Mobile payments

Auto Added by WPeMatico

Auto Added by WPeMatico

Sunday was a big day in fintech: Afterpay has agreed to merge with Square. This agreement sets two of the most admired financial technology companies in recent history on a path to becoming one.

Afterpay and Square have the potential to build one of the world’s most important payments networks. Square has built a very significant merchant payment network, and, via Cash App, a thriving high-growth consumer payment service. However, these two lines of business have historically not been integrated. Together, Square and Afterpay will be able to weave all of these services together into a single integrated experience.

Afterpay and Cash App each have double-digit millions of consumers, and Square’s seller ecosystem and Afterpay’s merchant network both record double-digit billions of payment volume per year. From the offline register and the online checkout flow to sending money in just a few taps, Square and Afterpay will tell a complete story of next-generation economic empowerment.

As Afterpay’s only institutional venture investor, I wanted to share some perspective on how we got here and what this merger means for the future of consumer finance and the payments industry.

Afterpay and Square have the potential to build one of the world’s most important payments networks.

Every five to 10 years, the global payments industry undergoes a critical innovation cycle that determines the winners and losers for the next several decades. The last major transition was the shift to NFC-based mobile payments, which I wrote about in 2015. The major mobile OS vendors (Apple and Google) cemented their position in the global payments stack by deftly bridging the needs of the networks (Visa, Mastercard, etc.) and consumers by way of the mobile devices in their pockets.

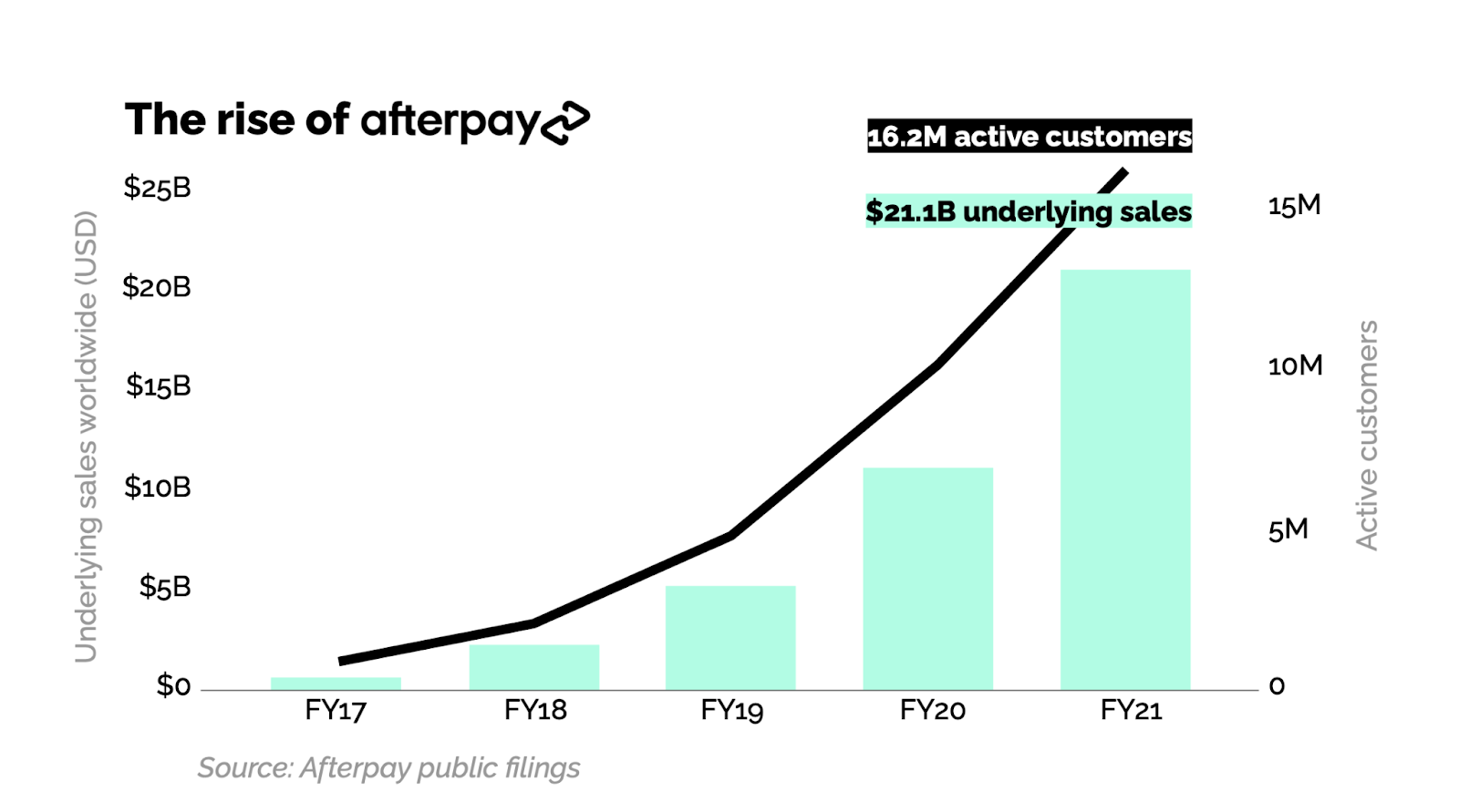

Afterpay sparked the latest critical innovation cycle. Conceived in a living room in Sydney by a millennial, Nick Molnar, for millennials, Afterpay had a key insight: Millennials don’t like credit.

