Mobile payments

Auto Added by WPeMatico

Auto Added by WPeMatico

JoomPay, a startup with a similar product to PayPal-owned Venmo in the U.S., is set to launch in Europe shortly after being granted a Luxembourg Electronic Money Institution (EMI) license. The app allows people to send and receive money with anyone, instantly and for free. “Venmo me” has become a common phrase in the U.S., where people use it to split bills in restaurants or similar instances. Venmo is in common use in the U.S., but it’s not available in Europe, although dozens of other innovative mobile peer to peer transfer options exist, such as Revolut, N26, Monese and Monzo. The waitlist for the app’s beta is open now (iOS, Android).

Europe leads the world’s instant payments industry, with $18 trillion in worldwide volume predicted by 2025, up from $3 trillion in 2020 — a growth of more than 500%. Western Europe — and COVID-19 — is now driving that innovation and will account for 38% of instant payment transaction value by 2025. While Europe lacks simple peer-to-peer payments solutions such as Venmo or Square Cash App in the U.S., challenger banks have stepped up to provide similar kinds of services. JoomPay’s opportunity lies in being able to be a middle-man between these various banking systems.

Shopping app Joom, which has been downloaded 150 million times in Europe, has spun-off JoomPay to solve this problem. The app allows users to send and receive money from any person, regardless of whether they use JoomPay or not — and you only need to know their email or the phone number. JoomPay connects to any existing debit/credit card or a bank account. It also provides its users with a European IBAN and an optional free JoomPay card with cashback and bonuses.

Yuri Alekseev, CEO and co-founder of JoomPay, said: “Since COVID-19 started, we’ve seen a significant decline in cash usage. People can’t meet as easily as before but still need to send money, and we offer a viable alternative.”

JoomPay may have an uphill struggle. Its main competitors in Europe are the huge TransferWise, Paysend and, of course, PayPal itself.

Powered by WPeMatico

Latin America (LATAM) is home to one of the fastest-growing mobile markets in the world. In 2018, there were 326 million mobile internet users in the region, and that figure is anticipated to increase to over 422 million users by 2025. Part of the reason for such exponential growth is that mobile is the main tool for internet access in Latin America, providing a portable way for people living in rural areas to get online. The social media boom and rise in messaging platforms in recent years have also spurred demand for optimized mobile services.

As mobile penetration continues in LATAM, it is facilitating innovative apps that promote opportunities for social mobility, financial control, access to overseas markets and societal development. And while a difference in maturity levels and local regulations dictates the mobile landscape for individual countries, there are visible trends throughout the region.

These trends are both reactions to LATAM’s unique mobile conditions and broader international influences, so can be telling of future mobile user expectations and behaviors. By recognizing and assimilating these trends, new mobile apps and services can disrupt the market in a more meaningful way.

Here are the current and upcoming trends of mobile growth across Latin America:

Approximately 70% of Latin America’s population is unbanked or underbanked, meaning there is a huge opportunity to improve financial access. One emerging solution is digital wallets, which work via top-ups and don’t require a bank account with a physical company or branch to set up. Digital wallets, therefore, bypass the mistrust that many Latin Americans have around official banking institutions.

COVID-19 has certainly contributed to the heightened demand for mobile wallets in LATAM. As a predominantly cash-driven location, concerns about handling paper money have been confirmed as new studies reveal that the virus can survive on physical currency for 28 days. In turn, masses of citizens and consumers have begun looking for safer alternatives to cash. In Mexico, digital wallets are thought to occupy a 27.7% share of the business-to-consumer e-commerce payments market by 2021, while Argentina has also been showing high in-store use of digital wallets during the pandemic.

Over in Venezuela, AirTM’s digital wallet has been processing funds promised by interim President Guaidó to essential workers. The company has been instrumental in delivering the money to healthcare staff after the Maduro regime blocked the provider operating in the country. Beyond financial aid, digital wallets in Venezuela and other countries with high inflation rates mean locals don’t have to carry large amounts of bills and coins with them.

Powered by WPeMatico

It’s only been a few months since Lili announced its $10 million seed round, and it’s already raised more funding — namely, a $15 million Series A.

The startup, founded by CEO Lilac Bar David and CTO Liran Zelkha, is creating a bank account and associated products designed for freelancers, with features like early access to direct deposit payments and the ability to set aside a percentage of income for taxes.

The account (and associated Visa debit card) is free of overdraft fees or minimum balance requirements; Bar David said the company only makes money from card processing fees.

