Robinhood

Auto Added by WPeMatico

Auto Added by WPeMatico

Before it was worth $7.6 billion, the original idea for Robinhood was a stock-trading social network. At my kitchen table in San Francisco in 2013, the founders envisioned an app for sharing hot tips to a feed complete with a leaderboard of whose predictions were most accurate. Once they had SEC approval, they pivoted toward the real money maker: letting people buy and sell stocks in the app, and pay to borrow cash to do so.

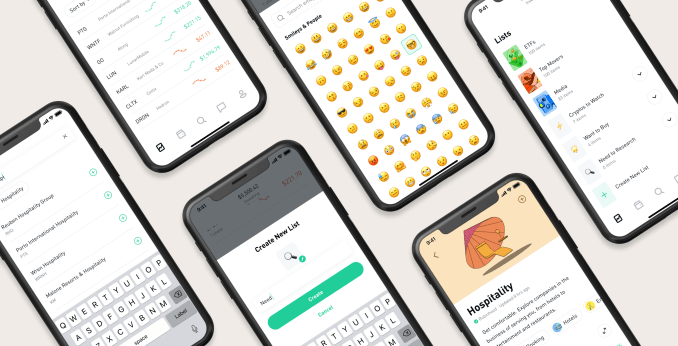

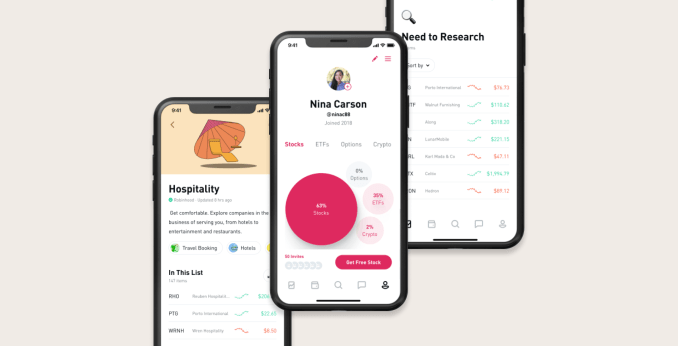

Now, seven years later, Robinhood is subtly taking the first steps back to its start. Today it’s launching Profiles. For now, they let users see analytics about their portfolio, like how concentrated they are in stocks versus options versus cryptocurrency, as well as across different business sectors. Complete with usernames and a photo, Profiles let you follow self-made or Robinhood-provided lists of stocks and other assets.

Profiles could give Robinhood’s customers the confidence to trade more, and create a sense of lock-in that stops them from straying to other brokerages that have dropped their per-trade fees to zero to match the startup, like Charles Schwab, Ameritrade and E-Trade, which was acquired for $13 billion today by Morgan Stanley, as reported by The Wall Street Journal.

The Profile features certainly sound helpful. They could reveal that your portfolio is too centered around tech, media and telecom stocks, or that you’re ignoring cryptocurrency or corporations from your home state. Lists also makes it easier to track specific business verticals, save stocks to buy when you have the cash or set aside some for deeper research. Robinhood pulls info from FactSet, Morningstar and other trusted sources to figure out which stocks and ETFs go into sector lists, or you can make and name your own. Profiles and lists begin to roll out to all users next week.

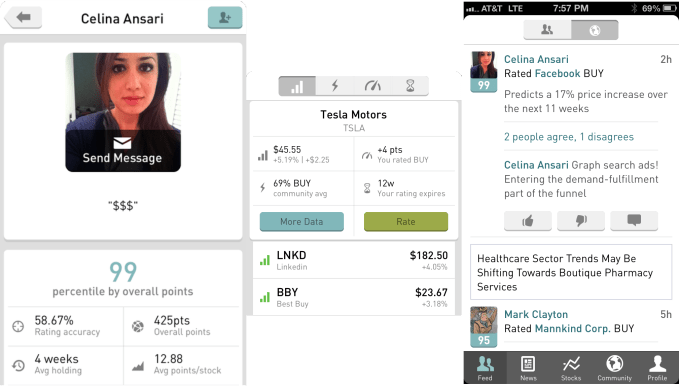

But what’s most interesting is how profiles lay the foundation for Robinhood as a social network. It’s easy to imagine letting users follow other accounts or lists they create. The original Robinhood app let users make predictions like “17% increase in Facebook share price over the next 11 weeks,” with comments to explain why. It showed users’ prediction accuracy, their average holding time for assets, a point score for smart foresight and community BUY or SELL ratings on stocks.

If Robinhood rebuilt some of these features, it might lessen the need for an expensive financial advisor or having enough cash to qualify for one with a different brokerage. Robinhood could let you crowdsource advice. “We understand the connotation of taking something from the rich and giving it to the poor. Robinhood is liberating information that’s locked up with professionals and giving it to the people,” Robinhood co-founder and co-CEO Vlad Tenev told me back in 2013.

Robinhood would certainly need to be careful about scammy tips going viral. Improper safeguards could lead to pump and dump schemes where those late to buy in get screwed when prices snap back to reality.

