initial public offering

Auto Added by WPeMatico

Auto Added by WPeMatico

On the heels of new filings from both Sumo Logic and JFrog, Snowflake, a venture-backed unicorn looking to go public on the strength of its data-focused cloud service, set an initial price range for its IPO.

The $75 to $85 per-share IPO price target values the firm at between $20.9 billion and $23.7 billion, huge sums for the private company. Its IPO could raise more than $2.7 billion for the startup.

Snowflake was last valued at around $12.5 billion when it raised a Series G worth $479 million earlier this year.

Built into those valuation projections are two private placements of stock in Snowflake, $250 million apiece from both Salesforce, the well-known CRM player, and Berkshire Hathaway, better known for its investment returns in the 80s and 90s, Cherry Coke and Charlie Munger’s humor.

Jokes aside, the inclusion of Salesforce in the IPO is notable, but not a shock, but Berkshire taking part in the public market debut of Snowflake, a company with historic losses that are nigh-tyrannical, is.

Here’s the S-1/A text on the setup:

Immediately subsequent to the closing of this offering, and subject to certain conditions of closing as described in the section titled “Concurrent Private Placements,” each of Salesforce Ventures LLC and Berkshire Hathaway Inc. will purchase $250 million of our Class A common stock from us in a private placement at a price per share equal to the initial public offering price. Based on an assumed initial public offering price of $80.00 per share, which is the midpoint of the price range set forth on the cover page of this prospectus, each of Salesforce Ventures LLC and Berkshire Hathaway Inc. would purchase 3,125,000 shares of our Class A common stock. […]

In addition, Berkshire Hathaway Inc. has agreed to purchase 4,042,043 shares of our Class A common stock from one of our stockholders in a secondary transaction at a price per share equal to the initial public offering price that will close immediately subsequent to the closing of this offering.

That second paragraph makes it clear that Berkshire is actually looking to snooker even more shares into its corner, for a total purchase price that might scale to more than $500 million.

What is so attractive about Snowflake? TechCrunch wrote a bit about that when the company filed, but the short gist is that it has epic growth, improving gross margins and dramatically curtailed losses. The package adds up to one valuable IPO, and something durable enough to tempt Buffett.

Regardless, what could be the most highly valued IPO of the year — Airbnb depending — here in America just got a lot more exciting.

Powered by WPeMatico

Wish, the San Francisco-based, 750-person e-commerce app that sells deeply discounted goods that you definitely don’t need but might buy anyway when priced so low — think pool floats, guinea pig harnesses, Apple Watch knockoffs — said yesterday that it has submitted a draft registration to the SEC for an IPO.

Because it filed confidentially, we can’t get a look at its financials just yet; we only know that its investors, who’ve provided the company with $1.6 billion across the years, think the company was worth $11.2 billion as of last summer, when it closed its most recent financing (a $300 million Series H round). Meanwhile, Wish itself says it has more than 70 million active users across more than 100 countries and 40 languages.

The big question, of course, is whether the now 10-year-old company can maintain or even accelerate its momentum.

It’s not a no-brainer. On the one hand, it’s a victim of the increasingly chilly relations between the U.S. and China, from where the bulk of Wish’s goods come. Then again, Wish has been beefing up its business elsewhere in the world partly as a result of the countries’ shifting stance toward one another.

For example, it told Recode last year that it’s increasingly looking to Latin American markets — Mexico, Argentina, Chile — for growth, and that it’s planning a bigger push into Africa, where it’s already available in South Africa, Ghana and Nigeria, among other countries.

Wish has always been a work in progress. It was co-founded by CEO Peter Szulczewski, a computer scientist who previously spent six years at Google before co-founding a company call ContextLogic, from which Wish evolved. The idea was to build a next-generation, mobile ad network to compete with Google’s AdSense network, but Szulczewski and his co-founder, Danny Zhang, realized they were “pretty bad at business development,” as he once said at an event hosted by this editor, so eventually they pivoted to Wish.

Wish originally asked people to create wish lists, then the company approached merchants, letting them know a certain number of customers wanted, say, a certain type of table. It was smart to recognize that showing the right recommendations to shoppers would become critical to its users, though it didn’t necessarily foresee the types of merchants it would ultimately work with, most of them in China, Indonesia and elsewhere in East Asia and Southeast Asia who are focused on value-conscious customers. As Wish quickly realized, these merchants didn’t have other ways to sell to or communicate with customers elsewhere in the world, so they didn’t mind paying Wish a 15% take to handle this for them.

