financial services

Auto Added by WPeMatico

Auto Added by WPeMatico

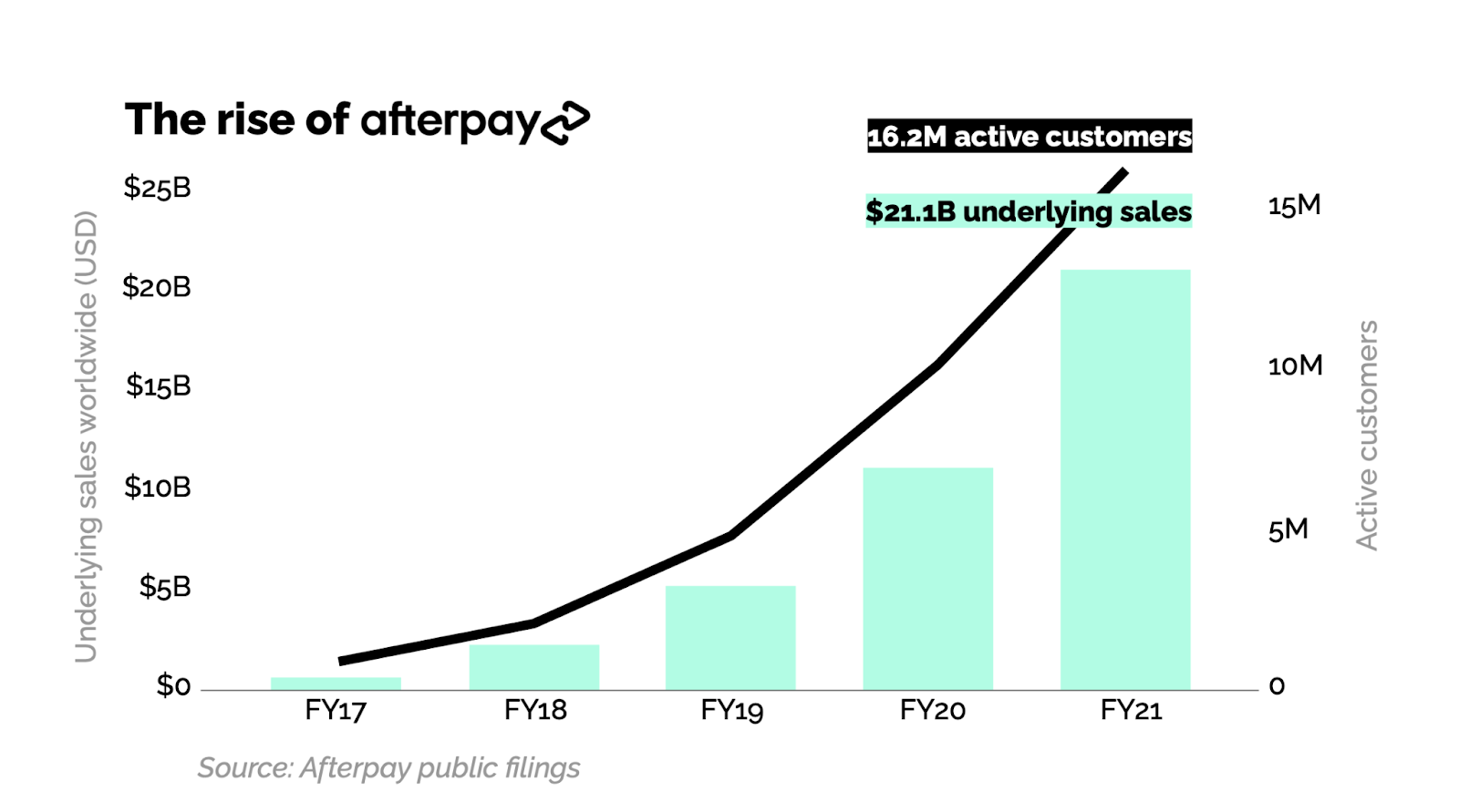

Sunday was a big day in fintech: Afterpay has agreed to merge with Square. This agreement sets two of the most admired financial technology companies in recent history on a path to becoming one.

Afterpay and Square have the potential to build one of the world’s most important payments networks. Square has built a very significant merchant payment network, and, via Cash App, a thriving high-growth consumer payment service. However, these two lines of business have historically not been integrated. Together, Square and Afterpay will be able to weave all of these services together into a single integrated experience.

Afterpay and Cash App each have double-digit millions of consumers, and Square’s seller ecosystem and Afterpay’s merchant network both record double-digit billions of payment volume per year. From the offline register and the online checkout flow to sending money in just a few taps, Square and Afterpay will tell a complete story of next-generation economic empowerment.

As Afterpay’s only institutional venture investor, I wanted to share some perspective on how we got here and what this merger means for the future of consumer finance and the payments industry.

Afterpay and Square have the potential to build one of the world’s most important payments networks.

Every five to 10 years, the global payments industry undergoes a critical innovation cycle that determines the winners and losers for the next several decades. The last major transition was the shift to NFC-based mobile payments, which I wrote about in 2015. The major mobile OS vendors (Apple and Google) cemented their position in the global payments stack by deftly bridging the needs of the networks (Visa, Mastercard, etc.) and consumers by way of the mobile devices in their pockets.

Afterpay sparked the latest critical innovation cycle. Conceived in a living room in Sydney by a millennial, Nick Molnar, for millennials, Afterpay had a key insight: Millennials don’t like credit.

Millennials came of age during the global mortgage crisis of 2008. As young adults, they watched their friends and family lose their homes by overextending on mortgage debt, bolstering their already lower trust for banks. They also have record levels of student debt. Therefore, it’s no surprise that millennials (and Gen Z right behind them) strongly prefer debit cards over credit cards.

