payments

Auto Added by WPeMatico

Auto Added by WPeMatico

Ticketmaster’s dominance has led to ridiculous service fees, scalpers galore and exclusive contracts that exploit venues and artists. The moronic approval of venue operator and artist management giant Live Nation’s merger with Ticketmaster in 2010 produced an anti-competitive juggernaut. It pressures venues to sign ticketing contracts under veiled threat that artists would otherwise be routed to different concert halls. Now it’s become difficult for venues, artists and fans to avoid Ticketmaster, which charges fees as high as 50% that many see as a ripoff.

The Ticket Fairy wants to wrestle away from Ticketmaster control of venues while giving fans ways to earn tickets for referring their friends. The startup is doing that by offering the most technologically advanced ticketing platform that not only handles sales and check-ins, but acts as a full-stack Salesforce for concerts that can analyze buyers and run ad campaigns while thwarting scalpers. Co-founder Ritesh Patel says The Ticket Fairy has increased revenue for event organizers by 15% to 25% during its private beta focused on dance music festivals.

Now after 850,000 tickets sold, it’s officially launching its ticketing suite and actively poaching venues from Eventbrite as it moves deeper into esports and conventions. With a little more scale, it will be ready to challenge Ticketmaster for lucrative clients.

Ritesh’s combination of product and engineering skills, rapid progress and charismatic passion for live events after throwing 400 of his own has attracted an impressive cadre of angel investors. They’ve delivered a $2.5 million seed round for Ticket Fairy, adding to its $485,000 pre-seed from angels like Twitch/Atrium founder Justin Kan, Twitch COO Kevin Lin and Reddit CEO Steve Huffman.

The new round includes YouTube founder Steve Chen, former Kleiner Perkins partner (and Mark’s sister) Arielle Zuckerberg and funds like 500 Startups, ex-Uber angels Fantastic Ventures, G2 Ventures, Tempo Ventures and WeFunder. It’s also scored music industry angels like Serato DJ hardware CEO AJ Bertenshaw, Spotify’s head of label licensing Niklas Lundberg, and celebrity lawyer Ken Hertz, who reps Will Smith and Gwen Stefani.

“The purpose of starting The Ticket Fairy was not to be another Eventbrite, but to reduce the risk of the person running the event so they can be profitable. We’re not just another shopping cart,” Patel says. The Ticket Fairy charges a comparable rate to Eventbrite’s $1.59 + 3.5% per ticket plus payment processing that brings it closer to 6%, but Patel insists it offers far stronger functionality.

Constantly clad in his golden disco hoodie over a Ticket Fairy t-shirt, Patel lives his product, spending late nights dancing and taking feedback at the events his clients host. He’s been a savior of SXSW the past two years, injecting the aging festival that shuts down at 2am with multi-night after-hours raves. Featuring top DJs like Pretty Lights in creative locations cab drivers don’t believe are real, The Ticket Fairy’s parties have won the hearts of music industry folks.

The Ticket Fairy co-founders. Center and inset left: Ritesh Patel. Inset right: Jigar Patel

Now the Y Combinator startup hopes its ticketing platform will do the same thanks to a slew of savvy features:

Still, the biggest barrier to adoption remains the long exclusive contracts Ticketmaster and other giants like AEG coerce venues into in the U.S. Abroad, venues typically work with multiple ticket promoters who sell from the same pool, which is why 80% of The Ticket Fairy’s business is international right now. In the U.S., ticketing is often handled by a single company, except for the 8% of tickets artists can sell however they want. That’s why The Ticket Fairy has focused on signing up non-traditional venues for festivals, trade convention halls, newly built esports arenas, as well as concert halls.

“Coming from the event promotion background, we understand the risk event organizers take in creating these experiences,” The Ticket Fairy’s co-founder and Ritesh’s brother Jigar Patel explains. “The odds of breaking even are poor and many are unable to overcome those challenges, but it is sheer passion that keeps them going in the face of financial uncertainty and multi-year losses.” As competitors’ contracts expire, The Ticket Fairy hopes to swoop in by dangling its sales-boosting tech. “We get locked out of certain things because people are locked in a contract, not because they don’t want to use our system.”

The live music industry can be brutal, though. Events can have slim margins, organizers are loathe to change their process and it’s a sales-heavy process convincing them to try new software. But while the record business has been redefined by streaming, ticketing looks a lot like it did a decade ago. That makes it ripe for disruption.

