financial services

Auto Added by WPeMatico

Auto Added by WPeMatico

Technology plays a huge role in nearly every aspect of financial services today. As the world moved online, tools and infrastructure to help people manage their money and make payments have burgeoned the world over in the past decade.

With much of the finance world now leveraging technology to conduct business, predict trends and deliver services, financial services regulators are also developing new technologies to monitor markets, supervise financial institutions and conduct other administrative activities. The emergence of purpose-built technologies to facilitate regulator oversight has, over the past few years, garnered its own moniker of supervisory technology, or suptech.

Interest in suptech is proliferating across the globe thanks to a diverse set of prudential and conduct regulators. A sampling of regulators developing suptech include the FDIC, CFPB, FINRA and Federal Reserve in the U.S.; the U.K.’s FCA and Bank of England; the National Bank of Rwanda in Africa; as well as the ASIC, HKMA and MAS in Asia. Several “super regulators” are also engaged in suptech efforts such as the Bank of International Settlements, the Financial Stability Board and the World Bank.

The strides in suptech demonstrate that creative thinking coupled with experimentation and scalable, easily accessible technologies are jump-starting a new approach to regulation.

In this post, we’ll examine a few core suptech use cases, consider its future and explore the challenges facing regulators as the market matures. The uses are diverse, so we’ll focus on three key areas: regulatory reporting, machine-readable regulation, and market and conduct oversight.

A quick general note: Nearly every financial services regulator is engaged in some type of suptech activity and the use cases discussed in this article are intended as a sample, not a comprehensive list.

As a preliminary matter, we should quickly survey a few definitions of suptech to frame our understanding. Both the World Bank and BIS have offered definitions that provide useful outlines for this discussion. The World Bank states that suptech “refers to the use of technology to facilitate and enhance supervisory processes from the perspective of supervisory authorities.” It’s a little circular, but helpful.

The BIS defines suptech as “the use of technology for regulatory, supervisory and oversight purposes.” This is a similarly loose definition that describes the broader scope better.

Regardless of differences on the margins, the “sup” in these suptech definitions acknowledges the primacy of the idea that regulators’ objectives are to oversee the conduct, structure, and health of the financial system. Suptech technologies facilitate related regulatory supervision and enforcement processes.

Regulatory reporting refers to a broad swath of activities such as financial firms providing trading data to regulatory authorities and regulators’ analysis of financial data or corporate information to determine the projected health or potential risks facing an institution or the market.

The MAS and FDIC are incorporating transactional and financial data reported by firms as a means to assess their financial viability. The MAS, in conjunction with BIS, has run tech sprints soliciting new ideas relating to regulatory reporting, while the FDIC has “a regulatory reporting solution that would allow ‘on-demand’ monitoring of banks as opposed to being constrained by ‘point-in-time’ reporting. This project is particularly targeted at smaller, community banks that provide only aggregated data on their financial health on a quarterly basis.”

The HKMA recently outlined its three-year plan for the development of suptech, which includes developing an approach to “network analysis.” The HKMA will analyze reporting data related to corporate shareholding and financial exposure to bring them “to life as network diagrams, so that the relationships between different entities become more apparent. Greater transparency of the connections and dependencies between banks and their customers will enable HKMA supervisors to detect early warning signals within the entire credit network.”

These reporting initiatives touch on a theme regulators have continuously struggled with: How to regulate markets and firms based on a reactive approach to historical data. Regulation and enforcement are often retrospective activities — examining past behavior and data to decide how to sanction an organization or develop a regulatory framework to govern a particular type of activity or financial product. This can result in an approach to regulation too rooted in past failures, which might lack the flexibility to anticipate or adapt to emerging risks or financial products.

Powered by WPeMatico

Orum, which aims to speed up the amount of time it takes to transfer money between banks, announced today it has raised $56 million in a Series B round of funding.

Accel and Canapi Ventures co-led the round, which also included participation from existing backers Bain Capital Ventures, Inspired Capital, Homebrew, Acrew, Primary, Clocktower and Box Group. The financing comes barely three months after Orum announced a $21 million Series A, and brings its total raised to over $82 million.

