payments

Auto Added by WPeMatico

Auto Added by WPeMatico

Facebook provided TechCrunch with new information on how its cryptocurrency will stay legal amidst allegations from President Trump that Libra could facilitate “unlawful behavior.” Facebook and Libra Association executives tell me they expect Libra will incur sales tax and capital gains taxes. They confirmed that Facebook is also in talks with local convenience stores and money exchanges to ensure anti-laundering checks are applied when people cash-in or cash-out Libra for traditional currency, and to let you use a QR code to buy or sell Libra in person.

A Facebook spokesperson said the company wouldn’t respond directly to Trump’s tweets, but noted that the Libra association won’t interact with consumers or operate as a bank, and that Libra is meant to be a complement to the existing financial system.

Trump had tweeted that “Unregulated Crypto Assets can facilitate unlawful behavior, including drug trade and other illegal activity. Similarly, Facebook Libra’s ‘virtual currency’ will have little standing or dependability. If Facebook and other companies want to become a bank, they must seek a new Banking Charter and become subject to all Banking Regulations, just like other Banks, both National and International.”

For a primer on how Libra works, watch our explainer video below or read our deep dive into everything you need to know:

In a wide-reaching series of interviews this week, the Libra Association’s head of policy Dante Disparte, Facebook’s head economist for blockchain Christian Catalini and Facebook’s blockchain project subsidiary Calibra’s VP of product Kevin Weil answered questions about regulation of Libra. Here’s what we’ve learned (their answers were trimmed for clarity but not edited):

Calibra’s Kevin Weil: We believe that creating a financial ecosystem that has significantly broader access where all it takes is a phone and lower transaction fees across the board is good for people. And we want to bring it to as many people around the world as we can. But as a custodial wallet we are regulated and will be compliant and we will only operate in markets where we’re allowed.

We want that to be as many markets as possible. That’s why we announced well in advance of actually launching a product — because we’ve been engaging with regulators. We’re continuing to engage with regulators and we can help them understand the effort that we’re taking to make sure that people are safe and also the value that accrues to the people in their countries when there’s broader access to financial services with lower transaction fees across the board.

TechCrunch: But what if you’re banned in the U.S.?

Weil: I’m hesitant to give a blanket answer. But in general, we believe that Libra is positive for people and we want to launch as broadly as possible. The world where the U.S. does that I think would probably cause other regulatory regimes to also be concerned about it. I think that’s very much a bridge that we’ll cross when we get there. But so far we’re having frank, open and honest discussions with regulators. Obviously, that continues next week with David’s testimony. And I hope it doesn’t come to that, because I think that Libra can do a lot of good for a lot of people.

TechCrunch’s Analysis: The U.S. House subcommittee has already submitted a letter to Facebook requesting that it cease development of Libra and Calibra until regulators can better examine it and take action. It sounds like Facebook believes a U.S. ban on Libra/Calibra would cause a domino effect in other top markets, and therefore make it tough to rationalize still launching. That puts even more pressure on the outcome of July 16th and 17th’s congressional hearings on Libra with the head of Facebook’s head of Calibra, David Marcus.

We already know that Facebook’s own Libra wallet called Calibra will be baked into Messenger and WhatsApp plus have its own standalone app. There, those with connected bank accounts and government ID that go through a Know Your Customer (KYC) anti-fraud/laundering check will be able to buy and sell Libra. But a big goal of Libra is to bring the unbanked into the modern financial system. How does that work?

Weil: Because Libra is an open ecosystem, any money exchange business or entrepreneur can begin supporting cash-in/cash-out without needing any permission from anyone associated with the Libra Association or member of the Libra Association. They can just do it. Today in a lot of emerging markets [there’s a service for matching you with someone to exchange cryptocurrency for cash or vice-versa called] LocalBitcoins.com and I think you’ll see that with Libra too.

Second, we can augment that by by working with local exchanges, convenience stores and other cash-in/cash-out providers to make it easy from within Calibra. You could imagine an experience in the Calibra app or within Messenger or WhatsApp, where if you want to cash in or cash out, you’ll pop up a map that highlights physical locations around that allow you to do it. You select one that’s nearby, you select an amount, and you get a QR code that you can take to them and complete the transaction.

I’d imagine that most of these businesses that we work with will support Libra more broadly, so even if we get these deals started it will benefit the whole ecosystem and every Libra wallet, not just Calibra.

TechCrunch: Have you struck relationships with any convenience store operators or money exchangers like Western Union or MoneyGram, or Walgreens, CVS or 7-Eleven? Are you in talks with them yet?

Weil: I probably shouldn’t comment on any specific deals but we’re in conversation with a lot of the folks you might think, because ultimately being able to move between Libra and your local currency is critical to driving adoption and utility in the early days . . . If you’re banked there are easier ways to do that. If you’re not banked and you’re in cash — those are the people we really want to serve with Libra — we’re working very hard to make that process easy for people.

TechCrunch’s analysis: This approach will let Calibra largely avoid the complicated and potentially error-prone process of KYCing people in person or handing out cash by offloading the responsibility and liability to other parties.

Weil: There are very important populations that don’t have an ID. People in a refugee camp may not, as an example, and we want Libra to serve them. So this is one example of many of why it’s important that Calibra isn’t the only option for people who want to participate in the Libra ecosystem . . . Others of these will be run by local providers and they have programs to meet customers face-to-face and other ways to serve people and even KYC them that we may not . . . We’re not going be the only wallet, we don’t want to be the only wallet.

This is one of the reasons NGOs have been members of the Libra association from the start, because we want to encourage the monetization of identity processes both through working with governments issuing credentials for more people and also making use of new types of information for identity and authentication. We hope this process will hep the last mile problem.

In the case of a non-custodial wallet, the user isn’t trusting anyone. The way the regulations have worked and this is evolving as we speak. The on-ramps and off-ramps to the crypto world are regulated and they have direct customer relationships and it’s their responsibility to KYC people. In our case we’ll be a custodial wallet and we’ll KYC people. There are a number of wallets in the Bitcoin or Ethereum ecosystem — non-custodial wallets that don’t have a direct relationships with the users. . . They have to get that Bitcoin somehow. Usually they’re going through an exchange where usually as part of the process they’re KYC’d.

In a lot of emerging markets you have LocalBitcoins.com where you can find a representative or agent who will meet you in person and exchange cash for bitcoin in whatever market you have to be in. And I believe that they just started making sure that they KYC everyone, but they’re doing it in person. And they have more flexibility in how they do it than you might otherwise. I think there are lots of ways that this will happen and the fact that Libra is an open ecosystem will enable people to be entrepreneurial about it.

There are lots an lots of people who are underserved by today’s financial ecosystem who have government ID. So even with requiring everyone go through a KYC process, we’ll be able to serve many, many people who are not well-served by today’s financial ecosystem. We want to find ways to support people who can’t KYC and the important part is that Calibra will fully interoperate with any other wallet, including ones that people in local markets are using because it’s a better fit for their needs.

TechCrunch: Through that interoperability, if someone with a non-custodial wallet receives Libra and then sends it a Calibra wallet user, does that mean you Libra coming into Calibra from users who weren’t KYC’d and could be laundering money?

Weil: So it’s part of the regulatory situation that’s evolving as we speak. There’s something called the Travel Rule . . . If there’s a transfer above a certain value you have to make sure that you understand both who the sender is, which you do if they’re using a custodial wallet, and who the receiver is. These are evolving regulations, but it’s something that obviously we’re going to make sure that we implement as regulations solidify.

TechCrunch’s Analysis: Calibra appears to be inviting regulation that it can strictly abide by rather than trying to guess at what the best approach is. But given it’s unclear when concrete rules will be established for transfers between non-custodial wallets and custodial wallets, or for in-person cashing, Facebook and Calibra may need to establish their own strong protocols. Otherwise they could be guilty of permitting the “unlawful behavior” Trump describes.

Dante Disparte of Libra: Taxing of digital assets is something that’s being designed at the local level and at the jurisdiction level. Our view of the world is that like with any form of money or any form of payment or banking, the onus in terms of compliance with tax is with the individual user and consumer, and the same would hold true broadly here.

We expect that the many, many wallets and financial services providers building solutions on the Libra blockchain would begin to provide tools that make it much easier than it is today [to calculate and file taxes] for digital assets and cryptocurrencies more generally . . . There’s plenty of time between now and Libra hitting the market to begin defining this more strictly at the jurisdictional level among providers.

TechCrunch’s Analysis: Again, here Facebook, Calibra and the Libra Association are hoping to avoid shouldering all the responsibility for taxes. Their position is that just as you have to take the initiative of paying your taxes whether or not you use a Visa card or your bank’s checks to transact, it’s on you to pay your Libra taxes.

TechCrunch: Do you think in the United States that it’s reasonable for the government to ask that Libra transactions be taxed?

Disparte: Tax treatments of digital assets broadly hasn’t been entirely clarified in most places around the world. And we hope that this is something that this project and the ecosystem around it helps to clarify.

Tax authorities will see a benefit from Libra at the consumption level and at the household level, while some cryptocurrencies have avoided taxes until the point they tried to cash out. But the nature of it and the lack of speculation and its design we think should give it a light tax treatment the way you would find with traditional currencies.

Christian Catalini of Facebook: Cryptocurrencies are taxed right now every time you have a sale on the differences in gains and losses. Because Libra is designed to be a medium of exchange, those gains and losses are likely to be very tiny relative to your local currency . . . Sales tax would likely be implemented the exact same way on Libra as it is today when you pay with a credit card.

At launch giving current regulations, the Calibra wallet will have to track every purchase and sale of Libra for a U.S. user and those differences will have to be reported on tax day. You can think of the losses, albeit they may be very small gains and losses relative to USD, as similar to the what people do today when they have a Coinbase account with Bitcoin.

The sales tax I think could be implemented in the exact same way as it today with any other sort of digital payment, it would be no different. If you’re buying goods or services with Libra you’ll be paying sales tax the same way as if you used a different form of payment. Like today when you see a percentage, that is the sales tax on your total.

Disparte: Maybe the best way to frame how taxes work all over the world is that it’s not up to Libra, Calibra, Facebook or any company to make that determination. It’s up to regulators and authorities.

TechCrunch: Does Calibra already have plans in place for how to handle sales tax?

Weil: That’s also a pretty rapidly evolving part of the regulatory ecosystem right now. It’s really an ongoing discussion. We will do whatever the regulation says we need to do.

TechCrunch’s Analysis: Here we have the firmest answers of our interviews. Facebook, Calibra and the Libra Association believe the proper approach to taxes is that Libra transactions carry a country’s traditional sales tax, and that Libra you hold in your wallet will have to pay taxes based on the Libra stablecoin’s value (that’s pegged to a basket of international currencies) relative to the U.S. dollar.

If the Libra Association recommends all wallets and transactions follow these rules and Calibra builds in protocols to handle these taxes simply, at least the government can’t argue Libra is a method of dodging taxes and everyone paying their fair share.

