initial public offering

Auto Added by WPeMatico

Auto Added by WPeMatico

Gingko Bioworks, a synthetic biology company now valued at around $15 billion, begins trading on the New York Stock Exchange today.

Gingko’s market debut is one of the largest in biotech history. It’s expected to raise about $1.6 billion for the company. It’s also one of the biggest SPAC deals done to date — Gingko is going public through a merger with Soaring Eagle Acquisition Corp., which was announced in May.

Shares opened at $11.15 each this morning under the ticker DNA — biotech dieharders will recognize it as the former ticker used by Genentech.

The exterior of the NYSE is decked out in Gingko décor. The imagery is clearly sporting Jurassic Park themes, as MIT Tech Review’s Antonio Regalado pointed out. It’s probably intentional: Jason Kelly, the CEO of Ginkgo Bioworks, has been re-reading “Jurassic Park” this week, he tells TechCrunch.

The décor also sports a company motto: “Grow everything.”

Ginkgo was founded in 2009, and now bills itself as a synthetic biology platform. That’s essentially premised on the idea that one day, we’ll use cells to “grow everything,” and Gingko’s plan is to be that platform used to do that growing.

Kelly, who often uses language borrowed from computing to describe his company, likens DNA to code. Gingko, he says, aims to “program cells like you can program computers.” Ultimately, those cells can be used to make stuff: like fragrances, flavors, materials, drugs or food products.

The biggest lingering question over Gingko, ever since the SPAC deal was announced, has centered on its massively high valuation. When Moderna, now a household name thanks to its COVID-19 vaccines, went public in 2018, the company was valued at $7.5 billion. Gingko’s valuation is double that number.

“I think that surprises people to be honest,” Kelly says.

Ginkgo’s massive valuation seems even starker when you look at its existing revenues. SEC documents show that the company pulled in $77 million in revenue in 2020, which increased to about $88 million in the first six months of 2021 (per an August investor call). The company has also reported losses: including $126.6 million in December 2020 and $119.3 million in 2019.

Gingko is aiming to increase revenue a significant amount in 2021. SEC documents initially noted that the company aimed to draw about $150 million in revenue in 2021, but the August earning call updated that total for the year to over $175 million.

Gingko aims to make money in two ways: first it contracts with manufacturers during the research and development phase (i.e. while the company works out how to manufacture a cell that spits out a certain fragrance, bio-based nylon or meatless burger). That process happens in Gingko’s “foundry,” a massive factory for bioengineering projects.

This source of money is already starting to flow. Gingko reported $59 million in foundry revenue for 2020, and anticipates $100 million in 2021, per the August investor call.

This revenue, though, isn’t covering the full costs of Gingko’s operations, according to the information shared by the company in SEC documents. It is covering an increasing share, though, and as Gingko scales up its platform, costs will come down. Based on fees alone, Kelly projects Gingko will break even by 2024 or 2025.

The second type of revenue comes from royalties, milestone payments or, in some cases, equity stakes in the companies that go on to sell products, like fragrances or meatless burgers, made using Gingko’s facilities or know-how. It’s this source of income that will make up the vast majority of the company’s future worth, according to its expectations.

Once the product is made and marketed by another company, it requires little to no more work on Gingko’s part — all the company does is collect cash.

The company is often hesitant to incorporate these earnings into projections, because they rely on other companies bringing products to market. That means it’s hard to know for sure when these downstream payments will emerge. “In our models, we are very sensitive that, at the end of the day, they’re not our products. I cannot predict when Roche might bring a drug to market and give me my milestones,” says Kelly.

Kelly says there’s evidence this model will start to work in the near-term.

Gingko earned a “bolus” milestone payment of 1.5 million shares of The Cronos Group, a cannabis company, for developing a commercially viable, lab-grown rare cannabinoid called CBG for commercial use (there are seven more in strains development, says Kelly). These milestone payments (in cash or shares) are earned when a company achieves some predetermined goal using Gingko’s platform.

