financial services

Auto Added by WPeMatico

Auto Added by WPeMatico

JoomPay, a startup with a similar product to PayPal-owned Venmo in the U.S., is set to launch in Europe shortly after being granted a Luxembourg Electronic Money Institution (EMI) license. The app allows people to send and receive money with anyone, instantly and for free. “Venmo me” has become a common phrase in the U.S., where people use it to split bills in restaurants or similar instances. Venmo is in common use in the U.S., but it’s not available in Europe, although dozens of other innovative mobile peer to peer transfer options exist, such as Revolut, N26, Monese and Monzo. The waitlist for the app’s beta is open now (iOS, Android).

Europe leads the world’s instant payments industry, with $18 trillion in worldwide volume predicted by 2025, up from $3 trillion in 2020 — a growth of more than 500%. Western Europe — and COVID-19 — is now driving that innovation and will account for 38% of instant payment transaction value by 2025. While Europe lacks simple peer-to-peer payments solutions such as Venmo or Square Cash App in the U.S., challenger banks have stepped up to provide similar kinds of services. JoomPay’s opportunity lies in being able to be a middle-man between these various banking systems.

Shopping app Joom, which has been downloaded 150 million times in Europe, has spun-off JoomPay to solve this problem. The app allows users to send and receive money from any person, regardless of whether they use JoomPay or not — and you only need to know their email or the phone number. JoomPay connects to any existing debit/credit card or a bank account. It also provides its users with a European IBAN and an optional free JoomPay card with cashback and bonuses.

Yuri Alekseev, CEO and co-founder of JoomPay, said: “Since COVID-19 started, we’ve seen a significant decline in cash usage. People can’t meet as easily as before but still need to send money, and we offer a viable alternative.”

JoomPay may have an uphill struggle. Its main competitors in Europe are the huge TransferWise, Paysend and, of course, PayPal itself.

Powered by WPeMatico

AvePoint, a company that gives enterprises using Microsoft Office 365, SharePoint and Teams a control layer on top of these tools, announced today that it would be going public via a SPAC merger with Apex Technology Acquisition Corporation in a deal that values AvePoint at around $2 billion.

The acquisition brings together some powerful technology executives, with Apex run by former Oracle CFO Jeff Epstein and former Goldman Sachs head of technology investment banking Brad Koenig, who will now be working closely with AvePoint’s CEO Tianyi Jiang. Apex filed for a $305 million SPAC in September 2019.

Under the terms of the transaction, Apex’s balance of $352 million plus a $140 million additional private investment will be handed over to AvePoint. Once transaction fees and other considerations are paid for, AvePoint is expected to have $252 million on its balance sheet. Existing AvePoint shareholders will own approximately 72% of the combined entity, with the balance held by the Apex SPAC and the private investment owners.

Jiang sees this as a way to keep growing the company. “Going public now gives us the ability to meet this demand and scale up faster across product innovation, channel marketing, international markets and customer success initiatives,” he said in a statement.

AvePoint was founded in 2001 as a company to help ease the complexity of SharePoint installations, which at the time were all on-premise. Today, it has adapted to the shift to the cloud as a SaaS tool and primarily acts as a policy layer enabling companies to make sure employees are using these tools in a compliant way.

The company raised $200 million in January this year led by Sixth Street Partners (formerly TPG Sixth Street Partners), with additional participation from prior investor Goldman Sachs, meaning that Koenig was probably familiar with the company based on his previous role.

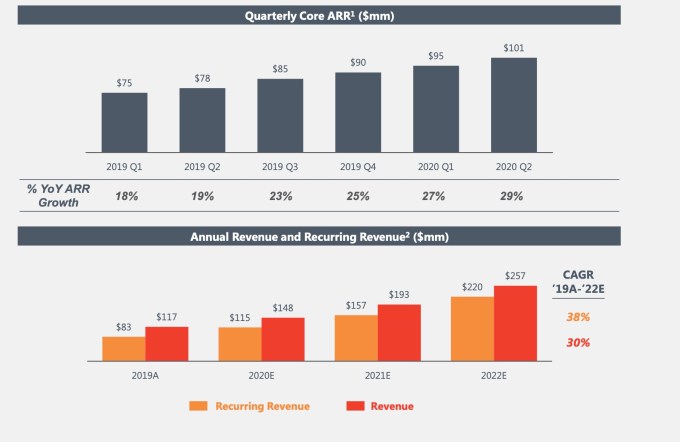

The company has raised a total of $294 million in capital before today’s announcement. It expects to generate almost $150 million in revenue by the end of this year, with ARR growing at over 30%. It’s worth noting that the company’s ARR and revenue has been growing steadily since Q12019. The company is projecting significant growth for the next two years with revenue estimates of $257 million and ARR of $220 million by the end of 2022.