Powered by WPeMatico

HQ Trivia’s troubles continue after a failed mutiny to oust the CEO, a 92% decline in downloads since versus a year ago, and layoffs of 20% of its staff last week. Now TechCrunch has learned HQ has failed to install a new CEO after months of searching. Meanwhile, users continue to complain about delays for payouts of their prizes from the live mobile trivia game, and about being booted from the game for no reason while on the final question.

Notably, Jeopardy winner Alex Jacob claims he hasn’t been paid the $20,000 he won on HQ Trivia on June 10th. This could shake players faith in HQ and erode their incentive to compete.

Guys, I need your help. I won $20,000 on @hqtrivia on June 10 and still haven’t heard anything about payment. Sadly, I don’t think they’re going to pay.

Please RT to tell HQ they should honor their jackpots. If I’m wrong, I’ll happily delete this & give $100 to someone who RT’d! pic.twitter.com/FmpY6unK49

— Alex Jacob (@whoisalexjacob) July 8, 2019

An HQ Trivia representative tells TechCrunch that the game has paid out $6.25 million to date and that 99% of players have been eligible to cash out within 48 hours of winning, but some winners may have to wait up to 90 days for it to ensure they didn’t break the rules to win. Given Jacob’s large jackpot, it’s possible the delay could be due to the company investigating to ensure he won fairly, though he’s clearly skilled at trivia given he won Jeopardy’s Tournament Of Champions in 2015. Jacob did not respond to requests for interview.

“We strive to make a game that is fair and fun for all players. As such, we have a rigorous process of reviewing winners for eligibility to receive cash prizes. Infrequently, we disqualify players for violating HQ‘s Terms of Service and Contest Rules” HQ Trivia’s press alias anonymously reponded to our request for comment. “It may take some eligible winners up to 90 days to receive cash prizes, however 99% of players have been able to cash out within 48 hours of winning a game and we have paid out a total of $6,252,634.58 USD to winners since launch.”

It seems that HQ’s internal problems are now metastasizing into public issues. Its team being short-staffed and distracted by weak morale could lengthen payout delays, which make players worry if they’ll ever get their cash. When they share those sentiments to social media, it could discourage others from playing. That, combined with concerns that bots and cheaters are winning the games, splitting the jackpots into tiny fractions so legitimate winners get less, has hurt the perception of HQ as a game where the smartest can win big.

Back in April, TechCrunch reported that 20 of HQ’s 35 staffers were preparing a petition to the board to remove CEO and co-founder Rus Yusupov for mismanagement. Yusupov caught wind of the plot and fired two of the leaders of the movement. However, HQ’s board decided it would bring in a new CEO. Board member and Tinder CEO Elie Seidman told TechCrunch that Yusupov had accepted he would be replaced by someone with the ability fire him and that a CEO search was ongoing. The startup’s lead investor Lightspeed has pledged to provide 18 months of funding once a new CEO was hired.

However, multiple sources tell TechCrunch that a new CEO has yet to be installed. One source tells me that management had promised a new CEO by the beginning of August, but that Yusupov had stalled the process seemingly to remain in power. HQ Trivia, Yusupov, and Seidman did not respond for requests for comment regarding the CEO search.

When asked about morale at the company, a source familiar with HQ’s internal situation told me “It’s terrible.” Yusupov is said to continue to be tough to work with, making decisions without full buy-in from the rest of the company. A substantial portion of the team was allegedly unaware of plans to launch a $9.99 subscription tier for HQ’s second game HQ Words until the company tweeted out the announcement.

Hopefully HQ Trivia can find a new captain to steer this ship back into smoother waters. The game has hundreds of thousands of players and many more with fond memories of competing. There’s still hope if it can evolve the product to give new users a taste of gameplay without waiting for the next scheduled match, find new revenue in expanded brand partnerships, fight off the bots and cheaters, and get everyone paid promptly. Perhaps there’s room for television tie-ins to bring HQ to a wider audience.

But before the startup can keep quizzing the world, HQ Trivia must endure its internal tests of resolve and find a champ to lead it.

Powered by WPeMatico

The new era of tech-enabled banks is coming, even in regulation-heavy Japan. Kyash, a fintech company with visions on becoming Japan’s first challenger bank, said today it has raised $14 million to continue its expansion.

To be clear, Kyash isn’t a bank. Yet. But it is currently applying for a host of licenses in Japan that could allow it to offer banking-style features, including checking accounts, ATM withdrawals and money remittance. Right now, it is a payment app that offers a connected Visa card in the style of Monzo, N26, Revolut (which has a Japan license) and others of that ilk.

The startup was founded in 2015 by Shinichi Takatori, a former banker and management consultant who saw the potential to merge tech and finance.

“I really noticed that information and communication has become ubiquitous but money itself hasn’t changed for a long time,” Takatori told TechCrunch in an interview.

The company took some time — two years — before it released a consumer product, but it quickly tied up with Visa to offer a prepaid debit card that connects to the Kyash app. That provides benefits like instant payment notifications, clear balance and lower fees for overseas spending, while costs are borne by merchants rather than users. They might seem elementary today, but they are still not standard among Japan’s traditional banks, Takatori explained.

The company declined to share its user numbers, but Takatori said this new round of funding — Kyash’s Series B — is a validation of the progress it has made.

The $14 million investment is co-led by Goodwater Capital, a U.S. investor that has backed fintech startups like Monzo, Stash and Toss in Korea, and Mitsubishi UFJ Capital, the investment arm of Japan’s largest bank.

Mitsubishi’s involvement means that Kyash counts Japan’s three largest banks as investors, with SMBC and Mizuho having previously put money into the company. Others that took part in this Series B include Toppan Printing, JAFCO and Shinsei Corporate Investment Limited.

So many banks on the cap table might seem like a strange thing for a disruptor — let alone the banks, which tend to behave territorially — but Takatori believes that there’s the potential for cooperation, not to mention that it will help the startup with its licensing efforts. Already, he revealed, Mitsubishi plans to integrate its card with the Kyash app to provide its customers with the best of both worlds.

“We’re not here to win over existing banks, but instead inform [them of] how money should work in next decade,” explained Takatori. “So why not collaborate in some way.”

Kyash has a tie-up with Visa that allows it to offer its customers a connected debit card and also provide issuing services to other fintech startups

There’s also the fact that, even with a license, Kyash and others are unlikely to be able to offer full banking services. That means they will have to serve as complementary offerings to the industry, which would likely mean that cooperation is good — essential — for both sides.

But, beyond the consumer play, a notable piece of Kyash’s business that has investors excited is its B2B payment business.

The company developed its own payment processing system to reduce costs, which is one reason it took time to launch. Thanks to a tie-up with Visa, it offers both issuing and processing of prepaid Visa cards to fintech companies in Japan that want to go down the payment route.

That’s increasingly popular, given the government push to make the country a “cashless society” ahead of the 2020 Olympic Games next year. It also could appeal to crypto companies in Japan, which offers the world’s most robust licensing, that want to follow the example of the Coinbase card in Europe or startups like Crypto.com and TenX, which offer similar prepaid cards.

Takatori said Kyash is “in discussions” with crypto companies, but that it has not made a decision on how to proceed yet. The company is also eyeing potential overseas expansions, although that is some way down the line.

“We have open eyes for globalization, it’s just a matter of when,” he told TechCrunch. “We still have a far way to go [in Japan, but] maybe after the Olympics.”

More pressingly, he sees the company looking to raise a “pretty quick” Series C round to give it acceleration into next year. That’s likely to go to more expansion and user acquisition as the licenses the startup has applied for are unlikely to be granted this year.

Powered by WPeMatico

Tired of cleaning up after take-out or getting hangry waiting at your table in restaurants? Well Uber Eats is barging into the dine-in business. A new option in some cities lets you order your food ahead of time, go to the restaurant, then sit down inside to eat, a tipster from competing dine-in app Allset tells us. We tested it, and Uber Eats Dine-In even waives the standard Uber delivery and service fees.

Adding Dine-In lets Uber Eats insert itself into more food transactions, expand to restaurants that care about presentation and don’t do delivery and avoid paying drivers while earning low-overhead revenue. Uber’s Dine-In option is now available in some cities, including Austin, Dallas, Phoenix and San Diego, where it could save diners time and fees while helping restaurants fill empty tables and waiters earn tips. But it also could coerce more restaurants to play ball with UberEats if their competitors do, eating into their margins.

Uber confirmed the existence of the Dine-In option, telling me, “We’re always thinking about new ways to enhance the Eats experience.” They also verified there are no delivery or service fees, and restaurants get 100% of tips left in-app by users. However, we found some items were silently marked up from restaurants’ listed prices in both Uber Eats Delivery and Dine-In options, which could help it make some money directly from these purchases. We also discovered this buried Uber Help Center FAQ with more details.

Uber has been rapidly experimenting with Uber Eats, trying discounted specials, Uber Eats Pool, where you pay less for slower delivery, and $9.99 unlimited delivery subscriptions. It’s steadily becoming an omnivore.

Dine-in appears next to the Delivery and Pick-Up options across the top of the Uber Eats app in select cities. You can choose to go eat “ASAP” or in some cases schedule when you want to arrive and sit down. You’ll be shown how long the food will take to prep, distance to the restaurant, your price and the restaurant’s rating. You’ll then be notified as the order is prepared and approaches readiness. Then you just deliver yourself to the restaurant and add a tip in-app or on the table.

Uber Eats should obviously make it easy for you to hail an Uber with the restaurant as the pre-set destination. An Uber spokesperson called that a good idea but not something it’s doing yet. Back in 2016, Uber tried a merchant-sponsored rides option where you’d get a rebate on your travel if you spent money at a given store. You could imagine restaurants that want to show off their ambiance giving customers some money back if they come across town to eat there.

The new feature could spell trouble for other dine-in apps like Allset that’s been in the business for four years. Users might also opt for Uber Eats Dine-In over restaurant reservation apps like OpenTable and Resy. Why waste time waiting to order and for your food to be cooked when you could just show up as it comes out of the oven?

“I think that more delivery players will be tapping into dine-in space. It’s all about convenience and time saving. But it’s going to be very difficult for them, given their focus on delivery,” Allset CEO Stas Matviyenko said of Uber becoming a competitor. He believes dedicated apps for different modes of dining will succeed. But Uber Eats’ ubiquity and its one-stop-shop model for all your dining needs could make it stickier than a dine-in only app you use less frequently.

With Dine-In, Uber could aid restaurants that are empty at the start or end of their open hours. Last year we reported that Uber Eats was giving restaurants prominence in a Featured section of the app to drive up demand if they offered discounts to customers. Similarly, Uber could let restaurants entice more Dine-In customers, especially when foot-traffic was slow, by providing discounts on food or subsidized Uber transportation. Better to knock a dollar or two off an entree if it means filling the restaurant at 5:30 or 9:30 pm.

And now that Uber Eats does delivery, take-out and dine-in, it’d make perfect sense to offer traditional restaurant reservations through the app as well. That would pit it directly against OpenTable, Resy and Yelp. Instead of trying to own a single use case that might only appeal to certain demographics in certain situations, Uber Eats’ strategy is crystallizing: be the app you open whenever you’re hungry.

Powered by WPeMatico

Meme creators have never gotten their fair share. Remixed and reshared across the web, their jokes prop up social networks like Instagram and Twitter that pay back none of their ad revenue to artists and comedians. But 300 million monthly user meme and storytelling app Imgur wants to pioneer a way to pay creators per second that people view their content.