Millennials came of age during the global mortgage crisis of 2008. As young adults, they watched their friends and family lose their homes by overextending on mortgage debt, bolstering their already lower trust for banks. They also have record levels of student debt. Therefore, it’s no surprise that millennials (and Gen Z right behind them) strongly prefer debit cards over credit cards.

But it’s one thing to recognize the paradigm shift and quite another to do something about it. Nick Molnar and Anthony Eisen did something, ultimately building one of the fastest-growing payments startups in history on their core product: Buy now, pay later … and never any interest.

Afterpay’s product is simple. If you have $100 in your cart and choose to pay with Afterpay, it will charge your bank card (typically a debit card) $25 every two weeks in four installments. No interest, no revolving debt and no fees with on-time payments. For the millennial consumer, this meant they could get the primary benefit of a credit card (the ability to pay later) with their debit card, without the need to worry about all the bad things that come with credit cards — high interest rates and revolving debt.

All upside, no downside. Who could resist? For the early merchants, virtually all of whom relied on millennials as their key growth segment, they got a fair trade: Pay a small fee above payment processing to Afterpay, get significantly higher average order values and conversions to purchase. It was a win-win proposition and, with lots of execution, a new payment network was born.

Image Credits: Matrix Partners

Afterpay went somewhat unnoticed outside Australia in 2016 and 2017, but once it came to the U.S. in 2018 and built a business there that broke $100 million net revenues in only its second year, it got attention.

Klarna, which had struggled with product-market fit in the U.S., pivoted their business to emulate Afterpay. And Affirm, which had always been about traditional credit — generating a significant portion of their revenue from consumer interest — also noticed and introduced their own BNPL offering. Then came PayPal with “Pay in 4,” and just a few weeks ago, there has been news that Apple is expected to enter the space.

Afterpay created a global phenomenon that has now become a category embraced by mainstream players across the industry — a category that is on track to take a meaningful share of global retail payments over the next 10 years.

