monzo

Auto Added by WPeMatico

Auto Added by WPeMatico

Assembling a startup team is harder than assembling 10 IKEA dressers, and the stakes are much, much higher.

Starting with the assumption that 90% of startups will fail and the most successful ones take an average of six years to IPO, founders must make careful decisions about whom they invite to join the core team.

Will that stellar engineer become a great CTO? Should your product person be opinionated or a team player? Are you even the best choice for CEO?

ThoughtSpot CEO Sudheesh Nair shared some of his thoughts about building a sturdy leadership team and drafted a thorough checklist for entrepreneurs who are putting a crew together. His initial advice?

“Investors love founder-CEOs, and founders are often fantastic candidates for this role. But not everyone can do it well, and more importantly, not everyone wants to.”

In a related article, Gregg Adkin, VP and managing director at Dell Technologies Capital, shared the framework he’s developed for helping founders set up their board.

Choosing the right mix of people can impact everything from fundraising to hiring: “Investors often ask founders about their board [because] it says a lot about their character, their judgment and their willingness to be challenged,” he writes.

Full Extra Crunch articles are only available to members.

Use discount code ECFriday to save 20% off a one- or two-year subscription.

Miranda Halpern spoke to Amsterdam-based coach Ward van Gasteren for our latest growth marketing interview, which is free to read.

In their discussion, van Gasteren addressed misconceptions about growth hacking, the mistakes most startups are likely to make, and the distinctions he draws between growth hacking and growth marketing:

“Growth hacking is great to kickstart growth, test new opportunities and see what tactics work,” he tells us.

“Marketers should be there to continue where the growth hackers left off: Build out those strategies, maintain customer engagement, and keep tactics fresh and relevant.”

Thanks very much for reading Extra Crunch this week; I hope you have a great weekend.

Walter Thompson

Senior Editor, TechCrunch

Image Credits: sureeporn / Getty Images

In his first column since returning to TechCrunch, reporter Ryan Lawler considered the potential ripples Square’s purchase of Afterpay may send across the pond of buy now, pay later startups.

For commentary and perspective, he interviewed:

The investors he spoke to agreed that deferring payments helps drive e-commerce, “but scale matters and long-term margins look slim for BNPL startups,” reports Ryan.

Image Credits: Ivan Bajic (opens in a new window) / Getty Images

Businesses have been deploying AI solutions for 20 years, but few have achieved the outstanding gains in efficiency and profitability promised when the technology first appeared.

But there’s a burgeoning new generation of enterprise AI, Eshwar Belani, an operating partner at Symphony AI, writes in a guest column.

“Companies on the leading edge of AI innovation have advanced to the next generation, which will define the coming decade of big data, analytics and automation — Enterprise AI 2.0.”

Image Credits: Joan Cros Garcia-Corbis (opens in a new window) / Getty Images

Over the next 18 months, one technologist says the increased adoption of embodied artificial intelligence will open a path to superintelligence — incredibly powerful software that dwarfs anything the human mind could produce.

“All the crazy Boston Dynamics videos of robots jumping, dancing, balancing and running are examples of embodied AI,” says Chris Nicholson, founder and CEO of Pathmind, which uses deep reinforcement learning to optimize industrial operations and supply chains.

“The field is moving fast and, in this revolution, you can dance.”

Image Credits: Nigel Sussman (opens in a new window)

The Exchange looks at the valuations of public insurtech companies and considers what that means for startups — but from a slightly different perspective.

“We’d typically riff on the new values of public neoinsurance companies and use that data to work our way into a guess concerning what the price declines might mean for related startups,” Alex Wilhelm writes. “Taking public-market data and using it to better understand private markets is pretty much the national pastime of this column.

“Not today.”

Image Credits: Anastassiia (opens in a new window) / Getty Images

The fact that the globe is awash in venture capital should not be news to readers of this newsletter.

For founders, it means more than just fat checks, Kunal Lunawat, the co-founder and managing partner of Agya Ventures, writes in a guest column.

“Founders would be well served to go back to the basics and focus on the principles of fundraising when determining who sits on their cap table.”

Image Credits: Nigel Sussman (opens in a new window)

