monzo

Auto Added by WPeMatico

Auto Added by WPeMatico

Consumer fintech startups were massively successful in 2019, attracting millions of new users and disrupting traditional retail banks and financial services with mobile-first, consumer-oriented products. Despite the economic downturn in public markets and the massive wave of cuts at public and private companies in recent weeks, fintech startups have been raising a ton of money.

It feels like they’re all building a war chest to survive the economic winter as traditional banks continue to iterate so they can catch up and offer more user-friendly services. This is not the time to raise fees, slow down on product development or plans to acquire new users.

Back in January, I looked at challenger banks and their growth trajectories, but since then, they have managed to attract even more customers. According to the most recent figures:

And that’s without mentioning Starling Bank, Atom Bank, Bunq, Bnext, Paysend, etc. At some point, there will be as many challenger banks as non-challenger banks — perhaps we shouldn’t call them challenger banks anymore.

Beyond these startups, trading app Robinhood recently reached 13 million users, international payments startup TransferWise has 7 million customers and cryptocurrency exchange Coinbase has 30 million users.

Powered by WPeMatico

More personnel changes are afoot at Monzo, as the U.K. challenger bank continues to bolster its leadership team.

Specifically, TechCrunch has learned that Sujata Bhatia, a former American Express executive in Europe, has been recruited as Monzo’s new Chief Operating Officer, replacing previous COO Tom Foster-Carter (who left the bank rather suddenly in November to found a startup of his own). Monzo confirmed Bhatia’s appointment, which is still subject to regulator approval, and I understand she is due to start the COO role in late June.

Prior to Monzo, Bhatia spent almost 16 years at American Express. Her most recent position at Amex was Senior Vice President for Global Merchant Services Europe. Before that she was Senior Vice President of Global Strategy and Capabilities, where, according to her LinkedIn profile, she lead a team of 400 people across 23 global markets.

Bhatia’s appointment follows the recruitment of Mike Hudack, the former CTO of Deliveroo and most recently a founding partner at London venture capital firm Blossom Capital. He joined Monzo in March as the challenger bank’s new Chief Product Officer. Going in the opposite direction was Meri Williams, Monzo’s Chief Technical Officer, who parted ways with the bank a few weeks later citing her wish to voluntarily help with “cost-cutting measures.”

Meanwhile, Bhatia joins Monzo at a somewhat turbulent time for the challenger bank, as it, along with many other fintech companies, attempts to insulate itself from the coronavirus crisis and resulting economic downturn, meaning that the new COO will likely need to hit the ground running.

Last month, I reported that Monzo was shuttering its customer support office in Las Vegas, seeing 165 customer support staff in the U.S. lose their jobs. And just a few weeks earlier, we reported that the bank was furloughing up to 295 staff under the U.K.’s Coronavirus Job Retention Scheme. In addition, the senior management team and the board has volunteered to take a 25% cut in salary, and co-founder and CEO Tom Blomfield has decided not to take a salary for the next twelve months.

Like other banks and fintechs, the coronavirus crisis has resulted in Monzo seeing customer card spend reduce at home and (of course) abroad, meaning it is generating significantly less revenue from interchange fees. The bank has also postponed the launch of premium paid-for consumer accounts, one of only a handful of known planned revenue streams, alongside lending, of course.

With that said, Monzo recently launched business accounts, many of which are revenue generating, with both free and paid tiers. I understand from sources that the number of business accounts opened to date already stands at approaching 20,000.

Related to this, having originally missed out on state aid via the capability and innovation fund designed to introduce more competition in SME banking, Monzo now has a second potential bite of the apple after previous grant winners Metro and Nationwide are returning the money.

As always, watch this space.

Powered by WPeMatico

Layoffs have struck the startup world swiftly, hurting hospitality and travel startups, as well as recruitment and scooter companies. New data shows that some of those layoffs, brought on by COVID-19, might be disproportionately impacting satellite campuses.

By nature, satellite offices are secondary to a startup’s headquarters. Opening smaller offices is a strategic move when a company gets a fresh round of funding or wants to expand to a new market. We’ve seen satellite offices pop up in cities like Portland, Phoenix or Austin, which has satellite offices for Apple, Facebook and Oracle, for example.

While most layoffs are coming from companies whose headquarters are located in the main entrepreneurial hubs of the Bay area and New York, the actual staff members are located in the satellite cities, according to data from Layoffs.fyi, a tracker created by former Y Combinator grad Roger Lee.