But it’s one thing to recognize the paradigm shift and quite another to do something about it. Nick Molnar and Anthony Eisen did something, ultimately building one of the fastest-growing payments startups in history on their core product: Buy now, pay later … and never any interest.

Afterpay’s product is simple. If you have $100 in your cart and choose to pay with Afterpay, it will charge your bank card (typically a debit card) $25 every two weeks in four installments. No interest, no revolving debt and no fees with on-time payments. For the millennial consumer, this meant they could get the primary benefit of a credit card (the ability to pay later) with their debit card, without the need to worry about all the bad things that come with credit cards — high interest rates and revolving debt.

All upside, no downside. Who could resist? For the early merchants, virtually all of whom relied on millennials as their key growth segment, they got a fair trade: Pay a small fee above payment processing to Afterpay, get significantly higher average order values and conversions to purchase. It was a win-win proposition and, with lots of execution, a new payment network was born.

Image Credits: Matrix Partners

Afterpay went somewhat unnoticed outside Australia in 2016 and 2017, but once it came to the U.S. in 2018 and built a business there that broke $100 million net revenues in only its second year, it got attention.

Klarna, which had struggled with product-market fit in the U.S., pivoted their business to emulate Afterpay. And Affirm, which had always been about traditional credit — generating a significant portion of their revenue from consumer interest — also noticed and introduced their own BNPL offering. Then came PayPal with “Pay in 4,” and just a few weeks ago, there has been news that Apple is expected to enter the space.

Afterpay created a global phenomenon that has now become a category embraced by mainstream players across the industry — a category that is on track to take a meaningful share of global retail payments over the next 10 years.

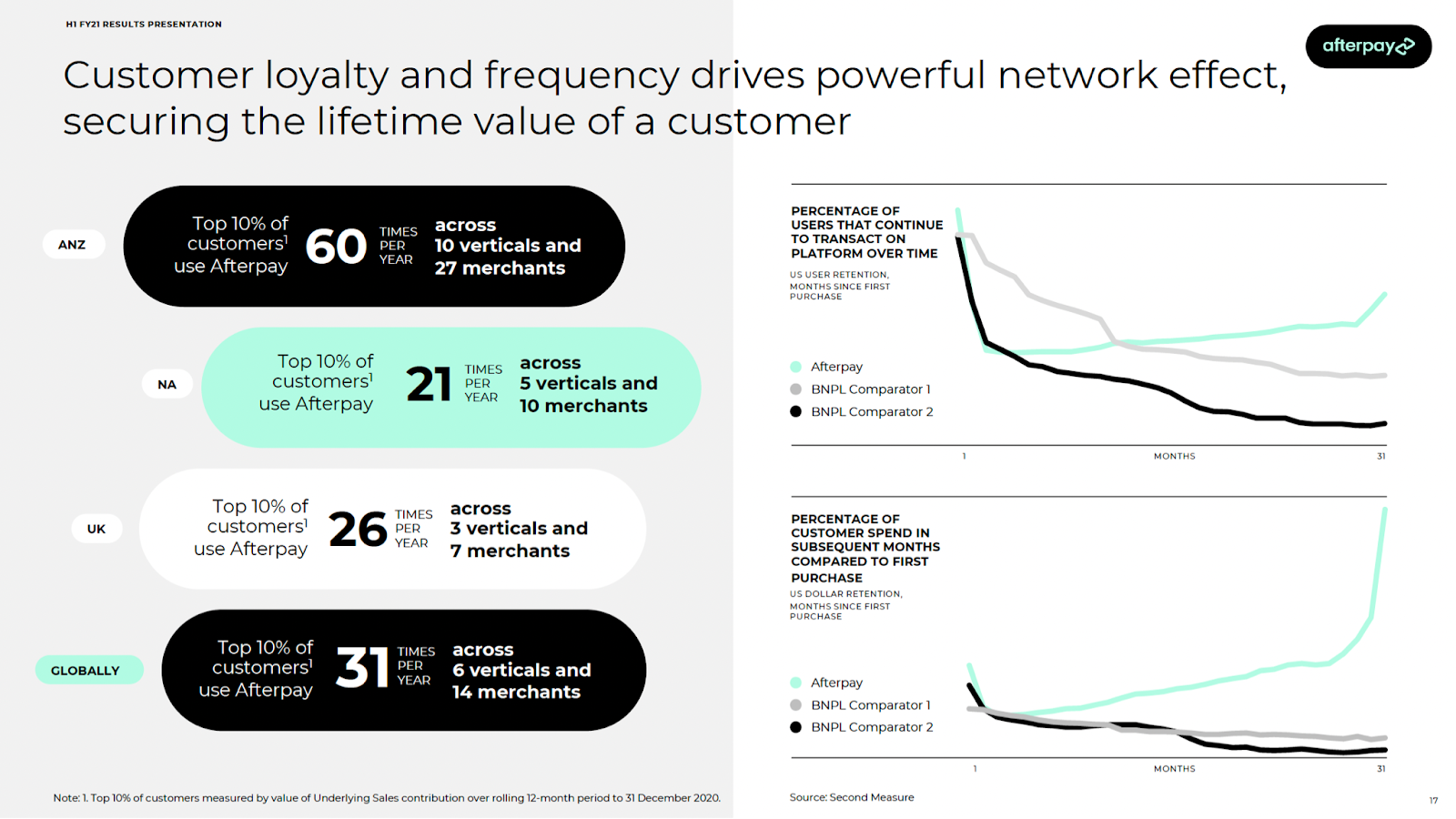

Afterpay stands apart. It has always been the BNPL leader by virtually every measure, and it has done it by staying true to their customers’ needs. The company is great at understanding the millennial and Gen Z consumer. It’s evident in the voice, tone and lifestyle brand you experience as an Afterpay user, and in the merchant network it continues to build strategically. It’s also evident in the simple fact that it doesn’t try to cross-sell users revolving debt products.

