Mobile payments

Auto Added by WPeMatico

Auto Added by WPeMatico

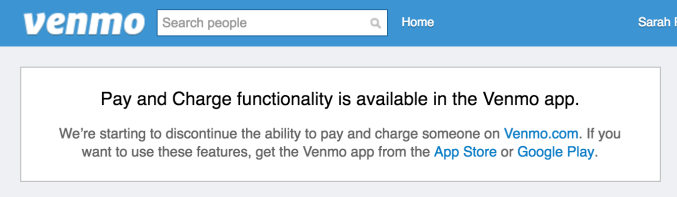

PayPal-owned, peer-to-peer payments app Venmo is ending web support for its service, the company announced in an email to users. The changes, which are beginning to roll out now, will see the Venmo .com website phasing out support for making payments and charging users. In time, users will see even less functionality on the website, the company says.

The message to users was quietly shared in the body of Venmo’s monthly transaction history email. It reads as follows:

NOTICE: Venmo has decided to phase out some of the functionality on the Venmo.com website over the coming months. We are beginning to discontinue the ability to pay and charge someone on the Venmo.com website, and over time, you may see less functionality on the website – this is just the start. We therefore have updated our user agreement to reflect that the use of Venmo on the Venmo.com website may be limited.

The decision represents a notable shift in product direction for Venmo. Though best known as a mobile payments app, the service has also been available online, similar to PayPal, for many years.

The Venmo website today allows users to sign in and view their various transaction feeds, including public transactions, those from friends, and personal transactions. You can also charge friends and submit payments from the website, send payment reminders, like and comment on transactions, add friends, edit your profile, and more.

Some users may already be impacted by the changes, and will now see a message alerting them to the fact that charging friends and making payments can only be done in the Venmo app from the App Store or Google Play.

It’s not entirely surprising to see Venmo drop web support. As a PayPal-owned property after its acquisition by Braintree which later brought it to PayPal, there’s always been a lot of overlap between Venmo and its parent company, in terms of peer-to-peer payments.

Venmo had grown in popularity for its simple, social network-inspired design and its less burdensome fee structure among a younger crowd. This made it an appealing way for PayPal to gain market share with a different demographic.

It’s also cheaper, which people like. PayPal doesn’t charge for money transfers from a bank account or PayPal balance, but does charge 2.9 percent plus a $0.30 fixed fee on payments from a credit or debit card in the U.S. Venmo, meanwhile, charges a fee of 3 percent for credit card payments, but makes debit card payments free. That’s appealing to millennials in particular, many of whom have ditched credit cards entirely, and are careful about their spending.

Plus, as a mobile-first application, Venmo was offering a more modern solution for mobile payments, at a time when PayPal’s app was looking a bit long in the tooth. (PayPal has since redesigned its mobile app experience to catch up.)

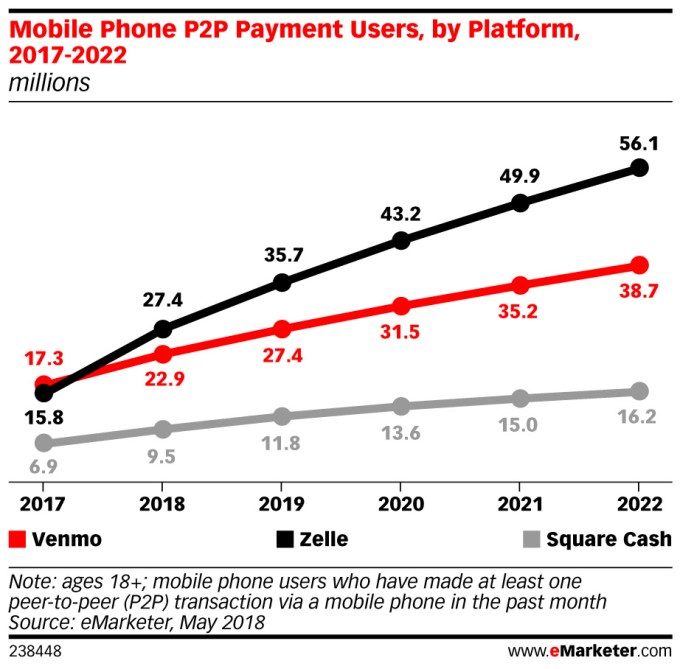

Another factor in Venmo’s decision could be that, more recently, it began facing competition from newcomer Zelle, the bank-backed mobile payments here in the U.S. which is forecast to outpace Venmo on users sometime this year, with 27.4 million users to Venmo’s 22.9 million. In light of that threat, Venmo may have wanted to consolidate its resources on its primary product – the mobile app.