“The events industry is more important than ever, with artists making the bulk of their income from touring instead of record sales, and demand from fans for live experiences is increasing at a global level,” Jigar concludes. “When events go out of business, everybody loses, including artists and fans. Everything we do at The Ticket Fairy has that firmly in mind – we are here to keep the ecosystem alive.”

Powered by WPeMatico

Facebook is finally ready to reveal details about its cryptocurrency codenamed Libra. It’s currently scheduled for a June 18th release of a white paper explaining its cryptocurrency’s basics, according to a source who says multiple investors briefed on the project by Facebook were told that date.

Meanwhile, the company’s Head of Financial Services & Payment Partnerships for Northern Europe Laura McCracken told German magazine WirtschaftsWoche‘s Sebastian Kirsch that the white paper would debut June 18th, and that the cryptocurrency would indeed be pegged to a basket of currencies rather than a single one like the US dollar to prevent price fluctuations. Kirsch tells me “I met Laura at Money2020 Europe in Amsterdam on Tuesday” after she watched fellow Facebook payments exec Paulette Rowe’s talk. “She told me that she wasn’t involved in what David Marcus’ [Facebook Blockchain] team was doing. But that I’d have to wait until June 18th when a whitepaper was supposed to be published to get more details.” She told him she thought the date was already a publicly known fact, which it wasn’t.

Then, yesterday TechCrunch received a request for a June 18th news embargo from one of the communications managers for Facebook’s blockchain team. The Information’s Alex Heath and Jon Victor also reported yesterday that Facebook’s cryptocurrency project would launch later this month.

Facebook declined to comment on any news regarding its cryptocurrency project. There is always a chance that the announcement date could fluctuate if snafus with partners or governments arise. One source says Facebook is targeting a 2020 formal launch of the cryptocurrency

The debut of Libra or whatever Facebook decides to call it could unlock a new era of commerce and payments for the social network. It could be used to offer low or no-fee payments between friends or remittance of earnings to familys from migrant workers abroad who are often gouged by money transfer services.

Sidestepping credit card transaction fees could also allow Facebook’s cryptocurrency to offer a cheaper way to pay merchants for traditional ecommerce, or facilitate microtransactions for a la carte news articles or tipping of content creators. And a better understanding of who buys what or which brands or popular could aid Facebook in ad measurement, ranking, and targeting to amplify its core business.

Here’s what we know about Facebook’s blockchain project:

Name: Facebook will likely use the Libra codename as the public facing name for its cryptocurrency, which The Information reports won’t be called GlobalCoin as the BBC had claimed. Facebook has registed a company called Libra Networks in Switzerland for financial services, Reuters reported. Libra could be a play on the word LIBOR, an abbreviation for the London Inter-bank Offered Rate that’s used as a benchmark interest rate for borrowing between banks. LIBOR is for banks, while Libra is meant to be for the people.

Token: The cryptocurrency will be a stablecoin — a token designed to have a stable price to prevent discrepancies and complications due to price fluctuations during a payment or negotiation process. Facebook has spoken with financial institutions regarding contributing capital to form a $1 billion basket of multiple international fiat currencies and low-risk securities that will serve as collateral to stabilize the price of the coin, The Information reports. Facebook is working with various countries to pre-approve the rollout of the stablecoin.

The head of Facebook’s Blockchain team David Marcus (left) speaks at TechCrunch Disrupt 2016

Usage: Facebook’s cryptocurrency will be transferrable with zero fees via Facebook products including Messenger and WhatsApp. Facebook is working with merchants to accept the token as payment, and may offer sign-up bonuses. The Information also reports Facebook also wants to roll out physical devices for ATMs so users can exchange traditional assets for the cryptocurrency.

Team: Facebook’s blockchain project is overseen by former PayPal President and VP of Facebook Messenger David Marcus. His team includes former Instagram VP of product Kevin Weil, Facebook’s former corporate head of treasury operations Sunita Parasuraman who The Information reports will oversee the token’s treasury, and many elite engineers cherrypicked from Facebook’s ranks. They’ve been working in a dedicated part of Facebook’s headquarters off-limits to other employees to boost secrecy, though the nature of the partnerships needed for launch have led to many leaks.

