payments

Auto Added by WPeMatico

Auto Added by WPeMatico

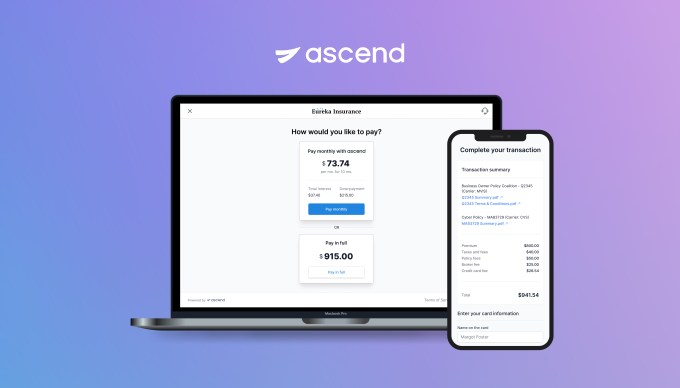

Ascend on Wednesday announced a $5.5 million seed round to further its insurance payments platform that combines financing, collections and payables.

First Round Capital led the round and was joined by Susa Ventures, FirstMark Capital, Box Group and a group of angel investors, including Coalition CEO Joshua Motta, Newfront Insurance executives Spike Lipkin and Gordon Wintrob, Vouch Insurance CEO Sam Hodges, Layr Insurance CEO Phillip Naples, Anzen Insurance CEO Max Bruner, Counterpart Insurance CEO Tanner Hackett, former Bunker Insurance CEO Chad Nitschke, SageSure executive Paul VanderMarck, Instacart co-founders Max Mullen and Brandon Leonardo and Houseparty co-founder Ben Rubin.

This is the first funding for the company that is live in 20 states. It developed payments APIs to automate end-to-end insurance payments and to offer a buy now, pay later financing option for distribution of commissions and carrier payables, something co-founder and co-CEO Andrew Wynn, said was rather unique to commercial insurance.

Wynn started the company in January 2021 with his co-founder Praveen Chekuri after working together at Instacart. They originally started Sheltr, which connected customers with trained maintenance professionals and was acquired by Hippo in 2019. While working with insurance companies they recognized how fast the insurance industry was modernizing, yet insurance sellers still struggled with customer experiences due to outdated payments processes. They started Ascend to solve that payments pain point.

The insurance industry is largely still operating on pen-and-paper — some 600 million paper checks are processed each year, Wynn said. He referred to insurance as a “spaghetti web of money movement” where payments can take up to 100 days to get to the insurance carrier from the customer as it makes its way through intermediaries. In addition, one of the only ways insurance companies can make a profit is by taking those hundreds of millions of dollars in payments and investing it.

Home and auto insurance can be broken up into payments, but the commercial side is not as customer friendly, Wynn said. Insurance is often paid in one lump sum annually, though, paying tens of thousands of dollars in one payment is not something every business customer can manage. Ascend is offering point-of-sale financing to enable insurance brokers to break up those commercial payments into monthly installments.

“Insurance carriers continue to focus on annual payments because they don’t have a choice,” he added. “They want all of their money up front so they can invest it. Our platform not only reduces the friction with payments by enabling customers to pay how they want to pay, but also helps carriers sell more insurance.”

Ascend app

Startups like Ascend aiming to disrupt the insurance industry are also attracting venture capital, with recent examples including Vouch and Marshmallow, which raised close to $100 million, while Insurify raised $100 million.

Wynn sees other companies doing verticalized payment software for other industries, like healthcare insurance, which he says is a “good sign for where the market is going.” This is where Wynn believes Ascend is competing, though some incumbents are offering premium financing, but not in the digital way Ascend is.

He intends to deploy the new funds into product development, go-to-market initiatives and new hires for its locations in New York and Palo Alto. He said the raise attracted a group of angel investors in the industry, who were looking for a product like this to help them sell more insurance versus building it from scratch.

Having only been around eight months, it is a bit early for Ascend to have some growth to discuss, but Wynn said the company signed its first customer in July and six more in the past month. The customers are big digital insurance brokerages and represent, together, $2.5 billion in premiums. He also expects to get licensed to operate as a full payment in processors in all states so the company can be in all 50 states by the end of the year.