Gingko has also worked with Aldevron to manufacture an enzyme critical to the production of mRNA vaccines, and plans to collect royalty payments from that relationship — though no foundry fees were collected from this project.

Finally, Gingko has negotiated an equity stake in Motif Foodworks, a spinout company based on its technology. That company has so far raised about $226 million, and will aim to launch a lab-grown beef product developed at Gingko’s foundry, paying Gingko the aforementioned foundry fees already for this contribution.

This rich source of cash will depend a lot on the outside contractor’s ability to manufacture and sell products made using Gingko’s platform. This opens the company up to some risk that’s beyond its control. Maybe, for instance, it turns people don’t want bio-manufactured meat as much as many anticipated — that means some types of downstream payments may not materialize.

Kelly says he’s not particularly worried about this. Even if one particular program fails, he’s planning on having so many programs running that one or two are bound to succeed.

“I’m just sorta like: some will work, some won’t work. Some will take a year, some will take three years. It doesn’t really matter, as long as everybody is working with us,” he says. “Apple doesn’t stress about what apps are going to be the next big app in the app store,” he continues.

One key metric to watch for Gingko going forward will be how many new cell programs they’re managing to close. So far, Gingko has added 30 programs this year, says Kelly. Last year, there were 50 programs.

Remember: Some of the projects are Gingko spinouts, like Motif Foodworks, not customers that come to the platform on their own. And historically, the number of companies Gingko has partnered with has been a point of criticism. Per SEC documents, the majority of revenue came from two large partners in 2020 — though Kelly told Business Insider that this was a pandemic-related downturn.

The more programs Gingko has, the more it becomes insulated from the success or failure of any one product. Plus it’s a sign that people are at least using the “app store” for biology.

“The biggest value driver of Gingko is how quickly we add programs,” Kelly says.

Powered by WPeMatico

Rivian, the electric vehicle startup backed by a host of institutional and strategic investors, including Ford and Amazon, has confidentially filed paperwork with the U.S. Securities and Exchange Commission to go public.

The size and price range for the proposed offering have yet to be determined. The initial public offering is expected to take place after the SEC completes its review process, subject to market and other conditions, the brief statement said.

The confidential filing comes less than two months since Rivian announced it had closed a $2.5 billion private funding round led by Amazon’s Climate Pledge Fund, D1 Capital Partners, Ford Motor and funds and accounts advised by T. Rowe Price Associates Inc. Third Point, Fidelity Management and Research Company, Dragoneer Investment Group and Coatue also participated in that round.

The company did not share a post-money valuation at the time of the July 2021 announcement.

The electric automaker, which now employs 7,000 people, is preparing to deliver its R1T pickup truck in September. The road to produce the R1T and an accompanying SUV requires capital, which Rivian has had little trouble raising.

Rivian has raised roughly $10.5 billion to date. In January, the company brought in $2.65 billion from existing investors T. Rowe Price Associates Inc., Fidelity Management and Research Company, Amazon’s Climate Pledge Fund, Coatue and D1 Capital Partners. New investors also participated in that round, which pushed Rivian’s valuation to $27.6 billion, a source familiar with the investment round told TechCrunch at the time.

Developing….

Powered by WPeMatico

ForgeRock filed its form S-1 with the Securities and Exchange Commission (SEC) this morning as the identity management provider takes the next step toward its IPO.

The company did not provide initial pricing for its shares, which will trade on the New York Stock Exchange under the symbol FORG. The IPO is being led by Morgan Stanley and J.P. Morgan Chase & Co., with the company being valued as high as $4 billion, according to Bloomberg, which is a significant uplift over the $730 million post-money value that PitchBook had for the company after its last round in 2020.

With the ever-increasing volume of cybersecurity attacks against organizations of all sizes, the need to secure and manage user identities is of growing importance. Based in San Francisco, ForgeRock has raised $233 million in funding across multiple rounds. The company’s last round was a $93.5 million Series E announced in April 2020, which was led by Riverwood Capital alongside Accenture Ventures. At that time, CEO Fran Rosch told TechCrunch that the round would be the last before an IPO, which was also what former CEO Mike Ellis told us after the startup’s $88 million Series D in September 2017.

