financial services

Auto Added by WPeMatico

Auto Added by WPeMatico

After Wisam Dakka and André Madeira left Snap in 2018, the two longtime product developers and coders cast about for a new app to build.

Looking around they realized there was no financial product that spoke to the generation of consumers they’d spent the last bit of their professional lives working to build for, so they decided it would be their next project.

“Our insight is that an individual’s relationship with money is a delicate and an emotional one. Most financial apps are not adopted by the masses because they are strict, lack empathy, and are unconsciously perceived as judgmental, which is why they are often downloaded and then ignored,” said Madeira, in a statement.

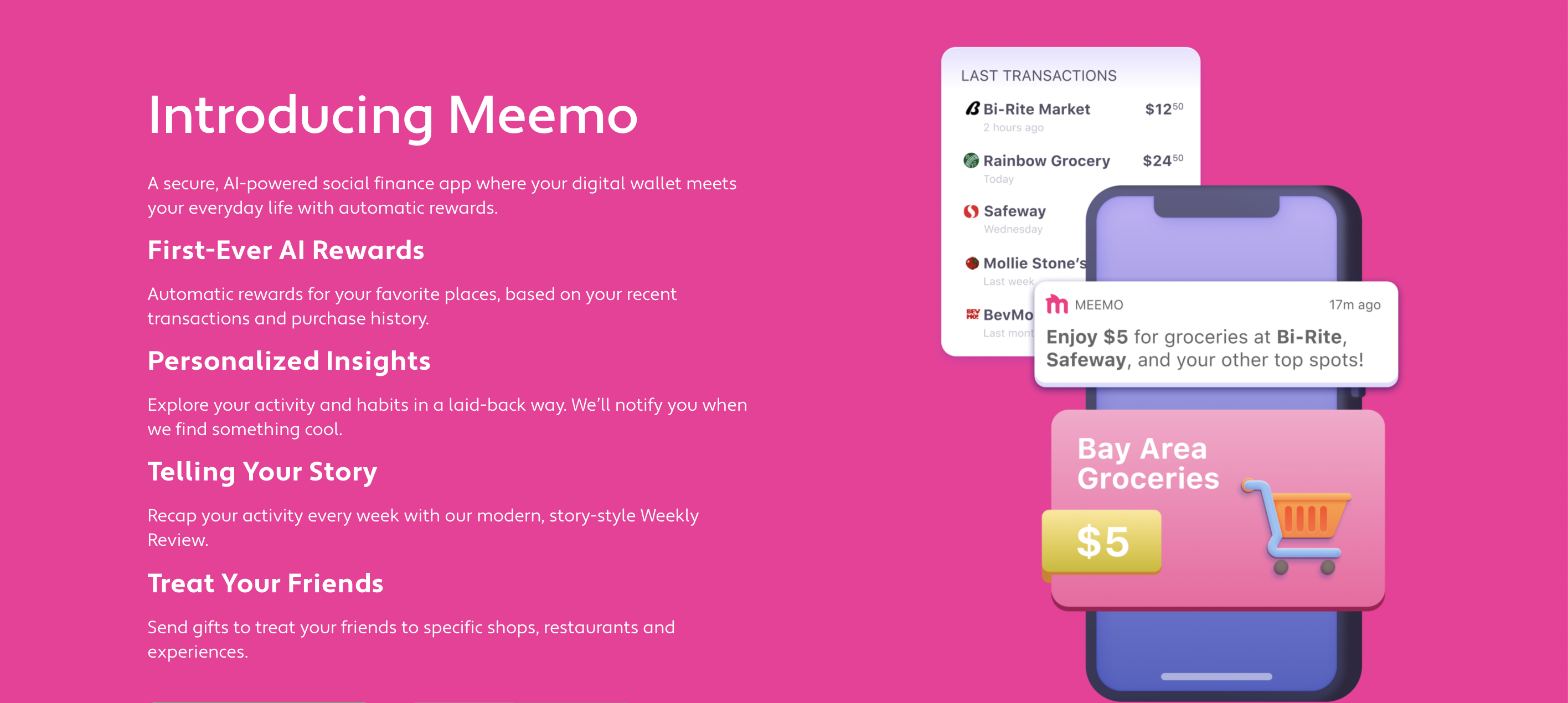

Their solution, launching today, is Meemo .

It’s a combination of a personal financial monitoring, rewards and gifting, and social shopping app all rolled into one.

“One of the things we learned at Snap, if you want to reach the masses you need to change how you create an app. It has to be effortlessly,” said Madeira. “It has to be automatic and social as well so we want to build an app that is all of that combined.”

