financial services

Auto Added by WPeMatico

Auto Added by WPeMatico

Technology has been used to manage regulatory risk since the advent of the ledger book (or the Bloomberg terminal, depending on your reference point). However, the cost-consciousness internalized by banks during the 2008 financial crisis combined with more robust methods of analyzing large datasets has spurred innovation and increased efficiency by automating tasks that previously required manual reviews and other labor-intensive efforts.

So even if RegTech wasn’t born during the financial crisis, it was probably old enough to drive a car by 2008. The intervening 11 years have seen RegTech’s scope and influence grow.

RegTech startups targeting financial services, or FinServ for short, require very different growth strategies — even compared to other enterprise software companies. From a practical perspective, everything from the security requirements influencing software architecture and development to the sales process are substantially different for FinServ RegTechs.

The most successful RegTechs are those that draw on expertise from security-minded engineers, FinServ-savvy sales staff as well as legal and compliance professionals from the industry. FinServ RegTechs have emerged in a number of areas due to the increasing directives emanating from financial regulators.

This new crop of startups performs sophisticated background checks and transaction monitoring for anti-money laundering purposes pursuant to the Bank Secrecy Act, the Office of Foreign Asset Control (OFAC) and FINRA rules; tracks supervision requirements and retention for electronic communications under FINRA, SEC, and CFTC regulations; as well as monitors information security and privacy laws from the EU, SEC, and several US state regulators such as the New York Department of Financial Services (“NYDFS”).

In this article, we’ll examine RegTech startups in these three fields to determine how solutions have been structured to meet regulatory demand as well as some of the operational and regulatory challenges they face.

Powered by WPeMatico

It takes a lot of trust to allow a company to come in and install a mystery box on their network to monitor for threats. It’s like inviting in a security guard to sit in your living room to make sure nobody breaks in.

Yet that’s exactly what Darktrace does. (The box, not the security guard.)

The Cambridge U.K.-founded company, now with a second headquarters in San Francisco, assumes that any network can be breached. Instead of looking at the perimeter of a network, Darktrace uses artificial intelligence (AI) and machine learning to scan and identify security weaknesses and malicious traffic inside a company’s network.

Traditional network monitoring typically uses signature-based threat detection of matching against known malicious files, but can be easily modified to evade detection. Instead, Darktrace builds up a profile of the network to understand what the baseline “normal” looks like so it can spot and identify potential issues, like large amounts of data exfiltration or suspect devices.

But how do you win over those who see a sea of meaningless buzzwords? How can you differentiate between the smoke and mirrors and the real deal?

“No one wants the black box making decisions without them knowing what it’s doing,” said Nicole Eagan, Darktrace’s co-founder and chief executive, in a call with TechCrunch.

“So, let them have visibility,” she said.

Darktrace’s founders have roots in the U.K. and U.S. intelligence, where they took what they knew of the cybersecurity threats to the private sector to where the new battleground opened up. In the past half-decade of its existence, the company has gained major clients on its roster — from telcos to banks, tech giants and car makers — supported by 900 staff in over 40 offices around the world.

About a quarter of its customers are in financial services, said Eagan. But it takes a lot for the heavily regulated companies to trust a mystery device on a company’s network where the data and security, like financial services, is highly regulated.

Powered by WPeMatico

Entering into the world of Anthemis is a bit like stepping into the frame of a Wes Anderson film. Eclectic, offbeat people situated in colorful interiors? Check. A muse in the form of a renowned British-Venezuelan economist? Check. A design-forward media platform to provoke deep thought? Check. An annual summer retreat ensconced in the French Alps? Bien sûr.

Sitting atop this most unusual fintech(ish) VC is its ponytailed founder and chairman Sean Park, whose difficult-to-place accent and Philosophy professor aura belie his extensive fixed income capital markets experience. He’s joined by founder and CEO Amy Nauiokas, who in addition to being one of Fintech’s most prominent female investors also owns a high-minded film and television production company.