Not everyone is happy about Venmo’s changes, of course. After all, even if the Venmo website wasn’t heavily used, it was used by some who will certainly miss it.

@venmo i only use the website to send/receive payments so in guess you’re cancelled!

— respectfully yours (@biking_away_) June 15, 2018

@venmo This makes me really #sad….”Venmo has decided to phase out some of the functionality on the https://t.co/Dw7W551BsL website over the coming months.” #CanWeGoBackToHowItWas

— V Lav (@Druzy920) June 14, 2018

@venmo Why are you breaking your website?

— Lozaning (@lozaning) June 14, 2018

@VenmoSupport @venmo Just got an email saying you’re phasing out website functions. What’s the justification? Pay and charge by web is incredibly useful.

— Woode (@Woode2380) June 14, 2018

Venmo email: “We are beginning to discontinue the ability to pay and charge someone on the https://t.co/iAFTbn3EY0 website, and over time, you may see less functionality on the website – this is just the start.”

Is this a threat?

— Noah Mittman (@noahmittman) June 14, 2018

Reached for comment, Venmo explained the decision to phase out the website functionality stems from how it sees its product being used.

A Venmo spokesperson told TechCrunch:

Venmo continuously evaluates our products and services to ensure we are delivering our users the best experience. We have decided to begin to discontinue the ability to pay and charge someone on the Venmo.com website. Most of our users pay and request money using the Venmo app, so we’re focusing our efforts there. Users can continue to use the mobile app for their pay and charge transactions and can still use the website for cashing out Venmo balances, settings and statements.

The company declined to clarify what other functionality may be removed from the website over time, but noted that using Venmo to pay authorized merchants is unaffected.

Powered by WPeMatico

Despite some concerns over its adoption by scammers, new payment service Zelle is shaping up to overtake rival Venmo this year, according to a new forecast from eMarketer. The firm expects Zelle to grow more than 73 percent in 2018, to reach 27.4 million users in the U.S., ahead of Venmo’s 22.9 million. Square Cash will trail with 9.5 million users.

This growth isn’t necessarily chalked up to user preference, but rather, ubiquity.

Zelle is backed by a network of over 30 U.S. banks, as their means of winning over users from other payment apps including Venmo, PayPal, and Square Cash. The banks had wanted to develop their own alternative these apps for several years, but only recently had those efforts gained momentum. The Zelle website now claims participation from over 100 financial institutions, as well as processor partners CO-OP Financial Services, FIS, Fiserv and Jack Henry, and network partners VISA and MasterCard.

The participating banks are now integrating Zelle into their own websites and mobile apps – meaning, users are finding Zelle as they use their existing banking applications. They’re not seeking it out directly, in many cases.

“One of the main hurdles new apps face is building trust and a sizable audience,” explained eMarketer forecasting analyst Cindy Liu. “But Zelle has leapfrogged the early stages of adoption by having the benefit of being embedded into the already existing apps of participating banks,” she said.

Earlier this year, Zelle said it was signing up users at a rate of 100,000 consumers per day, and claimed it had processed 247 million payments totaling $75 billion in 2017. That’s a sizable chunk of the peer-to-peer payments market.