EasyPost in San Francisco laid off 75 employees, nearly all in Salt Lake City and Louisville. U.K.-based Challenger bank Monzo laid off 165 customer support employees recently in Las Vegas.

Toast, based in Boston, laid off 1,300 employees, or 50% of its entire staff. Per Layoffs.fyi data, 12% of those layoffs were in Omaha, and another 10% were in Chicago.

KeepTruckin, based in San Francisco and last valued at $1.25 billion, laid off around 350 employees, and 33% of those employees were located in Nashville or Chicago.

These numbers are only a fraction of the total layoffs across the country, as Layoffs.fyi’s data set only includes publicly disclosed actions and tips. But even if the data is just serving as an anecdotal snapshot, it’s an important one to note.

Once the economy does recover to a new normal, it’s unclear whether HQ cities or satellite cities will be in a better position to bounce back. We caught up with some investors in Boston, a top startup hub that has recently faced its own flurry of layoffs, to hear their thoughts.

According to Lily Lyman, a partner at Boston-based venture capital firm Underscore, satellite offices are often where a company might locate the sales, customer success and business development staff. Logistically, those roles are the most vulnerable as consumer activity slows. For a lot of businesses, there are no sales and deals to be done right now.

“[These roles are getting] disproportionately affected in [reduction of forces] as companies expect a slowdown on the commercial side,” Lyman said. “While a logical decision to extend the cash runway, it does come with the risk that this withdrawal can damage relationships with customers that may be hard to recover.”

Not everyone sees cuts hitting satellite offices the hardest. Michael Skok, another partner at Underscore, said that “in some cases, we’ve seen that satellite offices are established in emerging markets which come with cost savings, so these offices may actually be more protected in these times.” In other words, if you’re cutting costs, San Francisco employee expenses might be higher than Denver employee expenses by sheer nature of the former having exorbitantly high living costs. Revolution Ventures, which invests in startups in emerging tech scenes, said it has not heard about satellite office layoffs from its portfolio as of recently.

And finally, to put it crassly, layoffs in a non-HQ city might quell some of the negative signaling that founders and venture capitalists are trying so hard to avoid (well, most of them at least). Slimming down operations is becoming a proactive response, not a reactive strategy as the pandemic continues to evolve.

Today’s data reminds us that layoffs are rarely an isolated occurrence, and staff cuts appear to be landing harder on less robust tech ecosystems.

Powered by WPeMatico

This week, Extra Crunch hosted a call with General Catalyst managing director Niko Bonatsos to discuss a number of startup topics, including what the novel coronavirus is doing to investing in the Valley, as well as his thoughts on robotics, homeschooling, edtech, SMBs, international investing and what he’s looking to see today in startups. Joining me on the live call was my fellow Equity host Alex Wilhelm and a couple of dozen EC members.

If you missed this conference call for EC members, don’t fret: We’ll have more of these to come in this era of work-from-home. In the meantime, here is a lightly edited transcript, along with a recording of the call if you’d like to listen in.

Powered by WPeMatico

Two years ago, we created the Matrix FinTech Index to highlight what we saw as the beginnings of a 10+ year mega innovation wave in financial services.

The trillion-dollar financial services industry was going to be turned on its head over the next decade, and we were just getting started. At the time, the top 10 publicly traded U.S. fintech companies had just surpassed the $100 billion mark in terms of total market capitalization, 12 unicorns had emerged in the category, and the U.S. VC industry had just poured in $6.7B — a record at the time.

As we predicted last year, the innovation cycle continues, and we are transitioning into its mid-phase. So what happened in U.S. fintech in 2019? In short, monster growth.

On the public side, fintechs delivered resoundingly. PayPal alone gained $26B in market capitalization. On a return basis, the public Matrix FinTech Index continued to crush every major equity index as well as the financial services incumbents. Nicely matching our forecasts, our Index delivered 213% returns over the last three years. The Index outperformed the financial services incumbents by 151 percentage points and the S&P 500 by 170 percentage points.

Powered by WPeMatico

Over the past year, startup banks have proven that they have a shot at disrupting retail banking. These challengers have amassed a war chest of funding, announced some ambitious international expansion plans and attracted millions of customers.

And yet, building a bank has proven to be even harder than building a startup in general. Retail banks aren’t willing to sit back and watch startups eat their lunch. Here’s a look back at the biggest moves of the year from challenger banks, some trends you should keep an eye on and the upcoming challenges for those startups.

Due to the regulatory framework and the size of the market, it is much easier to launch a challenger bank in Europe compared to anywhere else in the world. That’s why challenger banks have been thriving in Europe.