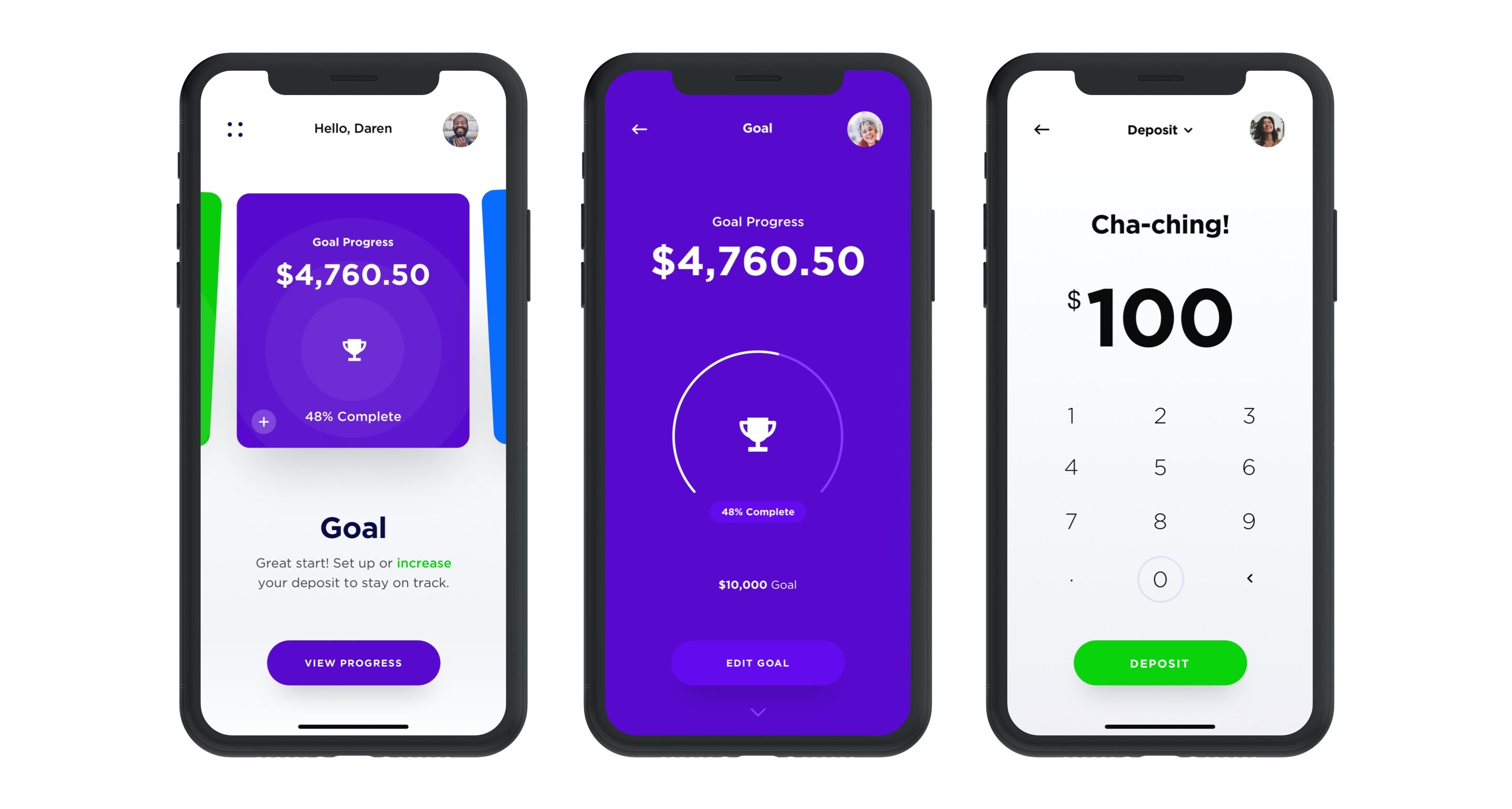

Alex Wilhelm checks in on results from Starling Bank and Monzo to see what the neobanks’ most recent financial figures say about the state of neobanks overall.

“Although some neobanks are managing to clean up their ledgers and work toward profits — or reach profitability — not all are in the black,” he notes.

But among those that are?

“At least a portion of the neobanking world is financially stable enough to consider public offerings.”

Image Credits: MicroStockHub (opens in a new window)/ Getty Images

The red-hot venture capital market may give founders lots of investors to choose from, but the most important thing (if you can be choosy) is being able to trust and rely on your investors, Ripple Ventures’ Matt Cohen and True’s Tony Conrad write in a guest column.

“This … new dynamic is forcing founders to be extremely selective about exactly who is sitting around their mentorship table,” they write.

“It’s simply not possible to have numerous deep and meaningful relationships to extract maximum value at the early stage from seasoned investors.”

Image Credits: A-Digit (opens in a new window) / Getty Images

Assembling a board of directors is not merely about finding individuals who can aid your early-stage journey, Gregg Adkin, the vice president and managing director at Dell Technologies Capital, writes in a guest column.

The composition of the board can also impact your fundraising.

“Investors often ask founders about their board [because] it says a lot about their character, their judgment and their willingness to be challenged,” he writes.

Adkins offers a framework he calls “SPIFS” — for strategy, people, image, finance and systems for compliance — to aid founders in setting up a board.

Image Credits: Nigel Sussman (opens in a new window)

In the wake of Deliveroo’s plans to abandon the Spanish market after the country passed legislation requiring companies dependent on gig workers to hire employees, Alex Wilhelm wondered about the battle for smaller markets and whether third place is sufficient.

“One company exiting a market is not a big deal, but we were curious about Deliveroo’s comments regarding the need for market leadership — or something close to it — to warrant continued investment,” he writes for The Exchange.

“Is this the common reality for startups battling for market position, no matter if those markets are cities or countries?”

Powered by WPeMatico

The global venture capital bet on neobanks is massive. London-based Starling Bank has raised more than $900 million, per Crunchbase. The same data source indicates that Chime has raised $1.5 billion. Monzo has raised nearly $650 million. And the list goes on: E-commerce-focused neobank Juni raised $21.5 million last month. Novo, an SMB-focused neobank, raised $41 million in June. Nubank has raised $2.3 billion. And FairMoney has locked down more than $50 million.

On and on and on.

The Exchange explores startups, markets and money.

Read it every morning on Extra Crunch or get The Exchange newsletter every Saturday.

