initial public offering

Auto Added by WPeMatico

Auto Added by WPeMatico

Hims & Hers, a San Francisco-based telehealth startup that sells sexual wellness and other health products and services to millennials, began trading publicly today on the NYSE after completing a reverse merger with the blank-check company Oaktree Acquisition Corp.

Its shares slipped a bit, ending the day down 5% from where they started, but the company, which was founded in 2017 and now claims nearly 300,000 paying subscribers for its various offerings, has never been focused on a splashy headline about its first-day performance, co-founder and CEO Andrew Dudum told us earlier today.

On the contrary, Dudum says that while Hims might have once imagined a traditional IPO, it decided to go the special purpose acquisition company (SPAC) route because of their pricing mechanisms and because it was approached by a SPAC led by renowned money manager Howard Marks, the founder of the global alternative investment firm Oaktree Capital Management. (“We fell in love with the Oaktree team and the capital market experience and deep resources they have.”)

We talked with Dudum about that SPAC’s structure; the lockups involved now that Hims’ shares are trading; and how much of the business still centers around one of its first offerings, which was a generic version of erectile dysfunction pills. Our conversation has been edited lightly for length and clarity.

TC: You’re a Bay Area-based company selling to a mostly U.S. audience. How are you thinking about expanding that footprint geographically?

AD: We do have a small operation selling in the U.K.; we’re getting our feet wet in that market and building out a team and infrastructure and fulfillment. If you look at the regulatory landscape, there’s a huge amount of room [to grow] in Europe, Australia, Canada, the Middle East and Asia, and so in that order, we’ll start to [move into those markets].

TC: What is your average customer cost?

AD: It has come down from $200 when we first launched, to roughly $100 last year, and we make, on average, close to $300 in the first couple of years in terms of a patient’s lifetime value.

TC: How quickly do customers churn?

AD: We break down lifetime value projections by quarter cohorts, and quarter over quarter, year over year, we’re monetizing each of these cohorts better, with high-margin profiles.

As of last quarter, the business was growing 90% year-over-year, with 76% gross margins and greater cash efficiency, and that’s because as we provide more offerings, there is more cross-purchasing. Also, word of mouth is becoming more of a dynamic, with more than 50% of the traffic to the site free at this point because we have built a brand with a young demographic.

TC: When are you projecting that you’ll turn profitable?

AD: We’ve reduced our annual burn and increased our margin efficiency and organic growth, so on a quarterly basis, we think in the next couple of years is a real possibility.

Image Credits: Hims & Hers

TC: Hims’ first wellness offerings included pills for male pattern hair loss and erectile dysfunction. How much revenue does that ED business account for?

AD: What we’ve disclosed is that roughly half [of our revenue] is that sexual health category — which includes [medicines for] generic erectile dysfunction, birth control, STDs, UTIs and premature ejaculation. The other half is predominately dermatology, including hair care [to address hair loss] and acne, and we’ve more recently moved into primary care and behavioral health.

TC: For retail investors, how do you differentiate the business from that of your rival Ro, which heavily promotes its ED products?

AD: There are a number of core differences between us and public and private players. First is our real focus on diversifying our offerings. With our focus on sexual health, dermatology, primary care and behavioral health, it’s in our DNA to quickly expand into new businesses.

We also think we’re different from most [rivals] in that we really invest time in building deep relationships with [those who represent] the future of healthcare markets — people in their teens, 20s and 30s. This demographic has a different set of tech expectations and consumer expectations than people in their 40s, 50s and 60s, and if we want to build for the future, that means building for the largest body of payers in the future.

Traditional healthcare companies monetize only the sick, but optimizing around that demographic precludes you from understanding what the next generation really needs and wants. I’ve never seen such a divergence between a patient population and legacy experience, and that’s a real advantage to us as a business.

TC: Hims just went public through a SPAC in a deal that gives the company around $280 million in cash — $205 million of that from Oaktree’s blank-check company and another $75 million through a private placement deal. How much runway does that give you?

