financial services

Auto Added by WPeMatico

Auto Added by WPeMatico

With its latest $34 billion acquisition of Red Hat, IBM may have found something more elementary than “Watson” to save its flagging business.

Though the acquisition of Red Hat is by no means a guaranteed victory for the Armonk, N.Y.-based computing company that has had more downs than ups over the five years, it seems to be a better bet for “Big Blue” than an artificial intelligence program that was always more hype than reality.

Indeed, commentators are already noting that this may be a case where IBM finally hangs up the Watson hat and returns to the enterprise software and services business that has always been its core competency (albeit one that has been weighted far more heavily on consulting services — to the detriment of the company’s business).

Also read as IBM taps out on Watson as its growth engine and returns to basics ie financial engineering and distribution https://t.co/nD7gHyYhQf

— Sunil Rawat (@_sunilrawat) October 28, 2018

Watson, the business division focused on artificial intelligence whose public claims were always more marketing than actually market-driven, has not performed as well as IBM had hoped and investors were losing their patience.

Critics — including analysts at the investment bank Jefferies (as early as one year ago) — were skeptical of Watson’s ability to deliver IBM from its business woes.

As we wrote at the time:

Jefferies pulls from an audit of a partnership between IBM Watson and MD Anderson as a case study for IBM’s broader problems scaling Watson. MD Anderson cut its ties with IBM after wasting $60 million on a Watson project that was ultimately deemed, “not ready for human investigational or clinical use.”

The MD Anderson nightmare doesn’t stand on its own. I regularly hear from startup founders in the AI space that their own financial services and biotech clients have had similar experiences working with IBM.

The narrative isn’t the product of any single malfunction, but rather the result of overhyped marketing, deficiencies in operating with deep learning and GPUs and intensive data preparation demands.

That’s not the only trouble IBM has had with Watson’s healthcare results. Earlier this year, the online medical journal Stat reported that Watson was giving clinicians recommendations for cancer treatments that were “unsafe and incorrect” — based on the training data it had received from the company’s own engineers and doctors at Sloan-Kettering who were working with the technology.

All of these woes were reflected in the company’s latest earnings call where it reported falling revenues primarily from the Cognitive Solutions business, which includes Watson’s artificial intelligence and supercomputing services. Though IBM chief financial officer pointed to “mid-to-high” single digit growth from Watson’s health business in the quarter, transaction processing software business fell by 8% and the company’s suite of hosted software services is basically an afterthought for business gravitating to Microsoft, Alphabet, and Amazon for cloud services.

To be sure, Watson is only one of the segments that IBM had been hoping to tap for its future growth; and while it was a huge investment area for the company, the company always had its eyes partly fixed on the cloud computing environment as it looked for areas of growth.

It’s this area of cloud computing where IBM hopes that Red Hat can help it gain ground.

“The acquisition of Red Hat is a game-changer. It changes everything about the cloud market,” said Ginni Rometty, IBM Chairman, President and Chief Executive Officer, in a statement announcing the acquisition. “IBM will become the world’s number-one hybrid cloud provider, offering companies the only open cloud solution that will unlock the full value of the cloud for their businesses.”

The acquisition also puts an incredible amount of marketing power behind Red Hat’s various open source services business — giving all of those IBM project managers and consultants new projects to pitch and maybe juicing open source software adoption a bit more aggressively in the enterprise.

As Red Hat chief executive Jim Whitehurst told TheStreet in September, “The big secular driver of Linux is that big data workloads run on Linux. AI workloads run on Linux. DevOps and those platforms, almost exclusively Linux,” he said. “So much of the net new workloads that are being built have an affinity for Linux.”

Powered by WPeMatico

In emerging market countries where economic volatility is a way of life, there aren’t a lot of relatively safe options for members of the burgeoning middle class to park their money.

For instance, countries like Nigeria have experienced a tremendous growth in the number of citizens entering the middle class, which now accounts for about 23 percent of the population (it’s around 50 percent in the U.S.), according to a recent article citing the African Development Bank.

While Nigeria now faces some significant headwinds from a weak domestic currency (the naira), high interest rates and a manufacturing recession, there are ways that local investment can both protect the wealth that’s been created and encourage investment domestically to potentially spur development.

At least, that’s the conclusion that college friends Razaq Ahmed and Edward Popoola came to while they were thinking about opportunities for new financial services options in their home country of Nigeria.

The two men, Ahmed with a background in finance and Popoola in computer science, are launching a company called CowryWise that gives Nigerian investors a way to save their money by investing in high-yield government bonds. The rates on those products are high enough to absorb the wild swings in value of the naira and still provide a healthy return for investors, according to Ahmed.