Most importantly, it’s evident in the usage metrics relative to competition. This is a product that people love, use and have come to rely on, all with better, fairer terms than were ever available to them than with traditional consumer credit.

Image Credits: Afterpay H1 FY21 results presentation

I’ve been building payment companies for over 15 years now, initially in the early days of PayPal and more recently as a venture investor at Matrix Partners. I’ve never seen a combination that has such potential to deliver extraordinary value to consumers and merchants. Even more so than eBay + PayPal.

Beyond the clear product and network complementarity, what’s most exciting to me and my partners is the alignment of values and culture. Square and Afterpay share a vision of a future with more opportunity and fewer economic hurdles for all. As they build toward that future together, I’m confident that this combination is a winner. Square and Afterpay together will become the world’s next generation payment provider.

Powered by WPeMatico

It’s no secret that the technology for easy business-to-business payments has not yet caught up to its peer-to-peer counterparts, but Yaydoo thinks it has the answer.

The Mexico City-based B2B software and payments company provides three products, VendorPlace, P-Card and PorCobrar, for managing cash flow, optimizing access to smart liquidity, and connecting small, midsize and large businesses to an ecosystem of digital tools.

Sergio Almaguer, Guillermo Treviño and Roberto Flores founded Yaydoo — the name combines “yay” and “do” to show the happiness of doing something — in 2017. Today, the company announced the close of a $20.4 million Series A round co-led by Base10 Partners and monashees.

Joining them in the round were SoftBank’s Latin America Fund and Leap Global Partners. In total, Yaydoo has raised $21.5 million, Almaguer told TechCrunch.

Prior to starting the company, Almaguer was working at another company in Mexico doing point-of-sale. His large enterprise customers wanted automation for their payments, but he noticed that the same tools were too expensive for small businesses.

The co-founders started Yaydoo to provide procurement, accounts payable and accounts receivables, but in a simpler format so that the collection and payment of B2B transactions was affordable for small businesses.

Image Credits: Yaydoo

The idea is taking off, and vendors are adding their own customers so that they are all part of the network to better link invoices to purchase orders and then connect to accounts payable, Almaguer said. Yaydoo estimates that the automation workflows reduced 80% of time wasted paying vendors, on average.

Yaydoo is joining a sector of fintech that is heating up — the global B2B payments market is valued at $120 trillion annually. Last week, B2B payments platform Nium announced a $200 million in Series D funding on a $1 billion valuation. Others attracting funding recently include Paystand, which raised $50 million in Series C funding to make B2B payments cashless, while Dwolla raised $21 million for its API that allows companies to build and facilitate fast payments.

The new funding will enable the company to attract new hires in Mexico and when the company expands into other Latin American countries. Yaydoo is also looking at future opportunities for its working capital business, like understanding how many invoices customers are setting, the access to actual payments, and how money flows out and in so that it can provide insights on working capital funding gaps. The company will also invest in product development.

The company has grown to over 800 customers, up from 200 in the first quarter of 2020. Its headcount also grew to 100 from 30 during the same time. In the last 12 months, over 70,000 companies have transacted on the Yaydoo network, and total payment volume grew to hundreds of millions of dollars.

Yaydoo is a SaaS subscription model, but the new funding will also enable the company to create a pool of potential customers with a “freemium” offering with the goal of converting those customers into the subscription model as they grow, Almaguer said.

Rexhi Dollaku, partner at Base10 Partners, said the firm saw the way B2B payments were becoming modernized and “was impressed” by the Yaydoo team and how it built a complicated infrastructure, but made it easy to use.

He believes Latin America is 10 years behind in terms of B2B payments but will catch up sooner than later because of the digital transformation going on in the region.

“We are starting to see early signs of the network being built out of the payments product, and that is a good indication,” Dollaku said. “With the funding, Yaydoo will be also able to provide more financial services options for businesses to address a working fund gap.”

Powered by WPeMatico

Chilean startup Xepelin, which has created a financial services platform for SMEs in Latin America, has secured $30 million in equity and $200 million in credit facilities.

LatAm venture fund Kaszek Ventures led the equity portion of the financing, which also included participation from partners of DST Global and a slew of other firms and founders/angel investors. LatAm- and U.S.-based asset managers and hedge funds — including Chilean pension funds — provided the credit facilities. In total over its lifetime, Xepelin has raised over $36 million in equity and $250 million in asset-backed facilities.

Also participating in the round were Picus Capital; Kayak Ventures; Cathay Innovation; MSA Capital; Amarena; FJ Labs; Gilgamesh Ventures. A group of angels also participated in the financing, including Kavak founder and CEO Carlos Garcia; Jackie Reses, executive chairman of Square Financial Services; Justo founder and CEO Ricardo Weder; Tiger Global Management Partner John Curtius; GGV’s Hans Tung; and Gerry Giacoman, founder and CEO of Clara, among others.

Nicolás de Camino and Sebastian Kreis founded Xepelin in mid-2019 with the mission of changing the fact that “only 5% of companies in all LatAm countries have access to recurring financial services.”

“We want all SMEs in LatAm to have access to financial services and capital in a fair and efficient way,” the pair said.