She also said that the platform has seen rapid growth this year, with transactions up 700% since the beginning of the pandemic and nearly 100,000 accounts opened since the launch in 2019.

Bar David suggested that the economic turmoil caused by COVID-19 has prompted (or forced) more skilled workers — such as programmers and digital marketers — to turn to freelancing. Meanwhile, she’s also seen “a big shift from part-time freelance to full-time freelance.”

Lili CEO Lilac Bar David

Bar David predicted that the recent growth of the freelance economy won’t simply disappear once the pandemic is over, because workers are discovering the benefits of freelancing.

“If you have a 9-to-5 job, you’re dependent on one employer,” she said. “If something happens you’re out of a job … If you’ve got a diversified customer base, you’re not dependent on just one source of income.”

In recent months, Lili has added new features like automatically generated quarterly income and expense reports, a digital debit card (which customers can use before the physical card arrives in the mail) and the ability to send and receive money via Google Pay (Lili already supported Cash App and Venmo) .

Bar David said the startup decided to raise more funding to expand its engineering team and further accelerate its growth. Apparently she was preparing for a traditional Series A fundraising process (albeit one that was conducted in the middle of a pandemic), but “our current investors were so tremendously impressed by the product-market fit and the growth” that they were willing to fund almost all of the new round.

So the Series A was led by previous investor Group 11, with participation from Foundation Capital, AltaIR Capital, Primary Venture Partners and Torch Capital — along with new backer Zeev Ventures.

“As the global workforce evolves at a rapid pace, we are excited to lead another round of funding to help Lili capitalize on unprecedented demand and offer an entirely new solution to help freelancers seamlessly save time and money,” said Group 11’s Dovi Frances in a statement.

Powered by WPeMatico

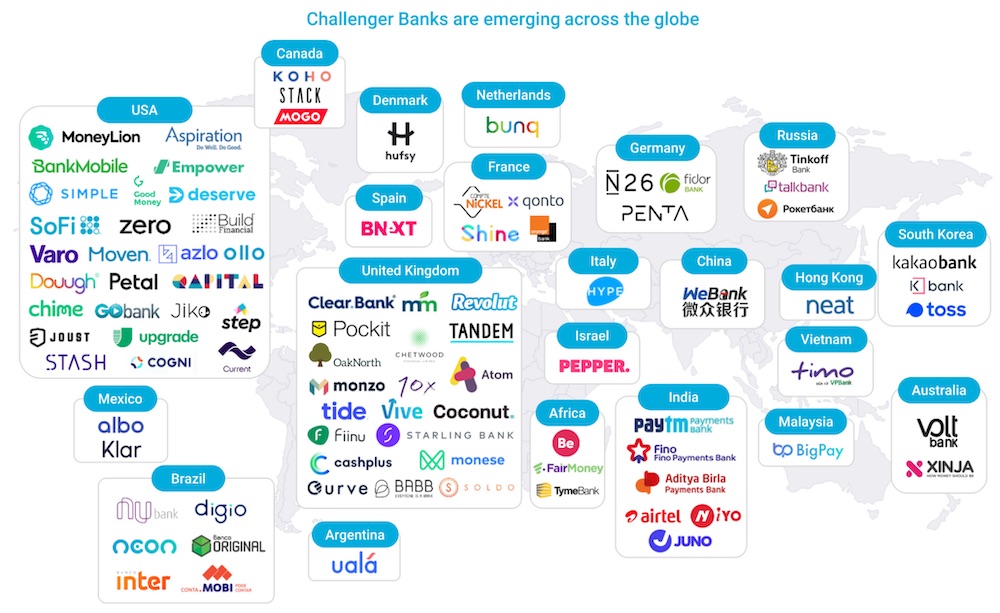

The neobank, or digital bank, phenomenon continues to take the world by storm, with global winners, from Brazil’s Nubank valued at $10 billion and Berlin’s N26 valued at $3.5 billion, to Chime, now valued at $14.5 billion as the most valuable consumer fintech in the United States.

Neobanks have led the charge of the $3.6 billion in venture capital funding for consumer fintech startups this year. And as the coronavirus-fueled acceleration of digital transformation continues, it seems the digital bank is here to stay, with some estimates pointing to neobanks reaching 60 million customers in North America and Europe by the end of 2020, and surpassing 145 million by 2024.

The space is also becoming more crowded, a trend which will only accelerate with fintech eating the world and creating greater infrastructure that enables any company to include a bank account as a product extension.

FT Partners Fintech Industry Research, January 2020

As a result, neobanks are not a monolithic model and not all are created equal. Looking underneath the hood of business models across the globe reveals remarkable operational differences and highlights specific features that are more likely to succeed in the long-term.