But embracing social could leverage some of its strongest assets: the youthfulness of its user base and the depth of connection to its users. The median age of a Robinhood customer is 30, and half say they’re first-time investors. Being able to turn to friends or experts within the app might convince them to pull the trigger on trades.

Most online brokerages are somewhat undifferentiated beyond differences in pricing, while their clunky, unstylized products don’t generate the same brand affinity as people have for Robinhood. Unsatisfied users could bail for a competitor at any time. Robinhood’s users are accustomed to social networking and the way it locks in users, because they don’t want to abandon their community.

When I asked Robinhood Profiles’ product manager Shanthi Shanmugam directly about whether this was the start of more social trading features, they suspiciously dodged the question, telling me, “When thinking about how to reflect who you are as an investor, we looked at how other apps represent you and it felt natural to leverage a design that felt more like a profile. When helping people group their investment ideas, it was easy to envision this as a playlist you might find on your favorite music app.”

That’s far from a denial. Offering social validation for trading could help Robinhood earn more from its customers despite their small total account balances. While Robinhood might have more than 10 million accounts versus E-Trade’s 5.2 million and Morgan Stanley’s 3 million, E-Trade’s average account size is $69,230 and Morgan Stanley’s is $900,000, while a survey found most of Robinhood’s held $1,000 to $5,000.

That all means that Robinhood earns less on interest sitting in users’ accounts than the old incumbents. But Robinhood earns the majority of its money on selling order flow and through its subscription Robinhood Gold feature that lets users pay monthly so they can borrow cash to trade with. Profiles and lists, and then eventually more social features, could get Robinhood’s users trading more so there’s more order flow to sell and more reason for them to buy subscriptions.

“Democratizing access is about lowering fees, minimums and other barriers people face — like confidence. Profiles and lists make finance easier to understand and more familiar for people,” says Shanmugam. More social features built safely, more reassurance, more trading, more revenue. Robinhood has raised $910 million. But to outgun larger competitors like the newly assembled Morgan Stanley/E-Trade that’s matched its zero-fee pricing, Robinhood will have to win with product.

Powered by WPeMatico

One share of Amazon stock costs more than $1,700, locking out less-wealthy investors. So to continue its quest to democratize stock trading, Robinhood is launching fractional share trading this week. This lets you buy 0.000001 shares, rounded to the nearest penny, or just $1 of any stock, with zero fee.

The ability to buy by millionth of a share lets Robinhood undercut Square Cash’s recently announced fractional share trading, which sets a $1 minimum for investment. Robinhood users can sign up here for early access to fractional share trading. “One of our core values is participation is power,” says Robinhood co-CEO Vlad Tenev. “Everything we do is rooted in this. We believe that fractional shares have the potential to open up investing for even more people.”

Fractional share trading ensures no one need be turned away, and Robinhood can keep growing its user base of 10 million with its war chest of $910 million in funding. As incumbent brokerages like Charles Schwab and E*Trade move to copy Robinhood’s free stock trading, the startup has to stay ahead in inclusive financial tools. In this case, though, it’s trying to keep up, since Schwab, Square, Stash and SoFi all launched fractional shares this year. Betterment has actually offered this since 2010.

Robinhood has a bunch of other new features aimed at diversifying its offering for the not-yet-rich. Today its Cash Management feature it announced in October is rolling out to its first users on the 800,000-person wait list, offering them 1.8% APY interest on cash in their Robinhood balance plus a Mastercard debit card for spending money or pulling it out of a wide network of ATMs. The feature is effectively a scaled-back relaunch of the botched debut of 3% APY Robinhood Checking a year ago, which was scuttled because the startup failed to secure the proper insurance it now has for Cash Management.

Additionally, Robinhood is launching two more widely requested features early next year. Dividend Reinvestment Plan (DRIP) will automatically reinvest into stocks or ETF cash dividends Robinhood users receive. Recurring Investments will let users schedule daily, weekly, bi-weekly or monthly investments into stocks. With all this, and Crypto trading, Robinhood is evolving into a full financial services suite that will be much harder for competitors to copy.

“We believe that if you want to invest, it shouldn’t matter how much money you have. With fractional shares, we’re opening up a whole universe of stocks and funds, including Amazon, Apple, Disney, Berkshire Hathaway, and thousands of others,” Robinhood product manager Abhishek Fatehpuria tells me.

Users will be able to place real-time fractional share orders in dollar amounts as low as $1 or share amounts as low as 0.000001 shares rounded to the penny during market hours. Stocks worth over $1 per share with a market capitalization above $25 million are eligible, with 4,000 different stocks and ETFs available for commission-free, real-time fractional trading.

“We believe that participation is power. Since day one, we’ve focused on breaking down barriers like trade commissions and account minimums to help people participate in the financial system,” says Fatehpuria. “We have a unique user base — half our customers tell us they’re first-time investors, and the median age of a Robinhood customer is 30. This means we have a unique opportunity to expand access to the markets for this new generation.”