When Arman Tabatabai and I recently sat down with Park and Nauiokas in their New York office, the firm’s leaders were in an upbeat mood, having blown past the temporary perception-setback associated with the abrupt resignation last year of Anthemis’ former CEO Nadeem Shaikh (for more on this, read TechCrunch writer Steve O’Hear’s coverage of the situation).

And as the conversation below demonstrates, Park and Nauiokas are well poised to bring the quirk into everything they touch, which these days runs the gamut from backing companies involved in sustainable finance, advancing their home-grown media platform and preparing a soon-to-be-announced initiative elevating female entrepreneurs.

Gregg Schoenberg: With the two of you now at the helm, how does Anthemis present itself today?

Sean Park: I’ll step back and say that when Amy and I were working at big financial institutions in the noughties, we saw that the industry was going to change and that existing business models were running into their natural diminishing returns.

We tried to bring some new ideas to the organizations we were working in, but we each had epiphany moments when we realized that big organizations weren’t built to do disruptive transformation — for bad reasons, but also good reasons, too.

GS: Let’s fast forward to today, where you have several strong Fintech VCs out there. But unlike others, Anthemis puts weirdness at the heart of its model.

Yes, you’ve backed some big names like Betterment and eToro, but you’ve done other things that are farther afield. What’s the underlying thesis that supports that?

Amy Nauiokas: Whatever we do at Anthemis has to be a non-zero-sum game. It has to be for good, not for evil. So that means that we aren’t looking in any place where you see predatory opportunities to make money.

Powered by WPeMatico

The Valley’s rocky history with cleantech investing has been well-documented.

Startups focused on non-emitting-generation resources were once lauded as the next big cash cow, but the sector’s hype quickly got away from reality.

Complex underlying science, severe capital intensity, slow-moving customers and high-cost business models outside the comfort zones of typical venture capital ultimately caused a swath of venture-backed companies and investors in the cleantech boom to fall flat.

Yet, decarbonization and sustainability are issues that only seem to grow more dire and more galvanizing for founders and investors by the day, and more company builders are searching for new ways to promote environmental resilience.

While funding for cleantech startups can be hard to find nowadays, over time we’ve seen cleantech startups shift down the stack away from hardware-focused generation plays toward vertical-focused downstream software.

A far cry from past waves of venture-backed energy startups, the downstream cleantech companies offered more familiar technology with more familiar business models, geared toward more recognizable verticals and end users. Now, investors from less traditional cleantech backgrounds are coming out of the woodwork to take a swing at the energy space.

An emerging group of non-traditional investors getting involved in the clean energy space are those traditionally focused on fintech, such as New York and Europe-based venture firm Anthemis — a financial services-focused team that recently sat down with our fintech contributor Gregg Schoenberg and I (check out the full meat of the conversation on Extra Crunch).

The tie between cleantech startups and fintech investors may seem tenuous at first thought. However, financial services have long played a significant role in the energy sector and is now becoming a more common end customer for energy startups focused on operations, management and analytics platforms, thus creating real opportunity for fintech investors to offer differentiated value.

Though the conversation around energy resources and decarbonization often focuses on politics, a significant portion of decisions made in the energy generation business is driven by pure economics — is it cheaper to run X resource relative to resources Y and Z at a given point in time? Based on bid prices for request for proposals (RFPs) in a specific market and the cost-competitiveness of certain resources, will a developer be able to hit their targeted rate of return if they build, buy or operate a certain type of generation asset?

Alternative generation sources like wind, solid oxide fuel cells or large-scale or even rooftop solar have reached more competitive cost levels — in many parts of the U.S., wind and solar are in fact often the cheapest form of generation for power providers to run.

Thus as renewable resources have grown more cost competitive, more infrastructure developers and other new entrants have been emptying their wallets to buy up or build renewable assets like large-scale solar or wind farms, with the American Council on Renewable Energy even forecasting cumulative private investment in renewable energy possibly reaching up to $1 trillion in the U.S. by 2030.

A major and swelling set of renewable energy sources are now led by financial types looking for tools and platforms to better understand the operating and financial performance of their assets, in order to better maximize their return profile in an increasingly competitive marketplace.

Therefore, fintech-focused venture firms with financial service pedigrees, like Anthemis, now find themselves in pole position when it comes to understanding cleantech startup customers, how they make purchase decisions, and what they’re looking for in a product.