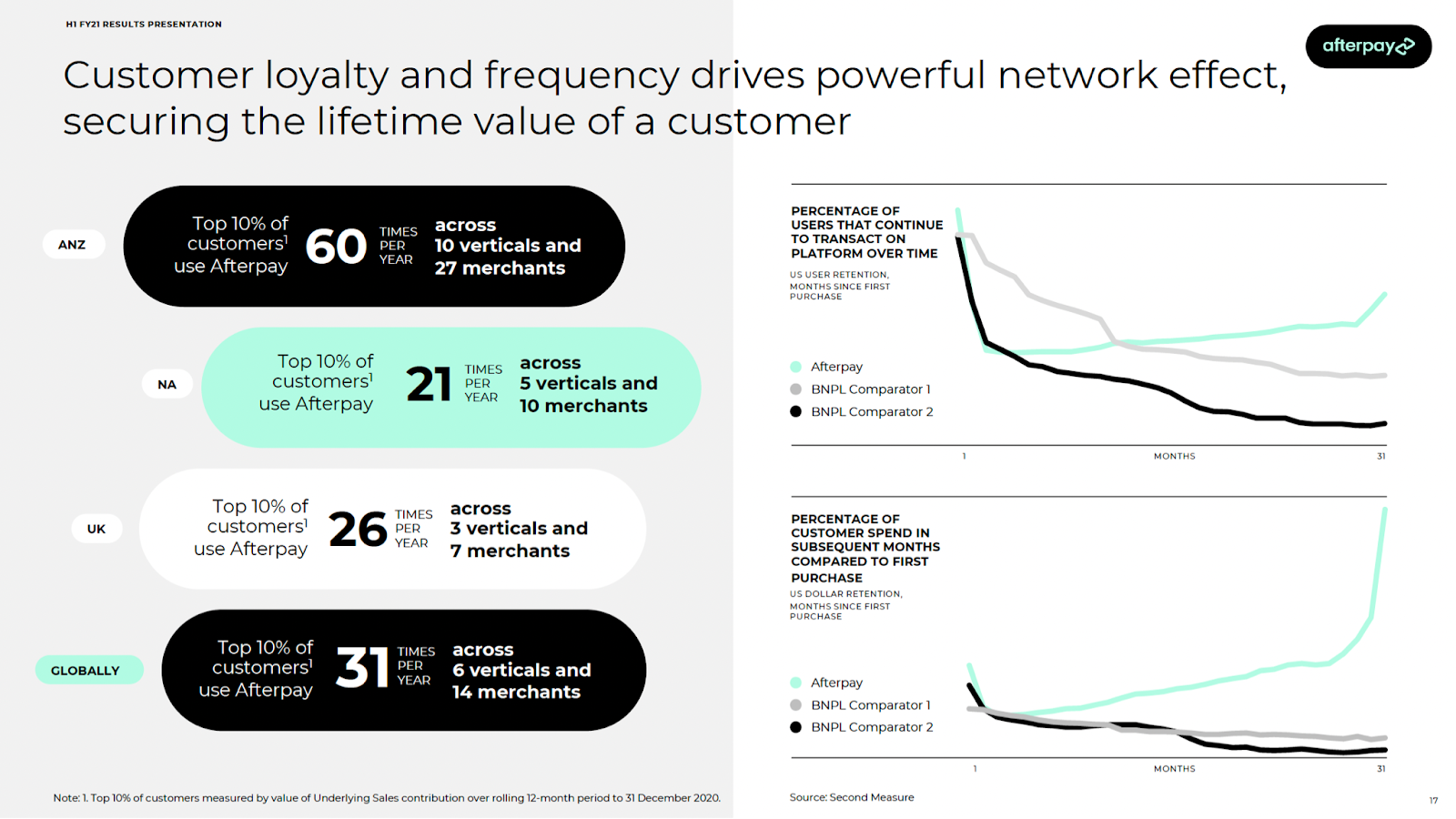

Afterpay stands apart. It has always been the BNPL leader by virtually every measure, and it has done it by staying true to their customers’ needs. The company is great at understanding the millennial and Gen Z consumer. It’s evident in the voice, tone and lifestyle brand you experience as an Afterpay user, and in the merchant network it continues to build strategically. It’s also evident in the simple fact that it doesn’t try to cross-sell users revolving debt products.

Most importantly, it’s evident in the usage metrics relative to competition. This is a product that people love, use and have come to rely on, all with better, fairer terms than were ever available to them than with traditional consumer credit.

Image Credits: Afterpay H1 FY21 results presentation

I’ve been building payment companies for over 15 years now, initially in the early days of PayPal and more recently as a venture investor at Matrix Partners. I’ve never seen a combination that has such potential to deliver extraordinary value to consumers and merchants. Even more so than eBay + PayPal.

Beyond the clear product and network complementarity, what’s most exciting to me and my partners is the alignment of values and culture. Square and Afterpay share a vision of a future with more opportunity and fewer economic hurdles for all. As they build toward that future together, I’m confident that this combination is a winner. Square and Afterpay together will become the world’s next generation payment provider.

Powered by WPeMatico

PayPal’s plan to morph itself into a “super app” has been given a go for launch.

According to PayPal CEO Dan Schulman, speaking to investors during this week’s second-quarter earnings call, the initial version of PayPal’s new consumer digital wallet app is now “code complete” and the company is preparing to slowly ramp up. Over the next several months, PayPal expects to be fully ramped up in the U.S., with new payment services, financial services, commerce and shopping tools arriving every quarter.

The company has spoken for some time about its “super app” ambitions — a shift in product direction that would make PayPal a U.S.-based version of something like China’s WeChat or Alipay or India’s Paytm. Like those apps, PayPal aims to offer a host of consumer services under one roof, beyond just mobile payments.

In previous quarters, PayPal said these new features may include things like enhanced direct deposit, check cashing, budgeting tools, bill pay, crypto support, subscription management, and buy now, pay later functionality. It also said it would integrate commerce, thanks to the mobile shopping tools acquired by way of its $4 billion Honey acquisition in 2019.

So far, PayPal has continued to run Honey as a standalone application, website and browser extension, but the super app could incorporate more of its deal-finding functions, price-tracking features and other benefits.

On Wednesday’s earnings call, Schulman revealed the super app would have a few other features as well, including high-yield savings, early access to direct deposit funds and messaging functionality outside of peer-to-peer payments — meaning you could chat with family and friends directly through the app’s user interface.

PayPal hadn’t announced its plans to include a messaging component until now, but the feature makes sense in terms of how people often combine chat and peer-to-peer payments today. For example, someone may want to make a personal request for the funds instead of just sending an automated request through an app. Or, after receiving payment, a user may want to respond with a “thank you,” or other acknowledgment. Currently, these conversations take place outside of the payment app itself on platforms like iMessage. Now, that could change.

“We think that’s going to drive a lot of engagement on the platform,” said Schulman. “You don’t have to leave the platform to message back and forth.”

With the increased user engagement, the company expects to see a bump in average revenue per active account.

Schulman also hinted at “additional crypto capabilities,” which were not detailed. However, PayPal earlier this month increased the crypto purchase limit from $20,000 to $100,000 for eligible PayPal customers in the U.S., with no annual purchase limit. The company also this year made it possible for consumers to check out at millions of online businesses using their cryptocurrencies, by first converting the crypto to cash then settling with the merchant in U.S. dollars.

Though the app’s code is now complete, Schulman said the plan is to continue to iterate on the product experience, noting that the initial version will not be “the be-all and end-all.” Instead, the app will see steady releases and new functionality on a quarterly basis.