When a company gets a full banking license from the central bank of a EU country, the startup can passport its license across all EU countries and operate across the continent.

N26 raised a ton of money in 2019: last January, the Berlin-based startup announced a $300 million funding round, raising another $170 million in July. The company is now valued at $3.5 billion.

With more than 3.5 million customers in Europe, N26 announced some ambitious expansion plans. N26 is now live in the U.S. and is already planning a launch in Brazil.

Revolut has also been aggressively expanding in order to beat its competitors to new markets. In addition to its home market in the U.K., Revolut is available across Europe. In 2019, the company expanded to Singapore and Australia and currently has at least 8 million users.

While Revolut announced that it should launch in the U.S. and Canada by the end of last year, the clock ran out on that prediction. The startup has been very transparent about its expansion plans, even though it sometimes means that you have to wait months or even years before a full rollout.

For instance, Revolut announced in September 2018 that it would launch in New Zealand, Hong Kong and Japan “in the coming months.” It later became “early 2019,” then “2019.” India, Brazil, South Africa, Mexico and the UAE have also all been mentioned at some point. In other words: launching a banking product in a new country is hard.

The U.S. is a tedious market as you have to get a license in all 50 states to operate across the country

Monzo has been doing well at home in the U.K. It has attracted 3 million customers and raised £113 million (~$144m) in funding last year from Y Combinator’s Continuity fund. It is expanding to the U.S., but the rollout has been slow.

Nubank is another well-funded challenger bank. Backed by Tencent, the startup has raised a $400 million Series F round from TCV. According to the WSJ, the startup has a valuation above $10 billion.

Originally from Brazil, Nubank expanded to Mexico and has plans to expand to Argentina.

Chime is increasingly looking like the bigger player in the U.S., recently raising a $500 million funding round and reached a valuation of $5.8 billion. It only operates in the U.S.

Starling Bank and Atom Bank only operate in the U.K. Bunq is based in Amsterdam with a product tailor-made for the Netherlands, but it accepts customers across Europe.

This isn’t meant to be an exhaustive list as it’s becoming increasingly hard to cover all challenger banks.

There are a few basic features that separate challenger banks from legacy retail banks. Signing up is extremely simple and only requires a mobile app. The mobile app itself is usually much more polished than traditional banking apps.

Users receive a Mastercard or Visa debit card that communicates with the company’s server for each transaction. This way, users can receive instant notifications, block and unblock their cards and turn off some features, such as foreign payments, ATM withdrawals and online transactions.

Challenger banks usually customers promise no markup fees on transactions in foreign currencies, but there are sometimes some limits on this feature.

So how do these companies make money? When you pay with your card, banks generate a tiny, tiny interchange fee of money on each transaction. It’s really small, but it could become serious revenue at scale with tens of millions or hundreds of millions of users.

Challenger banks also offer other financial services like insurance products, foreign exchange or consumer credit. Some challenger banks develop those features in house, but many of those features are actually managed by external fintech partners. Challenger banks generate a commission on those products.

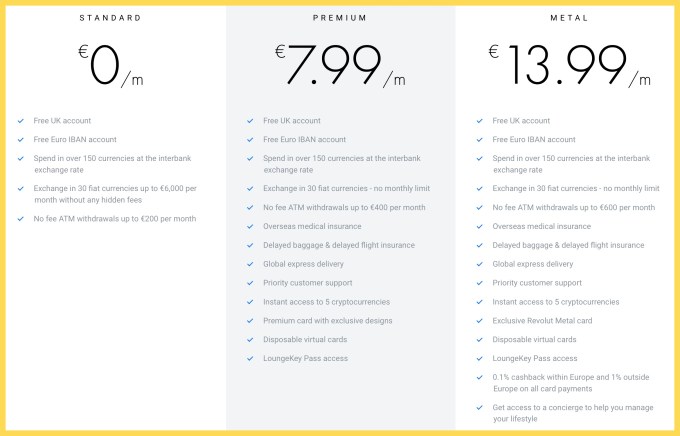

But the most promising product is premium subscriptions. While challenger banks started with free accounts and low, transparent fees, they have been selling premium subscriptions for a fixed monthly fee.

Challenger banks have become a software-as-a-service industry with a freemium component

For example, Revolut offers premium accounts for €7.99 per month with higher limits, some insurance benefits that you’d expect from a premium card and access to advanced features, such as cryptocurrencies and disposable virtual cards. There’s a super premium product for €13.99 called Metal with a metal card design, cashback on card payments and access to a concierge feature.