Once a user downloads Meemo and connects their main bank account or credit card to the app, Meemo will give that person insights into their spending history and potential rewards.

For most users, the initial experience will be through a gift card. Gifting, it turns out is what Dakka and Madeira think will be the secret sauce for the company’s growth (although getting people to use something if they’re being given money or free stuff is hardly rocket science).

There’s also the social element, which the two men think will be a draw as well. Meemo provides recommendations and social validation from friends by harvesting their buying history and sharing it with you.

Once a user downloads Meemo and has the history of their transactions, the app will surface the places where users spend the most money. They can then send gift cards to their friends for their favorite restaurants. The goal, eventually, is to get restaurants to subsidize the gifting portion and have their shoppers act as a direct marketing channel.

Image Credits: Meemo (opens in a new window)

Shops won’t be able to see who’s getting the gifts until they come into the store. What Meemo hopes to do is gather a profile of a user’s shopping behavior based on their purchases and offer them discounts to places that they may not frequent as often, but match their consumer profile.

Backing the company are investors including Saama Capital, Greycroft, monashees and Sierra Ventures, along with individual investors Amit Singhal, Hans Tung and serial entrepreneurs and the co-founders’ colleagues from Google and Snap.

Madeira and Dakka first met working on Google Search and went on to found Snap’s San Francisco office. The team is rounded out by long-time friends like Robson Araújo and Ranveer Kunal.

“We are very excited to back Dakka and Madeira in their creation of a new age finance app at Meemo that will combine improved financial management with deeper social engagement for today’s generation,” said Ash Lilani, managing partner at Saama Capital, in a statement. “With Dakka and Madeira’s past experience of assembling talented teams and building viral products, we believe Meemo has an opportunity to become a leader in this space.”

The company’s name is taken from a Portuguese word “mimo,” which means an affectionate treat, according to a statement. It’s available to download on iOS and Android.

Powered by WPeMatico

The COVID-19 pandemic has forced businesses to rethink how they accept and make payments. Paper invoices, checks and point-of-sale payments have given way to “corona-free payments” through mobile apps, electronic invoicing and ACH. Although significant, this is the sideshow to a more significant reshuffling of the payments industry.

Nearly $150 trillion in worldwide B2B and B2C transactions take place every year, but only a tiny portion are digital. A lot of technology companies want their piece of that massive pie. Until recently, though, only payment facilitators (aka, “payfacs”), gateways, banks and credit card companies had access to it.

That’s changing. Whether they know it yet or not, B2B tech platforms are becoming payments companies. Payfacs are competing to integrate their technology into these platforms, which drive an ever-growing number of transactions. Revenue-sharing deals are on the table, and payfacs are pushing the competitive advantages they can offer to the clients of these B2B platforms. Capabilities like cross-border payments, seamless customer onboarding, fraud protection, marketplace payments and B2B invoicing influence, which payfacs win in “integrated payments” (the jargon for this space) and which don’t.

B2B companies that use to leave the choice of gateway to their clients need to become savvy in payment technology, both to control the user experience and to tap this new business. There’s a massive amount of revenue on the table, and it’s just too easy to blow this opportunity and alienate clients in the process.

A decade ago, the revolution in cloud computing led to a wave of B2B tech platforms promising to “disrupt” every industry. Gyms got gym management platforms. Hospitals got clinic management platforms. Retailers got commerce management platforms. Media companies got subscription management platforms. Many of these fill-in-the-blank management platforms — all independent software vendors (ISVs) — helped clients manage their operations and interactions with consumers or other businesses.

But ISVs didn’t get involved in payments, which was odd, given how complementary payments were to their platforms and how much money was at stake. Mastercard says there is about $120 trillion annually in B2B payments worldwide, and paper checks still dominate about half of the U.S.’s $25 trillion payment volume. Meanwhile, retail e-commerce sales account for $4.2 trillion out of $26 trillion in total retail, or about 16.1%, according to eMarketer. Less than 8% of global commerce is thought to occur online.

You’d think B2B software companies would find a way to generate revenue on some of that $146 trillion in transactions, but most did not. Payment processing is its own, messy, complicated niche. Payfacs go through a grueling underwriting process to provision a merchant account, which includes know-your-customer (KYC) and anti-money laundering (AML) checks. If a merchant defaults, the payfac is next in line to make good on the transactions.

When you run a venture-backed B2B platform, you have enough to worry about already.

So, B2B platforms stayed clear. They formed integrations with a basket of payfacs (Stripe, PayPal, Square, my company BlueSnap, etc.) and then let their clients choose which one to use. That’s a lot of integrations to maintain.