Set to present at this year’s demo day from Y Combinator, CowryWise is one of a number of startups that Y Combinator has backed coming from the African continent, and an example of the wellspring of entrepreneurial talent that is flourishing in sub-Saharan Africa.

Using CowryWise, a customer would just have to sign up with their email address and phone number and link their bank account up to the CowryWise platform.

There are already roughly 57 million savings accounts in Nigeria and 32 million unique bank users. By investing in the bonds, these savers gain access to interest rates that range between 10 percent and 17 percent, according to Ahmed.

“The bonds… are similar to the treasuries issued by the U.S. government, which is A-rated,” says Ahmed. Even if there were foreign currency risk from investing in the naira, the inflation rate is currently around 11 percent, according to Ahmed. Given that most of the bonds are yielding interest rates on the higher end, it’s just a better deal for consumers, he said.

“There’s more value in keeping the money in government treasury bills” than in the bank, says Ahmed.

For Ahmed and Popoola, the decision to launch CowryWise was a way to bring investment opportunities to a retail investor that hadn’t been able to access the best that the financial system in Nigeria had to offer.

To target these retail investors meant leveraging technology to scale quickly and cheaply across the country. The two men started developing their service in January and tested it in February and March with friends and family.

CowryWise isn’t without competitors. Another Nigerian company, Piggybank, recently raised $1.1 million for its own automated savings solution. Like CowryWise, Piggybank also taps into government bonds to offer better rates to its investors.

That company already has 53,000 registered users — who have saved in excess of $5 million since 2016, according to a release.

There are subtle differences between the two. Piggybank touts its ability to save through bonds, but it is primarily working with banks to get Nigerians saving money. CowryWise is using Meristem Financial (Ahmed’s old employer) as the asset manager for its investments into the bond market.

Another difference is the time customers’ funds are locked up. Piggybank has a three-month savings period required before investors can withdraw funds, while CowryWise will let its customers withdraw cash immediately, according to this teardown of the two services.

Ultimately, there’s a large enough market for multiple players, and a need for better financial services, according to Ahmed.

“We kept having interest from retail investors on why they want to do micro-savings and micro-investment, but they didn’t have the required capital,” Ahmed says. “That was the major reason for staring the company. Why not democratize the assets? And make them available in investments and savings in this traditional instrument?”

Powered by WPeMatico

S&P Global announced today that it will acquire Kensho, a Cambridge, Massachusetts startup that has concentrated on artificial intelligence and analytics for big financial institutions. The total value of the deal is $550 million in a mix of cash and stock. Kensho, which counted S&P Global as a client/partner and an investor, launched in 2013 and has raised $67.5 million, according… Read More

S&P Global announced today that it will acquire Kensho, a Cambridge, Massachusetts startup that has concentrated on artificial intelligence and analytics for big financial institutions. The total value of the deal is $550 million in a mix of cash and stock. Kensho, which counted S&P Global as a client/partner and an investor, launched in 2013 and has raised $67.5 million, according… Read More

Powered by WPeMatico

Ahead of a big fundraising to fuel its mobile ambitions, “free” mobile service startup FreedomPop is taking an unexpected strategic side-road to expand into a completely different area: financial services. The company is licensing its customer conversion platform to Prudential, which plans to use it to up-sell existing customers to more of its products. FreedomPop itself is not… Read More

Ahead of a big fundraising to fuel its mobile ambitions, “free” mobile service startup FreedomPop is taking an unexpected strategic side-road to expand into a completely different area: financial services. The company is licensing its customer conversion platform to Prudential, which plans to use it to up-sell existing customers to more of its products. FreedomPop itself is not… Read More

Powered by WPeMatico

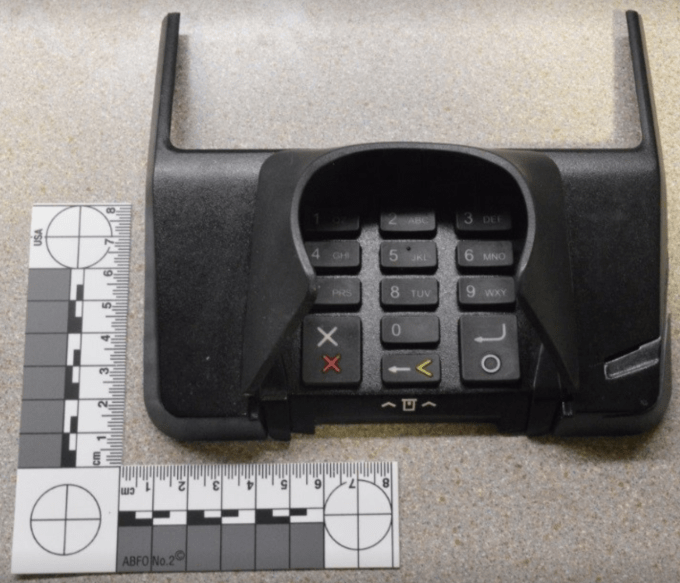

Police in Lower Pottsgrove, Pennsylvania have spotted a group of thieves who are placing completely camouflaged skimmers on top of credit card terminals in Aldi stores. The skimmers, which the gang placed in plain sight of surveillance video cameras, look exactly like the original credit card terminals but would store debit card numbers and PINs of unsuspecting shoppers. “While Aldi… Read More