While the timing of its IPO might have been unclear over the last few years, the company has been on a positive trajectory for growth. In its S-1, ForgeRock reported that as of June 30, its annual recurring revenue (ARR) was $155 million, representing 30% year-over-year growth.

While revenue is growing, losses are narrowing as the company reported a $20 million net loss down from $36 million a year ago. There certainly is a whole lot of room to grow, as the company estimates that the total global addressable market for identity services to be worth $71 billion.

Among the many competitors that ForgeRock faces is Okta, which went public in 2017 and has been growing in the years since. In March, Okta acquired cloud identity startup Auth0 for $6.5 billion in a deal that raised a few eyebrows. Another competitor is Ping Identity, which went public in 2019 and is also growing, reporting on August 4 that its ARR hit $279.6 million in its quarter ended June 30, for a 19% year-over-year gain. There have also been a few big exits in the space over the years, including Duo Security, which was acquired by Cisco for $2.35 billion in 2018.

“ForgeRock has a good access management tool and they continue to be a strong player in customer identity and access management (CIAM),” commented Michael Kelley, senior research director at Gartner.

Kelley noted that in 2020, ForgeRock converted most of its core access management services to a SaaS delivery model, which helped the company catch up with the rest of the market that already offered access management as SaaS. Also last year the company expanded into identity governance, introducing a brand new identity, governance and administration (IGA) product.

“I think one of the more interesting products that ForgeRock offers is ForgeRock Trees, which is a no-code/low-code orchestration tool for building complex authentication and authorization journeys for customers, which is particularly helpful in the CIAM market,” Kelly added.

ForgeRock was founded in 2010, but its roots go back even further to an open-source single sign-on project known as OpenSSO that was created by Sun Microsystems in 2005. When Oracle acquired Sun Microsystems in early 2010, a number of its open-source efforts were left to languish, which is what led a number of former Sun employees to start ForgeRock.

Over the last decade, ForgeRock has expanded significantly beyond just providing a single sign-on to providing an identity platform that can handle consumer, enterprise and IoT use-cases. The company’s platform today handles identity and access management as well as identity governance.

The ability to scale is a key selling point that ForgeRock makes in the S-1, noting that its platform can handle over 60,000 user-based access transactions per second per customer.

“As of June 30, 2021, we had four customers with 100 million or more licensed identities, the company stated in the S-1. “Our ability to serve mission-critical needs in complex environments for large customers enables us to grow our base of large customers and expand within each of them. “

Powered by WPeMatico

Update: Trading of Robinhood shares has been halted due to volatility. The company’s stock paused at $65.60 on Robinhood itself. Yahoo Finance has a higher $77.03 price on the company’s equity, up a stunning 64.59% today. Things are fluid, but Robinhood may have been halted and then rose again when it resumed trading. Stonks indeed.

Shares of Robinhood, an investing-focused consumer fintech company, soared this morning in premarket trading. The stonk phenomenon, which helped propel minor companies like GameStop and AMC earlier this year, appears to be impacting Robinhood’s own stock; that much GameStop and AMC trading took place on Robinhood’s platform during stonk-fever is irony not lost on this publication.

Here’s what things look like this morning, per Yahoo Finance:

Recall that Robinhood went public at $38 per share, the low end of its range, and sank in its early trading sessions to below its IPO price. Now, it’s worth $54 per share.

Cool.

Normally we’d crack a joke and close this small news item here, but with Robinhood’s IPO featuring a unique twist on the traditional public offering, we have to do a bit more work. When it went public, Robinhood reserved a chunk of its equity for purchase by its own users. The impact of this was that more retail investors likely owned Robinhood equity at the start of its trading life than would be normal with a traditional IPO.