Robinhood is racing to corner the freemium investment tool market before other startups and finance giants can catch up. It opened a waitlist for its U.K. launch next year, which will be its first international market. But in just the past month, Alpaca raised $6 million for an API that lets anyone build a stock brokerage app, and Atom Finance raised $12.5 million for its free investment research tool that could compete with Robinhood’s in-app feature. Meanwhile, Robinhood suffered an embarrassing bug, letting users borrow more money than allowed.

The move fast and break things mentality triggers new dangers when introduced to finance. Robinhood must resist the urge to rush as it spreads itself across more products in pursuit of a more level investment playing field.

Powered by WPeMatico

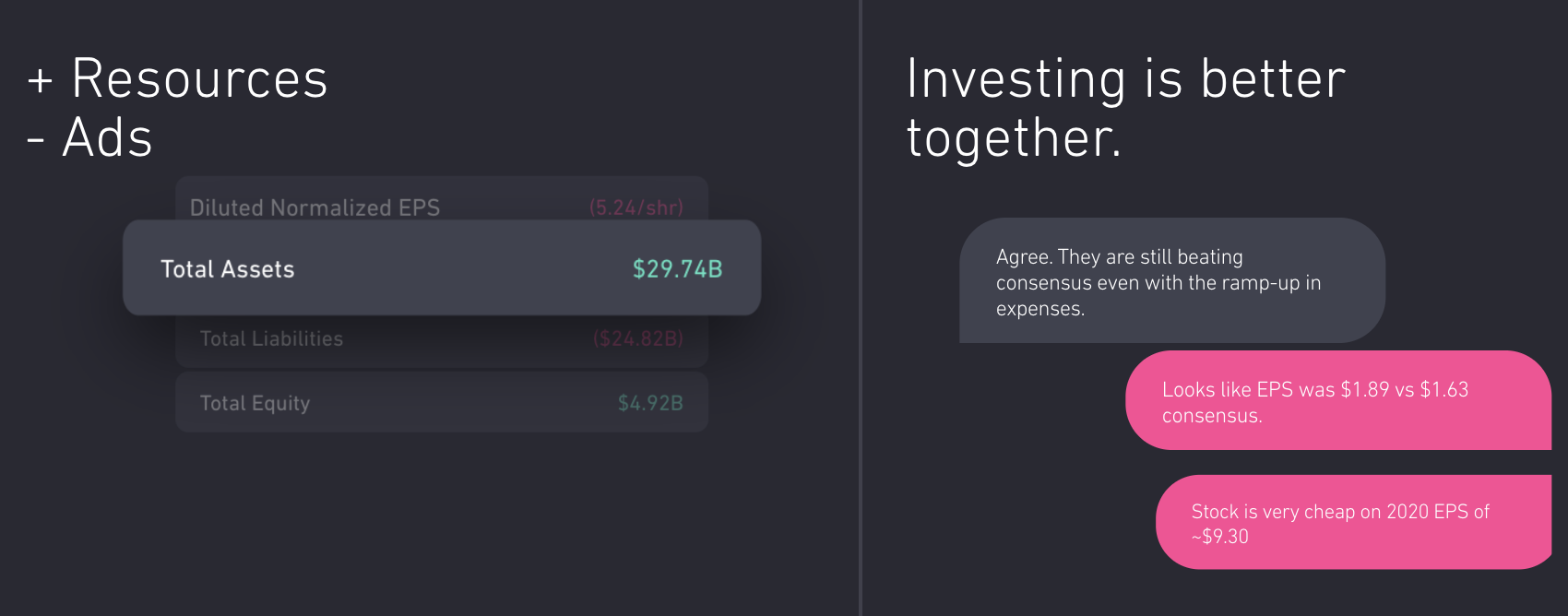

If you want to win on Wall Street, Yahoo Finance is insufficient but Bloomberg Terminal costs a whopping $24,000 per year. That’s why Atom Finance built a free tool designed to democratize access to professional investor research. If Robinhood made it cost $0 to trade stocks, Atom Finance makes it cost $0 to know which to buy.

Today Atom launches its mobile app with access to its financial modeling, portfolio tracking, news analysis, benchmarking and discussion tools. It’s the consumerization of finance, similar to what we’ve seen in enterprise SaaS. “Investment research tools are too important to the financial well-being of consumers to lack the same cycles of product innovation and accessibility that we have experienced in other verticals,” CEO Eric Shoykhet tells me.

In its first press interview, Atom Finance today revealed to TechCrunch that it has raised a $10.6 million Series A led by General Catalyst to build on its quiet $1.9 million seed round. The cash will help the startup eventually monetize by launching premium tiers with even more hardcore research tools.

Atom Finance already has 100,000 users and $400 million in assets it’s helping steer since soft-launching in June. “Atom fundamentally changes the game for how financial news media and reporting is consumed. I could not live without it,” says The Twenty Minute VC podcast founder and Atom investor Harry Stebbings.

Individual investors are already at a disadvantage compared to big firms equipped with artificial intelligence, the priciest research and legions of traders glued to the markets. Yet it’s becoming increasingly clear that investing is critical to long-term financial mobility, especially in an age of rampant student debt and automation threatening employment.