Xepelin is built on a SaaS model designed to give SMEs a way to organize their financial information in real time. Embedded in its software is a way for companies to apply for short-term working capital loans “with just three clicks, and receive the capital in a matter of hours,” the company claimed.

It has developed an AI-driven underwriting engine, which the execs said gives it the ability to make real-time loan approval decisions.

“Any company in LatAm can onboard in just a few minutes and immediately access a free software that helps them organize their information in real time, including cash flow, revenue, sales, tax, bureau info — sort of a free CFO SaaS,” de Camino said. “The circle is virtuous: SMEs use Xepelin to improve their financial habits, obtain more efficient financing, pay their obligations, and collaborate effectively with clients and suppliers, generating relevant impacts in their industries.”

The fintech currently has over 4,000 clients in Chile and Mexico, which currently has a growth rate “four times faster” than when Xepelin started in Chile. Over the past 22 months, it has loaned more than $400 million to SMBs in the two countries. It currently has a portfolio of active loans for $120 million and an asset-backed facility for more than $250 million.

Overall, the company has been seeing a growth rate of 30% per month, the founders said. It has 110 employees, up from 20 a year ago.

“When we talk about creating the largest digital bank for SMEs in LatAm, we are not saying that our goal is to create a bank; perhaps we will never ask for the license to have one, and to be honest, everything we do, we do it differently from the banks, something like a non-bank, a concept used today to exemplify focus,” the founders said.

Both de Camino and Kreis said they share a passion for making financial services more accessible to SMEs all across Latin America and have backgrounds rooted deep in different areas of finance.

“Our goal is to scale a platform that can solve the true pains of all SMEs in LatAm, all in one place that also connects them with their entire ecosystem, and above all, democratized in such a way that everyone can access it,” Kreis said, “regardless of whether you are a company that sells billions of dollars or just a thousand dollars, getting the same service and conditions.”

For now, the company is nearly exclusively focused on the B2B space, but in the future, it believes several of its services “will be very useful for all SMEs and companies in LatAm.”

“Xepelin has developed technology and data science engines to deliver financing to SMBs in Latin America in a seamless way,” Nicolas Szekasy, co-founder and managing partner at Kaszek Ventures, said in a statement. “The team has deep experience in the sector and has proven a perfect fit of their user-friendly product with the needs of the market.”

Chile was home to another large funding earlier this week. NotCo, a food technology company making plant-based milk and meat replacements, closed on a $235 million Series D round that gives it a $1.5 billion valuation.

Powered by WPeMatico

PayPal’s plan to morph itself into a “super app” has been given a go for launch.

According to PayPal CEO Dan Schulman, speaking to investors during this week’s second-quarter earnings call, the initial version of PayPal’s new consumer digital wallet app is now “code complete” and the company is preparing to slowly ramp up. Over the next several months, PayPal expects to be fully ramped up in the U.S., with new payment services, financial services, commerce and shopping tools arriving every quarter.

The company has spoken for some time about its “super app” ambitions — a shift in product direction that would make PayPal a U.S.-based version of something like China’s WeChat or Alipay or India’s Paytm. Like those apps, PayPal aims to offer a host of consumer services under one roof, beyond just mobile payments.

In previous quarters, PayPal said these new features may include things like enhanced direct deposit, check cashing, budgeting tools, bill pay, crypto support, subscription management, and buy now, pay later functionality. It also said it would integrate commerce, thanks to the mobile shopping tools acquired by way of its $4 billion Honey acquisition in 2019.

So far, PayPal has continued to run Honey as a standalone application, website and browser extension, but the super app could incorporate more of its deal-finding functions, price-tracking features and other benefits.

On Wednesday’s earnings call, Schulman revealed the super app would have a few other features as well, including high-yield savings, early access to direct deposit funds and messaging functionality outside of peer-to-peer payments — meaning you could chat with family and friends directly through the app’s user interface.

PayPal hadn’t announced its plans to include a messaging component until now, but the feature makes sense in terms of how people often combine chat and peer-to-peer payments today. For example, someone may want to make a personal request for the funds instead of just sending an automated request through an app. Or, after receiving payment, a user may want to respond with a “thank you,” or other acknowledgment. Currently, these conversations take place outside of the payment app itself on platforms like iMessage. Now, that could change.

“We think that’s going to drive a lot of engagement on the platform,” said Schulman. “You don’t have to leave the platform to message back and forth.”

With the increased user engagement, the company expects to see a bump in average revenue per active account.

Schulman also hinted at “additional crypto capabilities,” which were not detailed. However, PayPal earlier this month increased the crypto purchase limit from $20,000 to $100,000 for eligible PayPal customers in the U.S., with no annual purchase limit. The company also this year made it possible for consumers to check out at millions of online businesses using their cryptocurrencies, by first converting the crypto to cash then settling with the merchant in U.S. dollars.

Though the app’s code is now complete, Schulman said the plan is to continue to iterate on the product experience, noting that the initial version will not be “the be-all and end-all.” Instead, the app will see steady releases and new functionality on a quarterly basis.

However, he did say that early on, the new features would include the high-yield savings, improved bill pay with a better user experience, and more billers and aggregators, as well as early access to direct deposit, budgeting tools and the new two-way messaging feature.

To integrate all the new features into the super app, PayPal will undergo a major overhaul of its user interface.

“Obviously, the [user experience] is being redesigned,” Schulman noted. “We’ve got rewards and shopping. We’ve got a whole giving hub around crowdsourcing, giving to charities. And then, obviously, buy now, pay later will be fully integrated into it. … The last time I counted, it was like 25 new capabilities that we’re going to put into the super app.”