Powered by WPeMatico

Plum, the London and Athens-based fintech that offers a “smart” money management app to help you improve your “financial resilience,” has raised a further $10 million in funding as it gears up for European expansion.

The new round is led by Japan’s Global Brain and the European Bank for Reconstruction and Development, which has participated in previous Plum funding rounds.

In addition, the company has received further funding from early backer VentureFriends, matched by the U.K. taxpayer via the U.K. government’s Future Fund scheme. Plum has raised $19.3 million in total since being founded by Victor Trokoudes (an early TransferWise employee) and Alex Michael in 2016.

Launched in the U.K. the following year, Plum is one of a number of fintech startups that is vying to become a user’s financial hub or control centre, in a way that goes far beyond the first generation of personal finance manager apps and bank account aggregators.

You link the app to your bank account and gain access to a range of functionality, including savings, investments and analysis of your utility bills to help you make better purchasing decisions. Like similar apps, Plum’s “artificial intelligence” also deems what you can afford to save by analysing your bank transactions. It then puts money away each month in the form of round-ups and/or regular savings.

You can open an ISA investment account and invest based on themes, such as only in “ethical companies” or technology. Another related feature is “Splitter,” which, as the name suggests, lets you split your automatic savings between Plum savings pots and investments, selecting the percentage amounts to go into each pot, from 0-100%.

In a call with Trokoudes, he talked me through a few recent Plum updates that he says bring it much closer to fulfilling its financial control centre mission and being a candidate to replace your individual banking apps.

Crucially, you can now link all of your accounts to Plum, whereas previously Plum only let you access a single linked bank account. This gives you “full visibility” of your saving, spending and investments all in a single app.

On the roadmap is also the ability to make payments via Open Banking — and Trokoudes doesn’t rule out a Plum card in the future as a complementary feature with additional benefits, not a core offering, unlike numerous competitors.

More immediately, Plum is launching interest for savers who use Plum to set money aside but don’t want to invest any or all of it. Paid users are being offered an interest rate of 0.6% for instant access savings and 0.75% for 95 days’ notice. Plum users on its free tier can earn 0.35% interest.

Trokoudes explained that there’s also the option to split a percentage of the money put aside automatically, allocating deposits between the new interest-bearing account and Plum-powered investments.

Meanwhile, armed with fresh capital, Plum plans to launch in Spain and France by the end of 2020. The company claims 1 million registered users in the U.K., and now employs more than 60 people split across London, U.K. and Athens, Greece. Trokoudes tells me it will scale up further to 80 employees by the end of 2020 and is aiming for 5 million users across Europe by the end of 2021.

Adds Naoki Kamimaeda, partner and Europe office representative at Global Brain Corporation: “More users have started using fintech apps and personal financial management apps across the globe, to be more efficient and be better off. Among these fintech apps, Plum has a very unique position and very bold ambition to be a partner of individuals to save more money and manage their financial life in an easier and more effective manner.”

Powered by WPeMatico

Due to COVID-19, business continuity has been put to the test for many companies in the manufacturing, agriculture, transport, hospitality, energy and retail sectors. Cost reduction is the primary focus of companies in these sectors due to massive losses in revenue caused by this pandemic. The other side of the crisis is, however, significantly different.

Companies in industries such as medical, government and financial services, as well as cloud-native tech startups that are providing essential services, have experienced a considerable increase in their operational demands — leading to rising operational costs. Irrespective of the industry your company belongs to, and whether your company is experiencing reduced or increased operations, cost optimization is a reality for all companies to ensure a sustained existence.

One of the most reliable measures for cost optimization at this stage is to leverage elastic services designed to grow or shrink according to demand, such as cloud and managed services. A modern product with a cloud-native architecture can auto-scale cloud consumption to mitigate lost operational demand. What may not have been obvious to startup leaders is a strategy often employed by incumbent, mature enterprises — achieving cost optimization by leveraging managed services providers (MSPs). MSPs enable organizations to repurpose full-time staff members from impacted operations to more strategic product lines or initiatives.

Powered by WPeMatico

Singapore-based fintech startup GoBear has raised $17 million from returning investors Walvis Participaties, a Dutch venture capital firm, and Aegon N.V., a life insurance and asset management provider. The funding brings GoBear’s total funding so far to $97 million, and will be used to expand its consumer financial services platform, which is available in seven Asian markets: Hong Kong, Indonesia, Malaysia, the Philippines, Singapore, Thailand and Vietnam.