One hypothesis regarding Robinhood’s somewhat slack early trading performance was that early retail demand for its shares was sated by its effort to allow its users to buy stock in its shares, leading to a less-skewed supply/demand curve when it debuted.

Things have changed. What’s going on? Last week, an analyst put a $65 per share price target on the stock. And there are a handful of other ratings to chew on. But the wild swing in the price of Robinhood today appears from our vantage point to be another stonk moment. The stock is being traded like a short-squeeze, even if some market participants are skeptical of the idea due to what they view as a limited short interest in the company.

Checking the Robinhood IR page, there’s no news. Robinhood did not recently report earnings. And the company’s recent 606 filings that deal with PFOF incomes seemed to match up with expectations in revenue terms regarding what the company detailed in its Q2 2021 flash numbers. Perhaps there was more crypto in there than expected, but nothing truly wild.

It appears that Robinhood is simply going up because it is. This happens in 2021; we just have to get used to it.

But what matters most for our purposes is that Robinhood’s decision to sell some IPO stock to its users did not manage to create so much float for the now-public unicorn to diminish weird trading. You can go public in an unusual manner and still catch a stonk wave. Now we know.

Powered by WPeMatico

Rani Therapeutics, a San Jose-based company developing a pill to replace medical injections, went public on Friday.

According to S-1 filings, shares were estimated to price between $14 and $16 last week. On Friday, shares debuted slightly lower, around $11. Rani raised about $73 million in its debut.

Rani’s debut comes amidst a flurry of IPO activity in therapeutics. In 2020, 71 biotech companies went public. Already in 2021, 59 companies have IPO’ed, and even more are on the way. On July 30 alone, eight biotech companies were expected to begin trading, including Rani Therapeutics.

Rani Therapeutics, is, as founder Mir Imran puts it, “laser focused” on itself, rather than the IPO activity around it. The decision to go public was partially bolstered by the results of a phase I study — early evidence that the RaniPill, the company’s flagship product, could be brought into the clinic.

“We are already in humans, and clearly on a strong path to make oral biologics [a] reality. This is a hot and unique market for life science direction and we’re excited to be driving innovation in this area,” Imran tells TechCrunch.

Rani Therapeutics’ flagship product is RaniPill, essentially, a capsule designed to deliver medicines that would usually be delivered via injections. TechCrunch covered the pill in more detail here, but it works according to a few basic steps.

The pill is covered by a coating resistant to stomach acid. Once the pill enters the small intestine, the coating dissolves, allowing for a small balloon to inflate. Once that small balloon inflates, medication is delivered by a microneedle (which dissolves after the drug is administered). Then, the rest of the balloon is “excreted through normal digestive processes,” per the company’s S-1 filing.

This whole process occurs in a pill that, on the outside, looks like a gel capsule.

There is evidence for some conditions suggesting patients prefer oral drugs to injections: for example, studies on cancer patients have illuminated patient preference for oral therapies rather than regular injections. That’s not the case for every condition. Some patients show preference to long-acting medicines delivered via injection rather than having to take lots of pills (this is the case for some HIV patients).

However, it’s fair to say that needles aren’t exactly pleasant. A 2019 review and meta analysis of 35 studies found that between 20% and 30% of young adults are afraid of needles, a fear that can lead some people to avoid medical treatments or vaccines.

Rani Therapeutics has been developing capsules for drugs that have already been approved by the FDA, but are often administered via regular injections. They include:

The product furthest along in the research cycle is the pill developed to administer octreotide (called RT-101), which was tested in a phase I clinical trial on 62 participants. The trial results, partially reported in the S-1 filing, showed 65% bioavailability of the octreotide drug, compared to an injection. That suggests that the pills can get the drugs into the body efficiently, though these results are early.

Next year, the company plans to initiate two additional Phase I studies on PTH for osteoporosis, and human growth hormone. Studies on the rest of the drugs in the pipeline are scheduled for 2023.