Today there are five distinct models that are leading globally:

Interchange-led: Relies on payments revenue, sourced through interchange as the revenue driver. Every time a customer uses the neobank’s card as a payment method they get paid [e.g. Chime / US; Neon (hybrid of 1 & 2) / Brazil].

Credit-led: Leverages a credit-first model, starting off with a credit card or similar offering, and later providing a bank account [e.g. Nubank, Neon (hybrid of 1 & 2) / Brazil].

Powered by WPeMatico

Cryptocurrency exchange Coinbase is adding a new way to withdraw funds from your Coinbase account. If you’ve added a compatible debit card to your account, you can transfer USD, EUR or GBP to your bank account nearly instantly.

There are some drawbacks, and the main one is that you’ll pay a lot of fees. In the U.S., Coinbase deducts 1.5% from the transaction, or a minimum $0.55 if it’s a small transaction. In the U.K. and Europe, you pay 2% in fees or a minimum fee of £0.45/€0.52, respectively.

You also need to have a compatible card. Not all debit cards support incoming transfers. You need to have a Visa card that supports Visa Fast Funds. In the U.S., you can also use a Mastercard card with Mastercard Send.

It’s hard to know whether your bank or card issuer support those features. The best way to figure it out is probably by adding your card to Coinbase and seeing what Coinbase says.

Coinbase isn’t removing other withdrawal methods. For instance, if you’re looking for a cheaper way to withdraw your funds in Europe, a SEPA bank transfer costs €0.15 per transfer. And Coinbase supports instant SEPA transfers if your bank has enabled that.

The company also lets you link your PayPal account with your Coinbase account. Your funds should hit your PayPal account within a few seconds, and there are no fees on Coinbase’s side.

As you can see, there are many ways to move money from your bank account to your Coinbase account. Some of them are slower than others, some of them are more expensive than others. Crypto-to-crypto transactions are a bit simpler by comparison, as you only need your recipient’s wallet address to send tokens.

Image Credits: Coinbase

Powered by WPeMatico

Ahead of the upcoming school year, Apple this morning announced it’s bringing contactless student IDs in Apple Wallet to several more U.S. universities. The expansion will allow more than 100,000 additional college students to carry their student ID on their iPhone or Apple Watch, where it can be used for a variety of tasks, including paying for their meals and snacks and entry into buildings, like the student’s dorm and other campus facilities.

The expanded list of universities includes: Clemson University, Georgetown University, University of Tennessee, University of Kentucky, University of San Francisco, University of Vermont, Arkansas State University, South Dakota State University, Norfolk State University, Louisburg College, University of North Alabama and Chowan University.

These join the previously supported schools: Duke University, University of Oklahoma, University of Alabama, Temple University, Johns Hopkins University, Marshall University and Mercer University.

Apple first announced its plans for contactless student IDs at WWDC 2018, then rolled out to its debut schools last October.

The contactless IDs not only serve as a means of student identification, but also work as a payment mechanism for on-campus transactions — like meals at the cafeteria or textbooks and supplies at the college’s bookstore, for example. Contactless entry into buildings is also now common on college campuses, and these digital IDs can work to open doors, too, as an alternative to swiping an entry card.

Support for college student IDs is only one way that Apple is trying to replace the physical wallet. The company also supports the ability to add your debit and credit cards, transit and loyalty cards, tickets and even paper money through Apple Pay Cash. And now it’s launching its own credit card, too, which rewards you with cashback for shopping Apple and using Apple Pay.

“We’re happy to add to the growing number of schools that are making getting around campus easier than ever with iPhone and Apple Watch,” said Jennifer Bailey, Apple’s vice president of Internet Services, in a statement about the expansion. “We know students love this feature. Our university partners tell us that since launch, students across the country have purchased 1.25 million meals and opened more than 4 million doors across campuses by just tapping their iPhone and Apple Watch.”

Related to this launch, Apple says it’s also adding support for CBORD, Allegion and HID — solution providers for campus credentials and mobile access. With these technologies on board, Apple will be able to reach other schools integrated with these systems in the future.

Powered by WPeMatico

The latest pairing between a tech upstart and a financial titan is a digital prepaid card targeted at Southeast Asia’s 430 million-plus unbanked and underserved population.