This seems a bit counterintuitive, but premium subscriptions have been performing well, according to discussions with people working in the industry. You pay a lot in subscription fees in order to avoid small transactional fees. (And you also get a cool card.)

Challenger banks have become a software-as-a-service industry with a freemium component. It leads to a premium positioning and high expectations from customers.

Revolut’s fees top out at €13.99/month.

Powered by WPeMatico

Brexit has taken over discourse in the UK and beyond. In the UK alone, it is mentioned over 500 million times a day, in 92 million conversations — and for good reason. While the UK has yet to leave the EU, the impact of Brexit has already rippled through industries all over the world. The UK’s technology sector is no exception. While innovation endures in the midst of Brexit, data reveals that innovative companies are losing the ability to attract people from all over the world and are suffering from a substantial talent leak.

It is no secret that the UK was already experiencing a talent shortage, even without the added pressure created by today’s political landscape. Technology is developing rapidly and demand for tech workers continues to outpace supply, creating a fiercely competitive hiring landscape.

The shortage of available tech talent has already created a deficit that could cost the UK £141 billion in GDP growth by 2028, stifling innovation. Now, with Brexit threatening the UK’s cosmopolitan tech landscape — and the economy at large — we may soon see international tech talent moving elsewhere; in fact, 60% of London businesses think they’ll lose access to tech talent once the UK leaves the EU.

So, how can UK-based companies proactively attract and retain top tech talent to prevent a Brexit brain drain? UK businesses must ensure that their hiring funnels are a top priority and focus on understanding what matters most to tech talent beyond salary, so that they don’t lose out to US tech hubs.

Powered by WPeMatico

Monzo, the fast-growing U.K.-based challenger bank with more than two million account holders, has raised £113 million (~$144m) in additional funding.

Confirming TechCrunch’s scoop in April, the Series F round is led by Y Combinator’s “Continuity” growth fund, and gives the company a new £2 billion (~$2.5b) post-money valuation. That’s double the £1 billion valuation it garnered in October last year.

A number of other new and existing investors have also participated in the Series F. They include Latitude, General Catalyst, Stripe, Passion Capital, Thrive, Goodwater, Accel, and Orange Digital Ventures.

The investment by London-based Latitude, the growth fund from prolific seed investor LocalGlobe, is particularly noteworthy given that LocalGlobe itself didn’t previously back Monzo. The same might be said of YC’s Continuity, considering that Monzo isn’t a YC alumni (although GoCardless, Monzo co-founder Tom Blomfield’s previous startup, did take part in the Silicon Valley accelerator).

The take-away: a growth fund attached to an early-stage fund can be a great antidote to the anti-portfolio (the list of successful companies a VC firm either missed, were unable or chose not to invest in).

Meanwhile, Monzo’s new funding round and YC’s backing should be viewed within the context of not only fast growth and increasingly convincing product-market fit in the U.K. — the challenger bank is currently adding 200,000 new sign-ups for its current account each month — but also recently unveiled plans to tentatively launch across the pond.

We first reported that Monzo was busy assembling a U.S.-based team over five months ago, and the U.K. company made its U.S. plans official last week. This will see a U.S. Monzo app and connected Mastercard debit card available via in-person signups at events to be held soon. The rollout will initially consist of a few thousand cards, supported by a waitlist in preparation for a wider launch.

The U.S. launch is being done in partnership with a local bank, but in the longer term Monzo plans to apply for its own U.S. bank license, similar to the strategy it employed in the U.K. so as to own and operate as much of its technical, product and regulatory infrastructure as possible.

In the U.K., this has helped Monzo achieve an NPS score of 80, which Blomfield previously told me is unusually high for a bank. This is seeing 60% of U.K. signups remain long-term active, transacting at once per week. As a counterpoint, however, the percentage of Monzo users that pay a salary into their Monzo account sits at between about 27% and 30% of active users, suggesting that a significant number of Monzo customers aren’t yet using it as their main account (Monzo’s definition of salaried is anyone who deposits at least £1,000 per month by bank transfer).

Success in the U.S., therefore, isn’t a given, conceded Blomfield when I had a call with him earlier this month. Instead, he argued that the key to cracking North America will be creating a fully localised version of Monzo based on carefully listening to U.S. users and once again finding product-market fit. He says there are obvious and less obvious cultural and technical differences in the way Brits and Americans save, spend and manage their finances, and this will require significant product divergence from the U.K. version of Monzo. Today’s new £113 million injection of capital is clearly designed to provide some of the breathing space required to achieve that.