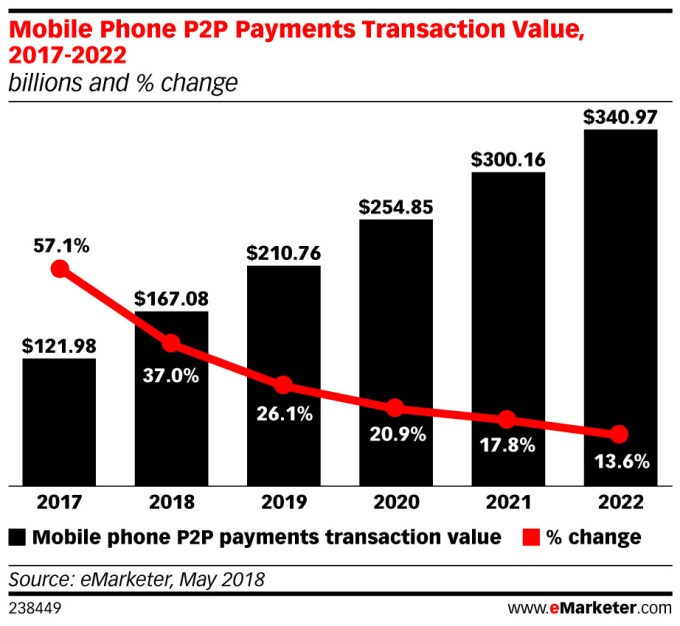

Emarketer’s forecast estimates the total number of U.S. p2p mobile payment users will grow 30 percent in 2018 to reach 82.5 million people, or 40.5 percent of U.S. smartphone users. It also expects the total transaction volume of p2p mobile payments to grow 37 percent this year to reach $167.08 billion. By 2021, that figure will reach over $300 billion.

That leaves room for all services to carve out their piece of the market, even if Zelle ends up in the lead.

Powered by WPeMatico

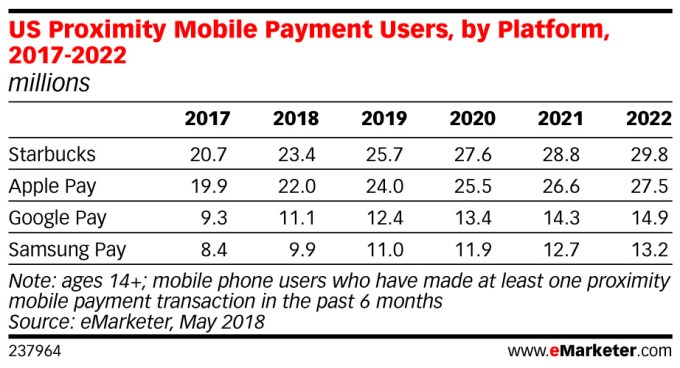

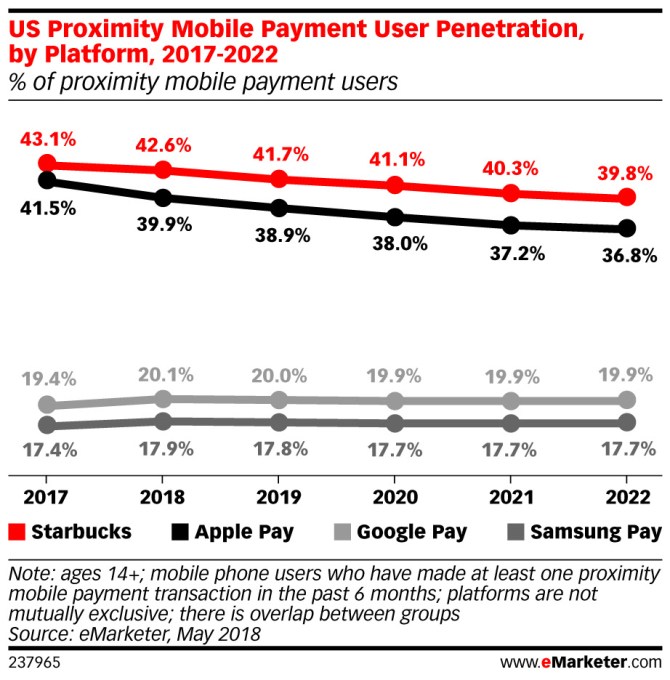

People really love getting their coffee more quickly. Starbucks, which has operated its own mobile payments service since 2011, is the market leader in terms of mobile payments users, beating out Apple Pay, Google Pay, and Samsung Pay, according to a new reporter from eMarketer out this morning. However, Starbucks’ lead over Apple Pay is only a small one – in 2017, it had 20.7 million U.S. users compared with Apple Pay’s 19.7 million. And that gap will remain small this year, with 23.4 million using Starbucks’ mobile payments compared with 22 million using Apple Pay.