Ultimately, the company’s goal is to validate the RaniPill independently of specific drugs. The company is pursuing an Investigational Device Exemption (IDE), which would allow the company to test RaniPill in a clinical study without a drug involved. This study aims to establish how safe the product is for repeated dosing, and is slated to begin next year.

“I think we want to continue to generate data with drugs, because we will be making drugs. But nonetheless, it’s important to establish what the platform’s safety and tolerability is,” said Imran. So that’s quite important as well.”

The company’s leadership does have a track record of successful exits in the biotech space.

Rani Therapeutics was founded in 2012 by Mir Imran, who has already overseen several exits and acquisitions of medical device companies. In 1985, Imran developed an implantable cardiac defibrillator as part of his first company, Intec Systems, which was later acquired by Eli Lilly. Since, he has started 20 medical device companies, of which 15 have either IPOed or been acquired.

However, for now, Rani Therapeutics financials report significant losses. Net losses for 2019 and 2020 totaled $26.6 million and $16.7 million, respectively. As of March 2021, the company was running a deficit of $119.6 million.

In total, the company has raised about $211.5 million in funding since inception, without counting cash generated from today’s IPO. Rani Therapeutics has plans to use the $73 million raised during the IPO to fund the IDE study and pursue additional clinical trials.

Powered by WPeMatico

U.S. edtech company Duolingo released a revised IPO price range this morning, boosting its potential per-share value to $100 after initially targeting a range that topped out at $95 per share.

Per the unicorn’s SEC filings, Duolingo is now targeting a $95 to $100 per share IPO price range, up from $85 to $95 per share, or a gain of around 12% at the bottom and 5% at the top.

TechCrunch previously called the Duolingo debut a bellwether of sorts for the larger U.S. edtech ecosystem; if Duolingo can price and trade well, investors in private companies may be more willing to invest, given a more proven and attractive exit market. On the other hand, if Duolingo prices weakly or trades poorly, the company could place a wet blanket atop the startup edtech world.

The fact that Duolingo is raising its IPO price range indicates that we are more likely on the path for a strong offering than a weak one.

For edtech companies that have hit unicorn status — like Masterclass, Course Hero, Quizlet and Outschool — it’s good news. For reference, those companies have raised $461.4 million, $97.4 million, $62 million and $130 million, respectively, per Crunchbase data.

The terms of the company’s IPO have not changed, aside from its proposed price. So, Duolingo is still selling 3.7 million shares in its debut, and some 1.41 million shares will be sold by existing equity holders. The company’s underwriters also reserved their right to buy 765,916 shares of the company’s stock at IPO price in the 30 days following its debut.

At the upper and lower bands of the company’s IPO price, its simple valuation excluding underwriter shares now lands between $3.41 billion and $3.59 billion. Inclusive of its greenshoe offering, those numbers rise to $3.48 billion and $3.67 billion.

Recall that when private, Duolingo’s November 2020 Series H valued the company at just over $2.4 billion. So long as Duolingo prices in its range, it will provide investors with a nice bump in the value of their investment. Duolingo was valued at just $1.6 billion in mid-2020, indicating that it has more than doubled in value since that investment.

Powered by WPeMatico

Turning the page from the early-stage venture capital market to the super late-stage exit market, this morning we’re talking about endpoint security company SentinelOne’s IPO in the context of Sprinklr’s own. We’ll have more on the public offering market later today when Doximity and Confluent price their respective IPOs after the close of trading.

The Exchange explores startups, markets and money. Read it every morning on Extra Crunch or get The Exchange newsletter every Saturday.

SentinelOne’s IPO, expected to price on June 29 and trade June 30, is a fascinating debut. Why? Because the company sports a combination of rapid growth and expanding losses that make it a good heat check for the IPO market. Its debut will allow us to answer whether public investors still value growth above all else. And this week, the company gave us an early dataset regarding its market value in the form of an IPO price range. This means we can do some unpacking and thinking.