Image Credits: AvePoint

The deal is expected to close in the first quarter of next year. Upon close the company will continue to be known as AvePoint and be publicly traded on Nasdaq under the new ticker symbol AVPT.

Powered by WPeMatico

Subscription services are on the rise. During the pandemic, Americans have been spending more time at home and more money on the digital products that make navigating our new normal easier.

More than ever, Americans’ lives are aided by companies like Netflix, Instacart and, of course, Amazon, which reported record-setting earnings from its 2020 Prime Day savings event.

A recent survey even found that spending on subscription services had more than tripled since March, with one in three respondents saying they’d purchased a new online subscription while quarantining.

Now, a new concern lingers: Is the market getting oversaturated? The question doesn’t just apply to streaming services and food delivery companies — it’s an issue financial technology businesses can’t afford to ignore.

As subscriptions become an increasingly alluring business model, fintechs will be forced to consider whether this proven strategy is worth the risk.

In the CompareCards survey, two-thirds of respondents said they purchased a new streaming service mainly for entertainment. Still, that doesn’t mean there isn’t room for fintechs to carve out their own space.

Bradley Leimer, co-founder of the financial consulting firm Unconventional Ventures, said he’s certainly seen more fintechs exploring subscription models. As Leimer explained, the financial services industry may have not fully embraced the idea, but it’s “starting to take notice.” Leimer, who has more than 25 years of experience in the industry, believes fintechs can learn a lot from subscription services — provided they’re willing to look in the right place.

One major lesson? Transparency. Subscription services give companies an opportunity to be upfront about their fees, as well as their benefits.

“When we talk about subscriptions, the more clear and more transparent we are, the better,” Leimer said.

Acorns is an easy case study. The microinvesting app offers three subscription levels — lite, personal and family — each with a clearly explained list of features. For what it’s worth, the company added more than 2 million users between March 2019 and March 2020, according to Forbes.

Leimer said fintechs should also take note of the way subscription services collaborate. For example, he pointed out how Amazon users can add an HBO subscription to their Prime Video account, essentially “bundling” two subscriptions into one. Fintechs, Leimer said, could stand to take a page out of that playbook.

“There are a lot of ways to sort of skin that cat — for a fintech company to generate income and for a customer to get value on top of that,” Leimer said.

Powered by WPeMatico

As 5G slowly moves from being a theoretical to an active part of the coverage map for the mobile industry — if not for consumers themselves — companies that are helping carriers make the migration less painful and less costly are seeing a boost of attention.

In the latest development, Cellwize, a startup that’s built a platform to automate and optimize data for carriers to run 5G networks within multi-vendor environments, has raised $32 million — funding that it will use to continue expanding its business into more geographies and investing in R&D to bring more capabilities to its flagship CHIME platform.

The funding is notable because of the list of strategic companies doing the investing, as well as because of the amount of traction that Cellwize has had to date.

The Series B round is being co-led Intel Capital and Qualcomm Ventures LLC, and Verizon Ventures (which is part of Verizon, which also owns TechCrunch by way of Verizon Media) and Samsung Next, with existing shareholders also participating. That list includes Deutsche Telekom and Sonae, a Portuguese conglomerate that owns multiple brands in retail, financial services, telecoms and more.

That backing underscores Cellwize’s growth. The company — which is based in Israel with operations also in Dallas and Singapore — says it currently provides services to some 40 carriers (including Verizon, Telefonica and more), covering 16 countries, 3 million cell sites, and 800 million subscribers.

Cellwize is not disclosing its valuation but it has raised $56.5 million from investors to date.

5G holds a lot of promise for carriers, their vendors, handset makers and others in the mobile ecosystem: the belief is that faster and more efficient speeds for wireless data will unlock a new wave of services and usage and revenues from services for consumers and business, covering not just people but IoT networks, too.

Notwithstanding the concerns some have had with health risks, despite much of that theory being debunked over the years, one of the technical issues with 5G has been implementing it.