The wide adoption of the Starbucks mobile payment service is not only due to speed and convenience that the barcode-based payment system offers – it’s also because payments are tied to loyalty, and the Starbucks app is where customers can monitor and manage their card balance and their “star rewards.” In addition, Starbucks has the benefit of being able to offer a consistent payments experience across its stores – there’s never a question in consumers’ minds as to whether they can use its mobile payments service. They know they can.

Other mobile proximity payment services don’t have the same advantage, as many retailers still don’t offer payment terminals that support the tap-to-pay services like Apple Pay and Google Pay.

According to eMarketer’s forecast, 23.4 million people ages 14 and older will use the Starbucks app to make a point-of-sale purchase at least once every six months, compared with 22 million who will use Apple Pay, 11.1 million who will use Google Pay, and 9.9 million who will use Samsung Pay.

Those numbers will increase across the board through 2022, but the rankings will remain the same – with Starbucks then seeing 29.8 million users to Apple Pay’s 27.5 million.

However, this forecast appears to be discounting the impact of the recent expansion of Apple Pay, which will allow users to send payments to friends through iMessage. When you receive this money, it’s added to an Apple Pay Cash card in your iPhone’s Wallet, which can then be used in stores, in addition to in apps or online. This built-in payments service inside one of the largest messaging platforms could prompt more users to adopt Apple Pay, even if they hadn’t before.

Another note: it seems which services are more popular than others is also tied to how long they’ve been around.

Apple Pay launched before Samsung and Google Pay, and is now accepted at more than half of U.S. merchants. Google Pay isn’t as widely accepted, but is pre-installed on Android, which will help it grow. Samsung Pay, meanwhile, has the lowest adoption in terms of users, but is most accepted by merchants, says eMarketer.

The rankings of the various payment services wasn’t the only notable finding from eMarketer’s new report.

The analysts also found that this year, for the first time, more than 25 percent of U.S. smartphone users ages 14 and older, will have used a mobile payment service at least once every six months. The number of payments users will increase by 14.5 percent to reach 55 million by the end of 2018, the firm estimates.

But over the next several years, these top four services will see their share of the mobile payments drop, even as their user numbers grow. That’s because they’ll face increased competition from other new payment apps, including those from merchants themselves.

“Retailers are increasingly creating their own payment apps, which allow them to capture valuable data about their users. They can also build in rewards and perks to boost customer loyalty,” eMarketer forecasting analyst Cindy Liu says.

eMarketer’s forecast (paywalled) is based on an analysis of third-party data, including Forrester, Juniper Research, and Crone Consulting’s data on U.S. mobile payments users.

Note: Updated after publication to clarify the data is focused on U.S. mobile users

Powered by WPeMatico

Google Pay got a big upgrade at Google I/O this week. At a breakout session, Google announced a series of changes to its payments platform, recently rebranded from Android Pay, including support for peer-to-peer payments in the main Google Pay app; online payments support in all browsers; the ability to see all payments in a single place, instead of just those in-store; and support for tickets and boarding passes in Google Pay’s APIs, among several other things.

Some of Google Pay’s expansions were previously announced, like its planned support for more browsers and devices, for example.

However, the company detailed a host of other features at I/O that are now rolling out across the Google Pay platform.

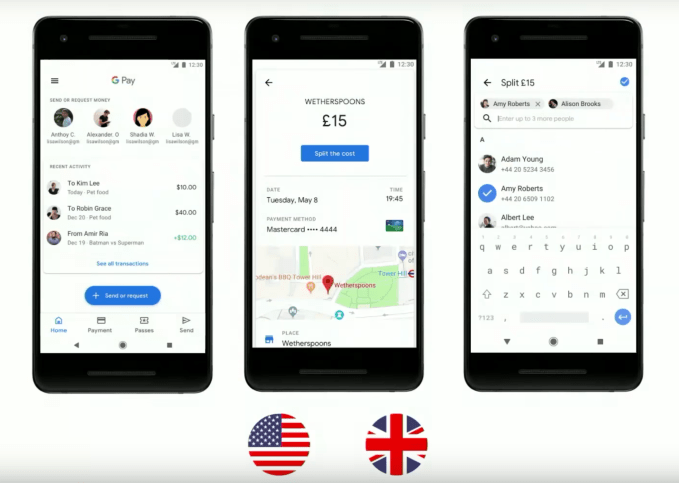

One notable addition is support for peer-to-peer payments which is being added to the Google Pay app in the U.S. and the U.K.

