workout, meditation and other schedules. With sports seasons suspended, IRL lets people sync with calendars of hip-hop album releases and more instead. Or you can subscribe to an influencer’s life and digitally accompany them to events. The goal is that IRL will be able to merge offline events back into its content recommendations as social distancing subsides.

The biggest challenge for IRL will be tuning its event recommendation algorithm. It has lost a lot of the traditional relevance signals about events, like how close they are to your home, how much they cost or if they’re even in your city. Transitioning to In Remote Life means a global range of happenings is now available to everyone, and because they’re often free to host, many lonely low-quality events have sprung up. That makes it much tougher for IRL to determine what to show.

For now, it’s basing recommendations on what you engage with most on its home screen, but I found that can make the initial experience very hit-or-miss. The top events in each category were rarely exciting. But IRL is planning to beef up its onboarding process to ask about your interests, and integrate with Spotify so it knows which musicians’ online concerts you’d want to attend.

Still, Shafi thinks IRL is already better than asocial alternatives. “Our main age range is 13 to 25, college and post-college metropolitan areas and across college campuses. Our average user has never used a calendar before, or they’ve just used a default calendar like Gcal or iCal.

Hopefully, IRL will take a more serious swing at helping friends realize they’re free at the same time and can hang out. While Down To Lunch failed in this space, now Facebook Messenger and Instagram are exploring it with their auto-status feature, and location apps like Snap Map and Zenly could adapt to share not just where you are, but if you have the intention to hang out.

“How can we use just a little bit of nudging, transparency or suggestion to get people to just do one more thing per month?,” Shafi asks. IRL is trying to figure out how to let you passively share that “I have 2 hours free” in a way that “never makes you feel rejected if they don’t respond.”

Facebook did launch a standalone Events calendar app back in 2016, but later paired down the calendaring features, folded it in with restaurant recommendations and renamed it Local. “As big as Facebook is, it can only do so many things insanely well,” Elman says of his old employer. “They could do more [on Events], but it’s never been the juggernaut like photos.”

Shafi is happy to have the opportunity in such a foundational space. He describes the concept of the calendar as one he’s sure will outlive him, so it’s worth the effort to make it social no matter how long it takes — though I’m sure his investors like Goodwater Capital, Founders Fund, Kleiner Perkins and Floodgate hope it’ll find a way to monetize eventually.

Revenue could come in the form of selling access to events through the app, or letting promoters and local businesses pay for enhanced discovery. For now, though, IRL is building a deeper connection with event and content publishers with the upcoming launch of its free Add To Calendar button they can build into their sites and emails. Elman says several services charge for these buttons that integrate with Apple and Google’s calendars, but IRL hopes giving them away will help fill its app with things to do, whatever that might be.

“Our tagline is ‘live your best life.’ It’s not judgmental. If your best life is playing video games on your couch with your homies, we don’t judge you for that.”

Powered by WPeMatico

Hello and welcome back to our regular morning look at private companies, public markets and the gray space in between.

Earlier this week, the popular free stock trading service Robinhood suffered downtime over a two-day period. The company, a well-funded unicorn taking on incumbents in its industry, failed to operate properly when the public markets were surging on Monday (bad) and falling on Tuesday (very bad).

Complaints flooded investing forums and social media. Images of Robinhood account screens featuring huge losses from the periods of downtime (or missed upside) weren’t hard to find. For Robinhood, it wasn’t its first misstep, but it was perhaps its worst. Mishandling the rollout of a high-yield savings function? Embarrassing, but hardly a serious wound. Some options oddness? Eh, not the worst.

Going down during surging volatility? Much worse. The company is already in the market with apologies and some give-aways to try to stem the negative news cycle. But what’s notable so far is that, while you might expect to see rival apps and services to Robinhood boom in the wake of its downtime, it instead appears that only select competitors to the popular company are seeing a jump in downloads this week. And given the insane market movements, it’s hard to pin some of their gains on Robinhood instead of, say, what stocks are themselves doing.

I’d expected by today to have some data in hand that painted a starker picture for Robinhood, given that the company’s recent missteps triggered a lot of negative press and user reaction. Let’s peek at what numbers can tell us, and try to figure out if there’s a lesson for consumer fintech and finservies companies while we’re at it.

Powered by WPeMatico

It wasn’t the leap year, a coding blip, or a hack that caused Robinhood’s massive outages yesterday and today that left customers unable to trade stocks. Instead, the co-CEOs

write that “the cause of the outage was stress on our infrastructure — which struggled with unprecedented load. That in turn led to a “thundering herd” effect — triggering a failure of our DNS system.”