Governance: Facebook is in talks to create an independent foundation to oversee its cryptocurrency, The Information reports. It’s asking companies to pay $10 million to operate a node that can validate transactions made with its cryptocurrency in exchange for a say in governance of the token. It’s possible that node operators could benefit financially too. By introducing a level of decentralization to the governance of the project, Facebook may be able to avoid regulation related to it holding too much power over a global currency.

Powered by WPeMatico

Entering into the world of Anthemis is a bit like stepping into the frame of a Wes Anderson film. Eclectic, offbeat people situated in colorful interiors? Check. A muse in the form of a renowned British-Venezuelan economist? Check. A design-forward media platform to provoke deep thought? Check. An annual summer retreat ensconced in the French Alps? Bien sûr.

Sitting atop this most unusual fintech(ish) VC is its ponytailed founder and chairman Sean Park, whose difficult-to-place accent and Philosophy professor aura belie his extensive fixed income capital markets experience. He’s joined by founder and CEO Amy Nauiokas, who in addition to being one of Fintech’s most prominent female investors also owns a high-minded film and television production company.

When Arman Tabatabai and I recently sat down with Park and Nauiokas in their New York office, the firm’s leaders were in an upbeat mood, having blown past the temporary perception-setback associated with the abrupt resignation last year of Anthemis’ former CEO Nadeem Shaikh (for more on this, read TechCrunch writer Steve O’Hear’s coverage of the situation).

And as the conversation below demonstrates, Park and Nauiokas are well poised to bring the quirk into everything they touch, which these days runs the gamut from backing companies involved in sustainable finance, advancing their home-grown media platform and preparing a soon-to-be-announced initiative elevating female entrepreneurs.

Gregg Schoenberg: With the two of you now at the helm, how does Anthemis present itself today?

Sean Park: I’ll step back and say that when Amy and I were working at big financial institutions in the noughties, we saw that the industry was going to change and that existing business models were running into their natural diminishing returns.

We tried to bring some new ideas to the organizations we were working in, but we each had epiphany moments when we realized that big organizations weren’t built to do disruptive transformation — for bad reasons, but also good reasons, too.

GS: Let’s fast forward to today, where you have several strong Fintech VCs out there. But unlike others, Anthemis puts weirdness at the heart of its model.

Yes, you’ve backed some big names like Betterment and eToro, but you’ve done other things that are farther afield. What’s the underlying thesis that supports that?

Amy Nauiokas: Whatever we do at Anthemis has to be a non-zero-sum game. It has to be for good, not for evil. So that means that we aren’t looking in any place where you see predatory opportunities to make money.

Powered by WPeMatico

Away from the limelight of urban cities, where an increasingly growing number of firms are fighting for a piece of India’s digital payments market, a South Korean startup’s app is quietly helping millions of Indians pay digitally and enjoy many financial services for the first time.

The app, called True Balance, began its life as a tool to help users easily find their mobile balance, or topping up pre-pay mobile credit. But in its four-year journey, its ambition has significantly grown beyond that. Today, it serves as a digital wallet app that helps users pay their mobile and electricity bills, and it also lets users pay later.

One thing that has not changed for the parent company of True Balance, BalanceHero, which employs less than 200 people, is its consumer focus. It is strictly catering to people in tier-two and tier-three markets — often dubbed as India 2 and India 3 — who have relatively limited access to the internet, and lower financial power. And it remains operational just in India.

Even as India is already the second largest internet market with more than 500 million users, more than half of its population remains offline. In recent years, the nation has become a battleground for Silicon Valley giants and Chinese firms that are increasingly trying to win existing users and bring the rest of the population online.

And like many other companies, BalanceHero’s bet on India is beginning to pay off. The startup told TechCrunch today that it has clocked $100 million in GMV sales and has amassed about 60 million registered users. Yongsung Yoo, a spokesperson for the startup, added that BalanceHero, which has raised $42 million to date, is also nearing profitability.

The South Korean firm’s playbook is different from many other players that are racing to claim a slice of India’s burgeoning digital payments market. True Balance competes with the likes of Paytm, MobiKwik, Google, Amazon and Walmart-owned Flipkart, though its competitors are still largely catering to the urban parts of India.

In the last two years, many firms have begun to explore smaller cities and towns, but their services are still too out-of-the-world for local residents. Raising awareness about digital services is a big challenge in such markets, Yoo said, so the startup is relying on existing users to help others make their first transactions and in paying bills.