However, he did say that early on, the new features would include the high-yield savings, improved bill pay with a better user experience, and more billers and aggregators, as well as early access to direct deposit, budgeting tools and the new two-way messaging feature.

To integrate all the new features into the super app, PayPal will undergo a major overhaul of its user interface.

“Obviously, the [user experience] is being redesigned,” Schulman noted. “We’ve got rewards and shopping. We’ve got a whole giving hub around crowdsourcing, giving to charities. And then, obviously, buy now, pay later will be fully integrated into it. … The last time I counted, it was like 25 new capabilities that we’re going to put into the super app.”

The digital wallet app will also be personalized to the end user, so no two apps are the same. This will be done using both artificial intelligence and machine learning capabilities to “enhance each customer’s experiences and opportunities,” said Schulman.

PayPal delivered an earnings beat in the second quarter with $6.24 billion in revenue, versus the $6.27 billion Wall Street expected, and earnings per share of $1.15, versus the $1.12 expected. Total payment volume from merchant customers also jumped 40% to $311 billion, while analysts had projected $295.2 billion. But the company’s stock slipped due to a lowered outlook for Q3, impacted by eBay’s transition to its own managed payments service.

In addition, PayPal gained 11.4 million net new active accounts in the quarter, to reach 403 million total active accounts.

Powered by WPeMatico

Business-to-business payments platform Nium announced Monday that it raised more than $200 million in Series D funding and saw its valuation rise above $1 billion.

The company, now Singapore-based but shifting to the Bay Area, touted the investment as making it “the first B2B payments unicorn from Southeast Asia.”

Riverwood Capital led the round, in which Temasek, Visa, Vertex Ventures, Atinum Capital, Beacon Venture Capital and Rocket Capital Investment participated, along with a group of angel investors like DoorDash’s Gokul Rajaram, FIS’ Vicky Bindra and Tribe Capital’s Arjun Sethi. Including the new funding, Nium has raised $300 million to date, Prajit Nanu, co-founder and CEO, told TechCrunch.

The B2B payments sector is already hot, yet underpenetrated, according to some experts. To give an idea just how hot, Nium was seeking $150 million for its Series D round, received commitments of $300 million from eager investors and settled on $200 million, Nanu said.

“This is our fourth or fifth fundraise, but we have never had this kind of interest before — we even had our term sheets in five days,” he added. “I believe this interest is because we’ve successfully managed to create a global platform that is heavily regulated, which gives us access to a lot of networks. This is an environment where payment is visible, and our core is powering frictionless commerce and enabling anyone to use our platform.”

Nium’s new round adds fuel to a fire shared by a number of companies all going after a global B2B payments market valued at $120 trillion annually: last week, Paystand raised $50 million in Series C funding to make B2B payments cashless, while Dwolla raised $21 million for its API that allows companies to build and facilitate fast payments. In March, Higo brought in $3.3 million to do the same in Latin America, while Balance, developing a B2B payments platform that allows merchants to offer a variety of payment methods. raised $5.5 million in February.

Nium’s approach is to provide access to a global payment infrastructure, including card issuance, accounts receivable and payable, and banking-as-a-service through a single API. The company’s network enables customers to then send funds to more than 100 countries, pay out in more than 60 currencies, accept funds in seven currencies and issue cards in more than 40 countries, Nanu said. The company also boasts money transfer, card issuances and banking licenses in 11 jurisdictions.

Francisco Alvarez-Demalde, co-founding partner and managing partner at Riverwood, said in an email that the combination of software — plus regulatory licenses — and operating a fintech infrastructure platform on behalf of neobanks and corporates is a global trend experiencing hyper-growth.

Riverwood followed Nium for many years, and its future vision was what got the firm interested in being a part of this round. Alvarez-Demalde said that “Nium has the incredible combination of a great market opportunity, a talented founder and team, and we believe the company is poised for global growth based on underlying secular technology trends like increasing real-time payment capabilities and the proliferation of cross border commerce.

“As a central payment infrastructure in one API, Nium is a catalyst that unlocks cross-border payments, local accounts and card issuance with a network of local market licenses, partners and banking relationships to facilitate moving money across the world,” he added. “Enterprises of all types are embedding financial services as part of their consumer experience, and Nium is a key global enabler of this trend.”

Nanu said the new funding enables the company to move to the United States, which represents 3% of Nium’s revenue. He wants to increase that to 20% over the next 18 months, as well as expand in Latin America. The investment also gives the company a 12- to 18-month runway for further M&A activity. In June, Nium acquired virtual card issuance company Ixaris, and in July acquired Wirecard Forex India to expose it to India’s market. He also plans to expand the company’s payments network infrastructure, invest in product development and add to Nium’s 700-person headcount.

Nium already counts hundreds of enterprise companies as clients and plans to onboard thousands more in the next year. The company processes $8 billion in payments annually and has issued more than 30 million virtual cards since 2015. Meanwhile, revenue grew by over 280% year over year.