Founder and CEO Adrian Chng told TechCrunch that GoBear will focus on what it calls its “three growth pillars”: an online financial supermarket that evolved from the company’s financial products aggregator/comparison service; an online insurance brokerage; and its digital lending business, which it recently expanded by acquiring consumer lending platform AsiaKredit.

The company has also added three new executives over the past few months: chief information technology officer Valeriy Gasratov; chief strategy officer Jinnee Lim as Chief Strategy Officer; and Mike Singh from AsiaKredit as its new chief lending officer.

GoBear originally launched in 2015 as a metasearch engine, before transitioning into financial services. The company now works with over 100 financial partners, including banks and insurance providers, and says its platform has been used by over 55 million people to search for more than 2,000 personal financial products.

The startup serves consumers who don’t have credit cards or other access to traditional credit building tools. Similar to other fintech companies that focus on underbanked populations, GoBear aggregates and analyzes alternative sources of data to judge lending risk, including patterns in consumer behavior. For example, Chng said if a loan application is filled out in less than a minute, it is more likely to be fraudulent, and applications made between 8:30PM and midnight are less risky than ones made between 2AM to 5AM.

Data points from smartphones is also used to assess creditworthiness in markets like the Philippines, where the credit card penetration rate is less than 10%, but more than 40% of the population uses a smartphone.

Despite the COVID-19 pandemic, Chng said GoBear has been gross margin positive since the end of 2019. Interest in travel insurance has declined, but the company has continued to see demand for other insurance products and lending. Its online insurance brokerage has grown its average order by 52% over the last three months, and the company has seen 50% year-over-year growth from its loan products.

There are other fintech companies in Asia that overlap with some of the services that GoBear offers, like comparison platform MoneySmart, CompareAsiaGroup and Grab Financial Group. In terms of competition, Chng told TechCrunch that not only is the market opportunity in Asia huge (he said there are 400 million underbanked people across GoBear’s seven markets), but the company also differentiates with its three core services, which are all interconnected and draw on the same data sources to score credit.

Chng anticipates that the pandemic will spur more financial institutions to begin digitizing their products and looking for partners like GoBear to help them manage risk. In turn, that will make more financial institutions open to using non-traditional data to score credit, enabling underbanked markets to have increased access to financial products.

“The momentum is here. I think now is the time for tech and data to transform financial services,” he said. “As a platform, we are really looking for partners to come with us for the next phase of growth and investment. I feel positive even with COVID-19, because I think that we will have more acceleration, and the opportunity to change people’s lives and benefit them and investors by solving tough problems will only increase.”

Powered by WPeMatico

The world of consumer banking has seen a massive shift in the last ten years. Gone are the days where you could open an account, take out a loan, or discuss changing the terms of your banking only by visiting a physical branch. Now, you can do all this and more with a few quick taps on your phone screen — a shift that has accelerated with customers expecting and demanding even faster and more responsive banking services.

As one mark of that switch, today a startup called Thought Machine, which has built cloud-based technology that powers this new generation of services on behalf of both old and new banks, is announcing some significant funding — $83 million — a Series B that the company plans to use to continue investing in its platform and growing its customer base.

To date, Thought Machine’s customers are primarily in Europe and Asia — they include large, legacy outfits like Standard Chartered, Lloyds Banking Group, and Sweden’s SEB through to “challenger” (AKA neo-) banks like Atom Bank. Some of this financing will go towards boosting the startup’s activities in the US, including opening an office in the country later this year and moving ahead with commercial deals.

The funding is being led by Draper Esprit, with participation also from existing investors Lloyds Banking Group, IQ Capital, Backed and Playfair.

Thought Machine, which started in 2014 and now employs 300, is not disclosing its valuation but Paul Taylor, the CEO and founder, noted that the market cap is currently “increasing healthily.” In its last round, according to PitchBook estimates, the company was valued at around $143 million, which, at this stage of funding, puts this latest round potentially in the range of between $220 million and $320 million.

Thought Machine is not yet profitable, mainly because it is in growth mode, said Taylor. Of note, the startup has been through one major bankruptcy restructuring, although it appears that this was mainly for organisational purposes: all assets, employees and customers from one business controlled by Taylor were acquired by another.

Thought Machine’s primary product and technology is called Vault, a platform that contains a range of banking services: checking accounts, savings accounts, loans, credit cards and mortgages. Thought Machine does not sell directly to consumers, but sells by way of a B2B2C model.

The services are provisioned by way of smart contracts, which allows Thought Machine and its banking customers to personalise, vary and segment the terms for each bank — and potentially for each customer of the bank.