Wish also focused around lightweight items that it could ship cheaply from China — if slowly — using something called ePacket. It’s a shipping option agreement that was established nine years ago with the cooperation of the U.S. Postal Service and Hong Kong Post (and later made available to 40 countries altogether) that enables products coming from China and Hong Kong to be sent cheaply as long as they meet certain criteria — they don’t weigh too much, they aren’t worth too much, they adhere to certain minimum and maximums regarding their size, and so forth.

The mix has proved powerful for Wish, despite growing competition from China-based outfits like AliExpress that offer many of the same goods to the same customers around the world. (Wish has also competed, always, with Walmart and Amazon.)

The company has also soldiered on despite apparent struggles to keep customers coming over time. Because it doesn’t sell essential items but rather a grab bag of different items, people tend to cycle out of the app after a few months of their first visit, as The Information once reported.

A bigger issue now is that, as of two months ago, a new USPS pricing structure went into effect that raises rates on international shipments. It also requires foreign recipient countries to ratify new rates under ePacket (whose recipient countries, by the way, have been downsized from 40 to 12). That means that companies like Wish either pay more to ship their goods — forcing its vendors to charge more — or they move to commercial networks.

Of course, a third option — and one that may position Wish well for the future — would be for Wish to invest in more local warehousing in the U.S., Europe and others of its growing markets, which it told Recode that it is doing, along with seeking more local vendors near its biggest markets.

Given shifts in the way that commercial real estate is being used — with retail-to-industrial property conversions accelerating, driven by the growth of e-commerce — it’s probably as good a time as any for Wish to be making these moves. Whether they are enough to sustain and grow the company is something that only time will tell.

Again, we’ll collectively know much more when we can get a look at that filing. It should make for interesting reading.

Wish’s private investors include General Atlantic, GGV Capital, Founders Fund, Formation 8, Temasek Holdings and DST Global, among others.

Powered by WPeMatico

In a turn of fortune, Airbnb today announced that it has filed to go public, albeit confidentially.

The move puts the home-sharing service on a path to a public offering sooner rather than later, and comes after reports that the company was prepping an IPO filing this month. Those same reports indicated that Airbnb could go public as soon as the end of the year.

A Q3 or Q4 Airbnb offering is therefore a distinct possibility.

Airbnb has mounted a comeback since COVID-19-related shutdowns slammed the travel market, tanking its revenues at the same time. Airbnb laid off nearly 2,000 workers, and took on expensive capital from external sources.

The company promised in 2019 that it would go public in 2020, but that pledge seemed far-off in the middle of the year. Since then, Airbnb has made noise about different parts of its business coming back to life, although changed by new travel and work and vacation patterns from its users.

If Airbnb has filed, we can presume that present results are good enough to get it life, else the firm would have not filed and would have simply gone public later. The question now becomes if its Q2 numbers were good enough to get it out the door, or if the company intends to update its S-1 filing with Q3 numbers, push the filing live and go public with more recovery time in its results.

Of course, such a course of action would put its public debut perilously close to the American election. And, Airbnb’s Q2 numbers are down not only from Q1 in revenue terms, but even more sharply from its year-ago results for the same calendar period. In short, Airbnb’s growth story may not be clear until Q3 numbers are tallied, a month and a half from now.

Airbnb joins other companies that have filed privately, like DoorDash, waiting in the wings for the right moment to go public, or the right set of results.

We’ll see, but the company’s public debut is back to being impending. Now the question becomes whether Airbnb intends to go public in an IPO, as the wording of its filing appears to suggest, or if a direct listing could still be in the cards. We think it’s more likely the former and not the latter, but, hey, in 2020 you never know.

Powered by WPeMatico

According to The Wall Street Journal, Airbnb could file confidentially to go public as early as this month. The same report states that Airbnb could follow that filing with an IPO before year’s end. Morgan Stanley and Goldman are helping the former startup with its IPO process, the Journal writes.

The news that Airbnb’s IPO could be back on caps a tumultuous year for the home-sharing unicorn, which promised in 2019 to go public in 2020. The company was widely tipped to be considering a direct listing before COVID-19 arrived, crashing the global travel market, and with it, Airbnb’s financial health.

Airbnb declined to comment on its IPO plans.