AD: The company doesn’t burn a tremendous amount — between $10 million and $20 million a year — so a relatively long runway if we keep operating the business as is. But it does allow us to expand and grow into new businesses, too, including into big categories like sleep, infertility, diabetes and other chronic conditions.

TC: What about acquisitions?

AD: We’ll keep an eye open for strategic opportunities and consolidation opportunities. More than a dozen businesses a month come to us to be consolidated into the brand, but generally speaking, we’ve had the belief that so much is in front of us that we don’t want to be distracted.

TC: Is there a lockup period for anyone?

AD: There’s a traditional lockup for executives and employees and the board.

TC: Did your SPAC sponsors get a board seat?

AD: No.

TC: How much do they now own of the company, and can they sell?

AD: Oaktree owns a couple percent and [the syndicate they brought to do the private placement] [owns] 12%. But the very reason we went with them was the quality of the team and the organization . . . and they have the added incentive for the next year or two from a compensation standpoint for the company to succeed and to prove [out their thesis that Hims is a smart investment].

TC: Do you think the traditional IPO process is broken?

AD: The traditional IPO market hasn’t changed. It takes 12 to 18 months of preparation, which is a crazy amount of time for management to be distracted, then there’s this one-day PIPE that gives institutions a tremendous amount of money instantaneously. Maybe it makes for a good CNBC headline, but at tremendous cost to the company. It’s atrocious. If you were a founder or employee and getting diluted twice as much as you have to be, you’d be really upset. It’s no surprise to me that founders like myself are looking at other modalities with better pricing and better structures.

Powered by WPeMatico

The dating and networking service Bumble has filed to go public.

The company, launched by a former co-founder of the IAC-owned Tinder, plans to list on the Nasdaq stock exchange, using the ticker symbol “BMBL.” Bumble’s planned IPO was first reported in December.

Bumble CEO Whitney Wolfe Herd was on the founding team at Tinder before starting Bumble. She filed suit against Tinder for sexual harassment and discrimination, which was at least somewhat inspirational in her quest to build a dating app that put women in the driver’s seat.

In 2019, Wolfe Herd took the helm of MagicLab, renamed to Bumble Group, in a $3 billion deal with Blackstone, replacing Badoo founder and CEO Andrey Andreev following a harassment scandal at the firm.

The company is targeting the public markets at a particularly heady time for new offerings, with investors embracing venture-backed IPOs throughout late 2020 and the start of 2021. Previously privately held companies like Airbnb, Affirm and others have seen their fortunes soar on the back of prices that public investors are willing to pay, perhaps inducing more IPO filings than the market might have otherwise seen.

You can read its IPO filing here. TechCrunch will have its usual tear-down of the document later today, but we have pulled some top-line numbers for you to kick off your own research.

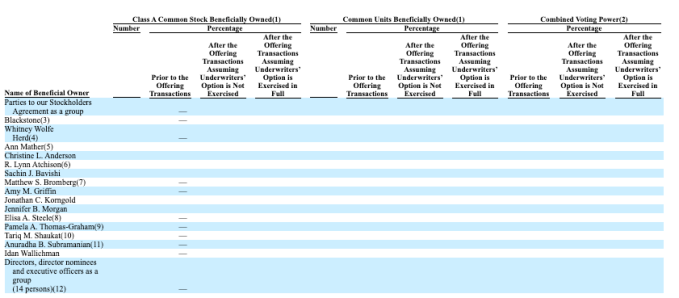

But before we do, the company’s board makeup, namely that it is over 70% women, is already drawing plaudits. Now, into its numbers.

Let’s consider Bumble from three perspectives: Usage, financial results and ownership.

On the usage front, Bumble is popular, as you would imagine a dating service would have to be to reach the scale required to go public. The company claims 42 million monthly active users (MAUs) as of Q3 2020 — many companies will try to get public on the strength of their third-quarter results from 2020, as it takes time to close Q4 and the full calendar year.

Those 42 million MAUs translated into 2.4 million total paying users through the first nine months of 2020; the percent, then, of paying users to MAUs is not 2.4 million divided by 42, but a smaller fraction.