“Our mission is two-fold,” Shoykhet says. “To modernize investment research tools through an intuitive platform that’s easily accessible across all devices, while democratizing access to institutional-quality investing tools that were once only available to Wall Street professionals.”

Shoykhet saw the gap between amateur and expert research platforms firsthand as an investor at Blackstone and Governors Lane. Yet even the supposedly best-in-class software was lacking the usability we’ve come to expect from consumer mobile apps. Atom Finance claims that “for example, Bloomberg hasn’t made a significant change to its central product offering since 1982.”

The Atom Finance team

So a year ago, Shoykhet founded Atom Finance in Brooklyn to fill the void. Its web, iOS and Android apps offer five products that combine to guide users’ investing decisions without drowning them in complexity:

“Our Sandbox feature allows users to create simple financial models directly within our platform, without having to export data to a spreadsheet,” Shoykhet says. “This saves our users time and prevents them from having to manually refresh the inputs to their model when there is new information.”

Shoykhet positions Atom Finance in the middle of the market, saying, “Existing solutions are either too rudimentary for rigorous analysis (Yahoo Finance, Google Finance) or too expensive for individual investors (Bloomberg, CapIQ, Factset).”

With both its free and forthcoming paid tiers, Atom hopes to undercut Sentieo, a more AI-focused financial research platform that charges $500 to $1,000 per month and raised $19 million a year ago. Cheaper tools like BamSEC and WallMine are often limited to just pulling in earnings transcripts and filings. Robinhood has its own in-app research tools, which could make it a looming competitor or a potential acquirer for Atom Finance.

Shoykhet admits his startup will face stiff competition from well-entrenched tools like Bloomberg. “Incumbent solutions have significant brand equity with our target market, and especially with professional investors. We will have to continue iterating and deliver an unmatched user experience to gain the trust/loyalty of these users,” he says. Additionally, Atom Finance’s access to users’ sensitive data means flawless privacy, security, and accuracy will be essential.

The $12.5 million from General Catalyst, Greenoaks, Global Founders Capital, Untitled Investments, Day One Ventures and a slew of angels gives Atom runway to rev up its freemium model. Robinhood has found great success converting unpaid users to its subscription tier where they can borrow money to trade. By similarly starting out free, Atom’s eight-person team hailing from SoFi, Silver Lake, Blackstone and Citi could build a giant funnel to feed its premium tiers.

Fintech can feel dry and ruthlessly capitalistic at times. But Shoykhet insists he’s in it to equip a new generation with methods of wealth creation. “I think we’ve gone long enough without seeing real innovation in this space. We can’t be complacent with something so important. It’s crucial that we democratize access to these tools and educate consumers . . . to improve their investment well-being.”

Powered by WPeMatico

Stock trading app Robinhood is valued at $7.6 billion, but it only operates in the U.S. Freshly funded fintech startup Alpaca does the dirty work so developers worldwide can launch their own competitors to that investing unicorn. Like the Stripe of stocks, Alpaca’s API handles the banking, security and regulatory complexity, allowing other startups to quickly build brokerage apps on top for free. It has already crossed $1 billion in transactions within a year of launch.

The potential to power the backend of a new generation of fintech apps has attracted a $6 million Series A round for Alpaca led by Spark Capital . Instead of charging developers, Alpaca earns its money through payment for order flow, interest on cash deposits and margin lending, much like Robinhood.

“I want to make sure that people even outside the U.S. have access” to a way of building wealth that’s historically only “available to rich people” Alpaca co-founder and CEO Yoshi Yokokawa tells me.

Alpaca co-founder and CEO Yoshi Yokokawa

Hailing from Japan, Yokokawa followed his friends into the investment banking industry, where he worked at Lehman Brothers until its collapse. After his grandmother got sick, he moved into day-trading for three years and realized “all the broker dealer business tools were pretty bad.” But when he heard of Robinhood in 2013 and saw it actually catering to users’ needs, he thought, “I need to be involved in this new transformation” of fintech.

Yokokawa ended up first building a business selling deep learning AI to banks and trading firms in the foreign exchange market. Watching clients struggle to quickly integrate new technology revealed the lack of available developer tools. By 2017, he was pivoting the business and applying for FINRA approval. Alpaca launched in late 2018, letting developers paste in code to let their users buy and sell securities.