Orum CEO Stephany Kirkpatrick launched the company in 2019 after working for several years at LearnVest, a personal finance site founded by Alexa von Tobel that was acquired by Northwestern Mutual in 2015 for an estimated $375 million. Tobel went on to form Inspired Capital, a venture capital firm that put money in Orum’s $5.2 million seed round last August. Prior to that, the firm also provided Orum with an “inspiration check” that was the first money into the business.

“Most Americans are not familiar with the intricacies of ACH [automated clearing house) or why it takes multiple business days to move money between accounts,” Kirkpatrick said. “But none of us can allow money to wait 5-7 days to hit our accounts. It needs to be instant.”

Her mission with Orum is straightforward even if the technology behind it is complex. Put simply, Orum aims to use machine learning-backed APIs to “move money smartly across all payment rails, and in doing so, provide universal financial access.”

Orum’s first embeddable product, Foresight, launched in September of 2020. It’s an automated programming interface designed to give financial institutions a way to move money in real time. The platform uses machine learning and data science to predict when funds are available and to identify any potential risks. Its Momentum product “intelligently” routes funds across payments rails and is powered by banking providers JPMorgan Chase and Silicon Valley Bank.

“They power the back end of our Momentum platform that allows the money to move on a multirail basis,” Kirkpatrick told TechCrunch. “They power our access to real-time payments.”

Orum says it serves a range of enterprise partners, including Alloy, HM Bradley, First Horizon Bank and Zero Financial (which was recently acquired by Avant).

The volume of transactions being conducted with Orum is growing 100% month over month, Kirkpatrick said. Most of its early growth has come from word of mouth.

The remote-first company prides itself on diversity — in both its employee and investor base. For one, 48% of its 55-person headcount are female, and 48% are “nonwhite,” according to Kirkpatrick. Orum also recently joined the Cap Table Coalition — a partnership between high-growth startups and emerging investors who want to work to close the racial wealth gap — to allocate over 10% of its Series B round to underrepresented founders. For example, the financing includes investors such as the Neythri Features Fund, a group of South Asian women investing in the next generation of female founders and diverse teams.

Jeffrey Reitman, partner at Canapi Ventures (a firm whose LPs mostly consist of banks), told TechCrunch that those bank LPs conduct hundreds of millions of ACH transactions annually,

“They need a path to achieving a state where funds can be transferred instantly,” he said. “Orum’s product paves the path for many players in financial services and fintech — and beyond — to partake in faster money movement without compromising key risk principles.”

To Reitman, the company’s major differentiators are its team, which he describes as consisting of “the best group of data scientists and engineers in the space.”

“Many of their customers consider the team to be instrumental in helping to set the risk dials on how they fund transactions by teasing out key data and insights from historical transaction data,” he said. “Second, Orum is building one of the densest and most comprehensive data sets around the risks of money movement. Better data means better risk models, and it will be hard for other offerings to match Orum’s approach to building this rich data set.”

Accel Partner Sameer Gandhi, who joined Orum’s board as part of the latest financing, agrees. He believes that in an 18-month period, Orum has built “game-changing technology and an exceptional team.”

“Orum is tackling financial infrastructure from its foundation,” he said.

The headline was updated post-publication to reflect the correct funding amount.