All of this growth puts the company on a trajectory for an initial public offering, Nanu said. He has already spoken to people who will help the company formally kick off that journey in the first quarter of 2022.

“Unlike other companies that raise money for new products, we aim to expand in the existing sets of what we do,” Nanu said. “The U.S. is a new market, but we have a good brand and will use the new round to provide a better experience to the customer.”

Powered by WPeMatico

It’s pretty easy for individuals to send money back and forth, and there are lots of cash apps from which to choose. On the commercial side, however, one business trying to send $100,000 the same way is not as easy.

Paystand wants to change that. The Scotts Valley, California-based company is using cloud technology and the Ethereum blockchain as the engine for its Paystand Bank Network that enables business-to-business payments with zero fees.

The company raised $50 million Series C funding led by NewView Capital, with participation from SoftBank’s SB Opportunity Fund and King River Capital. This brings the company’s total funding to $85 million, Paystand co-founder and CEO Jeremy Almond told TechCrunch.

During the 2008 economic downturn, Almond’s family lost their home. He decided to go back to graduate school and did his thesis on how commercial banking could be better and how digital transformation would be the answer. Gleaning his company vision from the enterprise side, Almond said what Venmo does for consumers, Paystand does for commercial transactions between mid-market and enterprise customers.

“Revenue is the lifeblood of a business, and money has become software, yet everything is in the cloud except for revenue,” he added.

He estimates that almost half of enterprise payments still involve a paper check, while fintech bets heavily on cards that come with 2% to 3% transaction fees, which Almond said is untenable when a business is routinely sending $100,000 invoices. Paystand is charging a flat monthly rate rather than a fee per transaction.

Paystand’s platform. Image Credits: Paystand

On the consumer side, companies like Square and Stripe were among the first wave of companies predominantly focused on accounts payable and then building business process software on top of an existing infrastructure.

Paystand’s view of the world is that the accounts receivables side is harder and why there aren’t many competitors. This is why Paystand is surfing the next wave of fintech, driven by blockchain and decentralized finance, to transform the $125 trillion B2B payment industry by offering an autonomous, cashless and feeless payment network that will be an alternative to cards, Almond said.

Customers using Paystand over a three-year period are able to yield average benefits like 50% savings on the cost of receivables and $850,000 savings on transaction fees. The company is seeing a 200% increase in monthly network payment value and customers grew two-fold in the past year.

The company said it will use the new funding to continue to grow the business by investing in open infrastructure. Specifically, Almond would like to reboot digital finance, starting with B2B payments, and reimagine the entire CFO stack.

“I’ve wanted something like this to exist for 20 years,” Almond said. “Sometimes it is the unsexy areas that can have the biggest impacts.”

As part of the investment, Jazmin Medina, principal at NewView Capital, will join Paystand’s board. She told TechCrunch that while the venture firm is a generalist, it is rooted in fintech and fintech infrastructure.

She also agrees with Almond that the B2B payments space is lagging in terms of innovation and has “strong conviction” in what Almond is doing to help mid-market companies proactively manage their cash needs.

“There is a wide blue ocean of the payment industry, and all of these companies have to be entirely digital to stay competitive,” Medina added. “There is a glaring hole if your revenue is holding you back because you are not digital. That is why the time is now.”

Powered by WPeMatico

The payments space — amazingly — remains up for grabs for startups. Yes, dear reader, despite the success of Stripe, there seems to be a new payments startup virtually every other day. It’s a mess out there! The accelerated growth of e-commerce due to the pandemic means payments are now a booming space. And here comes another one, with a twist.

WhenThen has built a no-code payment operations platform that, they claim, streamlines the payment processes “of merchants of any kind”. It says its platform can autonomously orchestrate, monitor, improve and manage all customer payments and payments ops.

The startup’s opportunity has arisen because service providers across different verticals increasingly want to get into open banking and provide their own payment solutions and financial services.

Founded six months ago, WhenThen has now raised $6 million, backed by European VCs Stride and Cavalry.

The founders, Kirk Donohoe, Eamon Doyle and Dave Brown, are three former Mastercard Payment veterans.

Based out of Dublin, CEO Donohoe told me: “We see traditional businesses embracing e-comm, and e-comm merchants now operating multiple business models such as trade supply, marketplace, subscription, and more. There is no platform that makes it easy for such businesses to create and operate multiple payment flows to support multiple business models in one place — that’s where we step in.”

He added: “WhenThen is helping e-commerce digital platforms build advanced payment flows and payment automation, in minutes as opposed to months. When you start to integrate different payment methods, different payment gateways, how you want the payment to move from collection through to payout gets very, very complex. I’ve been doing this for over a decade now, as an entrepreneur building different businesses that had to accept, collect and pay payments.”

He said his founding team “had to build very complex payment flows for large merchants, airlines, hotels, issuers, and we just found it was ridiculous that you have to continue to do the same thing over and over again. So we decided to come up with WhenThen as a better way to be able to help you build those flows in minutes.”