Today Imgur announces that it’s raised a $20 million venture equity round from Coil, a micropayment tool for creators that Imgur has agreed to build into its service. Imgur will eventually launch a premium membership with exclusive features and content reserved for Coil subscribers.

Users pay Coil a fixed monthly fee, install its browser extension, the Interledger protocol is used to route assets around, and then Coil pays creators dollars or XRP tokens per second that the subscriber spends consuming their content at a rate of 36 cents per hour. Imgur and Coil will earn a cut too, diversifying the meme network’s revenue beyond ads.

“Imgur began in 2009 as a gift to the internet. Over the last 10 years we’ve built one of the largest, most positive online communities, based on our core value to ‘give more than we take’” says Alan Schaaf, founder and CEO of Imgur. The startup bootstrapped for its first five years before raising a $40 million Series A from Andreessen Horowitz and Reddit. It’s grown into the premier place to browse ‘meme dumps’ of 50+ funny images and GIFs, as well as art, science, and inspirational tales. With the same unpersonalized homepage for everyone, it’s fostered a positive community unified by esoteric inside jokes.

While the new round brings in fewer dollars, Schaaf explains that Imgur raised at a valuation that’s “higher than last time. Our investors are happy with the valuation. This is a really exciting strategic partnership.” Coil founder and CEO Stefan Thomas who was formerly the CTO of cryptocurrency company Ripple Labs will join Imgur’s board. Coil received the money it’s investing in Imgur from Ripple Labs’ Xpring Initiative, which aims to fund proliferation of the Ripple XRP ecosystem, though Imgur received US dollars in the funding deal.

Thomas tells me that “There’s no built in business model” as part of the web. Publishers and platforms “either make money with ads or with subscriptions. The problem is that only works when you have huge scale” that can bring along societal problems as we’ve seen with Facebook. Coil will “hopefully offer a third potential business model for the internet and offer a way for creators to get paid.”

Founded last year, Coil’s $5 per month subscription is now in open beta, and it provides extensions for Chrome and Firefox as it tries to get baked into browsers natively. Unlike Patreon where you pick a few creators and choose how much to pay each every month, Coil lets you browse content from as many creators as you want and it pays them appropriately. Sites like Imgur can code in tags to their pages that tell Coil’s Web Monetization API who to send money to.

The challenge for Imgur will be avoiding the cannibalization of its existing content to the detriment of its non-paying users who’ve always known it to be free. “We’re in the business of making the internet better. We do not plan on taking anything away for the community” Schaaf insists. That means it will have to recruit new creators and add bonus features that are reserved for Coil subscribers without making the rest of its 300 million users feel deprived.

It’s surprising thT meme culture hasn’t spawned more dedicated apps. Decade-old Imgur precedes the explosion in popularity of bite-sized internet content. But rather than just host memes like Instagram, Imgur has built its own meme creation tools. If Imgur and Coil can prove users are willing to pay for quick hits of entertainment and creators can be fairly compensated, they could inspire more apps to help content makers turn their passion into a profession…or at least a nice side hustle.

Powered by WPeMatico

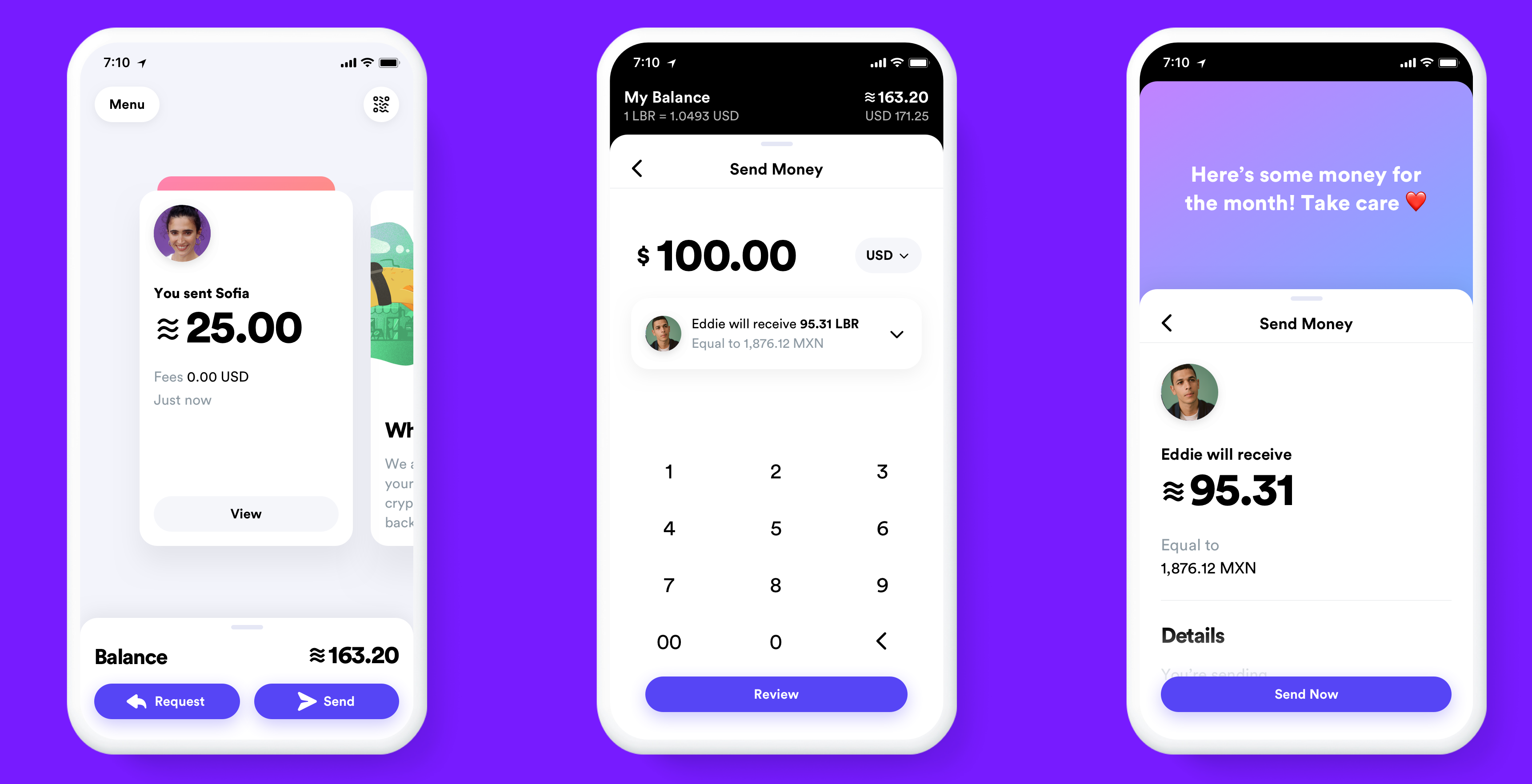

They’re not called Zuckerbucks, but Facebook just reinvented digital money. Facebook’s Libra cryptocurrency that will launch early next year is more like PayPal than Bitcoin — it’s designed to be easy enough for everyone to use. But it’s still complicated to understand, so I’m going to break it down for you nice and simple.

Watch our handy video above or read the transcript below.

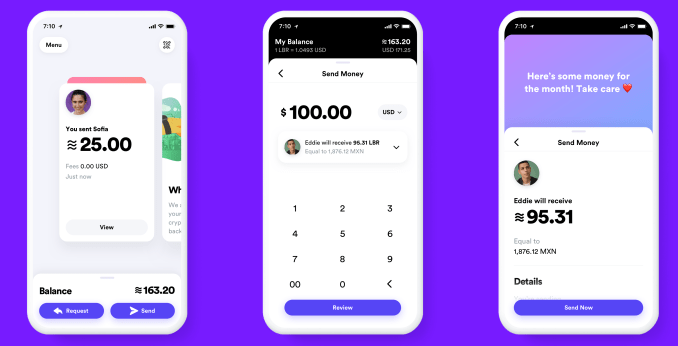

Libra is like cash that lives inside your phone. How do you buy Facebook’s cryptocurrency? Starting in 2020, you’ll be able to purchase Libra through Libra wallet apps on your phone or from some local grocery and convenience stores. You cash in your local currency like dollars and get nearly the same number of Libra coins, which are represented by this wavy three-line emoji instead of the $ symbol. But first you’ll have to verify your identity with a photo.

![]()

You’ll then be able to spend your Libra while online shopping, or potentially pay for things like Ubers or your subscription for Spotify, since those companies have partnered with Facebook to make Libra popular. Since it’s almost free to digitally move Libra from one account to the other, you won’t have to pay high credit card processing fees that can add almost 4% to your total. And some Libra wallet apps and shops will give bonus discounts or free coins for signing up and paying with Libra.

You’ll also be able to send and request money from friends like you would with Venmo or PayPal. It’s as easy to send Libra as it is a message. In fact, Facebook is building its own Libra wallet app called Calibra that will live inside of WhatsApp, Facebook Messenger and its own standalone app.

You won’t have to attach your real name and identity to any of your payments, but they will be public. Facebook knows it’s a little bit creepy and you probably don’t want it spying on what you buy. So Facebook set up a new company also called Calibra that will keep all your financial data separate from your Facebook profile. That means it can’t use your transaction data to target you with ads, re-order your News Feed or sell your info to marketers.

Eventually, Facebook hopes you’ll use Libra to pay your bills, scan your wallet’s QR code to purchase coffee or tap your phone to buy your public transit ticket. At any time, you can cash out of Libra and get your local currency back in your bank account, or handed to you at a local grocery store.

But how does the Libra cryptocurrency technically work…without a bunch of blockchain buzzwords? Libra is coded to have a stable price, be secure and be controlled not just by Facebook.