Yoo said the startup rewards these “digital agents” with cash back and other benefits. For these digital agents, many of whom do not have a day job, True Balance has emerged as a side project to make extra money.

Later this year, Yoo said the startup, which recently also added support for UPI in its service, will open an e-commerce store on its app and also offer insurance to users. To accelerate its growth and expansion, True Balance is in the final stages of raising between $50 million to $70 million in a new round that it expects to close in July this year, Yoo said.

Powered by WPeMatico

Automattic, the company behind WordPress.com, WooCommerce, Longreads, Simplenote and a bunch of other cool things, is acquiring a small startup called Prospress. Among other things, Prospress has developed WooCommerce Subscriptions, a recurring payment solution specifically designed for WooCommerce.

Given that physical and digital subscriptions are taking over the e-commerce world, it makes sense that Automattic wants to own WooCommerce Subscriptions. Charging customers on a regular basis is one of the most painful challenges when it comes to payment.

Prospress also works on a marketing automation tool to remind customers that they have abandoned their carts, follow up, cross sell and more. The company also has a tool to test your checkout functionality before going live. After the acquisition, the Prospress team will keep iterating on its own products and join the rest of the WooCommerce team.

This is a strategic acquisition more than anything else. Prospress has around 20 employees, so it’s not going to change the face of Automattic and its team of 900 people. But it’s an important move so that Automattic can own a bigger chunk of the (e-commerce) stack.

WooCommerce competitor Shopify doesn’t provide subscriptions out of the box. You have to use third-party products, such as Bold or ReCharge.

Like WordPress, WooCommerce is an open-source project — it integrates directly with WordPress. It means that anyone can download WooCommerce and host it on their servers. And the WooCommerce ecosystem is one of the main advantages of WooCommerce compared to obscure e-commerce solutions.

Many WooCommerce users probably host their e-commerce website on WordPress.com. But by controlling the payment module, Automattic can also generate some revenue if WooCommerce users choose to use WooCommerce Subscriptions as their payment solution.

Powered by WPeMatico

Just ahead of the launch of the Apple Card, a startup that has its own take on modernizing the credit card industry, Zero, is announcing the close of its $20 million Series A. The new round of funding was led by New Enterprise Associates (NEA), and brings Zero’s total raised to date to $35 million, including both equity and debt funding.

Other investors in the round include SignalFire, Eniac Ventures, Nyca Partners and some unnamed school endowments. Zero had previously announced an $8.5 million raise in fall 2017, led by Eniac, and had raised $7 million in venture debt from Silicon Valley Bank.

Zero has a clever idea that targets millennials’ hesitance to sign up for credit cards.

Today, only 33% of millennials have a major credit card, a Bankrate survey found — largely because they’re wary of falling into the vicious debt cycle. Instead, this younger demographic often only carries a debit card. But that also means they’re missing out on credit card benefits — like points, rewards and cash back.

Zero’s idea is to offer a rewards credit card that works like debit.

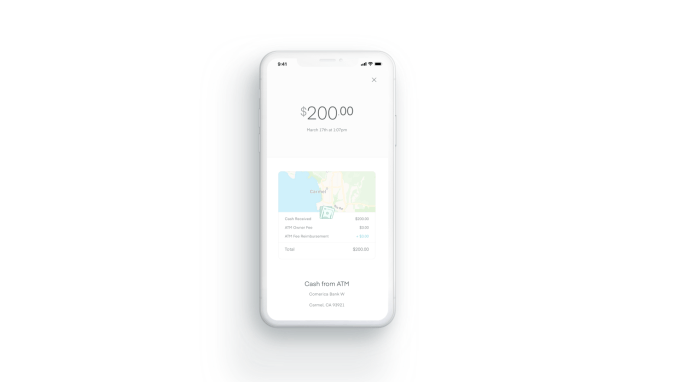

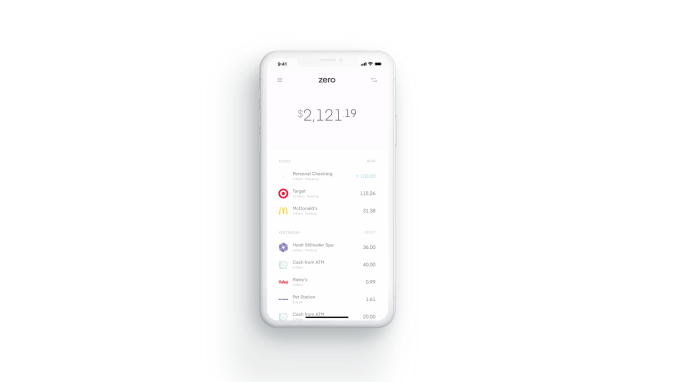

The Zerocard itself is a World Mastercard, so it earns credit card cash back. But unlike a traditional credit card, it’s combined with an FDIC-backed checking account called Zero Checking. That means Zerocard and Zero Checking work together in the app, allowing cardholders to see one net number they can spend from.