The ultimate goal of the company is not to replace brokers, but to offer them the technology to be more efficient with their operations, Wynn said.

“Brokers are here to stay,” he added. “What will happen is that brokers who are tech-enabled will be able to serve customers nationally and run their business, collect payments, finance premiums and reduce backend operation friction.”

Bill Trenchard, partner at First Round Capital, met Wynn while he was still with Sheltr. He believes insurtech and fintech are following a similar story arc where disruptive companies are going to market with lower friction and better products and, being digital-first, are able to meet customers where they are.

By moving digital payments over to insurance, Ascend and others will lead the market, which is so big that there will be many opportunities for companies to be successful. The global commercial insurance market was valued at $692.33 billion in 2020, and expected to top $1 trillion by 2028.

Like other firms, First Round looks for team, product and market when it evaluates a potential investment and Trenchard said Ascend checked off those boxes. Not only did he like how quickly the team was moving to create momentum around themselves in terms of securing early pilots with customers, but also getting well known digital-first companies on board.

“The magic is in how to automate the underwriting, how to create a data moat and be a first mover — if you can do all three, that is great,” Trenchard said. “Instant approvals and using data to do a better job than others is a key advantage and is going to change how insurance is bought and sold.”

Powered by WPeMatico

Cross-border commerce company Zonos raised $69 million in a Series A, led by Silversmith Capital Partners, to continue building its APIs that auto classify goods and calculate an accurate total landed cost on international transactions.

St. George, Utah-based Zonos is classifying the round as a minority investment that also included individual investors Eric Rea, CEO of Podium, and Aaron Skonnard, co-founder and CEO of Pluralsight. The Series A is the first outside capital Zonos has raised since it was founded in 2009, Clint Reid, founder and CEO, told TechCrunch.

As Reid explained it, “total landed cost” refers to the duties, taxes, import and shipping fees someone from another country might pay when purchasing items from the U.S. However, it is often difficult for businesses to figure out the exact cost of those fees.

Global cross-border e-commerce was estimated to be over $400 billion in 2018, but is growing at twice the rate of domestic e-commerce. This is where Zonos comes in: The company’s APIs, apps and plugins simplify cross-border sales by providing an accurate final price a consumer pays for an item on an international purchase. Businesses can choose which one or multiple shipping carriers they want to work with and even enable customers to choose at the time of purchase.

“Businesses can’t know all of a country’s laws,” Reid added. “Our mission is to create trust in global trade. If you are transparent, you bring trust. This was traditionally thought to be a shipping problem, but it is really a technology problem.”

As part of the investment Todd MacLean, managing partner at Silversmith Capital Partners, joined the Zonos board of directors. One of the things that attracted MacLean to the company was that Reid was building a company outside of Silicon Valley and disrupting global trade far from any port.

He says while looking into international commerce, he found people wound up being charged additional fees after they have already purchased the item, leading to bad customer experiences, especially when a merchant is trying to build brand loyalty.

Even if someone chooses not to purchase the item due to the fees being too high, MacLean believes the purchasing experience will be different because the pricing and shipping information was provided up front.

“Our diligence said Zonos is the only player to take the data that exists out there and make sense of it,” MacLean said. “Customers love it — we got the most impressive customer references because this demand is already out there, and they are seeing more revenue and their customers have more loyalty because it just works.”

In fact, it is common for companies to see 25% to 30% year over year increase in sales, Reid added. He went on to say that due to fees associated with shipping, it doesn’t always mean an increase in revenue for companies. There may be a small decrease, but a longer lifetime value with customers.

Going after venture capital at this time was important to Reid, who saw global trade becoming more complex as countries added new tax laws and stopped using other trade regulations. However, it was not just about getting the funding, but finding the right partner that recognizes that this problem won’t be solved in the next five years, but will need to be in it for the long haul, which Reid said he saw in Silversmith.

The new investment provides fuel for Zonos to grow in product development and go-to-market while also expanding its worldwide team into Europe and Asia Pacific. Eighteen months ago, the company had 30 employees, and now there are over 100. It also has more than 1,500 customers around the world and provides them with millions of landed cost quotes every day.