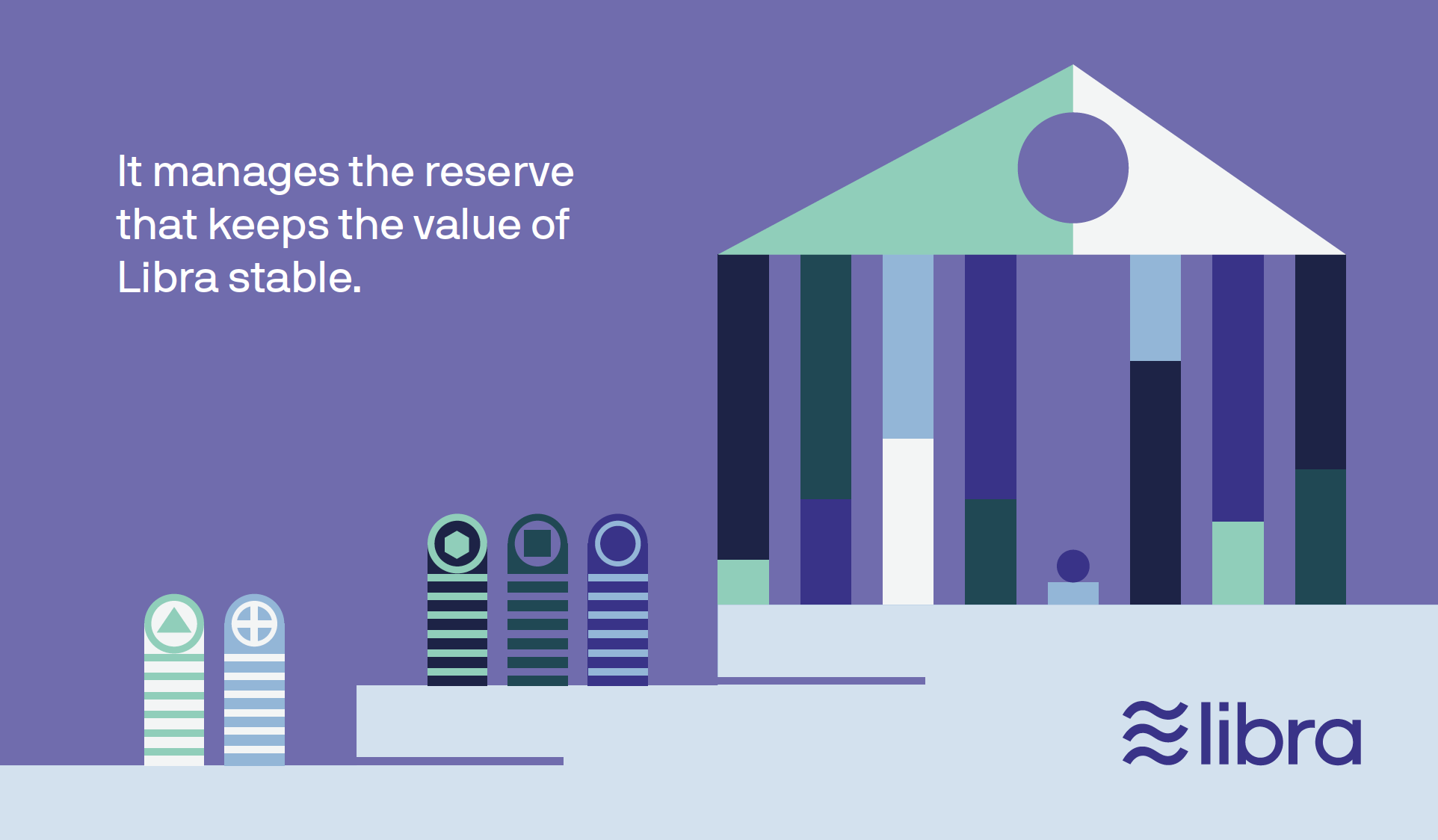

Instead, Libra is run by the 28-member Libra Association that it hopes will grow to 100 members by the time it launches in the first half of 2020. Financial companies like Visa and Mastercard, merchants and apps like eBay and Lyft, venture capital funds like Andreessen Horowitz and Union Square Ventures and nonprofits like Kiva are all members. They each paid at least $10 million to get one vote on the Libra council that controls what happens to the currency. They’ll be responsible for checking to make sure Libra transactions are real and creating the Libra Reserve.

Each time you cash in a dollar, that money goes into a big bank account called the Libra Reserve that creates and sends you roughly one Libra token. The Libra Reserve is made up of a collection of the most stable international currencies, like the U.S. dollar, British pound, the euro and the Japanese yen. The idea is that even if one of those currencies goes up or down in price, the value of the Libra will stay stable. That way, shops will accept the Libra as payment without worrying the value of the coin will drop tomorrow. Big swings in price are why older cryptocurrencies like Bitcoin or Ethereal haven’t grown popular as payment methods. Libra can also handle 1,000 transactions per second, while Bitcoin can only handle 7.

So how do Facebook and the other Libra Association members earn money? Off of interest on all the assets held in the Libra Reserve. After the Libra Association pays for its operations and investments in technology, members earns a cut of the remaining interest in proportion to how much they invested when they joined. If Libra gets popular, tons of people cash in and the reserve grows huge, the interest could add up to serious revenue for Facebook.

But there’s also a subtle second way Facebook could get rich from Libra. If the currency makes it easier for small businesses to accept payments online, they’ll sell more stuff. They’ll then have extra money to spend on Facebook ads, which will make it extra quick to buy things with Libra. Ninety million small businesses already have Facebook Pages, but Facebook only has 7 million advertisers. If it can turn more of those local merchants into ad buyers, Facebook’s revenues could skyrocket.

The big risk of Libra is that anyone will be able to develop apps for it. That could lead to another Cambridge Analytica situation. But instead of some shady app maker snatching your personal info, they could steal your digital currency. Facebook and the Libra Association say they won’t vet Libra developers, which leaves the door wide open to abuse. And if people get scammed, they’ll blame Facebook.

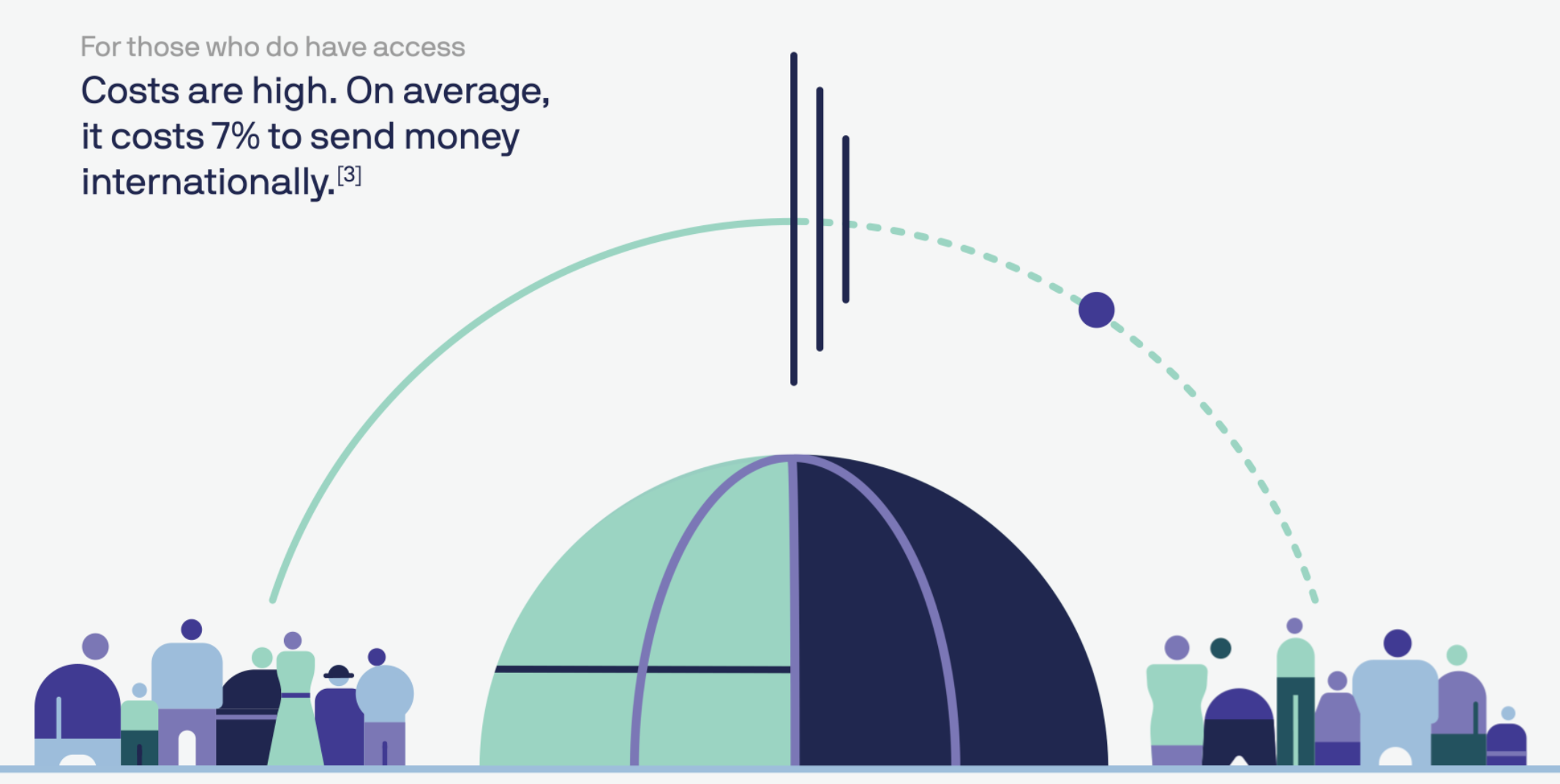

But if Facebook succeeds, the real win could be for the 1.7 billion people left in poverty with no bank account around the world. They’re exploited by international money sending services like Western Union or Monogram that charge steep 7% fees that take $50 billion away from families per year. And if they’re mugged, they could lose all their money since they have nothing stored online. All they’ll need is a photo ID and Libra could give them an alternative to a bank account that’s tougher to steal and could make it easy to pay for what they need.

There are plenty of reasons to worry that Libra could give Facebook and other tech giants more power or lead to people getting scammed. But it could also give disadvantaged people everywhere a way to join the modern economy. And at least it’s not called FaceCoin.

And if you want to know how Libra could spawn Facebook’s next scandal, read this:

Video by Gregory Manalo, b-roll via Libra Association

Powered by WPeMatico

Everyone’s worried about Mark Zuckerberg controlling the next currency, but I’m more concerned about a crypto Cambridge Analytica.

Today Facebook announced Libra, its forthcoming stablecoin designed to let you shop and send money overseas with almost zero transaction fees. Immediately, critics started harping about the dangers of centralizing control of tomorrow’s money in the hands of a company with a poor track record of privacy and security.

Facebook anticipated this, though, and created a subsidiary called Calibra to run its crypto dealings and keep all transaction data separate from your social data. Facebook shares control of Libra with 27 other Libra Association founding members, and as many as 100 total when the token launches in the first half of 2020. Each member gets just one vote on the Libra council, so Facebook can’t hijack the token’s governance even though it invented it.

With privacy fears and centralized control issues at least somewhat addressed, there’s always the issue of security. Facebook naturally has a huge target on its back for hackers. Not just because Libra could hold so much value to steal, but because plenty of trolls would get off on screwing up Facebook’s currency. That’s why Facebook open-sourced the Libra Blockchain and is offering a prototype in a pre-launch testnet. This developer beta plus a bug bounty program run in partnership with HackerOne is meant to surface all the flaws and vulnerabilities before Libra goes live with real money connected.

Yet that leaves one giant vector for abuse of Libra: the developer platform.

“Essential to the spirit of Libra . . . the Libra Blockchain will be open to everyone: any consumer, developer, or business can use the Libra network, build products on top of it, and add value through their services. Open access ensures low barriers to entry and innovation and encourages healthy competition that benefits consumers,” Facebook explained in its white paper and Libra launch documents. It’s even building a whole coding language called Move for making Libra apps.

Apparently Facebook has already forgotten how allowing anyone to build on the Facebook app platform and its low barriers to “innovation” are exactly what opened the door for Cambridge Analytica to hijack 87 million people’s personal data and use it for political ad targeting.