Powered by WPeMatico

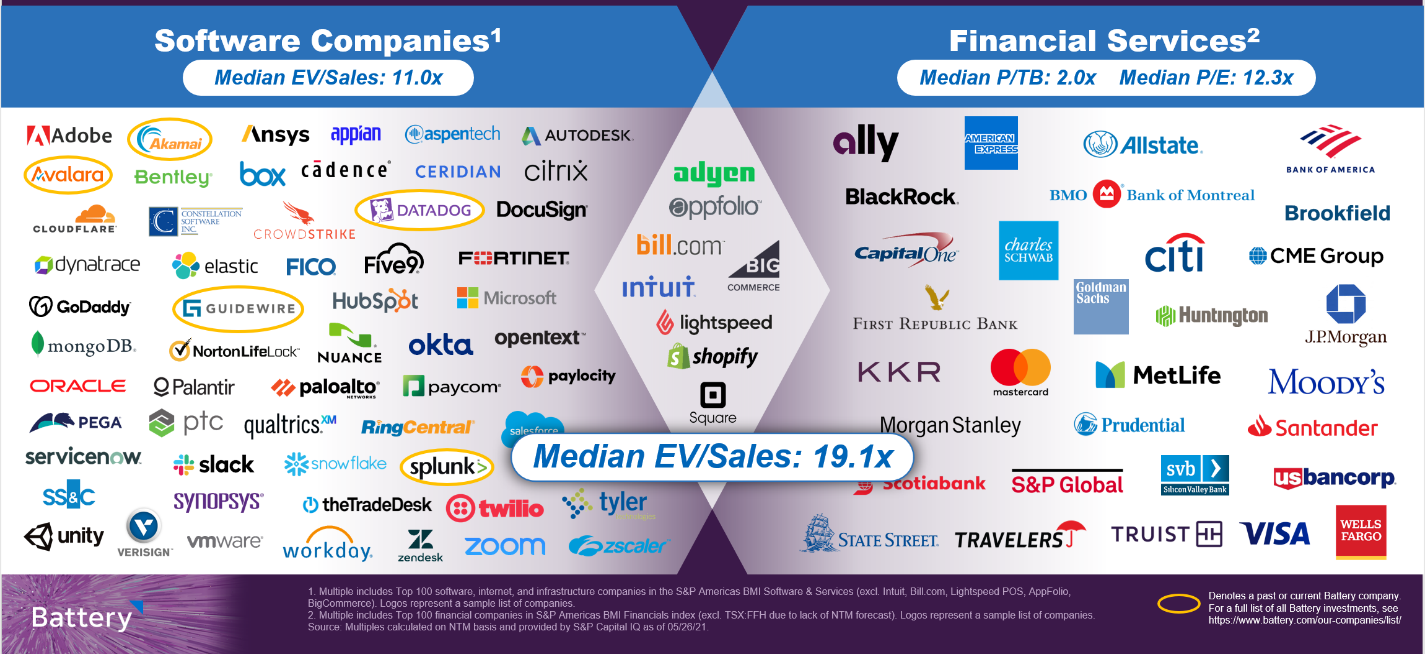

If money is the ultimate commodity, how can fintechs — which sell money, move money or sell insurance against monetary loss — build products that remain differentiated and create lasting value over time?

And why are so many software companies — which already boast highly differentiated offerings and serve huge markets— moving to offer financial services embedded within their products?

A new and attractive hybrid category of company is emerging at the intersection of software and financial services, creating buzz in the investment and entrepreneurial communities, as we discussed at our “Fintech: The Endgame” virtual conference and accompanying report this week.

These specialized companies — in some cases, software companies that also process payments and hold funds on behalf of their customers, and in others, financial-first companies that integrate workflow and features more reminiscent of software companies — combine some of the best attributes of both categories.

Image Credits: Battery Ventures

From software, they design for strong user engagement linked to helpful, intuitive products that drive retention over the long term. From financials, they draw on the ability to earn revenues indexed to the growth of a customer’s business.

Fintech is poised to revolutionize financial services, both through reinventing existing products and driving new business models as financial services become more pervasive within other sectors.

The powerful combination of these two models is rapidly driving both public and private market value as investors grant these “super” companies premium valuations — in the public sphere, nearly twice the median multiple of pure software companies, according to a Battery analysis.

The near-perfect example of this phenomenon is Shopify, the company that made its name selling software to help business owners launch and manage online stores. Despite achieving notable scale with this original SaaS product, Shopify today makes twice as much revenue from payments as it does from software by enabling those business owners to accept credit card payments and acting as its own payment processor.

The combination of a software solution indexed to e-commerce growth, combined with a profitable payments stream growing even faster than its software revenues, has investors granting Shopify a 31x multiple on its forward revenues, according to CapIQ data as of May 26.

Before even talking about how investors should value these hybrid companies, it’s worth making the point that in both private and public markets, fintechs have been notoriously hard to value, fomenting controversy and debate in the investment community.

Powered by WPeMatico

Fintech and proptech are two sectors that are seeing exploding growth in Latin America, as financial services and real estate are two categories in particular dire need of innovation in a region.

Brazil’s QuintoAndar, which has developed a real estate marketplace focused on rentals and sales, has seen impressive growth in recent years. Today, the São Paulo-based proptech has announced it has closed on $300 million in a Series E round of funding that values it at an impressive $4 billion.

The round is notable for a few reasons. For one, the valuation — high by any standards but especially for a LatAm company — represents an increase of four times from when QuintoAndar raised a $250 million Series D in September 2019.