A reminder regarding why we dwell on the exit market for unicorns: We care because the value of late-stage startups when they reach a liquidity point helps set valuation comps for myriad smaller startups. Furthermore, the level of public-market enthusiasm for loss-making, growth-focused companies will determine the scale of returns for many a venture capitalist, founder and early employee.

A reminder regarding why we dwell on the exit market for unicorns: We care because the value of late-stage startups when they reach a liquidity point helps set valuation comps for myriad smaller startups. Furthermore, the level of public-market enthusiasm for loss-making, growth-focused companies will determine the scale of returns for many a venture capitalist, founder and early employee.

So, let’s talk about SentinelOne’s cybersecurity IPO price range; Sprinklr’s social-media software debut will play foil.

It can make good sense to pay up for a quickly growing company’s shares. This is why you may hear of a startup raising an early-stage round at a very high revenue multiple.

Why put a $50 million price tag on a startup that just crossed the $1 million annual recurring revenue (ARR) threshold? If it’s growing sufficiently quickly, the math can pencil out. If that startup was growing at 300% per year, say, the revenue multiple that you paid in the round valuing the startup at $50 million would fall sharply over the next year, at which point other investors would probably scramble to put more capital into the firm at a higher price.

Bingo! You just got a markup on your initial investment, and the company has found someone else to lead their next round at a higher price, giving it even more capital to keep its growth game going and make your early investment appear prescient. See? Venture capital is easy.1

The same general idea applies to companies going public. Growth matters, and the more rapidly a company is adding revenue, the more money it will be worth because investors can anticipate its future scale (within reason). Some companies that sport quick growth can have other issues that impact their value. Extensive debt, for example, a history of uneven growth, or deteriorating economics could come into play. Or simply very high losses.

Powered by WPeMatico

Paytm, India’s most valuable startup, confirmed to its shareholders and employees on Monday that it plans to file for an IPO.

In a letter to shareholders and employees, Paytm said that it plans to raise money by issuing fresh equity in the IPO, and also sell existing shareholders’ shares at the event. The startup has offered its employees the option to sell their stakes in the firm.

This is the first time the Noida-headquartered firm, which is valued at $16 billion and has raised over $3 billion to date, has commented on its plans about the IPO. The startup said in the letter that it has received an in-principle approval from the board of directors to pursue the public market.

Paytm, which is backed by Alibaba and SoftBank, hasn’t shared when it plans to file for the IPO, but has sought shareholders’ response to their intention to sell stakes by the end of the month.

Two sources familiar with the matter told TechCrunch that Paytm plans to raise about $3 billion and is targeting a valuation of up to $30 billion in the IPO. Paytm declined to comment.

Paytm’s letter — obtained by TechCrunch — to shareholders on Monday.

This isn’t the first time Paytm has planned to explore the public route. Exactly 10 years ago, long before Paytm established itself as the largest mobile wallet firm and expanded to several financial and commerce services, the startup had filed with the regulator with intentions to become public. The startup at the time cancelled the IPO plan and instead raised money from VCs to explore new avenues for growth.

A lot is riding on a successful IPO of Paytm — which reported a consolidated loss of $233.6 million for the financial year that ended in March this year, down from $404 million a year ago. (The startup’s revenue fell 10% during this period to $437.6 million.) India’s stock markets are yet to be fully tested for tech startups’ stocks in the country — though retail investors have shown good signs in recent years.