“Right now, we are the leader for APIs in cross-border e-commerce, but we need to also be the technology leader regardless of the industry,” Reid added. “We can’t just accept that we are good enough, we need to be better at doing this. We are looking at expanding into additional markets because it is more than just servicing U.S. companies, but need to be where our customers are.”

Powered by WPeMatico

SellersFunding secured $166.5 million in a combination of Series A equity funding and a credit facility to continue developing its technology and payments platforms for e-commerce businesses.

Northzone led the round and was joined by Endeavor Catalyst and Fasanara. SellersFunding CEO Ricardo Pero did not disclose the funding breakdown, but did say the company previously raised two seed rounds for a total of $40 million in equity and more than $100 million in credit facilities, including one that the company was expanding to $200 million.

SellersFunding, with offices in Florida, New York and London, created a digital platform that delivers financial tools and resources to streamline global commerce for thousands of marketplaces, including working capital, cross-border cash management, tax solutions and business valuation.

Pero got the idea for the company after spending 20 years in the financial industry. He left JP Morgan in 2016 with a drive to start his own company. He was consulting for a friend selling on Amazon who asked him to help make sense of Amazon’s fees and to review the next year’s budget because the friend was struggling to keep up with growth.

“I helped him address the fees issue, but when I went to talk to traditional lenders, I found that they have no clue about e-commerce and the needs of SMEs,” he said.

In addition to being a lending source for businesses selling on these marketplaces, SellersFunding leverages sales data provided by the marketplaces and e-commerce platforms to create sales and cash flow estimates based on the credit limits given to clients so that owners can better understand the fees they are paying and make more informed decisions.

He founded the company in 2017, and today has over 30,000 registered users and is approaching $10 billion in sales volume that is feeding data into SellersFunding’s daily models. The company makes money as both a lender and on fees it charges for payments collected by its customers. Merchants can collect money from marketplaces and pay their suppliers in local or foreign currency.

SellersFunding has consistently grown 300% year over year, Pero said. As such, he intends to use the new funding to scale globally, expand the team, create a marketing budget and look for two small acquisitions in the U.S. and Europe.

The company will continue to invest on the payments side and to promote cross-border payments.

“When I look at the payments landscape, companies are competing on pricing and I don’t think we will ever have a focus there, but instead will compete on customer experience,” Pero added. “Our core business will always be lending and our core investments will be payments and technology, but then we will extend to other services that our clients want.”

With an eye on expanding internationally, it fit to bring on Northzone as a partner, he added. The venture firm is based in Europe and was of a similar vision for thinking globally.

Jeppe Zink, general partner at Northzone, said via email that Pero and his team “are the most experienced in this category” and are building a category leader that is “more experienced and understanding of the lending side than its competitors.”

“We have seen this massive rise in e-shopping, most of the new ones coming from marketplaces like Amazon and Shopify, and if you look at the sellers, thousands are small businesses sourcing their goods which means that they are very important customers,” Zink added. “Normal banks like Barclay can’t check credit. SellersFinding is helping small businesses get this credit, and rightly so. In the same way we thought neobanks won with accounts created when it comes to delivering credit and banking products, they are nowhere to be found yet.”

Powered by WPeMatico

When Anik Khan graduated from college, his first job was working on credit cards and business expenses at Accenture. There, he found that someone could bring in a couple of thousand dollars just by having the right credit cards and following the rewards and promotions.

It was back in 2017 when he and David Gao got the idea for his company MaxRewards, a digital wallet app that manages credit cards and automatically activates benefits like rewards, cashback offers and monthly credits. It also makes recommendations at the point of purchase on which card would yield the best reward for that purchase.

Going after the some 83% of Americans that have a credit card, the app version was officially launched in 2019, and now the Atlanta-based company is announcing a $3 million seed round co-led by Dundee Venture Capital and Calano Ventures. Also backing the company are Techstars, Fintech Ventures Fund, Service Provider Capital and Fleetcor president Nick Izquierdo.

Tracking his own credit cards manually prior to MaxRewards, Khan recalled in one year, getting $16,000 in rewards. However, utilizing those benefits was time-consuming and difficult, because the rewards and savings aren’t always made evident by the credit card companies.