Migrating can be costly and laborious, not least because carriers need to deploy more equipment at closer distances, and because they will likely be running hybrid systems in the Radio Access Network (RAN, which controls how devices interface with carriers’ networks); and they will be managing legacy networks (eg, 2G, 3G, 4G, LTE) alongside 5G, and working with multiple vendors within 5G itself.

Cellwize positions its CHIME platform — which works as an all-in-one tool that leverages AI and other tech in the cloud, and covers configuring new 5G networks, optimizing and monitoring data on them, and also providing APIs for third-party developers to integrate with it — as the bridge to letting carriers operate in the more open-shop approach that marks the move to 5G.

“While large companies have traditionally been more dominant in the RAN market, 5G is changing the landscape for how the entire mobile industry operates,” said Ofir Zemer, Cellwize’s CEO. “These traditional vendors usually offer solutions which plug into their own equipment, while not allowing third parties to connect, and this creates a closed and limited ecosystem. [But] the large operators also are not interested in being tied to one vendor: not technology-wise and not on the business side – as they identify this as an inhibitor to their own innovation.”

Cellwize provides an open platform that allows a carrier to plan, deploy and manage the RAN in that kind of multi-vendor ecosystem. “We have seen an extremely high demand for our solution and as 5G rollouts continue to increase globally, we expect the demand for our product will only continue to grow,” he added.

Previously, Zemer said that carriers would build their own products internally to manage data in the RAN, but these “struggle to support 5G.”

The competition element is not just lip service: the fact that both Intel and Qualcomm — competitors in key respects — are investing in this round underscores how Cellwize sees itself as a kind of Switzerland in mobile architecture. It also underscores that both view easy and deep integrations with its tech as something worth backing, given the priorities of each of their carrier customers.

“Over the last decade, Intel technologies have been instrumental in enabling the communications industry to transform networks with an agile and scalable infrastructure,” said David Flanagan, VP and senior MD at Intel Capital, in a statement. “With the challenges in managing the high complexity of radio access networks, we are encouraged by the opportunity in front of Cellwize to explore ways to utilize their AI-based automation capabilities as Intel brings the benefits of cloud architectures to service provider and private networks.”

“Qualcomm is at the forefront of 5G expansion, creating a robust ecosystem of technologies that will usher in the new era of connectivity,” added Merav Weinryb, Senior Director of Qualcomm Israel Ltd. and MD of Qualcomm Ventures Israel and Europe. “As a leader in RAN automation and orchestration, Cellwize plays an important role in 5G deployment. We are excited to support Cellwize through the Qualcomm Ventures’ 5G global ecosystem fund as they scale and expedite 5G adoption worldwide.”

And that is the key point. Right now there are precious few 5G deployments, and sometimes, when you read some the less shiny reports of 5G rollouts, you might be forgiven for feeling like it’s more marketing than reality at this point. But Zemer — who is not a co-founder (both of them have left the company) but has been with it since 2013, almost from the start — is sitting in on the meetings with carriers, and he believes that it won’t be long before all that tips.

“Within the next five years, approximately 75% of mobile connections will be powered by 5G, and 2.6 billion 5G mobile subscriptions will be serving 65% of the world’s population,” he said. “While 5G technology holds a tremendous amount of promise, the reality is that it is also hyper-complex, comprised of multiple technologies, architectures, bands, layers, and RAN/vRAN players. We are working with network operators around the world to help them overcome the challenges of rolling out and managing these next generation networks, by automating their entire RAN processes, allowing them to successfully deliver 5G to their customers.”

Powered by WPeMatico

It’s only been a few months since Lili announced its $10 million seed round, and it’s already raised more funding — namely, a $15 million Series A.

The startup, founded by CEO Lilac Bar David and CTO Liran Zelkha, is creating a bank account and associated products designed for freelancers, with features like early access to direct deposit payments and the ability to set aside a percentage of income for taxes.

The account (and associated Visa debit card) is free of overdraft fees or minimum balance requirements; Bar David said the company only makes money from card processing fees.

She also said that the platform has seen rapid growth this year, with transactions up 700% since the beginning of the pandemic and nearly 100,000 accounts opened since the launch in 2019.

Bar David suggested that the economic turmoil caused by COVID-19 has prompted (or forced) more skilled workers — such as programmers and digital marketers — to turn to freelancing. Meanwhile, she’s also seen “a big shift from part-time freelance to full-time freelance.”