It’s also noteworthy who is backing the company. Silicon Valley-based Ribbit Capital led its Series E financing, which also included participation from SoftBank’s LatAm-focused Innovation Fund, LTS, Maverik, Alta Park, an undisclosed U.S.-based asset manager fund with over $2 trillion in AUM, Kaszek Ventures, Dragoneer and Accel partner Kevin Efrusy.

Having backed the likes of Coinbase, Robinhood and CreditKarma, Ribbit Capital has historically focused on early-stage investments in the fintech space. Its bet on QuintoAndar represents clear faith in what the company is building, as well as its confidence in the startup’s plans to branch out from its current model into a one-stop real estate shop that also offers mortgage, title, insurance and escrow services.

The latest round brings QuintoAndar’s total raised since its 2013 inception to $635 million.

Ribbit Capital Partner Nick Huber said QuintoAndar has over the years built “a unique and trusted brand in Brazil” for those looking for a place to call home.

“Whether you are looking to buy or to rent, QuintoAndar can support customers through the entire transaction process: from browsing verified inventory to signing the final contracts,” Huber told TechCrunch. “The ability to serve customers’ needs through each phase of life and to do so from start to finish is a unique capability, both in Brazil and around the world.”

QuintoAndar describes itself as an “end-to-end solution for long-term rentals” that, among other things, connects potential tenants to landlords and vice versa. Last year, it expanded also into connecting a home buyers to sellers.

Image Credits: QuintoAndar

TechCrunch spoke with co-founder and CEO Gabriel Braga and he shared details around the growth that has attracted such a bevy of high-profile investors.

Like most other businesses around the world, QuintoAndar braced itself for the worst when the COVID-19 pandemic hit last year — especially considering one core piece of its business is to guarantee rents to the landlords on its platform.

“In the beginning, we were afraid of the implications of the crisis but we were able to honor our commitments,” Braga said. “In retrospect, the pandemic was a big test for our business model and it has validated the strength and defensibility of our business on the credit side and reinforced our value proposition to tenants and landlords. So after the initial scary moments, we actually felt even more confident in the business that we are building.”

QuintoAndar describes itself as “a distant market leader” with more than 100,000 rentals under management and about 10,000 new rentals per month. Its rental platform is live in 40 cities across Brazil, while its home-buying marketplace is live in four. Part of its plans with the new capital is to expand into new markets within Brazil, as well as in Latin America as a whole.

The startup claims that, in less than a year, QuintoAndar managed to aggregate the largest inventory among digital transactional platforms. It now offers more than 60,000 properties for sale across Sao Paulo, Rio de Janeiro, Belho Horizonte and Porto Alegre. To give greater context around the company’s growth of that side of its platform: In its first year of operation, QuintoAndar closed more than 1,000 transactions. It has now surpassed the mark of 8,000 transactions in annualized terms, growing between 50% and 100% quarter over quarter.

As for the rentals side of its business, Braga said QuintoAndar has more than 100,000 rentals under management and is closing about 10,000 new rentals per month. The company is not profitable as it’s focused on growth, although it’s unit economics are particularly favorable in certain markets such as Sao Paulo, which is financing some of its growth in other cities, according to Braga.

Now, the 2,000-person company is looking to begin its global expansion with plans to enter the Mexican market later this year. With that, Braga said QuintoAndar is looking to hire “top-tier” talent from all over.

“We want to invest a lot in our product and tech core,” he said. “So we’re trying to bring in more senior people from abroad, on a global basis.”

CEO Braga and CTO André Penha came up with the idea for QuintoAndar after receiving their MBAs at Stanford University. As many startups do, the company was founded out of Braga’s personal “nightmare” of an experience — in this case, of trying to rent an apartment in Sao Paulo.

The search process, he recalls, was difficult as there was not enough information available online and renters were forced to provide a guarantor, or co-signer, from the same city or pay rent insurance, which Braga described as “very expensive.”

“Overall, I felt it was a very inefficient and fragmented process with no transparency or tech,” Braga told me at the time of the company’s last raise. “There was all this friction and high cost involved, just real tangible problems to solve.”

The concept for QuintoAndar (which can be translated literally to “Fifth Floor” in Portuguese) was born.

“Little by little, we created a platform that consolidated supply and inventory in a uniform way,” Braga said.