“Other companies have tried to do something similar, but the issue is you don’t have the reward information or the offers,” Khan told TechCrunch. “If you were to aggregate this information, you still would have to activate all of these things and use them before they expired.”

Users connect their accounts and when they make a purchase, their location is cross-referenced with the merchant and an algorithm is applied to tell the user which card to use. The average app user has six credit cards.

MaxRewards is free to download and use, and the majority of the app’s functionalities are free. Users who want additional features, like the auto activation or rewards, can join MaxRewards Gold and are given the opportunity to choose their own monthly price — the average is over $25 per month — based on the value they expect to gain, Khan said.

MaxRewards offers and benefits. Image Credits: MaxRewards

Ron Watson, partner at Dundee, said his firm invests in seed-stage companies between the coasts and is interested in consumer and e-commerce companies. Watson said he was impressed with what MaxRewards has been able to do with a team of three. He also relates to the company’s mission, having grown up in a lower, middle-class family that did not frequently go on vacations.

When he got his first job and was suddenly flying everywhere, he recalls building up so many rewards to the point where he was able to go on a vacation to Hawaii and only spend maybe $100, he said.

“I used to put my points into a spreadsheet, but as I got older and had kids, I realized how hard it was for the average person to do that and how important it is to have automation,” Watson said. “I downloaded the app, and on the first day, saved $20.”

The company is often compared to NerdWallet or Mint, but in terms of functionality, Khan said he feels MaxRewards is unique due to its credit card system connectors. Rather than rely on third-party aggregators to discover the rewards, MaxRewards leverages its own proprietary connectors to card systems.

There are hundreds of thousands of offers to be discovered, and consumers are asking for even more features, so Khan decided it was time to go after seed funding. He had raised a small seed, about $200,000, from his time at Techstars, but the new funding will enable him to add to his team of three people. He expects to be at 20 by the end of the year. Khan also wants to accelerate its user acquisition, product improvement and compliance.

Next up, the company is going to automate rewards and savings across additional platforms like debit cards, payment apps and cashback apps, as well as create browser extensions and a web app. Khan also wants to do more on the education side with regard to using credit cards in a smart manner.

Arron Solano, managing partner at Calano, met Khan through Techstars and said he is an advocate for using credit cards in the right way. His firm was looking for a company like MaxRewards.

“During our first call, I remember telling my partner that Anik was a bulldog who knew what he was talking about, especially at that stage,” Solano added. “He had strong team members, his vision lined up well and that checked off a massive box for us. He energized us and showed he could find a market with insanely high ‘super users.’ ”

Powered by WPeMatico

PayPal Holdings, the U.S. fintech company, announced an acquisition of Paidy, a Japanese buy now, pay later (BNPL) service platform, for approximately $2.7 billion (300 billion yen), mostly in cash, to enhance its business in Japan.

The transaction completion, including the regulatory approval, is expected in the fourth quarter of 2021.

After the acquisition, the Japan-based company will continue to operate its existing business and maintain the brand while the leaders, Paidy’s president and CEO Riku Sugie and founder and executive chairman Russell Cummer, keep their positions.

Japan is the third largest e-commerce market in the world, and so this is a significant move by PayPal to gain more market share both in the country and the region, specifically in the area of providing deferred payment services as an alternative to credit cards.

PayPal has long played nice with payment cards — users can upload details of their cards to PayPal and use it as a kind of digital wallet to manage how they pay for things online through it — but it got its start actually as a payment platform in itself, where people could pay into and out of PayPal accounts. Paidy is, in that sense, a strengthening of PayPal’s first-party rails, providing a way to “own” that flow of money on its own infrastructure, not involving the card networks.

Paidy is basically a two-sided payments service, acting as a middleman between consumers and merchants in Japan. Using machine learning it determines the creditworthiness of a consumer related to a particular purchase, and then it underwrites those transactions in seconds, guaranteeing payments to merchants. Consumers then make deferred payment to Paidy for those goods.

Paidy’s platform, which offers a monthly payment installment service branded “3-Pay”, enables shoppers to make purchases online and then pay for them each month in a consolidated bill at a convenience store or via bank transfer.