But despite our general inclination to lump banking-focused fintech providers that serve consumers, business customers or both into a single bucket, there’s wide divergence in how the various neobank players are performing in the market.

Back in August 2020, The Exchange noted that many neobanks were racking up steep losses. Our read at the time was that the capital being poured into the fintech category was being invested aggressively in the name of growth. Based on recent results, that view is holding up.

But not all neobanks are the unprofitable enterprises that they once were. Chime indicated in September 2020 that it generates positive, unadjusted EBITDA. That’s a stricter profit metric than the one that Lyft used recently to claim its ascendance into the realm of profitable companies; Lyft posted positive adjusted EBITDA in its most recent quarter, but burned cash to fund its operations and posted a wide net loss in the period.

But not all neobanks are the unprofitable enterprises that they once were. Chime indicated in September 2020 that it generates positive, unadjusted EBITDA. That’s a stricter profit metric than the one that Lyft used recently to claim its ascendance into the realm of profitable companies; Lyft posted positive adjusted EBITDA in its most recent quarter, but burned cash to fund its operations and posted a wide net loss in the period.

And Starling Bank reached what it describes as profitable territory in October 2020. Things have changed since our first look into neobank results.

The trend of positive neobank news continued this June, when Revolut reported its recent financial performance. The company did post rather negative aggregate results for the 2020 period. But when we drilled down into its quarterly results, we saw the picture of a fintech company scaling its gross margins and revenues while nearly reaching adjusted net income neutrality by Q4 2020. We were impressed.

This morning, let’s add to our running dig into neobank results by parsing recently released data from Starling Bank and Monzo. As we’ll see, although some neobanks are managing to clean up their ledgers and work toward profits — or reach profitability — not all are in the black.

Powered by WPeMatico

Lower, an Ohio-based home finance platform, announced today it has raised $100 million in a Series A funding round led by Accel.

This round is notable for a number of reasons. First off, it’s a large Series A even by today’s standards. The financing also marks the previously bootstrapped Lower’s first external round of funding in its seven-year history. Lower is also something that is kind of rare these days in the startup world: profitable. Silicon Valley-based Accel has a history of backing profitable, bootstrapped companies, having also led large Series A rounds for the likes of 1Password, Atlassian, Qualtrics, Webflow, Tenable and Galileo (which went on to be acquired by SoFi).

In fact, Galileo founder Clay Wilkes introduced the VC firm to Dan Snyder, Lower’s founder and CEO. The two companies have a few things in common besides being profitable: they were both bootstrapped for years before taking institutional capital and both have headquarters outside of Silicon Valley.

“We were immediately intrigued because Ohio-based Lower echoes both of these themes,” said Accel partner John Locke, who led the firm’s investment in Lower and is taking a seat on the company’s board as part of the investment. “Like Galileo, Lower will be one of the most successful bootstrapped fintech companies globally. The combination of a company built in a nontraditional region across the globe and a bootstrapped company reminds us of [other] companies we have partnered with for a large Series A.”

There were other unnamed participants in the round, but Accel provided the “majority” of the investment, according to Lower.

Snyder co-founded Lower in 2014 with the goal of making the home-buying process simpler for consumers. The company launched with Homeside, its retail brand that Snyder describes as “a tech-leveraged retail mortgage bank” that works with realtors and builders, among others.

In 2018, the company launched the website for Lower, its direct-to-consumer digital lending brand with the mission of making its platform a one-stop shop where consumers can go online to save for a home, obtain or refinance a mortgage and get insurance through its marketplace. This year, it launched the Lower mobile app with a savings account.

Sitting (L to R): Co-founders Dan Snyder, Grayson Hanes

Standing (L to R): Co-founders Mike Baynes, Chris Miller

Not pictured: Robert Tyson; Image credit: Lower

Over the years, Lower has funded billions of dollars in loans and notched an impressive $300 million in revenue in 2020 after doubling revenue every year, according to Snyder.

“Our history is maybe a little atypical of fintech companies today,” he told TechCrunch. “We’ve had a view going back to the start of the company that we wanted to run it profitably. That’s been one of our pillars, so that’s what we’ve done. Also, we all grew up in the mortgage industry, so we saw firsthand the size of the market, but also how broken it was, so we wanted to change it.”

In launching the direct-to-consumer digital lending brand, the company was working to make the homebuying process more “digital, transparent and easier for consumers to access,” Snyder said.

At the same time, the company didn’t want to lose the human touch.

“We tried to design the app flow in a way where you can get as far along as you can in the application but if you want, at any point in time, to talk or chat with someone, we’re available,” Snyder added.

Image Credits: Lower

Lower’s typical customer is the millennial and now Gen Z who’s aspiring to own their first home, according to Snyder.

“They might be thinking, ‘OK, I might be living in an apartment now, but in the next few years I’m going to meet someone and/or have a child and I want to unlock the investment that is a home,’” he told TechCrunch. “And we’ll help them on that journey.”

Lower’s recently launched new app offers a deposit account it’s dubbed “HomeFund.” The interest-bearing, FDIC-insured deposit account offers a 0.75% Annual Percentage Yield and is designed to help consumers save for a home with a “dollar-for-dollar match in rewards” up to the first $1,000 saved, Snyder said.

Lower works with more than 35 major insurance carriers nationally, including Nationwide, Liberty Mutual and Allstate. It has more than 1,600 employees, about half of which are based in Lower’s home state. That’s up from about 650 employees in June of 2020.