It’s a little odd to think that there is an active market for banking services that are not built and owned by the banks themselves. After all, aren’t these the core of what banks are supposed to do?

But one way to think about it is in the context of eating out. Restaurants’ kitchens will often make in-house what they sell and serve. But in some cases, when it makes sense, even the best places will buy in (and subsequently sell) food that was crafted elsewhere. For example, a restaurant will re-sell cheese or charcuterie, and the wine is likely to come from somewhere else, too.

The same is the case for banks, whose “Crown Jewels” are in fact not the mechanics of their banking services, but their customer service, their customer lists, and their deposits. Better banking services (which may not have been built “in-house”) are key to growing these other three.

“There are all sorts of banks, and they are all trying to find niches,” said Taylor. Indeed, the startup is not the only one chasing that business. Others include Mambu, Temenos and Italy’s Edera.

In the case of the legacy banks that work with the startup, the idea is that these behemoths can migrate into the next generation of consumer banking services and banking infrastructure by cherry-picking services from the VaultOS platform.

“Banks have not kept up and are marooned on their own tech, and as each year goes by, it comes more problematic,” noted Taylor.

In the case of neobanks, Thought Machine’s pitch is that it has already built the rails to run a banking service, so a startup — “new challengers like Monzo and Revolut that are creating quite a lot of disruption in the market” (and are growing very quickly as a result) — can integrate into these to get off the ground more quickly and handle scaling with less complexity (and lower costs).

Taylor was new to fintech when he founded Thought Machine, but he has a notable track record in the world of tech that you could argue played a big role in his subsequent foray into banking.

Formerly an academic specialising in linguistics and engineering, his first startup, Rhetorical Systems, commercialised some of his early speech-to-text research and was later sold to Nuance in 2004.

His second entrepreneurial effort, Phonetic Arts, was another speech startup, aimed at tech that could be used in gaming interactions. In 2010, Google approached the startup to see if it wanted to work on a new speech-to-text service it was building. It ended up acquiring Phonetic Arts, and Taylor took on the role of building and launching Google Now, with that voice tech eventually making its way to Google Maps, accessibility services, the Google Assistant and other places where you speech-based interaction makes an appearance in Google products.

While he was working for years in the field, the step changes that really accelerated voice recognition and speech technology, Taylor said, were the rapid increases in computing power and data networks that “took us over the edge” in terms of what a machine could do, specifically in the cloud.

And those are the same forces, in fact, that led to consumers being able to run our banking services from smartphone apps, and for us to want and expect more personalised services overall. Taylor’s move into building and offering a platform-based service to address the need for multiple third-party banking services follows from that, and also is the natural heir to the platform model you could argue Google and other tech companies have perfected over the years.

Draper Esprit has to date built up a strong portfolio of fintech startups that includes Revolut, N26, TransferWise and Freetrade. Thought Machine’s platform approach is an obvious complement to that list. (Taylor did not disclose if any of those companies are already customers of Thought Machine’s, but if they are not, this investment could be a good way of building inroads.)

“We are delighted to be partnering with Thought Machine in this phase of their growth,” said Vinoth Jayakumar, Investment Director, Draper Esprit, in a statement. “Our investments in Revolut and N26 demonstrate how banking is undergoing a once in a generation transformation in the technology it uses and the benefit it confers to the customers of the bank. We continue to invest in our thesis of the technology layer that forms the backbone of banking. Thought Machine stands out by way of the strength of its engineering capability, and is unique in being the only company in the banking technology space that has developed a platform capable of hosting and migrating international Tier 1 banks. This allows innovative banks to expand beyond digital retail propositions to being able to run every function and type of financial transaction in the cloud.”

“We first backed Thought Machine at seed stage in 2016 and have seen it grow from a startup to a 300-person strong global scale-up with a global customer base and potential to become one of the most valuable European fintech companies,” said Max Bautin, Founding Partner of IQ Capital, in a statement. “I am delighted to continue to support Paul and the team on this journey, with an additional £15 million investment from our £100 million Growth Fund, aimed at our venture portfolio outperformers.”

Powered by WPeMatico

Allowance is going digital. Venmo has been spotted prototyping a new feature that would allow adult users to create for their teenage children a debit card connected to their account. That could potentially let parents set spending notifications and limits while giving kids more flexibility in urgent situations than a few dollars stuffed in a pocket.

Delving into children’s banking could establish a new reason for adults to sign up for Venmo, get them saving more in Venmo debit accounts where the company can earn interest on the cash and drive purchase frequency that racks up interchange fees for Venmo’s owner PayPal .