Claude Ritter, managing partner at Cavalry, said: “Basic payment orchestration platforms have been around for some time, focusing mostly on maximizing payment acceptance by optimizing routing. WhenThen provides the first end-to-end payment flow platform to equip businesses with the opportunity to control every stage of the payment flow from payment intent to payout.”

WhenThen supports a wide range of popular payment providers such as Stripe, Braintree, Adyen, Authorize.net, Checkout.com, etc., and a variety of alternative and locally preferred payment methods such as Klarna Affirm, PayPal and BitPay.

“For brave merchants considering global reach and operating multiple business models concurrently, I believe choosing the right payment ops platform will become as important as choosing the right e-commerce platform. Building your entire e-comm experience tightly coupled to a single payment processor is a hard correction to make down the line — you need a payment flow platform like WhenThen”, added Fred Destin, founder of Stride.VC.

Powered by WPeMatico

Google is making it possible to store digital versions of either COVID-19 test results or vaccination cards on users’ Android devices. The company on Wednesday announced it’s updating its Passes API, which will give developers at healthcare organizations, government agencies, and other organizations authorized by public health authorities the ability to create digital versions of tests and vaccination cards that can then be saved directly to the user’s device. The Passes API is typically used to store things like boarding passes, loyalty cards, gift cards, tickets and more to users’ Google Pay wallet. However, the Google Pay app in this case will not be required, Google says.

Instead, users without the Google Pay app will have the option to store the digital version of the COVID Card directly to their device, where it’s accessible from a home screen shortcut. Because Google is not retaining a copy of the card, anyone who needs to store the COVID Card on multiple devices will need to download it individually on each one from the healthcare provider or other organization’s app.

The cards themselves show the healthcare provider or organization’s logo and branding at the top, followed by the person’s name, date of birth and other relevant information, like the vaccine manufacturer or date of shot or test. According to a support document, healthcare providers or organizations could alert users to the ability to download their card via email, text, or through a mobile website or app.

In an example photo, Google showed the COVID-19 Vaccination Card from Healthvana, a company that serves L.A. County, However, it didn’t provide any other information about which healthcare providers are interested in or planning to adopt the new technology. Reached for comment, Google says there are some other big partners and states in the pipeline, but it doesn’t have permission to share those names at this time. Over the next few weeks, some of these names will be released, we understand.

The Passes API update doesn’t mean Android users can immediately create digital versions of their COVID vaccination cards — something people have been taking pictures of as a means of backup or, unfortunately in some cases, laminating it. (That’s not advised, however, as the card is meant to be used again for recording booster shots.)

Rather, the update is about giving developers the ability to begin building tools to export the data they have in their own systems about people’s COVID tests and vaccinations to a local digital card on Android devices. To what extent these digital cards will become broadly available to end users will depend on developer adoption.

For the feature to work, the Android device needs to run Android 5 or later and it will need to be Play Protect certified, which is a licensing program that ensures the device is running real Google apps. Users will also need to set a lock screen on their device for additional security.

Google says the update will initially roll out in the U.S., followed by other countries.

The U.S. is behind other markets in making digital versions of vaccination cards possible. Today, the EU’s COVID certificate, which shows an individual’s vaccination status, test results or recovery status from COVID-19, went live. The certificate (EUDCC) will be recognized by all EU members and will aid with cross-border travel. Israel released a vaccine passport earlier this year that allows vaccinated people to show their “green pass” at places that require vaccinations. Japan aims to have vaccination passports ready by the end of July for international travel.

In the U.S., only a few states have active vaccine certification apps. Many others have either outright banned vaccine passports — which has become a politically loaded term — or are considering doing so.

Given this context, Google’s digital vaccination card is just that — a digital copy of a paper card. It’s not tied to any other government initiatives nor is it a “vaccine passport.”

Powered by WPeMatico

This spring, Facebook confirmed it was testing Venmo-like QR codes for person-to-person payments inside its app in the U.S. Today, the company announced those codes are now launching publicly to all U.S. users, allowing anyone to send or request money through Facebook Pay — even if they’re not Facebook friends.

The QR codes work similarly to those found in other payment apps, like Venmo.

The feature can be found under the “Facebook Pay” section in Messenger’s settings, accessed by tapping on your profile icon at the top left of the screen. Here, you’ll be presented with your personalized QR code which looks much like a regular QR code except that it features your profile icon in the middle.

Underneath, you’ll be shown your personal Facebook Pay UR which is in the format of “https://m.me/pay/UserName.” This can also be copied and sent to other users when you’re requesting a payment.

Facebook notes that the codes will work between any U.S. Messenger users, and won’t require a separate payment app or any sort of contact entry or upload process to get started.

Users who want to be able to send and receive money in Messenger have to be at least 18 years old, and will have to have a Visa or Mastercard debit card, a PayPal account or one of the supported prepaid cards or government-issued cards, in order to use the payments feature. They’ll also need to set their preferred currency to U.S. dollars in the app.

After setup is complete, you can choose which payment method you want as your default and optionally protect payments behind a PIN code of your choosing.