The digital wallet app will also be personalized to the end user, so no two apps are the same. This will be done using both artificial intelligence and machine learning capabilities to “enhance each customer’s experiences and opportunities,” said Schulman.

PayPal delivered an earnings beat in the second quarter with $6.24 billion in revenue, versus the $6.27 billion Wall Street expected, and earnings per share of $1.15, versus the $1.12 expected. Total payment volume from merchant customers also jumped 40% to $311 billion, while analysts had projected $295.2 billion. But the company’s stock slipped due to a lowered outlook for Q3, impacted by eBay’s transition to its own managed payments service.

In addition, PayPal gained 11.4 million net new active accounts in the quarter, to reach 403 million total active accounts.

Powered by WPeMatico

Small and medium enterprises have become a big opportunity in the world of B2B technology in the last several years, and today a startup that’s building tools aimed at helping them manage their teams of workers is announcing some funding that underscores the state of that market.

Homebase, which provides a platform that helps SMBs manage various services related to their hourly workforces, has closed $71 million in funding, a Series C that values the company between $500 million and $600 million, according to sources close to the startup.

The round has a number of big names in it that are as much a sign of how large VCs are valuing the SMB market right now as it is of the strategic interest of the individuals who are participating. GGV Capital is leading the round, with past backers Bain Capital Ventures, Baseline Ventures, Bedrock, Cowboy Ventures and Khosla Ventures also participating. Individuals include Focus Brands President Kat Cole; Jocelyn Mangan, a board member at Papa John’s and Chownow and former COO of Snag; former CFO of payroll and benefits company Gusto, Mike Dinsdale; Guild Education founder Rachel Carlson; star athletes Jrue and Lauren Holiday; and alright alright alright actor and famous everyman and future political candidate Matthew McConaughey.

Homebase has raised $108 million to date.

The funding is coming on the heels of strong growth for Homebase (which is not to be confused with the U.K./Irish home improvement chain of the same name, nor the YC-backed Vietnamese proptech startup).

The company now has some 100,000 small businesses, with 1 million employees in total, on its platform. Businesses use Homebase to manage all manner of activities related to workers that are paid hourly, including (most recently) payroll, as well as shift scheduling, timeclocks and timesheets, hiring and onboarding, communication and HR compliance.

John Waldmann, Homebase’s founder and CEO, said the funding will go toward both continuing to bring on more customers as well as expanding the list of services offered to them, which could include more features geared to frontline and service workers, as well as features for small businesses who might also have some “desk” workers who might still work hourly.

The common thread, Waldmann said, is not the exact nature of those jobs, but the fact that all of them, partly because of that hourly aspect, have been largely underserved by tech up to now.

“From the beginning, our mission was to help local businesses and their teams,” he said. Part of his inspiration came from people he knew: a childhood friend who owned an independent, expanding restaurant chain, and was going through the challenges of managing his teams there, carrying out most of his work on paper; and his sister, who worked in hospitality, which didn’t look all that different from his restaurant friend’s challenges. She had to call in to see when she was working, writing her hours in a notebook to make sure she got paid accurately.

“There are a lot of tech companies focused on making work easier for folks that sit at computers or desks, but are building tools for these others,” Waldmann said. “In the world of work, the experience just looks different with technology.”

Homebase currently is focused on the North American market — there are some 5 million small businesses in the U.S. alone, and so there is a lot of opportunity there. The huge pressure that many have experienced in the last 16 months of COVID-19 living, leading some to shut down altogether, has also focused them on how to manage and carry out work much more efficiently and in a more organized way, ensuring you know where your staff is and that your staff knows what it should be doing at all times.

What will be interesting is to see what kinds of services Homebase adds to its platform over time: In a way, it’s a sign of how hourly wage workers are becoming a more sophisticated and salient aspect of the workforce, with their own unique demands. Payroll, which is now live in 27 states, also comes with pay advances, opening the door to other kinds of financial services for Homebase, for example.

“Small businesses are the lifeblood of the American economy, with more than 60% of Americans employed by one of our 30 million small businesses. In a post-pandemic world, technology has never been more important to businesses of all sizes, including SMBs,” Jeff Richards, managing partner at GGV Capital and new Homebase board member, said in a statement. “The team at Homebase has worked tirelessly for years to bring technology to SMBs in a way that helps drive increased profitability, better hiring and growth. We’re thrilled to see Homebase playing such an important role in America’s small business recovery and thrilled to be part of the mission going forward.”

It’s interesting to see McConaughey involved in this round, given that he’s most recently made a turn toward politics, with plans to run for governor of Texas in 2022.

“Hardworking people who work in and run restaurants and local businesses are important to all of us,” he said in a statement. “They play an important role in giving our cities a sense of livelihood, identity and community. This is why I’ve invested in Homebase. Homebase brings small business operations into the modern age and helps folks across the country not only continue to work harder, but work smarter.”

Powered by WPeMatico

Monarch, a subscription-based platform that aims to help consumers “plan and manage” their financial lives, has raised $4.8 million in seed funding.

Accel led the round, which also included participation from SignalFire, and brings the Mountain View-based yet fully distributed startup’s total funding since its 2019 inception to $5.5 million.

Co-founder and CEO Val Agostino was the first product manager on the original team that built Mint.com. There, he said, he saw firsthand that Americans with a greater understanding of financial matters “needed software solutions that went beyond just tracking and budgeting.”

“They needed help planning their financial future and understanding the tradeoffs between competing financial priorities,” he said.

Monarch aims to help people address those needs with software it says “makes it easy” for people to outline their financial goals and then create a detailed, forward-looking plan toward achieving them.