Lili CEO Lilac Bar David

Bar David predicted that the recent growth of the freelance economy won’t simply disappear once the pandemic is over, because workers are discovering the benefits of freelancing.

“If you have a 9-to-5 job, you’re dependent on one employer,” she said. “If something happens you’re out of a job … If you’ve got a diversified customer base, you’re not dependent on just one source of income.”

In recent months, Lili has added new features like automatically generated quarterly income and expense reports, a digital debit card (which customers can use before the physical card arrives in the mail) and the ability to send and receive money via Google Pay (Lili already supported Cash App and Venmo) .

Bar David said the startup decided to raise more funding to expand its engineering team and further accelerate its growth. Apparently she was preparing for a traditional Series A fundraising process (albeit one that was conducted in the middle of a pandemic), but “our current investors were so tremendously impressed by the product-market fit and the growth” that they were willing to fund almost all of the new round.

So the Series A was led by previous investor Group 11, with participation from Foundation Capital, AltaIR Capital, Primary Venture Partners and Torch Capital — along with new backer Zeev Ventures.

“As the global workforce evolves at a rapid pace, we are excited to lead another round of funding to help Lili capitalize on unprecedented demand and offer an entirely new solution to help freelancers seamlessly save time and money,” said Group 11’s Dovi Frances in a statement.

Powered by WPeMatico

Silverflow, a Dutch startup founded by Adyen alumni, is breaking cover and announcing seed funding.

The pre-launch company has spent the last two years building what it describes as a “cloud-native” online card processor that directly connects to card networks. The aim is to offer a modern replacement for the 20 to 40-year-old payments card processing tech that is mostly in use today.

Backing Silverflow’s €2.6 million seed round is U.K.-based VC Crane Venture Partners, with participation from Inkef Capital and unnamed angel investors and industry leaders from Pay.On, First Data, Booking.com and Adyen. It brings the fintech startup’s total funding to date to ~€3 million.

Bootstrapped while in development and launching in 2021, Silverflow’s founders are CEO Anne-Willem de Vries (who was focused on card acquiring and processing at Adyen), CBDO Robert Kraal (former Adyen COO and EVP global card acquiring & processing of Adyen) and CTO Paul Buying (founder of acquired translation startup Livewords).

“The payments tech stack needs an upgrade,” Kraal tells me. “Today’s card payment infrastructure based on 30 to 40-year-old technology is still in use across the global payment landscape. This legacy infrastructure is costing everyone time and money: consumers, merchants, payment-service-providers and banks. The legacy platforms require a lengthy on-boarding process and are expensive to maintain, [and] they also aren’t fit for purpose today because they don’t support data use”.

In addition, Kraal says that adding new functionality is a lengthy and expensive process, requiring the effort of specialised engineers which ultimately slows down innovation “for the whole card payments system”.

“Finally, every acquirer provides its customer with a different processing platform, which for a typical payment service provider (PSP) means they have to deal with multiple legacy platforms — and all the costs and specialised support each entails,” adds de Vries.

To solve this, Silverflow claims it has built the first payments processor with a “cloud-native platform” built for today’s technology stack. This includes offering simple APIs and “streamlined data flows” directly integrated into the card networks.

Continues de Vries: “Instead of managing a complex network of acquirers across markets with dozens of bank and card network connections to maintain, Silverflow provides card-acquiring processing as a service that connects to card networks directly through a simple API”.

Target customers are PSPs, acquirers and “global top-market merchants” that are seeing €500 million to 10 billion in annual transactions.

“As a managed service, Silverflow provides the maintenance for connections and new product innovation that users have typically had to support in-house or work on long-term product road maps with suppliers,” explains Kraal. “Based in the cloud, Silverflow is infinitely scalable for peak flows and also provides robust data insights that users haven’t previously been able to access”.

With regards to competitors, Kraal says there are no other companies at the moment doing something similar, “as far as we are aware”. Currently, acquirers use traditional third-party processors, such as SIA, Omnipay, Cybersource or MIGS. Some companies, like Adyen, have built their own in-house processing platform.

So, why hasn’t a cloud-native card processing platform like Silverflow been done before and why now? A lack of awareness of the problem might be one reason, says de Vries.

“Unless you have built several integrations to acquirers during your career, you are not aware that the 30 to 40-years-old infrastructure is still in use. This is not typically a problem some bright college graduates would tackle,” he posits.