And that transaction history, along with users’ other payments, will all be consolidated into one place.

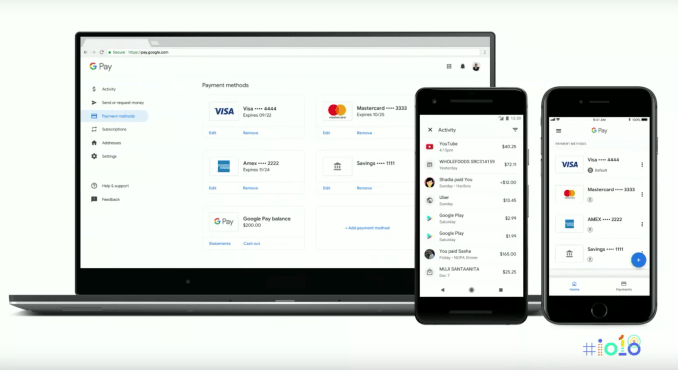

“In an upcoming update of the Google Pay app, we’re going to allow you to manage all the payment methods in your Google account – not just the payment methods that you used to pay in-store,” said Gerardo Capiel, Product Management lead at Google Pay, during the session at I/O. “And even better, we’re going to provide you with a holistic view of all your transactions – whether they be on Google apps and services, such as Play and YouTube, whether they be with third-party merchants, such as Walgreens and Uber, or whether they’re transactions you’ve made to friends and families via our peer-to-peer service,” he said.

The company also said it would allow users to send and request money, manage payment info linked to their Google accounts, and see their transaction history on the web with the Google Pay iOS app, too.

And because I/O is a developer conference, many of the new additions were in the form new and updated APIs.

For starters, Google launched a new API for incorporating Google Pay into other third-party apps.

“Via our APIs, we’re going to enable these ready-to-pay users [who already have payment information stored with Google Pay] to also checkout quickly and easily in your own apps and websites,” Capiel said.

The benefit to those developers who add Google Pay support is an increase in conversion rates and faster monetization, he noted.

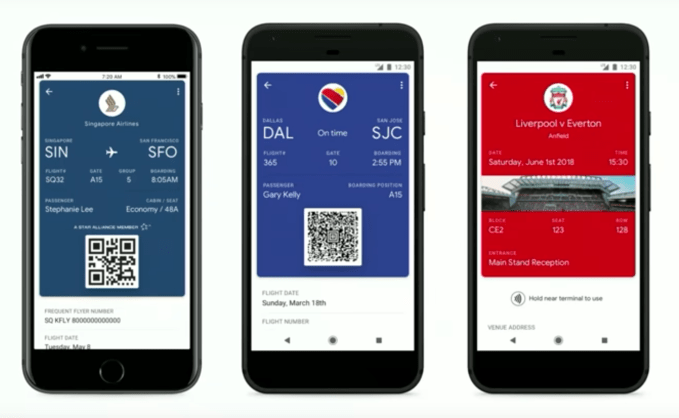

Plus, Google added support for tickets and boarding passes to the Google Pay APIs, where they joined the existing support for offers and loyalty cards.

This allows companies such as Urban Airship or DotDashPay to help business clients distribute and update their passes and tickets to Google Pay users.

“It shows an even stronger commitment on Google Pay’s part to make the digital wallet a priority,” Sean Arietta, founder and CEO of DotDashPay, told TechCrunch, following the presentation. “It also reinforces their focus on partners like DotDashPay to help build connections between consumers and brands. The fact that they are specifically highlighting a complete experience that starts with payments and ends with an NFC tap-to-identify, is really powerful. It makes the Google Pay story now complete,” he added.