As travelers stayed home, the company was forced to sharply cut staff and take on billions in capital at prices that, compared to its late 2019-momentum, looked rather expensive.

But since those blows, Airbnb has begun to make noise about positive progress regarding its platform usage, and, implicitly, its financial performance.

In June, Airbnb said that between “May 17 to June 6, 2020, there were more nights booked for travel to Airbnb listings in the US than during the same time period in 2019,” and that “globally, over the most recent weekend (June 5-7), we saw year-over-year growth in gross booking value” for “the first time since February.”

And in July, the company said that its users had “booked more than 1 million nights’ worth of future stays at Airbnb listings” globally in a single day, the first time since March 3rd that that had happened.

Precisely how far Airbnb has financially clawed its way back is not clear. But the company’s cost basis in the wake of its layoffs could lower the revenue base it needs to recover to reach something akin to profitability, a traditional IPO benchmark, though one that has lost luster in recent years.

And with local travel taking off — slowly-improving airline occupancy rates are, therefore, not indicative of Airbnb’s performance or health — the company could have retooled its business in the wake of COVID to something that can still put up attractive revenues at strong margins.

Needless to say, I am hyped to read the Airbnb S-1, so the sooner it drops the happier I’ll be. Getting an in-depth look at what happened to the unicorn during COVID-19 is going to be fascinating.

Airbnb joins DoorDash, Coinbase, Palantir and others on our IPO shortlist. More as we have it.

Powered by WPeMatico

Tech stocks retain their highs as the second quarter’s earnings season begins to fade into the rearview mirror, and there are still a number of companies looking to go public while the times are good. It looks like a smart move, as public investors are hungry for growth-oriented shares — which is just what tech and venture-backed companies have in spades.

The companies currently looking to go public are diverse. China-based real-estate giant KE Holdings — a hybrid listings company and digital transaction portal for housing — is looking to raise as much as $2.3 billion in a U.S. listing. Xpeng, another China-based company that builds electric vehicles, is looking to list in the U.S as well. Xpeng has the distinction of being gross-margin negative in every key time period detailed in its S-1 filing.

The Exchange explores startups, markets and money. You can read it every morning on Extra Crunch, or get The Exchange newsletter every Saturday.

And then there’s Duck Creek Technologies, a domestic tech company looking to go public on the back of growing SaaS revenues. This morning let’s quickly spin through Duck Creek’s history, peek at its financial results, calculate its expected valuation and see how its pricing fits compared to current norms.

Duck Creek is a Boston-based software company that serves the property and casualty (P&C) insurance market. Its customers include names like AIG, Geico and Progressive, along with smaller players that aren’t as well known to the American mass market.

Duck Creek is a Boston-based software company that serves the property and casualty (P&C) insurance market. Its customers include names like AIG, Geico and Progressive, along with smaller players that aren’t as well known to the American mass market.

The KE IPO will be a big affair because the company is huge and profitable with $3.86 billion in H1 2020 revenue leading to $227.5 million in net income. The Xpeng IPO will be interesting because Tesla’s strong share price has given float to a great many EV boats. But Duck Creek is a company slowly letting go of perpetual license software sales and scaling its SaaS incomes while still generating nearly half its revenues from services. It’s a company we can understand, in other words.

So let’s get under the skin of the Boston-based company that also claims low-code functionality. This will be fun.

Powered by WPeMatico

Software valuations are bonkers, which means it’s a great time to go public. Asana, Monday.com, Wrike and every other gosh darn software company that is putting it off, pay attention. Heck, even service-y Palantir could excel in this market.

Let me explain.

Over the past few weeks, TechCrunch has tracked the filing, first pricing, rejiggered pricing range, and, today, the first day of trading for BigCommerce, a Texas-based e-commerce company. You can think of it as a comp with Shopify to a degree.

Image Credits: IMGFlip (opens in a new window)

In the wake of the Canadian phenom’s blockbuster earnings report, BigCommerce boosted its IPO range. Yesterday the company did itself one better, pricing $1 per share above that raised range, selling 9,019,565 shares at $24 per share, of which 6,850,000 came from BigCommerce itself.

Before some additions, there are now 65,843,546 shares of BigCommerce in the world, giving the company an IPO valuation of around $1.58 billion.

Given that the company’s Q2 expected revenue range is “between $35.5 million and $35.8 million,” the company sported a run-rate multiple of 11.1x to 11x, depending on where its final revenue tally comes in. That felt somewhat reasonable, if perhaps a smidgen light.