“Second, to build this successfully, you need to have prior knowledge of the card payments industry to navigate all the legal, regulatory and technical requirements.

“Thirdly, any large corporate currently active in card payment processing will be aware of the problem and have the relevant industry knowledge. However, building a new processing platform would require them to allocate their most talented staff to this project for two-three years, taking away resources from their existing projects. In addition, they would also need to manage a complex migration project to move their existing customers from their current system to the new one and risk losing some of the customers along the way”.

Powered by WPeMatico

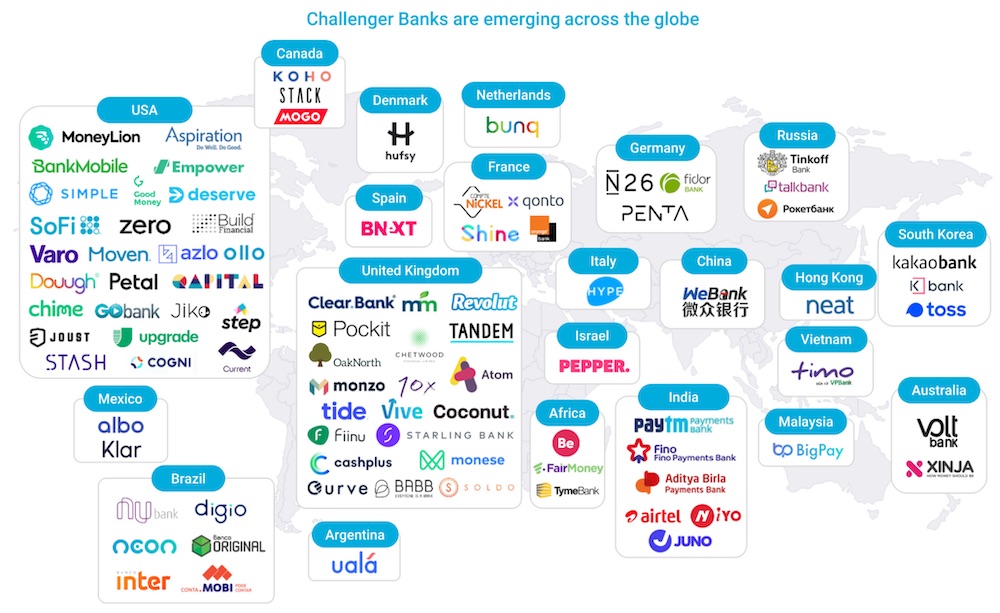

The neobank, or digital bank, phenomenon continues to take the world by storm, with global winners, from Brazil’s Nubank valued at $10 billion and Berlin’s N26 valued at $3.5 billion, to Chime, now valued at $14.5 billion as the most valuable consumer fintech in the United States.

Neobanks have led the charge of the $3.6 billion in venture capital funding for consumer fintech startups this year. And as the coronavirus-fueled acceleration of digital transformation continues, it seems the digital bank is here to stay, with some estimates pointing to neobanks reaching 60 million customers in North America and Europe by the end of 2020, and surpassing 145 million by 2024.

The space is also becoming more crowded, a trend which will only accelerate with fintech eating the world and creating greater infrastructure that enables any company to include a bank account as a product extension.

FT Partners Fintech Industry Research, January 2020

As a result, neobanks are not a monolithic model and not all are created equal. Looking underneath the hood of business models across the globe reveals remarkable operational differences and highlights specific features that are more likely to succeed in the long-term.

Today there are five distinct models that are leading globally:

Interchange-led: Relies on payments revenue, sourced through interchange as the revenue driver. Every time a customer uses the neobank’s card as a payment method they get paid [e.g. Chime / US; Neon (hybrid of 1 & 2) / Brazil].

Credit-led: Leverages a credit-first model, starting off with a credit card or similar offering, and later providing a bank account [e.g. Nubank, Neon (hybrid of 1 & 2) / Brazil].

Powered by WPeMatico

A month after completing Y Combinator’s accelerator program, BukuWarung, an financial tech startup that serves small businesses in Indonesia, announced it has raised new funding from a roster of high-profile investors, including partners of DST Global, Soma Capital and 20VC.

The amount of the funding was undisclosed, but a source told TechCrunch that it was between $10 million to $15 million. The new capital will be used to hire for BukuWarung’s technology team. TechCrunch first profiled BukuWarung in July.