Urban Airship was also touting the changes earlier this week, via a press release.

“We help businesses reinvent the customer experience by delivering the right information at the right time on any digital channel, and mobile wallets fill an increasingly critical role in that vision,” Brett Caine, CEO and president of Urban Airship, said in a statement. “Google Pay’s new support for tickets and boarding passes means customers will always have up-to-date information when they need it most – on the go.”

Some of Google’s early access partners on ticketing include Singapore Airlines, Eventbrite, Southwest, and FortressGB, which handles major soccer league tickets in the U.K. and elsewhere.

In terms of transit-related announcements, Google added a few more partners who will soon adopt Google Pay integration, including Vancouver, Canada and the U.K. bus system, following recent launches in Las Vegas and Portland.

The company also offered an update on Google Pay’s traction, noting the Google Pay app just passed 100 million downloads in the Google Play store, where it’s available to users in 18 markets worldwide.

Soon, Google said it will launch many of the core features and the Google Pay app globally to billions of Google users worldwide.

Powered by WPeMatico

As we reported last month, Google is uniting all of its different payment tools under the Google Pay brand. On Android, however, the Android Pay app stuck with its existing brand. That’s changing today, though, with the launch of Google Pay for Android. With this, Google is rolling out an update to Android Pay and introducing some new functionality that the company hopes will make… Read More

As we reported last month, Google is uniting all of its different payment tools under the Google Pay brand. On Android, however, the Android Pay app stuck with its existing brand. That’s changing today, though, with the launch of Google Pay for Android. With this, Google is rolling out an update to Android Pay and introducing some new functionality that the company hopes will make… Read More

Powered by WPeMatico

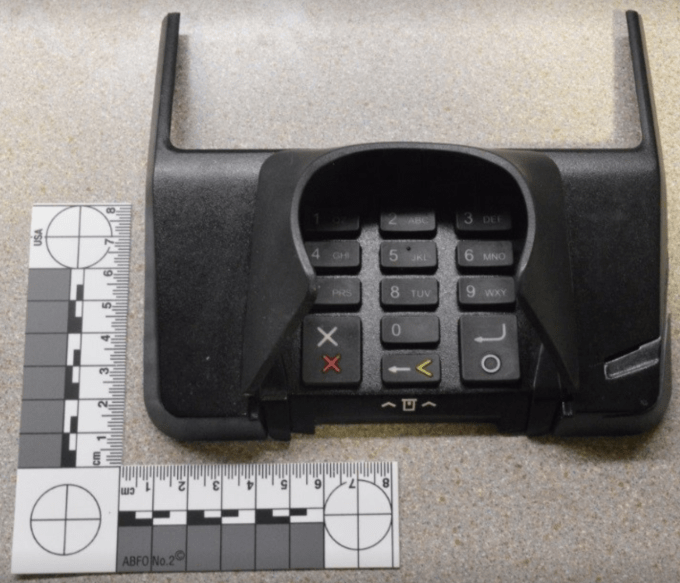

Police in Lower Pottsgrove, Pennsylvania have spotted a group of thieves who are placing completely camouflaged skimmers on top of credit card terminals in Aldi stores. The skimmers, which the gang placed in plain sight of surveillance video cameras, look exactly like the original credit card terminals but would store debit card numbers and PINs of unsuspecting shoppers. “While Aldi… Read More

Police in Lower Pottsgrove, Pennsylvania have spotted a group of thieves who are placing completely camouflaged skimmers on top of credit card terminals in Aldi stores. The skimmers, which the gang placed in plain sight of surveillance video cameras, look exactly like the original credit card terminals but would store debit card numbers and PINs of unsuspecting shoppers. “While Aldi… Read More

Powered by WPeMatico

iZettle — the commerce platform based out of Stockholm that competes against companies like Square, Paypal and SumUp to provide card transactions using smartphones and tablets as well as related accounting services — has raised another €40 million ($47 million) as it approaches a $1 billion valuation. CEO and co-founder Jacob de Geer told TechCrunch the money will go towards… Read More

iZettle — the commerce platform based out of Stockholm that competes against companies like Square, Paypal and SumUp to provide card transactions using smartphones and tablets as well as related accounting services — has raised another €40 million ($47 million) as it approaches a $1 billion valuation. CEO and co-founder Jacob de Geer told TechCrunch the money will go towards… Read More