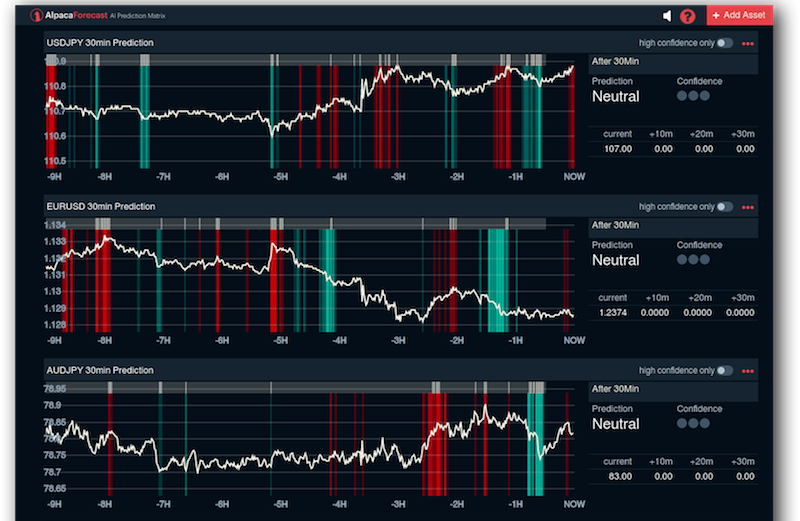

Now international developers and small hedge funds are building atop the Alpaca API so they don’t have to reinvent the underlying infrastructure themselves right away. Alpaca works with clearing broker NTC, and then marks up margin trading while earning interest and payment for order flow. It also offers products like AlpacaForecast, with short-term predictions of stock prices, AlpacaRadar for detecting price swings and its MarketStore financial database server.

AlpacaForecast

The $6 million from Spark Capital, Social Leverage, Portag3, Fathom Capital and Zillionize adds to $5.8 million in previous funding from investors, including Y Combinator. The startup plans to spend the cash on hiring to handle partnerships with bigger businesses, supporting its developer community and ensuring compliance.

One major question is whether fintech businesses that start to grow atop Alpaca and drive its revenues will try to declare independence and later invest in their own technology stack. There’s the additional risk of a security breach that might scare away clients.

Alpaca’s top competitor, Interactive Brokers, offers trading APIs, but other services as well that distract it from fostering a robust developer community, Yokokawa tells me. Alpaca focuses on providing great documentation, open-source contribution and SDKs in different languages that make it more developer-friendly. It will also have to watch out for other fintech services startups like DriveWealth and well-funded Galileo.

There’s a big opportunity to capitalize on the race to integrate stock trading into other finance apps to drive stickiness because it’s a consistent, voluntary behavior rather than a chore or something only done a few times a year. Lender SoFi and point-of-sale system Square both recently became broker dealers as well, and Yokokawa predicts more and more apps will push into the space.

Why would we need so many stock trading apps? “Every single person is involved with money, so the market is huge. Instead of one-player takes all, there will be different players that can all do well,” Yokokawa tells me. “Like banks and investment banks co-exist, it will never be that Bank of America takes 80% of the pie. I think differentiation will be on customer acquisition, and operations management efficiency.”

The co-founder’s biggest concern is keeping up with all the new opportunities in financial services, from cash management and cryptocurrency that Robinhood already deals in, to security token offerings and fractional investing. Yokokawa says, “I need to make sure I’m on top of everything and that we’re executing with the right timing so we don’t lose.”

The CEO hopes that Alpaca will one day power broader access to the U.S. stock market back in Japan, noting that if a modern nation still lags behind in fintech, the rest of the world surely fares even worse. “I want to connect this asset class to as many people as possible on the earth.”

Powered by WPeMatico

This time it actually has insurance. Zero-fee stock-trading app Robinhood is launching Cash Management, a new feature that earns users 2.05% APY interest on uninvested money in their account with the ability to spend it through a special Mastercard debit card. The waitlist opens today in the U.S. with the first users to be admitted soon. “If you have $5,000 in your account while you’re thinking about what to invest in, you’d have an extra $105 at the end of the year” thanks to Robinhood Cash Management’s interest, co-CEO Baiju Bhatt tells me.

The $7.6 billion-valuation startup first attempted something similar in December with Robinhood Checking, promising a stunningly tall 3% interest rate. But the product turned into a PR disaster when the Securities Investor Protection Corporation that was supposed to insure users’ funds declared Robinhood ineligible, with its CEO noting it had never agreed to cover checking accounts. That led Robinhood to shelve the feature, scrub its site of any mention of Checking and apologize.

Robinhood Cash Management’s debit cards, featuring the same design from the scrapped Checking launch

Now despite Bhatt claiming “Cash Management is a brand new program built from the ground up,” it will offer the same debit card design and network of 75,000 ATMs. It’s even using an identical promo image for its half-translucent green, black, white and American flag debit card designs. But each user’s funds will be covered by the Federal Deposit Insurance Corporation up to $1.25 million. To get around the $250,000 FDIC limit per bank, Robinhood is partnering with six banks that it will spread a user’s cash across as necessary to bundle up to that sum. Robinhood earns money by taking a chunk of the interchange fees from transactions on its debit card run in partnership with Sutton Bank, and from a fee paid by the six banks cash gets swept into.

To help it avoid further regulatory missteps, Robinhood yesterday added former SEC commissioner Dan Gallagher as its first independent board member. He joins the startup’s recently hired COO, CFO, chief compliance officer, VP of Risk & Compliance and VP of Legal & Regulatory to bring more supervision to Robinhood.