Robinhood was offline from Monday at 6:30am Pacific to 11pm Pacific, then had another outage this morning from 6:30am Pacific until just before 9am Pacific.

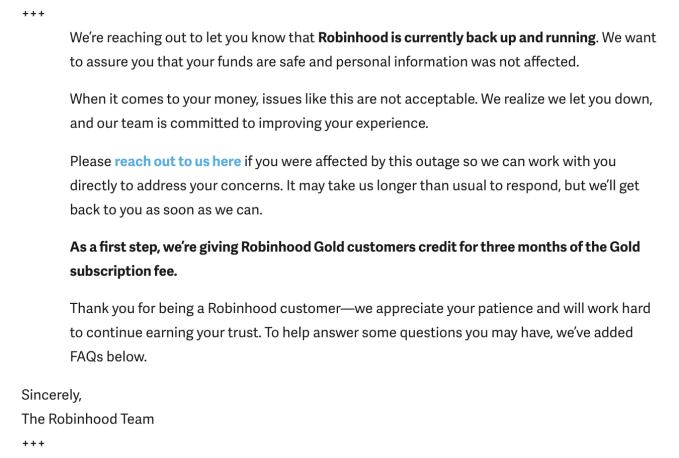

The $912 million-funded fintech giant will provide compensation to all customers of its Robinhood Gold premium subscription for borrowing money to trade plus access to Morningstar research reports, Nasdaq data, and bigger instant deposits. It’s offering them three months of service.

A month of Robinhood Gold costs $5 plus 5% yearly interest on borrowing above $1,000, charged daily. Before a pricing change, the flat fee per month could range as high as $200. However, compensated users will only get the $5 off per month, for a total of $15. That could seem woefully insufficient if Robinhood users missed out on buying back into stocks like Apple that went up over 9% on Monday. Robinhood is calling it a “first step”.

Impacted Robinhood users can contact the company here to ask for compensation. Below you can see the email Robinhood sent to custoemrs late last night.

Robinhood’s email to customers late last night

Robinhood is also working to contact impacted customers on a individual basis, and it’s looking into other forms of compensation on a case by case basis, company spokesperson Jack Randall tells me. It’s unclear if that might include cash to offset what traders might have lost by having their money locked in inaccessible Robinhood accounts during the outage.

Compensation could become a significant cost if the startup assesses that many of its 10 million users were impacted. The markets gained a record $1.1 trillion yesterday, but some Robinhood traders may not have been able to buy back in as the rebound occurred following mass selloffs due to fears of coronavirus.

Now the startup, valued at $7.6 billion, will have to try to regain users’ trust. “When it comes to your money, we know how important it is for you to have answers. The outages you have experienced over the last two days are not acceptable and we want to share an update on the current situation . . . We worked as quickly as possible to restore service, but it took us a while. Too long” wrote co-founders and co-CEO Baiju Bhatt and Vlad Tenev [disclosure: who I know from college].

As for exactly what triggered the downtime, the founders write that “Multiple factors contributed to the unprecedented load that ultimately led to the outages. The factors included, among others, highly volatile and historic market conditions; record volume; and record account sign-ups.” There’s been a frenzy of retail trading activity in the wake of coronavirus. There’s also been sudden spikes in stocks like Tesla amidst mainstream media attention.

Going forward, Robinhood promises to “work to improve the resilience of our infrastructure to meet the heightened load we have been experiencing. We’re simultaneously working to reduce the interdependencies in our overall infrastructure. We’re also investing in additional redundancies in our infrastructure.” However, they warn that “we may experience additional brief outages, but we’re now better positioned to more quickly resolve them.”

The outage comes at a vulnerable time for Robinhood as oldschool brokerages like Charles Schwab, Ameritrade, and Etrade all recently moved to eliminate per-trade fees to match Robinhood’s pioneering zero-comission trades. Though some of those brokerages experienced infrastructure troubles recently, Robinhood massive outages could push users towards those incumbents that they might perceive as more stable.

Powered by WPeMatico

It wasn’t the leap year, a coding blip, or a hack that caused Robinhood’s massive outages yesterday and today that left customers unable to trade stocks. Instead, the co-CEOs

write that “the cause of the outage was stress on our infrastructure — which struggled with unprecedented load. That in turn led to a “thundering herd” effect — triggering a failure of our DNS system.”