“Paidy pioneered buy now, pay later solutions tailored to the Japanese market and quickly grew to become the leading service, developing a sizable two-sided platform of consumers and merchants,” said Peter Kenevan, vice president, head of Japan at PayPal.

Paidy has more than 6 million registered users, and the plan is to integrate PayPal and other digital and QR wallets with Paidy Link to connect further online and offline merchants.

In April 2021, the Japan-based company launched Paidy Link, allowing users to link digital wallets with their Paidy account. PayPal was the first digital wallet partner to integrate with Paidy Link.

“PayPal was a founding partner for Paidy Link and we look forward to looking together to create even more value,” Sugie said in a statement.

“Japan has been a vibrant environment for our growth to date and we’re honored to have our team’s hard work and potential recognized by a global leader. Together with PayPal, we will be able to further achieve our mission of taking the hassle out of shopping,” Cummer said.

Powered by WPeMatico

TheCut, a technology platform designed to handle back-end operations for barbers, raised $4.5 million in new funding.

Nextgen Venture Partners led the round and was joined by Elevate Ventures, Singh Capital and Leadout Capital. The latest funding gives theCut $5.35 million in total funding since the company was founded in 2016, founder Obi Omile Jr. told TechCrunch.

Omile and Kush Patel created the mobile app that provides information and reviews on barbers for potential customers while also managing appointments, mobile payments and pricing on the back end for barbers.

“Kush and I both had terrible experiences with haircuts, and decided to build an app to help find good barbers,” Omile said. “We found there were great barbers, but no way to discover them. You can do a Google search, but it doesn’t list the individual barber. With theCut, you can discover an individual barber and discover if they are a great fit for you and won’t screw up your hair.”

The app also enables barbers, perhaps for the first time, to have a list of clients and keep notes and photos of hair styles, as well as track visits and spending. By providing payments, barbers can also leverage digital trends to provide additional services and extras to bring in more revenue. On the customer side, there is a search function with barber profile, photos of their work, ratings and reviews, a list of service offerings and pricing.

Omile said there are 400,000 to 600,000 barbers in the U.S., and it is one of the fastest-growth markets. As a result, the new funding will be used to hire additional talent, marketing and to grow the business across the country.

“We’ve gotten to a place where we are hitting our stride and seeing business catapulting, so we are in hiring mode,” he added.

Indeed, the company generated more than $500 million in revenue for barbers since its launch and is adding over 100,000 users each month. In addition, the app averages 1.5 million appointment bookings each month.

Next up, Omile wants to build out some new features like a digital store and the ability to process more physical payments by rolling out a card reader for in-person payments. TheCut will also focus on enabling barbers to have more personal relationships with their customers.

“We are building software to empower people to be the best version of themselves, in this case barbers,” he added. “The relationship with customers is an opportunity for the barber to make specific recommendations on products and create a grooming experience.”

As part of the investment, Leadout founder and managing partner Ali Rosenthal joined the company’s board of directors. She said Omile and Patel are the kind of founders that venture capitalists look for — experts in their markets and data-driven technologists.

“They had done so much with so little by the time we met them,” Rosenthal added. “They are creating a passionate community and set of modern, tech-driven features that are tailored to the needs of their customers.”

Powered by WPeMatico

Itamar Jobani was a software developer working for a medical company and “hated that time of the month” when he had to use the company’s chosen reimbursement tool.

“It was full of friction and as part of the company’s wellness team, I felt an urge to take care of the employee experience and find a better tool,” Jobani told TechCrunch. “I looked for something, but didn’t find it, so I tried to build it myself.”

What resulted was PayEm, an Israeli company he founded with Omer Rimoch in 2019 to be a spend and procurement platform for high-growth and multinational organizations. Today, it announced $27 million in funding that includes $7 million in seed funding, led by Pitango First and NFX, with participation by LocalGlobe and Fresh Fund, as well as $20 million in Series A funding led by Glilot+.

The company’s technology automates the reimbursement, procurement, accounts payable and credit card workflows to manage all of the requests and invoices, while also creating bills and sending payments to over 200 territories in 130 currencies.