That way, they won’t make the mistake of accidentally going over budget, as is often the case with traditional credit cards, which then benefit from charging interest on the unpaid balance.

Zero co-founder and CEO Bryce Galen says he had always liked optimizing his personal finances, but didn’t see the value in overspending to chase rewards.

“People spend 10 to 15% more on average just because they’re putting it on a credit card, and not seeing where they stand all the time,” he says. “Spending 10 to 15% more to chase 1 to 2% in rewards doesn’t make sense.”

Plus, he adds, “half of all credit card points are never even redeemed.”

With Zerocard, the company does away with other credit card annoyances as well.

Zerocard doesn’t charge annual fees like many traditional credit cards do. And Zero Checking doesn’t add any additional ATM fees beyond what the ATM owner charges. It also does away with foreign transaction fees, minimum balance fees and overdraft fees — like many of today’s challenger banks.

Meanwhile, the Zero app is built with an eye toward what makes apps great.

Galen, who led product development for Zynga’s “Words with Friends” has experience in this department, while co-founder and COO Joel Washington previously co-founded car sales marketplace Shift. The executive team, combined, has backgrounds that include time at Affirm, Apple, Capital One, Dropbox, Google, Postmates, Silicon Valley Bank, Upgrade and Wells Fargo.

Overall, Zero’s design feels clean and simple, compared to the cluttered and dated apps from traditional banks. It has smart features, too, like a detailed transaction view that shows the vendor’s logo and location on a map to make it easier to recognize purchases.

“Zero creates an innovative debit-style experience, with an elegant design, and truly compelling rewards. It’s a fabulous banking experience,” said Hans Morris, managing partner of Nyca Partners and former president of Visa, Inc., in a statement. “Few people understand how complex it is to launch either a credit card or a checking account program, and I believe Zero is the first U.S. startup to launch both,” he said.

Zero launched in November 2018, but only to a small number of customers. Though officially open for business, it was functioning more like a public beta — though it didn’t call it that at the time. Meanwhile, its waitlist continued to grow.

Today, there are still 204,000 people waiting to be allowed in — something that Galen says is now going to happen.

“We haven’t launched to everyone on the waitlist yet, but we expect to within the next few weeks,” he says.

Another interesting twist on traditional credit cards is Zero’s path to card upgrades: it encourages but also rewards customers for telling their friends. By doing so, customers gain access to better-looking cards and higher cash-back percentages.

Zero customers start with a “Quartz” card offering 1% back on purchases. When a friend they refer joins, they receive a higher-level card called “Graphite” that offers 1.5% back. Two friends earns you the “Magnesium” card with 2% back and four friends gets you the “Carbon” card with 3% back. The Carbon card is also solid metal, capitalizing on the millennial trend of wanting their cards to look cool. And metal cards are in particular demand.

To receive the full cash-back rates, customers have to pay their balances in full by the due date, Zero says.

The company has partnered with Salt Lake City-based WebBank to issue the card, and deposits are held at Memphis-based Evolve Bank & Trust, an FDIC member. Zero makes money primarily on interchange and interest on deposits.

While some users may leave balances on the card that generate interest, Zero isn’t focused on that aspect of the business for revenue generation.

“Most companies in fintech today are launching undifferentiated debit cards as a feature or extension to their product for an additional engagement and monetization stream,” says Rick Yang, partner at NEA, as to why he invested.

“Zero is completely focused on their card programs and building a differentiated solution that actually provides a value proposition that resonates with consumers. We’ve also been fascinated by the growth of debit outpacing credit, and we think that our solution gives consumers the best of both worlds,” he adds.

Zero is currently iOS-only, but is working on an Android version that is expected to be ready in August.