Powered by WPeMatico

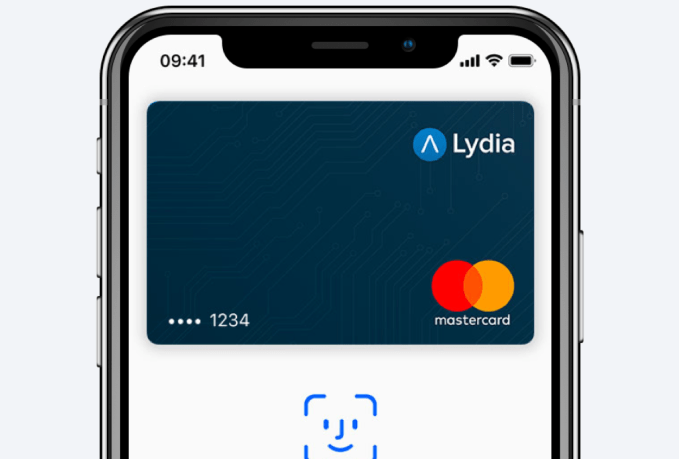

A peer-to-peer payment app that works similarly to Venmo from startup Lydia in France now works with Apple Pay (a feature originally announced in July), making it possible to spend your balance from the app wherever MasterCard and Apple Pay are accepted. It’s a neat use of Apple Pay to make it possible to do mobile payments without requiring that a user have a credit card – and it… Read More

A peer-to-peer payment app that works similarly to Venmo from startup Lydia in France now works with Apple Pay (a feature originally announced in July), making it possible to spend your balance from the app wherever MasterCard and Apple Pay are accepted. It’s a neat use of Apple Pay to make it possible to do mobile payments without requiring that a user have a credit card – and it… Read More

Powered by WPeMatico

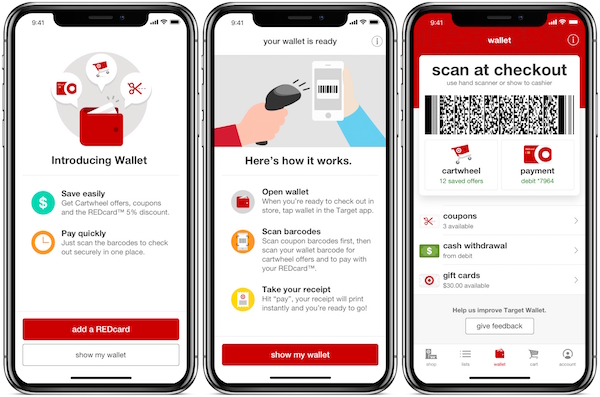

As promised earlier, Target today launched its own mobile payments system with the introduction of “Wallet” in the Target app. Wallet, as the name implies, allows Target shoppers in-store to both check out using their smartphone as well as take advantage of their Cartwheel digital coupons and discounts with only one scan of their barcode. Already, Cartwheel savings in… Read More

As promised earlier, Target today launched its own mobile payments system with the introduction of “Wallet” in the Target app. Wallet, as the name implies, allows Target shoppers in-store to both check out using their smartphone as well as take advantage of their Cartwheel digital coupons and discounts with only one scan of their barcode. Already, Cartwheel savings in… Read More

Powered by WPeMatico

Wells Fargo’s ATMs are getting an upgrade. The bank announced today that more than 40 percent – or over 5,000 of its ATMs – will now allow customers to perform transactions without having to pull out their bank card. Instead, users can take advantage of NFC – aka the “tap and pay” technology that powers mobile wallet systems like Apple Pay, Android Pay,… Read More

Wells Fargo’s ATMs are getting an upgrade. The bank announced today that more than 40 percent – or over 5,000 of its ATMs – will now allow customers to perform transactions without having to pull out their bank card. Instead, users can take advantage of NFC – aka the “tap and pay” technology that powers mobile wallet systems like Apple Pay, Android Pay,… Read More

Powered by WPeMatico