“We then help customers track their progress against their plan and automatically course correct as their financial situation changes, which it always does,” Agostino said.

Monarch came out of private beta in early 2021 with apps for web, iOS and Android, and is priced at $9.99 per month or $89.99 per year. The startup intentionally opted to not be ad-supported or sell customers’ financial data.

These approaches are “misaligned with users’ financial interests,” Agostino said.

“We felt that a subscription business model would best support that ethos and align our users’ interests with our own,” he added. Since launching publicly, Monarch has been growing its paid subscriber base by about 9% per week.

Image Credits: Monarch

Monarch launched during the pandemic, the uncertainty of which carried over into people’s financial lives, believes Agostino.

“As a result, we saw a lot of people make use of Monarch’s forecasting features to compare different ‘what if ‘scenarios such as switching jobs or moving to a different city or state,” he said.

Earlier this month, TechCrunch reported on a company with a similar mission, BodesWell, teaming up with American Express on a financial planning tool for its cardholders. Agostino said that Monarch is similar to BodesWell in that both startups help customers map a financial plan and future.

“The difference is that Monarch also has a full suite of PFM tools, such as budgeting, reporting and investment analysis,” he said. “The benefit to the consumer is that because Monarch is connected to your entire financial picture, we can help you actually stay on track with your financial plan and/or update the plan in real time if needed.”

Accel’s Daniel Levine said that until he came across Monarch, he was “somehow still a Mint customer despite its obsolescence.”

Over the past decade, the landscape for financial products has expanded dramatically, with more people having brokerage and crypto accounts, for example, Levine said.

In his view, Monarch stands out for a couple of reasons. For one, it’s a subscription product.

“One thing I always hated about Mint was when it would suggest the objectively wrong credit card for me,” Levine said. “It has all of my transaction data, it should tell me the card with the best rewards for me. Monarch is set up to never compromise what’s best for the user in favor of advertising.”

Secondly, Monarch’s aim is to serve as the infrastructure for its customers. To do that, it needs to monitor all of someone’s finances.

“They need to track checking, credit cards, brokerage, real estate and crypto,” he said. “Monarch is committed to doing that. It’s an incredibly painful problem and even though Monarch is a new entrant in the space, I think they’ve clearly separated themselves on that dimension.”

Powered by WPeMatico

The payments space — amazingly — remains up for grabs for startups. Yes, dear reader, despite the success of Stripe, there seems to be a new payments startup virtually every other day. It’s a mess out there! The accelerated growth of e-commerce due to the pandemic means payments are now a booming space. And here comes another one, with a twist.

WhenThen has built a no-code payment operations platform that, they claim, streamlines the payment processes “of merchants of any kind”. It says its platform can autonomously orchestrate, monitor, improve and manage all customer payments and payments ops.

The startup’s opportunity has arisen because service providers across different verticals increasingly want to get into open banking and provide their own payment solutions and financial services.

Founded six months ago, WhenThen has now raised $6 million, backed by European VCs Stride and Cavalry.

The founders, Kirk Donohoe, Eamon Doyle and Dave Brown, are three former Mastercard Payment veterans.

Based out of Dublin, CEO Donohoe told me: “We see traditional businesses embracing e-comm, and e-comm merchants now operating multiple business models such as trade supply, marketplace, subscription, and more. There is no platform that makes it easy for such businesses to create and operate multiple payment flows to support multiple business models in one place — that’s where we step in.”

He added: “WhenThen is helping e-commerce digital platforms build advanced payment flows and payment automation, in minutes as opposed to months. When you start to integrate different payment methods, different payment gateways, how you want the payment to move from collection through to payout gets very, very complex. I’ve been doing this for over a decade now, as an entrepreneur building different businesses that had to accept, collect and pay payments.”

He said his founding team “had to build very complex payment flows for large merchants, airlines, hotels, issuers, and we just found it was ridiculous that you have to continue to do the same thing over and over again. So we decided to come up with WhenThen as a better way to be able to help you build those flows in minutes.”

Claude Ritter, managing partner at Cavalry, said: “Basic payment orchestration platforms have been around for some time, focusing mostly on maximizing payment acceptance by optimizing routing. WhenThen provides the first end-to-end payment flow platform to equip businesses with the opportunity to control every stage of the payment flow from payment intent to payout.”

WhenThen supports a wide range of popular payment providers such as Stripe, Braintree, Adyen, Authorize.net, Checkout.com, etc., and a variety of alternative and locally preferred payment methods such as Klarna Affirm, PayPal and BitPay.

“For brave merchants considering global reach and operating multiple business models concurrently, I believe choosing the right payment ops platform will become as important as choosing the right e-commerce platform. Building your entire e-comm experience tightly coupled to a single payment processor is a hard correction to make down the line — you need a payment flow platform like WhenThen”, added Fred Destin, founder of Stride.VC.

Powered by WPeMatico

Not every startup wants to raise venture capital. And then there are those that do want to raise VC money but don’t want to use it for specific things.

In recent years, a number of firms have emerged looking to meet the credit needs of such venture-backed and growth startups: i80 Group is one of those firms.

Former Goldman Sachs investment banker Marc Helwani founded i80 in 2016 after investing in early-stage New York-based fintechs in 2014-2015 via his VC fund, Avenue A Ventures.

“It became very clear to me that fintech was going to explode,” he recalls. “At that time, it was still relatively new. And every time I spoke to a company, they would tell me, ‘We know how to raise VC, but what about the credit?’ I just saw this white space.”

For example, proptechs that buy homes on behalf of buyers don’t want to use venture money. Fintechs that want to make loans to consumers don’t want to use equity to do it. Instead, in those cases, credit might be more desirable.