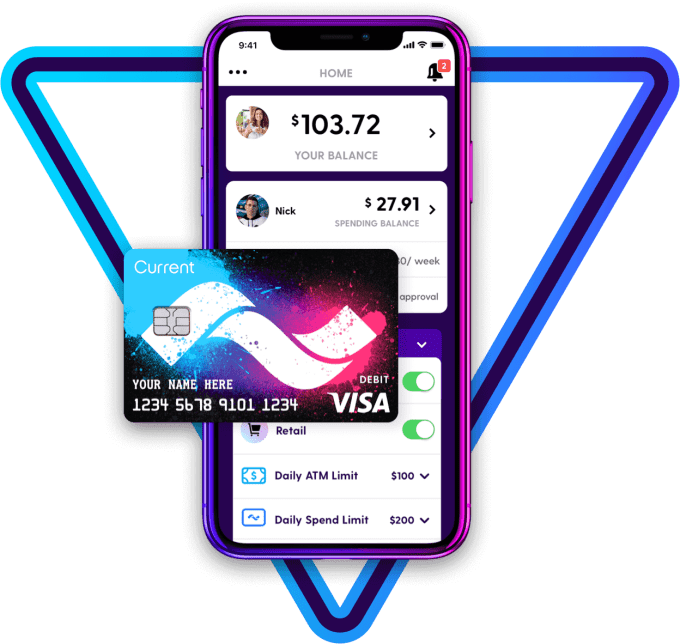

But Venmo is arriving late to the teen debit card market. Startups like Greenlight and Step let parents manage teen spending on dedicated debit cards. More companies like Kard and neo banking giant Revolut have announced plans to launch their own versions. And Venmo’s prototype uses very similar terminology to that of Current, a frontrunner in the children’s banking space with over 500,000 accounts that raised a $20 million Series B late last year.

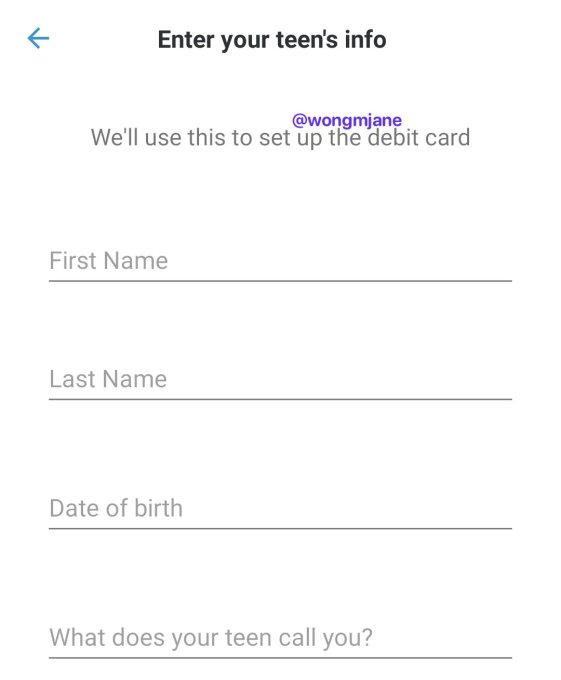

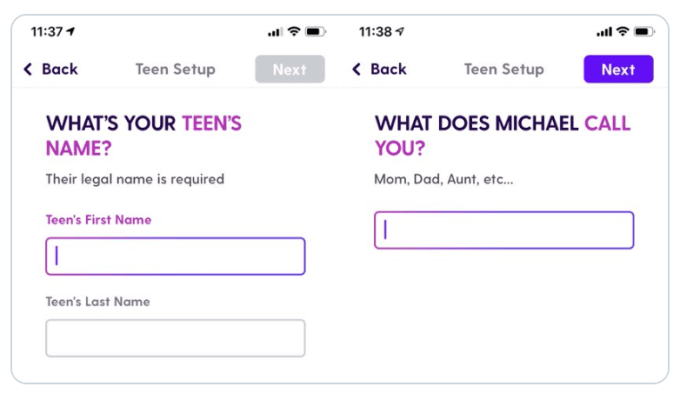

The first signs of Venmo’s debit card were spotted by reverse engineering specialist Jane Manchun Wong, who has provided slews of accurate tips to TechCrunch in the past. Hidden in Venmo’s Android app is code revealing a “delegate card” feature, designed to let users create a debit card that’s connected to their account but has limited privileges.