Then the company opened at $68 per share today, currently trading for $82 per share. Hello, 1999 and other insane times. BigCommerce is now worth, using some rough math, around $5.4 billion, giving it a run-rate multiple of around 38x, using the midpoint of its Q2 revenue range.

Powered by WPeMatico

How and when should startup founders think about the “exit”? It’s the perennial question in tech entrepreneurialism, but the hows and whens are questions to which there are a multitude of answers. For one thing, new founders often forget that the terms of the exit may not eventually be entirely in their control. There’s the board to think of, the strategic direction of the company, the first-in investors, the last-in. You name it. We’ll be chatting about this at Disrupt 2020.

Exits normally happen in only one of two ways: Either the startup gets acquired for enough money to give the investors a return or it grows big enough to list on the public markets. And it just so happens we have two perfect founders who will be able to unpack their own journeys on those two roads.

When Cloudflare went public last year it certainly wasn’t the end of its 10-year journey, and nor was it PlanGrid’s when it was acquired by Autodesk in 2018.

Cloudflare’s Michelle Zatlyn saw every nook and cranny of the company’s journey toward its IPO, which received a warm reception, even if there were a few bumps along the road leading up to it. What comes after an IPO and how do you even get there in the first place? Zatlyn will be laying it all out for us.

PlanGrid’s journey to acquisition by Autodesk was equally fascinating, and Tracy Young — who, as CEO and co-founder, shepherded the company to an $875 million exit — will be able to give us insight into what it’s like to dance with a potential acquirer, go through that (often fraught) process and come out the other side.

We’re excited to host this conversation at Disrupt 2020 and expect it to fill up quickly. Grab your pass before this Friday to save up to $300 on this session and more.

Powered by WPeMatico

Today Jamf, a software company that helps other firms manage their Apple devices, raised its IPO price range.

The company had previously targeted a $17 to $19 per-share range. A new SEC filing from the firm today details a far higher $21 to $23 per-share IPO price interval.

Jamf still intends to sell up to 18.4 million shares in its debut, including 13.5 million in primary stock, 2.5 million shares from existing shareholders and an underwriter option worth 2.4 million shares. The whole whack at $21 to $23 per share would tally between $386.4 million and $423.2 million, though not all those funds would flow to the company.

At the low and high-end of its new IPO range, Jamf is worth between $2.44 billion and $2.68 billion, steep upgrades from its prior valuation range of $1.98 billion to $2.21 billion.

Jamf follows in the footsteps of recent IPOs like nCino, Vroom and others in seeing demand for its public offering allow its pricing to track higher the closer it gets to its public offering. Such demand from public-market investors indicates there is ample demand for debut shares in mid-2020, a fact that could spur other companies to the exit market.

Coinbase, Airbnb and DoorDash are three such companies that are expected to debut in the next year’s time, give or take a quarter or two.

In anticipation of the Jamf debut that should come this week, let’s chat about the company’s recent performance.

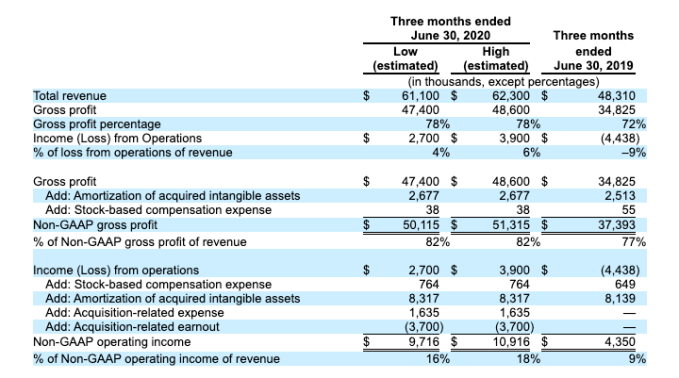

Observe the following table from the most-recent Jamf S-1/A:

From even a quick glance we can learn much from this data. We can see that Jamf is growing, has improving gross margins and has managed to swing from an operating loss to operating profit in Q2 2020, compared to Q2 2019. And, for you fans out there of adjusted metrics, that Jamf managed to generate more non-GAAP operating income in its most recent period than the year-ago quarter.

In more precise terms:

Profits! Growth! Software! Improving margins! It’s not a huge surprise that Jamf managed to bolster its IPO price range.