The QR code is also available from the Facebook Pay section of the main Facebook app, in a carousel at the top of the screen.

Facebook Pay first launched in November 2019, as a way to establish a payment system that extends across the company’s apps for not just person-to-person payments, but also other features, like donations, Stars and e-commerce, among other things. Though the QR codes take cues from Venmo and others, the service as it stands today is not necessarily a rival to payment apps because Facebook partners with PayPal as one of the supported payment methods.

However, although the payments experience is separate from Facebook’s cryptocurrency wallet, Novi, that’s something that could perhaps change in the future.

Image Credits: Facebook

The feature was introduced alongside a few other Messenger updates, including a new Quick Reply bar that makes it easier to respond to a photo or video without having to return to the main chat thread. Facebook also added new chat themes including one for Olivia Rodrigo fans, another for World Oceans Day, and one that promotes the new F9 movie.

Powered by WPeMatico

U.S.-based challenger bank Current, which has now grown to nearly 3 million users, announced this morning it has raised a $220 million round of Series D funding, led by new investor Andreessen Horowitz (a16z). The funding swiftly follows Current’s $131 million Series C at the end of last year, at which point the company had doubled its user base over just six months to more than 2 million users.

As a result of the new round, the fintech company has roughly tripled its valuation in five months, to $2.2 billion.

Other participants in the round include returning investors Tiger Global Management, TQ Ventures (the fund managed by media executive Scooter Braun), Avenir, Sapphire Ventures, Foundation Capital, Wellington Management and EXPA. David George, who led the round with a16z, will become a Current board member.

Current began its life as a teen debit card controlled by parents, but later expanded to offer personal checking accounts powered by the same underlying banking technology. Like a range of modern-day “neobanks,” or digital banks, the Current app offers a baseline of standard features like free overdrafts, no minimum balance requirements, faster direct deposits, instant spending notifications, banking insights, free ATMs, check deposits using your phone’s camera and more. It also last year launched a points rewards program in an effort to better differentiate its service from the growing number of competitors and became one of the first banks to transfer the early round of stimulus payments during the pandemic.

These days, Current is partnering with creators, like the recently announced MrBeast (aka Jimmy Donaldson), who said last week on his YouTube channel that he will personally send $1 to the first 100,000 people who sign up using his Creator code. MrBeast is also an investor.

Like other fintechs in its same space, Current has benefitted from the younger generation’s adoption of mobile banking apps instead of larger, traditional banks, which they feel don’t serve their interests. Its average customer age is 27, for example. Digital banks can keep costs down by not having to pay for the overhead of brick-and-mortar locations, allowing them to roll out benefits like reduced or zero account fees and other consumer-friendly protections.

Current today continues to offer teen banking, in a challenge to mobile banking app Step, which has also leveraged social media influencers to get the word out with a younger demographic. But Step today is appealing to the 13 to 18-year-old crowd directly, offering banking services and a secured card. Current, meanwhile, targets its service to the parents.

Its teen account costs $36 per year, while personal checking is available both as a free and premium ($4.99/mo) service. The company in the past has said its primary focus is the more than 130 million Americans who live paycheck to paycheck. This continues to be its main drive today, though the mission may attract a broader slice of the American population over time.

“We are still focused on onboarding people to the financial system, making sure that everyone has access to everything, and then democratizing — or going out and getting that value — in this new world that’s being rewritten and bringing it back to as many people as possible,” says Current CEO and founder Stuart Sopp. “Now, in that increase of scope and time. I think we’re going to pick up more and more people.”

Current says the new funds will be used to grow the company and its member base as it expands it range of banking products. One key area of new investment will be cryptocurrency, it says, which will involve a partnership and an educational component to help Current’s users better understand the crypto market.

As it turns out, Sopp’s background includes crypto, in addition to Wall Street trading. In fact, an early version of Current designed by Sopp and CTO Trevor Marshall involved crypto.

“A little-known fact is that Current started with Bitcoin wallet addresses and Ripple gateways,” he says. But the team realized the technology was a little too nascent at the time, and moved to mobile banking. “We have this background, and this knowledge of how it all works. Now do we need to build it ourselves? No, I don’t think we need to build it all ourselves. There’s lots of good companies out there,” he says.

Crypto fits into Current’s vision of democratizing access to financial systems to those in the U.S. who are today underserved by traditional banking and investing products and services.

“There’s a ton of value being created [in crypto] and we want to make sure we have this nexus of providing safe, and trustworthy financial services in that world, as well as what we already exist in,” notes Sopp. “And then, lending, credit cards,” he adds, noting how important these moves are “done safely, in a respectful way for our demographic — because traditionally most of our members have a FICO score of 650.”

In addition, Current will use the new funds for hiring across all roles, including marketing, product, engineering, finance, customer success, fraud and risk, and, of course, crypto. The company today has 100 employees, and plans to grow to around 200 or 300 in the next 18 months.

Current’s fundraise remarkably falls on the same day that competitor Step and Greenlight, both which focus on families, also raised new rounds.