A screenshot generated from hidden code in Venmo’s app, via Jane Manchun Wong

A set-up screen Wong was able to generate from the code shows the option to “Enter your teen’s info,” because “We’ll use this to set up the debit card.” It asks parents to enter their child’s name, birth date and “What does your teen call you?” That’s almost identical to the “What does [your child’s name] call you?” set-up screen for Current’s teen debit card.

When TechCrunch asked about the teen debit feature and when it might launch, a Venmo spokesperson gave a cagey response that implies it’s indeed internally testing the option, writing “Venmo is constantly working to identify ways to refine and enhance the user experience. We frequently test product offerings to understand the value it could have for our users, and I don’t have anything further to share right now.”

Typically, the tech company product development flow sees them come up with ideas, mock them up, prototype them in their real apps as internal-only features, test them externally with small percentages of real users, then launch them officially if feedback and data is positive throughout. It’s unclear when Venmo might launch teen debit cards, though the product could always be scrapped. It’d need to move fast to beat Revolut and Kard to market.

Current’s teen debit card

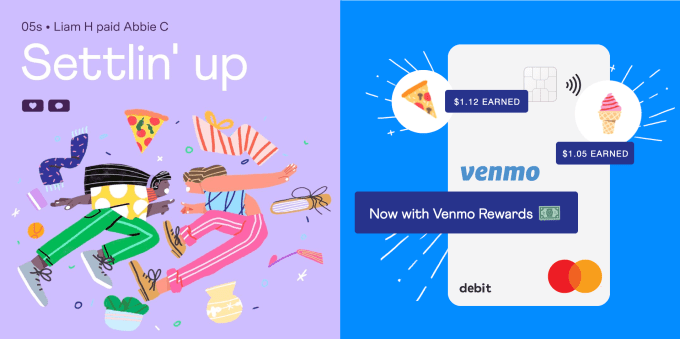

The launch would build upon the June 2018 launch of Venmo’s branded Mastercard debit card that’s monetized through interchange fees and interest on savings. It offers payment receipts with options to split charges with friends within Venmo, free withdrawls at MoneyPass ATMs, rewards and in-app features for reseting your PIN or disabling a stolen card. Venmo also plans to launch a credit card issued by Synchrony this year.

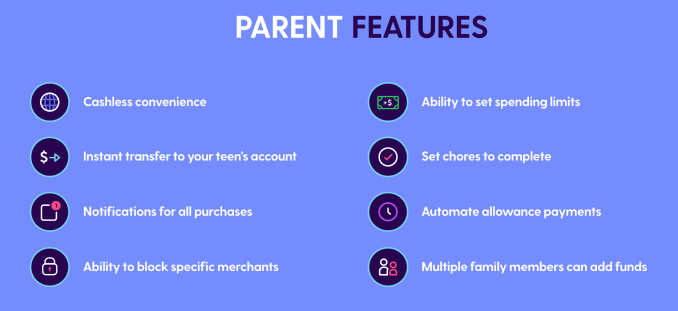

Venmo might look to equip its teen debit card with popular features from competitors, like automatic weekly allowance deposits, notifications of all purchases or the ability to block spending at certain merchants. It’s unclear if it will charge a fee like the $36 per year subscription for Current.

Current offers these features for parents who set up a teen debit card

Tech startups are increasingly pushing to offer a broad range of financial services where margins are high. It’s an easy way to earn cheap money at a time when unit economics are coming under scrutiny in the wake of the WeWork implosion. Investors are pinning their hopes on efficient financial services too, pouring $34 billion into fintech startups during 2019.

Venmo’s already become a popular way for younger people to split the bill for Uber rides or dinner. Bringing social banking to a teen demographic probably should have been its plan all along.

Powered by WPeMatico

Two years ago, we created the Matrix FinTech Index to highlight what we saw as the beginnings of a 10+ year mega innovation wave in financial services.

The trillion-dollar financial services industry was going to be turned on its head over the next decade, and we were just getting started. At the time, the top 10 publicly traded U.S. fintech companies had just surpassed the $100 billion mark in terms of total market capitalization, 12 unicorns had emerged in the category, and the U.S. VC industry had just poured in $6.7B — a record at the time.

As we predicted last year, the innovation cycle continues, and we are transitioning into its mid-phase. So what happened in U.S. fintech in 2019? In short, monster growth.

On the public side, fintechs delivered resoundingly. PayPal alone gained $26B in market capitalization. On a return basis, the public Matrix FinTech Index continued to crush every major equity index as well as the financial services incumbents. Nicely matching our forecasts, our Index delivered 213% returns over the last three years. The Index outperformed the financial services incumbents by 151 percentage points and the S&P 500 by 170 percentage points.