Robinhood co-founders and co-CEOs (from left): Baiju Bhatt and Vlad Tenev

The opt-in feature prevents users from missing out on earning interest if they keep money in their Robinhood account, and makes funds from stock sales quickly accessible via the debit card for spending or withdrawal. That convenience could give Robinhood an edge as its loses one if its key differentiators. Last week, its top incumbent competitors Charles Schwab, E*Trade and AmeriTrade all dropped their $4.95 to $6.95 fees on stock trades to match Robinhood’s free offering. That makes Cash Management and Robinhood Crypto even more critical to its continued growth. That’s necessary to justify the $7.6 billion valuation from its recent $323 million Series E raise led by DST Global that brings it to $860 million in total funding.

“We decided the best thing to do is giving people the peace of mind that their money is held at these banks, while trying to pay back the very best interest rates,” Bhatt tells me. [Disclosure: I know Robinhood’s co-founders from college.]

With Cash Management, once users deposit cash into the Robinhood accounts and opt into the program, they’re eligible to earn interest. Any balance on their account, including returns from sales of securities or cryptocurrencies, is swept into the FDIC-insured partner banks via Promontory’s debit suite system. Those banks include Wells Fargo, HSBC, Goldman Sachs, Citibank, U.S. Bank and Bank of Baroda. If one of those banks folds, the FDIC will make customers whole for up to $250,000, equaling $1.25 million across all six working with Robinhood. Users are able to opt out of specific banks.

There the cash earns a variable annual percentage yield (APY) that may fluctuate based on market factors like the Fed fund’s rate. Currently Robinhood offers a 2.05% APY, but refused to compare it to competitors. However, it ranks relatively high amongst popular banking options like these, according to Bankrate, especially given it has no minimum balance:

Robinhood Cash Management will also compete directly with Wealthfront Cash that launched in February and now offers 2.07% APY interest, but lacks a debit card or ATMs. Betterment Checking & Savings does provide a Visa debit card, but its current APY is 1.79%.

Cash Management users can select from the four debit card styles that are accepted anywhere that takes Mastercard, plus 75,000 ATMs. It also works with Apple Pay, Google Pay and Samsung Pay. There are no foreign transaction fees, maintenance fees or account minimum.

A variety of new Cash Management features are being added to the Robinhood app. You can get notifications and emails for all your transactions, and lock the card from your phone if you suspect fraud. You also can opt for location protection, which alerts you if your card is used too far away from your phone. An in-app ATM finder shows users where they can get cash without a fee.

“Partially we want this to be a good business but we also want this to be a big part of customer’s lives,” says Robinhood VP of product Josh Elman. Instead of nickel and diming Cash Management users, the startup monetizes by charging its partners. But the bigger strategy is to get more users on Robinhood in hopes some will subscribe to Robinhood Gold. There users pay a variable monthly fee depending on how much they want to borrow from the startup to trade on margin.

Robinhood co-CEO Baiju Bhatt speaks with TechCrunch’s Josh Constine at Disrupt SF 2018

“I think the main takeaway over the last year has been that since last December, our company has been very committed to building an organization that has a really strong culture [of compliance]” Bhatt concludes. “We’ve grown the leadership team over the last year with experience from risk and finance backgrounds. We think that’s reflected pretty clearly in how Robinhood operates and the diligence that went into building this new program.”

No longer a scrappy startup, the budding fintech giant must now grapple with much greater regulatory scrutiny. With more than 6 million users, the SEC won’t stand for it putting people’s finances in in jeopardy.

Powered by WPeMatico

Robinhood may be best known for its free stock trading, but today it’s rolling out a new version of the newsfeed, adding content from Reuters, Barron’s and market coverage from The Wall Street Journal, with no paywall or additional charge.

In addition, Robinhood is introducing video into the newsfeed, with ad-free videos from CNN Business, Cheddar and (again) Reuters.

The startup, which recently raised $323 million at a $7.6 billion valuation, has been showing more interest in content lately with the acquisition of the financial podcast and newsletter MarketSnacks — and as part of the redesign, the newsletter (now called Snacks) can be read directly in the app.

“A lot of this is not even about making investment decisions,” Robinhood’s vice president of Product Josh Elman told me. “[Some users] check Robinhood very, very often just to consume the news and understand the companies that they’re watching, the ones that they are invested in and continuing to hold.”

He added that just buying and selling stocks is “sort of a utility,” so Robinhood wants to help its users “to feel informed, to be empowered to make their own decisions.”

Before redesigning the newsfeed, Elman said the team did a seven-day study, where they asked subjects to create a diary of “all of their experiences reading and understanding market news.”

Among other things, Elman’s team learned that people “really want to read news from multiple, trusted sources,” which is why Robinhood is partnering with these publications. In addition, they saw that people like watching videos: “Even if it’s in the background, ultimately, people really told us they feel more confident and control in their decisions.”

Along with bringing in new content (which, again, is taken out from behind paywalls and is ad-free), Elman said the Robinhood newsfeed also features “all-new algorithms and a whole new display layer.” Robinhood users can see the new interface for themselves, but I was curious about those algorithms.

“We start with the companies you either own and hold in your portfolio or are watching, what types of sources do you frequently like to watch … and we make sure that we’re bringing you that news as much as possible,” Elman said. “And we have a lot of room to grow from here.”