In certain cases, fintech firms can even offer significant insight into shaping the efficacy of a product offering. For example, Anthemis portfolio company kWh Analytics provides a risk management and analytics platform for solar investors and operators that helps break down production, financial analysis and portfolio performance.

For platforms like kWh analytics, fintech-focused firms can better understand the value proposition offered and help platforms understand how their technology can mechanically influence rates of return or otherwise.

The financial service customers for clean energy-related platforms extends past just private equity firms. Platforms have been and are being built around energy trading, renewable energy financing (think financing for rooftop solar) or the surrounding insurance market for assets.

When speaking with several of Anthemis’ cleantech portfolio companies, founders emphasized the value of having a fintech investor on board that not only knows the customer in these cases, but that also has a deep understanding of the broader financial ecosystem that surrounds energy assets.

Founders and firms seem to be realizing that various arms of financial services are playing growing roles when it comes to the development and access to clean energy resources.

By offering platforms and surrounding infrastructure that can improve the ease of operations for the growing number of finance-driven operators or can improve the actual financial performance of energy resources, companies can influence the fight for environmental sustainability by accelerating the development and adoption of cleaner resources.

Ultimately, a massive number of energy decisions are made by financial services firms and fintech firms may often know the customers and products of downstream cleantech startups more than most. And while the financial services sector has often been labeled as dirty by some, the vital role it can play in the future of sustainable energy offers the industry a real chance to clean up its image.

Powered by WPeMatico

To become a global fintech player, locate your company in San Francisco and Africa.

That’s the approach of payments company Flutterwave, digital lending startup Mines, and mobile-money venture Chipper Cash—Africa-founded ventures that maintain headquarters in San Francisco and operations in Africa to tap the best of both worlds in VC, developers, clients, and the frontier of digital finance.

This arrangement wasn’t exactly coordinated across the ventures, but TechCrunch coverage picked up the trend and some common motives among these rising fintech firms.

Founded in 2016 by Nigerians Iyinoluwa Aboyeji and Olugbenga Agboola, Flutterwave has positioned itself as a global B2B payments solutions platform for companies in Africa to pay other companies on the continent and abroad.

Clients can tap its APIs and work with Flutterwave developers to customize payments applications. Existing customers include Uber, Booking.com and African e-commerce unicorn Jumia.com.

The Y-Combinator backed company is headquartered in San Francisco, runs its operations center in Nigeria, and plans to add offices in South Africa and Cameroon.

Flutterwave opened an office in Uganda in June and raised a $10 million Series A round in October. The company also plugged into ledger activity in 2018, becoming a payment processing partner to the Ripple and Stellar blockchain networks.

Powered by WPeMatico

OpenFin, the company looking to provide the operating system for the financial services industry, has raised $17 million in funding through a Series C round led by Wells Fargo, with participation from Barclays and existing investors including Bain Capital Ventures, J.P. Morgan and Pivot Investment Partners. Previous investors in OpenFin also include DRW Venture Capital, Euclid Opportunities and NYCA Partners.

Likening itself to “the OS of finance,” OpenFin seeks to be the operating layer on which applications used by financial services companies are built and launched, akin to iOS or Android for your smartphone.

OpenFin’s operating system provides three key solutions which, while present on your mobile phone, has previously been absent in the financial services industry: easier deployment of apps to end users, fast security assurances for applications and interoperability.

Traders, analysts and other financial service employees often find themselves using several separate platforms simultaneously, as they try to source information and quickly execute multiple transactions. Yet historically, the desktop applications used by financial services firms — like trading platforms, data solutions or risk analytics — haven’t communicated with one another, with functions performed in one application not recognized or reflected in external applications.

“On my phone, I can be in my calendar app and tap an address, which opens up Google Maps. From Google Maps, maybe I book an Uber . From Uber, I’ll share my real-time location on messages with my friends. That’s four different apps working together on my phone,” OpenFin CEO and co-founder Mazy Dar explained to TechCrunch. That cross-functionality has long been missing in financial services.