As a side note, there are encouraging signs from other London-based fintechs that have ventured across the pond. One recent example is the financial “digital assistant” chatbot Cleo, which entered the U.S. around a year ago and has been more successful than the company anticipated, seeing Cleo add 650,000 active U.S. users to date. In fact, the U.S. currently makes up more than 90% of new Cleo users, prompting one source to describe the U.K. startup as effectively a U.S. company now.

Powered by WPeMatico

Just five months after announcing £85 million in Series E funding, Monzo is already gearing up to raise additional funding, which would almost double its valuation.

As reported in the Sunday Times yesterday, the U.K. challenger bank is close to raising £100 million in further funding in a new round led by an unnamed U.S. investor. If the deal goes through, it will reportedly give Monzo a pre-money valuation of close to £2 billion, up from £1 billion in October.

Now TechCrunch has learned that the new U.S. backer is Y Combinator.

According to multiple sources within investor circles on both sides of the pond, the Silicon Valley accelerator and venture capital fund plans to invest in Monzo out of its growth fund, the vehicle it typically uses to double down on fast-growing companies within its alumni.

Notably, Monzo isn’t a graduate of YC. However, Monzo co-founder Tom Blomfield’s previous startup, the payments company GoCardless, did go through the accelerator program, making Blomfield himself an alumni.

Monzo declined to comment. Y Combinator couldn’t be reached at the time of publication and I’ll update this post should I hear back.

Meanwhile, the news that Y Combinator is lining up to invest in Monzo makes a lot of sense in a number of ways beyond Blomfield’s previous ties to the accelerator. The challenger bank already boasts a plethora of U.S. investors, such as U.S. venture capital firm General Catalyst, Thrive Capital and Stripe.

And, as TechCrunch reported exclusively, Monzo has quietly begun working on a U.S. launch. This includes setting up a small team states-side to begin laying the groundwork to bring a version of Monzo to North America. It will initially be powered by a U.S. banking partner while Monzo works on the necessary regulatory licenses to go it alone.

Monzo continues to grow at a clip here in the U.K., too. To date, the challenger bank claims more than 1.7 million customers since it launched in 2015.

Powered by WPeMatico

Monzo, the U.K. challenger bank with more than a million customers and a unicorn valuation to boot, has quietly begun working on a U.S. launch, TechCrunch has learned.

According to multiple sources, the fintech startup has set up a small team to begin laying the groundwork to bring a version of Monzo to North America, which will initially be powered by a U.S. banking partner while Monzo works on the necessary regulatory licenses to go it alone.

The plan, which could still be subject to change, is for Monzo to create a “lite” version of its product for U.S. customers, much in the same way it first launched in the U.K. with a pre-paid debit card before eventually offering a fully fledged bank account.

The thinking, according to one person familiar with the company’s strategy, is that this will enable Monzo to build up a U.S. customer base and iterate its product for the U.S. market in parallel with the challenger bank’s federal charter bank application.

I understand that the plan is for the initial Monzo U.S. product to offer in-app signup, the trademark “hot coral” Monzo debit card, an account and routing number, the ability to make and accept payments, ATM withdrawals, and real-time transaction notifications. In other words, many of the same features that has endeared Monzo with U.K. customers.

Contacted by TechCrunch, a Monzo spokesperson provided the following statement:

We’re really excited about international expansion over the coming months and years. After all, it’s hard to build a bank for a billion people in the UK alone!

However, we don’t have anything specific to share at this stage about those plans. When we do, we’ll be sure to tell the world.

Meanwhile, news that Monzo has begun executing U.S. expansion plans isn’t entirely surprising, even if appears to be happening significantly faster than previously thought.

Meanwhile, news that Monzo has begun executing U.S. expansion plans isn’t entirely surprising, even if appears to be happening significantly faster than previously thought.

Co-founder and CEO Tom Blomfield has openly talked about his ambition to bring Monzo to the U.S. one day, and the London-based challenger bank boasts an array of U.S. investors. They include most recently General Catalyst, along with the likes of Thrive Capital, Goodwater Capital, Stripe, Michael Moritz and Instagram co-founder Kevin Systrom.

The fintech company also recently opened a Las Vegas office, from which it offers twilight hours customer support for U.K. customers. Or at least that is the party line. Now it appears that Las Vegas could soon have Monzo customers closer to home to keep happy, too.

Powered by WPeMatico