Angel investors in the round include several high-profile founders and executives: finance technology platform Plaid’s co-founder William Hockey; Tinder co-founder Justin Mateen; Superhuman founder Rahul Vohra; Adobe chief product officer Scott Belsky; Clearbit chairman and startup advisor Josh Buckley; former Uber chief product officer Manik Gupta; Spotify’s former head of new markets in Asia Sriram Krishnan; 20VC founder Harry Stebbings; Nancy Xiao, an investor with Bond Capital; and Fast co-founder Allison Barr Allen. Angel investors from WhatsApp, Square and Airbnb also participated.

Launched last year by co-founders Chinmay Chauhan and Abhinay Peddisetty, BukuWarung is targeted at the 60 million “micromerchants” in Indonesia, including neighborhood store (or warung) owners. The app was originally created as a replacement for pen and apper ledgers, but plans to introduce financial services including credit, savings and insurance. In August, the company integrated digital payments into its platform, enabling merchants to take customer payments from bank accounts and digital wallets like OVO and DANA. BukuWarung’s goal is to fill the same role for Indonesian merchants that KhataBook and OKCredit do in India.

One of the reasons BukuWarung launched digital payments was in response to customer demand for contactless transactions and instant payouts during the COVID-19 pandemic. Since introducing the feature, the company said it has already processed several million U.S. dollars in total payment volume (TPV) on an annualized basis. The company says it now serves about 1.2 million merchants across 750 locations in Indonesia, focusing on tier 2 and tier 3 cities.

Digital payments is also the first step into building out BukuWarung’s financial services, which will help differentiate it from other bookkeeping. The payments features is currently free and BukuWarung is experimenting with different monetization models, including making a small margin on fees.

“The reason why we launched payments is also very strategic, because there is a lot of pull in the market. We have already seen several millions annualized TPV in less than a month, because the payments we offer are cost-efficient as well and cheaper than to get from a bank,” Chauhan told TechCrunch.

“If you look at the Indian players, like Khatabook, they have also launched digital payments. The reason for that is because it’s a very essential step for building a business and monetization,” he added. “If you don’t have payments, you can’t do anything like that.”

Chauhan added that building a financial services platform is the difference between providing a utility app that replaces bookkeeping ledgers, and becoming an essential service for merchants that will eventually include lending for working capital, savings and insurance products. The bookkeeping features on BukuWarung will feed into the financial services aspect by providing data to score creditworthiness, and help small merchants, who often have difficulty securing working capital from traditional banks, get access to lines of credit.

Powered by WPeMatico

Hasura, a service that provides developers with an open-source engine that provides them a GraphQL API to access their databases, today announced that it has raised a $25 million Series B round led by Lightspeed Venture Partners. Previous investors Vertex Ventures US, Nexus Venture Partners, Strive VC and SAP.iO Fund also participated in this round.

The new round, which the team raised after the COVID-19 pandemic had already started, comes only six months after the company announced its $9.9 million Series A round. In total, Hasura has now raised $36.5 million.

In addition to the new funding, Hasura also today announced that it has added support for MySQL databases. Until now, the company’s service only worked with PostgreSQL databases.

Rajoshi Ghosh, co-founder and COO (left) and Tanmai Gopal, co-founder and CEO (right). Image Credits: Hasura

As the company’s CEO and co-founder Tanmai Gopal told me, MySQL support has long been at the top of the most requested features by the service’s users. Many of these users — who are often in the healthcare and financial services industry — are also working with legacy systems they are trying to connect to modern applications and MySQL plays an important role there, given how long it has been around.

In addition to adding MySQL support, Hasura is also adding support for SQL Server to its lineup, but for now, that’s in early access.

“For MySQL and SQL Server, we’ve seen a lot of demand from our healthcare and financial services / fin-tech users,” Gopal said. “They have a lot of existing online data, especially in these two databases, that they want to activate to build new capabilities and use while modernizing their applications.

Today’s announcement also comes only a few months after the company launched a fully managed cloud service for its service, which complements its existing paid Pro service for enterprises.

“We’re very impressed by how developers have taken to Hasura and embraced the GraphQL approach to building applications,” said Gaurav Gupta, partner at Lightspeed Venture Partners and Hasura board member. “Particularly for front-end developers using technologies like React, Hasura makes it easy to connect applications to existing databases where all the data is without compromising on security and performance. Hasura provides a lovely bridge for re-platforming applications to cloud-native approaches, so we see this approach being embraced by enterprise developers as well as front-end developers more and more.”