As a result, employees can find themselves losing precious time — which in the world of financial services can often mean losing money — as they juggle multiple screens and perform repetitive processes across different applications.

Additionally, major banks, institutional investors and other financial firms have traditionally deployed natively installed applications in lengthy processes that can often take months, going through long vendor packaging and security reviews that ultimately don’t prevent the software from actually accessing the local system.

OpenFin CEO and co-founder Mazy Dar (Image via OpenFin)

As former analysts and traders at major financial institutions, Dar and his co-founder Chuck Doerr (now president & COO of OpenFin) recognized these major pain points and decided to build a common platform that would enable cross-functionality and instant deployment. And since apps on OpenFin are unable to access local file systems, banks can better ensure security and avoid prolonged yet ineffective security review processes.

And the value proposition offered by OpenFin seems to be quite compelling. OpenFin boasts an impressive roster of customers using its platform, including more than 1,500 major financial firms, almost 40 leading vendors and 15 of the world’s 20 largest banks.

More than 1,000 applications have been built on the OS, with OpenFin now deployed on more than 200,000 desktops — a noteworthy milestone given that the ever-popular Bloomberg Terminal, which is ubiquitously used across financial institutions and investment firms, is deployed on roughly 300,000 desktops.

Since raising their Series B in February 2017, OpenFin’s deployments have more than doubled. The company’s headcount has also doubled and its European presence has tripled. Earlier this year, OpenFin also launched it’s OpenFin Cloud Services platform, which allows financial firms to launch their own private local app stores for employees and customers without writing a single line of code.

To date, OpenFin has raised a total of $40 million in venture funding and plans to use the capital from its latest round for additional hiring and to expand its footprint onto more desktops around the world. In the long run, OpenFin hopes to become the vital operating infrastructure upon which all developers of financial applications are innovating.

“Apple and Google’s mobile operating systems and app stores have enabled more than a million apps that have fundamentally changed how we live,” said Dar. “OpenFin OS and our new app store services enable the next generation of desktop apps that are transforming how we work in financial services.”

Powered by WPeMatico

The San Francisco-based startup Branch International, which makes small personal loans in emerging markets, has raised $170 million and announced a partnership with Visa to offer virtual, pre-paid debit cards to Branch client networks in Africa, South-Asia and Latin America.

Branch — which has 150 employees in San Francisco, Lagos, Nairobi, Mexico City and Mumbai — makes loans starting at $2 to individuals in emerging and frontier markets. The company also uses an algorithmic model to determine credit worthiness, build credit profiles and offer liquidity via mobile phones.

“We’ll use [the money] to deepen existing business in Africa. Later this year we’ll announce high-yield savings accounts…in Africa,” says Branch co-founder and chief executive Matt Flannery.

The $170 million round from Foundation Capital and its new debit card partner, Visa, will support Branch’s international expansion, which could include Brazil and Indonesia, according to Flannery. Branch launched in Mexico and India within the last year. In Africa, it offers its services in Kenya, Nigeria and Tanzania.

A potential Branch customer

The Branch-Visa partnership will allow individuals to obtain virtual Visa accounts with which to create accounts on Branch’s app. This gives Branch larger reach in countries such as Nigeria — Africa’s most populous country with 190 million people — where cards have factored more prominently than mobile money in connecting unbanked and underbanked populations to finance.

Founded in 2015, Branch started operating in Kenya, where mobile money payment products such as Safaricom’s M-Pesa (which does not require a card or bank account to use) have scaled significantly. M-Pesa now has 25 million users, according to sector stats released by the Communications Authority of Kenya. Branch has more than 3 million customers and has processed 13 million loans and disbursed more than $350 million, according to company stats.

Branch has one of the most downloaded fintech apps in Africa, per Google Play app numbers combined for Nigeria and Kenya, according to Flannery.

Already profitable, Branch International expects to reach $100 million in revenues this year, with roughly 70 percent of that generated in Africa, according to Flannery.

In addition to Visa and Foundation Capital, the $170 Series C round included participation from Branch’s existing investors Andreessen Horowitz, Trinity Ventures, Formation 8, the IFC, CreditEase and Victory Park, while adding new investors Greenspring, Foxhaven and B Capital.