The company took the search phase online for the first time, according to Braga. It also eliminated the need for tenants to provide a guarantor, thereby saving them money. On the other side, QuintoAndar also works to help protect the landlord with the guarantee that they will get their rent “on time every month,” Braga said.

It’s been interesting watching the company evolve and grow over time, just as it’s been fascinating seeing the region’s startup scene mature and shine in recent years.

Powered by WPeMatico

An estimated 41 million Americans say they need life insurance but have yet to purchase coverage. Despite this awareness among consumers, the Life Insurance Marketing and Research Association estimates a $12 trillion coverage gap, with about 50% of millennials planning to purchase coverage within the next year.

There’s latent demand for life insurance currently unaddressed by much of the financial services industry, and embedded finance can be the solution. It’s imperative for companies to consider product lines and partnerships to expand markets, create new revenue streams and provide added value to their customers.

There’s latent demand for life insurance currently unaddressed by much of the financial services industry, and embedded finance can be the solution.

Connecting consumers with products they need through channels they already know and trust is both a massive revenue opportunity and a social good, providing financial resilience to families at a time when they need it most.

The concept of digitally bundling financial products in a packaged offering to a customer is certainly not new — but it is for the life insurance space.

Embedded finance uses technology and operations infrastructure to offer products and services through entities that may not be financial institutions at all. Think of embedded finance like on-demand shopping; customers benefit from both the transaction (buying financial protection for their families) and the convenience it provides (from whatever platform they are currently engaging with).

Similar to how Amazon saves shoppers 75 hours a year, bundling life insurance gives consumers back time in their day and can improve their financial health.

Powered by WPeMatico

Amount, a company that provides technology to banks and financial institutions, has raised $99 million in a Series D funding round at a valuation of just over $1 billion.

WestCap, a growth equity firm founded by ex-Airbnb and Blackstone CFO Laurence Tosi, led the round. Hanaco Ventures, Goldman Sachs, Invus Opportunities and Barclays Principal Investments also participated.

Notably, the investment comes just over five months after Amount raised $86 million in a Series C round led by Goldman Sachs Growth at a valuation of $686 million. (The original raise was $81 million, but Barclays Principal Investments invested $5 million as part of a second close of the Series C round). And that round came just three months after the Chicago-based startup quietly raised $58 million in a Series B round in March. The latest funding brings Amount’s total capital raised to $243 million since it spun off from Avant — an online lender that has raised over $600 million in equity — in January of 2020.

So, what kind of technology does Amount provide?

In simple terms, Amount’s mission is to help financial institutions “go digital in months — not years” and thus, better compete with fintech rivals. The company formed just before the pandemic hit. But as we have all seen, demand for the type of technology Amount has developed has only increased exponentially this year and last.

CEO Adam Hughes says Amount was spun out of Avant to provide enterprise software built specifically for the banking industry. It partners with banks and financial institutions to “rapidly digitize their financial infrastructure and compete in the retail lending and buy now, pay later sectors,” Hughes told TechCrunch.

Specifically, the 400-person company has built what it describes as “battle-tested” retail banking and point-of-sale technology that it claims accelerates digital transformation for financial institutions. The goal is to give those institutions a way to offer “a secure and seamless digital customer and merchant experience” that leverages Amount’s verification and analytics capabilities.

Image Credits: Amount

HSBC, TD Bank, Regions, Banco Popular and Avant (of course) are among the 10 banks that use Amount’s technology in an effort to simplify their transition to digital financial services. Recently, Barclays US Consumer Bank became one of the first major banks to offer installment point-of-sale options, giving merchants the ability to “white label” POS payments under their own brand (using Amount’s technology).

“The pandemic dramatically accelerated banks’ interest in further digitizing the retail lending experience and offering additional buy now, pay later financing options with the rise of e-commerce,” Hughes, former president and COO at Avant, told TechCrunch. “Banks are facing significant disruption risk from fintech competitors, so an Amount partnership can deliver a world-class digital experience with significant go-to-market advantages.”

Also, he points out, consumers’ digital expectations have changed as a result of the forced digital adoption during the pandemic, with bank branches and stores closing and more banking done and more goods and services being purchased online.

Amount delivers retail banking experiences via a variety of channels and a point-of-sale financing product suite, as well as features such as fraud prevention, verification, decisioning engines and account management.