Turning to the numbers, recall that Bumble sold a majority of itself a few years back. We bring that up as Bumble’s financial results are complicated thanks to its ownership structure.

After the IPO, Bumble Inc. will “be a holding company, and its sole material asset will be a controlling equity interest in Bumble Holdings,” per the S-1 filing. So, how is Bumble Holdings doing?

Medium? Doing the sums ourselves as the company’s S- 1 is fraught with accounting nuances, in the first nine months of 2019, Bumble managed the following:

And then, combining two columns to provide a similar set of results for the same period of 2020, Bumble recorded:

For those following along, we’re using the “Net (loss) earnings” line, for profitability, and not the “Net (loss) earnings attributable to owners / shareholders” as that would require even more explanation and we’re keeping it simple in this first look.

While Bumble saw modest growth in 2020 through Q3 and a sharp swing to losses on a GAAP basis, the company’s adjusted profitability grew over the same time period. The company’s adjusted EBITDA, a very non-GAAP metric, expanded from $80.0 million in the first three quarters of 2019 to $108.3 million in the same period of 2020.

While we are generally willing to allow quickly growing companies some leniency when it comes to adjusted metrics, the gap between Bumble’s GAAP losses and its EBITDA results is a stress-test of our compassion. Bumble also swung from free cash flow positivity during the first nine months of 2019 to the first quarters of 2020.

If you extrapolate Bumble’s Q1, Q2 and Q3 revenue to a full-year number, the company could manage $555.5 million in 2020 revenues. Even at a modest software-ish multiple, the company would be worth more than the $3 billion figure that we discussed before.

However, its sharp unprofitability in 2020 could damper its eventual valuation. More as we dig more deeply into the filing.

Finally, on the ownership question, the company’s filing is surprisingly denuded of data. Its principal shareholder section looks like this:

When we know more, we’ll share more. Until then, happy S-1 reading.

Powered by WPeMatico

Today Bumble, a popular dating-focused startup, was reported by Bloomberg to have filed IPO documents, albeit privately.

The news that Bumble is pursuing an IPO is not a surprise. TechCrunch covered the story in September, noting the huge revenues that its rival Tinder has managed to accrete, possibly indicative of a sufficiently large market to support two public dating players.

That Bumble has privately filed puts it, along with the crypto-focused Coinbase, as far along the IPO path before we can see their numbers. When they make their S-1 filings public the two companies will provide the market a look into their financial results.

Bumble and Coinbase are preceded in making such disclosures by Roblox, Affirm and Poshmark. The five companies will join others in seeking IPOs over the next few months.

According to a recent interview with GGV’s Hans Tung — an investor in Affirm and Airbnb and other unicorns — TechCrunch understands that quarters one, three and four in 2021 could prove to be active IPO periods. Bumble joining the fray in the final weeks of 2020 underscores how active the start of the year could be for highly priced private companies seeking liquidity while public markets trade near all-time highs.

TechCrunch reached out to Bumble for comment on the IPO report. The company declined to comment.

Bloomberg reports that Bumble could target a valuation of between $6 and $8 billion. This squares with prior reporting. How much revenue the market will require of Bumble to reach those prices, and at what pace of growth, is not clear.

But with the company reaching 100 million users earlier this year, perhaps all the math will pencil out.

Powered by WPeMatico

UiPath, the robotic process automation startup that has been growing like gangbusters, filed confidential paperwork with the SEC today ahead of a potential IPO.

“UiPath, Inc. today announced that it has submitted a draft registration statement on a confidential basis to the U.S. Securities and Exchange Commission (the “SEC”) for a proposed public offering of its Class A common stock. The number of shares of Class A common stock to be sold and the price range for the proposed offering have not yet been determined. UiPath intends to commence the public offering following completion of the SEC review process, subject to market and other conditions,” the company said in a statement.