Robinhood was offline from Monday at 6:30am Pacific to 11pm Pacific, then had another outage this morning from 6:30am Pacific until just before 9am Pacific.

The $912 million-funded fintech giant will provide compensation to all customers of its Robinhood Gold premium subscription for borrowing money to trade, offering them three months of service. A month of Robinhood Gold costs $5 plus 5% yearly interest on borrowing above $1,000, charged daily. However, users will only get the $5 off per month, for a total of $15.

Impacted Robinhood users can contact the company here to ask for compensation. Below you can see the email Robinhood sent to custoemrs late last night.

Robinhood’s email to customers late last night

Robinhood is also working to contact impacted customers on a individual basis, and it’s looking into other forms of compensation on a case by case basis, company spokesperson Jack Randall tells me. It’s unclear if that might include cash to offset what traders might have lost by having their money locked in inaccessible Robinhood accounts during the outage.

Compensation could become a significant cost if the startup assesses that many of its 10 million users were impacted. The markets gained a record $1.1 trillion yesterday, but some Robinhood traders may not have been able to buy back in as the rebound occurred following mass selloffs due to fears of coronavirus.

Now the startup, valued at $7.6 billion, will have to try to regain users’ trust. “When it comes to your money, we know how important it is for you to have answers. The outages you have experienced over the last two days are not acceptable and we want to share an update on the current situation . . . We worked as quickly as possible to restore service, but it took us a while. Too long” wrote co-founders and co-CEO Baiju Bhatt and Vlad Tenev [disclosure: who I know from college].

As for exactly what triggered the downtime, the founders write that “Multiple factors contributed to the unprecedented load that ultimately led to the outages. The factors included, among others, highly volatile and historic market conditions; record volume; and record account sign-ups.” There’s been a frenzy of retail trading activity in the wake of coronavirus. There’s also been sudden spikes in stocks like Tesla amidst mainstream media attention.

Going forward, Robinhood promises to “work to improve the resilience of our infrastructure to meet the heightened load we have been experiencing. We’re simultaneously working to reduce the interdependencies in our overall infrastructure. We’re also investing in additional redundancies in our infrastructure.” However, they warn that “we may experience additional brief outages, but we’re now better positioned to more quickly resolve them.”

The outage comes at a vulnerable time for Robinhood as oldschool brokerages like Charles Schwab, Ameritrade, and Etrade all recently moved to eliminate per-trade fees to match Robinhood’s pioneering zero-comission trades. Though some of those brokerages experienced infrastructure troubles recently, Robinhood massive outages could push users towards those incumbents that they might perceive as more stable.

Powered by WPeMatico

Robinhood, the startup with a stock trading app valued upwards of at least $7.6 billion, suffered one of its worst outages on one of the busiest trading days of the year.

As the Dow Jones Industrial Average enjoyed the single biggest point-gain in the history of the index, Robinhood’s application fell prey to an error that locked users out of the service for the duration of Monday’s trading.

“We started experiencing downtime issues across our platform this morning at market open,” a spokesperson wrote in an email. “We don’t have an estimate when the issue will be resolved but all of us at Robinhood are working as hard as we can to resume service.”

One potential cause of the outages could just be the high trading volumes that have accompanied highly volatile markets over the past month. While there were some early reports that the bug was caused by a Leap Day bug, the company has denied that a February 29th error was at fault.

The company’s mistake could cost its users lots of money as they sought to trade on stocks that were hit in last week’s string of losses due to investor worries over the impact the novel coronavirus, COVID-19, would have on the global economy.

This isn’t the first time that Robinhood’s code has got the company into trouble. Last year, faulty coding allowed users to borrow more money than the company intended, giving a potential windfall to would-be traders.

Back in 2013 when the founders of the company discussed their idea around TechCrunch reporter Josh Constine’s kitchen table, they envisioned the app as a way to share hot tips. That quickly morphed into a trading platform that the company says has more than 10 million users on its platform.

The secret to the company’s initial success was free stock trading — a pricing model which many of its competitors have since gone on to copy.

According to Apptopia, Robinhood is far and away the most popular of the free stock trading services, having far more volume and users than its legacy contenders. However, as today’s outage showed, that user base may be negatively impacted by not working with companies who have had their services stress tested over decades. Even so, the big trading houses have also experienced technical issues over the past week, as CNBC reported earlier today.

Powered by WPeMatico