It gives company finance teams a real-time look at what items employees are asking for funds to buy, and what is actually being spent. For example, teams can submit a request and go through an approval flow that can be customized with purchasing codes tied to a description of the transaction. At the same time, all transactions are continuously reconciled versus having to spend hours at the end of the month going through paperwork.

“Organizations are running in a more democratized way with teams buying things on behalf of the organization,” Jobani said. “We built a platform to cater to those needs, so it’s like a disbursement platform instead of a finance team always being in charge.”

The global B2B payments market is valued at $120 trillion annually and is expected to reach $200 trillion by 2028, according to payment industry newsletter Nilson Report. PayEm is among many B2B payments startups attracting venture capital — for example, last month, Nium announced a $200 million in Series D funding at a $1 billion valuation. Paystand raised $50 million in Series C funding to make B2B payments cashless, while Dwolla raised $21 million for its API that allows companies to build and facilitate fast payments.

Meanwhile, PayEm itself saw accelerated growth in the second quarter of 2021, including increasing its transaction volume by four times over the previous quarter and generating millions of dollars in revenue. It now boasts a list of hundreds of customers like Fiverr, JFrog and Next Insurance. It also launched new features like the ability to create corporate cards.

The company, which also has an office in New York, has 40 employees currently, and the new funds will enable the company to triple its headcount, focusing on hiring in the United States, and to bring additional features and payment capabilities to market.

“Each person can have a budget and a time frame for making the purchase, while accounting still feels in control,” Jobani added. “Everyone now has the full context and the right budget line item.”

Powered by WPeMatico

Embedded fintech company Zeal secured $13 million in Series A funding to continue developing its platform for building individualized payroll products.

Spark Capital led the Series A, with participation from Commerce Ventures and a group of individual investors, including Marqeta CEO Jason Gardner and CRO Omri Dahan, Robinhood founder Vlad Tenev, UltimateSoftware executives Mitch Dauerman and Bob Manne and Namely founder Matt Straz. The latest round now gives the company $14.6 million in total funding, which includes a $1.6 million seed round in 2020, CEO Kirti Shenoy told TechCrunch.

The Bay Area company’s origin was as Puzzl, a payment processing startup for the gig economy, founded in 2018 by Shenoy and CTO Pranab Krishnan. It was part of Y Combinator’s 2019 cohort. The pair had to pivot the company after needing to move some of its thousands of 1099 contractors to W2 employee status.

They went looking for payroll processors that could handle high volumes of payroll automatically, like ADP or Paycor, but found they didn’t match some of the capabilities Shenoy and Krishnan wanted, including to pay workers daily and customize earning components.

To ensure other companies didn’t run into the same problem, they decided to build a payroll API that enables their customers to build their own payroll products, even being able to pay their workers everyday. Traditionally, companies would layer together antiquated third-party payroll tools and spend millions of dollars on consulting fees. Zeal’s API tool modernizes the payroll process and takes on the payroll liability while managing the back-end payment logistics, Shenoy said.

Currently, enterprises use Zeal to pay large volumes of workers and keep payment data on their own native systems, while software platforms that sell business-to-business services use Zeal to build their own payroll product to sell to their customers.

“Our mission is to touch every American paycheck with our tax and payment technology, ensuring that American employees are paid correctly and efficiently,” Krishnan said.

And that is a complex goal: there are 200 million American employees, over $8.8 trillion of payroll is processed annually in the U.S. and the country’s 11,000 tax jurisdictions produce over 25,000 income tax code changes a year.

Meanwhile, Shenoy cited IRS data that showed more than 40% of small and medium businesses pay at least one payroll penalty per year. That was one of the drivers for Zeal’s latest product, the Abacus gross-to-net calculator, which payroll companies can use to ensure they are compliant in paying their income taxes.

The co-founders intend to use the new funding to build out their team and strengthen compliance measures to ensure its track record with enterprises.

“We are starting to win more enterprise deals and moving millions of dollars each day,” Shenoy said. “This has been a legacy space for so long, so companies want to work with a provider to move fast.”

Shenoy predicts that more companies will shift to hyper-customized experiences in the next five to 10 years. Whereas the default was a company like ADP, companies will want to control their own data and build products so their customers can do everything payroll-related from one platform.