Looking ahead, the company plans to add more services and has an “aggressive roadmap” for adding new features to its platform. Today, for example, Lower sells primarily to Fannie Mae and Freddie Mac. And while it services the majority of its loans, like many large lenders, it uses a subservicer. That will change, however, in early 2022, when Lower intends to launch its own native servicing platform.

And while the company intends to continue to run profitably, Snyder said he and his co-founders “think the time is now to gain share.”

“We want to become a global brand, raise money and gain market share,” he added. “We’re going to continue to double down on product and build out our capabilities. We are the best-kept secret in fintech and plan to change that with smart branding, advertising and sponsorships.”

And last but not least, Lower is eyeing the public markets as part of its longer-term roadmap.

“Ultimately, we know we can build a great public company,” Snyder told TechCrunch. “We’re of the scale to be a public company right now, but we’re going to keep our heads down and we’re going to keep building for the next few years and then I think we can be in a spot to be a strong public business.”

Accel’s Locke points out that in the U.S., mortgage and home finance are among the largest financial service markets, and they have primarily been handled by large banks.

“For most consumers, getting a mortgage through these banks continues to be an overly complex, slow-moving process,” Locke told TechCrunch. “We believe by providing consumers a great mobile experience, Lower will gain share from incumbent banks, in the same way that companies like Monzo have in banking or Venmo in payments or Trade Republic and Robinhood in stock trading.”

Powered by WPeMatico

Monzo founder Tom Blomfield is departing the U.K. challenger bank entirely at the end of the month, staff were informed earlier today.

Blomfield held the role of CEO until May last year when he assumed the newly created title of president and resigned from the Monzo board. However, having been given the time and space to consider his long-term future at the bank he helped create six years ago, and with a refreshed executive team now in place, he says it is time to “hand over the baton”.

In a brief but candid telephone interview, Blomfield also revealed that, as well as being unhappy during the last couple of years as CEO when the company scaled well beyond a “scrappy startup”, the pandemic and subsequent lockdowns exacerbated pressures placed on his own mental well-being. “I’m very happy to talk about what’s gone on with me, because I don’t think people do it enough”, he says.

“I stopped enjoying my role probably about two years ago… as we grew from a scrappy startup that was iterating and building stuff people really love, into a really important U.K. bank. I’m not saying that one is better than the other, just that the things I enjoy in life is working with small groups of passionate people to start and grow stuff from scratch, and create something customers love. And I think that’s a really valuable skill but also taking on a bank that’s three, four, five million customers and turning it into a 10 or 20 million customer bank and getting to profitability and IPOing it, I think those are huge exciting challenges, just honestly not ones that I found that I was interested in or particularly good at”.

In early 2019 after realising he was “doing too much and not enjoying it,” Blomfield began talking to Monzo investor Eileen Burbidge of Passion Capital, and Monzo Chair Gary Hoffman, about changing roles and how he needed more help. Then, he says, “COVID just exacerbated things,” a period when Monzo also had to cut staff, shutter its Las Vegas office and raise bridge funding in a highly publicised down round.

“I think [for] a lot of people in the world — and you and I have spoken about this — going through a pandemic, going through lockdown and the isolation involved in that has an impact on people’s mental health,” says Blomfield. “I don’t think I was any different, so I was really struggling. I had a really, really supportive exec team around me and a really supportive set of investors on board and I was really grateful that when I put my hand up and said, ‘I need help,’ they were super receptive to that”.

Blomfield also comes clean about his role as president, a title that was intended as a way to provide the time and space for him to get well and figure out if he would return longer-term to Monzo or depart entirely. Contrary to rumours, Blomfield says he wasn’t pushed out by investors. Instead, the Monzo board actually put pressure on him to remain as CEO longer than he wanted or perhaps should have (a version of events corroborated by my own sources). “When I took that president role, it was not certain one way or another what would happen,” Blomfield says, apologising in case I felt I was misled when I reported the news.

(The truth is, within weeks of running that news piece, I knew it was far from certain Blomfield would ever return, with multiple sources, including people close to and worried about Blomfield, confiding in me how burned out the Monzo founder was. As weeks turned into months and following additional sourcing, I had enough information to write a follow-up story much earlier but chose to wait until a formal decision was taken.)

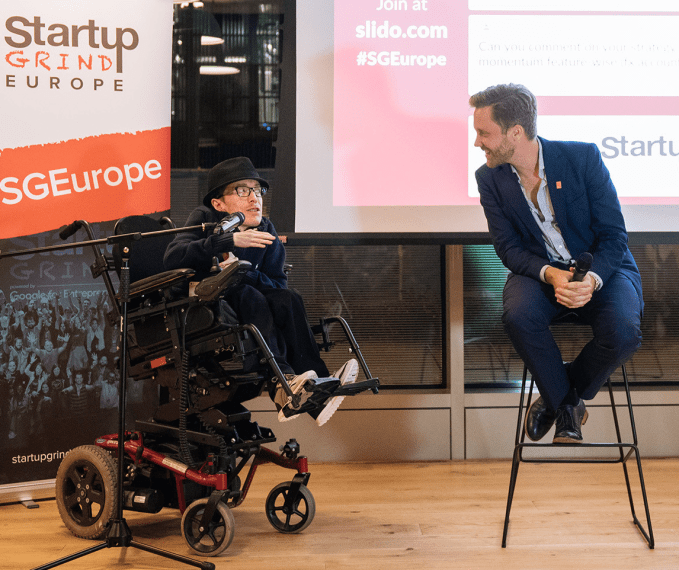

TechCrunch’s Steve O’Hear interviewing Monzo’s Tom Blomfield. Image Credits: Startup Grind