The company has raised more than $1.2 billion from investors like Accel, CapitalG, Sequoia and others. Its biggest raise was $568 million led by Coatue on an impressive $7 billion valuation in April 2019. It raised another $225 million led by Alkeon Capital last July when its valuation soared to $10.2 billion.

At the time of the July raise, CEO and co-founder Daniel Dines did not shy away from the idea of an IPO, telling me:

We’re evaluating the market conditions and I wouldn’t say this to be vague, but we haven’t chosen a day that says on this day we’re going public. We’re really in the mindset that says we should be prepared when the market is ready, and I wouldn’t be surprised if that’s in the next 12-18 months.

This definitely falls within that window. RPA helps companies take highly repetitive manual tasks and automate them. So for example, it could pull a number from an invoice, fill in a number in a spreadsheet and send an email to accounts payable, all without a human touching it.

It is a technology that has great appeal right now because it enables companies to take advantage of automation without ripping and replacing their legacy systems. While the company has raised a ton of money, and seen its valuation take off, it will be interesting to see if it will get the same positive reception as companies like Airbnb, C3.ai and Snowflake.

Powered by WPeMatico

The WSJ is reporting that Airbnb is expected to price its IPO at either $67 or $68 per share. The American hospitality unicorn raised its IPO price target earlier this week, from $44 to $50 to $56 to $60.

While we’re still waiting for official pricing, Airbnb is worth $41 billion at its IPO price, using the upper pricing estimate and the company’s share count of 602,448,251 from its most recent S-1/A filing. That figure rises sharply if we included more than 50 million shares that could be added to the mix upon the exercise of vested employee options. The company’s fully diluted valuation at its IPO price was calculated to be $47 billion.

Axios reports that Airbnb raised $3.5 billion at its fully diluted valuation.

Regardless of how you prefer to value the company, its worth has risen sharply from an early pandemic nadir of $18 billion. After COVID-19 ravaged the company’s business, it laid off staff and took on external capital.

Since the end of Q1 and the first months of Q2, Airbnb has recovered, allowing it to file to go public and earn its highest valuation to date.

The company’s pricing comes after both DoorDash and C3.ai each priced above their own raised ranges, and saw their shares skyrocket in the first day’s trading. Some exuberance was therefore not unexpected.

Airbnb starts trading tomorrow morning. More then.

Powered by WPeMatico

According to media reports, food-delivery giant DoorDash priced its IPO at $102 per share, ahead of its final IPO pricing range of $90 to $95 per share.

The company’s debut has been warmly anticipated by public investors, as evinced by the company raising its range from an initial target of $75 to $85.

While we’re still waiting for official pricing, the price point makes DoorDash worth $32 billion at the time of its IPO price on a non-diluted basis (we’re using the company’s final S-1/A share count of 317,656,521). That valuation rises if one includes options that have vested but not been exercised, and even more if shares set aside for future compensation are also tallied. CNBC calculates DoorDash’s valuation to be $38.7 billion on a diluted basis.

Regardless, any of the valuation marks for DoorDash at $102 per share are far and away greater than its final pre-IPO valuation of around $16 billion, set this summer when the company took on additional capital. The unicorn raised more money during a growth boom, allowing it to add to its cash reserves ahead of its IPO with limited dilution.

DoorDash, which doubled its private startup valuation, is now incredibly well-capitalized to take on rivals Uber Eats and others. And at a price far above its raised range, it has more cash than it probably hoped for. How it uses that cash to preserve pandemic-driven gains will be a key narrative from the company in 2021.

More when we get official numbers.

Powered by WPeMatico

DoorDash filed to go public today, publishing numbers that showed rapid growth, enhanced profitability and an improving cash flow record which helped explain how the company had grown to a $16 billion valuation while private. The unicorn’s impending liquidity event will enrich a host of venture capital firms that bet on its eventual maturity.

Instead of posting this entry of The Exchange on Monday, we’ve put it out today for your Friday and weekend reading. Enjoy! — Alex and Walter.