Enter i80. The firm offers credit exclusively, and over the years has quietly committed more than $1 billion to over 15 companies –including real estate marketplace Properly, finance app MoneyLion and SaaS financing company Capchase — that have all raised a significant amount of venture capital but are looking for credit “to help them scale very efficiently and in a non-dilutive manner so they can retain more ownership of their companies,” Helwani said.

Its $1 billion milestone follows fund commitments nearing $500 million from an unnamed “leading global asset manager” as well as other institutional and retail investors.

Image Credits: Founder and Chief Investment Officer Marc Helwani / i80 Group

I80 — which derives its name from the highway that connects New York and San Francisco — is mainly focused on the fintech and proptech sectors.

“They are the two centers for the venture ecosystem,” Helwani said. “And we’re trying to be a bridge between those two cities.” I80 has offices in both locations and will soon be opening one in Montreal.

The firm works in conjunction with VC firms such as a16z (more formally known as Andreessen Horowitz); Affirm and PayPal co-founder Max Levchin’s SciFi; Khosla Ventures; Union Square Ventures; and QED.

“In a perfect world, venture capital would be called venture equity,” Helwani said. “VCs’ capital is critical for companies to hire and get office space. But when it comes time to do what the actual business is, such as provide loans or buy homes, capital like ours is very accretive without VCs and management losing ownership in the business. In these cases, using both credit and equity makes a lot of sense.”

Helwani is reluctant to call what i80 offers venture “debt.” He says that has a very specific connotation and is what Silicon Valley Bank and others like it do in providing debt as a percentage of a previous equity round. Instead, according to Helwani, i80’s approach is to minimize fees. The vast majority of its deals are “interest-rate related.”

“With mortgages, for example, we never think about the fees upfront, and focus more on the interest rate,” Helwan said. “We believe the more transparent we are, the more companies will want to work with us.”

I80 conducts quarterly calls with VCs and for now, that’s how it typically sources most of its deal flow. It also gets referrals. Helwani believes that i80 stands out from other firms also offering credit in that it’s “not trying to be credit investors in VC clothing.”

He also thinks that the fact that the i80 team is made of operators, as well as investors, is a contributing factor.

The firm is set to close another half a dozen deals in the next 60 to 90 days, and then plans to set its sights on raising more capital.

“We want to fill this void, and help companies raise money in their subsequent rounds at higher valuations,” Helwani said.

Powered by WPeMatico

The fintech sector has been hugely successful (and hugely profitable) for much of the last decade, and even more so during the pandemic. But it might come as a surprise to learn that many in the industry believe that the story is just beginning and the sector is poised to achieve much more, with fintech’s next decade expected to be radically different from the last 10 years.

Long before the pandemic, the way in which banks were regulated was changing. Initiatives like Open Banking and the Revised Payment Services Directive (PSD2) were being proposed as a way to promote competition in the banking industry — allowing smaller challenger firms to break into a market that has long been dominated by corporate titans.

Now that these initiatives are in place, however, we’re seeing that their effect goes way beyond opening up a gap for challenger banks. Since open banking requires that banks make valuable data available via APIs, it is leading to a revolution in the way that small and mid-size enterprises (SMEs) are funded — one in which data, and not hard capital, is the most important factor driving fintech success.

In order to understand the changes that are sweeping fintech and reconfiguring the way that the industry works with small businesses, it’s important to understand open banking. This is a concept that has really taken hold among governmental and supranational banking regulators over the past decade, and we are now beginning to see its impact across the banking sector.

Allowing third parties access to the data held at banks will allow the true financial position of SMEs to be assessed, many for the first time.

At its most fundamental level, open banking refers to the process of using APIs to open up consumers’ financial data to third parties. This allows these third parties to design, build and distribute their own financial products. The utility (and, ultimately, the profitability) of these products doesn’t rely on them holding huge amounts of capital — rather, it is the data they harvest and contain that endows them with value.

Open-banking models raise a number of challenges. One is that the banking industry will need to develop much more rigorous systems to continually seek consumer consent for data to be shared in this way. Though the early years of fintech have taught us that consumers are pretty relaxed when it comes to giving up their data — with some studies indicating that almost 60% of Americans choose fintech over privacy — the type and volume shared through open-banking frameworks is much more extensive than the products we have seen up until now.

Despite these concerns, the push toward open banking is progressing around the world. In Europe, the PSD2 (the Payment Services Directive) requires large banks to share financial information with third parties, and in Asia services like Alipay and WeChat in China, and Tez and PayTM in India are already altering the financial services market. The extra capabilities available through these services are already leading to calls for the U.S. banking system to embrace open banking to the same degree.

If the U.S. banking industry can be convinced of the utility of open banking, or if it is forced to do so via legislation, several groups are likely to benefit:

By far the biggest beneficiary of open banking, however, will be SMEs. This is not necessarily because open-banking frameworks offer specific new functionality that will be useful to small and medium-sized businesses. Instead, it is a reflection of the fact that SMEs have historically been so poorly served by traditional banks.

SMEs are underserved in a number of ways. Traditional banks have an extremely limited ability to view the aggregate financial position of an SME that holds capital across multiple institutions and in multiple instruments, which makes securing finance very difficult.

In addition, SMEs often have to deal with dated and time-consuming manual interfaces to upload data to their bank. And (perhaps worst of all) the B2B payment systems in use at most banks provide very limited feedback to the businesses that use them — a lack of information that can cost businesses dearly.