Meanwhile, Blomfield describes his resignation as a Monzo employee as “bitter-sweet,” and is keen to praise what the Monzo team has already achieved, including since his much-reduced involvement. “I think the team has done phenomenally well over the last year or so in really difficult circumstances,” he says. In particular, he cites Monzo’s new CEO TS Anil as doing a “phenomenal” job, while describing Sujata Bhatia, who joined as COO last year, as “an absolute machine, a real operator”.

To that end, Monzo now has almost 5 million customers, up from 1.3 million in 2019. Monzo’s total weekly revenue is now 30% higher than pre-pandemic, helped no doubt by over 100,000 paid subscribers across Monzo Plus and Premium in the last five months (sources tell me the company surpassed £2 million in weekly revenue in December for the first time in its history). Albeit at a lower valuation, the challenger bank also raised £125 million from new and existing investors during the pandemic.

Blomfield also says that Anil and Bhatia and other members of the Monzo executive team have specific skills — that he simply doesn’t have — related to scaling and managing a bank approaching 5 million customers. And even if he did, he has learned the hard way that there are aspects of running a large company that not everyone enjoys.

“Going from a CEO where you’re front and centre dealing with all of the different pressures every day to a much lighter role is a huge huge weight off my shoulders and has given me the time and space to recover”, he adds. “I’m now feeling pretty great. I’m enjoying life again”.

As for what’s next for Blomfield, he says he wants to “chill out” for a bit and perhaps take a holiday. He’s also finishing his vaccination training so that he can volunteer to help deliver the U.K.’s national COVID-19 vaccination rollout. A recent tweet by Blomfield about a side project also led to speculation that he has begun a new venture. Not true, says Blomfield, telling me it was a five-day project designed to get back into coding and play with a robotic 2D printer. And while he’s very much left Monzo, he says he’ll continue cheering on the company from the outside.

Powered by WPeMatico

Productivity software has been getting a major re-examination this year, and human resources platforms — used for hiring, firing, paying and managing employees — have been no exception. Today, one of the startups that’s built what it believes is the next generation of how HR should and will work is announcing a big fundraise, underscoring its own growth and the focus on the category.

Hibob, the startup behind the HR platform that goes by the name of “bob” (the company name is pronounced, “Hi, Bob!”), has picked up $70 million in funding at a valuation that reliable sources close to the company tell us is around $500 million.

“Our mission is to modernize HR technology,” said Ronni Zehavi, Hibob’s CEO, who co-founded the company with Israel David. “We are a people management platform for how people work today. Whether that’s remotely or physically collaborative, our customers face challenges with work. We believe that the HR platforms of the future will not be clunky systems, annoying, giant platforms. We believe it should be different. We are a system of engagement rather than record.”

The Series B is being led by SEEK and Israel Growth Partners, with participation also from Bessemer Venture Partners, Battery Ventures, Eight Roads Ventures, Arbor Ventures, Presidio Ventures, Entree Capital, Cerca Partners and Perpetual Partners, the same group that also backed Hibob in its last round (a Series A extension) in 2019. It has raised $124 million to date.

The company has its roots in Israel but these days describes its headquarters as London and New York, and the funding comes on the back of strong growth in multiple markets. In an interview, Zehavi said that Hibob specialises in the mid-market customers and says that it has more than 1,000 of them currently on its books across the U.S., Europe and Asia, including Monzo, Revolut, Happy Socks, ironSource, Receipt Bank, Fiverr, Gong and VaynerMedia. In the last year Hibob has had “triple-digit” year-on-year growth (it didn’t specify what those digits are).

Human resources has never been at the more glamorous end of how a company works, and it can sometimes even be looked on with some disdain. However, HR has found itself in a new spotlight in 2020, the year when every company — whether one based around people sitting at desks or in more interactive and active environments — had to change how it worked.

That might have involved sending everyone home to sign in from offices possibly made out of corners of bedrooms or kitchens, or that might have involved a vastly different set of practices in terms of when and where workers showed up and how they interacted with people once they did. But regardless of the implementations, they all involved a team of people who needed to be linked together, still feeling connected and managed; and sometimes hired, furloughed, or let go.

That focus has started to reveal the strains of how some legacy systems worked, with older systems built to consider little more than creating an employee identity number that could then be tracked for payroll and other purposes.

Hibob — Zehavi said they chose the name after the person who owned the bob.com domain wanted too much to sell it, but they liked “bob” for the actual product — takes an approach from the ground up that is in line with how many people work today, balancing different software and apps depending on what they are doing, and linking them up by way of integrations: its own includes Slack, Microsoft Teams and Mercer, and other packages that are popular with HR departments.

While it covers all of the necessary HR bases like payroll and further compensation, onboarding, managing time off and benefits, it further brings in a variety of other features that help build out bigger profiles of users, such as performance and culture, with the ability for peers, managers and workers themselves to provide feedback to enhance their own engagement with the company, and for the company to have a better idea of how they are fitting into the organization, and what might need more attention in the future.