But notable in DoorDash’s impressive results is the impact of COVID-19, accelerating secular trends already in place, and boosting the unicorn’s growth. Before we get into pricing this IPO and guessing what the company might be worth, let’s strive to understand what portion of its 2020 business gains could stem from the pandemic — and might not persist into the future.

We’re not being pessimistic; we merely want to better understand the company. And DoorDash agrees with our general thrust, writing in its S-1 filing that “58% of all adults and 70% of millennials say that they are more likely to have restaurant food delivered than they were two years ago,” adding that it believes “the COVID-19 pandemic has further accelerated these trends.”

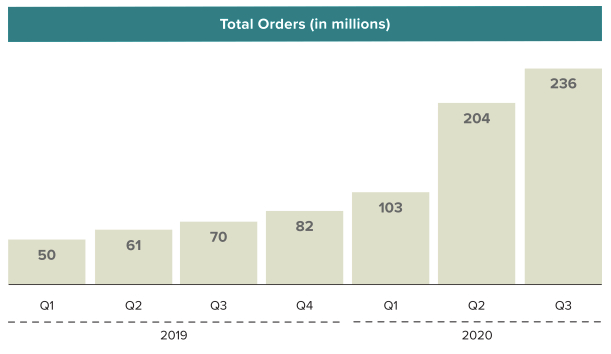

Even more, elsewhere in its filings DoorDash states plainly that COVD-19 led it to experience “a significant increase in revenue, Total Orders, and Marketplace [gross order volume] due to increased consumer demand for delivery, more merchants using our platform to facilitate both delivery and take-out, and improved efficiency of our local logistics platform.” The company then went on to warn investors that the “circumstances that have accelerated the growth of our business stemming from the effects of the COVID-19 pandemic may not continue in the future, and we expect the growth rates in revenue, Total Orders, and Marketplace [gross order volume] to decline in future periods.”

We’re not idly speculating.

Let’s observe how DoorDash’s growth accelerated from 2019 through 2020 and then peek at how the company’s economics improved during the same period, giving the company a shot at adjusted profitability for the full year, a nearly unheard of result in the on-demand market.

DoorDash generates revenue when a customer orders food via its service, splitting the total bill of food costs, taxes, fees and tips, distributing them to itself, the merchant creating the goods and the delivery person.

In an “illustrative” example that DoorDash notes its 2019 “approximate average per-order information,” the split works out as follows:

Given that the company is giving us old data and DoorDash’s performance has been stellar this year in terms of generating more gross profit, I wonder what has happened amidst 2020’s upheaval. But, the old numbers do for what we need, which is to understand the link between gross order volume (GOV) and DoorDash revenue. When the former goes up, the latter goes up.

So, as orders rise:

Powered by WPeMatico

The long-anticipated IPO of Alibaba-affiliated Chinese fintech giant Ant Group could raise tens of billions of dollars in a dual-listing on both the Shanghai and Hong Kong exchanges.

Shares for the company formerly known as Ant Financial are expected to price at around HK$80, or roughly 68 to 69 Chinese Yuan. The company is selling around 134 million shares in the Hong Kong portion of its debut, worth around $17.25 billion American dollars at HK$80 apiece.

Given that the share sale is expected to raise a similar amount of money from its Shanghai listing, the company’s IPO could raise as much as $34.5 billion. That tally would make the debut the largest in history, besting the recent Aramco IPO that raised around $29.4 billion.

Alibaba owns a 33% stake in Ant Group. At its currently expected share price, Ant Group would be worth as much as $310 billion, according to The New York Times, or $313 billion per CNBC.

Ant Group’s huge IPO fits its own epic scale. As TechCrunch reported in July, Ant had around 1.3 billion annual active users in March of this year, a number that could have risen in recent quarters. Ant’s Alipay competes with Tencent’s WeChat Pay in the huge and lucrative Chinese market.

The Ant Group IPO could be viewed as a moment in which the United States stock markets showed weakness. When Alibaba went public back in 2014, it did so via the New York Stock Exchange. The Chinese tech giant later dual-listed on the Hong Kong exchange. To see Ant Group dual-list on the Hong Kong and Shanghai indices without a float in New York shows what is possible outside of the United States when it comes to capital financing.