Given these deficiencies, it’s not surprising that fintech startups are keen to lend to small businesses, and that SMEs are actively looking for novel banking products and services. There have, of course, already been some success stories in this space, and the kinds of banking systems available to SMEs today (especially in Europe) are leagues ahead of the services available even 10 years ago.

However, open banking promises to accelerate this transformation and dramatically improve the financial services available to the average SME. It will do this in several ways. Allowing third parties access to the data held at banks will allow the true financial position of SMEs to be assessed, many for the first time.

Via APIs, fintech companies will be able to access information on different types of accounts, insurance, card accounts and leases, and consolidate data from multiple countries into one overall picture.

This, in turn, will have major effects on the way that credit-worthiness is assessed for SMEs. At the moment, there is a funding gap facing many SMEs, largely because banks have been hesitant to move away from the “balance sheet” model of assessing credit risk. By using real-time analytics on an SME’s current business activities, banks will be able to more accurately assess this risk and lend to more businesses.

In fact, this is already happening in countries where open banking is well advanced – in the U.K., Lloyds’ Business ToolBox offers unlimited credit checks on companies and directors in addition to account transaction data.

Open banking will also allow peer comparison analytics far ahead of what we have seen until now. APIs can be used to provide SMEs real-time feedback on how they are performing within their market sector. Again, this ability is already available in the U.K., with Barclays’ SmartBusiness Dashboard offering marketing effectiveness tools as part of a customizable business dashboard.

These capabilities will be so useful to SMEs that they are likely to drive the popularity of any fintech product that offers them. For SMEs, this value will lie mainly in intelligent data-analytics-based insights, recommendations and automatic prompts that can be built on top of account aggregation.

Then, additional insights generated from these same monitoring tools could enable banks and alternative lenders to be more proactive with their lending — offering preapproved lines of credit, in a timely manner, to SMEs that would have previously found it difficult to access funding.

Crucially for the fintech sector, it’s almost a certainty that SMEs will be willing to pay fees for data-analytics-based value-added services that help them grow. This is why some startups in this space are already attracting huge levels of funding, and why open banking is at the heart of the relationship between tech and the economy.

So if fintech has had a good year, this is likely to be just the start of the story. Backed by open-banking initiatives, the sector is now at the forefront of a banking revolution that will finally give SMEs the level of service they deserve and unleash their true potential across the economy at large.

Powered by WPeMatico

Mortgages may not be considered sexy, but they are a big business.

If you’ve refinanced or purchased a home digitally lately, you may not have noticed the company powering the software behind it — but there’s a good chance that company is Blend.

Founded in 2012, the startup has steadily grown to be a leader in the mortgage tech industry. Blend’s white label technology powers mortgage applications on the site of banks including Wells Fargo and U.S. Bank, for example, with the goal of making the process faster, simpler and more transparent.

The San Francisco-based startup’s SaaS (software-as-a-service) platform currently processes over $5 billion in mortgages and consumer loans per day, up from nearly $3 billion last July.

Today, Blend made its debut as a publicly traded company on the New York Stock Exchange, trading under the symbol “BLND.” As of early afternoon, Eastern Time, the stock was trading up over 13% at $20.36.

On Thursday night, the company had said it would offer 20 million shares at a price of $18 per share, indicating the company was targeting a valuation of $3.6 billion.

That compares to a $3.3 billion valuation at the time of its last raise in January — a $300 million Series G funding round that included participation from Coatue and Tiger Global Management. Also, let’s not forget that Blend only became a unicorn last August when it raised a $75 million Series F. Over its lifetime, Blend had raised $665 million before Friday’s public market debut.

In filing its S-1 on June 21, Blend revealed that its revenue had climbed to $96 million in 2020 from $50.7 million in 2019. Meanwhile, its net loss narrowed from $81.5 million in 2019 to $74.6 million in 2020.

In 2020, the San Francisco-based startup significantly expanded its digital consumer lending platform. With that expansion, Blend began offering its lender customers new configuration capabilities so that they could launch any consumer banking product “in days rather than months.”

Looking ahead, the company had said it expects its revenue growth rate “to decline in future periods.” It also doesn’t envision achieving profitability anytime soon as it continues to focus on growth. Blend also revealed that in 2020, its top five customers accounted for 34% of its revenue.

Today, TechCrunch spoke with co-founder and CEO Nima Ghamsari about the company’s decision to go with a traditional IPO versus the ubiquitous SPAC or even a direct listing.

For one, Blend said he wanted to show its customers that it is an “around for a long time company” by making sure there’s enough on its balance sheet to continue to grow.

“We had to talk and convince some of the biggest investors in the world to invest in us, and that speaks to how long we’ll be around to serve these customers,” he said. “So it was a combination of our capital need and wanting to cement ourselves as a really credible software provider to one of the most regulated industries.”

Ghamsari emphasized that Blend is a software company that powers the mortgage process and is not the one offering the mortgages. As such, it works with the flock of fintechs that are working to provide mortgages.

“A lot of them are using Blend under the hood, as the infrastructure layer,” he said.

Overall, Ghamsari believes this is just the beginning for Blend.

“One of the things about financial services is that it’s still mostly powered by paper. So a lot of Blend’s growth is just going deeper into this process that we got started in years ago,” he said. As mentioned above, the company started out with its mortgage product but just keeps adding to it. Today, it also powers other loans such as auto, personal and home equity.

“A lot of our growth is actually powered by our other lines of business,” Ghamsari told TechCrunch. “There’s a lot to build because the larger digitization trends are just getting started in financial services. It’s a relatively large industry that has lots of change.”

In May, digital mortgage lender Better.com announced it would combine with a SPAC, taking itself public in the second half of 2021.

Powered by WPeMatico