As part of the investment, Spark Capital’s partner Natalie Sandman has joined Zeal’s board of directors. The firm previously invested in other embedded fintech companies like Affirm and Marqeta, and she thinks there are new experiences in the sector that APIs can unlock.

Sandman felt the payroll-building pain points herself when she worked at Zenefits. At the time, the company was trying to do the same thing, but there were no APIs to connect with. There were all of these spreadsheets to transfer data, but one wrong deduction would trickle down and cause a tax penalty.

Shenoy and Krishnan are both “customer-obsessed,” she said, and are balancing speed with thoughtfulness when it comes to understanding how their customers want to build payroll products.

She is seeing a macro shift to audience-driven human resources where bringing new employees online will mean embedding them into products that will be more valuable versus the traditional spreadsheet.

“To me, it is a no-brainer that APIs provide flexibility in the way wages and deductions need to be made,” Sandman said. “You can lose trust in your employer. Payroll is at the deepest trust point and where you want transparency and a robust solution to solve that need.”

Powered by WPeMatico

Tuna is on a mission to “fine tune” the payments space in Latin America and has raised two seed rounds totaling $3 million, led by Canary and by Atlantico.

Alex Tabor, Paul Ascher and Juan Pascual met each other on the engineering team of Peixe Urbano, a company Tabor co-founded and he referred to as a “Groupon for Brazil.” While there, they came up with a way to use A/B testing to create a way of dealing with payments in different markets.

They eventually left Peixe Urbano and started Tuna in 2019 to make their own payment product that enables merchants to use A/B testing of credit card processors and anti-fraud providers to optimize their payments processing with one integration and a no-code interface.

Tabor explained that the e-commerce landscape in Latin America was consolidated, meaning few banks controlled more of the market. The address verification system merchants use to verify a purchaser is who they say they are, involves sending information to a bank that is returned to the merchant with a score of whether that match is legitimate.

“In the U.S., that score is used to determine if the purchaser is legit, but they didn’t implement that in Latin America,” he added. “Instead, merchants in LatAm have to tap into other organizations that have that data.”

That process involves manual analysis and constant adjusting due to fraud. Instead, Tuna’s A/B tests between processors and anti-fraud providers in real time and provides a guarantee that a decision to swap providers is based on objective data that considers all components of performance, like approval rates, and not just fees.

Over the past year, the company added 12 customers and saw its revenue increase 15%. It boasts a customer list that includes the large Brazilian fashion chain Riachuelo, and its platform integrates with others including VTEX, Magento and WooCommerce.

The share of e-commerce in overall retail is less than 10% in Latin America. Marcos Toledo, Canary’s managing partner, said via email that e-commerce in LatAm is currently at an inflexion point: not only has the global pandemic driven more online purchases, but also fintech innovation that has occurred in recent years.

In Brazil alone, e-commerce sales grew 73.88% in 2020, but Toledo said there was much room for improvement. What Tuna is building will help companies navigate the situation and make it easier for more customers to buy online.

Toledo met the Tuna team from his partner, Julio Vasconcellos, who was one of the co-founders of Peixe Urbano. When the firm heard that the other Tuna co-founders were starting a business that was applying some of the optimization methods they had created at Peixe Urbano, but for every company, they saw it as an opportunity to get involved.

“The vast tech expertise that Alex, Paul and Juan bring to a very technical business is something that we really admire, as well as their vision to create a solution that can impact companies throughout Latin America,” Toledo said. “The no-code solution that Tuna is building is exciting because it is scalable and can help companies not only get better margins, but also drive their developers to other efforts — and developers have been a very scarce workforce in the region.”

To meet demand for an e-commerce industry that surpassed $200 billion in 2020, Tuna plans to use the new funding to build out its team and grow outbound customer success and R&D, Tabor said.

Up next, he wants to be able to show traction in payments optimization and facilitators in Brazil before moving on to other countries. He has identified Mexico, Colombia and Argentina as potential new markets.