Branch last raised $70 million in 2018. The company’s overall VC haul and $100 million revenue peg register as pretty big numbers for a startup focused primarily on Africa. Pan-African e-commerce startup Jumia, which also announced its NYSE IPO last month, generated $140 million in revenue (without profitability) in 2018.

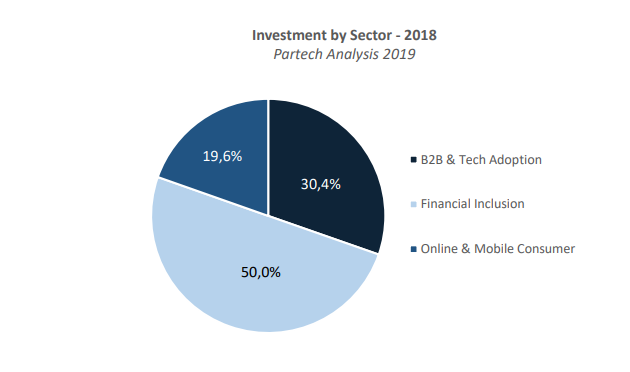

Startups building financial technologies for Africa’s 1.2 billion population have gained the attention of investors. As a sector, fintech (or financial inclusion) attracted 50 percent of the estimated $1.1 billion funding to African startups in 2018, according to Partech.

Startups building financial technologies for Africa’s 1.2 billion population have gained the attention of investors. As a sector, fintech (or financial inclusion) attracted 50 percent of the estimated $1.1 billion funding to African startups in 2018, according to Partech.

Branch’s recent round and plans to add countries internationally also tracks a trend of fintech-related products growing in Africa, then expanding outward. This includes M-Pesa, which generated big numbers in Kenya before operating in 10 countries around the world. Nigerian payments startup Paga announced its pending expansion in Asia and Mexico late last year. And payment services such as Kenya’s SimbaPay have also connected to global networks like China’s WeChat.

Powered by WPeMatico

Social investing and trading platform eToro announced that it has acquired Danish smart contract infrastructure provider Firmo for an undisclosed purchase price.

Firmo’s platform enables exchanges to execute smart financial contracts across various assets, including crypto derivatives, and across all major blockchains. Firmo founder and CEO Dr. Omri Ross described the company’s mission as “…enabl[ing] our users to trade any asset globally with instant settlement by tokenizing assets and executing all essential trade processes on the blockchain.” Firmo’s only disclosed investment, according to data from Pitchbook, came in the form of a modest pre-seed round from the Copenhagen Fintech Lab accelerator.

Firmo’s mission aligns well with that of eToro — which is equal parts trading platform, social network and educational resource for beginner investors — with the company having long communicated hopes of making the capital markets more open, transparent and accessible to all users and across all assets. By gobbling up Firmo, eToro will be able to accelerate its development of offerings for tokenized assets.

The acquisition represents the latest step in eToro’s broader growth plan, which has ramped up as of late. Earlier in March, the company launched a crypto-only version of its platform in the US, as well as a multi-signature digital wallet where users can store, send and receive cryptocurrencies.

The Firmo deal and eToro’s other expansion activities fit squarely into the company’s belief in the tokenization of assets and the immense, sector-defining opportunity that it creates. Etoro believes that asset tokenization and the movement of financial services onto the blockchain are all but inevitable and the company has employed the long-tailed strategy of investing heavily in related blockchain and crypto technologies despite the ongoing crypto winter.

“Blockchain and the tokenization of assets will play a major role in the future of finance,” said eToro co-founder and CEO Yoni Assia. “We believe that in time all investible assets will be tokenized and that we will see the greatest transfer of wealth ever onto the blockchain.” Assia expressed a similar sentiment in a recent conversation with TechCrunch, stating “We think [the tokenization of assets] is a bigger opportunity than the internet…”

After the acquisition, Firmo will operate as an internal R&D arm within eToro focused on developing blockchain-oriented trade execution and the infrastructure behind the digital representation of tokenized assets.