On Monday, Razer, the Singapore-based company best known for its gaming laptops and peripherals, announced a partnership with Visa to develop a Visa prepaid solution. The service, which allows unbanked users to top up and cash out easily, will be available as a mini program embedded in Razer Pay, the gaming company’s mobile payments app. That means Razer’s 60 million registered users will be able to pay at any of the 54 million merchant locations around the world that take Visa.

Going virtual is the natural step given the region’s fast-growing digital population, but the pair does not rule out the possibility to introduce a physical prepaid card down the road, Razer’s chief strategy officer Li Meng Lee told TechCrunch over a phone interview.

Both parties have something to gain from this marriage. Hong Kong-listed Razer has in recent years been doubling down on fintech to prove it’s more than a hardware company. Payment services seem like an inevitable development for Razer whose users in the region are accustomed to buying in-game credits at convenience stores.

“For many years, the people who have been making digital payments before it became a sexy word in the last couple of years… [many of them] are the gamers who go to a 7-Eleven, pay in cash, and get a pin code to buy virtual skins for the games,” noted Lee. “Because of that, we’ve been able to build up more than a million service points across Southeast Asia.”

The key differentiator of Razer’s prepaid service, Lee said, is that customers paying at Visa merchants don’t have to already own a bank account, whereas that prerequisite is common for many other e-wallet services.

Razer’s fintech arm Pay is handling transactions for a slew of internet services like Lazada and Grab and has made a big offline push, boasting a network of more than one million touchpoints through retailers including 7-Eleven and Starbucks where it’s accepted.

All in all, Razer claimed it processed over $1.4 billion in payment value last year — but that includes its “merchant services” business, covering on and offline payments, as well as Razer Pay.

The payment app first launched in Malaysia in mid-2018 and recently branched into Singapore as its second market. Lee said the service plans to roll out in the rest of Southeast Asia soon, upon which the Visa prepaid mini app will also be available in those markets.

For Visa, the tie-up with an internet firm could be a potential boost to its reach in the mobile-first Southeast Asia where some 213 million millennials and youths live.

“This is a great opportunity for us to be working with Razer in addressing how we work to bring the unbanked and underserved population into the financial system,” Chris Clark, Visa’s regional president for the Asia Pacific, told TechCrunch. “We will be doing some work with Razer on financial literacy and financial planning to bring that education to the population across the region.”

Razer’s fintech ambition has been evident since it announced to gobble up MOL, a company that offers online and offline payments in Southeast Asia, in April 2018. Besides payments, Lee said other microfinance services such as lending and insurance are also on the cards as part of an effort to ramp up user stickiness for Razer’s fintech arm.

Note: The original version of this article has been updated to correct that Razer’s $1.4 billion in GMV includes merchant services as well as Razer Pay.

Powered by WPeMatico

Japanese messaging app company Line is pumping 20 billion JPY ($182 million) into its mobile payment business as it tries to turn things around following a challenging year in 2018.

The company announced the infusion into Line Pay, a subsidiary that it fully owns, in a filing that stated the new capital is “necessary funds for its future business operation.” No further details were provided.

The investment comes on the heels of Line’s latest financial report which saw it post a 5.79 billion JPY loss as revenue grew by 24 percent to reach 207.18 billion JPY in 2018. Line has long been a top money maker in the App Store, but its efforts to build out content around its messaging platform and games division have turned out to be expensive, with a job service, manga platform and e-commerce business among its ventures.

In addition to more content, payments are also seen as “glue” that can increase engagement within the Line ecosystem and its main messaging app.

The company is going after the cashless opportunity in Japan, where it is the dominant chat app with an estimated 50 million registered users. The country is notable for its continued use of cash, but the government is using the upcoming 2020 Olympic Games as an opportunity to move toward a digital future. Aside from its core Line Pay service, which sits inside the Line chat app, Line is introducing its own credit card with Visa and has gone after Chinese tourists through a tie-in with Tencent, the internet giant behind China’s top messaging app WeChat.

Outside of Japan, Line Pay is also available in Thailand (where it works with the Bangkok metro provider), Taiwan (where it counts two banks as partners) and Indonesia, which Line says are its next three largest markets in terms of user numbers. Together, across those four countries, Line claims it has 165 million monthly active users and 40 million registered Line Pay users. Line said GMV reached 55 billion JPY ($482 million) per month back in November 2017; there’s been no update since.

The service was launched more widely but it has shuttered in other markets, including Singapore where it was ended in February 2018.