Overall, Amount clients include financial institutions collectively managing nearly $2 trillion in U.S. assets and servicing more than 50 million U.S. customers, according to the company.

Hughes declined to provide any details regarding the company’s financials, saying only that Amount “performed well” as a standalone company in 2020 and that the company is expecting “significant” year-over-year revenue growth in 2021.

Amount plans to use its new capital to further accelerate R&D by investing in its technology and products. It also will be eyeing some acquisitions.

“We see a lot of interesting technology we could layer onto our platform to unlock new asset classes, and acquisition opportunities that would allow us to bring additional features to our platform,” Hughes told TechCrunch.

Avant itself made its first acquisition earlier this year when it picked up Zero Financial, news that TechCrunch covered here.

Kevin Marcus, partner at WestCap, said his firm invested in Amount based on the belief that banks and other financial institutions have “a point-in-time opportunity to democratize access to traditional financial products by accelerating modernization efforts.”

“Amount is the market leader in powering that change,” he said. “Through its best-in-class products, Amount enables financial institutions to enhance and elevate the banking experience for their end customers and maintain a key competitive advantage in the marketplace.”

Powered by WPeMatico

It looks like everyone and their mother is trying to reinvent the Brazilian banking system. Earlier this year we wrote about Nubank’s $400 million Series G, last month there was the PicPay IPO filing and today, alt.bank, a Brazilian neobank, announced a $5.5 million Series A led by Union Square Ventures (USV).

It’s no secret that the Brazilian banking system has been poised for disruption, considering the sector’s little attention to customer service and exorbitant fee structure that’s left most Brazilians unbanked, and alt.bank is just the latest company trying to take home a piece of the pie.

Following Nubank’s strategy of launching a bank with colors that are very un-bank-like, signaling that they do things differently, alt.bank similarly launched its first financial product in 2019 — a fluorescent-yellow debit card which the locals have endearingly dubbed, “o amarelinho,” meaning, “the little yellow card.”

The company, founded by serial entrepreneur Brad Liebmann, follows the founder’s $480 million exit of Simply Business, which was acquired by U.S. insurance giant Travelers in 2017.

Unlike many fintechs, alt.bank has a strong social mission and pays commissions for referrals that last for the customer’s lifetime.

“Most fintechs just help wealthy people get wealthier, so I thought let’s do something with a social mission,” Liebmann told TechCrunch in an interview.

To drive home the mission, and really target the unbanked, Liebman and his team of 80 employees have designed an app that can be used by the illiterate. Instead of words, users can follow color-coded prompts to complete a transaction. The company also plans to launch credit products soon.

According to the company, close to a million people have downloaded the android app since launch, but Liebman declined to disclose how many active users the company actually has.

Today, the company’s core offerings include the debit card, a prepaid credit card, Pix (similar to Zelle), a savings account and even telemedicine visits via a partnership with Dr. Consulta, a network of healthcare clinics throughout the country. The prepaid credit card is key because online stores in Brazil don’t accept debit card purchases.

In addition to the perk of ongoing commissions, alt.bank has also partnered with three major drugstores, allowing their users to get 5-30% off any item at the stores, including medication.

While the company is based in São Paulo and São Carlos, Liebmann and his family are currently based in London due to regulations around the pandemic.

The investment in alt.bank marks USV’s first investment in South America, solidifying a trend by other major U.S. investors such as Sequoia who only in the last several years have started looking to LatAm for deals.

“The bar was high for our first investment in South America,” said Union Square Ventures partner John Buttrick. “The combination of the alt.bank business model and world-class management team enticed us to expand our geographic focus to help build the leading digital bank targeting the 100 million Brazilians who are currently being neglected by traditional lenders,” he added in a statement.

Powered by WPeMatico

Nearly exactly one month ago, digital real estate platform Loft announced it had closed on $425 million in Series D funding led by New York-based D1 Capital Partners. The round included participation from a mix of new and existing investors such as DST, Tiger Global, Andreessen Horowitz, Fifth Wall and QED, among many others.

At the time, Loft was valued at $2.2 billion, a huge jump from its being just near unicorn territory in January 2020. The round marked one of the largest ever for a Brazilian startup.

Now, today, São Paulo-based Loft has announced an extension to that round with the closing of $100 million in additional funding that values the company at $2.9 billion. This means that the 3-year-old startup has increased its valuation by $700 million in a matter of weeks.