Fintech startups have broadly seen their fortunes rise during 2020 as the global pandemic changed consumer behavior and moved more commerce and payments into the digital realm. And IPOs have generally performed strongly as well, meaning that Ant Group could find a few tailwinds for its equity when it begins to trade.

Ant has not been content to stick to its knitting, keeping itself busy by investing in other startups. The company took a small stake in installment-payment service Klarna earlier this year, for example.

At a valuation of more than $310 billion, Ant Group would be worth about as much as JPMorgan Chase, the most valuable American bank today. It would also best U.S.-based digital payments leader PayPal, which is currently valued at $236 billion, as well as Square, which is valued at $77 billion.

Powered by WPeMatico

After pricing at $27 per share, Datto’s stock rose during regular trading. By mid-afternoon the data and security software company was worth $28.10 per share, up a hair over 4%.

The company’s IPO comes on the back of a rapid-fire Q3 in which a host of technology companies, particularly software, made it to the public markets. While the number of un-exited unicorns in the United States still rose in the quarter, Q3 brought with it a wave of liquidity that felt long coming.

Datto’s IPO is one among what appears set to be a smaller Q4 class, though offerings like Airbnb and Affirm are still tipped to be coming in short order. Airbnb and Affirm each announced that they have filed privately to float, though have yet to publicly drop their S-1 filings.

The Datto IPO was interesting for a few reasons, including its mix of slower growth and rising profitability, its place in the midst of the current Vista drama and how well it was priced.

While 2020 has brought with it many venture-backed IPOs, the year has also brought a nearly commensurate number of complaints about the IPO process itself. After many tech, and tech-ish, companies saw their values skyrocket after pricing and listing, vocal tech and venture figures argued that IPOs were effectively handing upside from companies to underwriting banks, and their customers.

There was some merit to the arguments. Datto, however, will not stoke similar fires. Up a mere few points from its IPO price, it was priced pretty much perfectly from the perspective of raising as much money as it could for itself in its debut.

Datto will use its IPO proceeds to pay down debts that it accrued during its takeover from Vista (private equity: a good deal for private equity). However, Datto’s CEO Tim Weller told TechCrunch in a call that the company will still be well-capitalized after the public offering, saying that it will have a very strong cash position.

The company should have places to deploy its remaining cash. In its S-1 filings, Datto highlighted a COVID-19 tailwind stemming from companies accelerating their digital transformation efforts. TechCrunch asked the company’s CEO whether there was an international component to that story, and whether digital transformation efforts are accelerating globally and not merely domestically. In a good omen for startups not based in the United States, the executive said that they were.

The company did not entertain a SPAC-led public debut, with Datto’s founder, Austin McChord, saying that his company had long planned a traditional public offering. Closing on the Vista front, McChord said that the removal of Vista’s Brian Sheth was immaterial to Datto’s IPO process.

Powered by WPeMatico

The gaming company Roblox announced today that it had confidentially filed paperwork with the SEC to make its public debut.

In February, the company, which operates a free-to-play gaming empire with tens of million of users, was valued at $4 billion after a Series G funding round led by Andreessen Horowitz . The company has raised more than $335 million in venture capital funding, according to Crunchbase.

The company has not detailed the number of shares it plans to offer and furthermore notes in standard legalese that their timely debut is “subject to market and other conditions.” After a slow 2019 for tech IPOs the rebound of public markets in mid-pandemic 2020 has provided an awfully wide window for tech startups reaching for their debuts.

In the games space, we recently saw the debut of Unity Technologies, which makes a popular game engine that developers use to build and monetize gaming titles.

Roblox offers an interesting sell to both consumers and developers, shipping a free-to-play vision of the future which pushes developers away from graphics-intense game design toward building content that can be played on a wide variety of devices. The games company has been more successful than most in translating a first-party experience’s success into a robust developer network. Roblox’s platform has been particularly successful with young audiences.

Powered by WPeMatico