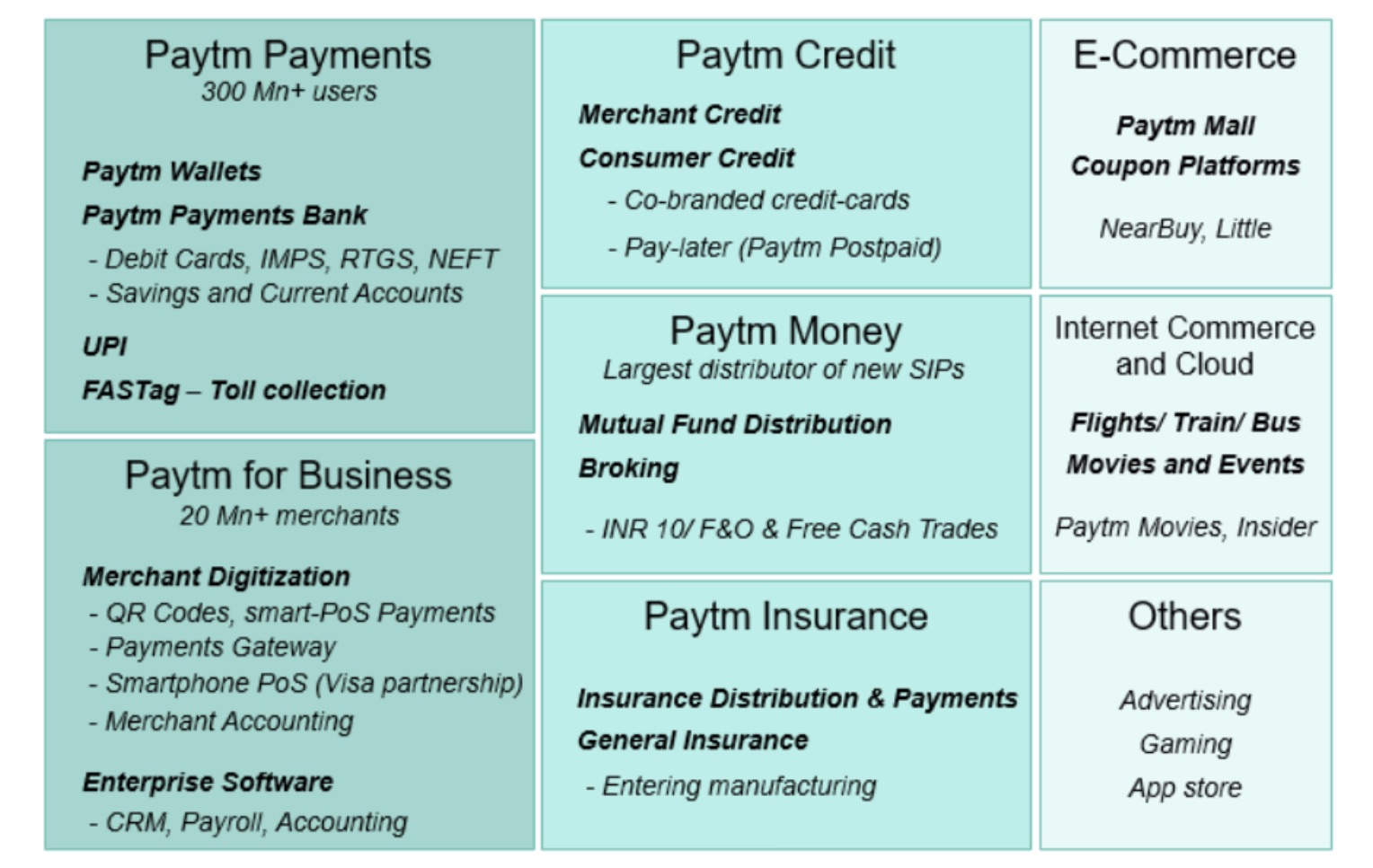

The startup, which competes with Google Pay and Flipkart-backed PhonePe, has realigned its payments strategy in recent years to assume a leadership position in the merchant payments market.

In a report to its clients late last month, analysts at Bernstein said the startup’s credit tech vertical is likely to lead the next wave of its revenue growth.

An overview of Paytm’s financial services ecosystem (Bernstein)

“With the advent of UPI, there has been a rising narrative that questioned Paytm’s market leadership,” the analysts wrote, referring to the exponential growth of payments stack developed by retail banks in India that has been adopted by several firms, including Google and PhonePe (as well as Paytm), and which has somewhat lowered the appeal of mobile wallets in India.