Powered by WPeMatico

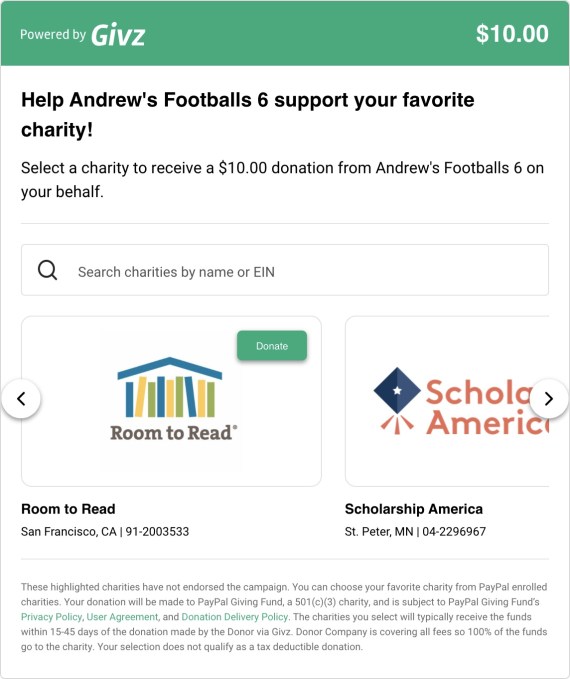

Givz, which has developed an API-powered platform that gives brands a way to convert discounts into donations, has raised $3 million in seed funding.

Eniac and Accomplice co-led the financing for the New York-based startup. Additional investors include Supernode Ventures, Claude Wasserstein of Fine Day, Phoenix Club and Dylan Whitman.

Givz was founded in 2017 to make charitable giving more accessible and convenient for the masses. In March 2020, right before the COVID-19 pandemic hit, the company pivoted from B2C to B2B and used the technology rails it had built to create the e-commerce marketing platform that Givz is today.

The company aims to drive “full-price purchasing behavior” by giving consumers the ability to convert the money they would be saving if getting a discount, and donating it to their favorite charities.

Prior to the funding, Givz had been working with more than 80 enterprise, mid-market and SMB retail and e-commerce clients such as H&M, Tom Brady’s TB12, Seedlip and Terez, and accumulated more than 40,000 individual users. Since the shift last year, the company has helped drive more than $1 million to 1,100 charities, according to CEO and founder Andrew Forman.

It just launched on Shopify, which Forman says will give the startup access to the 1.7 million retailers that use Shopify as their e-commerce platform.

Givz operates under the premise that “donation-driven marketing” consistently outperforms discounts and costs less, “making it an attractive addition” to corporate marketing.

“We are creating a new marketing category and generating the largest sustainable charitable giving platform in the process,” he told TechCrunch.

An example of a company using Givz can be found in Tervis, which offered customers “For every $50 you spend, you’ll receive $15 to give to the charity of your choice.”

“They used Givz technology to allow consumers to choose the charity of their choice and make a turnkey disbursement to hundreds of charities,” Forman explained. “They saw a 20% lift in website conversion and a 17% increase in average order value as a result of this offer.”

Image Credits: Givz

Currently, Givz has eight employees with plans to more than double that number over the next year.

The company plans to use the new capital toward that hiring, and to do some marketing of its own.

“We also want to explore the full potential around the consumer behavior data we collect,” Forman said.

In the short term, Givz is focused on “Shopify growth” with direct to consumer brands.

“But we have successful use cases and huge potential with enterprise retailers and financial institutions,” Forman told TechCrunch. “In the future, we have our sights set on restaurants, the gaming industry and global expansion. I believe that using personalized donations to incentivize consumer behavior has endless application across industries, verticals and continents.”

Eniac partner Vic Singh said that there’s been a trend of brands experimenting with different ways to target the socially conscious consumer.

“We believe Givz’s donation-driven marketing platform offers brands the best way to attract the socially conscious consumer while elevating their brand, moving more inventory and driving increased order value rather than simplistic traditional discounting,” he added.

Accomplice’s TJ Mahony said that both he and Singh believed SMS would emerge as a new marketing category, which led to early investments in Attentive and Postscript, respectively.

“We both saw a similar opportunity with Givz,” he wrote via e-mail. “Discounting is a well worn marketing muscle, but it’s detrimental to the brand, margins and customer expectations. We believe continuous impact marketing becomes the alternative to discounting and marketers will begin to build teams and budget around thoughtful and persistent giving strategies.”

Powered by WPeMatico