But in this case, it won’t be users’ interests and birthdays that get grabbed. It could be hundreds or thousands of dollars’ worth of Libra currency that’s stolen. A shady developer could build a wallet that just cleans out a user’s account or funnels their coins to the wrong recipient, mines their purchase history for marketing data or uses them to launder money. Digital risks become a lot less abstract when real-world assets are at stake.

In the wake of the Cambridge Analytica scandal, Facebook raced to lock down its app platform, restrict APIs, more heavily vet new developers and audit ones that look shady. So you’d imagine the Libra Association would be planning to thoroughly scrutinize any developer trying to build a Libra wallet, exchange or other related app, right? “There are no plans for the Libra Association to take a role in actively vetting [developers],” Calibra’s head of product Kevin Weil surprisingly told me. “The minute that you start limiting it is the minute you start walking back to the system you have today with a closed ecosystem and a smaller number of competitors, and you start to see fees rise.”

That translates to “the minute we start responsibly verifying Libra app developers, things start to get expensive, complicated or agitating to cryptocurrency purists. That might hurt growth and adoption.” You know what will hurt growth of Libra a lot worse? A sob story about some migrant family or a small business getting all their Libra stolen. And that blame is going to land squarely on Facebook, not some amorphous Libra Association.

Image via Getty Images / alashi

Inevitably, some unsavvy users won’t understand the difference between Facebook’s own wallet app Calibra and any other app built for the currency. “Libra is Facebook’s cryptocurrency. They wouldn’t let me get robbed,” some will surely say. And on Calibra they’d be right. It’s a custodial wallet that will refund you if your Libra are stolen and it offers 24/7 customer support via chat to help you regain access to your account.

Yet the Libra Blockchain itself is irreversible. Outside of custodial wallets like Calibra, there’s no getting your stolen or mis-sent money back. There’s likely no customer support. And there are plenty of crooked crypto developers happy to prey on the inexperienced. Indeed, $1.7 billion in cryptocurrency was stolen last year alone, according to CypherTrace via CNBC. “As with anything, there’s fraud and there are scams in the existing financial ecosystem today . . . that’s going to be true of Libra too. There’s nothing special or magical that prevents that,” says Weil, who concluded “I think those pros massively outweigh the cons.”

Until now, the blockchain world was mostly inhabited by technologists, except for when skyrocketing values convinced average citizens to invest in Bitcoin just before prices crashed. Now Facebook wants to bring its family of apps’ 2.7 billion users into the world of cryptocurrency. That’s deeply worrisome.

Facebook founder and CEO Mark Zuckerberg arrives to testify during a Senate Commerce, Science and Transportation Committee and Senate Judiciary Committee joint hearing about Facebook on Capitol Hill in Washington, DC, April 10, 2018. (Photo: SAUL LOEB/AFP/Getty Images)

Regulators are already bristling, but perhaps for the wrong reasons. Democrat Senator Sherrod Brown tweeted that “We cannot allow Facebook to run a risky new cryptocurrency out of a Swiss bank account without oversight.” And French Finance Minister Bruno Le Maire told Europe 1 radio that Libra can’t be allowed to “become a sovereign currency.”

Most harshly, Rep. Maxine Waters issued a statement saying, “Given the company’s troubled past, I am requesting that Facebook agree to a moratorium on any movement forward on developing a cryptocurrency until Congress and regulators have the opportunity to examine these issues and take action.”

Yet Facebook has just one vote in controlling the currency, and the Libra Association preempted these criticisms, writing, “We welcome public inquiry and accountability. We are committed to a dialogue with regulators and policymakers. We share policymakers’ interest in the ongoing stability of national currencies.”

That’s why as lawmakers confer about how to regulate Libra, I hope they remember what triggered the last round of Facebook execs having to appear before Congress and Parliament. A totally open, unvetted Libra developer platform in the name of “innovation” over safety is a ticking time bomb. Governments should insist the Libra Association thoroughly audit developers and maintain the power to ban bad actors. In this strange new crypto world, the public can’t be expected to perfectly protect itself from Cambridge Analytica 2.$.

Get up to speed on Facebook’s Libra with this handy guide:

Powered by WPeMatico

Facebook has finally revealed the details of its cryptocurrency, Libra, which will let you buy things or send money to people with nearly zero fees. You’ll pseudonymously buy or cash out your Libra online or at local exchange points like grocery stores, and spend it using interoperable third-party wallet apps or Facebook’s own Calibra wallet that will be built into WhatsApp, Messenger and its own app. Today Facebook released its white paper explaining Libra and its testnet for working out the kinks of its blockchain system before a public launch in the first half of 2020.

Facebook won’t fully control Libra, but instead get just a single vote in its governance like other founding members of the Libra Association, including Visa, Uber and Andreessen Horowitz, which have invested at least $10 million each into the project’s operations. The association will promote the open-sourced Libra Blockchain and developer platform with its own Move programming language, plus sign up businesses to accept Libra for payment and even give customers discounts or rewards.

Facebook is launching a subsidiary company also called Calibra that handles its crypto dealings and protects users’ privacy by never mingling your Libra payments with your Facebook data so it can’t be used for ad targeting. Your real identity won’t be tied to your publicly visible transactions. But Facebook/Calibra and other founding members of the Libra Association will earn interest on the money users cash in that is held in reserve to keep the value of Libra stable.

Facebook’s audacious bid to create a global digital currency that promotes financial inclusion for the unbanked actually has more privacy and decentralization built in than many expected. Instead of trying to dominate Libra’s future or squeeze tons of cash out of it immediately, Facebook is instead playing the long-game by pulling payments into its online domain. Facebook’s VP of blockchain, David Marcus, explained the company’s motive and the tie-in with its core revenue source during a briefing at San Francisco’s historic Mint building. “If more commerce happens, then more small businesses will sell more on and off platform, and they’ll want to buy more ads on the platform so it will be good for our ads business.”

In cryptocurrencies, Facebook saw both a threat and an opportunity. They held the promise of disrupting how things are bought and sold by eliminating transaction fees common with credit cards. That comes dangerously close to Facebook’s ad business that influences what is bought and sold. If a competitor like Google or an upstart built a popular coin and could monitor the transactions, they’d learn what people buy and could muscle in on the billions spent on Facebook marketing. Meanwhile, the 1.7 billion people who lack a bank account might choose whoever offers them a financial services alternative as their online identity provider too. That’s another thing Facebook wants to be.

Yet existing cryptocurrencies like Bitcoin and Ethereum weren’t properly engineered to scale to be a medium of exchange. Their unanchored price was susceptible to huge and unpredictable swings, making it tough for merchants to accept as payment. And cryptocurrencies miss out on much of their potential beyond speculation unless there are enough places that will take them instead of dollars, and the experience of buying and spending them is easy enough for a mainstream audience. But with Facebook’s relationship with 7 million advertisers and 90 million small businesses plus its user experience prowess, it was well-poised to tackle this juggernaut of a problem.

Now Facebook wants to make Libra the evolution of PayPal . It’s hoping Libra will become simpler to set up, more ubiquitous as a payment method, more efficient with fewer fees, more accessible to the unbanked, more flexible thanks to developers and more long-lasting through decentralization.

“Success will mean that a person working abroad has a fast and simple way to send money to family back home, and a college student can pay their rent as easily as they can buy a coffee,” Facebook writes in its Libra documentation. That would be a big improvement on today, when you’re stuck paying rent in insecure checks while exploitative remittance services charge an average of 7% to send money abroad, taking $50 billion from users annually. Libra could also power tiny microtransactions worth just a few cents that are infeasible with credit card fees attached, or replace your pre-paid transit pass.

…Or it could be globally ignored by consumers who see it as too much hassle for too little reward, or too unfamiliar and limited in use to pull them into the modern financial landscape. Facebook has built a reputation for over-engineered, underused products. It will need all the help it can get if wants to replace what’s already in our pockets.

By now you know the basics of Libra. Cash in a local currency, get Libra, spend them like dollars without big transaction fees or your real name attached, cash them out whenever you want. Feel free to stop reading and share this article if that’s all you care about. But the underlying technology, the association that governs it, the wallets you’ll use and the way payments work all have a huge amount of fascinating detail to them. Facebook has released more than 100 pages of documentation on Libra and Calibra, and we’ve pulled out the most important facts. Let’s dive in.

Facebook knew people wouldn’t trust it to wholly steer the cryptocurrency they use, and it also wanted help to spur adoption. So the social network recruited the founding members of the Libra Association, a not-for-profit which oversees the development of the token, the reserve of real-world assets that gives it value and the governance rules of the blockchain. “If we were controlling it, very few people would want to jump on and make it theirs,” says Marcus.

Each founding member paid a minimum of $10 million to join and optionally become a validator node operator (more on that later), gain one vote in the Libra Association council and be entitled to a share (proportionate to their investment) of the dividends from interest earned on the Libra reserve into which users pay fiat currency to receive Libra.

The 28 soon-to-be founding members of the association and their industries, previously reported by The Block’s Frank Chaparro, include:

Facebook says it hopes to reach 100 founding members before the official Libra launch and it’s open to anyone that meets the requirements, including direct competitors like Google or Twitter. The Libra Association is based in Geneva, Switzerland and will meet biannually. The country was chosen for its neutral status and strong support for financial innovation including blockchain technology.

To join the association, members must have a half rack of server space, a 100Mbps or above dedicated internet connection, a full-time site reliability engineer and enterprise-grade security. Businesses must hit two of three thresholds of a $1 billion USD market value or $500 million in customer balances, reach 20 million people a year and/or be recognized as a top 100 industry leader by a group like Interbrand Global or the S&P.

Crypto-focused investors must have more than $1 billion in assets under management, while Blockchain businesses must have been in business for a year, have enterprise-grade security and privacy and custody or staking greater than $100 million in assets. And only up to one-third of founding members can by crypto-related businesses or individually invited exceptions. Facebook also accepts research organizations like universities, and nonprofits fulfilling three of four qualities, including working on financial inclusion for more than five years, multi-national reach to lots of users, a top 100 designation by Charity Navigator or something like it and/or $50 million in budget.

The Libra Association will be responsible for recruiting more founding members to act as validator nodes for the blockchain, fundraising to jump-start the ecosystem, designing incentive programs to reward early adopters and doling out social impact grants. A council with a representative from each member will help choose the association’s managing director, who will appoint an executive team and elect a board of five to 19 top representatives.

Each member, including Facebook/Calibra, will only get up to one vote or 1% of the total vote (whichever is larger) in the Libra Association council. This provides a level of decentralization that protects against Facebook or any other player hijacking Libra for its own gain. By avoiding sole ownership and dominion over Libra, Facebook could avoid extra scrutiny from regulators who are already investigating it for a sea of privacy abuses as well as potentially anti-competitive behavior. In an attempt to preempt criticism from lawmakers, the Libra Association writes, “We welcome public inquiry and accountability. We are committed to a dialogue with regulators and policymakers. We share policymakers’ interest in the ongoing stability of national currencies.”