Finally, for the SaaS-heads out there, the following:

This data lets us have a little fun. Recall that we have seen possible valuations for Jamf at IPO that started at $1.98 billion to $2.21 billion, and now include $2.44 billion and $2.68 billion? With our two ARR ranges for the end of Q2, we can now come up with eight ARR multiples for Jamf, from the low-end of its initial IPO price estimate, to the top-end of its new range.

Here they are:

From that perspective, the pricing changes feel a bit more modest, even if they work out to a huge spread on a valuation basis.

Regardless, this is the current state of the Jamf IPO. Rackspace also filed a new S-1/A today, but we can’t find anything useful in it. A bit like the Jamf S-1/A from Friday. Perhaps we’ll get a new Rackspace document soon with pricing notes.

And, of course, like the rest of the world we await the Palantir S-1 with bated breath. Consider that our white whale.

Powered by WPeMatico

On the heels of nCino’s blockbuster debut, GoHealth’s public offering proved a more sedate affair, at least when comparing the two companies’ initial trading days.

GoHealth priced above its anticipated IPO range, selling more shares than initially planned in the process. By vending 43.5 million shares at $21 apiece — $1 per share more than the top of its preceding $18 to $20 range, and four million shares more than its target of 39.5 million — the insurance technology company put more than $900 million onto its balance sheet this week.

The debut is a win for Chicago’s industry and tech scenes. GoHealth was worth a little less than $6.7 billion at its IPO price, not counting shares that may be sold to its underwriters, which would boost its valuation.

Despite its better-than-anticipated pricing, however, GoHealth shares sagged in afternoon trading, slipping to $19.00 per share, down 9.5% as of the time of writing. The declines stand in contrast to the recent debuts of nCino, Lemonade and others, which saw their shares instantly gain value after going public.

GoHealth’s CEO, however, stressed the long-term vision of his company in an interview with TechCrunch. Speaking with Clint Jones during GoHealth’s first trading day, the executive told TechCrunch that his company’s offering was oversubscribed, and had met its goal of accumulating long-term investors during its IPO process.

The company intends to hire with its new funds, including 1,000 more licensed insurance agents, the CEO said.

Asked whether the company has plans to acquire smaller companies with its IPO funds, Jones told TechCrunch that it could be “opportunistic” regarding buying tech platforms, or smaller teams with particular talent. For the many startups competing in other parts of the insurance marketplace world — TechCrunch has covered the space extensively, including a bevy of funding rounds for insurtech startups — a newly wealthy public company could provide an interesting exit opportunity.

The company’s strong IPO pricing, if somewhat slack first-day’s trading, feels akin to a wash for related, smaller firms watching its public offering with interest; how GoHealth trades moving forward could help set the tone for select insurtech startup valuations.

For today, however, we have yet another unicorn tech-ish offering all wrapped up. GoHealth’s path to the public market’s wasn’t as straightforward as some, but it got there all the same.

Powered by WPeMatico

If you’re an angel who invested in a startup that was meant to go public in 2014, you might be getting a little bit impatient. High-risk, high-reward investing has lost its shine in this environment: the stock market is a mess these days, and you want your cash back.

Enter recapitalization events, where startups restructure their entire cap table to squeeze out old investors, bring on new ones and shift the way equity and debt is managed. For investors, it’s a killer way to enter a company on friendlier terms than normal (read: desperation), and a nice way to get liquidity on a startup you’re betting on.

For founders, it’s rarely good news, as departing investors is not a metric they’re going to add to the pitch deck. As one investor said on background, the spur of coronavirus-related recapitalization events shows “hella dilution for desperate times.”

That’s what makes Workhuman’s transparency with its recent recapitalization event all the more enticing.

Last year, the human-resources platform brought in $580 million in revenue from customers like LinkedIn, Cisco, J&J and other clients. In April, business grew 40%. Co-founder and CEO Eric Mosley says business has grown five times in size since the company pulled back from its 2014 plans to IPO. Workhuman hasn’t raised a single venture round since 2004 (and doesn’t plan to any time soon).

Being conservative has paid off; although Workhuman has operated for nearly two decades, Mosley says he thinks the company is still at the “tip of the iceberg.” The company recently had a recapitalization event to sell the stakes of its earliest investors, who cut a $200,000 check more than 20 years ago.

Powered by WPeMatico