That then links into a bigger organizational chart and conceptual charts that highlight strong performers, those who are possible flight risks, those who are leaders and so on. While there have been a number of others in the HR world that have built standalone apps that cover some of these features (for example, 15five was early to spot the value of a platform that made it much easier to set goals and provide feedback), what’s notable here is how they are all folded into one system together.

The end effect, as you can see here, looks less like word salad and more interactive, graphic interfaces that are presumably a lot more enjoyable and at least easier to use for HR people themselves.

The importance for investors has been that the product and the startup has identified the opportunity, but has delivered not just more engagement, but a strong piece of software that still provides the essentials.

“This is certainly not a Workday,” said Adam Fisher, a partner at Bessemer, in an interview. “Our overall thesis has been that HR is only growing in importance. And while engagement is super important, that opportunity is not enough to create the market.”

The end result is a platform that has a significant shot at building in even more over time. For example, another large area that has been seeing traction in the world of enterprise and B2B software is employee training. Specifically, enterprise learning systems are creating another way to help keep people not only up to speed on important aspects of how they work, but also engaged at a time when connections are under strain.

“Training, a SuccessFactors -style offering, is definitely in our road map,” said Zehavi, who noted they are adding new features all the time. The latest has been compensation, sometimes known as merit increase cycles. “That is a very complex issue and requires deeper integrations finance and the CFO’s office. We streamlined it and made it easy to use. We launched two months ago and it’s on fire. After learning and development there are other modules also down the road.”

Powered by WPeMatico

JoomPay, a startup with a similar product to PayPal-owned Venmo in the U.S., is set to launch in Europe shortly after being granted a Luxembourg Electronic Money Institution (EMI) license. The app allows people to send and receive money with anyone, instantly and for free. “Venmo me” has become a common phrase in the U.S., where people use it to split bills in restaurants or similar instances. Venmo is in common use in the U.S., but it’s not available in Europe, although dozens of other innovative mobile peer to peer transfer options exist, such as Revolut, N26, Monese and Monzo. The waitlist for the app’s beta is open now (iOS, Android).

Europe leads the world’s instant payments industry, with $18 trillion in worldwide volume predicted by 2025, up from $3 trillion in 2020 — a growth of more than 500%. Western Europe — and COVID-19 — is now driving that innovation and will account for 38% of instant payment transaction value by 2025. While Europe lacks simple peer-to-peer payments solutions such as Venmo or Square Cash App in the U.S., challenger banks have stepped up to provide similar kinds of services. JoomPay’s opportunity lies in being able to be a middle-man between these various banking systems.

Shopping app Joom, which has been downloaded 150 million times in Europe, has spun-off JoomPay to solve this problem. The app allows users to send and receive money from any person, regardless of whether they use JoomPay or not — and you only need to know their email or the phone number. JoomPay connects to any existing debit/credit card or a bank account. It also provides its users with a European IBAN and an optional free JoomPay card with cashback and bonuses.

Yuri Alekseev, CEO and co-founder of JoomPay, said: “Since COVID-19 started, we’ve seen a significant decline in cash usage. People can’t meet as easily as before but still need to send money, and we offer a viable alternative.”

JoomPay may have an uphill struggle. Its main competitors in Europe are the huge TransferWise, Paysend and, of course, PayPal itself.

Powered by WPeMatico

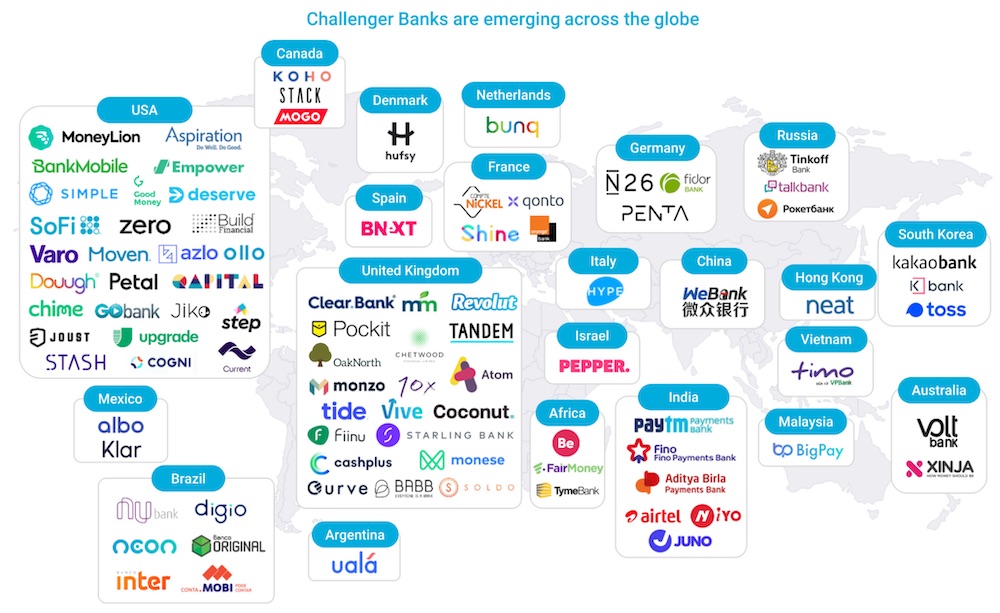

The neobank, or digital bank, phenomenon continues to take the world by storm, with global winners, from Brazil’s Nubank valued at $10 billion and Berlin’s N26 valued at $3.5 billion, to Chime, now valued at $14.5 billion as the most valuable consumer fintech in the United States.