Beyond payment, Line is also moving into banking and financial services. It is working to launch a digital bank in Japan and last year it announced plans to investigate the potential to roll out loans, insurance and other services backed by its own cryptocurrency. While it didn’t hold an ICO — its “Link” token is earned or can be bought on exchanges — Line did dive into crypto in a major way, opening its own exchange and starting a crypto investment fund, too. With the bear market in full effect, and token valuations dropping by 90 percent across the board, we haven’t heard too much more from Line regarding its crypto plans.

Powered by WPeMatico

A little more retail momentum for Apple Pay: Apple has announced another clutch of U.S. retailers will soon support its eponymous mobile payment tech — most notably discount retailer Target.

Apple Pay is rolling out to Target stores now, according to Apple, which says it will be available in all 1,850 of its U.S. retail locations “in the coming weeks.”

Also signing up to Apple Pay are fast food chains Taco Bell and Jack in the Box; Speedway convenience stores; and Hy-Vee supermarkets in the Midwest.

“With the addition of these national retailers, 74 of the top 100 merchants in the US and 65 per cent of all retail locations across the country will support Apple Pay,” notes Apple in a press release.

Speedway customers can use Apple Pay at all of its approximately 3,000 locations across the Midwest, East Coast and Southeast from today, according to Apple, as well as at Hy-Vee stores’ more than 245 outlets in the Midwest.

It says the payment tech is also rolling out to more than 7,000 Taco Bell and 2,200 Jack in the Box locations “in the next few months.”

Back in the summer Apple announced it had signed up longtime holdout CVS, with the pharmacy introducing Apple Pay across its ~8,400 standalone locations last year.

Also signing up then: 7-Eleven, which Apple says has now launched support for Apple Pay in 95 percent of its U.S. convenience stores in 2018.

Last year retail giant Costco also completed the rollout of Apple Pay to its more than 500 U.S. warehouses.

While, in December, Apple Pay also finally launched in Germany — where Apple slated it would be accepted at a range of “supermarkets, boutiques, restaurants and hotels and many other places” at launch, albeit “cash only” remains a common demand from the country’s small businesses.

Update: In a blog post about the Apple Pay launch, Target confirmed that users of its Target REDcard credit or debit cards cannot use the store payment card with Apple Pay.

The retail giant also said it will soon support contactless mobile payment technologies on the Android smartphone platform, naming Google Pay and Samsung Pay specifically, as well as supporting contactless payment cards from Mastercard, Visa, American Express and Discover.

“Offering guests more ways to conveniently and quickly pay is just another way we’re making it easier than ever to shop Target,” said Target’s chief information officer, Mike McNamara, in a statement.

Powered by WPeMatico

Apple’s mobile payment technology has finally launched in Germany, some four years after it debuted in the U.S.

On its newly launched Apple Pay website for Germany, Apple lists partner banks and credit card companies at launch, with customers from the likes of Deutsche Bank, O2 Banking, N26, Comdirect, HypoVerensbank, Bunq and Boon able to tap up the payment method directly.

Some fifteen banks and services are supported at launch. A further nine banks are slated as adding support in 2019, including DKB, INK and Revolut.

iOS users in the country can now add supported debit or credit cards to Apple Pay to make contactless payments with their device, rather than having to carry cash. Apple’s Face ID and Touch ID biometrics are used to a security layer to the payment system.

The local Apple Pay site also lists a selection of retailers, with Apple writing: “Apple Pay works in supermarkets, boutiques, restaurants, hotels and many other places. You can also use Apple Pay in many apps — and on participating websites with Safari on your Mac, iPhone or iPad.”

Aside from convenience, the other consumer advantage Apple touts for the system is privacy, with Apple Pay using a device-specific number and unique transaction code — and the user’s actual card numbers never stored on their device or on Apple’s servers — which means trackable card numbers aren’t shared with merchants, so purchases can’t be tied back to the individual.

While that might sound like an abstract concern, a Bloomberg report this summer revealed details of a multi-million deal in which Google pays for transaction data from Mastercard — in order to try to link online ad views with offline purchases in the US.

Facebook has also long been known to buy offline data to supplement the interest signals it collects on users from inside (and outside) its social network — further fleshing out ad-targeting profiles.

So escaping the surveillance net of one flavor of big tech can require buying into another. Or else going low tech and paying in cash.

Apple does not say what took it so long to add Germany to its now pretty long list of Apple Pay countries but Apple Insider suggests the relatively late adoption was down to pushback from local banks over fees, noting that it’s four months after the official announcement of a German launch.

It’s also true that paying by plastic isn’t always an option in Germany, as cash remains the dominant payment method of choice — also, seemingly, for privacy purposes. So Apple Pay is at least aligned with those concerns.

Powered by WPeMatico