The company plans to use the new funding to add support for more databases and to tackle some of the harder technical challenges around cross-database joins and the company’s application-level data caching system. “We’re also investing deeply in company building so that we can grow our GTM and engineering in tandem and making some senior hires across these functions,” said Gopal.

Powered by WPeMatico

Lana, a new startup based in Madrid, is looking to be the next big thing in Latin American fintech.

Founded by serial entrepreneur Pablo Muniz, whose last business was backed by one of Spain’s largest financial services institutions, BBVA, Lana is looking to be the all-in-one financial services provider for Latin America’s gig economy workers.

Muniz’s last company, Denizen, was designed to provide expats in foreign and domestic markets with the financial services they would need as they began their new lives in a different country. While the target customer for Lana may not be the same middle to upper-middle-class international traveler that he had previously hoped to serve, the challenges gig economy workers face in Latin America are much the same.

Muniz actually had two revelations from his work at Denizen. The first — he would never try to launch a fintech company in conjunction with a big bank. And the second was that fintechs or neobanks that focus on a very niche segment will be successful — so long as they can find the right niche.

The biggest niche that Muniz saw that was underserved was actually in the gig economy space in Latin America. “I knew several people who worked at gig economy companies and I knew that their businesses were booming and the industry was growing,” he said. “[But] I was concerned about the inequalities.”

Workers in gig economy marketplaces in Latin America often don’t have bank accounts and are paid through the apps on which they list their services in siloed wallets that are exclusive to that particular app. What Lana is hoping to do is become the wallet of wallets for all of the different companies on which laborers list their services. Frequently, drivers will work for Uber or Cabify and deliver food for Rappi. Those workers have wallets for each service.

(Photo by Cris Faga/Pacific Press/LightRocket via Getty Images)

Lana wants to unify all of those disparate wallets into a single account that would operate like a payment account. These accounts can be opened at local merchant shops and, once opened, workers will have access to a debit card that they can use at other locations.

The Lana service also has a bill pay feature that it’s rolling out to users, in the first evolution of the product into a marketplace for financial services that would appeal to gig workers, Muniz said.

“We want to become that account in which they receive funds,” he said. “We are still iterating the value proposition to gig economy companies.”

Working with companies like Cabify, and other, undisclosed companies, Lana has plans to roll out in Mexico, Chile, Peru and, eventually, Colombia and Argentina.

Eventually, Lana hopes to move beyond basic banking services like deposits and payments and into credit services. Already hundreds of customers are using the company’s service through the distribution partnership with Cabify, which ran the initial pilot to determine the viability of the company’s offering.

“The idea of creating Lana was initially tested as an internal project at Cabify,” Muniz wrote in an email. “Soon Cabify and some potential investors saw that Lana could have a greater impact as an independent company, being able to serve gig economy workers from any industry and decided to start over a new entrepreneurial project.”

Through those connections with Cabify, Lana was able to bring in other investors like the Silicon Valley-based investment firm Base 10.

“One of the things we’ve been interested in is in inclusion generally and in fintech specifically,” said Adeyemi Ajao, the firm’s co-founder. “We had gotten very close to investing in a couple of fintech companies in Latin America and that is because the opportunity is huge. There are several million people going from unbanked to banked in the region.”

Along with a few other investors, Base 10 put in $12.5 million to finance Lana as it looks to expand. It’s a market that has few real competitors. Nubank, Latin America’s biggest fintech company, is offering credit services across the continent, but most of their end users already have an established financial history.

“Most of their end users are not unbanked,” said Ajao. “With Lana it is truly gig workers… They can start by being a wallet of wallets and then give customers products that help them finance their cars or their scooters.”

The ultimate idea is to get workers paid faster and provide a window into their financial history that can give them more opportunities at other gig economy companies, said Ajao. “The vision would be that someone can plug in their financial information for services. If they’re working for Rappi and have never been an Uber driver and they want to be an Uber driver, Lana can use their financial history with Rappi to offer a loan on a car,” he said.

That financial history is completely inaccessible to a traditional bank, and those established financial services don’t care about the history built in wallets that they can’t control or track. “Today if you’ve been a gig worker and you go to a bank, that’s worth nothing,” said Ajao.

Powered by WPeMatico