“This new generation of customers doesn’t want to bank in physical branches,” said a16z’s David George, in a statement. “We believe there will be a shift in the next 10 years to mobile and consumer-focused banking services powered by innovation in technology, and with Current’s exceptional growth over the past year, they’ve clearly demonstrated they’re at the forefront of this trend. Their product is among the best in the market, and they have proven an ability to reach customers who previously were unserved or underserved by traditional banks,” he said.

Powered by WPeMatico

Brazilian mobile payments app PicPay filed on Wednesday an F-1 with the Securities and Exchange Commission (SEC) for an IPO valued at up to $100 million. The company plans to list on the Nasdaq under the ticker symbol PICS.

PicPay operates largely as a financial services platform that includes a credit card, a digital wallet similar to that of Apple Pay, a Venmo-style P2P payments element, e-commerce and social networking features.

“We want to transform the way people and companies interact, make transactions, and communicate in an intelligent, connected, and simple experience,” said José Antonio Batista, CEO of PicPay, in a statement.

While the company is based in São Paulo now and operates across Brazil, PicPay originally launched in Vitoria in 2012, a coastal city north of Rio. In 2015 the company was acquired by the group J&F Investimentos SA, a holding company owned by Brazilian billionaire brothers Wesley and Joesley Batista, which also own the gigantic meatpacker JBS SA.

According to the company’s registration statement, J&F was involved in the biggest corruption scandal in Brazil’s history, known as The Car Wash, and in 2017 entered into a plea deal with the Brazilian Federal Prosecutor. In December 2020 the company agreed to pay a fine of $1.5 billion and contribute an extra $442.6 million to social projects in Brazil. That being said, J&F continues to be a powerful conglomerate in the country, positioning itself as a strong backer for PicPay.

2020 was an explosive year for PicPay as the company saw its active userbase grow from 28.4 million to 36 million as of March 2021. According to the company’s 2020 financial report, which PicPay shared with TechCrunch, the company’s revenues also grew drastically from $15.5 million in 2019, to $71 million in 2020. The company is not yet profitable, however, and PicPay shelled out $146 million in 2020 to fuel its growth.

“We believe that the growth of our base and user engagement in our ecosystem demonstrates the scalability of our business model and reveals a great opportunity to generate more value for these customers,” Batista added.

Fintech is one of the most popular sectors in Brazil today, because there’s a lot of room for improvement in the region. The country has traditionally been controlled by four major banks, which have been slow to adapt to technology and also charge very high fees.

PicPay’s IPO is being led by Banco Bradesco BBI, Banco BTG Pactual, Santander Investment Securities Inc., and Barclays Capital Inc.

*The Brazilian Real was valued at 5.50 to $1 USD on the date of publication.

Powered by WPeMatico

Flux, the London fintech that has built a technology platform for banks and merchants to power itemised digital receipts and more, has seen its lengthy pilot with Barclays bear fruit.

Announced formally today — but actually quietly rolled out a few months ago — Flux-powered digital receipts are now available as an opt-in for all U.K. Barclays debit card holders within the bank’s main mobile banking app. Previously, the functionality was only available within the Barclays Launchpad app, which is available for customers that want to try out experimental or upcoming features.

Early last year, Barclays announced that it has invested in Flux, taking a minority stake, so the strengthening of its partnership isn’t too much of a surprise. Flux also went through the Techstars-powered Barclays accelerator in its very early days. However, not all corporate accelerators lead to great outcomes as corporates are notoriously risk-adverse. This one certainly wasn’t rushed but it’s meaningful regardless, giving Flux a major shot in the arm in reaching mainstream banking customers beyond the existing challenger bank partnerships it has forged.

“Customers who pay using their Barclays debit card for future in store purchases at H&M, shoe retailer schuh and food outlets, which include Just Eat and Papa Johns, will see their receipts sent automatically to their app after making a purchase. They can then easily and securely view their receipts whenever they need by tapping on the transaction,” says Barclays. Crucially, although opt-in, Barclays customers will receive a prompt to set up digital receipts when they purchase items from retailers currently on-boarded to Flux.

Founded in 2016 by former early employees at Revolut, Flux bridges the gap between the itemised receipt data captured by a merchant’s point-of-sale (POS) system and what little information typically shows up on your bank statement or mobile banking app. Off the back of this, it can also power loyalty schemes and card-linked offers, as well as give merchants much deeper POS analytics via aggregated and anonymised data on consumer behaviour, such as which products are selling best in unique baskets.

On the banking side, along with Barclays, Flux has partnered with challenger banks Starling and Monzo. Once banking customers link their account to the service, Flux delivers digital receipts (and where available rewards and loyalty) for transactions at Flux retailer partners.

Longer term, Flux wants to become a standard for the interchange of item level digital receipt data — and the proprietary platform that powers that standard — but has always faced a chicken-and-egg problem: It needs bank integrations to sign up merchants and it needs merchant integrations to sign up banks. Barclays going live properly is another significant turn in the upstart’s flywheel.

Powered by WPeMatico