Powered by WPeMatico

The biggest players in online stock trading all just copied Robinhood by removing their fees for stock and ETF trading. Charles Schwab announced yesterday it would drop its $4.95 fee, leading to plummeting share prices for it as well as competitors. By the end of yesterday, Ameritrade announced it too would axe its $6.95 fees, and then E*Trade followed suit this morning killing off its own $6.95 fee. However, none of their share price recovered.

From yesterday before Schwab’s announcement through now, Schwab fell 12%, from $41.84 to $36.54; E*Trade fell 19%, from $43.69 to $35.20; and Ameritrade fell 28%, from $46.70 to $33.54. Clearly investors aren’t thrilled that these financial giants are bowing to pressure from a measly startup.

Yet the move could definitely hurt growth for the $7.6 billion-valued fintech upstart Robinhood. It has relied on the free stock trades to pull in users that it then monetizes with its Robinhood Gold subscription to premium services, including the ability to trade on margin by temporarily borrowing money from the company.

Schwab drops its fees

“The changes taking place across the brokerage industry reflect a focus on the customer that‘s been inherent to Robinhood since the beginning,” said a spokesperson for the startup. “We remain focused on offering intuitively designed products that reduce barriers to our financial system, including account minimums and commission fees.”

Robinhood was hoping a high 3% interest rate checking account feature announced in December might help differentiate it from online stock brokerages. But after it prematurely launched the checking product without proper insurance, massive backlash ensued and the company announced it would shelve and rethink the idea. But that hiccup didn’t stop it from raising another $323 million this July to bring its total raised to $862 million. Its young user base and cryptocurrency exchange could give it potential that aged trading platforms lack.

![]()

Powered by WPeMatico

Investment and stock trading app Robinhood stored some user credentials, including passwords, in plaintext on internal systems, the company revealed today. This particularly dangerous security misstep could have seriously exposed its users, though it says that it has no evidence the data was accessed improperly. Better change your password now.

Sensitive data like passwords and personal information are generally kept encrypted at all times. That way if the worst came to pass and a company’s databases were exposed, all the attacker would get is a bunch of gibberish. Unfortunately it seems that there might have been a few exceptions to that rule.

A number of users, including CNET’s Justin Cauchon, received the following notice from Robinhood in an email:

When you set a password for your Robinhood account, we use an industry-standard process that prevents anyone at our company from reading it. On Monday night, we discovered that some user credentials were stored in a readable format within our internal systems. We wanted to let you know that your password may have been included.

We resolved this issue, and after thorough review, found no evidence that this information was accessed by anyone outside of our response team.

It seems that if it were truly “industry-standard,” then the rest of the industry would also have stored passwords in plaintext. Come to think of it, that would explain a lot, since Google, Facebook, Twitter, and others have all managed to make this same mistake recently.

A Robinhood representative stressed the rapidity of the company’s response to the issue, though they would not comment on how it was first discovered, nor how long the data was stored that way, nor what deviation from these industry norms caused the problem, nor how many users were affected, nor whether answers to these questions would ever be forthcoming. They did offer the following statement:

We swiftly resolved this information logging issue. After a thorough review, we found no evidence that this customer information was accessed by anyone outside of our response team. Out of an abundance of caution, we have notified customers who may have been impacted and encouraged them to reset their passwords. We take our responsibility to customers seriously and place an immense focus on working to ensure their information is secure.

If you got an email, you were among the unlucky few many majority handful some, so change your password. If you didn’t get an email… also change your password. You can never be too careful.

Powered by WPeMatico

Robinhood, the U.S.-based “zero-fee” stock-trading app and cryptocurrency exchange, is stealthily recruiting for a new London office ahead of plans to eventually launch in the U.K., TechCrunch has learned.

According to sources within London’s thriving fintech industry, Robinhood is hiring for multiple U.K. positions. These span recruitment, operations, marketing/PR and customer support. Notably, the company is also seeking people in compliance and product, including product design.

In other words, significant localisation and local product market fit appears to be the intention. Compliance is also an important part of Robinhood’s future U.K. regulatory requirements as it applies to local regulator the FCA for the appropriate licenses. Robinhood declined to comment on its U.K. plans.

Meanwhile, news that Robinhood is stealthily recruiting ahead of a planned U.K. launch is interesting in the context of local fintech startups that have launched or announced their own fee-free trading offerings.

Launched late last year, London-based Freetrade has built a bona-fide “challenger broker,” including obtaining the required license from the FCA, rather than simply partnering with an established broker. The app lets you invest in U.K. stocks and ETFs, but will soon add U.S. stocks, too. Trades are “fee-free” if you are happy for your buy or sell trades to execute at the close of business each day. If you want to execute immediately, the startup charges a low £1 per trade.

In June last year, Revolut, also headquartered in London, announced its intention to add commission-free trading to its banking app, in what was seen as a bid to compete with Robinhood. So far, no product has surfaced, although I’m told we should see trading added to Revolut in Q1 this year.

What’s intriguing about the Revolut-Robinhood comparisons is that the two companies share a number of investors, namely Index and DST. Both companies have incredibly high valuations, too, and, depending on respective burn rates, quite deep pockets.