A Libra is a unit of the Libra cryptocurrency that’s represented by a three wavy horizontal line unicode character ≋ like the dollar is represented by $. The value of a Libra is meant to stay largely stable, so it’s a good medium of exchange, as merchants can be confident they won’t be paid a Libra today that’s then worth less tomorrow. The Libra’s value is tied to a basket of bank deposits and short-term government securities for a slew of historically stable international currencies, including the dollar, pound, euro, Swiss franc and yen. The Libra Association maintains this basket of assets and can change the balance of its composition if necessary to offset major price fluctuations in any one foreign currency so that the value of a Libra stays consistent.

A Libra is a unit of the Libra cryptocurrency that’s represented by a three wavy horizontal line unicode character ≋ like the dollar is represented by $. The value of a Libra is meant to stay largely stable, so it’s a good medium of exchange, as merchants can be confident they won’t be paid a Libra today that’s then worth less tomorrow. The Libra’s value is tied to a basket of bank deposits and short-term government securities for a slew of historically stable international currencies, including the dollar, pound, euro, Swiss franc and yen. The Libra Association maintains this basket of assets and can change the balance of its composition if necessary to offset major price fluctuations in any one foreign currency so that the value of a Libra stays consistent.

The name Libra comes from the word for a Roman unit of weight measure. It’s trying to invoke a sense of financial freedom by playing on the French stem “Lib,” meaning free.

The Libra Association is still hammering out the exact start value for the Libra, but it’s meant to be somewhere close to the value of a dollar, euro or pound so it’s easy to conceptualize. That way, a gallon of milk in the U.S. might cost 3 to 4 Libra, similar but not exactly the same as with dollars.

The idea is that you’ll cash in some money and keep a balance of Libra that you can spend at accepting merchants and online services. You’ll be able to trade in your local currency for Libra and vice versa through certain wallet apps, including Facebook’s Calibra, third-party wallet apps and local resellers like convenience or grocery stores where people already go to top-up their mobile data plan.

Each time someone cashes in a dollar or their respective local currency, that money goes into the Libra Reserve and an equivalent value of Libra is minted and doled out to that person. If someone cashes out from the Libra Association, the Libra they give back are destroyed/burned and they receive the equivalent value in their local currency back. That means there’s always 100% of the value of the Libra in circulation, collateralized with real-world assets in the Libra Reserve. It never runs fractional. And unliked “pegged” stable coins that are tied to a single currency like the USD, Libra maintains its own value — though that should cash out to roughly the same amount of a given currency over time.

When Libra Association members join and pay their $10 million minimum, they receive Libra Investment Tokens. Their share of the total tokens translates into the proportion of the dividend they earn off of interest on assets in the reserve. Those dividends are only paid out after Libra Association uses interest to pay for operating expenses, investments in the ecosystem, engineering research and grants to nonprofits and other organizations. This interest is part of what attracted the Libra Association’s members. If Libra becomes popular and many people carry a large balance of the currency, the reserve will grow huge and earn significant interest.

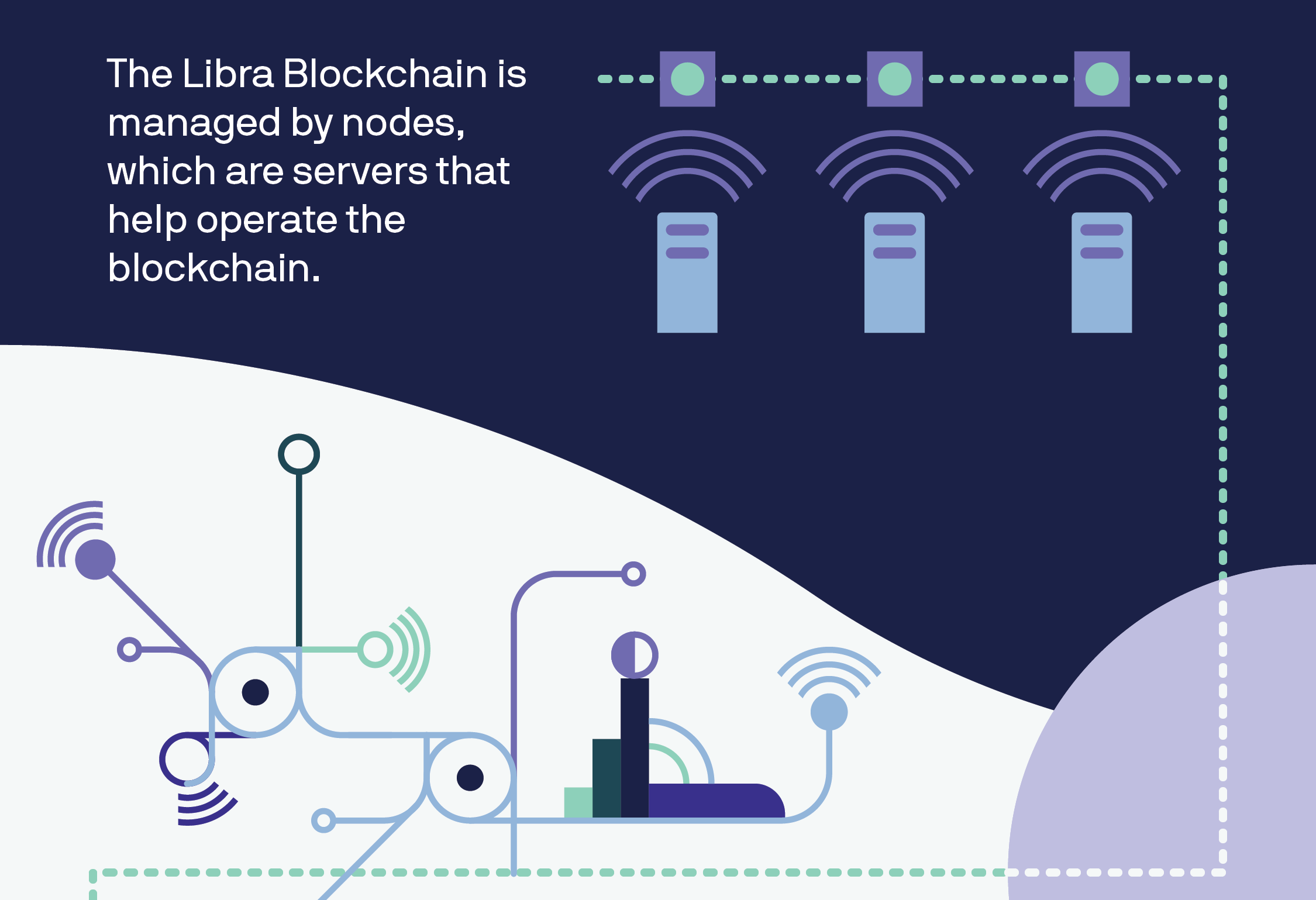

Every Libra payment is permanently written into the Libra Blockchain — a cryptographically authenticated database that acts as a public online ledger designed to handle 1,000 transactions per second. That would be much faster than Bitcoin’s 7 transactions per second or Ethereum’s 15. The blockchain is operated and constantly verified by founding members of the Libra Association, which each invested $10 million or more for a say in the cryptocurrency’s governance and the ability to operate a validator node.

When a transaction is submitted, each of the nodes runs a calculation based on the existing ledger of all transactions. Thanks to a Byzantine Fault Tolerance system, just two-thirds of the nodes must come to consensus that the transaction is legitimate for it to be executed and written to the blockchain. A structure of Merkle Trees in the code makes it simple to recognize changes made to the Libra Blockchain. With 5KB transactions, 1,000 verifications per second on commodity CPUs and up to 4 billion accounts, the Libra Blockchain should be able to operate at 1,000 transactions per second if nodes use at least 40Mbps connections and 16TB SSD hard drives.

Transactions on Libra cannot be reversed. If an attack compromises over one-third of the validator nodes causing a fork in the blockchain, the Libra Association says it will temporarily halt transactions, figure out the extent of the damage and recommend software updates to resolve the fork.

Transactions aren’t entirely free. They incur a tiny fraction of a cent fee to pay for “gas” that covers the cost of processing the transfer of funds similar to with Ethereum. This fee will be negligible to most consumers, but when they add up, the gas charges will deter bad actors from creating millions of transactions to power spam and denial-of-service attacks. “We’ve purposely tried not to innovate massively on the blockchain itself because we want it to be scalable and secure,” says Marcus of piggybacking on the best elements of existing cryptocurrencies.

Currently, the Libra Blockchain is what’s known as “permissioned,” where only entities that fulfill certain requirements are admitted to a special in-group that defines consensus and controls governance of the blockchain. The problem is this structure is more vulnerable to attacks and censorship because it’s not truly decentralized. But during Facebook’s research, it couldn’t find a reliable permissionless structure that could securely scale to the number of transactions Libra will need to handle. Adding more nodes slows things down, and no one has proven a way to avoid that without compromising security.

That’s why the Libra Association’s goal is to move to a permissionless system based on proof-of-stake that will protect against attacks by distributing control, encourage competition and lower the barrier to entry. It wants to have at least 20% of votes in the Libra Association council coming from node operators based on their total Libra holdings instead of their status as a founding member. That plan should help appease blockchain purists who won’t be satisfied until Libra is completely decentralized.

The Libra Blockchain is open source with an Apache 2.0 license, and any developer can build apps that work with it using the Move coding language. The blockchain’s prototype launches its testnet today, so it’s effectively in developer beta mode until it officially launches in the first half of 2020. The Libra Association is working with HackerOne to launch a bug bounty system later this year that will pay security researchers for safely identifying flaws and glitches. In the meantime, the Libra Association is implementing the Libra Core using the Rust programming language because it’s designed to prevent security vulnerabilities, and the Move language isn’t fully ready yet.

Move was created to make it easier to write blockchain code that follows an author’s intent without introducing bugs. It’s called Move because its primary function is to move Libra coins from one account to another, and never let those assets be accidentally duplicated. The core transaction code looks like: LibraAccount.pay_from_sender(recipient_address, amount) procedure.

Eventually, Move developers will be able to create smart contracts for programmatic interactions with the Libra Blockchain. Until Move is ready, developers can create modules and transaction scripts for Libra using Move IR, which is high-level enough to be human-readable but low-level enough to be translatable into real Move bytecode that’s written to the blockchain.

The Libra ecosystem and the Move language will be completely open to use and build, which presents a sizable risk. Crooked developers could prey on crypto novices, claiming their app works just the same as legitimate ones, and that it’s safe because it uses Libra. But if consumers get ripped off by these scammers, the anger will surely bubble up to Facebook. Yet still, Calibra’s head of product tells me, “There are no plans for the Libra Association to take a role in actively vetting [developers],” Calibra’s head of product Kevin Weil tells me.

Even though it’s tried to distance itself sufficiently via its subsidiary Libra and the association, many people will probably always think of Libra as Facebook’s cryptocurrency and blame it for their woes.

Read our full story on the dangers of Libra’s unvetted developer platform

The Libra Association wants to encourage more developers and merchants to work with its cryptocurrency. That’s why it plans to issue incentives, possibly Libra coins, to validator node operators who can get people signed up for and using Libra. Wallets that pull users through the Know Your Customer anti-fraud and money laundering process or that keep users sufficiently active for over a year will be rewarded. For each transaction they process, merchants will also receive a percentage of the transaction back.