Police in Lower Pottsgrove, Pennsylvania have spotted a group of thieves who are placing completely camouflaged skimmers on top of credit card terminals in Aldi stores. The skimmers, which the gang placed in plain sight of surveillance video cameras, look exactly like the original credit card terminals but would store debit card numbers and PINs of unsuspecting shoppers. “While Aldi… Read More

Powered by WPeMatico

While cryptocurrencies stole the spotlight in 2017, a clutch of companies were quietly working behind the scenes to slowly bring the financial services establishment to its knees. It may turn out that these startup entrants of the last several years will prove to be the more relevant disruptors. Read More

While cryptocurrencies stole the spotlight in 2017, a clutch of companies were quietly working behind the scenes to slowly bring the financial services establishment to its knees. It may turn out that these startup entrants of the last several years will prove to be the more relevant disruptors. Read More

Powered by WPeMatico

Symphony, a secure messaging app that counts 15 of the world’s biggest banks among its investors and 200,000 paying customers, has raised a new tranche of funding to fuel its expansion into new markets. Symphony has closed in on $63 million; and according to sources close to the company, the startup is now valued at over $1 billion — confirming our reporting from December. Read More

Symphony, a secure messaging app that counts 15 of the world’s biggest banks among its investors and 200,000 paying customers, has raised a new tranche of funding to fuel its expansion into new markets. Symphony has closed in on $63 million; and according to sources close to the company, the startup is now valued at over $1 billion — confirming our reporting from December. Read More

Powered by WPeMatico

Data governance and management startup Collibra — originally founded in Belgium but now based out of New York to help businesses in sectors like finance and healthcare to manage and comply with data retention policies — has raised $50 million in its latest round of funding. The company is not disclosing the valuation, but we heard that it is in the region of $650 million (which is… Read More

Data governance and management startup Collibra — originally founded in Belgium but now based out of New York to help businesses in sectors like finance and healthcare to manage and comply with data retention policies — has raised $50 million in its latest round of funding. The company is not disclosing the valuation, but we heard that it is in the region of $650 million (which is… Read More

Powered by WPeMatico

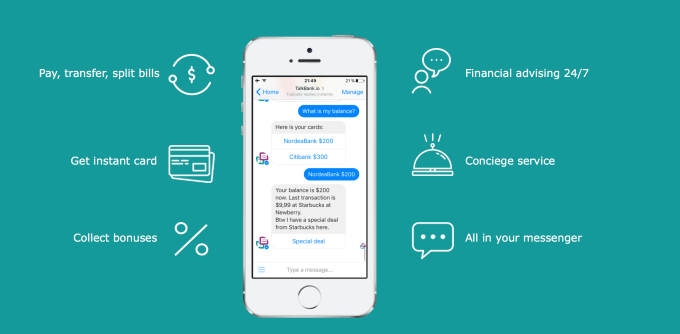

As a fan of banks – I like the lollipops they give out – I’m slightly disturbed by services like TalkBank. This Russian company replaces one-on-one teller interaction with a chatbot that can tell you your balance, offer on the spot advice, and even send you cool deals related to your credit cards. Founded by Mikhail Popov, Alexander Popov, and Vladimir Kozhevnikov the company… Read More

As a fan of banks – I like the lollipops they give out – I’m slightly disturbed by services like TalkBank. This Russian company replaces one-on-one teller interaction with a chatbot that can tell you your balance, offer on the spot advice, and even send you cool deals related to your credit cards. Founded by Mikhail Popov, Alexander Popov, and Vladimir Kozhevnikov the company… Read More

Powered by WPeMatico

Digital-only UK “challenger” bank, Starling Bank, has added support for Apple Pay — meaning its customers can now add their Starling debit card to their Apple Wallet and make contactless payments drawing from funds in their Starling account via their Apple devices.

Digital-only UK “challenger” bank, Starling Bank, has added support for Apple Pay — meaning its customers can now add their Starling debit card to their Apple Wallet and make contactless payments drawing from funds in their Starling account via their Apple devices.