Neobanks have led the charge of the $3.6 billion in venture capital funding for consumer fintech startups this year. And as the coronavirus-fueled acceleration of digital transformation continues, it seems the digital bank is here to stay, with some estimates pointing to neobanks reaching 60 million customers in North America and Europe by the end of 2020, and surpassing 145 million by 2024.

The space is also becoming more crowded, a trend which will only accelerate with fintech eating the world and creating greater infrastructure that enables any company to include a bank account as a product extension.

FT Partners Fintech Industry Research, January 2020

As a result, neobanks are not a monolithic model and not all are created equal. Looking underneath the hood of business models across the globe reveals remarkable operational differences and highlights specific features that are more likely to succeed in the long-term.

Today there are five distinct models that are leading globally:

Interchange-led: Relies on payments revenue, sourced through interchange as the revenue driver. Every time a customer uses the neobank’s card as a payment method they get paid [e.g. Chime / US; Neon (hybrid of 1 & 2) / Brazil].

Credit-led: Leverages a credit-first model, starting off with a credit card or similar offering, and later providing a bank account [e.g. Nubank, Neon (hybrid of 1 & 2) / Brazil].

Powered by WPeMatico

Venture capitalists and other investors have poured capital into fintech startups around the world in recent years, including a record number of rounds worth $100 million or more in the second quarter of 2020. In Q2 2020 venture-backed fintech startups raised 28 nine-figure rounds, underscoring the scale of the bet investors are making on fintech’s long-term success.

The Exchange explores startups, markets and money. You can read it every morning on Extra Crunch, or get The Exchange newsletter every Saturday.

Inside that fintech wave are various hubs of activity, including payments tech, investing and banking. That last category has helped give rise to so-called neobanks, startup banking entities that offer mobile-first, consumer-friendly banking tools and services. Given the old-fashioned nature of banking in many countries (and how far out of reach banking remains for many) neobanks have seen strong uptake by users in recent years.

And the startup cohort has raised oceans of capital to help fuel its growth. In America, Chime was most recently valued at $5.8 billion after raising hundreds of millions in late 2019. More recently, neobank Revolut added $80 million to its Q1 2020 round worth $500 million. Revolut is also worth north of $5 billion. Monzo is well-funded (albeit at a recent valuation reduction), Latin America-focused NuBank is worth $10 billion, according to Crunchbase, Starling recently raised another £40 million, while Germany’s N26 is worth over $3 billion after its most recent nine-figure round.

From the fundraising perspective, then, neobanks are killing the game. And thanks to recent tailwinds from the COVID-19 pandemic that have bolstered interest in savings-related products, many of the same entities could be enjoying a strong year thus far. But recent self-reporting of some neobank’s 2019-era results details ample red ink — perhaps more than we might have anticipated.

From the fundraising perspective, then, neobanks are killing the game. And thanks to recent tailwinds from the COVID-19 pandemic that have bolstered interest in savings-related products, many of the same entities could be enjoying a strong year thus far. But recent self-reporting of some neobank’s 2019-era results details ample red ink — perhaps more than we might have anticipated.

Of course, startups don’t raise money for fun; they raise it to invest it in their operations and drive scale. So, we knew that these megafundraisers were losing money on purpose. All the same, let’s peek at the economics of several neobanks, as their now dated and thus not at all current results can provide useful context on two points: Why investors are excited to put their capital to work in neobanks, and why neobanks always seem to have another check to announce.

To prevent my receiving unhappy emails from irked fans of these companies, please bear in mind that we’re looking several quarters back when observing the following results.

It would be lovely to have more recent data, but with European neobanks reporting their — roughly — 2019 results in recent weeks, this is what we have. We are going to parse the numbers, but we will not conflate past performance with current results. We do not know much about 2020 neobank financial performance.

Anyhoo, to the numbers. You can read the full documents from Monzo here, Starling here (or here, if that link is struggling) and Revolut here.

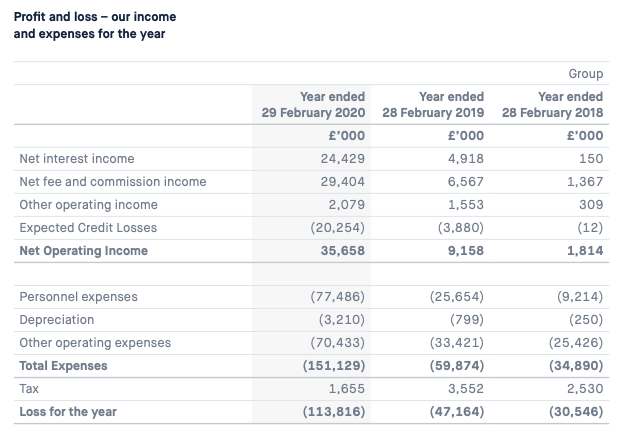

Let’s start with Monzo, which has a clear set of figures for us to peek at:

Image Credits: Monzo

Powered by WPeMatico

Monzo, the U.K. challenger bank with more than 4 million customers, has confirmed it has closed £60 million in top-up funding.