Powered by WPeMatico

Although the 2008 global financial crisis sparked the fintech movement, in Latin America, the rise of ecommerce was responsible for the first wave of fintech startups.

Because digital payments were key to enabling the growth of ecommerce, investors funded companies like Braspag, PagSeguro, PayU, Mercado Pago and Moip in the early 2000s to take advantage of this opportunity.

Payment is still the most relevant segment, with successful cases like Stone and PagSeguro, but after the financial crisis, we started to see the rise of financial technology in lending and neobanking, generating impressive cases like Nubank, Neon, Creditas, Credijusto and Ualá.

As the ecosystem evolves and expands, let’s take a closer look at emerging trends in Latin America that might give us a hint about where to expect its next fintech unicorns.

Latin America has seen explosive growth in ride-hailing and food delivery platforms such as Uber, Didi, Rappi and iFood, creating a totally new market opportunity — many gig economy workers can’t access basic financial services such as bank accounts, personal loans and insurance. Even those who have access often struggle with financial products that that don’t suit their needs because they were designed for full-time workers.

Spotting this opportunity, Uber Money launched at Money 2020, focusing on providing drivers with financial services. As 50% of the population in Latin America is unbanked where Uber has more than 1 million drivers, the region is definitely a ripe market. Cabify is going even farther by spinning off Lana, its company that provides financial services, so it can expand its market beyond Cabify drivers to include other gig economy professionals.

Although established players in this sector have a clear advantage, they aren’t the only ones looking to explore this opportunity; Brazilian YC alumni Zippi is offering personal loans to ride-hailing drivers based on their driving earnings. As the gig economy tends to keep growing in the region, I believe we will start to see more solutions for those professionals.

As the banking world has been shaken by fintechs, insurance companies are growing aware that high regulatory barriers won’t protect their industry from disruption.

Insurance penetration in Latin America has been historically low compared to developed markets — 3.1%, compared to 8% — but the insurance market is growing well and tends to close this gap. Adding this to bad services and complex products that insurances provide, insurtech has an immense opportunity to grow.

Because purchasing insurance is historically a complicated and painful experience, the first insurtechs in the region focused on providing a better experience by digitizing the process and using online channels to acquire customers. Those insurtechs worked together with the insurance companies and operating as online broker, but now, we’re starting to see startups providing new insurance products, as well as traditional insurances in different models.

Some are partnering with insurance companies while others are competing directly with them; Think Seg and Miituo partnered with larger players to provide a pay-as-you-go model for car insurance, while Mango Life and Kakau are offering a better purchasing experience. On the other end, Crabi and Pier are rethinking the insurance model from the ground up.

As insurtechs emerge as a potential threat, incumbents are more willing to work with startups that can improve their services to enable them to compete on better grounds, which is exactly what companies such as Bdeo, Lisa, and HelloZum are doing.

Although penetrating the insurance industry is more complicated than other financial services due to high regulatory demands and steep initial operating costs, insurtechs fueled by VC investment will without any doubt try to do it. And, if we’ve learned anything from other fintech segments, it’s that entrepreneurs will find ways to overcome initial challenges.

Powered by WPeMatico

It didn’t take much for the founders of Cora, Brazil’s newest startup to tackle some aspect of the broken financial services industry in the country, to raise their first $10 million.

Igor Senra and Leo Mendes had worked together before — founding their first online payments company, MOIP, in 2005. That company sold to WireCard in 2016 and after three years the founders were able to strike out again.

They built their initial business servicing the small and medium-sized businesses that make up roughly two-thirds of the Brazilian economy and represent some trillion dollars’ worth of transactions. But at WireCard, they increasingly were told to approach larger customers that didn’t have the same kind of demand for their services, according to Mendes.

So they built Cora — a technology-enabled lender to the small and medium-sized businesses that they knew so well.

The round was led by Kaszek Ventures, one of Latin America’s largest and most successful investment funds, with participation from Ribbit Capital — one of the most influential early-stage fintech investment firms globally.

“We created Cora to pursue our life purpose, which is to solve the financial problems faced by small and medium businesses. These businesses

The company is currently operating in closed beta and plans to launch its first product, a free SME-only mobile account, in the first half of 2020, according to the statement. Cora will later release a portfolio of payments, credit-related products and financial management tools that are currently being developed.

“So far, large financial institutions have mainly built products that focus either on individuals or on large corporate clients and have totally ignored small and medium sized enterprises, who are the most relevant creators of value in our economies,” said Mendes in a statement. “We want to offer a high-quality, customer-centric suite of financial products that addres

Powered by WPeMatico