Baillie Gifford led the Series D-2 round, which also included participation from Tarsadia, Flight Deck, Caffeinated and others. Individuals also put money in the extension, including the founders of Better (Zach Frenkel), GoPuff, Instacart, Kavak and Sweetgreen.

Loft has seen great success in its efforts to serve as a “one-stop shop” for Brazilians to help them manage the home buying and selling process.

Image Credits: Loft

In 2020, Loft saw the number of listings on its site increase “10 to 15 times,” according to co-founder and co-CEO Mate Pencz. Today, the company actively maintains more than 13,000 property listings in approximately 130 regions across São Paulo and Rio de Janeiro, partnering with more than 30,000 brokers. Not only are more people open to transacting digitally, more people are looking to buy versus rent in the country.

“We did more than 6x YoY growth with many thousands of transactions over the course of 2020,” Pencz told TechCrunch at the time of the company’s last raise. “We’re now growing into the many tens of thousands, and soon hundreds of thousands, of active listings.”

The decision to raise more capital so soon was due to a variety of factors. For one, Loft has received “overwhelming investor interest” even after “a very, very oversubscribed main round,” Pencz said.

“We have seen a continued acceleration in our market share growth, especially in São Paulo and Rio de Janeiro, the two markets we currently operate in,” he added. “We saw an opportunity to grow even faster with additional capital.”

Pencz also pointed out that Baillie Gifford has relatively large minimum check size requirements, which led to the extension being conducted at a higher price and increased the total round size “by quite a bit to be able to accommodate them.”

While the company was less forthcoming about its financials as of late, it told me last year that it had notched “over $150 million in annualized revenues in its first full year of operation” via more than 1,000 transactions.

The company’s revenues and GMV (gross merchandise value) “increased significantly” in 2020, according to Pencz, who declined to provide more specifics. He did say those figures are “multiples higher from where they were,” and that Loft has “a very clear horizon to profitability.”

Pencz and Florian Hagenbuch founded Loft in early 2018 and today serve as its co-CEOs. The aim of the platform, in the company’s words, is “bringing Latin American real estate into the e-commerce age by developing online alternatives to analogue legacy processes and leveraging data to create transparency in highly opaque markets.” The U.S. real estate tech company with the closest model to Loft’s is probably Zillow, according to Pencz.

In the United States, prospective buyers and sellers have the benefit of MLSs, which in the words of the National Association of Realtors, are private databases that are created, maintained and paid for by real estate professionals to help their clients buy and sell property. Loft itself spent years and many dollars in creating its own such databases for the Brazilian market. Besides helping people buy and sell homes, it offers services around insurance, renovations and rentals.

In 2020, Loft also entered the mortgage business by acquiring one of the largest mortgage brokerage businesses in Brazil. The startup now ranks among the top-three mortgage originators in the country, according to Pencz. When it comes to helping people apply for mortgages, he likened Loft to U.S.-based Better.com.

This latest financing brings Loft’s total funding raised to an impressive $800 million. Other backers include Brazil’s Canary and a group of high-profile angel investors such as Max Levchin of Affirm and PayPal, Palantir co-founder Joe Lonsdale, Instagram co-founder Mike Krieger and David Vélez, CEO and founder of Brazilian fintech Nubank. In addition, Loft has also raised more than $100 million in debt financing through a series of publicly listed real estate funds.

Loft plans to use its new capital in part to expand across Brazil and eventually in Latin America and beyond. The company is also planning to explore more M&A opportunities.

This article was updated post-publication to reflect accurate investor information.

Powered by WPeMatico

When the world shifted toward virtual one year ago, one service in particular saw heated demand: remote online notarization.

The ability to get a document notarized without leaving one’s home suddenly became more of a necessity than a luxury. Pat Kinsel, founder and CEO of Boston-based Notarize, worked to get appropriate legislation passed across the country to make it possible for more people in more states to get documents notarized digitally.

That hard work has paid off. Today, Notarize has announced $130 million in Series D funding led by fintech-focused VC firm Canapi Ventures after experiencing 600% year over year revenue growth. The round values Notarize at $760 million, which is triple its valuation at the time of its $35 million Series C in March of 2020. This latest round is larger than the sum of all of the company’s previous rounds to date, and brings Notarize’s total raised to $213 million since its 2015 inception.