“The Firmo team has done ground-breaking work in developing practical applications for blockchain technology which will facilitate friction-less global trading,” said Assia.

“The adoption of smart contracts on the blockchain increases trust and transparency in financial services. We are incredibly proud and excited that [Firmo] will be joining the eToro family. We believe that together we have a very bright future and look forward to pursuing our shared goal to become the first truly global service provider allowing people to trade, invest and save.”

Powered by WPeMatico

Atlanta-based Movius, a company that allows companies to assign a separate business number for voice calls and texting to any phone, today announced that it has raised a $45 million Series D round led by JPMorgan Chase, with participation from existing investors PointGuard Ventures, New Enterprise Associates and Anschutz Investment company. With this, the company has now raised a total of $100 million.

In addition to the new funding, Movius also today announced that it has brought on former Adobe and Sun executive John Loiacono as its new CEO. Loiacono was also the founding CEO of network analytics startup Jolata.

“The Movius opportunity is pervasive. Almost every company on planet Earth is mobilizing their workforce but are challenged to find a way to securely interact with their customers and constituents using all the preferred communication vehicles – be that voice, SMS or any other channel they use in their daily lives,” said Loiacono. “I’m thrilled because I’m joining a team that features highly passionate and proven innovators who are maniacally focused on delivering this very solution. I look forward to leading this next chapter of growth for the company.”

Sanjay Jain, the chief strategy officer at Hyperloop Transportation Technologies, and Larry Feinsmith, the head of JPMorgan Chase’s Technology Innovation, Strategy & Partnerships office, are joining the company’s board.

Movius currently counts more than 1,400 businesses as its customers, and its carrier partners include Sprint, Telstra and Telefonica. What’s important to note is that Movius is more than a basic VoIP app on your phone. What the company promises is a carrier-grade network that allows businesses to assign a second number to their employees’ phones. That way, the employer remains in charge, even as employees bring their own devices to work.

Powered by WPeMatico

Japanese messaging app company Line is pumping 20 billion JPY ($182 million) into its mobile payment business as it tries to turn things around following a challenging year in 2018.

The company announced the infusion into Line Pay, a subsidiary that it fully owns, in a filing that stated the new capital is “necessary funds for its future business operation.” No further details were provided.

The investment comes on the heels of Line’s latest financial report which saw it post a 5.79 billion JPY loss as revenue grew by 24 percent to reach 207.18 billion JPY in 2018. Line has long been a top money maker in the App Store, but its efforts to build out content around its messaging platform and games division have turned out to be expensive, with a job service, manga platform and e-commerce business among its ventures.

In addition to more content, payments are also seen as “glue” that can increase engagement within the Line ecosystem and its main messaging app.

The company is going after the cashless opportunity in Japan, where it is the dominant chat app with an estimated 50 million registered users. The country is notable for its continued use of cash, but the government is using the upcoming 2020 Olympic Games as an opportunity to move toward a digital future. Aside from its core Line Pay service, which sits inside the Line chat app, Line is introducing its own credit card with Visa and has gone after Chinese tourists through a tie-in with Tencent, the internet giant behind China’s top messaging app WeChat.

Outside of Japan, Line Pay is also available in Thailand (where it works with the Bangkok metro provider), Taiwan (where it counts two banks as partners) and Indonesia, which Line says are its next three largest markets in terms of user numbers. Together, across those four countries, Line claims it has 165 million monthly active users and 40 million registered Line Pay users. Line said GMV reached 55 billion JPY ($482 million) per month back in November 2017; there’s been no update since.

The service was launched more widely but it has shuttered in other markets, including Singapore where it was ended in February 2018.

Beyond payment, Line is also moving into banking and financial services. It is working to launch a digital bank in Japan and last year it announced plans to investigate the potential to roll out loans, insurance and other services backed by its own cryptocurrency. While it didn’t hold an ICO — its “Link” token is earned or can be bought on exchanges — Line did dive into crypto in a major way, opening its own exchange and starting a crypto investment fund, too. With the bear market in full effect, and token valuations dropping by 90 percent across the board, we haven’t heard too much more from Line regarding its crypto plans.

Powered by WPeMatico