Powered by WPeMatico

To become a global fintech player, locate your company in San Francisco and Africa.

That’s the approach of payments company Flutterwave, digital lending startup Mines, and mobile-money venture Chipper Cash—Africa-founded ventures that maintain headquarters in San Francisco and operations in Africa to tap the best of both worlds in VC, developers, clients, and the frontier of digital finance.

This arrangement wasn’t exactly coordinated across the ventures, but TechCrunch coverage picked up the trend and some common motives among these rising fintech firms.

Founded in 2016 by Nigerians Iyinoluwa Aboyeji and Olugbenga Agboola, Flutterwave has positioned itself as a global B2B payments solutions platform for companies in Africa to pay other companies on the continent and abroad.

Clients can tap its APIs and work with Flutterwave developers to customize payments applications. Existing customers include Uber, Booking.com and African e-commerce unicorn Jumia.com.

The Y-Combinator backed company is headquartered in San Francisco, runs its operations center in Nigeria, and plans to add offices in South Africa and Cameroon.

Flutterwave opened an office in Uganda in June and raised a $10 million Series A round in October. The company also plugged into ledger activity in 2018, becoming a payment processing partner to the Ripple and Stellar blockchain networks.

Powered by WPeMatico

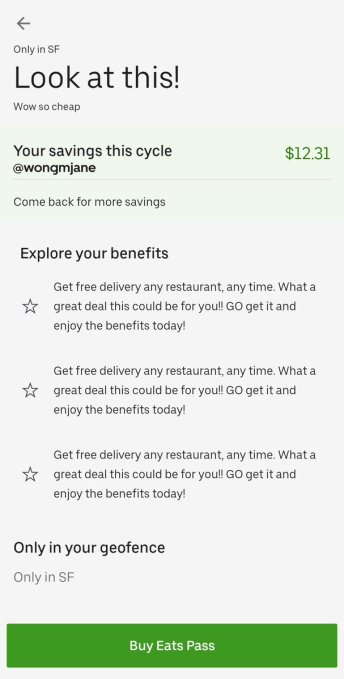

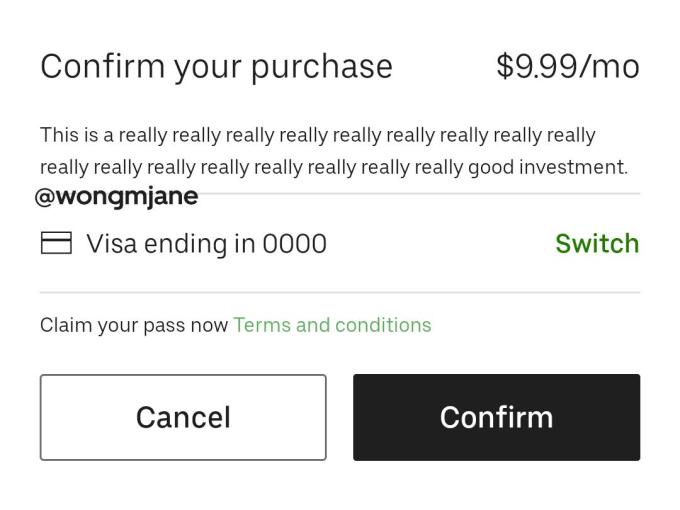

What’s the cord-cutting equivalent to ditching your kitchen? Uber’s upcoming subscription to unlimited free food delivery. Uber is preparing to launch the $9.99 per month Uber Eats Pass, according to code hidden in Uber’s Android app.

The subscription would waive Uber’s service fee that’s typically 15% of your order cost. Given that’s often $5 or more, users stand to save a lot if they order in frequently. But Uber could still earn money on menu item markups, cover costs with a flat order fee that protects against someone ordering a single taco, and, most importantly, build loyalty and scale at a time of intense food delivery competition.

The subscription would waive Uber’s service fee that’s typically 15% of your order cost. Given that’s often $5 or more, users stand to save a lot if they order in frequently. But Uber could still earn money on menu item markups, cover costs with a flat order fee that protects against someone ordering a single taco, and, most importantly, build loyalty and scale at a time of intense food delivery competition.

The Uber Eats Pass was first spotted by Jane Manchun Wong, the notorious reverse-engineering specialist who’s become a frequent TechCrunch tipster. She managed to generate screenshots from Uber’s Android app code that reveals a prototype of the feature. “Get free delivery, any restaurant, any time,” it says, showing the amount of money you could save or already saved.