Businesses that earn these incentives can keep them, or pass some or all of them along to users in the form of free Libra tokens or discounts on their purchases. This could create competition between wallets to see which can pass on the most rewards to their customers, and thereby attract the most users. You could imagine eBay or Spotify giving you a discount for paying in Libra, while wallet developers might offer you free tokens if you complete 100 transactions within a year.

“One challenge for Spotify and its users around the world has been the lack of easily accessible payment systems – especially for those in financially underserved markets,” Spotify’s Chief Premium Business Officer Alex Norström writes. “In joining the Libra Association, there is an opportunity to better reach Spotify’s total addressable market, eliminate friction and enable payments in mass scale.”

This savvy incentive system should massively help ratchet up Libra’s user count without dictating how businesses balance their margins versus growth. Facebook also has another plan to grow its developer ecosystem. By offering venture capital firms like Andreessen Horowitz and Union Square Ventures a portion of the reserve interest, they’re motivating to fund startups building Libra infrastructure.

So how do you actually own and spend Libra? Through Libra wallets like Facebook’s own Calibra and others that will be built by third-parties, potentially including Libra Association members like PayPal. The idea is to make sending money to a friend or paying for something as easy as sending a Facebook Message. You won’t be able to make or receive any real payments until the official launch next year, though, but you can sign up for early access when it’s ready here.

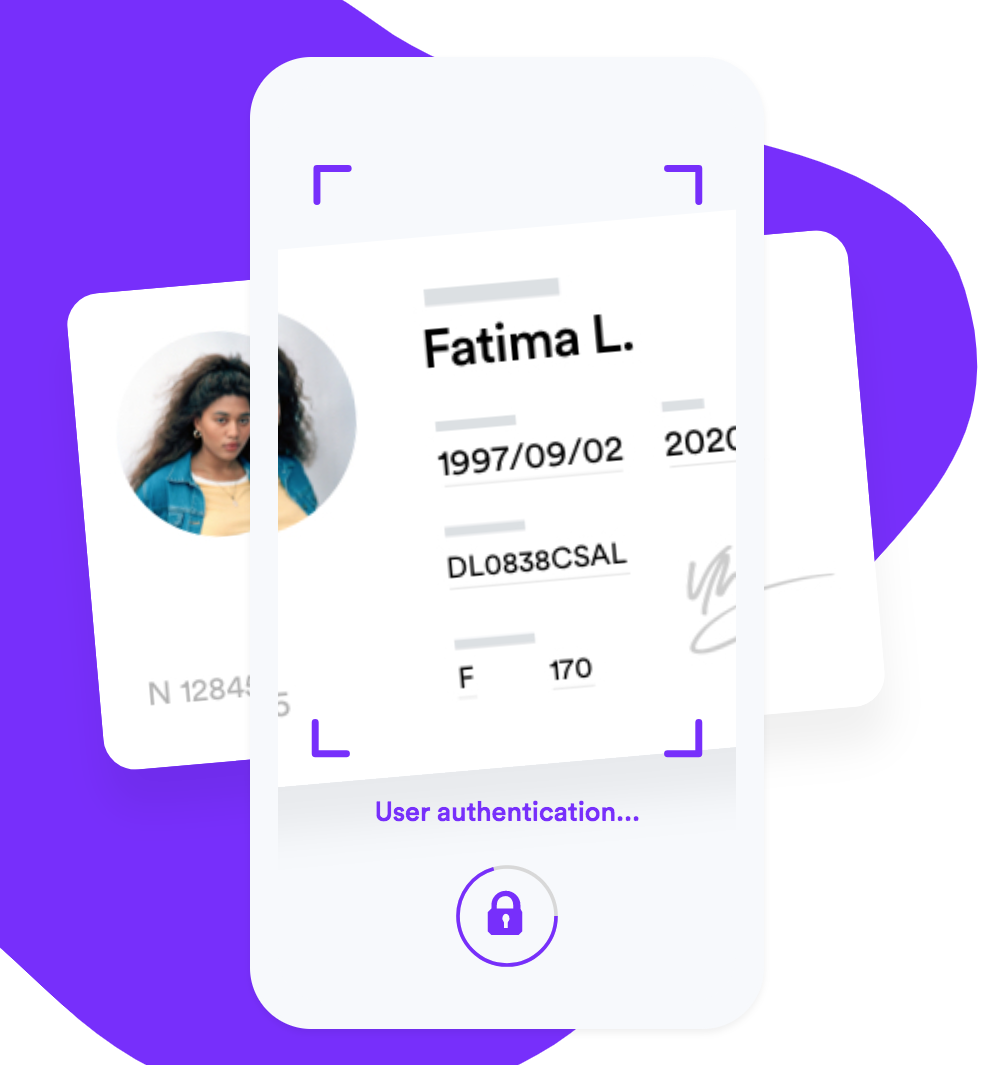

None of the Libra Association members agreed to provide details on what exactly they’ll build on the blockchain, but we can take Facebook’s Calibra wallet as an example of the basic experience. Calibra will launch alongside the Libra currency on iOS and Android within Facebook Messenger, WhatsApp and a standalone app. When users first sign up, they’ll be taken through a Know Your Customer anti-fraud process where they’ll have to provide a government-issued photo ID and other verification info. They’ll need to conduct due diligence on customers and report suspicious activity to the authorities.

From there you’ll be able to cash in to Libra, pick a friend or merchant, set an amount to send them and add a description and send them Libra. You’ll also be able to request Libra, and Calibra will offer an expedited way of paying merchants by scanning your or their QR code. Eventually it wants to offer in-store payments and integrations with point-of-sale systems like Square.

The Libra Association’s e-commerce members seem particularly excited about how the token could eliminate transaction fees and speed up checkout. “We believe blockchain will benefit the luxury industry by improving IP protection, transparency in the product life cycle and — as in the case of Libra — enable global frictionless e-commerce,” says FarFetch CEO Jose Neves.

Facebook CEO Mark Zuckerberg explained some of the philosophy behind Libra and Calibra in a post today. “It’s decentralized — meaning it’s run by many different organizations instead of just one, making the system fairer overall. It’s available to anyone with an internet connection and has low fees and costs. And it’s secured by cryptography which helps keep your money safe. This is an important part of our vision for a privacy-focused social platform — where you can interact in all the ways you’d want privately, from messaging to secure payments.”

By default, Facebook won’t import your contacts or any of your profile information, but may ask if you wish to do so. It also won’t share any of your transaction data back to Facebook, so it won’t be used to target you with ads, rank your News Feed, or otherwise earn Facebook money directly. Data will only be shared in specific instances in anonymized ways for research or adoption measurement, for hunting down fraudsters or due to a request from law enforcement. And you don’t even need a Facebook or WhatsApp account to sign up for Calibra or to use Libra.

“We realize people don’t want their social data and financial data commingled,” says Marcus, who’s now head of Calibra. “The reality is we’ll have plenty of wallets that will compete with us and many of them will not be in social, and if we want to successfully win people’s trust, we have to make sure the data will be separated.”

In case you are hacked, scammed or lose access to your account, Calibra will refund you for lost coins when possible through 24/7 chat support because it’s a custodial wallet. You also won’t have to remember any long, complex crypto passwords you could forget and get locked out from your money, as Calibra manages all your keys for you. Given Calibra will likely become the default wallet for many Libra users, this extra protection and smoother user experience is essential.

For now, Calibra won’t make money. But Calibra’s head of product Kevin Weil tells me that if it reaches scale, Facebook could launch other financial tools through Calibra that it could monetize, such as investing or lending. “In time, we hope to offer additional services for people and businesses, such as paying bills with the push of a button, buying a cup of coffee with the scan of a code or riding your local public transit without needing to carry cash or a metro pass,” the Calibra team writes. That makes it start to sound a lot like China’s everything app WeChat.

Facebook got one thing right for sure: Today’s money doesn’t work for everyone. Those of us living comfortably in developed nations likely don’t see the hardships that befall migrant workers or the unbanked abroad. Preyed on by greedy payday lenders and high-fee remittance services, targeted by muggers and left out of traditional financial services, the poor get poorer. Libra has the potential to get more money from working parents back to their families and help people retain credit even if they’re robbed of their physical possessions. That would do more to accomplish Facebook’s mission of making the world feel smaller than all the News Feed Likes combined.

If Facebook succeeds and legions of people cash in money for Libra, it and the other founding members of the Libra Association could earn big dividends on the interest. And if suddenly it becomes super quick to buy things through Facebook using Libra, businesses will boost their ad spend there. But if Libra gets hacked or proves unreliable, it could cost lots of people around the world money while souring them on cryptocurrencies. And by offering an open Libra platform, shady developers could build apps that snatch not just people’s personal info like Cambridge Analytica, but their hard-earned digital cash.

Facebook just tried to reinvent money. Next year, we’ll see if the Libra Association can pull it off. It took me 4,000 words to explain Libra, but at least now you can make up your own mind about whether to be scared of Facebook crypto.

Powered by WPeMatico

MobiKwik, a mobile wallet app in India that has expanded to add several financial services in recent years, said today it plans to enter international markets as it approaches profitability with the local operation. The company is kick-starting its overseas ambitions with cross-border mobile top-ups support.

The 10-year-old firm said it has partnered with DT One, a Singapore-headquartered payments network, to enable international mobile recharge (topping up credit to a mobile account), rewards and airtime credit services in more than 150 nations across some 550 mobile operators. The feature is now live on the app.

The feature is aimed at Indians living overseas and immigrants in India, Upasana Taku, co-founder of MobiKwik told TechCrunch in an interview. Millions of Indians go overseas to pursue education or look for a job. Currently, there is no convenient way for them to either help — or receive help from — their families and friends in India when they need to top up their phones.

Similarly, millions of people come to India in search of a job. The new functionality from MobiKwik will allow their families and friends to top up their mobile credit as well. Taku said there is no processing fee for customers, as MobiKwik is absorbing all the overhead expenses.

For MobiKwik, mobile recharge is just the entry point to assess interest from users, Taku added. “This is the first service we are launching. We will eventually add other essential services as well. Mobile recharge will offer us good data points and will help us understand different markets,” she added.

MobiKwik is also studying different regulatory frameworks in overseas markets and holding conversations with stakeholders, she added.

The announcement comes at a time when MobiKwik is inching closer to profitability, a feat unheard of for a mobile wallet app provider in India. The firm, which claims to have grown its revenue by 100% in the last two years, expects to be profitable by this year and go public by 2022. (Interestingly, MobiKwik was looking to raise a big round at $1 billion valuation two years ago — which never happened.)

In the last year, the firm has expanded to offer financial services such as loans, insurance and investment advice. MobiKwik competes with a handful of payment services in India, including Paytm, PhonePe and Google Pay that either support, or fully work on top of a government-backed payment infrastructure called UPI. In April, UPI apps were used to carry out 782 million transactions, according to official figures.

The big numbers have attracted major investors, too. With $285.6 million in funding, India emerged as Asia’s top fintech market in the quarter that ended in March this year.