“However, under the hood, Paytm leads on merchant payments and has built an ecosystem of synergistic fintech verticals around its ‘super-app.’ The ecosystem spans payments (wallet/UPI), full-suite merchant acquiring, credit tech, digital bank, wealth, and insurance tech. We believe the super-app battle in India is not a ‘winner takes all’ but a game of execution, business building, and creating a superior customer experience with ecosystem integration,” Bernstein analysts added.

Paytm is the latest Indian giant startup that has expressed an interest in becoming public in recent months. Earlier this year, food delivery startup Zomato said it plans to raise $1.1 billion through an initial public offering. TechCrunch reported last month that Flipkart was in talks to raise over $1 billion in what is expected to be its financial fundraise ahead of an IPO.

Powered by WPeMatico

Brazilian mobile payments app PicPay filed on Wednesday an F-1 with the Securities and Exchange Commission (SEC) for an IPO valued at up to $100 million. The company plans to list on the Nasdaq under the ticker symbol PICS.

PicPay operates largely as a financial services platform that includes a credit card, a digital wallet similar to that of Apple Pay, a Venmo-style P2P payments element, e-commerce and social networking features.

“We want to transform the way people and companies interact, make transactions, and communicate in an intelligent, connected, and simple experience,” said José Antonio Batista, CEO of PicPay, in a statement.

While the company is based in São Paulo now and operates across Brazil, PicPay originally launched in Vitoria in 2012, a coastal city north of Rio. In 2015 the company was acquired by the group J&F Investimentos SA, a holding company owned by Brazilian billionaire brothers Wesley and Joesley Batista, which also own the gigantic meatpacker JBS SA.

According to the company’s registration statement, J&F was involved in the biggest corruption scandal in Brazil’s history, known as The Car Wash, and in 2017 entered into a plea deal with the Brazilian Federal Prosecutor. In December 2020 the company agreed to pay a fine of $1.5 billion and contribute an extra $442.6 million to social projects in Brazil. That being said, J&F continues to be a powerful conglomerate in the country, positioning itself as a strong backer for PicPay.

2020 was an explosive year for PicPay as the company saw its active userbase grow from 28.4 million to 36 million as of March 2021. According to the company’s 2020 financial report, which PicPay shared with TechCrunch, the company’s revenues also grew drastically from $15.5 million in 2019, to $71 million in 2020. The company is not yet profitable, however, and PicPay shelled out $146 million in 2020 to fuel its growth.

“We believe that the growth of our base and user engagement in our ecosystem demonstrates the scalability of our business model and reveals a great opportunity to generate more value for these customers,” Batista added.

Fintech is one of the most popular sectors in Brazil today, because there’s a lot of room for improvement in the region. The country has traditionally been controlled by four major banks, which have been slow to adapt to technology and also charge very high fees.

PicPay’s IPO is being led by Banco Bradesco BBI, Banco BTG Pactual, Santander Investment Securities Inc., and Barclays Capital Inc.

*The Brazilian Real was valued at 5.50 to $1 USD on the date of publication.

Powered by WPeMatico

This afternoon Bumble priced its IPO at $43 per share, ahead of its raised IPO range of $37 to $39 per share.

Bumble filed to go public in mid-January, and offered up its first price range on February 2. That range, $28 to $30 per share, wound up coming up short. Bumble raised its price range to $37 to $39 per share earlier this week.

Before counting a possible underwriters’ option, Bumble raised $2.15 billion by selling 50,000,000 million shares in its public offering. The company will begin to trade tomorrow morning.

Bumble’s debut comes amidst a number of other 2021 offerings, including MetroMile’s SPAC-led public combination earlier this week. Other well-known companies are anticipated to list this year, including Coinbase and, perhaps, Robinhood.

The public offering of Bumble shares comes after a sustained period when one company, Match, was presumed to be the only possible public dating company. However, the smaller Bumble has proven that there is room for at least one more.

TechCrunch explored Bumble’s financial results here, if you’d like more.

Powered by WPeMatico