Co-founded by Baiju Bhatt and Vlad Tenev (pictured above), Robinhood claims 6 million accounts and is valued at $5.6 billion, having raised a total to date of $539 million. It has around 300 employees across its HQ in Menlo Park, California and its regional HQ in Lake Mary, Florida.

Revolut claims 3.5 million users, and at its last funding round was valued at $1.7 billion. The fintech has raised a total of $340 million, and has a headcount of 600 in London and across its various regional offices.

Powered by WPeMatico

Robinhood is undercutting the big banks by forgoing brick-and-mortar branches with its new zero-fee checking and savings account features. With no overdraft or monthly fees, a juicy 3 percent interest rate and a claim of more U.S. ATMs than the five biggest banks combined, Robinhood is using the scalability of software to pass impressive perks on to customers. The free stock trading app already used that approach to attack brokers like E*Trade and Charles Schwab that charge a per-trade fee. Now it’s breaking into the larger financial services market with a model that could put the squeeze on Wells Fargo, Chase and Bank of America.

Today Robinhood launches checking and savings accounts in the U.S. with a Mastercard debit card issued through Sutton Bank that starts shipping December 18th. Users earn 3 percent on all the dough they keep with Robinhood, yet there’s no minimum balance or fees for monthly membership, overdrafts, foreign transactions or card replacements. That’s a pretty sweet deal compared to the other leading banks that all charge for some of that or offer much lower interest rates. The trade-off is that while customers get 24/7 live text chat support, they won’t be able to walk into a local bank branch. Users who want early access can sign up here.

Robinhood expects to turn a profit thanks to a lean 300-employee operation, earning a margin on investing your money in U.S. treasuries and a revenue share with Mastercard on interchange fees charged to merchants when you swipe. The launch could be critical to keeping Robinhood worthy of its $5.6 billion valuation from when it took a $363 million Series D in March just a year after raising at a $1.3 billion valuation. The 6 million-user app invested in launching a free cryptocurrency trading exchange early this year only to see coin prices plummet and mainstream interest fall off. But with banks hammering users with surprise fees and mediocre user experience, there’s a huge opportunity for a mobile-first startup to disrupt how we store money.

“Brick-and-mortar locations are costly. Our goal with this product was to build a completely digital experience so we can reduce our overhead so we can pass more of the value back to customers,” Robinhood co-CEO Baiju Bhatt tells me. [Disclosure: I know Bhatt and co-CEO Vlad Tenev from college.] “Saving accounts in the U.S. pay on average 0.09 percent and we all know the banks are making far more than that from the deposits. With Robinhood you earn 3 percent off all of your money. Mental math is hard, so if you look at the median U.S. household that has about $8,000 in liquid savings, they’d earn $240 a year.”

Robinhood will be sending invites to users in January for the new feature that they can use exclusively or alongside their existing bank. Anyone approved to use Robinhood’s stock brokerage is eligible, but users can also sign up directly for checking and savings with no obligation to trade stocks. Robinhood claims signing up won’t impact your credit score. Users get to customize a Robinhood-branded debit card that’s accepted wherever Mastercard is. Because the feature is run within Robinhood’s brokerage, it’s ensured by the SIPC instead of the FDIC, but you still get the same insurance on up to $250,000 cash.

One of the most appealing features of Robinhood checking and savings is getting access to 75,000 free-to-use ATMs in places like Target, Walgreens and 7-Eleven. Users won’t be able to tell just by looking at an ATM whether it’s in the network, but the Robinhood app features a map for finding the nearest one. You can deposit checks via Robinhood’s app too, and if you need to send a check, you can just tell the startup how much to deliver to whom and it will mail the check for you.

“These fees like overdraft fees — they’re not fees millionaires are paying. It’s ordinary folks paying. It’s actually more expensive for those that have less money and it’s cheaper for those that have more money. We think that isn’t right and we think that’s bad business,” Bhatt gripes. Because Robinhood built its own clearing house for moving money, and it lacks the overhead of traditional banks, it’s able to save enough money to make its no-fee structure work. “We want to build a financial services company that democratizes America’s financial system.”

Robinhood will have to convince users it’s worthy of their trust, as a security breach could be disastrous. There’s also the question of whether people are ready to ditch their bank branch. “Behaviors about and going into a branch are definitely changing,” says Bhatt. My biggest concern was not having any consistency in who I talk to when I need banking help. Bhatt tells me the company plans to roll out more personalized customer service features in the coming months, but there may always be edge cases that make the lack of in-person support annoying.

Getting into banking could open a lucrative revenue stream for Robinhood as it charts its path to IPO. The startup recently hired Jason Warnick, a 20-year veteran of Amazon, to be its CFO and get it prepped to go public. Wall Street will want to see a more robust business that’s not as vulnerable to foes like stock brokerage Charles Schwab, which is already lowering fees to stay competitive with Robinhood. Not only will checking and savings see users move more money into their Robinhood accounts that it can invest to earn a profit, but it also poises the startup to tackle more financial services in the future. More lucrative products like loans could make paying 3 percent much easier for Robinhood to handle.

Powered by WPeMatico