Powered by WPeMatico

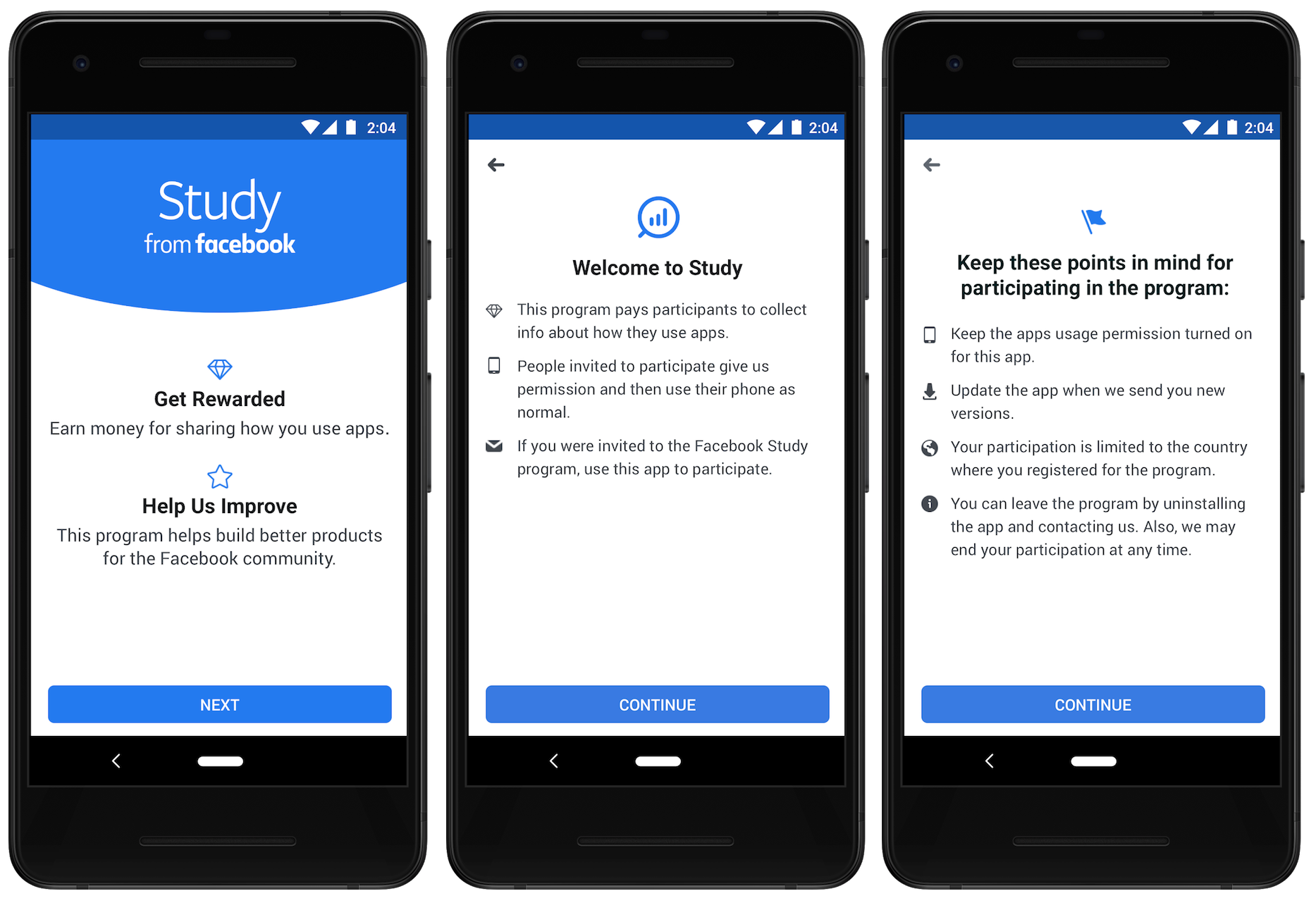

Facebook shut down its Research and Onavo programs after TechCrunch exposed how the company paid teenagers for root access to their phones to gain market data on competitors. Now Facebook is relaunching its paid market research program, but this time with principles — namely transparency, fair compensation and safety. The goal? To find out which other competing apps and features Facebook should buy, copy or ignore.

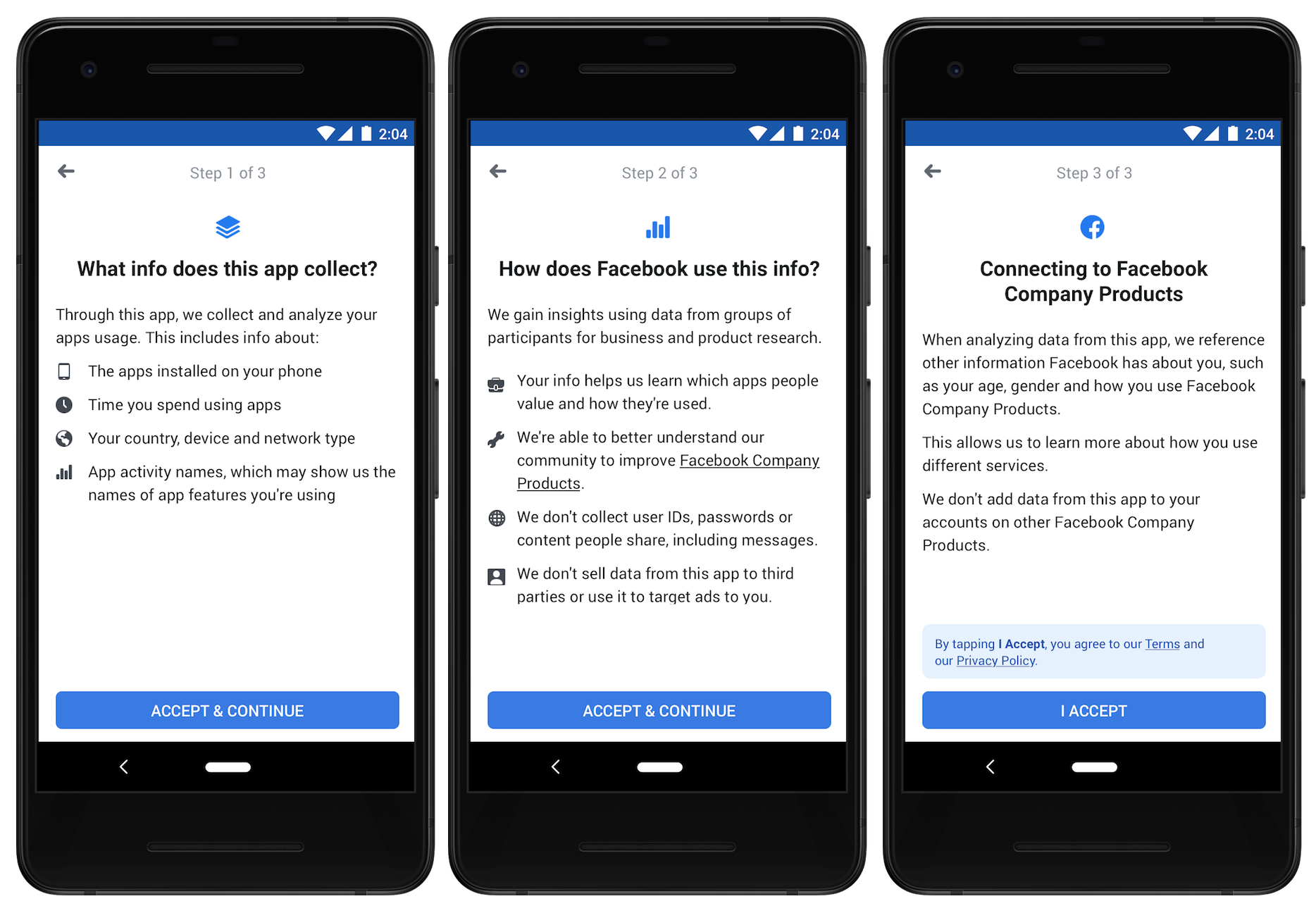

Today Facebook releases its “Study from Facebook” app for Android only. Some adults 18+ in the U.S. and India will be recruited by ads on and off Facebook to willingly sign up to let Facebook collect extra data from them in exchange for a monthly payment. They’ll be warned that Facebook will gather which apps are on their phone, how much time they spend using those apps, the app activity names of features they use in other apps, plus their country, device and network type.

Facebook promises it won’t snoop on user IDs, passwords or any of participants’ content, including photos, videos or messages. It won’t sell participants’ info to third parties, use it to target ads or add it to their account or the behavior profiles the company keeps on each user. Yet while Facebook writes that “transparency” is a major part of “Approaching market research in a responsible way,” it refuses to tell us how much participants will be paid.

“Study from Facebook” could give the company critical insights for shaping its product roadmap. If it learns everyone is using screensharing social network Squad, maybe it will add its own screensharing feature. If it finds group video chat app Houseparty is on the decline, it might not worry about cloning that functionality. Or if it finds Snapchat’s Discover mobile TV shows are retaining users for a ton of time, it might amp up teen marketing of Facebook Watch. But it also might rile up regulators and politicians who already see it as beating back competition through acquisitions and feature cloning.

TechCrunch’s investigation from January revealed that Facebook had been quietly operating a research program codenamed Atlas that paid users ages 13 to 35 up to $20 per month in gift cards in exchange for root access to their phone so it could gather all their data for competitive analysis. That included everything the Study app grabs, but also their web browsing activity, and even encrypted information, as the app required users to install a VPN that routed all their data through Facebook. It even had the means to collect private messages and content shared — potentially including data owned by their friends.

Facebook’s Research app also abused Apple’s enterprise certificate program designed for distributing internal use-only apps to employees without the App Store or Apple’s approval. Facebook originally claimed it obeyed Apple’s rules, but Apple quickly disabled Facebook’s Research app and also shut down its enterprise certificate, temporarily breaking Facebook’s internal test builds of its public apps, as well as the shuttle times and lunch menu apps employees rely on.

In the aftermath of our investigation, Facebook shut down its Research program. It then also announced in February that it would shut down its Onavo Protect app on Android, which branded itself as a privacy app providing a free VPN instead of paying users while it collected tons of data on them. After giving users until May 9th to find a replacement VPN, the Onavo Protect was killed off.

This was an embarrassing string of events that stemmed from unprincipled user research. Now Facebook is trying to correct its course and revive its paid data collection program but with more scruples.

Unlike Onavo or Facebook Research, users can’t freely sign up for Study. They have to be recruited through ads Facebook will show on its own app and others to both 18+ Facebook users and non-users in the U.S. and India. That should keep out grifters and make sure the studies stay representative of Facebook’s user base. Eventually, Facebook plans to extend the program to other countries.

If users click through the ad, they’ll be brought to Facebook’s research operations partner Applause’s website, which clearly identifies Facebook’s involvement, unlike Facebook Research, which hid that fact until users were fully registered. There they’ll be informed how the Study app is opt-in, what data they’ll give up in exchange for what compensation and that they can opt out at any time. They’ll need to confirm their age, have a PayPal account (which are only supposed to be available to users 18 and over) and Facebook will cross-check the age to make sure it matches the person’s Facebook profile, if they have one. They won’t have to sign and NDA like with the Facebook Research program.