Backing the round are existing investors Y Combinator, General Catalyst, Accel, Stripe, Goodwater, Orange, Thrive and Passion Capital, along with new investors Reference Capital and Vanderbilt University.

One of fintech’s worst-kept secrets, the down round sees the bank take a 40% hit in its paper pre-money valuation compared to its previous round, now priced at £1.24 billion.

That’s likely a reflection of the current funding climate amidst the coronavirus crisis, with Monzo having to raise a bridge round at quite possibly the worst time.

I also understand from sources that a number of Monzo’s later-stage investors played hardball, in a bid to force down the challenger bank’s ticket price, perhaps after investing at the height of the funding market pre-COVID-19. What is also interesting about the new round is that the share price is the same as the bank’s last equity crowdfund, meaning that the most recent armchair investors haven’t seen a paper loss.

Monzo is also disclosing that its business banking product has now reached 25,000 signups. Launched officially in March, the business bank account is aimed at sold traders and SMEs, with both free and premium paid-for versions available, offering various feature sets.

Meanwhile, it has been a turbulent time for Monzo, as it, along with many other fintech companies, tries to insulate itself from the coronavirus crisis and resulting economic downturn.

Planned layoffs in the U.K. were communicated internally earlier this month — up to 120, but now thought to be around 80. It followed earlier U.S. layoffs and the shuttering of its Las Vegas-based customer support office, and almost 300 U.K. staff being furloughed.

Like other banks and fintechs, the coronavirus crisis has resulted in Monzo seeing customer card spend reduce at home and (of course) abroad, meaning it is generating significantly less revenue from interchange fees. The bank has also postponed the launch of premium paid-for consumer accounts, one of only a handful of known planned revenue streams, alongside lending, of course, and the more recent business banking.

Separately, in May, Monzo co-founder Tom Blomfield announced internally that he was stepping down as CEO of the U.K. challenger bank to take up the newly created role of president. His replacement is current U.S. CEO TS Anil, who now also holds the title of “Monzo UK Bank CEO,” subject to regulatory approval.

Powered by WPeMatico

More than five years after starting the company, Monzo co-founder Tom Blomfield is stepping down as CEO of the U.K. challenger bank to take up the newly created role of president.

Current U.S. CEO, TS Anil, will become the new “Monzo UK Bank CEO,” subject to regulatory approval, and for now will hold both U.K. and U.S. roles.

Anil previously held exec roles at Visa, Standard Chartered Bank and Citi, and therefore brings a ton of banking and financial services experience. This includes things like dealing with regulators and overseeing a large corporate structure, two things a scale-up challenger bank like Monzo, with more than 4 million customers and over 1,500 staff, requires.

The thinking behind Blomfield’s move to president is a startup cliché but also likely holds water; he’ll be able to spend more time doing the things he enjoys most (and is arguably best at), such as focusing on the longer-term vision, product and how Monzo can stay close to and best serve customers. Meanwhile, Anil — and, in the future, other country-specific CEOs — can do the day to day, more regulated aspects of running a bank.

In a brief call with Blomfield just moments ago, he told me he had been thinking about a transition into a different role for about 18 months, but it wasn’t until much more recently that a formal decision was taken.

“I went through all the stuff I love about my job, and it was all the stuff I did in the first two or three years,” he said. “And I went through all the stuff that drains me, and it’s all the stuff I’ve done in the last two years, honestly. Things I think TS is awesome at.”

Although it is unlikely that a huge amount will change immediately, Blomfield says he hopes that he’ll be able to spend a “bunch more time doing the stuff I really, really love, which is community, talking to customers, helping develop the product proposition, long-term vision, and talking to journalists, like you Steve, obviously, and try to unwind my involvement a little bit in more formal regulated banking activities.”

Meanwhile, it has been somewhat of a turbulent time for Monzo in recent months, as it, along with many other fintech companies, has attempted to insulate itself from the coronavirus crisis and resulting economic downturn.

Last month, I reported that Monzo was shuttering its customer support office in Las Vegas, seeing 165 customer support staff in the U.S. lose their jobs. And just a few weeks earlier, we reported that the bank was furloughing up to 295 staff under the U.K.’s Coronavirus Job Retention Scheme. In addition, the senior management team and the board has volunteered to take a 25% cut in salary, and co-founder and CEO Tom Blomfield has decided not to take a salary for the next 12 months.

Like other banks and fintechs, the coronavirus crisis has resulted in Monzo seeing customer card spend reduce at home and (of course) abroad, meaning it is generating significantly less revenue from interchange fees. The bank has also postponed the launch of premium paid-for consumer accounts, one of only a handful of known planned revenue streams, alongside lending, of course.

And just last week, it was reported that Monzo is closing in on £70-80 million in top up funding, to help extend its coronavirus crisis runaway. However, as new and some existing investors play hardball, the company has reportedly had to accept a 40% reduction in its previously £2 billion valuation as part of its last funding round last June, with a new valuation of £1.25 billion.

With that said, it’s not all been bad news. Monzo recently launched business accounts, many of which are revenue generating, with both free and paid tiers. It also recruited Sujata Bhatia, a former American Express executive in Europe, as its new COO.

And, hopefully, in his new role as president, Blomfield will sound re-energised next time I call him.

Powered by WPeMatico