An Uber spokesperson did not dispute the legitimacy of the findings and told TechCrunch, “We’re always thinking about new ways to enhance the Eats experience.” They declined to provide further details, which could hint that a launch is imminent but some details are still subject to change. For now we don’t know exactly which perks come with an Eats Pass or where it will be launching first.

At $9.99 per month, the Uber Eats Pass would cost the same and work similarly to Postmates Unlimited and DoorDash DashPass. If they all seem like good deals, you see why they’re less about immediate revenue and more about customer lock-in. You’re a lot less likely to order GrubHub or Caviar if you’ve already pre-paid to cover your Uber Eats delivery costs. And whichever apps emerge from this battle will have instituted the scale and steady behavior to raise prices or just enjoy large lifetime value from each subscriber.

Exploring new business opportunities could help perk up Uber’s share price, which closed at $41.50 today, two weeks after IPOing at an opening price of $42. There are fears that intense competition across both ridesharing and food delivery could make for an expensive road ahead for the newly public company. Any way it can gain an edge on its rivals’ users from straying to them is important. The logistics giant is already experimenting with allowing restaurants to offer discounts in exchange for promoted placement in the app, which is the first step to Uber becoming an ads company, where businesses pay for extra exposure.

If Uber combined Eats Pass with its car service subscription Ride Passes, you have the foundation for a sort of Uber Prime experience — one where you pay an upfront subscription fee that scores you perks and discounts but also makes you likely to spend a lot more on Uber. That bundle could be even more central to Uber than Amazon, which has few direct rivals in the west. People will need to eat and get around for the foreseeable future. Subsidizing loyalty now could be costly in the short-term, but poise Uber for years of lucrative business down the line.

Powered by WPeMatico

A day after India’s largest wallet app Paytm entered the credit card business, local ride-hailing giant Ola is following suit. Ola has inked a deal with state-run SBI and Visa to issue as many as 10 million credit cards in the next three and a half years, it said today.

The move will help Visa and SBI (State Bank of India) acquire more customers in India, where most transactions are still bandied out over cash. For Ola, which rivals Uber in India, the foray into credit cards represents a new avenue to monetize its customers, as TechCrunch previously reported.

With about 150 million users availing more than 2 million rides on its platform each day, Ola is sitting on a mountain of data about its users’ financial power and spends. With the card, dubbed Ola Money-SBI Credit Card, the mobility firm is also offering several discounts and savings to retain its loyal customer base.

Ola, which is nearing $6 billion in valuation and counts SoftBank and Naspers among its investors, said it will offer its credit card holders “highest cashback and rewards” in the form of Ola Money that could be redeemed for Ola rides, as well as flight and hotel bookings. There will be 7% percent cashback on cab spends, 5% on flight bookings, 20% on domestic hotel bookings (6% on international hotel bookings), 20% on more than 6,000 restaurants and 1% on all other spends.

In an interview with TechCrunch, Nitin Gupta, CEO of Ola financial services, claimed that the company was offering “five times rewards to customers” in comparison to average credit card companies. “Also, the card is a first of its kind offering that can be managed digitally through the Ola App. We are committed to creating an inclusive ecosystem where mobility and financial services go hand in hand in leading growth and development,” he said. Ola said it has already rolled out the card to some users and will invite other eligible customers to avail it.

“Mobility spends form a significant wallet share for users and we see a huge opportunity to transform their payments experience with this solution. With over 150 million digital-first consumers on our platform, Ola will be a catalyst in driving India’s digital economy with cutting edge payment solutions,” Bhavish Aggarwal, co-founder and CEO of Ola, said in a statement.

Ola appears to be following the playbook of Grab and Go-Jek, two ride-hailing services in Southeast Asian markets that have ventured into a number of businesses in recent years. Both Grab and Go-Jek offer loans, remittance and insurance to their riders, while the former also maintains its own virtual credit card. Interestingly, Uber, which also offers a credit card in some markets, has no such play in India.

The move will allow Ola to look beyond ride-hailing and food delivery, two businesses that appear to have hit a saturation point in India, said Satish Meena, an analyst with research firm Forrester.