A slew of other investors participated in the round, including Alphabet’s independent growth fund CapitalG, Citi Ventures, Wells Fargo, True Bridge Capital Partners and existing backers Camber Creek, Ludlow Ventures, NAR’s Second Century Ventures and Fifth Wall Ventures.

Notarize insists that it “isn’t just a notary company.” Rather, Canapi Ventures partner Neil Underwood described it as the “last mile” of businesses (such as iBuyers, for example).

The company has also evolved to “also bring trust and identity verification” into those businesses’ processes.

Over the past year, Notarize has seen a massive increase in transactions and inked new partnerships with companies such as Adobe, Dropbox, Stripe and Zillow Group, among others. It’s seen big spikes in demand from the real estate, financial services, retail and automotive sectors.

“In 2020, the world rushed to digitize. Online commerce ballooned, and businesses in almost every industry needed to transition to digital basically overnight so they could continue uninterrupted,” Kinsel said. “Notarize was there to help them safely close these deals with trust and convenience.”

The company plans to use its new capital to expand its platform and product and scale “to serve enterprises of all sizes.” It also plans to double down on hiring in the next year.

“Notarize is disrupting outdated business models and technologies, and there’s massive potential, particularly in the financial services space, as more companies will need to offer secure digital alternatives to in-person transactions,” Canapi’s Underwood said.

Notarize’s success comes after a difficult 2019, when the company saw “critical financing” fall through and had to lay off staff, according to Kinsel. Talk about a turnaround story.

Powered by WPeMatico

Pie Insurance, a startup offering workers’ compensation insurance to small businesses, announced this morning that it has closed on $118 million in a Series C round of funding.

Allianz X — investment arm of German financial services giant Allianz — and Acrew Capital co-led the round, which brings the Washington, D.C.-based startup’s total equity funding raised to over $300 million since its 2017 inception. Pie declined to disclose the valuation at which its latest round was raised, other than to say it was “a significant increase.”

Return backers Greycroft, SVB Capital, SiriusPoint, Elefund and Moxley Holdings also participated in the Series C financing.

The startup, which uses data and analytics in its effort to offer SMBs a way to get insurance digitally and more affordably, has seen its revenues climb by 150% since it raised $127 million in a Series B extension last May. Its headcount too has risen — to 260 from 140 last year.

Pie began selling its insurance policies in March 2018. The company declined to give recent hard revenue numbers, saying it only has grown its gross written premium to over $100 million and partnered with over 1,000 agencies nationwide. Last year, execs told me that in the first quarter of 2020, the company had written nearly $19 million in premiums, up 150% from just under $7.5 million during the same period in 2019.

Like many other companies over the past year, Pie Insurance — with its internet-driven, cloud-based platform — has benefited from the increasing further adoption of digital technologies.

“We are riding that wave,” said Pie Insurance co-founder and CEO John Swigart. “We believe small businesses deserve better than they have historically gotten. And we think that technology can be the means by which that better experience, that more efficient process, and fundamentally, that lower price can be delivered to them.”

Pie’s customer base includes a range of small businesses including trades, contractors, landscapers, janitors, auto shops and restaurants. Pie sells its insurance directly through its website and also mostly through thousands of independent insurance agents.

Workers’ compensation insurance is the only commercial insurance mandated for nearly every company in the United States, points out Lauren Kolodny, founding partner at Acrew Capital.

“Historically, it’s been extremely cumbersome to qualify, onboard and manage workers’ comp insurance — particularly for America’s small businesses which haven’t been prioritized by larger carriers,” she wrote via email.

Pie, Koldony said, is able to offer underwriting decisions “almost instantly,” digitally and more affordably than legacy insurance carriers.

“I have seen very few insurtech teams that come close,” she added.

Dr. Nazim Cetin, CEO of Allianz X, told TechCrunch via email that his firm believes Pie is operating in an “attractive and growing market that is ripe for digital disruption.”

The company, he said, leverages “excellent,” proprietary data and advanced analytics to be able to provide tailored underwriting and automation.

“We see some great collaboration opportunities with Allianz companies too,” he added.

Looking ahead, the company plans to use its new capital to invest further in technology and automation, as well as to grow its core workers’ comp insurance business and “lay the groundwork for new business offerings in 2021 and beyond.”

Powered by WPeMatico