In recent years, Ola has started to explore financial services. It offers riders “micro-insurance” that covers a range of risks, including loss of baggage and medical expenses. The company said earlier this year, it has sold more than 20 million insurances to customers. Using Ola Money to facilitate cashbacks also underscores Ola’s push to increase the adoption of its mobile wallet, which, according to estimates, lags Paytm and several other wallet and UPI payment apps.

The company has also made a major push in the electric vehicles business, which it spun off as a separate company earlier this year. In March, its EV business raised $300 million from Hyundai and Kia. The company has said that it plans to offer one million EVs by 2022. Its other EV programs include a pledge to add 10,000 rickshaws for use in cities.

Powered by WPeMatico

Paytm, India’s largest mobile wallet app, has branched out to several businesses in recent years as threat from Google and Facebook grows. On Tuesday, it added another category to the list: credit cards.

The firm, operated by One97 Communications, today unveiled Paytm First Credit Card with lofty benefits as it races to bulk up its financial offerings. The cards, issued by Citi Bank, will be the first in the country to offer unlimited, one percent cashback on purchases, Paytm claimed in a statement. The company is hoping to rope in about 25 million credit card customers in the coming months.

The penetration of credit cards remains very low in India with under 50 million people possessing one. With people conducting most of their businesses through cash in the nation, banks have little understanding of a customer’s credit history and score. And it also doesn’t help that banks in India are still wary of issuing credit cards to those who don’t perfectly fit the traditional blue collar job.

But why is a company that made its name through a mobile payment wallet open to its customers engaging with credit card companies? Paytm itself is struggling to grow its business and retain existing customers. Some of its recent major bets haven’t exactly paid off. Its ecommerce business Paytm Mall remains tiny despite bleeding money.

Yo! The First. Paytm First. pic.twitter.com/5kAxozc2IH

— Vijay Shekhar (@vijayshekhar) May 13, 2019

But more importantly, payments itself has become a commoditized space. Users park their money in Paytm and do transactions from there. Paytm makes money from this accumulated sum. This business flourished for years, especially in the months after the Indian government invalidated much of the cash in the nation. But then the government launched its own payment infrastructure called UPI, which removes the need for a middleman.

This has made payments more convenient for users, who are increasingly jumping ship. UPI apps such as PhonePe that have emerged in the last two and a half years now see more transactions than wallet apps. To make matter worse for Paytm, Google and Facebook — two companies that have larger userbase in India — have entered the payments space. Google Pay reached 100 million installs on Google Play Store recently, and WhatsApp plans a nation-wide roll out of its payment feature in India later this year.

So Paytm is now expanding its financial offerings and credit card play fits well in it. With more than 200 million active users, Paytm rivals banks on both the number of customers and volume of transaction it processes.

“Our new offering is designed to bring utmost flexibility to our customers in their digital payment options and will help spur large-ticket cashless payments,” Vijay Shekhar Sharma, chairman and CEO of One97 Communications said in a statement.

Backed by SoftBank, Alibaba, and most recently Warren Buffett’s Berkshire Hathaway, Paytm has the capital to spur the adoption of its new credit card. As part of the package, Paytm’s credit card holders will be able to avail dining, shopping, travel and other offers that Citi Bank provides to its privilege customers. In the first four months of issuing a card, the company will offer its customers discounts worth Rs 10,000 ($142) on spending of Rs 10,000.

Paytm First Credit Card will work both in India and elsewhere and support contactless transactions. Like any other credit card, customers will be able to pay back a sum in multiple monthly instalments. Paytm First Credit Card will charge users a nominal fee of Rs 500 ($7.1) that will be waived off if their spendings through the card exceeds Rs 50,000 ($710) in a year.

If the gamble works, Paytm will be able to retain some customers and convince many to do big-ticket transactions. For Citi Bank, this partnership is just an easy ploy to acquire some customers.

In the meantime, Paytm continues to aggressively expand its financial offerings. In recent years, it has launched a digital payments bank, and has started to offer prepaid Forex cards for international purchases. It also lets customers buy gold, and employers issue food allowance wallets for their staff. Last year, the company announced Paytm Money to facilitate purchase of mutual funds.

Earlier this year, the company launched Paytm First, a subscription bundle that includes access to subscriptions from other services such as Zomato, Uber, Gaana, and Eros Now. In an interview with TechCrunch late last month, Paytm’s Sharma said payments is the moat around which you can build a number of services. “Now that’s a business model… payment itself can’t make you money.”

Powered by WPeMatico